What’s next for inflation? Pendal portfolio manager Tim Hext explains in his weekly Bond, Income and Defensive Strategies report.

Find out more about Pendal’s fixed interest strategies

INFLATION has been this year’s hot topic — but it failed to show up in this week’s Q1 2021 CPI data in Australia.

Underlying inflation was a very tepid 0.3% for the quarter. Headline did better with higher fuel prices at 0.6%.

Inflation generally only really picks up 18 months after a recession ends. This means early 2022.

For now tradable (goods) inflation is coming through, at +1.1% for the quarter. Supply chain shortages globally are impacting. But services are stuck down at 0.4% quarterly, almost the lowest we’ve ever seen.

Housing held down services inflation this quarter. HomeBuilder subsidies have hidden an underlying 2% rise in actual building costs. Meanwhile rents — which recent data had suggested were rising — remained flat.

These should start to pick up in the year ahead as government schemes wind down.

Next month’s budget will be one to watch. If borders were to open next year the housing shortage that was building before the crisis will once again be exposed.

While the RBA may eventually want inflation to reach 2.5% they will have breathed a sigh of relief that it’s low for now.

Next week’s Statement of Monetary Policy will need significant “mark to markets” on the RBA’s pessimistic GDP and employment forecasts. But their inflation forecasts will only need modest upward adjustments.

Importantly, they can hold out till 2024 before inflation reaches target, enabling them to maintain the view that cash rates will stay here till then.

Markets kept modest rate hikes factored in for 2024 and beyond, but took out some of the pricing for hikes before then.

Three months is a long time between inflation prints in Australia so we will look to the US for signs in the next few months.

Stimulus cheques have hit accounts so we will watch the next few prints very closely. The starting point there is higher, so inflation should appear there first.

For now we maintain the view that anything 2% or lower for hedging inflation is excellent medium-term value. It provides insurance against a significant outbreak and realised levels should pay for themselves.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Spotlight on Emerging Markets: A monthly update from James Syme and Paul Wimborne (pictured), managers of Pendal’s Global Emerging Markets Opportunities Fund

- Indian equities outperformed the broader MSCI Emerging Markets Index for the third quarter in a row in Q1 2021, as Indian economic data and company results remained broadly supportive

- But Covid-19 data in India has worsened sharply since mid-March, amid distressing stories of human tragedy

- We remain positive on India for our two-year investment horizon, but we are alert to key near-term risks

- Find out about Pendal Global Emerging Markets Opportunities Fund.

BEYOND the human tragedy, the emergence of a new wave of Covid-19 in India is a clear concern for investors.

Indian equities outperformed the broader MSCI EM Index for the third quarter in a row in Q1 2021, as Indian economic data and company results remained broadly supportive.

We have remained overweight India and this was a positive contributor to performance in March and in the first quarter.

Since then Covid data in India has worsened sharply — and we have all witnessed the distressing results in global media coverage.

Here we provide our view on some of the concerns for India and Indian equities.

In terms of Covid data, our preferred metric is the seven-day moving average of cases (and deaths) per million people, which normalises for reporting practices and country size.

Smoothed cases per million people bottomed at 8 in mid-February, before climbing to 17 in mid-March, 45 at the end of March and close to 100 in the first few days of April.

For context, several other emerging markets have seen a serious deterioration in Covid-19 case data in the last few weeks — often at a much higher level than in India. For example, Turkish smoothed cases per million started March at 100 and rose to about 600 in early April.

The key question is whether India will need to reimpose a strict national lockdown to control infections — as they did mid-2020.

For now, the increase in cases is localised (the state of Maharashtra is about one-third of new cases) and local lockdowns and travel restrictions should slow the rate of growth. Even so, near-term risks are elevated and case numbers in less-affected areas will need to be tightly monitored.

Ultimately, vaccinations need to be the solution.

India is one of the world’s biggest producers of vaccines, and has strong experience rolling out national medical (and other) programs. The vaccination rate picked up strongly in recent weeks to a rate of more than 3.5 million doses/day — although on a per capita basis, this is still well below most developed nations.

Experience in the UK and Israel suggests case numbers can be kept under control once half the population has been vaccinated.

More than 90 million people in India have now been vaccinated. At 100 million people per month, India may be five to six months from that threshold. If the vaccination rate can pick up yet further, that timeline would be shortened.

While there are reasons to be worried about Covid-19, the economy continues to deliver promising data.

All forms of PMI data have been strong in the year-to-date (March Manufacturing PMI, for example, was 55.4). Vehicle sales have continued a strong trend that started in October 2020.

With the central bank remaining on hold and fiscal policy remaining stimulative, the policy drivers of growth remain supportive.

Drivers that have historically limited growth remain benign.

Credit growth has been restrained for several years, while excess liquidity in the banking system has risen to INR 7 trillion.

The trade deficit for February was US$94.4 billion, remaining at around its lowest level in a decade. This suggests plenty of potential for domestic demand to increase without balance of payments stress emerging.

Inflation has picked up on a weaker currency and higher commodity prices, but consensus estimates for the 12 months ahead is for CPI to reach only 4.7%. This should not threaten the economic recovery.

The Covid-19 situation is the most pressing concern.

We remain positive on India for our two-year investment horizon. But we also remain alert to key near-term risks.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

WE CONTINUE to see two key issues for markets following a relatively quiet news week in Australia and the US.

First is the divergence in Covid cases between developed and emerging markets. This could potentially lead to a constrained re-opening, negatively affecting the outlook for global cyclicals.

The second issue relates to the bond market and whether Covid case levels act as a handbrake on the recovery. At the moment economic growth concerns are holding bonds at lower yields and driving rotation back to defensives and growth stocks.

We share concerns that a broad re-opening will happen later than many think – and this could affect the outlook for specific stocks.

But we don’t believe this will stop a sharp acceleration in global growth while the Covid situation continues to improve in the US, EU and China. Receding fears in those regions should encourage yields back towards the 2% level.

Equities should remain supported and in decent shape in this environment. But a number of factors suggest a period of consolidation is likely.

