This month’s Emerging Markets Spotlight demonstrates why we believe country-specific factors are critical when assessing EM investments. James Syme and Paul Wimborne (pictured), managers of Pendal’s Global Emerging Markets Opportunities Fund, explain:

FOLLOWERS of our views will be aware we’ve held a significantly positive tilt towards some Latin American equity markets since the third quarter of last year — including several new names and increased weightings in Mexico and Brazil.

Latin America has historically shown a strong relationship between GDP growth and commodity prices — and also between US dollar equity returns and commodity prices.

Commodity prices remain extremely strong by recent standards. After starting 2020 at about US$100/t, iron ore sits at around US$200/t. Copper has moved from US$2.80/lb to around US$4.50/lb; soybeans from US$9.40/bu to above US$15/bu.

These moves in export prices feed through to commodity-based economies in many ways. Trade balances and current account balances strengthen, tax revenue rises, corporate wages and investment can rise.

This upward pressure on currencies, corporate earnings and liquidity creates a potentially very attractive opportunity for equity investors like us.

Yet we remain zero weight Argentina, Chile, Colombia and Peru.

Why? In a word, politics.

Every unhappy country is unhappy in its own way. So what are the specifics in each of these cases?

Argentina

Argentina has the least functional politics of the four. The populist government of president Fernandez and vice-president Kirchner has struggled repeatedly with indebtedness (mostly to the IMF), inflation and a weak economy.

It has been illegal for companies to fire workers since last year, the private sector is subject to arbitrary price controls (which has caused output to slump), citizens have very limited access to foreign exchange, aggressive wealth taxes are being imposed (with the promise that they are one-offs) and almost every economic statistic is horrendous.

Consensus economic forecasts for 2021 are for CPI inflation at 45% and unemployment at 11.5%.

Until there is prospect for a change of political leadership, Argentina is effectively uninvestable in our eyes.

Chile

Chile has two major political problems.

Firstly, president Pinera is highly unpopular and the right-wing coalition he heads seems to be collapsing. This has allowed the Opposition to pass several populist bills largely seen as negative for the private sector and financial markets.

These include a new mining royalty Bill that will be a significant negative for the critically-important resources industry. The Bill has been approved by the energy and mining committee in the lower house of parliament and is likely to pass the Senate as early as this month.

The government is unlikely to be able to stop it. It similarly failed to stop three Bills allowing the public to draw down assets from their private pensions.

Unhappiness with the government and with the state of the economy and society has led to a second important development in Chile.

In October 2020, following mass protests against inequality, Chileans voted overwhelmingly to replace the constitution implemented during the military rule of General Pinochet.

The new constitution will almost certainly create expanded rights to healthcare, education, housing and welfare — and consequently will require significantly higher taxation.

It may also constrain the private sector in other ways, and may restructure the relationship between commodity producers and the state. These are not automatically negative outcomes, but the uncertainty clearly creates significant risk for investors.

Colombia

Unlike Argentina and Chile, the problems in Colombia stem from an attempt by the government to maintain orthodox fiscal policy.

Colombia has had an investment grade credit rating since 2011, but the fiscal deficit has expanded from 1.9% of GDP in 2019 to 8.9% last year and an estimated 8.2% this year.

Tax revenues have to be increased. Analysts estimate 1% of GDP in additional revenue is the minimum required to maintain the credit rating. The proposed budget would increase taxes on middle-class Colombians, and has proved wildly unpopular.

Previous finance minister Alberto Carrasquilla first withdrew the budget — and then resigned — when violent demonstrations broke out across the country. Protesters blocked roads and fought with the police.

New finance minister Jose Manuel Restrepo has instead sought a national consensus around a budget based on alternate taxes and spending cuts — but protests have continued.

This is not the first violent demonstrations that the Duque government has faced. A collision between bond markets and the Colombian people makes for a difficult environment for equity investors.

Peru

Peru is in the middle of its presidential election. The first round took place in April and the second round is expected on June 6.

Hard-left populist Pedro Castillo of the Free Peru Party won the most votes in the first round and is leading in polls ahead of the election run-off.

His opponent, conservative candidate Keiko Fujimori of the Popular Force Party, is enjoying a lot of political support from other right-wing parties. But allegations of corruption, money-laundering and obstruction of justice are weighing heavily on her campaign.

Castillo is a radical, anti-establishment candidate who has said he does not plan to nationalise private companies in Peru. But he plans an increase in government spending of 10 percentage points of GDP and has hinted at extremely high corporate taxes to help fund this.

Polling suggests a landslide win for Castillo. The prospect of this is placing significant stress on financial markets.

Conclusion

The pick-up in capital flows to emerging markets, a global recovery, higher commodity prices and the steady roll-out of vaccination are all powerful positive drivers for higher-risk, commodity-exporting EM countries.

We are overweight Mexico, Brazil and South Africa in the portfolio.

But we have avoided the smaller Latin American markets for these generally political, but country-specific, reasons.

Download this article as a PDF.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS were broadly flat last week — the S&P/ASX 300 returned 0.35% and the S&P 500 fell 0.39%.

However we did see material rotation: tech rallied and the high-momentum areas of commodities and crypto fell — in some cases sharply.

A combination of factors were behind this:

-

- A sense that concerns over inflation were at a crescendo, which was not translating into a significant bond yield spike. This suggests the market is very long on the inflation trade.

- Early signals that the Fed may kick off the debate over tapering a couple of months earlier than expected.

- Comments from Beijing on an excessively rapid rise in commodity prices raised concerns they may act to curb prices. There was also a warning on the surge in Chinese interest in cryptocurrencies. This is a reminder of Beijing’s desire to retain control of its financial system and launch its own digital currency.

So far equities have held up well, consolidating in a range rather than correcting like other risk assets. In our view equities remain well supported by corporate earnings, driven in turn by the strong economic recovery.

Macro and policy outlook

The market latched onto a number of potential signals out of the Fed last week:

- Minutes from the Fed’s recent meeting noted that if the economy continued to make rapid progress towards its goals, it may be appropriate at some point to begin discussing a plan for adjusting the pace of asset purchases.

- Other comments such as a need to be “nimble on policy” reinforced this change in tone regarding tapering.

- Federal Open Market Committee member Richard Clarida maintained a line of current inflation as transitory. But he went on to say the Fed was “attuned and attentive to incoming data” and “monetary policy is as much about risk management as it is about the baseline”.

All this was accompanied by dovish comments regarding timelines. But it may represent an adjustment in the Fed’s tone, signalling a focus on ensuring that inflation expectations remain under control.

