Significant Features: The Barrow Hanley Concentrated Global Share Fund No. 3 is an actively managed, concentrated portfolio of global shares and is diversified across a broad range of global sharemarkets.

Fund Objectives: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD over the medium to long term.

Sustainable investing options aren’t as obvious in property and infrastructure as they are in equities and fixed income. Michael Blayney explains what to look for

INVESTING in property and infrastructure in a sustainable way isn’t always as easy or obvious as buying into equities and fixed income.

Add in structural challenges amplified by the pandemic and it’s clear investors need to do their homework to find opportunities in the world of real assets.

But there are opportunities.

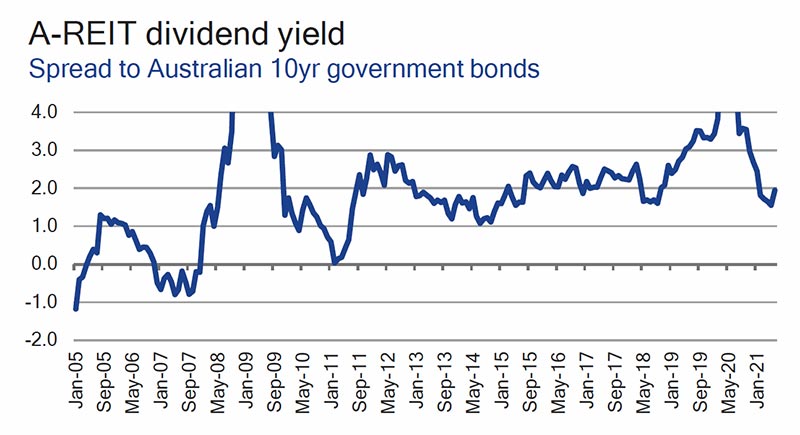

“Long term, inflation-linked cash flows are attractive, albeit with some downside risk due to REITs [Real Estate Investment Trusts] interest rate sensitivity,” says Michael Blayney, head of Pendal’s multi-asset investment team.

“They are also relatively high-yielding assets.”

Similarly, there are opportunities in infrastructure, with long-term, stable returns, particularly from assets that will benefit from the transition to a low-carbon economy.

But sorting through the options can be hard going.

In the property world it’s a challenge finding a benchmark to compare one asset with another.

“In respect of the overall opportunity set of negative exclusions for REITs, any impact is relatively less than general equities,” Blayney says.

“The most obvious exclusions are landlords of hotels or casinos. In Australia, that impacts less than 1 per cent of the A-REIT universe. Globally it can be up to 5 per cent of the universe, depending on how strictly screening criteria are applied.”

Few major portfolio construction issues are caused by explicitly excluding these sub-sectors.

“The bigger issue is the lack of dedicated sustainable product in the AREIT category,” Blayney says.

In the infrastructure world, investors can get access to some of the biggest polluters — such as utilities and assets trying to find climate solutions — and promote the transition to a low-carbon economy.

Find out about

Pendal Multi-Asset Funds

“Typical listed infrastructure portfolios are often exposed to carbon risk, because many assets are inherently linked to the use and distribution of fossil fuels — such as electric and gas utilities, some seaports, pipelines, and also airports,” Blayney says.

“Toll roads are less of an issue than airports, since decarbonising cars is already happening. But large-scale decarbonised air travel is not yet a reality.

“Digital infrastructure, such as data centres, are somewhat of a conundrum.

“On one hand greater uptake of technology can act to reduce emissions via less commuting and less business travel. On the other hand datacentres can have a significant carbon footprint due to high levels of energy consumption.

“Other assets in the digital infrastructure category — such as fibre and towers — can also make a positive contribution to decarbonisation via reduced commuting and business travel, and enabling a portfolio to leverage itself for growth in the digital economy,” Blayney says.

“Finally, within infrastructure allocations, investors have an opportunity to support clean-energy technologies while earning a strong risk-adjusted return.

“Examples include investing in renewable energy generation, in large-scale battery storage technology, and in better waste management,” he says.

How much portfolio construction in property and alternatives is influenced by ESG factors or sustainability considerations depends much more on implementation — and the subjective views of the portfolio manager making the investment decisions — rather than the hard screening of the assets themselves, says Blayney.

About Pendal’s multi-asset capabilities

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

These include Australian and international shares, property securities, fixed interest, cash investments and alternatives.

In March 2024, Perpetual Group brought together the Pendal and Perpetual multi-asset teams under the leadership of Michael O’Dea.

