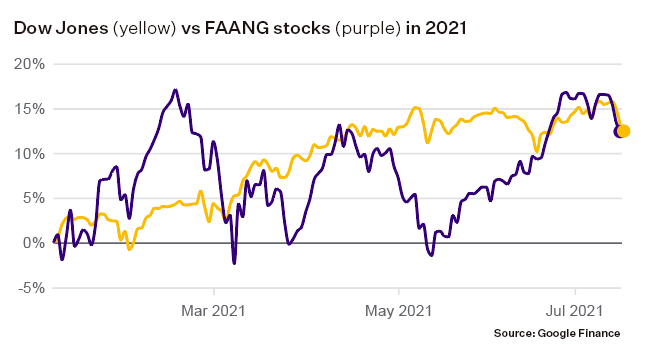

This year the Dow Jones has been keeping pace with the FAANG tech stocks — and even outperforming them. Pendal’s Ashley Pittard explains why global equities investors are looking further afield.

- Investors are looking to broaden their horizons beyond FAANG stocks.

- Inflation and wages are the critical variables.

- The world is normalising and that provides opportunities.

ASHLEY Pittard thinks the 2020s are a bit like the late 1960s and early 1970s. At least in equity market terms.

“Back then there were nice returns in equities. Inflation was increasing but it wasn’t out of control,” says Pendal’s head of global equities. “A limited number of stocks dominated the market.”

As equities appreciated in the late 1960s, and economies grew, there was a broadening out of the market, and investors looked further afield.

“The equivalent in recent years was the FAANG stocks. Everyone wanted them. But why they’ve underperformed over the last year is that growth has expanded into other areas. Commodities, for example,” Pittard says, likening the expansion to the movement beyond the “nifty 50” stocks of the late 1960s.

“What you are seeing now is that people want to own the growth stocks and rent cyclical stocks … but as the world normalises, people will be forced to own the cyclical companies.”

The big change over the past month was triggered by the US Federal Reserve.

“The Fed made it pretty clear that rates will go up and the market read that the risk of overheating had dramatically changed,” Pittard says.

It all evolves around the long-term dynamics of the market, Pittard says. Will inflation be higher over the next three to five years, than the last three to five years?

“I think it will. Interest rates are significantly lower than they have been over the past decade. Wage growth is now recovering and compounding at three to five per cent per annum,” he says. “In fact, you are seeing some fast-food companies paying up to $1,500 sign on bonuses for staff.”

“And if you look at house prices in the US, they’re at 30-year highs. House price growth is at 14.5 per cent.”

“It appears that things are getting in place for inflation to be over the Fed’s two per cent target number, and it won’t be transitory,” Pittard says.

Pittard’s fund on average only turns over 20 per cent each year. The fund managers spend time for looking for undervalued assets and waiting for them to appreciate.

“We like to buy the waterfront property when its trading at a discount and then we’ve got the patience to let things play out.”

– Ashley Pittard, Pendal’s head of global equities

Pittard gives the example of his fund increasing positions in Boeing following a series of accidents involving the 737 Max, and Airbus during the COVID crisis when airlines were on their knees.

“Today, the airlines have gotten rid of many of their old 747s, and the older pilots got axed. Now the US domestic capacity is back at 80 per cent, and recently United Airways said it wanted to buy 250 planes.”

The anecdote highlights that there are opportunities available if you are patient and can find assets that are under-valued because of the abnormal world in which we’ve been living.

“Our core tenant … is that the world is beginning to normalise. Around the world, people are starting to go out. There are fewer lockdowns and as a result people are spending more money on travel and eating out. Wage growth is getting back to normal. And that means there’s opportunities.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

- Run in markets has made many equity markets, styles and sectors expensive.

- Niche opportunities are available but beware some emerging markets.

- COVID Delta-variant and moreover future variants the big unknown.