So the tapering debate has potentially begun. The real question is ‘will this end the equity rally?’ We remain of the view that it will not.

The reasons for inflation concerns are clear: strong demand, supply-chain bottlenecks and surveys showing companies feel they have cost pressures coming through.

We agree the risk of inflation is higher than it has have been for some time. But it is not a forgone conclusion.

There is an alternative perspective which may yet come to pass. There are a number of arguments supporting the case against widespread inflation, including:

-

- Supply bottlenecks may quickly be unwound. We are seeing a demand spike with supply still lagging. But there is evidence the supply response is coming, for example in export data from Taiwan and Korea.

- Commodity prices have not been a good lead indicator for broader inflation for the last 25 years.

- Productivity: Wages can go up without a big shift in core inflation if productivity is also rising. We have just seen the US GDP recover to pre-Covid levels with 8 million fewer jobs — an indication that productivity has surged.

- Supply of labour: This is likely to rise, particularly in the US after September as benefits return to pre-Covid levels, alleviating wage pressure.

- Plateauing demand: We may have reached peak levels of demand in a number of key segments. Durable goods, housing and auto sales are at levels that are likely to plateau. This would lead to inflationary pressures easing.

- Debt levels: The US has record debt just shy of 380% of GDP, although it has shifted from households to the government. History suggests high debt levels lead to declining velocity of money. M2 money velocity ratio in the US is sitting at just over 1.1 compared to 1.4 pre-pandemic. US bank results suggest they are still not extending credit — a necessary pre-requisite to see some inflation.

- Household spending: A third of US stimulus payments are paying down debt rather than increasing spending. This is a sign that people are wary of overall debt levels, which may subdue spending.

- Tax: The prospect of tax increases may reinforce caution among consumers.

- Demographics: Populations are aging and older people tend to spend less — so ageing can be deflationary.

- Technology continues to provide opportunities to deliver services and products more efficiently.

There is anecdotal evidence of wage pressures, but so far nothing is showing up in the data.

A lot is made of the rise in the breakeven inflation rates. But the inflation sceptics point out that this is highly correlated to commodity prices. They cite the Cleveland Fed’s long-term expected inflation measure as a better historical indicator of wage pressure and inflation. This has barely risen, suggesting no sign of wage-push inflation.

In conclusion there are many reasons to be wary about building inflation and rising bond yields. This seems to be the consensus view and reflects broad market positioning.

But it is not certain that we are seeing a secular shift in inflation. There are good reasons to argue against betting the farm on an inflationary outcome.

This goes to the issue of managing for different scenarios in our portfolios.

We have exposure to stocks that will benefit from higher inflation. But we also see the need to maintain some hedges on low inflation — notably quality growth names such as Xero.

COVID and vaccine outlook

Here there are two areas of notable risk:

-

- A continued spread of Covid in emerging markets and countries without access to vaccines

- Effectiveness of vaccines against new variants.

On the first issue we are seeing more positive trends in India as new cases and positivity rates continue to fall. (Although there are still questions about the accuracy of data.)

Overall new case numbers are dropping globally.

One key concern for Australia is that countries with strong track records such as Taiwan and Vietnam are seeing new waves of cases higher than any before. This is leading to lock-downs and dramatic reductions in mobility.

This brings the focus onto vaccine provision.

Global doses are approaching 30 million per day but only about 8% of the global population has been vaccinated.

The US is making more vaccines available (20 million doses by the end of June). The WHO approved the Sinopharm vaccine, allowing it to be exported.

On the issue of efficacy we had positive news this week from the UK. Due to detailed genomic analysis British scientists are now able to assess effectiveness of vaccines against the more infectious Indian B.1.617.2 strain.

In the UK those with two doses of vaccine are showing a high degree of protection against the Indian strain. Those who catch it are not getting as sick.

Health trends in the US remain positive, supporting the re-opening trade. As consumer confidence begins to rise significantly we are seeing clear signs that the next leg of recovery is kicking in.

Travel interest has returned to pre-Covid levels, according to data from travel-related apps. We are yet to see this translate materially in improved airline demand, but we suspect this could shift quickly.

Markets

Equity markets held up well last week despite a sell-off in commodities and the cratering of crypto.

Gold continued to rebound, resuming its status as a defensive asset class. Brent crude was off 3.3% on rising expectations of an Iranian deal which would allow more supply into the market.

The Bitcoin sell-off looks like the last domino to fall among the proxies we have been tracking for excess liquidity. Other indicators such as renewable energy ETFs, IPO ETFs and speculative technology stocks have also had significant corrections. This is a healthy sign for markets, suggesting speculative froth has receded.

The Australian market has held up well in face of a sell-off in cyclicals. It has consolidated over the last month, following a 15% move from early November.

The liquidity supporting the market is evident as banks continue to grind higher. We note that Commonwealth Bank is now about 21x next-12-month price/earnings, suggesting people are looking to park cash in safe-haven equities due to low rates.

Stock news

Carsales.com (CAR, -8.2%) was the worst performer in the ASX100 after announcing a deal to buy 49% of a US online caravan site in the US. There was a degree of market scepticism over this strategy.

Concerns over tapering dragged on cyclicals. BlueScope Steel (BSL, -6.6%), Santos (STO, -5.7%) and Alumina (AWC, -5.3%) were hardest hit.

James Hardie’s (JHX, -2.6%) result was complicated. North American volumes disappointed, although this was offset by better pricing and demand in Europe.

Technology stocks benefited from the rotation.

Appen (APX, +19.4%) was the strongest performer in the ASX100. Management announced an organisational restructure and confirmed its recently downgraded guidance which helped the bounce. It is still down about 70% from its August 2020 peak.

Xero (XRO, +13.1%) bounced back strongly after last week’s reaction to its result. It seems the focus has shifted to potential growth in FY22 and FY23 as the UK pushes more small businesses onto cloud accounting through the “making tax digital” program.

Ampol (ALD, +9.2%) and Viva (VEA, +2.5%) benefited from a long-awaited government fuel security package. This provides scaled support for sector-based refiner margins for six years (and potential for nine years). The government will pay for 50% of capex needed for upgrades to improve fuel standards. This is supportive for the long-term rating of both companies.

Aristocrat (ALL, +8.9%) upgraded earnings ahead of today’s result. Its gaming and digital businesses are going well. The former reflects the US re-opening.

Qantas’s (QAN, +6.5%) quarterly update indicated that cash flow is now positive.

