- Retailers are resetting business models, adapting to online shopping

- E-gaming, gyms and childcare to boost shopping malls

- Property investors should take a closer look at the once-maligned sector

A SURPRISING resurgence in retailing is underway in the real estate industry as shopping malls reset around food and entertainment, fending off the threat of online vendors.

E-sports computer gaming, gyms, childcare centres and even car dealerships are driving a renaissance at shopping malls, which are emerging strongly from 18 months of pandemic restrictions and lockdowns.

Pendal’s Julia Forrest, a portfolio manager specialising in property for the Australian equities team, says during the reset forced on the sector by COVID-19 retailers closed unprofitable stores and optimised staffing levels.

It also forced landlords to the negotiating table to reset rents at lower but more sustainable levels for the long term.

“The retail sector is probably in a better position now than it was at the beginning of 2020,” says Forrest.

Amid further lockdowns across the country and the threat of a resurgence of the pandemic, the strong outlook for retail is an important and unheralded theme for portfolio construction.

Before the pandemic, the retail sector was under pressure. Sales growth was falling, shops were cutting shifts, discounting was on the rise and some retailers were closing or going into administration.

“We went into 2020 expecting rents to fall but for completely different reasons than COVID,” says Forrest.

“But the rental reset in 2020 was somewhere between 12 and 15 per cent lower.”

“You can be more certain about the cash flows with retailers going forward.”

Julia Forrest

The lower rents, coupled with government subsidies for wages, the closure of less profitable stores, higher productivity as staffing levels were reset and a move to online and omni-channel retailing, has put the sector in a better position than many expected.

At the same time, strong demand for other property assets like office and industrial has improved the relative attractiveness of malls for investors.

“You can be more certain about the cash flows with retailers going forward.”

Omni-channel approach

Forrest says shopping malls are adapting well to the threat of online shopping, moving to an omni-channel approach and lifting the experiences available at a mall.

“There’s e-gaming that has opened in one of the centres in Victoria that’s drawing in young teenage boys, which isn’t the typical target market for malls.

“They are adding childcare centres to the periphery. They’re starting to add car dealerships and things like car care and parts – the kind of thing that you’ve seen in the bulky goods category or large format retail are now moving into malls.”

Forrest says investors should keep an eye on the big asset sales in the pipeline to gauge how valuations are changing.

“The AMP assets, Pacific Fair and Macquarie Centre will probably trade, and they’ll probably trade close to book value.

“That’s a reflection of capital seeking best quality assets with good locations and optionality from repurposing.”

About Julia Forrest and Pendal Property Securities Fund

Julia has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

SYDNEY’S LOCKDOWN dominated local news last week, but the S&P/ASX 300 fell only 0.5%.

The takeover bid for Sydney Airport (SYD) reminded us of the abundant liquidity — and propensity among long-term investors to look through Covid-related earnings issues, supporting market sentiment.

At a global macro level we saw bonds rally for the first four days of last week. This reinforces the narrative that we are through peak growth and the delta variant is exacerbating a global slowdown.

Sentiment reversed on Friday, perhaps suggesting that sentiment had turned too negative. We expect more sentiment swings through the northern summer as we wait for data on the economy and the effect of the Delta variant.

There are signs of a potential stimulatory shift in Chinese policy. This could be a positive development that supports resources in coming months.

Outlook for Covid and vaccines

The Sydney outbreak has taken a turn for the worse, breaking containment lines. We are now looking at a far longer period of restrictions.

While Covid remains contained to Greater Sydney the economic impact will be material, though not severe for the broader domestic economy.

Growth in new case numbers is tracking worse than Victoria’s second wave last year. On the plus side tightened lockdown measures, higher testing numbers and the ability of contact tracers to identify exposure sites should help. But the higher transmissibility of the Delta variant is an offsetting factor.

The Delta variant is now dominant in the US, prompting further scrutiny. At this point it appears cases will start to rise materially. The key variable is what this means for hospitalisations. Until we have greater visibility the market may continue to worry about the potential for restrictions to return.

The UK continues to run the gauntlet on new cases. So far a surge in infections has not translated into hospitalisations.

There is a growing debate about the effectiveness of vaccines and the need for boosters. Early studies on Delta indicated the mRNA vaccines were very effective — well into the 80% range in preventing Covid.