Biden’s capital gains tax announcement prompted some sticker shock. But fears faded on the realisation that there’s a long way to go in terms of eventual outcomes.

The S&P/ASX 300 was down 0.03% last week. The S&P 500 lost 0.11%.

Covid and vaccines update

A spike in Indian cases reminds the world of Covid’s ability to spread exponentially in certain conditions. There has also been a deterioration in developed countries such as Japan and Canada.

This highlights the risk that we will see a two-tier global economy based on access to vaccines. Beyond the human and health implications, this could constrain the global recovery, putting pressure on commodities such as oil and underpinning the fall in bond yields.

There is some positive news out of the EU, where new cases have begun to decline. A recent upturn in the US has also rolled over.

We have not seen a significant wave develop outside of Spring break, rolled-back restrictions and the rise in cases in Michigan. New US cases are down 11% week-on-week and hospitalisations are 3% lower.

There is a view building that the US is getting close to herd immunity. Some 42% of the population has had at least one shot — the threshold at which cases started dropping significantly in Israel.

This includes 54% of the adult population and 80% of the most vulnerable segments. About a quarter of the US population has been previously affected and there is evidence that children (a material part of the unvaccinated portion) are less likely to spread the virus.

Excess vaccines is an issue to watch as the US program begins to slow.

In the past week vaccinations fell from 3.6 million per day to 3.3 million. This was partly due to suspension of the Johnson & Johnson vaccine, but we also saw a 12% drop in the number of Moderna vaccines administered.

This rate should recover as Johnson & Johnson becomes available again. But surveys suggest that the roughly 60% of Americans who actively want the vaccination should have received at least an initial dose by mid-May.

We then need to watch what happens with Americans who want to wait and see (about 20%), those who will take it if required (about 10%) and the remaining 10% who are not prepared to take it at all.

The key question is: when will excess US vaccines become available to potentially direct to other countries.

Now that supply has ramped up, the US should have enough to fully vaccinate 335 million people by May and 395 million by June.

While the US is likely to stockpile a large amount for top-ups, there should be significant scope to direct vaccines to countries in need. This development could emerge in the next two months — and could see a very positive shift in sentiment.

In summary, while the near-term surge in cases is concerning, and weighs on growth expectations, the good news is:

-

- Overwhelming evidence that vaccines work

- The supply chain is ramping up materially

- Current concerns may be resolved in a few months

Economics and policy outlook

US media coverage last week focused on proposed increases to income and capital gains tax as part of the Biden Administration’s American Families package. Details will be put to Congress this week.

Tax hikes are not new news – they were first outlined in Biden’s presidential campaign. The reality is, this is the much more controversial part of Biden’s plan and will encounter a much tougher passage through Congress.

While tax hikes should emerge, they are likely to be smaller than the proposed numbers.

A subtle but important point: it is becoming evident that the prescription drug pricing package will not be included in the American Families Plan. This is likely to be addressed in a separate bill, which is a positive for health care companies.

Markets

US reporting season has been very strong. S&P 500 earnings have continue to see upward revisions. The current trajectory suggests the market is on 20x FY22 earnings. This is full, but much less demanding than the 24x we had been running at.

There is a reasonable potential for markets to consolidate in the near term, though we view this as more a pause than a change in trend.

Key market factors:

-

- Market breadth is very wide with 95% of stocks running above 200-day moving average. As we have pointed out recently, this is typically positive for the medium-term outlook and argues against a material correction. But history suggests a period of consolidation is likely with this many stocks doing well.

- Sentiment indicators are very positive. Again, this is not a reason for a major reversal, but it leaves the market vulnerable to marginal bad news.

- The market rebound is tracking very closely to the post-recession experience in 2009-10 and 1982-84. In both cases a consolidation tended to occur 12-15 months after the trough.

- Economic momentum is now so strong that there is some risk of a near-term fade affecting sentiment. Again, based on history, near-term S&P 500 market performance has been muted following periods when the ISM Manufacturing index has been at its strongest levels.

The one caveat here is that we are in unchartered waters given low rates, strong growth and the shift in policy. However at this point we see some near-term consolidation as the most likely outcome.

In another healthy sign, we are seeing speculative froth ease off. Indicators such as the Tesla stock price, IPO and renewable energy ETFs and speculative tech names have all rolled over since early February.

The crypto space had been holding up, but there are signs the Coinbase IPO may have marked a peak – at least in the near term. Bitcoin peaked at about US$64K on the same day and is $52K at the time of writing.

Our sense is that liquidity, which is still abundant, is being deployed into the real economy. This is a positive sign and supportive of recovery.

Overall markets were quiet last week with bond yields and equities effectively flat. It’s interesting to note that commodity prices are holding up despite the fall in bond yields in recent weeks.

Iron ore, for example, was up 4.4% for the week and 12.8% month-to-date. This suggests bonds are being bought for portfolio insurance, rather than on a prevailing view that growth is about to disappoint.

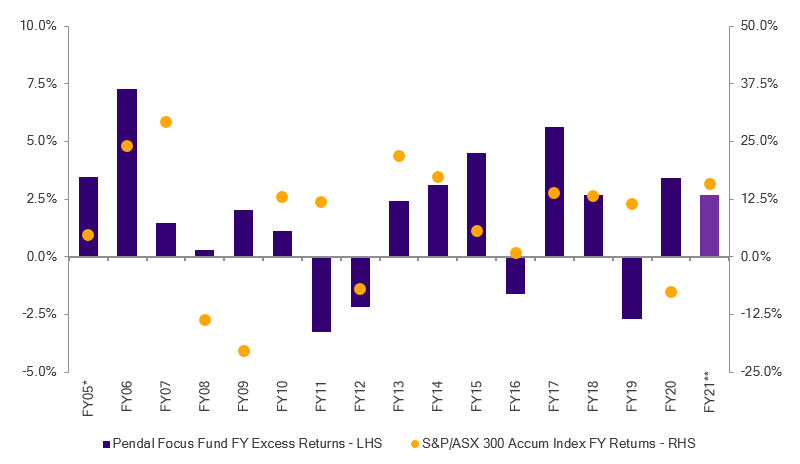

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

This week Canada’s central bank become the first to signal its stimulus exit. Pendal portfolio manager Tim Hext explains what it means for Australian investors

- Vimal Gor: Bond sell-off looks to have run its course

- Vimal Gor: how to think about the role of bonds in a portfolio right now

- Find out more about Pendal’s fixed interest strategies

WE WOKE on Thursday to headline news that the COVID economic crisis was over — even as the health crisis worsened in some parts of the world.