The newly expanded nine-strong team will manage more than $6 billion in AUM and create a platform with the scale and resources to deliver leading multi-asset solutions for clients.

Michael is a highly experienced investor with more than 23 years industry experience, including almost a decade leading the team at Perpetual.

As Portfolio Manager, Patrick co-manages our Australian smaller companies and micro-cap funds and conducts fundamental analysis on a range of smaller companies. Patrick has been part of the Smaller Companies team for a collective period of eleven years. Patrick initially joined the company in 2005 and developed his career as a highly regarded small cap analyst. Patrick worked at a small cap boutique as a portfolio manager for 3 years before re-joining Pendal’s Smaller Companies team in January 2018. Patrick holds a Bachelor of Commerce (1st class Honours) from the University of Queensland and is a CFA Charterholder.

Significant Features: The Pendal Property Investment Fund is an actively managed portfolio of primarily Australian listed property securities.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 300 A-REIT (Sector) (TR) Index over the medium to long term.

The enduring trend to digitalisation and a faster-than-expected economic recovery are two insights we can learn from strong results among European banks. Paul Wild explains

THE WORD “digitalisation” appears in more and more investor reports and conversations across asset classes and regions — including as a driver of recent European bank results.

Digitalisation refers to the use of technology “to change a business model and provide new revenue and value-producing opportunities” according to researcher Gartner.

It’s distinct from “digitisation”, which simply means converting things such as bank accounts or books from analog to digital.

We’ve noted the digitalisation trend recently in relation to Australian stocks such as Xero and PushPay.

Our emerging markets portfolio managers have also written about its role in driving businesses such as food delivery and online games.

Digitalisation of the economy was underway well before Covid. But the pandemic has accelerated adoption and looks to have raised the benchmark.

The recent run of positive results among European banks is another demonstration of how the trend is helping the bottom line for financials.

People aren’t visiting bank branches liked they used to, often because they can’t. Instead, they’re banking online, and that has big benefits for lenders, who for decades have been trying to reduce their costly branch network.

Pendal wins Fund Manager of the Year 2020

As people who bank online know, once you start, you seldom enter a branch.

“We’re seeing decent progress in the banks on the cost side, which has much to do with digitalisation,” says Paul Wild, a senior fund manager who focuses on global equities at Pendal Group’s UK-based business, J O Hambro Capital Management.

“They are going ahead with branch closures, given the Covid crisis has forced customers to move online and into mobile banking.”

European Central Bank data shows that last year the number of bank branches continued to decline across the region by an average of more than 8 per cent. The pandemic helped accelerate the trend. And the lower costs will fall to the bottom line.

Reduced provisioning suggests Europe is recovering quickly

Paul also points out that reduced provisioning among European banks has been a driver of performance this season — which indicates the European economy is recovering quickly.

“The key drivers continue to be much lower provisioning, because the economy has normalised much faster than expected,” Wild says.

“In some instances we are seeing write-backs for generic provisions. Given the economy is where it is, provisioning levels should stay low for the foreseeable future.

There also been much better fee income, he says. “Generally, for European banks fees are about one-third of total revenue and we’ve seen a very strong performance on that front,” Wild says.

Meanwhile, interest rates are starting to rise in Eastern Europe with Scandinavia set to follow.

European bank stocks look good value

Banks in Europe, like some of their peers in other parts of the world, are relatively cheap, says Paul.

“Against a market that is trading at the high end of historic valuations — and a market where again growth stocks have done surprisingly well at a time when bond yields and real interest rates are low but the economic outlook seems to be quite favourable — the banks stick out,” he says.

“At 0.75x tangible book value they are cheap on a historic basis with positive earnings momentum in the sector driving higher returns on equity, complemented by very high shareholder pay-outs to come.”

Investors should also keep an eye on September 30, when the European Central Bank will allow banks to pay dividends again, having asked them to suspend payouts during the COVID-19 crisis.

“We expect to see some very large distributions from European banks, including some very large share buybacks as well,” Wild says.

About Paul Wild and Pendal global equities strategies

Paul Wild is senior fund manager with J O Hambro Capital Management, a London-based active investment manager which is part of Pendal Group.

Pendal offers a range of global equities strategies to Australian investors including:

- Pendal Concentrated Global Share Fund

- Regnan Global Equity Impact Solutions Fund

- Pendal Global Emerging Markets Opportunities Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Oliver co-manages the Pendal income strategies with Amy Xie Patrick. He has extensive experience in macro, quant and credit research. Primarily, his role is to enhance the Income & Fixed Interest team’s quant process including development of machine learning models and big data capabilities. Prior to joining the team, Oliver spent two years in the Pendal Investment Products team, where he worked closely with both the portfolio management and distribution teams, providing quantitative support, portfolio positioning and commentary to the business and clients. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Significant Features: The Pendal Government Bond Fund is an actively managed portfolio of primarily Australian government bond securities.

