The Pendal Monthly Income Plus Fund’s September 2022 distribution will be paid on or around 26 September for the period ending 20 September 2022.

The change is being made for operational reasons and will be for September 2022 only.

We anticipate the early payment of the September distribution will not impact the size of the distribution that would normally be paid.

Investors will still receive distribution statements in accordance with our usual process.

Please call our Investor Services support line on 1300 346 821 if you have any questions.

Pendal Dynamic Income Fund (APIR: BTA8657AU, ARSN: 622 750 734)

Pendal Enhanced Credit Fund (APIR: RFA0100AU, ARSN: 089 937 815)

Pendal Fixed Interest Fund (APIR: RFA0813AU, ARSN: 089 939 542)

Pendal Monthly Income Plus Fund (APIR: BTA0318AU, ARSN: 137 707 996)

Pendal Sustainable Australian Fixed Interest Fund (APIR: BTA0507AU, ARSN: 612 664 730)

Regnan Credit Impact Trust (APIR: PDL5969AU, ARSN: 638 304 220)

Effective 1 July 2021, the buy/sell spread for the following funds will change as set out in the table below:

| FUND NAME | OLD | NEW |

| Pendal Dynamic Income Fund | 0.30% (0.07%/0.23%) | 0.24% (0.12%/0.12%) |

| Pendal Enhanced Credit Fund | 0.30% (0.07%/0.23%) | 0.18% (0.09%/0.09%) |

| Pendal Fixed Interest Fund | 0.16% (0.06%/0.10%) | 0.12% (0.06%/0.06%) |

| Pendal Monthly Income Plus Fund | 0.27% (0.07%/0.20%) | 0.20% (0.10%/0.10%) |

| Pendal Sustainable Australian Fixed Interest Fund | 0.14% (0.05%/0.09%) | 0.14% (0.07%/0.07%) |

| Regnan Credit Impact Trust | 0.20% (0.06%/0.14%) | 0.20% (0.10%/0.10%) |

The buy/sell spread is an additional cost to you and is generally incurred whenever you invest in or withdraw from a Fund. The buy/sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy/sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy/sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Funds.

Pendal will continue to monitor market conditions and review and update the buy/sell spread regularly as required. You should therefore review the current buy/sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy/sell spread for each Fund.

In-depth insight from Pendal’s Head of Bond, Income and Defensive Strategies, Vimal Gor (pictured).

FULL EMPLOYMENT is once again front and centre in government policy. But what exactly is full employment and where do we stand in Australia?

These are probably the most crucial questions for our economy.

In his latest newsletter Pendal’s Vimal Gor explains how issues concerning full employment are affecting investment decision making in Australia.

As always with economics there are no precise answers. But an understanding of the road signs is critical to anticipating the future path of monetary policy.

To continue reading, download Vimal’s latest Bond, Income & Defensive Strategies newsletter. (PDF)

About Vimal Gor and Pendal’s Bond, Income and Defensive Strategies (BIDS) boutique

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, Vimal oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Vimal sets the strategy, processes and risk management for the boutique and all funds managed within it.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is an independent, global investment management business focused on delivering superior returns for our clients through active management.

Contact a Pendal key account manager here

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

WHILE the NSW victory in the NRL State of Origin was impressive last weekend, another important interstate contest is now underway — the state budget updates.

We’ve had two states come in with their 2021-22 budgets in the past week — NSW and South Australia.

State budgets do matter to investment managers. But before we look at what they mean, it’s important to remind ourselves on one crucial and massive difference between the states and the federal government: the states do not have a printing press.

They cannot simply print money to meet a repayment. They must first earn or borrow money before spending it.

The federal government (thru the Reserve Bank) can simply create money with a keystroke. The only reason they tax is to drain money they have spent from the system, with the aim of limiting inflation.

This creates very different dynamics when building a budget for a state versus the federal government.

States should aim to run balanced operating budgets through the cycle. Like all of us they must “live within their means”.

For the federal government the notion of a balanced budget is irrelevant. The only question they should ask is: does the budget help produce full employment without inflation being too high? If this means creating and spending more money than is drained through taxes (a budget deficit), then so be it.

The budget position is merely an accounting result of attempting to strengthen the economy — or if inflation is too high, slow it down.

Therefore the federal government is to be applauded for finally catching on that they need to keep spending despite an improving economy — as they did in the recent budget. We are not yet at full employment and we do not have an inflation problem, so why would you stop?