The Bank of Canada (BoC) released its monetary policy report — becoming the first to signal its stimulus exit.

So what has Canada done? Have we moved past the economic impact? If so, what does that mean for Australian investors?

The BoC is paring back the level of bond purchases in its Quantitative Easing (QE) program from Wednesday. It’s a sign the BoC no longer thinks it needs to prop up the economy.

The numbers have been encouraging. The March 2021 CPI increased 2.2% against the COVID lows of March 2020. The February 2021 CPI print was up 1.1% against pre-COVID price levels of February 2020.

There is confidence in the Canadian recovery based on the economic data post-lockdown.

There were substantial job gains in February and March. Stronger commodity prices. Fewer business insolvencies coupled with high business confidence. And a rapid surge in house prices: 17% across Canada and 20% in capital cities such as Toronto.

It is almost a mirror image of our own recovery here in Australia.

Now the question is: will the RBA taper as well? And if so, when?

It isn’t surprising that the developments in Canada sparked a flurry of discussions. But it turns out we have forgotten to read the pesky fine print. Again!

In Australia, the RBA’s main objectives are:

- Inflation between 2% to 3%, on average, over a business cycle

- Full employment

- Stability of the Australian currency

In Canada, the BoC has a single objective to hit a 2% inflation target — not over a business cycle, but at a point in time. There are no unemployment objectives. No currency objectives.

The BoC prefers not to walk, talk and chew gum at the same time.

The similarities between Australia and Canada’s recovery may seem uncanny (although Australian housing prices have risen only a mere 6% compared to Canada’s 17%).

But there are stark differences.

The BoC has shown more willingness to tackle inflation while there is still a fair amount slack in the Canadian economy. In contrast, the RBA is reluctant to dampen growth until our unemployment numbers are into the lows 4s.

Additionally, with the AUD/USD currently range-bound between 0.75 and 0.8, it’s difficult to see the RBA charting a similar course to the BoC.

Until the pied piper of inflation plays his tune, it appears unlikely the RBA will be lured away from its current path.

Maybe keep the champagne on ice just a little longer.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

THE COUNTERTREND bond rally continued last week, pushing down yields and supporting a continued recovery in growth and defensive stocks.

It is worth noting the market overall has risen in both environments. The ASX 300 was up 4.2% in Q1 when yields were rising and it is up another 4.2% quarter-to-date with yields falling.

This highlights the market’s breadth. The laggard sectors have held up reasonably well in both the value and growth-dominant legs, allowing the overall market to rise. This reflects high levels of underlying liquidity and the continued chase for returns.

The S&P/ASX 300 gained 1% for the week and the S&P 500 was up 1.4%.

The question now is how long the bond rally phase can continue. More on that below, but at a high level we believe the move lower in yields will be limited and bond yields are likely to return to their higher levels within three months.

The bond market rally

There have been five key drivers of the recent rally in bonds, in our view:

-

- Positioning: There was a strong consensus position and very crowded trade long recovery and re-opening plays and short defensive assets like bonds in Q1.

- Yield differential: The yield pick-up for European and Japanese investors buying US treasuries hedged back to domestic currency was at its highest levels for five years.

- Peak growth approaching: In terms of the second derivative – the rate of growth — this peaks in April and early May and slows thereafter.

- Covid spike: Cases are picking up in US and big emerging markets such as Brazil, India and Chile. There are also renewed fears about Covid variants.

- Vaccine safety concerns: The Johnson & Johnson vaccine has now also been linked to blood clots, leading to a temporary suspension in the US.

Covid and vaccine issues

Looking at points four and five above, we believe there are some material medium-term risks for the management of Covid and full global re-opening. But the near-term trends are supportive enough to avoid any breaking down of the current re-opening economic recovery.

In the EU new daily cases remain elevated. The seven-day average is more than 300 people per million compared to fewer than 200 in the US and about 100 in the UK. There are signs this number is stabilising in the EU.

Brazil is surging and is now running just ahead of the EU. Given low rates of testing there, the real number is probably 50% more.

There is some focus on Manaus where some 70% of the population already had Covid — but people are being re-infected with the Brazilian strain (P1). This highlights concerns with the duration of immunity.

Adding to the confusion a new double mutant strain has been reported in India. So far no one knows if it is more resistant to vaccines.

Regarding the surge in Covid cases, the key point is we will achieve herd immunity later than many expected. The outlook for emerging markets in particular has declined. This means a more subdued medium-term global re-opening recovery, which means monetary policy remains looser for longer.

Vaccine duration

The debate over how long vaccines remain protective is important in this context.

Pfizer released data indicating the average effectiveness of its vaccine was 91% over six months. While ostensibly a good number, given it starts at 95% this implies effectiveness is falling into the 80s by the end of the period.

This is backed up by studies showing the presence of relevant antibodies has fallen by two-thirds (for people in the 18-55 year cohort) over that period. For people in the older age cohorts, the degree of antibody decrease is greater still.

This still leaves enough antibodies for the vaccine to be considered effective against the original strain after six months, although for people above 70 years old it is getting closer to the cut-off mark.

However it’s believed the degree of relevant antibodies is deflated by a material factor in the case of the South African and Brazilian variants. It’s unclear if older populations would still be immune after six months.

There is a degree of complexity in measuring the presence of antibodies and rates of decline, particularly among different types of vaccines.

There can be no conclusion on the Covid outlook at this point, but we can make some inferences:

-

- Covid is likely to remain an endemic disease like the flu. It will remain prevalent and disease management will be an important focus.

- Re-opening international borders is likely to be more complicated than expected. New variants are one issue. So is the fact that we will have people with different vaccines received at different times. There is no homogenous standard to assess people’s risk of getting the disease.

