Resolving the humanitarian crisis in Ukraine must be our first concern says Pendal’s head of global equities ASHLEY PITTARD. But if a peaceful resolution is found, what can global equities investors expect next?

- Russia’s invasion of Ukraine could impact pace of US rate rises

- Fears of stagflation could ultimately trigger more rate hikes

- Find out about Ashley’s Pendal Concentrated Global Share Fund

RUSSIA’S unprovoked invasion of Ukraine means global central banks won’t be as aggressive raising interest rates as they would have been otherwise, especially in Europe.

And while bourses have sold off, particularly in Europe, typically equity markets recover within a year, says Pendal’s head of global equities Ashley Pittard.

“On average, markets fall between 4 and 15 per cent in the near term after an attack,” says Pittard.

“When it looks like someone is getting control, usually a year after that equity markets are higher.”

The war in Ukraine is first and foremost a humanitarian crisis, Pittard says, and the flood of refugees out of Ukraine is tragic.

In economic terms, the immediate impact has been on commodities and share markets.

Led by oil, commodity prices are sharply higher. The cost of a barrel of Brent crude headed towards $US140 this week, the highest since 2008. The jump in commodity prices is likely to trigger higher inflation for longer, Pittard says.

Wars tend to be inflationary, he says.

Find out about

Pendal Concentrated Global Share Fund

“It may mean inflation in the United States is in the 5 to 7 per cent range for longer than most people expected.

“So, the Federal Reserve will have to raise rates but maybe it will do it a bit slower because it won’t want to be too aggressive when there’s a war on.”

“It means there could ultimately be more interest rate hikes, though they may be delayed,” Pittard says.

“And there’s the risk of stagflation, rather than nice growth and moderate inflation.”

Share market volatility has increased, particularly in the Euro region.

In the first full week of trading after the invasion of Ukraine, European bourses ended down around 10 per cent, whereas the US, Japan and Chinas were down two per cent at most.

The local S&P/ASX200 was one of the few developed economy bourses that ended the week high.

European markets are now down 20 per cent off their peaks of last year, whereas Wall Street is off around 10 per cent.

“In Europe it doesn’t matter if you are a beverage company or a financial. Everything’s being sold because the region’s economies are so intertwined with Russia,” Pittard says.

“And much of that reflects the critical energy supplies that run between Russia and Europe.

“The US is less reliant on Russia so the volatility hasn’t been as great.”

A Pendal statement on Russia’s invasion of Ukraine

During these tragic times, Pendal’s sympathy lies with the people of Ukraine in their struggle to maintain their freedom.

As responsible investors, Pendal Group and its affiliates J O Hambro Capital Management, TSW and Regnan have taken decisive steps to reduce our already minimal exposure to Russian securities.

We are limiting direct risk in client portfolios and taking decisive steps to comply with evolving sanctions and restrictions. We will refrain from investing in Russian and Belarusian securities for the foreseeable future.

The situation is evolving rapidly and we continue to monitor the emerging risks, which may take an unexpected form as the consequences ripple through the financial and economic systems.

As active managers, our purpose is to navigate our clients through a world in flux to protect their interests during uncertain times.

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The first half of this year will be all about volatility, but the Fed’s ability to control inflation will be the critical factor in 2022, says Pendal’s head of global equities ASHLEY PITTARD

- 2022 kicks off with rotation from tech to value stocks

- Fed rate rises critical to second-half outlook

- Commodities should benefit from China acceleration

THIS year will again be a tale of two halves for investors, and the critical factor is whether the US Federal Reserve can control inflation, without busting the business cycle.

That’s the view of Pendal’s head of global equities Ashley Pittard.

“Last year was a tale of two halves,” Pittard says. “The first was about re-opening, and the second was about Delta and Omicron.

“This year will also be a tale of two halves, but it will be very different.

“The first half this year will be all about volatility. The Fed has been behind the curve and needs to increase interest rates to get inflation under control.

