Close

Leave Feedback

Welcome to the new btim.com.auTake a two minute tour to see what we've changed

Hi there! Welcome to the new look Pendal website... Take a two minute tour to see what we’ve changed.

Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Amy Xie Patrick: No more sugar hits for China

August 14, 2024

This article is more than 12 months old. Find our latest insights here

What is the state of play in China? Head of income strategies AMY XIE PATRICK offers an overview of China’s recent Third Plenum and the implications on world economies.

- Property fall-out akin to China’s own Global Financial Crisis

- The cyclical picture for China “not going to get better” in near term

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

IN China, the Third Plenum ended with little fanfare.

The market didn’t expect much by way of stimulus policies since almost all hopes of that kind have been repeatedly dashed over the past two years.

As a forum focused on the medium term, it addressed structural over cyclical issues facing China’s economy. The overarching message was about prioritising sustainable long-term growth over short-term sugar hits.

The property market fall-out

We’ve written at length in the past about the nature of China’s economy and its intricate ties to the property sector. We won’t rehash those details here.

The economy’s dependency on real estate means that there are significant withdrawal symptoms to be addressed in the aftermath of the massive Chinese housing slump.

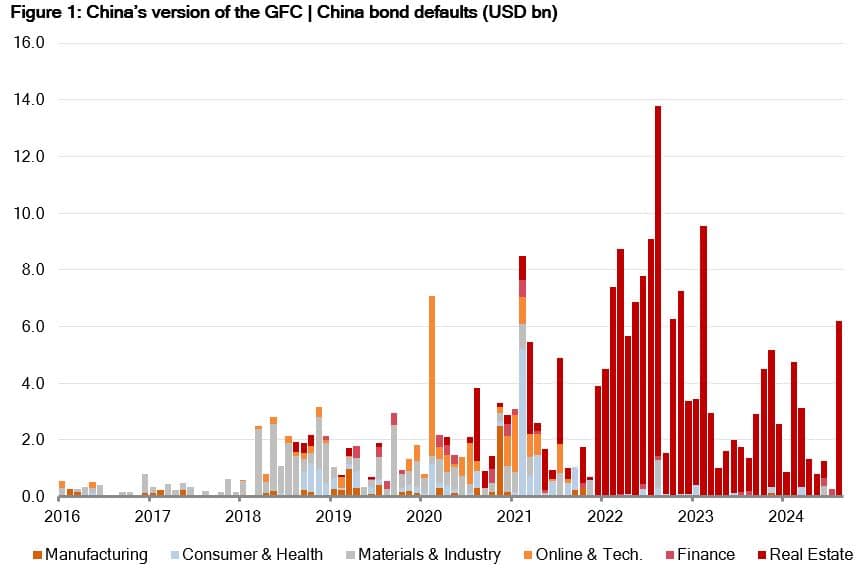

The fall-out is akin to China’s own version of the Global Financial Crisis (GFC).

Source: Bloomberg

It took the US economy close to a decade to heal over the wounds from the GFC. During that time, authorities focused on banking sector repair and regulation.

Fiscal policy remained conservative, leaving quantitative easing (QE) to provide indirect support through the financial markets. Private sector businesses and households focused on balance sheet repair. Low interest rates could do little to incentivise demand for borrowing during this repair phase.

China has many of the same constraints today.

Financial sector reforms are vital for ensuring that new excesses don’t build up in place of previous property-related bets.

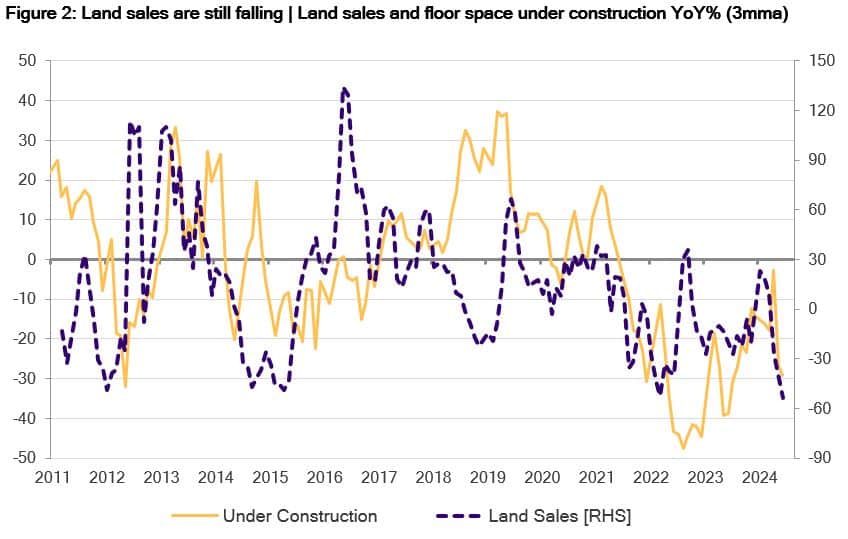

Fiscal policy is unable to provide much boost because local governments who dish out much of this stimulus are hamstrung by the devastating hit to their revenues as land sales collapsed with the housing slump.