- The need for booster shots will continue for some time. Hence Pfizer’s comments regarding the need for a third shot.

The investment consequences of this are complex. One outcome is a dispersion in performance within cyclicals in the US. Domestic cyclicals are outperforming global cyclicals given the issues in both the EU and emerging markets.

Positive near-term news on Covid

These are all medium-term issues. In the near term, developments have been positive on balance, despite the issue with the Johnson & Johnson vaccine.

In Europe, vaccination rates are now dialling up and supply issues are being resolved. The EU is about two to three months behind the US in terms of the vaccine roll-out.

At this point the increase in US Covid cases remains relatively muted, despite a sharp spike in Michigan. The vaccination rate remains at record levels and more than 80% of over-65s have had at least one shot.

The manufacturing capacity of the Moderna vaccine looks set to meet demand requirements. This helps alleviate concerns with other vaccines, though it has run into some supply issue outside the US. At this point we expect concerns over vaccines — which have helped drive bond yields down — should not persist.

Economics and policy outlook

Returning to drivers of the recent bond rally, we believe the strength of the economy will prove more durable than the market expects.

Therefore the peak growth argument for buying bonds will not be sustained.

Data suggests the US economy is booming and this is flowing through into the rest of the world. Consumer spending is at record levels, supported by a surge in consumer net worth and the economic re-opening. The question is how sustainable this is, in the context of an expected peak in the next month.

Our first observation is that the increase in net worth extends well beyond the top decile by wealth. The top 10% of the US by wealth has seen a total 30% increase in net worth, but the next 40% have seen a 33% increase. This is important because it includes income groups that are more likely to spend than save.

This is flowing through into spending plans. Recent survey data asking about expected spending one year out has surged, indicating that consumer spending could extend for longer than expected.

Another reason is that we are seeing household net worth rise at the same time that household debt has fallen materially — from about 105% of GDP to about 75%. The starting point for the savings rate is also very high.

This is fundamentally different to the post-GFC era. Then households had run down savings rates and built up debt, so consumption faced a double headwind as savings rates rose to repay debt. The opposite could happen this cycle.

Meanwhile we are in an environment where households are still covering their spending with wages, ie they are still not eating into the estimated US$3 trillion of excess saving.

In addition, companies are reporting record low levels of inventory as they struggle to meet demand. This suggests they will need to re-build inventories in future quarters. Some of this is being constrained by supply bottlenecks (eg in auto), so this also helps extend the cycle.

Housing also continues to boom. Low rates are a cyclical tailwind, but structural factors are just as important. Housing formation declined materially post-GFC. We are now seeing a supply response to address the current underbuild, which is also supported by aging Millennials and the work-from-home trend. This provides a more sustainable platform for on-going economic strength.

The point here is that the expectation of a peak in growth, as a driver of recent bond strength, is more about sentiment. We expect continued economic strength, evidence of supply chain bottlenecks and some emerging inflation pressures in the next here months.

In this environment it is hard to see real rates staying at -1% and anchoring bond yields at current levels.

Markets

There are a few broad observations on equities at this point.

- The correlation between the yield curve and performance of defensives versus cyclicals and growth versus value has been very clear in recent weeks. If we get a reversal in recent bond rally we should see the value and cyclical trade resume.

- Equity market volatility continues to be supressed. This is worrying some people who believe it’s being held down artificially by central banks. If it continues this should help bolster confidence in equities. It also potentially encourages more equity positioning in risk parity strategies.

- There is not yet any negative signal from credit spread, which have hit post-GFC lows. We see this as correlated with equity valuations.

Last week we got the trifecta of bonds, commodities and equities rallying together. The US dollar also began to roll over, which supports commodities.

Australia, like the rest of the world, last week saw growth stocks lead in what was otherwise a broad rally. Names like Xero (XRO, +5.9%), CarSales.com (CAR, +5.1%), Afterpay (APT, +4.9%), NextDC (NXT, +4.5%) and Wisetech (WTC, +3.8%) were among the best performers in the ASX 100.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Sustainable investing leader Regnan has analysed the environmental impacts of hydrogen production in a new research report aimed at investors.

Regnan’s H2 beyond CO2 report reviews popular hydrogen production technologies and identifies factors that may lead to competitive advantages and potential constraints.

The report — produced by Regnan’s Abby Frank, Alison George, Maxime Le Floch and Oshadee Siyaguna — can be downloaded here.

-

- Hydrogen production shows strong potential for investors but there are issues to be managed

- Investors can identify key factors that will influence winners and losers

- Listen to an interview with the report’s authors on Decarb Connect podcast

- Find out more about Regnan or contact Jeremy Dean at jeremy.dean@regnan.com

THERE’S a lot of excitement among investors, scientists and politicians about the scope for hydrogen to be a major energy source of the future, based on its potential contribution to decarbonisation goals.

But there is still a long way to go before hydrogen can be considered a practical alternative to traditional energy sources such as gas.

The conundrum for the world economy between now and 2050 is to reach net-zero emissions while providing enough energy to meet demand from an expanding global population.

This energy transition is at the heart of the United Nations’ Sustainable Development Goals (SDGs), the global agenda launched in 2015 to tackle the world’s toughest environmental and social challenges.

In theory, hydrogen could be used as a fuel for transport and power, as heat for industrial processes and buildings, and as a feedstock for chemicals like fertilisers and industrial products like metals.

In practice, hydrogen’s appeal is difficult to judge.

Hydrogen production needs to be assessed across all sustainability dimensions. Investors and companies are wary of locking into a technology only to find problems later on.

This happened with earlier generations of biofuels and liquified natural gas, all of which were initially promoted as impact solutions.

“It’s a relative game between low-carbon technologies,” says Maxime Le Floch, an analyst with sustainable investing leader Regnan.

Mr Le Floch is a contributor to H2 beyond CO2, a new Regnan research report that examines the environmental impact of hydrogen production for investors.

He is part of a London-based team that manages the Regnan Global Equity Impact Solutions Fund, which aims to generate market-beating, long-term returns by investing in solutions to the world’s environmental and societal problems.