But data from Israel is concerning. It indicates the effectiveness of Pfizer in preventing Delta infections is in the mid-60% range. This is from a larger sample set than previous studies.

This could be due to the fact that Israelis had their injections four-to-five months earlier, which may suggest waning immunity and a lower efficacy in preventing infection.

The vaccines are still highly effective against severe infections. But this shows why a debate over the need for booster shots is gaining impetus.

Economic outlook

We have had a series of weaker data points for the first time in months. US unemployment, PMI data, unemployment claims and vehicle sales have all softened and money supply growth has slowed.

Much of this can be explained by holidays, shortages of certain products or labour and some hot weather. But it is a trend that needs to be watched. Along with the increasing prevalence of the Delta strain this has triggered a further flattening of the yield curve on concerns for near-term economic growth.

We need to bear in mind the link between market price action and policy.

There is a view that if inflation and growth expectations soften sufficiently – and the yield curve flattens below 100bps – we could see the Fed delay tapering. This moderating factor suggests we may be near the end of the recent rally in bonds, although a move higher is unlikely in the next few months.

In China the State Council signalled a shift in policy to be more supportive of growth. A cut in the reserve requirement ratio (RRR) for banks followed, which can help credit growth.

This is most likely in response to weak consumption. But China faces a similar challenge to Australia: low levels of immunity and a reliance on vaccines that may have limited effectiveness against the Delta strain. This could force the Chinese to maintain restrictions for longer.

Beijing’s move to prop up growth via traditional investment-related stimulus would be supportive of commodities.

Meanwhile the European Central Bank announced its policy framework.

The ECB is taking a less activist approach to inflation than the Fed. They will tolerate an overshoot of inflation targets, but won’t actively try to generate inflation. The wash-out is no real shift in Europe’s more conservative approach.

Markets

Bond yields fell for much of last week on concerns over the economic outlook, before reversing on Friday.

As a result the US 10-year Treasury yield fell only 6 bps to 1.36%. The Australian equivalent fell 12 bps to end at the same yield.

Brent crude fell 2.7% despite the lack of a deal between OPEC and its partners on increasing supply. Concerns over growth — coupled with speculation that OPEC’s cohesion may be waning — are probably at play.

Most sectors in the S&P/ASX 300 fell last week, though the index was propped up by the bid for Sydney Airport (SYD, +33.4%). Otherwise there was a relatively small spread across sectors, with growth lagging after a good run.

The bid for SYD by a consortium of pension funds was last week’s big news. The offer of $8.25 per share was a 40% premium. It values the stock at 25x EBITDA based on post-Covid FY23 earnings, versus a historical trading range of 18-21x.

This represents an enterprise value of $30 billion versus the previous peak of $29 billion. We see this as a very competitive bid in the wake of an uncertain rate of recovery in international travel and the impact of the Western Sydney Airport. There may be a higher offer to follow, but the increase is likely to be small. The bid is conditional on board approval and Unisuper agreeing to roll its 15% holding into the venture.

Tabcorp (TAH, -8.1%) announced a plan to demerge its Lotteries and Keno business by June 2022, effectively rejecting offers for its wagering business. The stock’s fall reflects the high cost of the demerger – a $225 million to $275 million one-off and $40 million ongoing.

Crown (CW, -7.8%) delivered a market update that was softer than expected. Market attention remains fixed on the Victorian Royal Commission, which has now ended and will report in October. The risk of losing its licence – as well as the potential impact on revenue from upgraded compliance procedures – will have an impact on valuations from potential bidders.

Ramsay Health Care (RHC, +0.7%) raised its bid for UK-listed private hospital group Spire. This is unlikely to change the minds of big shareholders who hold a blocking stake to prevent the deal. This leaves the company back where it started, but in a bit of strategic bind, which is reflected in the price.

A2 Milk (A2M, +10.4%) has rebounded on signs of an improvement in volume and pricing in China’s infant formula market. We remain wary. China’s low birth-rate will likely result in lower demand, while local providers continue to gain market share.