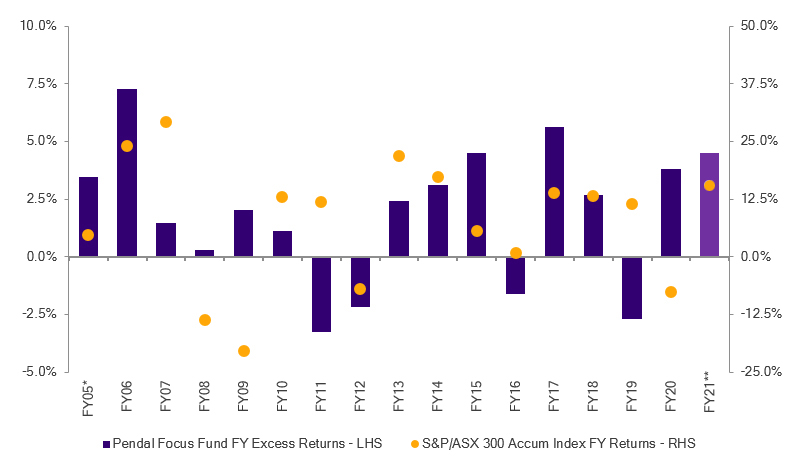

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

Find out more about Pendal’s fixed interest strategies

THERE were plenty of positive signs this week.

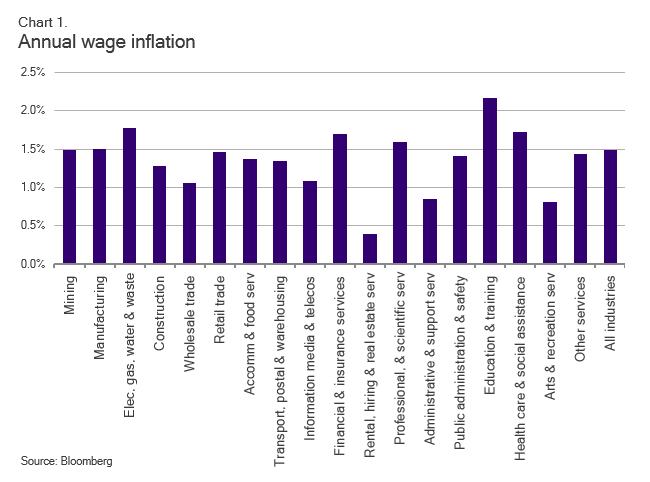

Despite a slight pull-back in the latest job numbers and consumer confidence, we’re seeing wage inflation recover from a down-trend that was underway before the pandemic shock.

April was expected to be more subdued than earlier months because the data now reflects the full impact of JobKeeper ending.

There were plenty of worries that hard won post-Covid gains would be lost as talks of tapering accelerate overseas.

But now there is a difference.

Before the pandemic the RBA acted as a lone wolf, tackling unemployment with monetary expansion, while the federal government kept a lid on spending due to its budget surplus obsession.

Now the RBA and federal government are in lock step as Team Australia.

Fiscal policy is the main game

The pandemic crisis finally freed the Liberal government from the shackles of dogma — Budget surplus at all costs.

The transformation is now complete with the release of the federal Budget.

Employment is now above its pre-COVID level and GDP is expected to soar this year. But the government continues to plough more into the economy, presumably to secure a full employment victory this time.

New stimulus initiatives are worth 4.1% GDP over four years. This compares to the paltry 2019 budget spend worth 0.5% of GDP when unemployment was drifting north of 5%.

These are good signs indeed — not just for the Australian economy but also for the Liberal government.

As the saying goes, fortune favours the brave.

They may learn that not all spending is bad. The good news this time is that the strategy is affordable.

A continued surge in commodity prices — as well as tax receipts from growth instead of higher taxes — will make this a “self-funded” expenditure.

Monetary policy

We anticipate the RBA’s monetary response will remain expansionary to support the federal government’s fiscal response.

That will involve keeping the cash rate target and the interest rate of RBA Exchange Settlement account balances low. It’s also highly likely there will an extension of the Quantitative Easing (QE) program as part of the toolkit.

The incredible rebound in the Australian economy has given the RBA a shot in the arm.

These complementary actions between the monetary and fiscal policies make full employment a goal rather than a dream.

The implications

Despite the stimulatory Budget surplus, a massive increase in supply of Australian government bonds (CGLs) is not anticipated, because the spend can be largely funded through economic growth.

An extension of the RBA’s QE program will continue to provide support.

We therefore continue to favour CGLs versus semi-government bonds as the economy recovers.

We’re also keeping a watchful eye on inflation to see if it will turn structural this time or remain transitory — as was the case in historical post-crisis periods.

As highly expansionary fiscal and monetary policies remain in place after the economy hits full capacity next year, we suspect inflation will stick above target for another few years at least.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Many US and European stocks are reporting strong earnings. Pendal’s Head of Global Equities Ashley Pittard (pictured) explains what this means for global equities portfolios.

- US and European companies post better-than-expected earnings

- Stronger macro environment to drive growth

- Ashley Pittard: How to position a global shares portfolio for the recovery

- Find out more about Pendal Concentrated Global Share Fund

STOCK SELECTION is the key to successful portfolio management in 2021 as a booming earnings season in the US and Europe indicates the broader global economy is roaring out of its COVID-induced coma.

In the US, S&P 500 stocks grew earnings by 47 per cent in aggregate year-on-year in the first quarter, on the back of sales rising more than 10 per cent.

European companies did even better with a 153 per cent lift in earnings and a 3.2 per cent rise in sales.

Pendal’s head of global equities, Ashley Pittard, says the strong performance is a result of pent-up consumer demand, the rebuilding of corporate supply chains and immense government stimulus.

But he says investors should be cautious about the index dominance of America’s big tech stocks — the so-called FAANGs of Facebook, Amazon, Apple Netflix and Google-owner Alphabet — which can give a misleading impression of the market’s overall prospects.

“How you wanted to be positioned the last few years, it was all in the FAANG stocks,” he says. “The market was very narrow because the US tech sector were the only companies that could grow their earnings.

“Now, it’s not going to be as narrow because earnings growth is going to be broader.

“The earnings today due to a stronger macro environment means that the market will be more broad, which therefore should mean that we will get higher equity markets.”

Portfolio construction perspective

From a portfolio construction perspective, Pittard says investors should move to a concentrated stock-selection stance and avoid shadowing the tech-dominated indexes.

