Mainstream Online Web Portal

LoginInvestors can view their accounts online via a secure web portal. After registering, you can access your account balances, periodical statements, tax statements, transaction histories and distribution statements / details.

Advisers will also have access to view their clients’ accounts online via the secure web portal.

Tim Hext: Rate hikes off, rate cuts on in 2025

This article is more than 12 months old. Find our latest insights here

Today’s inflation numbers mean the rate-cut window is open in Australia from early next year. Pendal’s head of government bond strategies, TIM HEXT, explains why

- Two easings expected in February and May

- Why bonds, why now? Pendal’s income and fixed interest experts explain

- Browse Pendal’s fixed interest funds

TODAY’S 1% quarterly CPI number would not normally be cause for celebration. After all, that’s 4% annualised – above the RBA target.

But the RBA focuses more on trimmed-mean inflation to avoid high and low swing items like petrol and food.

On this measure, the Q2 CPI number was 0.8% – still not quite in the target band, but comfortably heading that way.

Calls for rate hikes are off, the RBA can again be patient and the inflation picture should improve into year end.

Markets liked it. At the time of writing three-year bonds had fallen from 3.95% to 3.73%.

RBA governor Michele Bullock can avoid the wrath of the government and Anthony Albanese can return to selling his pre-election cost-of-living relief without a rate hike spoiling it.

Key items in the CPI: 1% headline (1% forecast) for Q2

We already had two-thirds of the items from the monthly CPI in April and May, so the headline was no surprise.

There was remarkable consistency across key areas, as food, housing, transport and insurance all went up around 1%.

In the context of these recent moves, housing and insurance were lower than previous outcomes, though there were some seasonal elements for insurance.

Health was up 1.5% as medical and hospital services grew at 2%. This is more structural and recent battles between providers and health insurance show the strains in this sector.

Tobacco was up 3% on tax indexation, which alone added almost 0.1% to CPI. International travel was up 8%, though domestic travel partly offset that – down 5%.

Trimmed (underlying) inflation 0.8% (forecast 1%) – why the forecasting miss?

Given the headline number came in as expected, why did economists miss the trimmed number, which came in at 0.8%?

At the risk of losing readers’ interest, this gets into how “trimmed-mean inflation” works.

Basically, the RBA (or ABS these days) lines up every item from highest to lowest change – weighted for its contribution to the index – and cuts off the top and bottom 15%.

That is, 30% of weighted items are trimmed.

Petrol is nearly always trimmed (it’s 3% of the CPI weight), as are many food and non-alcoholic items (a combined 17% weight).

Volatility in travel prices means they are generally trimmed these days (6% of weight).

This still leaves around 5-10% of weighted items to be trimmed and the extent of their movements feeds back into the trimmed mean.

If I’ve lost you, find your resident mathematician – there’s generally one around in finance.

Rate hikes off, rate cuts on – but not till 2025 despite a potential flat headline CPI in Q3

The RBA releases its forecasts every quarter at its early February, May, August and November meetings.

Given the lack of any guidance from the RBA these days, these forecasts are important.

In May, the RBA expected trimmed mean inflation to be 0.8% in Q2, so it will be pleased with today’s result. The inflation scares from the monthly April and May numbers, which Bullock felt the need to acknowledge at the June RBA meeting, have passed.

When we get the new set of forecasts next week, we think headline CPI will be forecast at 3.2% for year end – down from 3.8% due to electricity subsidies announced in recent Federal and State budgets.

Trimmed mean inflation, however, will likely only be revised down from 3.4% to 3.2%.

That is, trimmed mean inflation will still likely be too high for a rate cut this year, though there should be some probability priced.

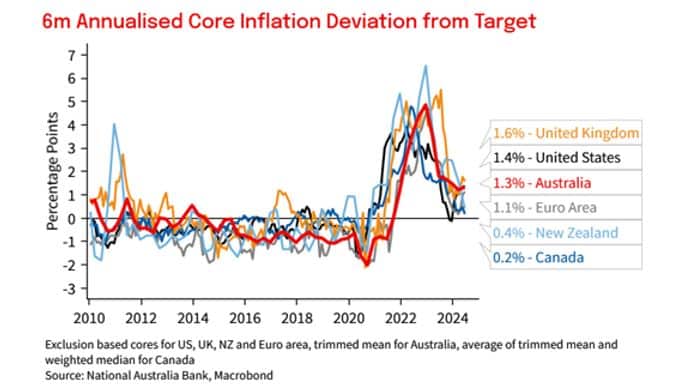

Global factors eventually win over

Here is an interesting chart (courtesy of NAB) on how much higher CPI is than target across key countries.

Inflation is measured on a six-month annualised basis (six months times two) to measure the current pulse more closely. All countries are still over target, but most are either cutting or about to cut.

Australia will be no different.

Looking ahead

Rate cuts globally, better behaved wages, sluggish growth, rising unemployment, and falling oil prices should see the rate cut window open in February 2025.

In Australia, we expect two easings in February and May next year, and six easings in the US by mid-next year.

That’s the RBA at 3.85% and the Fed at 4% by June.

From there, we think the risk is for further cuts, but our confidence is lower.

All this is positive for bonds and real yields. We think Australian ten-year bonds will trade down to 3.75% in the months ahead, before settling down in a 3.5% to 4% range early next year.

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current at July 31, 2024. PFSL is the responsible entity and issuer of units in the Pendal Monthly Income Plus Fund (ARSN: 137 707 996) and Pendal Dynamic Income Fund (ARSN: 622 750 734) (Funds). A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com