ECONOMIC data out of Australia and many parts of the globe have been very positive for most of the past year, albeit from a low base. Equity markets have responded positively, and markets have run sharply higher.

Wall Street is up close to 40 per cent over the past year. European markets have also improved though not to the same extent. London’s FTSE is up more than 8 per cent. Germany’s DAX and the broad based STOXX Europe 600 are both around 20 per cent higher.

It’s the same story in Asian markets, with Japan’s Nikkei up 30 per cent, and markets in Hong Kong and Shanghai 20 per cent higher than a year ago. The local S&P/ASX-200 is 25 per cent higher.

“The strong growth, particularly in the employment market, has been quite remarkable,” says Michael Blayney (pictured above), head of the Multi-Assets team at Pendal. “But what you are seeing now in equity markets is that most of that good news is priced in. In fact, some are starting to look considerably expensive.”

When allocating capital, Blayney is now looking for more niche opportunities. While there’s been broad-based increases over the past year, there’s less opportunity in doing that going forward.

“We’ve had a handful of assets like Mexican equities, listed property and dividend futures in Europe. We have quite a bit of exposure to small caps as well. They are much more bespoke investments,” Blayney says. “Where our mandate allows, we’ve shifted active risk taking from outright equity exposure – and are now focused on trades linked to the reopening rotation into value opportunities.

“We’ve got this combination of good economics and good momentum. But valuations are getting a bit toppy. At this point in the cycle, we are looking at more bespoke trades and relative value opportunities.”

At this time of the cycle, emerging markets are often nominated as opportunities for asset allocation. But Blayney points out that not all opportunities in emerging markets are the same.

“If you look at China, it’s actually a bit expensive. It’s one of the few markets in the world where we’ve seen downward earnings revisions and that’s a bit unique at the moment. The Chinese economy is weakening to the extent that we may soon see an easing of policy. As a result, we are a little bit more cautious on China.

“Also, there’s structural issues to think about. China has an ageing population. People talk about demographics as benefits of emerging markets, but they aren’t always positive, especially if you look at China and Korea. For example, demographics in China have deteriorated to such an extent that the regime had to abandon its “one child policy” several years ago, which has now been replaced with a “three child policy”.

“Then there’s Taiwan. They have a lot of exposure to semi-conductors, and that’s relevant from a valuation perspective and also a geopolitical perspective. There is a very limited capacity to produce very high-end semi-conductors and Taiwan, in particular, is sitting on this very important strategic asset,” Blayney says.

“Those sorts of geopolitical risks make you think about whether there could be a major conflict between the United States and China over Taiwan,” Blayney says. “It’s that type of tail risk that current ‘priced for perfection’ valuations in many parts of financial markets globally are ignoring”

Covid case numbers are less important than you think

If you’re investing money in Australia today, the big issue on everyone’s mind is the impact of the delta variant of COVID-19 breaching quarantine and what it means for the local economy and financial markets.

Looking at overseas experiences is a good way of gaining some insight into what to expect.

“We are starting to look at some of the hospitalisation data out of the United Kingdom,” says Michael Blayney, head of the Multi-Assets Investments team at Pendal. “Looking at the rate of hospitalisations and people on ventilators will eventually be more relevant than the number of infections.

“We will need to get to the point where we can treat COVID like the flu. Naturally we will be somewhat more vigilant than we are with the flu, but vaccination is likely to be effective against preventing the most severe cases and that has massive implications for mobility and people’s ability to go out and spend which flows through optimism in financial markets,” Blayney says.

The UK and Israel, which both have high vaccination rates and are experiencing surges in the delta variant of COVID-19, are good case studies, Blayney says.

“If we start to see hospitalisation rates going up, and an escalation in more serious cases, then that will have a very negative impact on risk sentiment, though so far, so good. Conversely getting to herd immunity can provide a significant tailwind to many parts of the market that have lagged due to COVID.”