“The S&P is near an all-time high valuation at 24 times earnings, but if you strip out the top ten stocks, the market is still very compelling. That’s why I believe that over the next three years, as long as you’re a stock picker or you’re very selective or very concentrated you will do very, very well.

“But if you shadow the index — you just mirror the market — and you’re going to do poorly.”

One reason the big tech companies did so well in the Covid recession was they brought forward demand — they were able to service households in lockdown that were unable to travel, visit the shops and eat out, Pittard says.

Now, as the pandemic lifts, household spending will resume normal patterns.

“It’s like coming out of prohibition. People are going to go nuts. You can already see it and we don’t even have full vaccinations.”

Businesses are also lifting spending. In past recessions, inventories build up as demand reduces, leaving businesses with surplus stock to run through as the economy recovers. This time, inventories were run down as global supply chains reeled.

“So, what has to happen? They get everybody in, everybody’s doing overtime, everybody’s getting paid more and they’re rebuilding inventories,” says Pittard.

Underpinned by government spending

Government spending is underpinning the boom.

“It’s more than double what they did in the global financial crisis,” says Pittard.

In terms of regional allocation, Pittard advises being underweight US stocks and investing instead in Europe and the UK.

“You’re getting broader earnings growth, and you don’t need to be in those top 10 stocks that have had their day because they brought forward demand.”

Pittard says the main risk to portfolios is inflation resulting from central banks keeping interest rates artificially low as they seek to drive the economic recovery.

“Over time, every government that has tried to control prices has failed,” he says. “What governments are doing now are controlling the bond rate… in a normally functioning market the bond rate is at or higher than the inflation rate.”

The best asset allocation to deal with that risk?

“You want to be more concentrated, you want to be more stock specific, you want to have a higher active share, you want to have a long-term view and you want to have quality stocks.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

LIKE A horror movie where you get a fright — even though you already know something bad’s about to happen — the markets last week experienced a mini-panic after the first signs of inflation.

We won’t know for a year or so if this inflationary pulse is transitory or more structural. In the interim, debate is likely to ebb and flow between fear and ambivalence.

The key question is: what does it mean for markets and portfolio positioning?

We are still in the camp that markets can rise.

But we think this will be driven by earnings growth rather than valuation expansion — a reversal of the past decade’s trend.

Governments and central banks are focused on generating growth to address social issues such as inequality and to underwrite investment in resilient supply chains and infrastructure for energy transition.

This should support earnings, which can in turn support markets — as long as there is no significant policy tightening.

Without the broad tailwind of valuation re-rating, earnings become a key differentiator of stocks in the market. Picking cyclical winners or improving structural growth stories will be key.

Last week saw the S&P 500 sell off 1.35% and the S&P/ASX 300 lose 0.71%. But there was significant underlying volatility in a knee-jerk reaction to inflation data.

Most sectors sold off. Growth sectors such as Technology (-6.46%) sold off the most, but traditional inflation hedges such as Resources (-1.72%) were also down. This is creating opportunities.

Economics and policy

US inflation data came through much stronger than expected. The consumer price index (CPI) was up 3% year-on-year in April and 0.92% ahead of March. A surge in prices is evident in areas related to re-opening such as airline tickets, travel lodging and used cars and trucks.

The CPI is expected to peak next month at +3.6% year-on-year before the base effect starts to moderate.

The market’s reaction was exacerbated by the Fed’s response. A number of Board members quickly characterised the data as transitory and emphasised that policy will remain loose.

The market is adjusting to the risk of inflation after decades without it. Its key question is the credibility of a commitment to keeping rates steady as inflation rises. This will continue to impact the US dollar and bond yields.

We wouldn’t be shocked to see inflation surprising on the upside over the year. It would be a natural outcome from an economy doing better and the increasingly co-ordinated nature of the global recovery as vaccines roll-outs progress.

But we emphasise that this does not have to be negative for equities overall because it’s likely to coincide with better earnings.

Over the medium term wage growth will be the key factor. There is already evidence in the US that tighter labour markets in certain sectors along with the effect of higher unemployment benefits, is leading to wage growth. Amazon and McDonalds have both announced 10% wage increases covering some 600,000 workers.

We do not expect a wage-price spiral to form. There is still a lot of capacity in the economy and structurally deflating factors. But given that governments are looking for higher wages to help address social issues (particularly in lower-income work) this will remain a key macro factor to monitor.

In the US the odds are growing of a bipartisan “traditional” infrastructure bill of $800-900 billion — funded by tax enforcement rather than tax increases to get Republicans over the line.

A bi-partisan bill could be ready by mid-August. This emphasises that there is more stimulus to come, albeit spread over a number of years.

There is some risk to this. Democrats are concerned it may make subsequent, more progressive policy bills harder to pass.

In Australia the federal budget sent an important signal that growth is the goal. For now traditional Liberal policies such as fiscal conservatism are in hibernation. Increased spending on areas such as infrastructure helps the underlying economy and corporate earnings.

COVID and vaccines

There is incremental improvement in global case numbers. The Indian data is difficult to interpret due to measurement challenges. But the rolling over of the daily new positive test rate is a small sign of hope.

Europe continues to progress. There is increasing focus on European re-opening and economic recovery, which is supportive for global cyclicals.

The US is approaching the point where Israel experienced a substantial shift down in new Covid cases.

This is leading to a real shift in re-opening momentum. Surveys suggest a dramatic change in sentiment towards participation in public activities such as movie-going, eating out and air travel. This is a pre-cursor of the release of pent-up demand.

There are some concerning developments we need to keep an eye on.

The UK is beginning to see the spread of the Indian variant despite a high level of vaccinations (55% vaccinated and 30% with two doses).

There are concerns around the variant’s transmissibility. Modelling suggests a 10-20% transmissibility rate is manageable but more than 30% is a problem. No one knows the transmissibility of the Indian variant, but experts suggest there is a 35-50% chance it is more than 30%. This could delay a roll-back of restrictions.

The other issue is the effectiveness of vaccines on this variant.

Early signs are positive. In areas of the UK hit by the Indian variant there are fewer cases among over-60s (where the vaccination rate is higher).

This ties into a second area of concern related to the Seychelles. Despite vaccination rates above 70%, cases have surged in this island nation off the African east coast. A third of new cases are among people who have already been vaccinated (using the Sinopharm and Astra Zeneca vaccines).

It is too early to make a call, but this highlights potential issues around the effectiveness of certain vaccines to Covid variants.

This highlights the importance of booster shots and complicates the re-opening of borders.

