Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Amy Xie Patrick: What the Fed’s shift from inflation to employment means for investors

A shift in focus from inflation to employment hints at a likely rate cut in September. Pendal’s head of income strategies AMY XIE PATRICK explains

- Learn more about Pendal’s income and fixed interest capability

- Find out about Amy Xie Patrick’s Pendal Monthly Income Plus fund

SINCE December 2018, we’ve known Fed chair Jay Powell is not afraid to pivot.

Back then the Fed hiking cycle was forced to an abrupt halt when the US economy came under the strain of the first round of Trump’s trade tariffs.

By the following October, the Fed had cut rates by 75 percentage points to 1.75%.

Powell’s latest comments at last weekend’s Fed’s annual gathering in Jackson Hole, Wyoming, may prove to be another example.

In his speech, Powell acknowledged downside risks to employment, suggested further easing from the current “restrictive” policy stance may be appropriate and – for the first time in months – did not make this conditional on the inflation outlook.

Since these remarks, the US bond market has priced in an 85% chance of a cut at the next Federal Open Market Committee meeting in September.

This would take the upper bound of the Fed Funds target rate to 4.25%.

Sceptics view the move as Jay Powell bending to political pressure from President Trump.

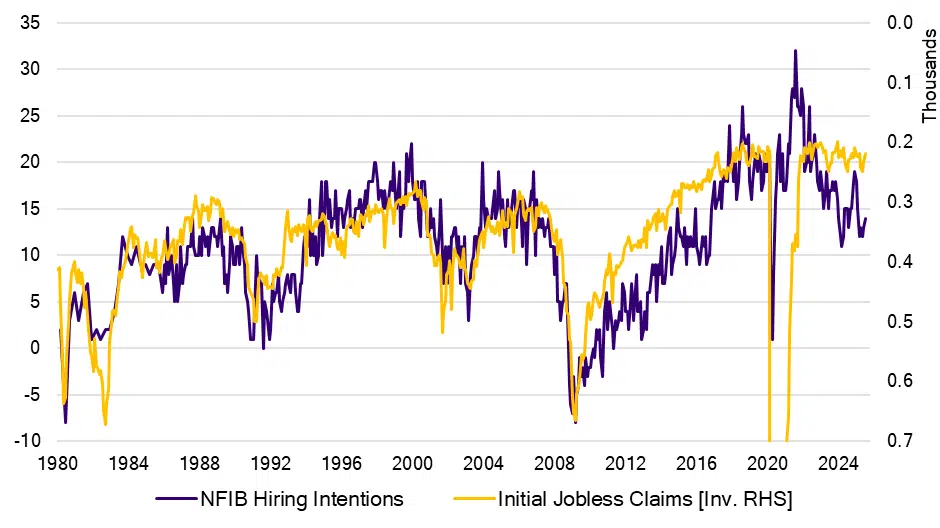

The chart below suggests the Fed ought to be getting a little more worried.

US hiring and firing: NFIB Hiring Intentions and Initial Jobless Claims

Source: Bloomberg

The purple line shows the hiring intentions of US businesses, according to a monthly survey by the National Federation of Independent Business.

The yellow line is an inverted series of US initial jobless claims – a weekly series to reflect new joblessness.

The long-standing relationship between the purple and yellow lines is clear to see, and intuitive to grasp.

When businesses stop hiring, they eventually have to start firing. And vice versa.

When businesses feel the bottom is in, they stop firing, and then they start hiring.

This relationship seems to have dislocated of late. We need more time to see whether this is an actual dislocation, or one of those blips in the long-run data.

A possible explanation?

Perhaps businesses sense the slowdown and have paused hiring, but burned by the post-Covid labour shortages, are not yet willing to let people go.

A likely rate cut

September will likely bring a rate cut from the Fed.

Pendal’s analysis of the long-term decision-making bias of the Fed leans heavily on market pricing.

In other words, the Fed doesn’t like to surprise or disappoint (unlike some other central banks we know). That analysis also shows how sensitive the Committee is to labour-market dynamics.

If the Fed has now pivoted its focus from inflation to employment, we too should be looking at the best leading indicators for where labour markets are headed.

If you’d like to hear more about what those lead indicators might be, Pendal’s Income & Fixed Interest team would welcome an opportunity to chat.

You can contact us through the client account team here.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at 26 August 2025.

PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Funds and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Funds is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Funds.

An investment in the Funds or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com