Hydrogen’s potential

“Hydrogen is competing against other technologies for decarbonisation in different parts of the economy,” Le Floch says.

“New hydrogen fuel vehicles have been touted, though with the pace of progress of electric vehicles, hydrogen becomes less likely there. But in other applications like heavy industrial and steel-making, hydrogen might be very interesting.

“We need to keep in mind that these are very long investment cycles, so decisions made today have an impact in 10, 20 or 30 years time. There is a whole carbon cost curve that shows where different solutions stack.”

Growing support for investment in hydrogen technology needs a dose of scepticism — not because the enthusiasm is wrong. It’s just too early to say it’s correct.

“The nature of the investment process within the Regnan Global Equity Impact Solutions team is very comprehensive,” says Regnan’s head of research Alison George, a co-author of the report.

“It’s not just looking at SDGs, but all of the environmental and social impacts. Hydrogen might look attractive, but what are all the implications?”

Key economic, environmental and social issues associated with H2 production. Source: Regnan

George says when researching hydrogen, the economics are discussed constantly, and decarbonisation is talked about some of the time. “But there were gaps in the environmental case.”

“We needed some of these questions answered to determine if it was suitable for the fund. It was really a process of trying to fill some pretty surprising gaps,” she says.

The result was H2 beyond CO2, a report that looks beyond carbon emissions analysis alone.

The report can be downloaded here.

“The entire approach of the fund is to find solutions to the grand problems of sustainability and that approach informs investment decisions. There’s a preference for solutions with the greatest contribution to make, and the clearest pathway to making a difference,” George says.

Key hydrogen production technologies

The report concludes that climate change benefits can be achieved through both green hydrogen and blue hydrogen, but with some important caveats.

For green hydrogen, which is made with electricity, the energy source drives the climate outcomes and the majority of other environmental impacts.

An answer, potentially, is to couple electrolysers with intermittent renewables like wind and solar to help manage output peaks and avoid generator curtailment.

That would support growth in renewables and improve the economics of hydrogen production as well as maximising the contribution to climate goals.

“Few of us have been asking the right questions… this report gives essential answers on the sustainability of climatetech” – Alex Cameron, Decarb Connect podcast

Blue hydrogen has the potential to be a sustainable and economic option for hydrogen production — particularly in regions with local natural gas resources, existing pipelines and transport infrastructure.

But it relies on successful carbon capture and reliable carbon storage. They must be maintained for longer periods to be climate effective.

The Regnan report shows there is much more work to be done in the field of hydrogen.

“Some solutions look great on paper but when you scrutinise the environmental impacts things start to get more nuanced,” Le Floch says. “There’s a great need for more research.”

Case study: hydrogen production with offshore wind

Almost 200 years ago, physicist Hans Christian Orsted discovered electromagnetism, and changed the course of history.

Orsted laid the foundation for the modern generation of electricity, and his name is now synonymous with energy in the Scandinavian countries. Orsted, the company, is the biggest offshore wind developer in the world.

Orsted is one of the few global companies able to generate huge amounts of energy through its offshore wind projects across Europe and in Taiwan. It is a critical piece of the renewable energy puzzle, and not just in terms of wind.

“If you want to decarbonise hydrogen production then you need large sources of energy,” says Regnan’s Maxime Le Floch.

“You can take electricity from the grid but that does not always work. So this is why developing hydrogen production with offshore wind makes sense and projects are being announced.

“Offshore wind projects are on a big scale – and scale is a challenge for other sources of renewable energy like onshore wind and solar,” Le Floch says.

“We are talking about gigawatt scale projects in the North Sea, for instance.”

It demonstrates the necessary links between different energy sources, if renewable power is to reach its potential. It also highlights that companies that could benefit from greater use of hydrogen don’t necessary sit in that sector.

“Orsted is getting involved in exploratory projects around hydrogen and much of the work is to demonstrate that the technology can work,” Le Floch says.

About the authors

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

Oshadee Siyaguna is a senior ESG analyst with Regnan, responsible for research and engagement and the generation of analysis and insights on ESG themes and issues. Oshadee joined Regnan as an ESG analyst in 2015. Prior to that he was Assistant Vice President at PolitEcon Research.

Abby Frank is an ESG analyst with Regnan, responsible for research and engagement and the generation of analysis and insights on ESG themes and issues. Abby joined Regnan in 2018.

Maxime Le Floch is an investment analyst with Regnan’s Global Equity Impact Solutions team. He has a decade of experience in sustainable investment. Maxime previously worked as an investment analyst at Hermes where he helped manage Hermes Impact Opportunities Equity Fund and led the integration of ESG and stewardship across investment strategies.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems, while the Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

MARKETS remain supported by strong economic data. The S&P 500 gained 2.76% last week, while the S&P/ASX 300 was up 2.52%. Market breadth remains high.

It was interesting to see mega cap growth in the US stage a comeback of sorts.

We are mindful that a stabilisation in bond yields could lead to a valuation re-rating of the defensive/healthcare sectors. The consensus trade of rotation from defensives into cyclicals that benefit from the reopening feels like it has run its course to some degree.

Covid-19 and vaccines outlook

It’s generally more of the same in regard to new cases and vaccines.

We are keeping a close eye on an increase in new US cases, particularly given our exposure across materials, housing and gaming there.

Concerns over the impact of a new wave of cases on lockdowns and restrictions appear to have stabilised. Sentiment has been helped by the vaccination program (now running at 3 million new doses daily) and record highs printed in economic indicators. Hospitalisation rates remain under control.

New daily cases in France and Germany continue to improve. But their vaccination programs continue to run well below that of the UK and US. Almost half the UK population has now received one dose. In the US it’s 35% and in Germany 15%.

France brought in additional restrictions last week, but our position in Atlas Arteria (ALX, +1.85%) rose nevertheless.

Economics and data

The March US ISM Services index came in at 63.7, up from 55.3 in February. This is a record high and reflects the impact from stimulus payments. It is yet another indication that the US economy is running hot.

The Fed continues to jawbone the market, attempting to convince all that they won’t change tack and raise rates in response to near-term inflationary pressure.

