Inflation isn’t under control and the RBA still has work to do, argues Pendal’s OLIVER GE

You can also listen to this podcast on Apple or Spotify

An excerpt from this interview with Oliver Ge, an assistant portfolio manager with Pendal’s income and fixed interest team

Inflation isn’t under control and the RBA still has work to do, argues Oliver Ge, an assistant portfolio manager with Pendal’s income and fixed interest team

“I think at 4.1% we’re still at least a couple of hikes away,” says Oliver in our latest fast podcast.

“Depending on where wages and inflation prints later this month, I think possibly we may follow the path of New Zealand or the UK into the 5.5%, possibly 6% region.”

Oliver points to three things blunting the impact of rate rises:

“Firstly, the Australian economy is demonstrating a level of resilience that’s greatly surpassed most expectations.

“Secondly, there seems to be a wage-price spiral in certain aspects of inflation that continues to channel within the CPI basket, so it persists at a level that warrants concern.

“Thirdly, despite market chatter about the potential fallout from high interest rates – particularly for mortgage holders – our analysis shows that Australians, on aggregate, aren’t as vulnerable as one might assume.”

Oliver goes into detail in the podcast.

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Which companies will benefit from AI technology in the long term? Which are caught up in a short-term frenzy? Pendal global equities analyst SUE SCOTT explains what to look for

- AI has changed investment landscape within months

- Companies ignore AI at their own peril

- Find out about Pendal Concentrated Global Share Fund

WITHIN months, artificial intelligence (or AI) has changed the investment landscape, helping drive the S&P500 into a bull market.

But which companies and sectors stand to benefit from AI technology in the longer term?

Which are just caught up in a short-term frenzy?

The technology has the potential to change every industry, says Sue Scott, a senior investment analyst with Pendal’s Concentrated Global Share Fund.

It’s about much more than investing in companies providing computing power and AI services, says Scott.

It’s about investing in companies that understand AI will become intrinsic to how business runs.

“The genie is out of the bottle. At an enterprise level you risk disruption if you ignore it.

“AI is going to have a significant impact on how all industries operates.”

Signs of a good AI strategy

What does Pendal’s global equities team look for when assessing a company’s AI capabilities?

“We’re looking for signs that the board and management are examining how the technology can improve their products and services and increase productivity,” Scott says.

“It’s not about how many times it’s mentioned on a conference call. It’s about understanding AI.

“Does the board have technical expertise? Are management introducing pilot programs? Are they thinking about the ways they can harness AI to improve productivity? Do they have a robust governance function?

“They’re the sorts of things were asking any of the companies we invest in.”

Look also for companies with a strong Chief Technology Officer, she says.

The CTO role “is becoming increasingly important, whether you’re a technology company, a mining company, or a consumer company.”

Find out about Pendal Concentrated Global Share Fund

AI pitfalls

AI has its challenges too, Scott says.

“Mass adoption means a huge amount of additional computing power is required, which is currently expensive and energy intensive.

“Lots of data storage is required and you need a network robust enough to transport all the information.

“The elephant in the room is regulation. Regulators have shown in the past that they are very slow on the uptake when it comes to new technology,” she says.

Scott says while Open AI’s Chat GPT was only launched late last year, AI has been around for much longer.

“AI is essentially a combination of computer science and data sets that enable problem solving and that’s been happening for years,” she says.

“Think about your first interaction with a chatbot and how that has improved over the last few years. Think about how much better search, Siri and Alexa are.”

“There’s also been huge developments in industrial sectors – autonomous mining trucks, automated fulfillments centres underpinned by AI technology have driven productivity gains, while consumer sectors have benefited from improved online advertising conversion rates.”

A printing press moment

The release of OpenAI’s ChatGPT was a turning point, however.

Scott agrees with founder OpenAI founder Sam Altman’s comment that AI could be a “printing press moment”.

“Right now it’s a load of raw data that generates outputs based on statistical probabilities when prompted. In the future you will see more multi-modality models. It won’t be just text but images, audio and video.

“A ChatGPT-equivalent won’t be writing just the speech, but the slide presentation to go with it. A search engine won’t just give the recipe for a chocolate cake, but also a video explanation of how to make that cake.”

All companies should be thinking about AI and how it can improve commercial outcomes for their business, she says.

About Sue Scott

Sue joined Pendal in 2016 as a senior investment analyst for the global equities team. She is responsible for global sector coverage of the technology, consumer discretionary and materials sectors.