“Expectations of rate rises have risen over the past couple of months. Late last year we expected market volatility to increase, and January hasn’t let us down,” Pittard says.

There’s already significant rotation from the tech stocks into the value sector, including banks and energy companies, he says. That’s demonstrated by the big fall in the tech stock heavy NASDAQ, which so far this month is down more than 10 per cent.

“A lot of these stay-at-home companies are being torched,” Pittard says.

“Heading into the holiday period, we thought tech stocks were likely to underperform, and the lofty valuations in that part of the market, and the relative weighting of tech companies in indices, meant equities would underperform. And that’s what’s happened.”

It’s likely to continue if early profit reports for the last quarter are indicative. With about 5 per cent of companies having reported, two of the most notable have been tech stocks, Pittard says.

Find out about

Pendal Concentrated Global Share Fund

Netflix’s share price fell more than 20 per cent immediately after it reported disappointing subscriber growth numbers.

High-tech home fitness company Peloton outlined production challenges and potential staff lay-offs and its share price fell as low as $US24 a share. That’s down from its peak of $US160 a share last year.

In contrast, several non-tech companies have provided positive earnings results.

Rail companies Union Pacific and Alston, construction company Scandic Builders, and sportwear group PUMA have all performed relatively well, Pittard says.

What’s next?

That’s the story of the first half of 2022 — inflation and higher interest rates, volatility and rotation out of tech stocks.

“The second half will depend on how well the Fed does its job,” Pittard says. “Will it go too hard and push the economy into recession or will it do enough to cap inflation and not kill the business cycle?”

“If the Fed does a good job — clamps down on inflation without short-circuiting the cycle, then in the second half there’ll still be geopolitical tensions.

“And there’s mid-term elections in November. If the Republicans win the House back, it makes it harder for President Joe Biden to do much in his second two years.

“But at least if you get four rate hikes, and not six or seven, then in the back half of the year there should be a re-rating of the market,” Pittard says.

One sector which could benefit is commodities.

“While the US is raising rates, China is cutting rates. They’re adding more liquidity and that economy is built on manufacturing which needs commodities. That underlying dynamic should help commodities over time.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

The key question for 2022 is whether the US Fed can keep inflation under control without short-circuiting the business cycle, says Pendal’s head of global equities ASHLEY PITTARD

- Investors head into 2022 with unusual macro settings

- Risk is tech stocks underperform, dragging down the market

- Opportunity for mid and small caps to outperform

GLOBAL equities investors enter 2022 with very unusual macro-economic settings in place – high inflation and low bond yields.

It’s Covid-related — as is the recent rotation back to perceived safer assets such as US tech stocks.

The rotation is contributing to one of the biggest risks to global equities in the coming year — mega caps underperforming and markets going backwards with increased volatility, says Pendal’s head of global equities, Ashley Pittard.

“The past year has been a tale of two halves,” says Pittard.

“The Delta variant of Covid-19 hit mid-year and delayed the recovery and the re-opening story. The market rotated back to safe havens.

“For example, five of the top stocks in the Nasdaq 100 – Microsoft, Apple, Alphabet, Tesla and NVIDIA – contributed 72 per cent of the total NASDAQ return.

“There’s lofty valuations in equities and a narrowness of the market because of the tech companies.

“There has been a massive initial public offering frenzy, there’s inflation that is now more than transitory and the US Federal Reserve is withdrawing stimulus.”