About Michael Blayney and Pendal’s Multi-Asset capabilities

Michael Blayney leads Pendal’s multi-asset team. Michael has more than 20 years of investment management and consulting experience. He was previously Head of Investment Strategy at First State Super and head of Diversified Strategies at Perpetual.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The team — which also includes Stuart Eliot and Allan Polley — manages our multi-asset portfolios with a focus on strategic asset allocation, active management and tactical asset allocation.

* The Pendal Defensive Equity Income Fund closed to applications and reinvestments effective 7 June 2018 and will terminate effective 17 July 2018, with the assets liquidated and the net proceeds returned to investors. More information.

Significant Features: The Pendal Defensive Equity Income Fund aims to provide a consistent monthly income to investors.

Fund Objective: The Fund aims to provide a consistent monthly income plus franking credits; a total return (including franking credits and after fees, costs and taxes) that exceeds the benchmark over rolling 3-year periods; and reduced exposure to the S&P/ASX 200 Index.

- European bourses have long been seen as less attractive equity markets

- Led by banks, many stocks in the region now look undervalued.

- Growth in Europe expected to continue way above trend until beyond 2023.

IT’S BEEN a while since Europe excited global equity investors. For most of the past few decades, there’s always been something a little more exciting – the US, emerging economies, private markets.

But as the world emerges from the COVID pandemic, there’s a whiff of excitement about European equities. And that provides opportunity.

“In my world – continental Europe – earnings forecasts still look very much too low,” says Paul Wild, senior fund manager at JOHCM Global & International Equities. With second quarter earnings season only a fortnight away, Wild expects continued surprises vis-à-vis a year earlier.

“While it’s clear that peak earnings momentum has past, it is still going to remain positive. We could see earnings growth approaching 50 per cent for 2021. Also with European GDP in 2022 likely higher than this year, the earnings outlook stays strong”

Banks and financial companies, like most major markets, are a large part of European equities. But they are behaving atypically at the moment, and that could provide an opportunity.

“The story of European financials is not really yield curve driven at the moment. It’s more about the effects of coming out of the crisis, and that’s about normalising provisions,” Wild says.

Banks increased provisions for bad debts at the beginning of the pandemic, but as the macro environment turned out to be better than forecast, provisioning requirements have fallen. The banks are over-capitalised, Wild says, and that means big dividend payouts later in the year.

2021 Money Management of the Year Awards

Pendal Australian Shares Portfolio

Winner – SMA Australian Equities

Pendal Property Investment Fund

Winner – Australian Property Securities

The other factor for European (and global) banks is inflation.

“The commentary from the Fed a few weeks ago is far and away the key event of recent times,” Wild says. “The market was very much positioned … for the Fed to let things run hot. But the Fed’s dot plot effectively called for two rate hikes in 2023 – they were much more hawkish than what the market was positioned for. The yield curve flattened.”

The question is: has the market interpreted the Fed correctly?

“It’s very difficult for anyone to make a real call on inflation with absolute convictions at the moment given the transitory effects, given past mistakes it seems unlikely the Fed will be too pre-emptive” Wild says.

“Overall global valuations are pretty high at the moment, but Europe looks quite reasonable versus the MSCI World. Whilst bonds are still priced for the moon,” he says.

“If you buy a Government bond, in many cases you are committing yourself to a negative real return. So, then you look at equities and the cash dividend potential, particularly in Europe. It looks like growth in the region can stay sustainably strong until the back of 2023,” Wild says.

“For so long Europe has just been lacking in any positive theme, and that’s now changed as it emerges stronger from the pandemic.”

About Paul Wild and Pendal global equities strategies

Paul Wild is senior fund manager with J O Hambro Capital Management, a London-based active investment manager which is part of Pendal Group.

Pendal offers a range of global equities strategies to Australian investors including:

- Pendal Concentrated Global Share Fund

- Regnan Global Equity Impact Solutions Fund

- Pendal Global Emerging Markets Opportunities Fund