Markets

The inflation data prompted a risk-off move in markets. Equities and commodities fell, while the US dollar held firm.

We have been discussing the notion of market consolidation for a few weeks now. It feels like this is playing out with the crescendo of the inflation print. But the market is proving broadly resilient.

The VIX Volatility Index spiked last week. Though over the past year spikes have come at progressively lower levels with quicker reversions — a positive sign.

The US earnings season has been very strong. Earnings for Q1 were revised up 29% (and FY22 up 8%). This has alleviated pressure on P/E ratios and brought the S&P 500 back towards 20x earnings.

This valuation rating is very much in line with the laxity of monetary conditions.

A key risk to rating is any sign of tighter policy. At this point the Fed’s guidance is for a gradual tightening. But higher market rates, credit or bonds may challenge this. The key point is that a re-rating is unlikely, leaving earnings as the key factor for stocks.

The ASX’s sell-off last week was broad-based. Staples (+0.98%), Health Care (+0.73%) and Financials (+0.63%) eked out gains, but all other sectors lost ground.

A2 Milk (A2M, -21.2%) was the worst performer in the ASX 100 after management issued yet another earnings downgrade. It feels like the company is getting close to new base in terms of margins and market expectations. We think there need to be signs of material operational improvement to see opportunity emerging.

Xero (XRO, -15.9%) sold off along with other tech names, but the market was also disappointed with its earnings result. EBITDA came in below market expectations as the company invested more in R&D and customer acquisition. Previously, the market has welcomed further investment by tech growth companies, but the mindset has shifted in the current environment. The market no longer assumes incremental benefit to revenue growth.

XRO remains our pick in the sector. Its rating is in line with comparable, cloud-based companies. Our positive thesis is built on a growing appetite among governments and companies for digitally-enabled businesses. Xero continues to grow its subscriber base. We expect average revenue per user to benefit from product development and bolt-on deals enabling provision of new services.

Most other tech names fell on back of the inflation data last week. Afterpay (APT) was down 10.5% and Wisetech (WTC) fell 7.9%.

Chemical company Incitec Pivot (IPL, -10.41%) was among the weakest. It revealed more operating issues at its US ammonia plant, which led to another downgrade. Commodity price increases are ameliorating a lot of the earnings pain.

Crown (CWN, +7.59%) was the best performer as Star (SGP, +3.84%) tabled a bid to rival Blackstone’s, raising some competitive tension in the takeover process.

Treasury Wine Estate (TWE, +6.69%) delivered a well-received strategy update. The key factor was a continued turnaround in the US business as the economy recovers and some oversupply issues start to recede. This is helping offset a hit to its Chinese business from tariffs on Australian wine.

Boral (BLD, +5.12%) received a no-premium takeover bid from Seven Group (SVW,-5.16%), creating uncertainty over the latter’s intentions.

Finally Commonwealth Bank (CBA, -2.83%) rounded out the bank updates. It was a positive quarter, reflecting broad trends seen at the other banks.

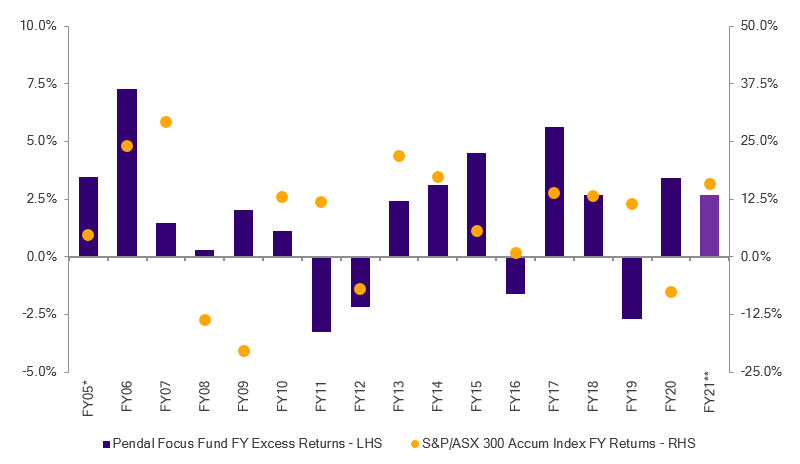

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

The next five years will see inflation significantly higher than the past decade. We should be alert to this but not alarmed says Pendal portfolio manager Tim Hext in our weekly Bond, Income and Defensive Strategies note.

Find out more about Pendal’s fixed interest strategies

THE two big highlights of the week were the federal budget and US inflation numbers — and they are more closely linked than it might seem.

Federal Budget

The RBA and Treasury now forecast GDP and employment at full capacity for next year.

That means no slack left in the economy. Normally this would signal a tightening of monetary and fiscal policy. But times have changed.

Invoking the continuing transition from the crisis, the RBA and government are both firmly foot-to-the-floor.

For the government a looming federal election translates to “why not keep handing money out?” After all no one seems too troubled.

Even the usual crowd of economists who warn of impending doom from too much debt have gone quiet. The only ones who can hold their heads high are proponents of Modern Monetary Theory. They understand better just how government debt works.

The RBA seems to have gotten itself in a corner. Like the rest of us they expected the health crisis to be far worse. Unlike us they made commitments (or guidance in some cases) out to 2024 based on that expectation.

The RBA is more oil tanker than speedboat when it comes to turning around. For now they remain committed to Quantitative Easing, Yield Curve Control and no rate hikes.

This is now based solely on benign inflation and wage forecasts — not growth and employment, which are strong.

Future RBA statements will be watched closely for watering down of rhetoric.

US inflation

That leads us to this week’s US CPI numbers. CPI was 0.8% for April and 4.2% year-on-year.

Extraordinary numbers.

Economists and no doubt the Federal Reserve will be quick to reassure us this is transitory.

Supply bottlenecks in the auto industry have prompted a spike in used car and rental car prices. Hotel rooms, airfares, sporting events — most things have spiked as the economy reopens.

These spikes won’t repeat but other spikes are coming. Rents are creeping up and wages are already rising. Commodity prices are taking off.

If there is excess capacity in labour markets perhaps the Fed can get away with the idea of ignoring these transitory factors and we can return to business-as-usual low inflation.

I suspect though with ongoing massive fiscal and monetary stimulus the inflation genie is out of the bottle.

Low inflation expectations may become, if not unhinged, at least challenged in the years ahead. Wages could well follow. Inflation in Australia will also follow.

Eventually technology and demographics will keep a lid on inflation becoming a massive problem.