At this point the market is giving it the benefit of the doubt. As a result US bonds remained stable — 10-year Treasury yields fell 1bp. The Australian equivalent fell 8bps to 1.76%.

The RBA provided commentary on housing. We remain mindful of the risk of macro-prudential measures, particularly for the bank sector. These do not appear imminent given current data on investor participation and affordability.

Markets

The US dollar index (DXY) weakened slightly last week while most commodities were up. Iron ore rose 3.7%, copper 1.2% and gold 1%.

Brent crude fell 2.9% despite oil inventories reaching six week lows, following OPEC’s decision to gently increase supply. It is up 21.5% for the calendar year-to-date.

Our key consideration at the moment is the changing shape of the rotation thematic within the equity market.

In most markets that have had a reasonable run in the last 12 months, the constituents of the “momentum” and “value” buckets have changed quite materially over the last quarter.

Generally the (non-materials) cyclical stocks that used to be the considered “value” have now become the momentum stocks. There is a developing argument that some of the high-flying growth stocks that have underperformed in recent months are now looking relatively attractive.

This could be yet another material shift in the market drivers. There is a high degree of uncertainty which emphasises the importance of having a balanced, non-binary approach to portfolio construction in this environment.

A combination of stabilisation in treasuries and a moderating rotation in the market was generally supportive for equity indices in aggregate.

Only eight stocks in the ASX100 fell last week. AMP (AMP, -4.9%) fell furthest as the company announced the CEO’s departure following weeks of speculation. Disappointment in the effort to realise value via asset sales seems to be a key factor.

Chemical and explosives company Incitec Pivot (IPL, -3.8%) fell after management announced its Wagaman ammonia plant in the US would be offline for longer than expected. Earnings downgrades were in the order of 10%.

Afterpay (APT, +15.1%) was the best performer in the ASX 100, consistent with the better performance from large-cap tech growth stocks in the US. This reflects our view that the recent thematic rotation may have run its course for now.

Our preferred exposure to tech growth, Xero (XRO), gained 6.1%. Other growth stocks such as Seek (SEK, +8.8%), REA Group (REA, +8.7%), and Carsales.com (CAR, +6.9%) caught a bid.

Gold miners Northern Star (NST, +11.2%), Evolution (EVN, +9.1%) and Newcrest (NCM, +6.6%) benefited from a shift back into more defensive areas.

Cleanaway (CWY, +12.3%) made a bid for the Australian-based assets of global waste management group Suez. Suez is subject to a hostile takeover bid on the Paris bourse, which complicates the deal. Nevertheless the market responded well to potential domestic industry consolidation.

It is worth noting the scale of mergers and acquisitions activity in the market. Globally, M&A activity is running at about US$900 billion in 2021.

This is already higher than the total for any year in the past two decades. We suspect there is plenty more to come in 2021 as confidence in the recovery grows.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

EQUITY MARKETS shrugged off concerns over rising Covid cases in the US and in Europe to deliver further gains last week.

The theme of stronger growth — underpinned by yet more encouraging data from the US — seems to be winning.

While there was disruption in the wake of failed hedge fund Archegos, it was felt mainly at a stock-specific level rather than as a broader market event.

The S&P/ASX 300 delivered a 0.63% gain last week, while in the US the S&P 500 was up 2.8%.

Covid and vaccine outlook

There are some localised surges in new Covid cases in the US. Michigan provides a case in point. The 7-day rolling average of new daily cases there has almost returned to the peaks of Q4 2020 as the UK strain spreads. Nevertheless, a national bounce in cases remains relatively muted.

Europe is still struggling to contain a rebound in cases, though there are early signs the surge may not be as bad as previous waves. The impact on sentiment is ameliorated by stronger economic data.

There is a pick-up in the US hospitalisation rate. But at this point the consensus is this will be a mild wave which will not require significant new restrictions. This risk does need to watched, however, given the market’s current appetite for re-opening stocks.

Vaccinations in Europe have begun to step up and are on course for 50% penetration by July.

US vaccinations continue to break new records and are now running at 2.7 million shots a day. Vaccine production capacity is set to rise 50% in April, allowing further acceleration. Almost 40% of the population has been vaccinated.

Economic data remains strong

Economic data continues to demonstrate the strength of the US economic rebound. March payroll data showed 916,000 new jobs versus a consensus expectation of 660,000. Payroll data for the previous two months was also revised up 156,000.

Total US employment, having stalled in recent months, is now accelerating again. The pace of recovery is in stark contrast to post-GFC. It took five years for employment to regain pre-GFC levels. At the current rate, that mark would be reached in 2022. This underpins our view that current policy settings are partly a response to the perceived economic and social failures of the response to the GFC.

There remains a large gap with pre-Covid employment — about 11 million jobs. This helps hold wage inflation in check for the short-term at least.

But if the recovery continues at its current pace it is hard to see the Fed holding to their stated position of no interest rate increases until 2023.

Consumer spending is strengthening in the wake of stimulus payments. In the April 2020 stimulus round, recipients spent about 65% more at the peak than those who did not receive a cheque. In January 2020, the peak rate was only about 30% more. This package looks more like the first one — peaking in the week following cheques at around 58% more. Consumer confidence indicators are also breaking higher.

The US Purchasing Managers Index (PMI), a gauge of sentiment in manufacturing and services, remains elevated at around 65 (on a scale of 1 to 100). The record is 70, achieved in the mid-1980s. Business confidence in Europe is also rising according to surveys, despite a surge in new cases.

More detail emerges on US policy

The Biden administration revealed more detail on the proposed infrastructure package, “The American Jobs Plan.”

It proposes US$2.2 trillion spending, largely in line with consensus expectations. Traditional “hard” infrastructure would account for US$1.7 trillion. The remaining US$500 billion would be allocated to social support policies to address issues such as inequality.

The near-term impact is likely to be less muted than the headline figures suggest, given the spending is extended over a number of years.

Debate over how it is funded — given the need for higher taxes — will be a key area of focus in the near term.