Sue has more than 24 years of experience in the finance industry. Before Pendal she advised global and Australian investors in Morgan Stanley’s Institutional Equity Division.

Pendal Concentrated Global Share fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Just as mortgage holders locked in fixed rates two years ago, now could be the time to lock in 10-year bonds, argues Pendal’s TIM HEXT in our latest fast podcast

You can also listen to this podcast on Apple or Spotify

An excerpt from this interview with Pendal’s head of government bond strategies Tim Hext:

It looks like RBA boss Phil Lowe’s “got one more hike he’s itching to do” in July or August, says our head of government bond strategies Tim Hext in our latest fast podcast.

“The inflation data should start to turn down from that point,” says Tim.

“The RBA should then use that as a reason to be on pause for the rest of the year.

“Looking further beyond, towards the middle of next year, I think what you’re going to see is potentially the US starting to cut rates early next year.

“With that backdrop, there is a possibility we get lower rates in the second half of next year, even if inflation – and particularly wages – remain a bit sticky.”

For now, Tim argues investors should consider 10-year bonds which are hovering around the 4 per cent mark.

“I don’t think interest rates and cash rates in Australia, though they’re currently 4.1 per cent, are going to be averaging that over the next five or 10 years.

“I think they’ll settle eventually back down in the 2 to 3 per cent band.

“It’s a bit like mortgage holders two years ago should have locked in fixed rates for their mortgages.

“Now I reckon investors ought to consider locking in fixed rates for their investments.”

Listen to the full podcast above

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

Impact investing can be an important source of diversification in a number of ways, argues Regnan’s TIM CROCKFORD

- Impact investing can be a source of diversification

- Small, mid-cap, growth exposure

- Find out about Regnan Global Equity Impact Solutions Fund

IMPACT investment funds can be an important source of diversification in an equity portfolio because of their focus on small and mid-caps – and a tendency towards holding over very long time-frames, says Regnan’s Tim Crockford.

Crockford leads Regnan’s London-based impact investing team, which aims to find listed businesses well-placed to solve the world’s biggest environmental and societal problems.

Typically, these are companies with market capitalisations in the US$1 billion to US$10 billion range.

“Ultimately, as an impact investor you are managing on three dimensions rather than two,” says Crockford.

“It’s not just about risk and return, but also about the positive impact of companies bringing something good to the world.

“As a result, from a strategic asset allocation lens that gives you something very different from what you get with a traditional listed global equity allocation.

“The first level of that differentiation is that it gives you exposure to those smaller and mid-cap companies.”

That’s especially important in 2023 because smaller companies are trading relatively cheaper than their larger counterparts in an inversion of normal patterns driven by the market’s appetite for US mega-cap tech stocks.

“You would normally expect to pay a premium for small companies because they tend to have higher growth rates,” says Crockford.

“But something has changed across 2022 and smaller caps are now trading at a lower PE multiple than large caps.

“These kinds of abnormalities in markets can persist longer than you expect them to persist, but things eventually mean revert — they rarely become the new normal.”

Early access

Crockford says impact investing also offers investors a way to hold growth stocks at an earlier stage than in a traditional portfolio.

The Regnan Global Equity Impact Solutions Fund aims to buy companies at a point when they are seeing a tipping point in demand for their product or service.

Find out about

Regnan Global Equity Impact Solutions Fund

“What we do is try to identify businesses where growth rates are starting to tick up,” says Crockford.

“Like it or not, human beings find it very difficult to forecast growth rates that are increasing and compounding.

“That tends to make the market myopic and short term — analysts are trained to take the past and extrapolate that in the future.

“We look for these inefficiencies across our investment universe of environmental and social solutions providers and seek to take advantage of them.

“These are companies that have the potential to grow into large caps over the very long-term holding periods that we have for them.”

Longer time frame

The longer time frame of impact funds is another differentiator from a traditional equity allocation.

“This is a generational opportunity,” says Crockford.

“This is not the FOMO trade of the next six months. This is about finding companies with a structural tailwind for the next decade and beyond.”

As industry, consumers and governments invest to make the world more sustainable, winners will emerge over the next decades from the companies that supply the products and services to enable this, Crockford believes.

To find them, investors need to broaden their horizons beyond the top end of the market.

“We’ve been looking under stones that have not been turned over for a long time to find names that have been forgotten about in areas in markets that have been forgotten.