Find out about

Pendal Concentrated Global Share Fund

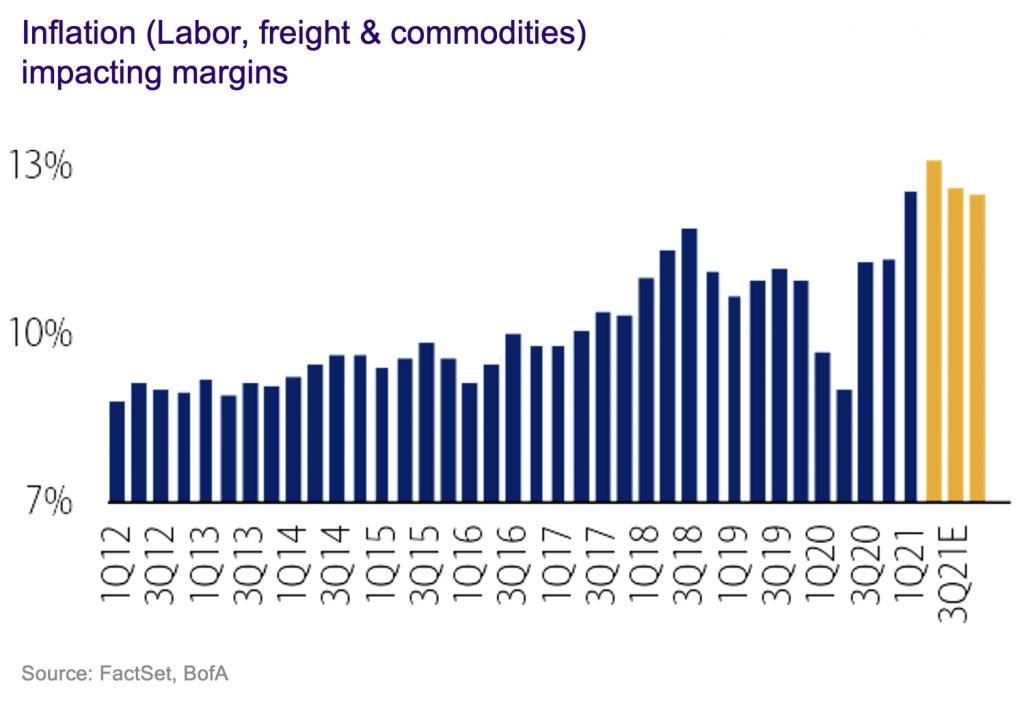

Inflation is critical. Pittard argues it’s more than transitory because wage increases are now being embedded into economies, and the cost of housing – be that home prices or rents – are set to rise. Higher inflation will impact company profit margins and earnings.

“So the big risk for 2022 is muted or negative returns for global indices and increased volatility,” he says.

Opportunity in 2022

Opportunity in 2022 depends heavily on the US Federal Reserve, Pittard says.

“Can the US Fed keep inflation under control without short-circuiting the business cycle? That’s the key question.

“If earnings growth can broaden outside tech companies — and capital spending increases outside really large caps and the top five NASDAQ stocks — markets will do very, very well.

“We have already seen some fragility in the earnings growth of the ultra-large tech companies.

“But if we see broad-based capital spending and earnings growth, the mid and small caps will do well.

“The banks will do well. Businesses that have pricing power will do well and emerging markets will do well.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Are the FAANGs losing their bite? The latest US earnings season has revealed new opportunities and risks, says Pendal’s head of global equities ASHLEY PITTARD

- Global equities earnings growth extends beyond tech stocks

- Europe, small caps provide opportunities

- Find out about Pendal Concentrated Global Share Fund

FAANGs out, MAMAAs in. At least in terms of acronyms — maybe not in terms of earnings.

Facebook’s decision to change its company name to Meta Platforms — and the incredible performance of Microsoft, which is now the largest company in the world — has made obsolete the famous acronym that’s dominated global equity markets for five years.

FAANG (Facebook, Apple, Amazon, Netflix, Google) doesn’t work anymore.

Instead, the more homely, less ferocious, MAMAAs better represents the tech market leaders, says Ashley Pittard, head of global equities at Pendal. That’s Microsoft, Apple, Meta (Facebook’s new name), Amazon and Alphabet (Google’s parent company).

The new acronym doesn’t quite bare the teeth of the old acronym.

“During the last couple of quarters, other sectors away from the MAMAAs have been compounding really strongly,” Pittard says.

“We are getting through the US earnings season and most of the ultra-large caps have reported.