The states in Australia are primarily public service providers – health, education, police and so forth. No income or company taxes and no (or few) welfare payments.

These services are less dependent on economic cycles, so the tax and spending base of states should also be less dependent on economic cycles. That’s one of the reasons taxes such as stamp duty and payroll are inefficient, while a land tax and GST are preferable. (Good luck with the politics though.)

Recent operating budgets are improving, but borrowing is going higher in NSW

That brings us to the state budgets.

The improving economy is seeing operating budgets improve. South Australia should win the race back to a balanced budget in 2022-23 (if we exclude Western Australia). NSW and Queensland are forecasting balanced budgets in 2024-25. Victoria will be the laggard, forecasting deficits over a four-year forecasting period.

Following recent elections Tasmania will come out in August and Western Australia in September. In Perth they are probably too busy counting all the cash to hurry with a budget that is already well into surplus and moving higher.

For bond investors the operating position is only part of the equation.

Rating agencies put a high importance on it because it shows the sustainability of debt. But it is infrastructure spending — in General Government and State Owned Corporations — that largely drives funding tasks.

On this account all states are still going hard. NSW alone is spending $27 billion this year and around $108 billion over four years. This should see public sector investment continue to grow at 5% a year, helping drive overall GDP growth.

The NSW funding task announced last week actually moved higher despite an improved operating position. It seems they are now borrowing to put money into the NSW Generations Fund (NGF), rather than merely using asset sales.

Given ratings agencies allow them to use the NGF to offset gross debt for their metrics, it seems like a free kick. Borrow at 2% and invest in riskier assets assuming a 6-7% return.

Like the federal government’s Future Fund this is essentially a credit arbitrage which should work through the cycle. However the federal government used the one-off windfall of Telstra and budget surpluses to seed the Future Fund, rather than current borrowings. If this pays off it is ultimately good for NSW. But it does increase the state’s exposure to the economic cycle and asset prices.

Wages are making a comeback

The other important change from the NSW budget is the reinstatement of the 2.5% wage increase.

This has been in place from almost day one of the LNP Government in 2011, but was put back to 1.5% last year. The NSW government is Australia’s biggest employer with more than 400,000 workers. Even the federal government has removed its 2% wage cap, now linking it to private sector outcomes.

This all leads us to think the RBA wage forecasts of 1.75% this year and 2.25% medium term are far too low —particularly as unemployment falls to 4%. We expect 2.5% wage growth this year and above 3% by 2023.

Risk reward remains underweight semis

Our portfolios are generally underweight semi (state) governments with a bias to holding West Australian and Tasmanian bonds.

Despite ratings pressures we never worry about getting repaid due to the federal government’s implicit support.

However two positive forces behind outperformance of semi governments in the last year – RBA Quantitative Easing and Bank Balance sheet Liquid Asset purchases – are likely to taper in the year ahead.

These factors, together with high borrowing tasks, mean the cost of borrowing relative to the federal government should move higher.

We expect semi-government spreads around 15 to 20 basis points higher in the medium term.

About Tim Hext

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Jack is an investment analyst, focusing on large cap in the metals and mining sector.

Jack has more than 14 years of industry experience in specialist mining roles in Europe, Canada and Australia.

Prior to joining Pendal, Jack worked at Bank of America Merrill Lynch where he co-led the firm’s research coverage of Australian mining companies. He holds a Bachelor of Science (Hons) Degree in Economics from the University of Bath and the Chartered Institute for Securities and Investment Diploma.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

THE MARKET spent last week digesting the shift in Fed messaging.

The S&P 500 rose 2.8%, while the S&P/ASX 300 fell 0.8% as sentiment wavered in the face of the Sydney lockdown.

The US economy remains strong heading into its reporting season. We are also seeing economic and earnings momentum build elsewhere in the world.

Coupled with a stable bond market and receding fears of a policy mistake this bodes well for markets grinding higher.

Covid and vaccines

The key question is how the Sydney outbreak and the impact of the Delta variant will affect domestic economic re-opening.

Cases are likely to spike in the next few days while the lockdown takes effect. The lockdown in the Northern Beaches outbreak last Christmas led to a deceleration in case growth within a week.

The higher transmissibility works against containment. But on the positive side improved track-and-trace capability means there are fewer unknown cases leading to unexpected outbreaks than in previous instances.