But the next five years will see inflation significantly higher than the last 10 — something we should all be alert but not alarmed at.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Which asset classes look good in light of this week’s federal Budget? Pendal’s head of Multi Asset Michel Blayney explains

THE federal government Budget, released on Tuesday night, was big spending in keeping with the fiscal stimulus needed to bolster the economy, still recovering from the COVID-19 induced recession.

There were tax breaks for individuals and businesses, as well as large outlays across the economy, including aged care, health and infrastructure.

But what does it will mean for investors? Should the Budget cause investors to think differently about their portfolio?

“Certainly the budget measures should make people think about what they’ve invested in,” says Michael Blayney, who leads Pendal’s Multi-Asset Investments team. “If for no other reason than it locks in stronger economic growth.”

Blayney is relatively sanguine about the ongoing Budget deficit as a result of big spending last year and this year.

Budget forecasts suggest deficits this financial year through the next four will total close to $500 billion.

“While the numbers sound high, there are a few things to keep in context. It’s less than half the debt of many other major developed nations and its quite serviceable, particularly with low interest rates. Ultimately debt is serviceable as long as the economy grows, and that fact can get a bit lost.

“The key investment implication is the stimulatory effect the Budget is having. You have this combination of low interest rates and people not being worried about fiscal discipline.

“That’s a new way of thinking which the pandemic created. At the same time, you have this supply chain disruption, in goods like semiconductors.

“Put together, investors need to be thinking about putting some inflation-proofing into portfolios.

“That’s not about forecasting inflation. It’s about constructing a good portfolio that looks at a possible range of outcomes and includes assets that do well in different economic scenarios,” Blayney says.

Asset classes to consider

Current options to consider include alternative assets, commodities and inflation-linked bonds over nominal bonds.

Also real assets provide an opportunity, such as listed property, though the caveat there is that cash flows of those assets are linked to inflation.

At least in the near term, more value-oriented stocks look more compelling, Blayney believes.

“Having a tilt towards value in a portfolio can help with some of that inflation proofing.”

Blayney says the housing market is something to watch closely, because in Australia it’s “gone bananas”.

Not that there is an imminent collapse about to happen.

“The budget included measures to promote people to get into housing. Viewed in isolation that’s a good thing. But the crux of the problem is that house prices are too high and any government policy that comes along, coupled with low interest rates, encourages prices.

“There’s not an immediate investment implication, but we know from the global financial crisis what happens when housing goes bust. We saw that in the US and Ireland.”

A tick for infrastructure spending

Blayney prefers spending on infrastructure packages to hand-outs, and the latest budget gets his tick of approval on that front.

“Infrastructure spending helps with sustained economic growth whereas cash tends to fuel speculative activity.”

While the economic growth outlook is strong, as demonstrated in the official Treasury forecasts which puts growth next financial year at 4.25 per cent, Blayney is worried about valuations.

“You are starting to see a bit of speculative activity. The poster child here is cryptocurrency. There’s been an explosion in this space and some look highly speculative. The pricing of some cryptocurrencies is also extremely volatile.

“I also think tech valuations have been getting stretched,” Blayney says. “At least the tech companies are still making revenue and earnings.”

The challenge for investors is that they have to invest somewhere, and this is where a long-term view is critical.

For Blayney, the short term might lean towards value investing, but the long term goes the other way.

“People have to think strategically through the cycle and I think they will have to hold more growth stocks than they have historically in order to deal with the economic environment and still earn a decent return.”

About Michael Blayney and Pendal’s Multi-Asset capabilities

Michael Blayney leads Pendal’s multi-asset team.

Michael has more than 20 years of investment management and consulting experience. He was previously Head of Investment Strategy at First State Super and head of Diversified Strategies at Perpetual.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The team — which includes Stuart Eliot, Allan Polley and Rita Fung — manages our multi-asset portfolios with a focus on strategic asset allocation, active management and tactical asset allocation.

Investors need to adapt to changing circumstances when building effective portfolios — just as cricketers adjust their style for different pitches. Pendal’s head of equities Crispin Murray explains.

JUST AS CRICKETERS adjust their style for different pitches, so investors need to adapt the way they think to changing economic circumstances, says Pendal’s head of equities, Crispin Murray.

“Cricket is one sport, one set of rules — but very different games,” says Pendal’s head of equities Crispin Murray.

“From the fast-paced pitch at Brisbane’s Gabba to the swing of Edgbaston in England or the spin-friendly wickets of India, cricket teams adapt the way they play to the different environments they encounter.”

So too investors need to adapt to changing circumstances when building effective portfolios, says Murray.

“That’s an analogy I want people to think about. Today we have a very different investment environment, and it requires different strategies in the post-COVID world.”

For example the risk of inflation — a top-of-mind concern for many investors — may be increasing, but sustained price rises are no certainty, says Murray.

“If we see growth picking up, some of that slack in the economy disappearing and inflation picking up — and no response from Central Banks — that’s when you’ll see the market beginning to add to the probability of inflation risk,” he says, speaking to the recent Conexus Financial Fiduciary Investors Symposium.

But when constructing a portfolio, investors need to keep in mind that changes in the probability of an outcome can have a disproportionate effect on the pricing of assets that protect against that outcome.

“There is real value in having inflation hedges in your portfolio because the option value that they give you in terms of that insurance is actually far more valuable today than it would have been five years ago.”

Murray says the world is at a turning point post-COVID as policy-makers turn their attention to reducing inequality, rebuilding domestic capacity and supply chains and transitioning to clean energy.

“We’re early in the cycle, we’re still coming off such a dramatic economic downturn that there is slack in the economy.”

He says equities can play a unique and multifaceted role in portfolios in this kind of climate.

“We’re in a world where returns on other asset classes are going to be very low. Your running yield on bonds is low and the risk is that capital could be negatively impacted.

“Equities can provide a solution there. One of the aspects of equities that we quite like is where we see predictable sustainable, strong cash flow yields.

“In more mature industries, that’s the role you’re asking those companies to play in terms of giving you good yield. People will value that particularly in a zero-rate world.

Also, “equities can provide a hedge against inflation.”

Finally, Murray says investors should not discount accelerating digital disruption.

“I think it’d be dangerous to just ignore growth stocks.

“What makes these companies so valuable — and what I think people have underestimated historically — is that once you get that flywheel moving, and you’re getting scale, the level of capital required to generate growth is actually relatively limited.

“That creates this very powerful value generator for those sorts of companies.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above) and portfolio manager Jim Taylor. Reported by portfolio specialist Chris Adams.