Viva Energy (VEA, +5.9%) delivered a well-received update. EBITDA was well ahead of consensus and the non-refining business is back to its previous peak profit level, despite a decline in the aviation business. This demonstrates the industry structure is helping support margins, while the company is also controlling costs. Government moves to protect refining have also removed a great deal of uncertainty.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

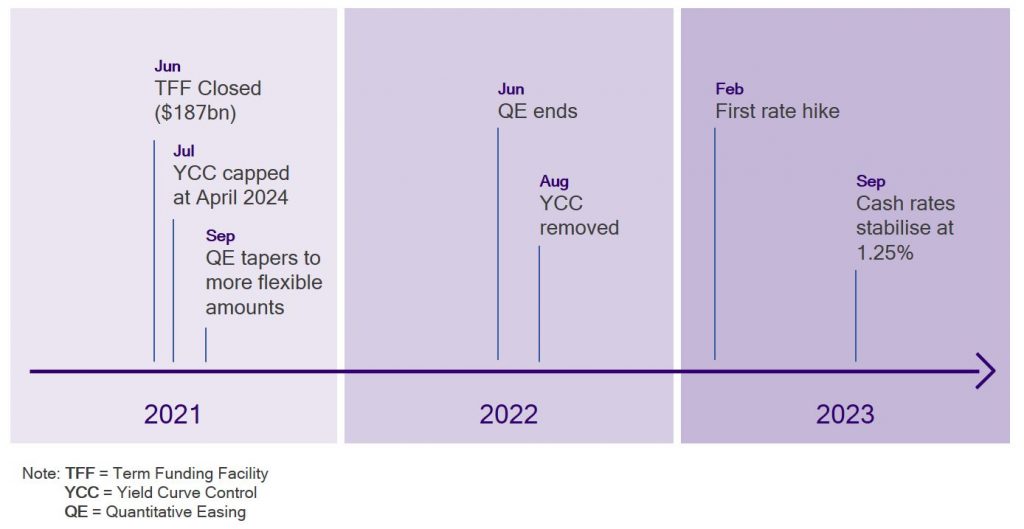

THE RESERVE BANK last week started the slow unwind of extraordinary monetary policy.

In recognition of the overall stronger economy, Yield Curve Control will not extend beyond the current April 2024 bond.

When the current $100 billion of Quantitative Easing (QE) ends in September, the pace will fall from $5 billion a week to $4 billion a week. It will be reviewed again in November.

Together with the closing of new borrowing from the Term Funding Facility (in total $187 billion lent) this represents the first steps back toward conventional monetary policy.

In our view the timeline looks something like this:

QE will likely taper further once the US Fed starts its own taper later this year.

The end of QE is probably brought forward by recent AUD weakness, relieving RBA concerns that higher rates here would push the AUD above 80c.

Of course there are a number of clear criteria laid out by the RBA to actually hike cash rates.

Inflation must be sustainably within the 2-3% band. For that to happen they believe wages need to be at least 3%, which in turn requires full employment.

The view is full employment is nearer 4% than 5%. We wrote extensively about employment and wages in our last newsletter. (Contact a Pendal key account manager for a PDF copy).

Given our views on inflation and wages we expect rates to lift-off in the first half of 2023. We expect them to stop around 1.25% to 1.5% before staying there for some time.

Of course this is a view into the future. In a week dominated by lockdowns and US bond rallies, bond markets here saw lower yields.

There is a lot more to play out in US employment markets in the months ahead.

Unlike Australia where jobs are now higher than before Covid, the US still has 8.5 million jobs “missing”.

The bulls blame higher welfare payments discouraging people from returning to low-paying jobs. The bears suggest COVID has shown the way for businesses to permanently operate with fewer staff.

The truth is likely a bit of both.

How this plays out in the months ahead will set the tone for bonds markets and eventually equity markets.

We will dive deeper into this topic in the weeks ahead.

About Tim Hext

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

China’s authorities are re-examining rules around Chinese companies listing outside the country’s stock exchanges. Samir Mehta (pictured) – portfolio manager of Pendal Asian Share Fund – explains what it means for investors

CHINA is reviewing the rules that govern its companies listing on foreign stock exhanges. What does this mean for investors?