Uncertainty remains elevated. But on balance we do not expect the overall market to fall on fear of the economic consequences of a more severe lockdown.

The regularity of these outbreaks prevents any earnings momentum building in the re-opening related stocks. We do not expect the most exposed re-opening trades to outperform until we are further along the vaccination path.

Impact of the delta strain

The big issue is whether the delta variant changes the outlook for growth in Australia and globally.

Will there be more widespread outbreaks in Australia? Will this more contagious strain lead to a slowing of momentum in the US and Europe?

On the former, we think the speed of response means we’re unlikely to see a repeat of last winter’s Victorian experience. We are also better prepared medically.

Globally we are still tracking the effects of delta strain outbreaks. The UK continues to experience only limited growth in hospitalisations despite a surge in new cases. This reflects the effect of vaccinations, though it could still change.

New cases in the US have plateaued. The delta strain is likely to become dominant there in the next few weeks. It is particularly prevalent in areas of the mid-west and north where there are low vaccination rates. We will need to watch the impact on hospitalisations in the next few weeks.

The higher transmissibility of delta raises the threshold on herd immunity.

In the US it’s believed up to 20-25% of the population has already had Covid. With vaccinations at 53% we may still be quite close to herd immunity. This will need to be tracked.

Economics and policy

US economic data remains strong. Companies are running low on inventory and struggling to replenish in the face of strong consumer demand.

There are signs that excess savings are being put to work. Personal consumption has held up despite the end of fiscal aid. There is a rotation of spending from goods to services as mobility increases — and a great deal of scope for this to play out further.

All this should provide a good outcome in the upcoming earnings season in the US. Australia will be different due to the stop-start nature of our re-opening.

On the policy side key Fed members assuaged market fears on a pivot in policy. The key message last week was that having effectively achieved their goal on an inflation overshoot this year, they will not need to see inflation remain above target thereafter.

They also acknowledged they are factoring the risk of higher-than-expected inflation into their deliberations.

These messages reinforce the view that the Fed is not as potentially reckless as some had feared.

In this context speculative trades such as crypto could come under more pressure.

The counter argument remains that the Fed does not have the degree of control it currently believes, given the combined degree of fiscal and monetary stimulus. But this will not be apparent for some time.

Elsewhere in the US the odds of a bipartisan infrastructure bill are rising, however it is not expected until the Northern autumn.

The Australian labour market continues to do better than expected. Overall employment is back above pre-Covid levels. Full-time employment has rebounded better than casual labour. Regional areas are doing better than cities, which reflects the effect of lost tourism and a strong mining sector.

Slack in the labour market is becoming a lot more limited. Measures of “excess” workers — those working few hours due to economic reasons — have returned to pre-Covid levels. The number of jobless looking for work has also fallen to eight-year lows.

This makes it difficult to see how the RBA continues with the mantra of no rate rises for the next three years.

Markets and stocks

Markets remained largely benign. US bond yields rose a little following the strong rally. Commodities were generally stronger and growth sectors continued to lead US equities higher.

Last week we saw rotation to tech growth names and miners in the local market. Financials and health care were the weakest sectors. The latter was dragged down by CSL (CSL, -6.7%).

CSL was hit by a ruling in the US that Mexicans crossing the border to give paid plasma donations will be considered illegal work. This could have an impact of 5-8% of CSL’s total collections. Plasma collection recovery has been a key factor in the CSL’s bounce, so this sets back the company.

Oil Search (OSH, -5.5%) fell despite oil price strength as the Abu Dhabi sovereign wealth fund divested part of its stake. We continue to remain positive on the oil sector given very favourable supply and demand dynamics.

Banks underperformed, led by Bendigo Bank (BEN, -5.1%) and Commonwealth Bank (CBA, -4.3%), which reflected weakness in the US financial sector the previous week, in response to the Fed’s more hawkish tone.

Insurers were also weaker, with QBE (QBE) off 3.8% and IAG (AG) down 3.4%. This was partly in response to Victorian floods and news that the High Court had rejected the insurance sector’s appeal against having to pay out on Covid-related business continuity claims. This issue is not yet settled, given there are still very few test cases.

Afterpay (APT, +12.8%) continued its run. This was partly given its high leverage to the rotation to growth. It also announced the launch of a “shop anywhere” option which will allow some customers to pay in instalments at non-affiliated merchants in the US. This is initially limited to 11 retailers including Amazon and Nike, with Afterpay benefiting from referral fees. The market also liked Paypal’s decision to increase prices 25% for their buy-now-pay-later service in the US. This only applies to a small percentage of their gross merchandise value (GMV) — mainly small businesses who do not have a negotiated price. The true impact is debatable, but it does reduce one of the competitive risks for APT.