“This is about identifying individual businesses that have differentiated technology, differentiated services and a differentiated way of doing business.

“That gives them a moat. That gives them the ability to deliver this impactful environmental or social solution in a way that the peers can’t match.

“The fact that they are small now? Look the winners of the last market cycle – we didn’t refer to them as ‘big tech’ back in 2008.”

About Tim Crockford

Tim Crockford leads Regnan’s Equity Impact Solutions team and is senior fund manager of Regnan Global Equity Impact Solutions Fund. Tim previously managed the Hermes Impact Opportunities Equity Fund after co-founding the Hermes impact team in 2016.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

China has emerged quickly from zero-Covid, but its property industry is holding the economy back. What does that mean for investors? Here’s a view from Pendal’s head of income strategies AMY XIE PATRICK

You can also listen to this podcast on Apple or Spotify

An excerpt from this podcast

Amy Xie Patrick, Pendal’s head of income strategies:

The dropping of zero-Covid measures largely means that the huge restrictions on mobility no longer exist in China and you can go about living life as you wish.

Post Covid we saw in Australia a massive lift in the demand for services, a massive lift in the desire to go traveling, and a shift in consumption towards services.

That’s exactly what’s happened in China in the first few months of re-opening.

The difference with the China story though, is that a large part of the economy is still on its knees – and that’s the property part of the economy.

When the property sector is in a slump, it means that confidence from the private sector generally is in a slump as well.

That’s what’s is leading to a lot of the recent data showing that the initial momentum from China’s reopening story seems to be petering out.

The longer-term structural story for property in China is not a good one.

The Chinese inflation picture – and especially its Producer Price Index (a leading indicator of inflation) –will continue to drag more on the global inflation story – which is good for bonds, argues Amy.

We think there are many strong reasons both cyclically and structurally to be favoring fixed income and bonds in portfolios right now.

The way the China growth story is shaping up for 2023 presents as one of the top five reasons to be buying bonds right now.

Find out about

Pendal’s Income and Fixed Interest funds

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

With inflation still high but ‘sufficiently well-behaved’, the factors influencing recession are now unemployment and wages. Pendal’s TIM HEXT explains in this fast podcast

You can also listen to this podcast on Apple or Spotify

An excerpt from this interview with Pendal’s head of government bond strategies Tim Hext:

Consumers are feeling gloomy but are we still headed for recession?

With inflation “sufficiently well-behaved”, the main factors are now unemployment and wages, says our head of bond strategies Tim Hext.

“I think in the US it’s still the case that we are going to have a very mild recession at some point.

Whie it’s taken longer than expected, the impact of 5.25% of rate hikes in just over a year are starting to show through among consumers.

“The one thing that’s keeping the US economy ticking over still quite well is employment.

Jobs and wages should remain “not strong, but well-behaved” this year, which should stop any chance of near-term rate cuts, says Tim.

In Australia the chances of recession are far lower due to population growth, says Tim.

“But there is definitely a possibility we’ll have a GDP per capita recession. In other words, the economy will be better off but individually we may not feel that way.

Tim goes into detail here

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

How should fixed interest investors think about the turmoil among US regional banks? In our latest fast podcast, Pendal assistant portfolio manager OLIVER GE gives a plain-language explanation

You can also listen to this podcast on Apple or Spotify

An excerpt from this podcast with Oliver Ge, an assistant portfolio manager with Pendal’s Income and Fixed Interest team

“The problems with First Republic and SVB are not unique,” says Oliver.

“There are potentially cracks opening up in the 5th, 6th, 7th, and 13th largest banks.”

If further failures occur, investors may be over-confident that the Federal Reserve wil continue to launch rescue missions, says Oliver.

The relatively mild market response could suggest “a disconnect between what investors are pricing in and what’s actually happening”, he says.

In this podcast, Oliver explains what that could mean for investors – and why he believes cash and government bonds are an important consideration for portfolios right now.

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

It’s become increasingly important for equities investors to understand how companies in their portfolios are protected from data breaches, says Pendal’s SUE SCOTT

- Increased focus on cyber security

- Investors need comfort from cyber policies

- Find out about Pendal Concentrated Global Share Fund

AFTER the recent Optus and Medibank data breaches, stockmarket investors may be wondering what to look for when assessing how vulnerable a company is to a hack attack.

Big, listed companies can make attractive targets for hackers.

“The larger the company, the more data it has and the more critical it is to society,” asks Sue Scott, a senior analyst in Pendal’s global equities team.