Before we consider this, it’s useful to understand three cross-currents affecting Chinese technology businesses and stocks:

1. Regime change under President Xi

The Chinese leader has articulated more forcefully than most that the Chinese Communist Party (CCP) is supreme. Jack Ma found this out to his detriment when he made a speech in which he was critical of regulators. It is acknowledged off the record by people in the know that a large shareholding in Ant Financial is owned by the Shanghai faction (those considered close to ex-President Jiang Zemin – a political rival of the current administration).

2. A clear ideological battle-line drawn under President Trump’s administration in 2018

I do not think this is a clear-cut ideological contest between capitalism (the US) and communism (China). The CCP is a Marxist-Leninist party which uses the tools of capitalism effectively. This ideological divide is more about superpower rivalry, and we happen to have a label attached to it.

3. Data is the real source of the current predicament for governments

The collection, use and security of data are now arranged around national boundaries. Any industry considered a national priority or subject to national security is now wrapped in data nationalism. Accounting oversight for US-listed securities (rightfully demanded by US Congress through the Public Company Accounting Oversight Board) flies in the face of data nationalism.

China reviews foreign listing rules

Chinese authorities are currently re-examining rules around listing outside China’s stock exchanges.

“Once amended, the rules would require firm structures using the Variable Interest Company (VIE) model to seek approval before going public in Hong Kong or the US,” Bloomberg reported recently.

The VIE model was pioneered by Chinese Internet company Sina Corporation in 2001 as a means to list its shares on the New York Stock Exchange in 2001. It set the stage for a flood of IPOs and capital raisings by Chinese companies in US capital markets.

Scroll down for an explanation of the VIE model.

Since 2018 I have considered any Chinese ADRs as risky for exactly this eventuality.

Hence, in the past two-and-a-half years, I have chosen to own stocks listed either on the Hong Kong or the Shanghai/Shenzhen stock exchanges.

I have a large underweight position in China, partly due to valuations, partly because of increased regulatory risks and partly on account of the tightening macro environment.

Following recent events I have to wait and judge whether Hong Kong-listed firms are likely to be dealt with as heavy-handedly as any US-listed Chinese stocks.

Rationally speaking that should not be the case. The Chinese mainland now completely controls Hong Kong – but geopolitics and national security concerns can trump rationality.

The other big risk revolves around data and business models.

In the US technology behemoths operate in loosely defined spheres of influence (Facebook vs Amazon vs Microsoft vs Google). That is not the case in China.

Every large company and upstart challenger wants to encroach upon and compete against incumbents, using not just data but aggressive cash burn and sometimes harsh competitive tactics (monopolising users or suppliers via threats).

Moats matter

This requires a return to first principles – to understand what is the genuine competitive moat for a business.

And we need to analyse whether that moat is now threatened by Chinese government’s imposition of national security priorities. This is not going to be easy.

My fortune in positioning the portfolio with a large underweight in China allows me some breathing space. Markets by definition are fickle and move from euphoria to panic, as we currently observe.

I welcome that wholeheartedly. Consternation concentrates the mind.

Learn more: what is a Variable Interest Company (VIE)?

China’s Sina Corporation pioneered the concept of the Variable Interest Company (VIE) as a means to list its shares on the New York Stock Exchange.

The first Chinese internet company to do so in 2001, Sina set the stage for a flood of IPOs and capital raisings by Chinese companies from US capital markets.

It was an ingenious legal “contract”.

“It enabled Chinese companies to sidestep restrictions on foreign investment in sensitive sectors including the Internet industry,” Bloomberg columnist Matt Levine commented earlier this month.

“The structure allows a Chinese firm to transfer profits to an offshore entity – registered in places like the Cayman Islands or the British Virgin Islands – with shares that foreign investors can then own.”

Those were the heady days of globalisation, marked by China’s entry into the World Trade Organization (WTO). The internet was in its infancy while Asian economies were struggling from the aftermath of the financial crisis of 1997-98.

As that decade progressed, one catchphrase became increasingly popular: “economic decoupling”.

Most economic forecasters and market participants (myself included) hoped for or predicted the imminent cutting of the umbilical cord that joined Asia to the West. That moment of decoupling is upon us, although the contours are vastly different from what we envisaged.

Churchill’s characterisation of the Soviet Union in October 1939 as “a riddle wrapped in a mystery inside an enigma” is an apt description of the VIE structure.