“You are seeing sales up 15 per cent. Earnings are up 39 per cent. Of that, 79 per cent have beaten on third-quarter earnings and 73 per cent have beaten on revenue.

“The results are still being impacted by the Delta lockdown which affected the September quarter earnings season, so it isn’t yet a true indication of what a re-opened, normalised environment is,” Pittard says.

“It’s upbeat for the third quarter. There was strong demand, productivity measures helped keep costs down and there are headwinds of supply chain cost pressures.

“But there’s no doubt that if you look at those FAANG stocks, it’s the first time in many years that they’ve missed on revenue,” Pittard says.

Find out about

Pendal Concentrated Global Share Fund

“If you take Apple as an example, it missed revenue forecasts for the first time since 2017. Its earnings were in-line for the first time since 2016.

“Amazon missed on revenue. They’re getting hit on wages growth, supply chain and network inefficiencies.”

The result is a broadening out in earning growth.

“You’re continuing to see broadening of the sectors growing… and you will continue to see the rotation to other sectors and out of those MAMAAs stocks, which have been the darlings of the last five years.

Where to next?

So, the question is where to rotate into.

The stocks and sectors doing best are those leveraged to better economic growth including sectors like energy, materials, industrials, and financials, Pittard says. Small caps could also outperform.

“Defensive areas like consumer staples, health care and telecommunications aren’t growing by as much,” Pittard says.

He adds that Europe, which is relatively underweight tech stocks and overweight energy, materials, industrials, and financials, is growing faster than the US.

The ultra large tech stocks have led the S&P500 up more than double over the past five years, whereas the STOXX Europe 600, which measures a basket of European stocks, is up less than 50 per cent in the same period.

“It’s because Europe hasn’t grown earnings like the US over the last five years. That’s because the growth in earnings has been driven by tech stocks,” Pittard says. “But I expect this to mitigate.”

“I expect to see the European markets, small caps on Wall Street and sectors outside the MAMAA stocks to re-rate higher and that’s where there’s going to be earnings growth.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

If the pick-up in capital spending among businesses continues, higher prices are much more likely to be here to stay, says Pendal’s head of global equities Ashley Pittard

- Capital spending can trigger longer term, sustainable inflation

- Big rises in profit margins spur businesses to invest

- Evidence points to inflation shifting from transitory to structural

CAPITAL spending is the dark horse in the debate on inflation, says Pendal’s head of equities Ashley Pittard.

Wage and transport costs and consumer spending tend to grab the headlines. But capital investment by business, with long lead times, can provide a significant, sustainable fillip to prices.

“If we start seeing capital expenditure re-rating year on year, that will solidify inflation coming through,” says Ashley Pittard, head of Pendal’s Global Equities boutique.

“In the first quarter of this year capex was mixed in the United States. But in the second quarter it was the strongest capex since 2004.”

The prospect of inflation remains the big question in financial markets: is it transitory or structural?

Central banks around the world have mostly argued it is transitory. But in recent weeks the US Federal Reserve, the European Central Bank and the Reserve Bank of Australia, among others, have spoken of winding back bond purchase programs.

If the pick-up in capital spending continues, higher prices are much more likely to be here to stay.

Businesses, particularly in Europe and North America, are willing to invest because of the earnings boosts they’ve experienced in the first half of this year — and based on improved profit margins.

“Earnings growth is up almost 100 per cent across the S&P500 for the June quarter, but sales growth was up only 27 per cent,” Pittard says.

“In Europe, the sales growth was 28 per cent, which is very similar, but the earnings growth was 243 per cent.”

Europe’s outperformance partly reflects the mix of sectors with energies and financials higher contributors to European bourses. Those sectors have done very well with commodity prices rising, and relatively few bad debts to deal with for the banks.

Also, Europe started from a lower base and had more scope to climb, Pittard says.

“Earnings have been strong year-on-year and against 2019. But companies are also getting massive margin expansion and in some cases the highest margins ever,” he says. “This is encouraging capital spending which is adding to inflation.”