“These companies are more likely to be targeted for a cyber-attack,” Scott says. “Given our investment philosophy, it’s a particular risk for several of our portfolio companies.

“Understanding the risk, and what is being done by management to mitigate the associated with a cyber-attack on that business is critical.”

Scott use the example of Spanish financial services giant CAIXA, which Pendal has assessed for cyber-security risks.

Find out about Pendal Concentrated Global Share Fund

CAIXA has the largest IT platform in Spain and processes some 30,000 transactions per second.

“They receive 74 attacks every hour and the number of attacks has increased 2.6 times in 2022 compared to 2021,” Scott says.

Yet CAIXA hasn’t experienced a successful critical attack, says Scott.

What to look out for

Before investing, Pendal scrutinised the policy framework CAIXA has in place to understand preparedness for cyber-attacks and mitigation efforts.

“Importantly we saw that there are very clear roles and responsibilities defined within CAIXA.

“It has a cyber policy that’s corporate wide and mandatory for everyone to comply with.

“They have a specialised Cyber Security Committee which includes executive management representation; an audit team which presents to the board regularly; and three board members with specific technical expertise.

“Board members receive training and it’s reflected in the KPIs of management.”

An important addition at CAIXA is the Cyber Risk and Compliance role, separate from the Chief Technology Officer role.

“CAIXA felt when tackling cyber security, it’s important to have someone with a technical focus, and someone focused on governance.

“It also undertakes independent assessments of their cyber security capabilities twice a year, as well as complying with all European regulation regarding cyber safety,” Scott says.

Danger from within

Risks can also come from staff — whether intentional (such as a dissatisfied employee) or unintentional.

CAIXA monitors unusual behaviour among staff and their use of data.

“If there’s any abnormalities exposed then they investigate further,” Scott says.

“For non-intentional risks CAIXA has comprehensive training programs for staff and customers.”

One challenge is the ability to attract the relevant talent into a cyber security division.

“Everyone wants technical talent now to negate cyber risk. The fact that CAIXA has scale and is heavily resourced has helped attract people and keep the attrition rate very low,” Scott says.

“It gives us a lot of comfort talking to them, helping us understand what good looks like in terms of a cybersecurity policy and implementation of that policy.

“While good policy and technical expertise aren’t enough to prevent all attacks, they do mitigate the risk of an attack where critical business functions are affected, and reputational damage is inflicted.”

About Sue Scott

Sue joined Pendal in 2016 as a senior investment analyst for the global equities team. She is responsible for global sector coverage of the technology, consumer discretionary and materials sectors.

Sue has more than 24 years of experience in the finance industry. Before Pendal she advised global and Australian investors in Morgan Stanley’s Institutional Equity Division.

Pendal Concentrated Global Share fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

- Find out about Regnan Global Equity Impact Solutions Fund

REGNAN portfolio manager Tim Crockford spends most of his time searching for companies with an innovative edge in solving the world’s biggest problems.

Right now the opportunities lie with smaller companies, he argues

IT would take nerves of steel to write-off US large-cap equities.

Trading at just below 20x price/earnings, the S&P 500 can be seen as either over-valued or under-valued, depending where you think the world is going.

Given the rally in Big Tech through the first quarter, quite a few investors would seem convinced that there’s life — and value — left in long-duration, large-cap growth.

But this feels like a belief that the future will replay the past.

Are there alternatives?

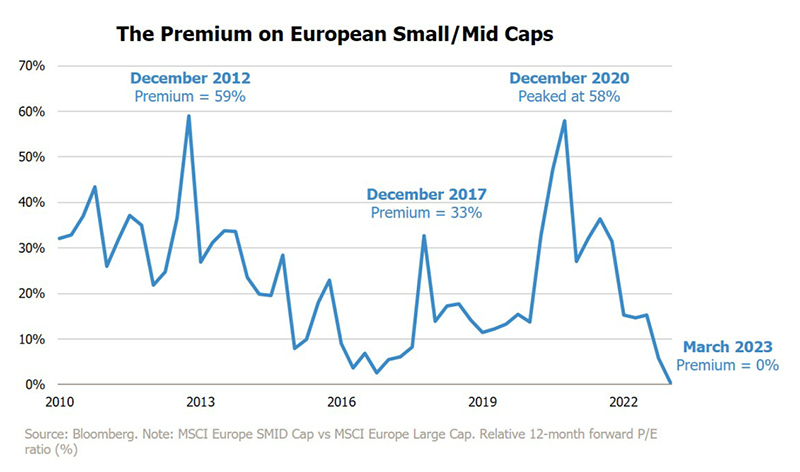

The chart shows the premium on European small and mid-cap relative to their large cap peers.