Again quoting Matt Levine at Bloomberg (everyone should read his work):

“I have a soft spot for Chinese VIEs. The idea is that, under Chinese law, it is somewhere between “complicated” and “forbidden” for foreigners to own certain big important Chinese tech companies. This is a problem for those companies if they want to raise capital from foreign investors and list their stocks on foreign stock exchanges. But there is a solution. Ownership of a company is a complicated notion, a vague jumble of rights to elect directors, approve mergers, and claim a residual interest in the company’s cash flows. You could break those things up and sell them separately.

“Write a profit-sharing contract that says: ‘A will pay B all of A’s profits after expenses for the next 100 years, renewable at B’s option,’ and hey that’s a residual claim on cash flows. (Or something more vague: ‘A will pay B an annual consulting fee that B decides in its total discretion based on the economic value of the relationship,’ etc. Not technically a residual claim but what else is it?). ‘B will provide management services to A and A will follow B’s instructions,” hey that’s basically control. ‘B will have the right to appoint a majority of A’s board of directors,’ put it in a contract, it’s not actually stock ownership. Etc. Write some contracts that, bundled together, look like ownership, but aren’t ownership.

“With Chinese companies, this sort of thing is generally called a ‘variable interest entity’. You set up a company in the Cayman Islands that can be owned by anyone. The Caymans company enters into a series of contracts with the local Chinese company, giving it, not ownership, but certain carefully curated economic interests and control rights over the Chinese company. Then you list the Caymans company in the US, and people buy its stock, and they sort of pretend that they’re buying stock in the Chinese company — they sort of pretend that the Chinese company is a subsidiary of the Caymans holding company — even though really they’re only buying an empty shell that has certain contractual relationships with the Chinese company.”

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Pendal’s Sustainable Australian Fixed Interest Fund invests in social bonds that help vulnerable Australians while also aiming to generate strong returns. This is the story of a family helped by Hume Community Housing, which is partly financed by those social bonds.

There are few things as devastating as a marriage breakdown.

When a parent with three children suddenly becomes single and homeless it can seem like an impossible situation.

Things were grim for Samuel and his family when they found themselves homeless. In desperation, they were forced to live on an overcrowded property with his parents.

Samuel had grown up in social housing and overcome many challenges. Now circumstances threatened to pass on generational disadvantage to his children.

Fortunately, he was put in touch with Hume Community Housing via Uniting’s Doorways for Men with Families program.

Hume is a Community Housing Provider (CHP) which develops affordable housing for low-income Australians with help from investors in Pendal’s Sustainable Australian Fixed Interest Fund.

Hume’s funding comes partly from the federal government’s National Housing Finance and Investment Corporation (NHFIC), which raises money by issuing social bonds to investors such as Pendal.

NHFIC lends out the money raised (more than $2 billion so far) to CHPs at low interest rates and on better terms than banks — while providing attractive returns to investors.

Cheaper financing means CHPs such as Hume can help more people like Samuel and his family.

Lives turned around

Hume runs a housing independence program that helps people like Samuel transition from homelessness to longer stable accommodation.

Hume provided housing to Samuel and his family at a low cost, allowing the single dad to provide for his family and build up a solid tenancy record.

This turned Samuel’s life around – as well as that of his children.

“Hume were incredible,” says Samuel. “They always called in to see me. They cared.”

After an initial meeting Hume quickly sprang into action.

Three days later they phoned and asked Sam to visit one of their locations in Claymore in south-western Sydney.

He accepted the place on the spot.

Samuel began building ties in his new community by fixing bikes for local children.

Soon the whole neighbourhood could watch their kids race their bikes on the street.

“I got all the bikes off the rubbish piles and fixed them up. Every kid in our street had a bike by the end of it and they were all happy.

“Somebody was throwing out a lawn mower, so I fixed it and before long everybody in the street was using it. We interacted more as a community and we became friends. Even men in the street stepped in to support one another if they needed it.”

Help from Hume

Helping with the transition was Hume’s Housing Independence Officer Sedina, who worked closely with Samuel, connecting him to support services and ensuring his family’s wellbeing.

Sedina went above and beyond the call of compassion. At Christmas time Hume told him when the local church was giving out presents for the kids.