Find out about

Pendal Concentrated Global Share Fund

Price rises are already coming through with US inflation up 7.8 per cent in July, German inflation at 3.4 per cent (the highest rate since 2008) and Spain at 3.3 per cent.

“You are seeing Europe getting inflation in the mid threes. You have the US with inflation well above 5 per cent,” Pittard says.

For businesses, when borrowing is so cheap, and earnings are rising, they pay down their debt quicker and can invest more, he says.

If the investment is productive it can eventually reduce inflation. But in the short-to-medium term it will put pressure on prices.

Capital spending adds another piece of the argument that inflation is more than transitory.

“There is no doubt it is a timing issue before transitory inflation becomes structural inflation,” Pittard says.

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Pendal Wholesale Plus Active Growth Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a significant weighting towards growth assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium to long term.

Much of the confusion about ESG stems from three questions. Here Regnan senior ESG and impact analyst MURRAY ACKMAN explains the answers

- Diversity targets are often flawed

- But DEI is a good indicator of how well a company is managing risk

- Find out about Regnan Credit Impact Trust

- Find out about Pendal Sustainable Australian Fixed Interest fund

ESG can be pretty confusing for investors.

The acronym (which stands for Environmental, Social and Governance issues) refers to a jargon-filled investment space which requires an understanding of regulations, methodologies and taxonomies.

And the more ESG evolves, the more complicated it becomes for investors trying to judge the effect of these criteria on their investments.

Why is ESG so confusing? How can you see through the noise?

Much of the confusion about ESG stems from three questions facing investors.

Here we’ll try to explain them.

1. Are we looking at the same thing?

Third-party ESG data providers often have different views and methodologies for rating different companies.

That means ESG data requires more interpretation than, for example, balance sheets or credit ratings.

Credit rating agencies may offer different ratings — but they largely analyse the same numbers from financial statements.

An ESG report can include absolutely everything that has an impact on the macro, meso and micro environmental, social and governance risks a company may face.

There is also the overwhelming challenge of conflation.

A fossil fuel extraction company may be managing its risks reasonably well — but if investors don’t want to invest in fossil fuels then it seems rather irrelevant.

2. Are you saying what I think you’re saying?

Everywhere we see advertisements aimed at convincing people that if they invest with a particular manager they’ll be able to save the world.

To combat this kind of hyperbole, regulators and gatekeepers have stepped in to reduce potentially misleading and deceptive conduct.

Find out about

Regnan Credit Impact Trust

Murray Ackman,

Sustainable Finance and

Impact Investing Director

This includes education for clients, longer caveats and attempts at standardising terms such as “sustainable investing”.

For investors, this means more surveys, greater reporting, a focus on data and ensuring proper systems are in place.

Regulators are pushing for standard language and consistent data to help people understand what’s being said.

That’s a positive step — but more education, more disclosure and more reporting are not enough. People don’t read every food label before eating.

Now ESG is starting to be viewed less as a marketing problem and more as a compliance challenge.

At Regnan, we continue to strongly believe that including ESG criteria in the investing process provides more information to make better investment decisions.

3. Does ESG actually affect investment decisions?

Are ESG consideration linked to reality? Does it do what clients actually want? Do ESG funds outperform?

You should be able to find ESG integration statements on most big asset manager websites which outline how they include ESG considerations in their decision making.

Realistically, sometimes ESG considerations might have only a limited influence on an investment decision. But this differs across asset classes.

For example, omitting energy stocks that gained significantly would’ve made outperformance difficult for some equity strategies over the past two years. But it would have had little impact on fixed income.

How much ESG is included in investment decision-making is ultimately up to clients.

Do you want to invest to make a more sustainable economy and potentially avoid some risks? Or is performance the only thing that matters?

At the end of the day, fund managers, super funds and financial planners are all trying to serve the needs of their clients.

What approach is best? It’s about working out what ESG does for different clients.