Market outlook

There was some concern that banks selling down positions to help cover the impact of failed hedge fund Archegos would trigger a broad market impact in the vein of Long Term Capital Management (LCTM) in the late 1990s. Total losses from Archegos look to be US$6-8 billion and have hit a number of banks very hard.

Some second-order effects may emerge. At this point associated sell-downs have been seen in specific stocks, but have not destabilised the broader market. The off-setting effects of abundant liquidity and confidence in recovery are holding sway.

Market breadth remains a supportive factor for equity markets. Some 94% of stocks in the S&P 500 are above their 200-day moving average. This is more than at any point since May 2013.

This doesn’t mean we can’t see a correction or consolidation – but it makes it less likely that we are at a market top. A typical sign of extended market tends to be narrower and narrower markets in terms of drivers – and we are clearly not at that point.

Inflation remains the key risk that can de-rail markets.

There are signs of inflationary pressure in specific areas in supply chains. The issue is how quickly – and to what degree – this flows through to wages. The link to wage inflation has not been present for the past 20 years – and we are a long way from employment capacity. Nevertheless, this remains an important factor to watch.

Bond yields edged upwards in the US. The 10-year Treasury yield rose 4bps to 1.67% on the back of stronger economic data. The Australian equivalent rose 16bps to 1.84%.

The US dollar rose another 0.4% as measured by the DXY against a basket of currencies. It is now up 3.3% over the year-to-date, helped by the strength of recovery relative to places such as Europe.

This has weighed on commodities in recent months, although iron ore gained 3.9% last week. Brent crude also rose — up 4.7%, helped by signals that OPEC would continue to be restrained in supply in response to increased demand.

Australian equities recap

Cyclicals such as Materials (+2.7%) and Industrials (+1.6%) tended to outperform on the ASX last week. Confidence in re-opening persisted despite a snap lockdown in Brisbane.

Construction-related stocks continued to perform well on strong housing demand. BlueScope Steel (BSL, +7.4%), Boral (BLD, +7.1%) and James Hardie (JHX, +6.4%) were among the best performers in the ASX 100.

Miners also caught a bid. Mineral Resources (MIN, +6.9%), which has exposure to both iron ore and lithium, was the best of them in the ASX 10, followed by Alumina (AWC, +5.0%), South32 (S32, +4.8%) and Fortescue (FMG, +4.3%).

AGL (AGL, -6.3%) was among the worst performers. It seems the more the market worked through the detail of the proposed demerger, the more it highlighted the limited value in the stock at current levels.

Tabcorp (TAH, -3.5%) gave back some recent gains as it announced a review of its business, potentially delaying a break-up off the company and possible sale of the wagering business. At this point we still expect a demerger of the lotteries and wagering business to be the most likely outcome.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Bonds look like great value after a sell-off that appears to have run its course, argues Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor (pictured)

- Bond sell-off a ‘credibility test’ for central banks

- Reversal of decades of falling inflation unlikely

- Bonds look good value

- Find out about Pendal’s fixed interest strategies

RECENT instability in bond markets is shaping into a credibility test for central banks, but Pendal’s Vimal Gor cautions investors against expecting a reversal of the deflationary environment of the past few decades.

A sharp sell-off in bond markets in recent weeks has sent the yield on US 10-year treasuries above 1.7 per cent from scarcely over 1 per cent a few weeks ago.

Gor, who leads Pendal’s Bond, Income and Defensive Strategies team, says the sell-off indicates a divergence between the views of the markets and central banks.

“What it’s telling you is the market is questioning central banks’ credibility,” he says, speaking at last week’s Conexus Fixed Income and Private Credit Forum Digital event.

“They’re questioning both their forward guidance and their willingness to stick to quantitative easing packages.”

Reflation not inflation

Still, Gor cautions against expecting a reversal of the deflationary environment of the past few decades because the demographic and technological drivers of lower prices have not changed.

“I think it’s more reflation than inflation,” he says.

“We know inflation is going to be higher over in the next few months” because it will be compared to the lower prices seen during the heights of the COVID pandemic. “But it’s a very big ask to expect the deflation environment to have come to an end.

“So yes, there is a short run pickup in inflation, which is pressuring bond yields higher, but I question whether that narrative is going to run much further.

“If anything, bonds look great value to us now.

“I think that the sell-off in bonds has largely run its course.”

QE risks for markets

Gor raises questions over the long-term risks of quantitative easing (QE) for markets, saying that central banks determination to hold bond yields down is artificially lifting the price of every other asset.

“Historically, the way yield curves worked is the central bank sets the short-term interest rate, which has an effect on the very short end part of the curve and has less effect as you go up the curve as that’s driven by supply and demand.

“So the front end is locked, the back end moves around.

“Now the central bankers are telling you they want to control the entire yield curve.

“Effectively, they’re telling you that the central bank knows better than the private sector where the price of credit and interest rates should be.

This limits the returns available in government bonds and forces investors to seek a return elsewhere.

“If you hold bond yields down artificially… it has impact on every other asset. Everything from private equity to venture capital to SPACS [special purpose acquisition companies] to real estate – every asset in the world is largely a derivative of a central bank.”

Cryptocurrency role in portfolios

The risk inherent in QE means investors should consider seeking out defensive alternatives to bonds as they construct portfolios, with cryptocurrencies like bitcoin a potential supplement to bonds.

“If I was to say to you ‘sell all your government bonds and buy crypto’ well that’s a ridiculous statement and I’d never say it.

“But instead of owning 100 per cent of your defensive assets in government bonds … how about you think about utilising other strategies and at times utilise crypto because they do have positive characteristics that you find it very few other assets.

“So were you to utilise them at the right time, they would add significantly to your defensive portfolio. That’s how we approach it.”

About Vimal Gor and Pendal’s Bond, Income and Defensive Strategies (BIDS) boutique

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, Vimal oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Vimal sets the strategy, processes and risk management for the boutique and all funds managed within it.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

RECENT trends persisted last week.

On the negative side new daily Covid cases rose in the US as mobility increased with the warmer weather. European numbers also continued to surge higher.

Bond yields were more stable, although there was more selling on Friday.