Boral (BLD, +8.3%) announced the sale of much of its North American business at a higher price than most expected. We also saw the next act of the Seven Group (SVW, -5.8%) takeover offer play out. SVW raised its offer price for BLD stock (to $7.30 or $7.40 depending on the take-up) and extended the offer period.

Mining stocks bounced back as commodity prices rebounded. Independence Group (IGO, +5.6%) did best, followed by South32 (S32, +5.4%). Other deep cyclicals such as BlueScope Steel (BSL, +5.0%) did well on this trend.

Woolworths (WOW, -0.1%) de-merged its liquor and hotel business Endeavour Group (EDV, +1.3%) without triggering much of a stock response. We remain cautious on EDV — capital intensity and regulation both loom as potential headwinds. WOW now trades on about 28x price to earnings, which is high given the limited growth.

Cameron Squadrito joined Pendal’s Income & Fixed Interest team as an assistant portfolio manager in March 2026.

Cameron has worked closely with the Pendal team for more than five years, most recently as a senior dealer and brings with him extensive markets experience.

Cameron’s role includes supporting the team in enhancing the models, indicators and frameworks that inform our active investment decisions, as well as the day-to-day management of the portfolios.

Cameron is a CFA Charterholder and holds a Bachelor of Economics from the University of Sydney.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

The US Federal Reserve hit back last week against the view that they were complacent on inflation.

There was no explicit message on tapering out of the latest meeting of the Fed’s monetary policy arm, the Federal Open Market Committee.

But the “dot plot” of the committee’s rate expectations — and the language in an accompanying statement — were clearly more hawkish than the market expected.

The US yields curve flattened in response. Two and five-year yields rose, while 10-year yields were flat and 30-year yields fell. This also triggered a rally in the US dollar.

In the equity market we saw a sharp rotation out of cyclicals and commodities and into technology. Overall the S&P/ASX 300 was up 0.7% and the S&P 500 was down 1.9%.

Economics and policy

The key point in the Fed release was a shift in the FOMC “dot points” — a chart that outlines interest rate expectations of the 12 FOMC members.

The median view of the committee shifted from zero to two expected hikes by the end of 2023. The three senior committee members are all apparently expecting at least one hike.

The median inflation forecast for 2021 shifted up markedly from about 2.2% to about 3%. This is still considered transitory. Fed chair Jerome Powell noted the recent retracement in the lumber price, for example.

As a result expectations for 2023 CPI remained constant at about 2.1%.

This suggests average inflation will return to where the Fed wants to see it earlier than they previously thought, which explains a shift in the first expected rate hike.

All this should be considered in the context that the Fed has been as inaccurate as anyone else when it comes to forecasting the path of rates, based on its historical predictions versus actual outcome.

There was also a change in the wording of the release, which suggested the tapering decision was no longer more than six months away.

The Fed’s hawkish tone gave the market more confidence that inflation will be contained. Break-even inflation expectations fell, which prompted flattening in the Treasury yield curve.

Yield curve shift

The shift in the yield curve was material, which probably reflects the strength of the consensus position towards inflationary trades.

The debate now is whether this is just an adjustment in signalling or a more significant pivot in the Fed’s stance. Statements this week will be important to watch.

The Fed is unlikely to want any further flattening in the yield curve. So we would not be surprised to see the messaging shift subtlety back to promoting growth.

The US dollar rose along with the short end of the yield curve. This shift in Fed signalling probably means the USD will remain well supported for a period.

This weighed on commodity prices, particularly in crowded trades such as copper, which fell 8.3%. Gold was off 5.8%.

The fundamental supply-and-demand equation remains favourable for commodities. Our medium-term view remains positive, but we may see some near-term weakness as the consensus inflation trade is washed out.

Impact on portfolio construction

This all led to the inevitable rotation towards growth stocks, notably technology.

For the moment the strong rotation from growth to value that began in November looks to have played out.

Instead, in recent months we have seen momentum swing between the two. This emphasises the need to remain balanced in portfolio construction.

We have been adding to our growth exposure in recent weeks to hedge such a policy risk. But we remain underweight more traditional rate sensitives such as REITs.