Some might hate anything that suggests companies need to consider the environment. Some might not want to make the world worse. Others may want to make the world a better place.

These are values judgements.

Here’s a very simply way I explain ESG investing:

- If you only care about performance, that doesn’t necessarily mean you should ignore ESG funds. Some ESG funds are top performers across the board. ESG approaches may also highlight non-financial risks that can become financial risks.

- If you want to avoid investing in bad stuff, focus on a fund that has negative screens (eg no tobacco producers or controversial weapon makers). What is considered bad may differ between clients, but these type of screens are becoming more uniform.

- If you prefer to invest in good stuff, look for funds that have some kind of process for selection of investments, and some kind of measurement on what those investments are doing.

- If you want really good stuff, look for something that explicitly addresses “impact”. There may be more novel strategies available, but there will likely be trade-offs such as having funds locked-up or high volatility in performance.

It’s natural for clients to be apprehensive about ESG because it’s a new topic full of technical words. But while there are definitely some parts that need more work, there are quite a few of us working on improvements.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Some billionaires argue diversity, equity and inclusion policies are a bad thing – and could even cause plane crashes. Pendal’s MURRAY ACKMAN explains why they’re wrong

- Diversity targets are often flawed

- But DEI is a good indicator of how well a company is managing risk

- Find out about Regnan Credit Impact Trust

- Find out about Pendal Sustainable Australian Fixed Interest fund

AMERICAN billionaires seem to be picking fights with big brands and civil rights groups over whether corporate diversity, equity and inclusion (DEI) policies are discriminatory.

Or even whether they cause aircraft malfunctions.

If you’ve been following the “woke backlash”, you’d be familiar with recent flash points such as the campaign against Harvard’s first Black female president Claudine Gay.

Tesla’s Elon Musk, hedge fund manager Bill Ackman and Lululemon founder Chip Wilson have all been engaging in civil discourse on social media recently, expressing anti-DEI views.

Musk went as far as suggesting that Boeing, fresh from having a fuselage panel fall off mid-flight last month, was prioritising diversity over safety. That drew a swift rebuke from civil rights groups.

“DEI must DIE,” Musk said recently on his X social network. “The point was to end discrimination, not replace it with different discrimination.”

This week the Tesla CEO erased mention of DEI in the electric vehicle maker’s corporate filings.

Find out about

Regnan Credit Impact Trust

Murray Ackman,

Sustainable Finance and

Impact Investing Director

Do DEI critics have a point? And what does that mean for investors and companies?

What are the concerns about DEI?

Musk’s criticism of Boeing centred around the impact and unintended consequences of connecting executive pay to diversity targets and ESG metrics.

At the start of 2022 Boeing altered its bonus scheme, rewarding executives who hit certain climate and DEI targets.

Boeing is certainly not alone here.

In 2011, just 1 per cent of listed companies had such a policy. By 2021 it was 38 per cent, and the trend continues.

Supporters argue this is positive for companies and shareholders.

The idea is that such policies safeguard future economic results from risks while aligning the managerial objectives with shareholder interests.

Sharemarket analysts look for such policies as a sign that a business cares about a particular issue.

Who’s right?

Does linking executive pay to diversity improve a business? Or are such corporate DEI policies a sign of excess?

There are plenty of studies – including from Pereptual’s Regnan sustainable investing business – suggesting DEI can drive business outperformance.

A 2021 study from sustainable investing leader Regnan found that DEI – and especially equity and inclusion – can drive business outperformance.

A series of McKinsey & Company reports found “not only that the [DEI] business case remains robust but also that the relationship between diversity on executive teams and the likelihood of financial outperformance has strengthened over time”.

Yet Regnan also found many businesses think about diversity and inclusion in a flawed way. For example, DEI policies often focus on the needs of minority groups, while majorities are not always adequately considered.

For investors and companies alike, we believe organisational settings should allow all talent to flourish – including ‘majority talent’ as well as talent that is traditionally under-represented.