It is now approaching zero — the lowest it has been since the aftermath of the Global Financial Crisis.

We wouldn’t like to call the market.

But what we can do is identify opportunities in the European small and mid-cap area that we feel deserve serious consideration.

Here are two.

Alfen is a manufacturer of smart grid solutions that accelerate the energy transition.

It’s the only company in Europe combining smart grids, energy storage systems and electric vehicle (EV) charging systems into a single integrated approach.

A key growth market for the business is its range of smart-connected EV chargers, enabling the broader adoption of electric vehicles.

The prospective growth of EV hardly needs to be emphasised.

Ford Europe, as one example, expects to switch completely to electric vehicles in just two years.

Find out about

Regnan Global Equity Impact Solutions Fund

Stevanato Group has been operating for 70 years, most of that time manufacturing basic glassware.

Its current — and future — strength lies in “containment” technology.

This involves machinery that greatly accelerates the production of sterile medical equipment, particularly pre-filled syringes and vials used in high-growth biologic therapeutics.

About Tim Crockford

Tim Crockford leads Regnan’s Equity Impact Solutions team and is senior fund manager of Regnan Global Equity Impact Solutions Fund. Tim previously managed the Hermes Impact Opportunities Equity Fund after co-founding the Hermes impact team in 2016.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

It’s back to the future for investors with 2023 looking like a “normal financial crisis”, says Chris Lees, co-manager of Pendal Global Select Fund

- Opportunities in technology and consumer staples

- Exporters in UK, Europe and Japan are favoured

- Find out about Pendal Global Select Fund.

IT’S back to the future for investors with 2023 looking like a “normal financial crisis”, says Chris Lees, co-manager of Pendal’s Global Select Fund.

“The classic 60/40 asset allocation model is working again,” says Lees in a recent quarterly webinar.

Scroll down to watch the full presentation.

Inflation remains the big unknown — specifically whether we’re facing a 1970s-style scenario when rates rose and then were cut too early, triggering a second round of price rises.

Or a 1980s-type scenario where rates stayed higher for longer and inflation was killed off.

Or should investors expect an injection of liquidity – the so-called ‘Greenspan put’ – if markets fall sharply?

Lees and fellow co-manager Nudgem Richyal have not bought any western banks for the fund in about 15 years. “The banks are not as cheap, and not as safe, as many investors and depositors think.”

“We don’t find them particularly attractive at 0.5 to 1.5 times book [value],” Lees said.

“We do however own as couple of emerging market banks which are very profitable, with 300-to-500 basis points of net interest margin spreads. They are growth stocks in emerging markets.”

“We still think the short-term risk to interest rates is still probably on the upside, and the short-term risk to earnings is probably on the downside,” Lees says.

“The investment environment is clearly changing from last year’s inflation and interest rate shock to this year’s banking shock,” he says.

This means sectors such as financials and energy have deteriorated, from an investor’s viewpoint. Technology and consumer staples have improved, he says

Pendal Global

Select Fund

Something very

different in

global equities

“At the regional level, we’ve seen the UK, Europe and Japan improve at the margin, and specifically the exporters in those markets,” Lees says.

“And that’s the type of stock that we’ll be looking to add to the portfolio next – some world class champions in the UK, Europe and Japanese technology or consumer staples sectors.”

About Chris Lees and Nudgem Richyal

Chris Lees co-manages Pendal Global Select Fund with Nudgem Richyal. The pair have been working together in global equities investing for more than 20 years.

Chris has more than 32 years of investment industry experience. He joined Pendal Group’s UK-based asset manager J O Hambro Capital Management (JOHCM) in 2008 after spending 19 years at Baring Asset Management, ultimately as head of its global sector team.

About Pendal Global Select Fund

Pendal Global Select Fund is a global equities portfolio with a distinctive, yet proven approach.

Fund managers Chris Lees and Nudgem Richyal have worked closely together for more than 20 years.

They manage a portfolio of 30-60 stocks using quantitative analysis and fundamental research based on decades of experience.

The team draws on the expertise of 40-plus investment professionals at JOHCM and Regnan.