In commodities we prefer energy to metals at this point. We see fundamentals in energy as a bit more supportive, while it has also been a less crowded trade.

Covid and vaccines outlook

We continue to monitor developments around the Delta variant of Covid, given its potential for larger outbreaks and a higher vaccination threshold for herd immunity.

The UK is the bellwether in this regard. So far a rise in cases has not fed through to higher hospitalisations. This is potentially due to Delta being more benign than the original strain. The level of vaccinations may also be playing a role.

The latest Australian outbreak needs to be monitored, given the slow rollout of vaccines.

The risk of further restrictions has risen. Domestic re-opening trades are struggling to perform in this context. There is a clear divergence from global re-opening exposures. But we are mindful that sentiment can swing quickly in this regard.

Markets

It is important to emphasise that the Fed’s hawkish bent does not mean markets have peaked for this cycle.

First, the broad policy environment remains supportive. We are still looking at two years of near-zero rates and monetary policy has a large lag. Fiscal policy also remains high stimulative.

Second, we can be guided by history. The first hike in a cycle normally prompts a market correction. However the actual peak tends to occur after rates have risen a number of times.

Some speculative excess has been cleared out and the rotation is significant. However equity markets overall seem to have digested the Fed’s shift quite comfortably so far.

US 10-year Treasury yields fell by a basis point last week, while two-year yields rose 11bps to 0.26%.

The divergence between oil and copper is interesting. Copper is off 11.1% for the month while Brent crude is up 6%. Again, this probably reflects consensus positioning in recent months.

The Australian market was dominated last week by thematic rotation. Technology (+12.4%) and Health care (+6.2%) led, while resources dragged down Materials (-4.7%).

Banks (+2.2%) held up reasonably well, in contrast to overseas markets. There may be some near-term vulnerability here.

Gold miners led the underperformers. Northern Star (NST, -13.9%) was the worst in the ASX 100, followed closely by Newcrest (NCM, -8.4%) and Evolution (EVN, -8.1%).

Copper miner Oz Minerals (OZL, -12.2%) also lagged.

Contractor Downer (DOW, -7.2%) also fell, following a broker note which highlighted wage pressure in the contracting space. We do not agree with the conclusion that wage pressure seen in the Pilbara can be applied to expectations for other industries and locations across the country. DOW continued with its stock buy-back, which also suggests this is not the issue some fear it to be.

ResMed (RMD, +12.5%) was the best in the ASX 100. In this case the growth rotation was augmented by news of a product recall from a competitor.

Afterpay (APT, +10.5%) is the most leveraged to the growth trade at the moment. Xero (XRO, +6.1%) also benefited.

A stronger US dollar is beneficial for Ansell (ANN, +9.4%), Cochlear (COH, +4.8%), James Hardie (JHX, +3.6%) and RMD, among others.

Finally, Coles (COL, -1.9%) held a strategy day which flagged that capex will need to rise to compensate for under-investment in recent years. Capex will rise from 2% to more than 3% of sales per year.

This raises questions for the supermarket sector as rising capital intensity may dilute returns. COL also signalled that they are seeing the trend to more neighbourhood style unwinding, although in the current environment we doubt this is material.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

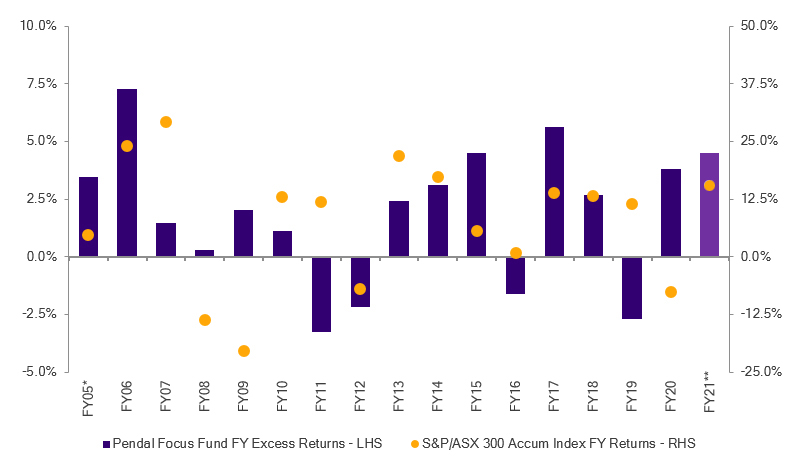

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.