These are essential pre-requisites for an equitable and inclusive workplace. Businesses benefit from fair employment practices, supportive cultures and open decision-making.

What it means for investors

While there is now a lot of ESG measurement going on inside companies, it’s fair to say there could be a deeper discussion about how inclusive culture can be good for a business.

But is Elon Musk right to say there is undue focus placed on DEI?

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

The billionaire’s complaints could make sense in the context of a boot-strapped start-up operating from the proverbial garage.

But it feels provocative coming from the CEO of a business with one of the highest market caps in history.

Based on our experience at Pendal, businesses clearly demonstrate what they care about by what they report.

And that is useful for investors.

Investors should expect to see comprehensive DE&I plans from companies. And take caution with companies that ignore these responsibilities.

And they should look beyond the reported diversity numbers to understand if a business has the right structure to allow for diversity and growth.

While it’s entertaining to see billionaires argue among themselves, investors must understand how a company thinks about diversity and inclusion if they want to understand whether it is managing risks.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

A global taskforce backed by Australia aims to shift global financial flows away from ‘nature-negative outcomes’. Pendal’s MURRAY ACKMAN explains

- Investors need to consider biodiversity

- Agriculture, food sectors impacted most

- Find out about Regnan Credit Impact Trust

- Find out about Pendal Sustainable Australian Fixed Interest fund

MORE than half of global GDP depends on natural resources — and these days investors are well aware of biodiversity risk when making portfolio decisions.

Now a group of companies representing the sectors most exposed to the impact of nature loss has come together to guide investors away from what they call “nature-negative outcomes” towards “nature-positive outcomes”.

The Taskforce on Nature-related Financial Disclosures (TNFD) is made up of representatives from 40 organisations in sectors such as agribusiness, the blue economy (ocean resources), food and beverage, mining, construction and infrastructure.

It’s also backed by the Australian federal government — which has provided funding and participated in pilot programs.

New guidelines

In September, the taskforce issued a set of guidelines which aims to integrate nature into decision-making and give organisations a complete picture of their environmental risks,” says Pendal ESG credit analyst Murray Ackman.

It is, in part, a consequence of greater disclosure requirements around environmental risks, Ackman says.

“More than half the world’s GDP is estimated to depend on biodiversity and ecosystem services.

“Fresh water, fertile soils, clean air and even insects pollinating plants — the flow-on effects of the degradation of biodiversity are immense.

“As we become more aware of threats such as climate change, we’re beginning to understand how interrelated everything is.

“The framework is still emerging, but people are hoping biodiversity risk will become tied into a company’s social licence.

A global initiative

Investor focus on biodiversity has intensified in the past couple of years as regulation evolves to combat prevent “greenwashing”.

“The TNFD is a new global initiative which aims to give financial institutions and companies a complete picture of their environmental risks,” Ackman says.

“Biodiversity should be considered in managing business risks, and also in terms of system wide risks. It can can be seen as a proxy for resilience.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

“Companies that have an understanding of their biodiversity risk are more likely to have a multifaceted understanding of all their risks.

“Some sectors are more impacted than others. There is a more immediate effect on agriculture than on business software providers, for example.”

Investor influence

Already some big investors are using their influence to push companies to understand their biodiversity risk.

Though insisting that all companies spend time and resources deep-diving into biodiversity risk might not be an optimal outcome, says Ackman.

“At Pendal, our focus is on direct risks in certain sectors like agriculture or sectors involved in selling food.

“We focus on the angels and demons — the extremes. We look at the sectors with a huge risks.

“On the angel side, we’re looking for solutions to some of the biodiversity challenges. That includes investing in World Bank bonds.

“In other sectors, biodiversity risk falls under the broad umbrella of whether a company is managing credit risk in general. Are they managing all their potential risks?” Ackman says.

Find out about

Regnan Credit Impact Trust

Murray Ackman,

Sustainable Finance and

Impact Investing Director

Pendal has invested in a Biodiversity and Sustainable Development bond from the World Bank, which has an explicit focus on biodiversity.