Fund Objective: The Fund aims to provide a return (before fees and expenses) that exceeds the Bloomberg AusBond Govt 0+ Yr Index over a rolling 3 year period.

Environmental, social and governance factors have come to the fore in the latest ASX reporting season, says Regnan’s Alison George.

- Subtle messages are shing through profit and dividend results

- Covid, gender, environment come to the fore in ASX reporting season

- Find out more about responsible investing leader Regnan

AS THE 2021 full-year earnings season draws to a close, the story of significant profits and dividends — but cautious outlook statements — has been repeated again and again.

Iron ore miners, materials companies, many discretionary stocks and some of the financials have outlined strong performances.

Relatively few companies have failed to meet market expectations. Some four in five companies are reporting profits higher than a year earlier during peak Covid periods.

But behind the headlines another trend gained momentum this earnings season: a greater deference to environmental, social and governance factors among Australia’s biggest ASX-listed companies.

And this is likely to grab more attention in the lead-up to the annual general meeting season in coming months.

“A number of things are spurring companies,” says Alison George, head of research at responsible investing leader Regnan.

“On the social side, Covid and all its implications are being aired. For example there’s discussions about payments that some companies received from the government but didn’t really need.”

Find out about

Regnan Global Equity Impact Solutions Fund

Companies are also focusing on reports from major global bodies about climate change and the transformation needed to address it, George says.

Reporting season ends just two months before the next big global climate change conference — the United Nations Climate Change Conference in Glasgow, Scotland.

“The global gathering has focused companies on their response to climate change, the risks involved and also the opportunities,” George says.

“There’s also been a focus on diversity — and gender diversity in particular. There’s a tie with Covid, because female workers have been hardest hit,” she says.

“There’s also been more discussion about discrimination against women working on mine sites.”

The latter mostly concerns a state parliamentary inquiry in Western Australia, where major iron ore miners BHP, Rio Tinto and Fortescue Metals have made submissions pointing to the poor treatment of women. BHP outlined alleged cases of sexual assault and harassment, and said it was taking steps to better protect women.

“Fairness and equity in pay arrangements have been a feature of reporting seasons for the past couple of years,” George says. “But it’s manifested this year in issues around broader societal fairness in light of Covid challenges.”

More than most other reporting seasons ESG considerations have come to the fore. And companies that address these issues could benefit in terms of valuations.

Pendal Focus Australian Share Fund

A high-conviction equity fund with 16 years of strong performance in a range of market conditions

George points to BlueScope Steel, which this earnings season did not simply commit to a long-term net zero emissions goal — it outlined a plan to get there.

“BlueScope makes steel which is a hugely emissions-intensive activity, but is also needed for sustainable development.

“Many companies have net zero emissions aspirations, but BlueScope has backed this with detailed plans and resourcing — both financial and human. That provides investor conviction that the plans are credible.”

As earnings season ends and the annual general meeting season kicks off later in the year, companies that have provided a blueprint for achieving ESG goals will benefit.

“What we want to hear from companies is how they are positioning themselves for ‘future-Australia’, of which carbon transition is a key feature,” George says. “But its also about new technologies, changing consumer preferences and shifting demographics.”

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Significant Features: The Pendal Stable Cash Plus Fund is actively managed and aims to take advantage of investment opportunities within the Australian debt market. The Fund aims to reduce volatility of returns through limited exposure to interest rate movements and prudent credit management. The Fund invests in a combination of money market instruments, commercial paper, asset backed commercial paper and deposits with financial institutions. Securities held will have a Standard and Poor’s (or equivalent) short term credit rating of A-2 or higher.

Fund Objective: The Fund targets a return (before fees and expenses) that exceeds the RBA Cash Rate by at least 0.45% p.a. The suggested investment timeframe is 1 year or more.

With over 14 years’ industry experience, Oliver is an analyst focused on the Health Care and Utilities sectors. Starting his career with the business in 2004, Oliver has also worked with the Quantitative Services, Product and Performance and Attribution teams. He holds a Bachelor of Commerce (Finance and Financial Economics) from the University of New South Wales, where he was awarded the Australian Institute of Banking and Finance Award in his penultimate year, and is a CFA Charterholder.