Monetary policy can’t help because lower interest rates threaten the stability of the yuan and ultimately the stock of China’s foreign currency reserves.

With home prices now able to fall as well as rise, households won’t be persuaded to add more property to their portfolios just because mortgage rates fall at the margin. There are bigger capital holes to fill in their existing property portfolios.

Source: Bloomberg

Structural over cyclical

The cyclical picture for China is not going to get better in the near term.

Beijing has been unwavering in its resolve to de-lever and de-risk the property sector. These goals have been in play since after the GFC, but each time something got in the way.

Here’s a timeline:

- In 2013, deleveraging efforts ended with a devaluation experiment which resulted in China losing a quarter of its foreign currency reserves.

- In 2015, deleveraging efforts led to a slowdown in demand that swept across commodities and ignited a wave of defaults in the US energy sector.

- In 2017, deleveraging efforts had to be slowed as fighting Trump’s trade war became a priority.

- In 2020, deleveraging efforts had to swiftly U-turn to offset the pandemic.

- Since 2021, the deleveraging commitment has stuck.

While communication from the Third Plenum renewed the government’s commitment to the growth target, more noise was made about the longer-term transition goals for the economy. The hope is to fill property void with high-tech and innovation.

There was also talk of a smoother mechanism for fiscal transfers between central government and local governments. Fiscal reform is a lengthy process, and the overarching goal would be to ease the pain from anaemic land sales revenues rather than greatly increase local governments’ fiscal firepower.

Structurally, changes are afoot on the technology front in China.

Since 2017, the real estate sector’s contribution to final demand in the Chinese economy has fallen from close to 25% to now under 20%, while contributions from the high-technology sectors have growth from 11% to just under 15% (data from IEA).

Renewables power generation capacity now makes up more than 85% of total annual newly added power capacity whereas thermal power has dwindled to under 5%.

The picture 15 years ago was almost the mirror opposite.

In electric vehicles (EVs), thanks to government subsidies and consumer incentives, sales in China make up close to 40% of total vehicle sales. This compares to only 21% in Europe and 10% in the US.

Thank goodness for asynchronous cycles?

China’s unwavering resolve since 2021 to deleverage the property sector has been successful thanks, in large part, to the strength of the global recovery from the pandemic shock.

This acted as economic immunity for the rest of the world from China’s property crisis and prevented a feedback loop that would have otherwise thwarted Beijing’s efforts again.

Subsequently, China’s domestic deflation and weak demand has helped developed market inflation to normalise via the goods channel.

Source: Bloomberg

But now is where things start to get tricky.

There is little reason to hope for big-bang stimulus from China. The policy focus is about strengthening local institutions, balance sheet repair, and positioning new engines of long-term growth.

At the same time, growth is weak or softening in other parts of the world:

- Europe has been dancing on the precipice of recession for the best part of two years.

- Asia’s recovery from the pandemic was weaker than other areas in the world due to its strong links with China.

- Excess cash and savings from pandemic fiscal stimulus are running out for economies like the US and Australia.

China’s investment focus on technology and renewables will not provide the offset needed to steady the ship of the global economy in the near term.

From inflation to deflation?

Of course, it wasn’t long ago that central banks had the opposite inflation problem to what exists today.

No matter how low they kept interest rates and how hard they engaged in QE, inflation continued to undershoot its target in the pre-pandemic era. Part of the problem was the balance sheet recession caused by the GFC. The other issue was continued price deflation in goods and tradeables.

This deflation can be traced back to China producing more than it could consume and relying on global demand to absorb its excess manufacturing capacity.

With a new investment wave in high-tech sectors coming from China comes risks of more deflation from too much capacity in China. This is already apparent in EVs, where the competitive price pressures from Chinese EV producers have forced companies like Tesla to slash prices to defend market share.

The difference between today and a decade ago is the competitive realm. It has moved on from commoditised manufactured goods to high-tech.

“Good enough” is far harder to achieve in high-performance computer chips than plastic children’s toys. Nevertheless, with global trade partners all trying to “de-risk” from China, alternative hopes for long-term growth are few and far between.

These concerns about overinvestment may be just as valid in the west as it is for China. It has certainly been a feature of the latest US earnings season, with growing market scepticism on the pace and scale of company investments into artificial intelligence.

When overinvestment leads to overcapacity, technological success will have a hard time finding its way into company earnings success. Just look at the Chinese stock market.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at August 14, 2024.

PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Funds and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Funds is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Funds.

An investment in the Funds or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance.

Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com

Keep updated

Sign up to receive the latest news and views