“When Sedina would come into the street, even if she was speaking to someone else on the street, she’d get out of the car and talk with the children and say hello and ask if there was anything that needed to be done to the house and if we needed anything,” says Samuel.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Hume is part of the thriving Community Housing Provider (CHP) sector which manages more than 35,000 properties in NSW alone.

With help from funding from the National Housing Finance and Investment Corporation, Hume aims to help Australia’s diverse community maintain their tenancies, break the cycle of disadvantage, participate in life, and to reach their full potential.

“NHFIC is very important for financing, because it’s possibly as low a cost for borrowing you could ever achieve,” says Wendy Hayhurst, chief executive of the Community Housing Industry Association.

“And it’s performed very well because it’s got a government guarantee.”

In Samuel’s case it’s been a resounding success. After five months on the Hume program and with a stable rental record, Samuel and his family secured a private rental tenancy closer to his extended family.

You can see the joy on his children’s faces as they play on the swings, knowing they are on the path to a brighter, more secure future.

“To be honest, I was stuffed before coming to Hume,” says Samuel.

“My kids are happy and settled and we’re doing more family-oriented stuff now. Hume helped me to get my life back.”

Pendal thanks Hume Community Housing for their co-operation in producing this article. Hume is a Community Housing Provider with more than 30 years experience in providing homes and services to more than 9000 customers in NSW. For more information go to www.humehousing.com.au.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Alex is responsible for credit research coverage of Infrastructure, Utilities, and Financials.

Before joining the team, Alex spent seven years as a Primary Analyst at S&P Global Ratings, focusing on infrastructure, utilities, and general corporate issuers in Australia and New Zealand.

Prior to his role at S&P, Alex worked for three years as a Senior Analyst in the Audit Division at Deloitte Australia.

He holds a Master of Philosophy in Economic History from the University of Oxford and a Bachelor of Commerce from Monash University.

Alex is also a CFA Charterholder.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS CONTINUE to grind higher, though breadth is narrowing and technical signals suggest we could be in for a period of consolidation.

Last week the S&P/ASX 300 gained 0.14% and the S&P 500 1.71%.

At this point the market continues to look through domestic lockdowns. Domestic cyclicals held up last week, while growth stocks took a breather from their recent run.

US payroll data was reasonable, but did nothing to change expectations on central bank tapering. OPEC’s latest meeting on output policy will stretch into this week, while oil prices continued to rise.

Covid and vaccines

Case numbers in the Sydney cluster are rising faster than the previous Avalon and Crossroads outbreaks. The good news is testing is also much higher — so the overall ratio of cases to tests is likely to be much closer to previous outbreaks.

At this point lockdowns and effective contact tracing suggest this outbreak should be containable within weeks rather than months. This is certainly the view reflected in markets.

Other parts of the world are re-opening, prompting a debate about our path to normalisation. At some point there will need to be a leap of faith allowing a degree of Covid in the community on the premise that it won’t lead to poor health outcomes.

The maths around target immunity levels for domestic re-opening is a function of variant transmissibility, vaccine effectiveness and vaccine penetration.

The Delta variant’s greater infection rate has raised the required threshold of immunity. The shift to greater use of Pfizer should help. We may see an acceleration in the timing of second doses.

We suspect the trigger may be availability of vaccine for anyone who wants it, rather than a specified proportion of the population vaccinated. But this is unlikely to arrive before the fourth quarter of 2021. A full re-opening of international borders is likely to be delayed beyond this.

We continue to watch the UK carefully as a possible test case, where new case numbers continue to climb sharply, but hospitalisations remains subdued.

Economics and policy

June payrolls came in stronger than consensus at the headline level in the US with 850,000 new jobs added. But the overall picture was mixed.

Hours worked dropped marginally while the unemployment rate rose a touch to 5.9%. The overall participation rate remains low at 61.6%.

The key outcome was no shift in sentiment towards the timing of Quantitative Easing (QE) tapering or rate hikes.

There are still 5.5 million fewer jobs than before Covid (about 40% of which are in leisure and hospitality). The paradox? While a lot fewer people are employed, there are clearly bottlenecks in labour supply which are creating wage pressures.

How material this is — and how permanent — will be tied to the participation rate. This is unlikely to be resolved until we get into the fourth quarter of 2021. By then all unemployment insurance payments will have expired and parents will be able to send their kids to school.