“This bond is helping to put nature as central to development through promoting conservation, training, and policy to seek nature-based solutions in agriculture, forestry and fisheries.

“We view biodiversity as more than just another risk reporting framework.

“We see it as an opportunity to invest in solutions, and we’re optimistic that we will see more ways to bring about development and environmental outcomes through these types of investments.”

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

There’s a dearth of true ‘social bonds’ in the market, but the reward for issuers can be great, explains Pendal ESG credit analyst MURRAY ACKMAN

- Pendal believes social bonds should serve the underprivileged

- Find out about Regnan Credit Impact Trust

- Find out about Pendal Sustainable Australian Fixed Interest fund

MOST social bond investors have the same aim: to make money while making a positive difference in society.

An example is the federal government’s National Housing Finance and Investment Corporation, which last year issued almost $200 million in social bonds, making returns for investors while providing cheap funding for social and affordable homes.

But not all social bonds are equal when it comes to use of proceeds, cautions Murray Ackman, a credit ESG analyst with Pendal’s income and fixed interest team.

“At the heart of social bond issuance is what the proceeds are is used for,” says Ackman.

“At Pendal, we want the proceeds to benefit the under-served. In the social bond market, that isn’t always the case.”

Not all social bonds are equal

The term ‘social bond’ has different meanings to different investors.

Social bonds are defined by The International Capital Market Association as use of proceeds bonds that raise funds for new and existing projects that address or mitigate a specific social issue or seek to achieve positive social outcomes.

But Pendal takes a more refined view, focusing on bonds that benefit the underprivileged.

“It means that we run into the risk of the proceeds of social bonds not being allocated as we’d want,” says Ackman.

“An issuer might promoted a ‘social bond’ — but it may not meet our criteria of helping the underserved in society.”

“For example, we’ve seen so-called ‘social bonds’ where proceeds have gone towards anyone impacted by Covid. That’s everyone.”

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

“In the Netherlands, around 70 per cent of the population is eligible for some kind of social housing.

“So, the Dutch Housing Authority can do a ‘social bond’ — but that’s not going to fit our criteria.

“Our view is clear. A social bond should be an instrument to serve the underprivileged in society.”

‘True’ social bonds in demand

Availability of ‘true’ social bonds is contricted in a market where demand already outstrips supply.

Ackman believes issuers could do more to expand the market.

“Managers are looking for social bonds, not just because they want to bring social change, but also because there is so much demand for them, they will perform well in the secondary market,” Ackman says.

Social bond issuance is an area where supra nationals, such as the World Bank, play a large role, and semi-governments (typically state governments) can play a bigger role.

“If state governments are issuing social bonds, they need to target the underserved. Proceeds used to upgrade schools might not fit the definition, because that is just what state government do.

Find out about

Regnan Credit Impact Trust

Murray Ackman,

Sustainable Finance and

Impact Investing Director

“What’s more interesting is if the proceeds are used to provide more accessible schooling for the disabled, or new schools are built in regional and remote communities,” Ackman says.

Imapact of social bonds can be hard to track

There is also a challenge in reporting because established benchmarks might not be available.

“With green bonds you can report emissions avoided, or renewables generated, but in social bonds it can be much more bespoke. That’s fine for our purposes, though. We want to invest in projects that make meaningful change and a positive social contribution to society.”

Given the challenges in the market, and high demand, Ackman says issuers need to become more creative in how they bundle together bonds.

“We’d love to see a big bank that lends to ‘for-purpose’ organisations — those driven by a social mission, rather than profit — to pull a whole bunch of loans together and issue a social bond.

“That would benefit from a big bank credit rating, make it safer to invest in, and have a great social purpose attached. It’s happening in green bonds, and it would be good to see it in social bonds.”

“There are a lot of challenges that come with social bonds, but the demand is there.

“It is up to the issuers to meet that demand.”

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.