WHILE headline Australian index moves have been muted recently, we are seeing material shifts within the market.

This is fertile ground for active investors.

Inflationary pressures continue to be front of mind for investors. As a result we are seeing rotation away from long-duration deflationary trades such as growth and low volatility/quality stocks towards shorter-duration inflationary trades like commodities and value stocks.

This is supportive for Australian equities relative to markets such as the US, given our higher weighting to commodities and value stocks.

The S&P/ASX 300 was up 0.75% last week and the S&P 500 gained 1.3%.

Covid and vaccines

The tragic situation in India continues to hold attention and emphasises the danger that the virus and its mutations still pose.

Elsewhere there was little deviation from recent trends. New daily cases continue to decline in the US. The EU finally appears to be getting on top of recent outbreaks, demonstrating the effectiveness of lockdowns. EU hospitalisations are also improving rapidly.

With China, the US and EU all showing signs of control we expect the recovery in global growth to remain intact.

More than 60 per cent of Israelis have had at least one dose of vaccine. Vaccination rates remain strong at 45-55%, though there is a question whether this will be replicated in other countries.

The rate of UK vaccinations started to slow after 45% had a jab. The US is at this point now. Surveys suggest about 20% of the population still strongly resists vaccination.

There is now chatter around inducements to encourage the “wait and see” cohort. This issue has implications for the pace of re-opening and needs to be watched.

Economics and policy

The big news last week was the large miss in US payroll data, which showed 266,000 new jobs versus an expectation of 1.1 million. This figure is at odds with all indications for labour demand.

The unemployment rate ticked up to 6.1%, the first increase since April 2020.

Many are pointing to a “crowding out” effect of government stimulus. There is a sense that people have money in their pockets and are delaying job hunting until after summer, confident demand will still be there.

On the positive side, the participation rate increased by 0.2% to 61.7%. The average work week also increased to 35 hours.

Average hourly earnings increased by 0.7%, versus an expectation of no growth. This is especially remarkable given the big job increases came in lower-paid parts of the economy such as leisure and hospitality.

Trends in wage growth are important to watch given their importance for the inflationary pulse.

From a Fed perspective this data stumble inserts a gap into the “string” of strong jobs reports that Fed Chair Powell says is needed to constitute substantial progress toward his goals. This is likely to calm market fears around balance sheet tapering for the moment.

Domestically the federal government flagged that the Budget would continue to be expansionary, with no desire to tap the brakes yet. Spending is likely to be highly targeted, including a focus on social outcomes.

This is in line with a shift in thinking evident in other Western governments.

Markets

Commodities were strong last week, reflecting the focus on inflation. Iron ore rose another 13.2% to US$211 per tonne. Copper gained 3.1% and Brent crude 1.8%.

In equities this translated to strength in Materials (+3.9%) and Energy (+1.9%) while Information Technology (-9.9%) sold off.

This thematic rotation — coupled with the buy-now-pay-later sector starting to cycle the high base effect of sales last year — saw Afterpay (APT) fall 18.9%.

Fellow WAAAX stocks Appen (APX, -21.5%), Altium (ALU, -15.0%) and Wistech (WTC, -10.2%) rounded out the ASX 100’s worst performers last week. Our preferred name in the space, Xero (XRO), held up better than the sector but was down 5.5%.

The health care growth names were also underperformers. Fisher & Paykel Health Care (FPH, -6.5%) and Ramsay Health Care (RHC, -6.5%) were among the weakest. ResMed (RMD, -5.0%) is likely still feeling the impact of a high base effect given the strength in ventilator sales this time last year.

CSL (CSL, -1.2%) bucked the broader trend in health care. Uncertainty over the impact of lockdowns on plasma collection have weighed on the stock over the past year.

Travel stocks took a hit after fresh lockdown concerns in Sydney. Sydney Airport (SYD) was down 4.4% and Qantas (QAN) lost 3.6%. This was against the backdrop of the Covid situation in India, which suggests international travel is likely to remain complicated for longer than many expected.

QBE Insurance (QBE, +7.8%) was the best performer in the ASX 100. It bucked the trend of recent halves and delivered an AGM update that did not downgrade expectations. Instead, management highlighted the supportive environment for growth in premiums, which are up 13% in the past year. IAG (IAG, +4.7%) and Suncorp (SUN, +4.5%) were also strong.

Westpac (WBC, +4.4%), ANZ (ANZ, -3.4%) and National Australia Bank (NAB, +0.5%) all reported last week. Results were generally in line with expectations and confirmed the more benign environment.

The question now is whether the banks can continue to perform without the tailwind of rising yields in the near term. The outlook for costs is a key question in this regard.

Westpac has far more scope here and management grasped this nettle, flagging $1.5 billion of planned reductions to bring the cost base back in line with peers.

Elsewhere commodity price strength was reflected in the outperformers as investors sought inflation hedges.

Copper miner Oz Minerals (OZL) gained 7.4%, contractor Worley (WOR) was up 7.3% and rare earths play Lynas (LYC) moved ahead 5.5%. The diversified majors BHP (BHP, +5.0%), Rio Tinto (RIO, +4.9%) and South 32 (S32, +4.2%) all gained ground.

On the M&A front Apollo upped its initial bid for Tabcorp (TAH, +2.4%) from $3 billion to $3.5 billion. There are now multiple suitors circling with credible bids.

As of Monday morning Star (SGR, -1.8%) had also entered the ring with a merger proposal for Crown (CWN, -0.8%). There is a logic to the proposal including significant synergies. But in our opinion this bid and the existing one from private equity undervalue CWN’s assets.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

PENDAL GROUP (ASX: PDL) today announced it has entered into an agreement to acquire 100% of Thompson, Siegel & Walmsley (TSW), a US-based, value-oriented investment manager, for US$320million (A$413 million).

Established in 1969 and headquartered in Richmond, Virginia, TSW operates primarily in long-only equity (US and international) with US$23.6 billion (A$30.5 billion) of funds under management (FUM).

The acquisition price represents 7.6x 1H21 EBITDA (annualised, excluding synergies) and is expected to be double-digit EPS accretive in the first full year after completion.

Pendal Group Chairman Mr James Evans said: “This is a strategic and compelling opportunity to acquire a highly successful complementary business, which will create immediate value and facilitate our growth opportunities in the US market.

“The acquisition will deliver scale and diversification benefits for Pendal across investment capability, asset classes, geographies and distribution channels.

“The Board believes this acquisition will accelerate shareholder returns and strengthen the diversity of earnings.”