Until then the employment data is unlikely to bring forward tightening expectations.

Inflation outlook

Debate on inflation remains the key macro issue.

We are tracking several bottlenecks in this regard. Some logistical issues appear to be the worst they have been since 1974. Analysis by Goldman Sachs on the temporary factors driving inflation suggests they peaked in May at 1.05% incremental inflation and should halve by November.

This means that even if the inflation thesis is correct, it will be hard to detect in the next few months. Combined with ongoing QE, this could keep bonds range-bound and prevent any dramatic rotation back to value in the equity market.

That doesn’t mean we are not creating seeds for higher inflation in the medium term. Last week’s data on US house prices — which are growing at their fastest rate in 30 years — is a reminder of the wealth effects created by current policies.

Markets and stocks

US holiday season has generally seen quieter markets.

Last week US 10-year Treasury yields fell 10 bps to 1.43%, while their Australian equivalent fell 9 bps to 1.48%. The US Dollar index strengthened 0.4%.

Brent Crude rose 1.5% to US$75.16. We are waiting to see if OPEC agrees to raise production to help offset the rebound in demand. The UAE is withholding agreement at this point, arguing for a greater share of production.

Inroads made into global oil inventories are worth bearing in mind. They peaked at about 1200 million barrels in December 2019, fell to about 330 million barrels on a rebound in demand and are now falling 50-60 million barrels per month. Additional supply will be needed to ensure a smooth run-down of inventories as Europe and the US continue to re-open.

This is supportive for an oil price remaining in the US$70-80 range — and perhaps even nudging above it.

The Australian market’s FY21 return was the highest since 1992.

It was driven by a rebound in earnings, with the valuation multiple effect actually contracting over the year. Deeper cyclicals such as steel, building materials and gaming performed best given their high operating leverage. Defensives such as infrastructure, utilities and gold miners fared worst.

It is interesting to note the material de-rating of metals and energy sectors despite very strong pricing fundamentals and earnings momentum. Energy stocks, in particular, have not performed on a rising oil price.

The disconnection here is probably tied to a view around the sustainability of economic growth and the increasing impact of Environmental, Social and Governance (ESG) issues on the cost of capital.

ASX highlights

Last week AGL Energy (AGL -9.8%) was the worst performer in the ASX 100 after announcing details of its demerger. The plan is to split into a company that holds the “dirty” assets (Accel) and a “clean” company (new AGL).

AGL appears to be using the latter to raise capital and give Accel a stake to act as collateral for refinanced debt. Management also highlighted more headwinds to near-term earnings from wholesale gas costs and low electricity prices. EBITDA was set to drop more than 20% in FY21 ahead of another material step down in F22.

We continue to see the stock as a value trap given the overhang of a capital raise, the overlay of regulatory risk, and the ongoing issue of low electricity prices.

Lendlease (LLC, -7.1%) delivered another downgrade. Lockdowns in the UK and elsewhere disrupted development projects and there was a lack of clarity around the company’s current strategy.

Nine Entertainment (NEC, -3.7%) fell after gaining the rights to the UEFA Champions League European football competition for its Stan Sport service. The market was quick to factor in cost without any offsetting benefits. Nine is continuing to see strong advertising demand — so far unaffected by the recent lockdown.

IDP Education (IEL, +17.8%) was the best performer following its acquisition of British Council’s Indian operation for $238 million. This leaves IDP as the only administrator of British Council’s English language tests in India. It’s the biggest market for these services, growing about 20% per annum pre-Covid. The deal is expected to be 13% accretive since it’s financed from the balance sheet rather than capital raising, with scope for additional synergies.

Metcash (MTS, +7.8%) delivered a well-received result. The supermarket business was a mild disappointment since operating leverage was not as high as expected. But it appears to be holding onto gains in market share. This was offset by strength in hardware and liquor, which combined are now a greater share of earnings than the supermarket business. Management announced a share buyback, surprising the market and signalling confidence in the outlook.

Telstra (TLS, +5.6%) rose as it announced the sale of a 49% stake in its mobile tower division to a consortium of super funds. The price was a substantial premium to overall group valuation multiple and above market expectations. This reflects strong demand for less economically-sensitive infrastructure assets. Roughly half the proceeds will be returned to shareholders.