Transaction highlights:

- The acquisition is expected to be double-digit EPS accretive in the first full year after completion.

- Pendal’s consolidated FUM will increase 30% to $A132 billion after the acquisition. Its US client FUM will increase 112% to US$44.7 billion (A$57.8 billion).

- TSW has robust business momentum driven by recent large client wins and strong investment performance. Four out of the six funds (where TSW is the sole sub-advisor) hold a 4/5-star Morningstar rating and rank in the top quartile over the last three-year period.

- The acquisition will double Pendal’s addressable market in the US.

- TSW CEO Mr John Reifsnider will be appointed CEO of Pendal’s combined US business.

- The US$320 million purchase consideration will be funded with a combination of equity, debt and existing capital. Equity will be raised through a fully underwritten placement and — to enable retail shareholder participation — a shareholder purchase plan.

Pendal Group CEO Mr Nick Good said: “TSW is a natural strategic and cultural fit with Pendal and expands our successful diversified business model in the largest equity market in the world.

“TSW is highly complementary to Pendal’s US business, with almost no overlap of investment strategies and clients.

“This will deliver the opportunity to generate new FUM through the expansion of our addressable market in the US and our ability to distribute both TSW and JOHCM products through an expanded global distribution network.

“Both businesses have solid flow momentum and high-performing investment strategies. With this growth profile I believe we will be well placed to take advantage of more opportunities inherent in the positive US economic outlook and increasingly strong investor sentiment globally.”

Highly regarded

TSW is a highly regarded value-oriented investment manager. It has a solid base of institutional and sub-advisory relationships and a track record of strong investment performance. Some 86% of TSW FUM outperformed benchmarks over the past year, highlighting the discernable rotation to value strategies over the past six months.

TSW’s investment capability spans international value, US equity and fixed income.

TSW has an experienced, stable team of 74 employees and a long-tenured and talented investment team of 20, with deep bench-strength across all strategies.

Its recent large client wins are testament to the quality of the team and the momentum of the business. The TSW team are fully supportive of the acquisition and are aligned with Pendal’s values, investment independence philosophy, and its growth aspirations.

Alignment of culture and business models

“Cultural fit is all-important in fund management acquisitions,” said Mr Good. “Both parties have put significant effort into considering compatibility, investment, client approach and alignment and mutual commitment to growth.”

TSW’s CEO Mr John Reifsnider will be appointed CEO of Pendal’s combined US business, taking over the role from Mr Good. Mr Reifsnider will also join Pendal’s global executive committee.

“John is an outstanding leader and the right person to head the combined US business,” said Mr Good. “I have every confidence he will continue to drive the positive momentum that is evident in both companies and seize the new growth opportunities we see ahead of us.”

Mr Reifsnider said: “This is a unique opportunity for TSW to join a strategically compatible and highly regarded global investment management company that is a natural fit and has strong alignment to our investment approach and culture.

“All of us at TSW are thrilled to be joining Pendal Group. We see excellent potential for growth and an exciting future.

“I am delighted to take on the role of CEO of the combined businesses. Pendal has been very successful in the US with an extraordinary 10 consecutive years of positive flows and an enviable reputation in the market.

“Investment autonomy is fundamental to both our businesses and to our success. That match has been a very important consideration for the TSW team.”

Mr Good said: “Pendal’s acquisition of JOHCM was a success. We are approaching this acquisition of TSW with the same intent and focus and are confident that we will be able to implement a seamless transition.”

Equity raising

To fund the acquisition Pendal is undertaking a fully underwritten placement to raise A$190 million through the issue of 27.9 million new fully paid shares, representing about 8.6% of current issued capital.

Details of the offer can be found on Pendal’s shareholder webpage here.

The shareholder purchase plan (SPP) will open on May 17, 2021 and close on June 7, 2021.

The SPP is subject to the terms set out in the SPP offer booklet, which is expected to be lodged with the ASX and sent to eligible retail shareholders following the opening of the SPP offer on May 17, 2021.

Pendal expects to complete the transaction in the September quarter, 2021.

Further details are set out in the investor presentation provided to the ASX [PDF download] on Monday, May 10, 2021.

The investor presentation contains important information including key risks and foreign selling restrictions with respect to the Offer.

This presentation can also be accessed on the Pendal website at https://investors.pendalgroup.com/Investor-Centre.

Webcast details

Pendal will present in relation to its 1H21 half year financial results and the acquisition of TSW today, Monday May 10 at 10.30am AEST. The webcast of the results announcement will be available live at https://webcast.openbriefing.com/7243.

If you wish to view the presentation live via the webcast we recommend logging in 10-to-15 minutes prior to start time.

About Thompson, Siegel and Walmsley

TSW is a US-based value-oriented investment management company, operating primarily in the long-only equity (international and US) and fixed income asset classes with US$23.6 billion of FUM at March 31, 2021.

Established in 1969 and headquartered in Richmond, Virginia, TSW is 75.1% owned by the NYSE listed BrightSphere Investment Group (BSIG), but operates as an independent, autonomous, indirect subsidiary. The remaining 24.9% of shares in TSW are held by TSW current and former management.

TSW has a well-known record in attracting and retaining investment talent, with an average tenure of 12 years among the investment team members.

About John Reifsnider

John has been CEO of TSW since January 2021 and has been with the firm for more than 15 years. He was appointed Co-President of TSW in September 2018 overseeing the day-to-day management of the firm and serving as member of the Board of Managers.

Prior to that, he was the Head of Distribution. He remains highly engaged in TSW’s distribution activities. Before joining TSW in 2005, he was Managing Director at Atlantic Capital Management, responsible for business development and client service.

John started his career in the investment industry in 1990.

John earned his BBA from the University of Toledo, is currently registered with FINRA, and is registered as an Investment Adviser Representative. He is an active volunteer for non-profit youth sports organisations.

About Pendal

Pendal Group is an independent global investment manager focused on delivering superior investment returns for clients through active management. Pendal manages A$101.7 billion in FUM (at March 31, 2021) through J O Hambro UK, Europe & Asia; JOHCM USA; Pendal Australia and Regnan.

Pendal operates a multi-boutique style business across a global marketplace through a meritocratic investment-led culture. Its experienced, long-tenured fund managers have the autonomy to offer a broad range of investment strategies with high conviction based on an investment philosophy that fosters success from a diversity of insights and investment approaches.

Listed on the ASX since 2007 (ASX: PDL), the company has offices in Sydney, Melbourne, London, Prague, Singapore, New York, Boston and Berwyn.