This is balanced with optimism around the stimulus and pent-up demand as vaccine penetration improves in the US and UK. There are also signs of the wealth effect supporting spending on housing market strength.

The bearish argument is that economic momentum peaks in the next month with strong growth already priced in and the emerging risk of another Covid wave affecting demand.

The bull case is that the market cycle continues, supported by a strong economy, even as the momentum of growth slows. This is supported by the notion that we are in the early phase of the recovery, with corporate earnings picking up and no sign of tightening.

We are in the latter camp at this point, though our portfolio positioning reflects our view that we must be mindful of material risks. We do think market leadership will continue to shift. We are already seeing the more speculative growth names continue to underperform in the US.

The S&P/ASX 300 gained 1.7% last week, while the S&P500 was up 1.6%.

Covid and Vaccines outlook

Localised outbreaks in New York, Michigan and Pennsylvania pushed up total US new daily cases by 8% week-on-week.

In New York an estimated 20% of cases are the E484K mutation (seen in the Brazilian and South African strains) which is less responsive to the vaccination. A further 40% have the B117 (UK strain) variant.

A variant-specific vaccine will be trialled in early summer and may be available by September.

The key risk is that case levels remain elevated due to these strains, which could impact sentiment and activity. This highlights the complexity of re-opening international borders later in the year.

It will be important to track US hospitalisations which tend to follow case numbers with a lag of one to two weeks.

Pressure on the medical system has eased and is not an issue now, given the penetration of vaccinations in the over-65 age cohort.

Vaccination rates in the US should ramp up with increased supply, allowing jabs for 3-4 million people daily. It’s expected that two-thirds of the US population will be vaccinated by the end of April.

Europe’s vaccination rate is now running two months behind the UK. Daily vaccination rates are trending down in France and Germany and rising cases are leading to further lockdowns. This is affecting markets, weighing on the price of oil. Continued issues in Europe could also help support the US dollar and bond market.

Economy and policy outlook

April could be the strongest month for US economic growth that we see in our working lives.

The effective stimulus distributed in March is the equivalent of payments in April 2021. There are signals of strong pent-up demand while the surge in equities and house prices is contributing to the wealth effect.

All this is very supportive of likely consumer spending, underpinning corporate earnings. Data is likely to be strong, perhaps bringing more pressure to bear on bonds.

As this initial surge passes, the question is whether it will signal a temporary high in bond yields. If so, we are likely to see some rotation back to yield-sensitives in the equity market. This is an important question in terms of portfolio construction.

There was debate over the US infrastructure Bill last week with a desire to put more longer-dated stimulus in train to help offset the drag as the current packages expire next year. At this point there is talk of US$3-4 trillion spread over ten years. This may be put to Congress in two packages.

One package could focus on mainly physical infrastructure, which would likely attract bipartisan support. The other, more progressive package could focus on other equality-focused measures and be passed via the budget reconciliation process.

We are also keeping an eye on the debate over tax, which has implications for earnings and specific sectors. The Biden tax proposals equate to about US$2 trillion, including an increase in the corporate tax rate to 28%.

If fully implemented these measure would be a 6% hit to S&P500 earnings.

There are also initiatives to change taxation for companies earning offshore, which may surprise the market. Pharma companies are likely to come in for specific proposals.

Higher taxes are coming but the current package is likely to be watered down. The corporate rate may be lifted to 24-25% with end impact closer to 3-4% of corporate earnings.

Debate over the filibuster is shaping up as a major issue in the US.

If materially watered down this will open the door for far more Democrat policy agenda — leading to greater spending on environmental issues and higher regulation. This could lead to higher US bond yields and a weaker USD.

Markets outlook

US 10-year government bond yields stabilised last week, though they rose on Friday after chatter about further stimulus measures. The USD continues to grind higher, encouraging some rotation to more defensive names.

Currency strength and stable yields are potentially driven by the carry now available in US bonds for foreign investors, given the low cost of capital.

We see a battle emerging between this liquidity support versus the reality of growth and rising inflationary pressure.

The virtuous circle of liquidity that helped support speculative tech names in the US may be unwinding. It looks as though not as much of the stimulus is being invested in the market.

People are also getting outside, meaning there’s less time to day trade.

The proxy here is the ARK Innovation ETF — and by association Tesla — which are down 27% and 30% respectively from their highs. ARK in particular could be hit hard if outflows accelerate.

Australian equity strength was broad based last week. We saw more high-quality defensives join the rally, having lagged year to date.

TPG Telecom (TPG, -7.4%) was the weakest stock in the ASX100 after news that founder David Teoh was stepping down as Chair. The reason was not disclosed. He retains a 17% stake in TPG, with 80% of this held in escrow until the end of June 2022.

Teoh is regarded as the architect of TPG’s historically aggressive approach on pricing. So the news was seen as a positive for Telstra (TLS, +6.3%), which was one of the market’s strongest performers. TLS also outlined a new corporate structure which will enable it to partially or fully divest infrastructure assets such as its mobile towers. This could potentially free up capital for share buy-backs.

Crown Resorts (CWN, +19.6%) received a takeover approach from private equity firm Blackstone and was the best performer in the ASX 100.

Blackstone’s offer is highly conditional and opportunistic in nature. The bid is only in line with the stock’s pre-Covid level. Blackstone is taking advantage of a discount related to the regulatory reviews — but it is conditional on the resolution of those issues.

The market’s view is that this is designed to flush out a joint venture partner that could buy in combination with Blackstone at a higher price. While the bid highlights the under-valued nature of CWN’s attractive assets — which forms part of our investment thesis — there is still a fair bit of water to flow under this bridge before a deal is finalised.

Small cap tech company Pushpay (PPH, +8.7%) — in which we also invest — rose as one of the early venture capital backers sold a block of stock equivalent to 15% of the float to US tech fund manager Sixth Street Advisors. This removed a significant overhang and brings in an investor with a strong track record in backing the likes of Air BNB and Spotify.

Xero (XRO, +6.1%) made a small bolt-on acquisition ($25 million) of Swedish e-invoicing company Tickstar. This is a sensible move in line with the company’s growth strategy in our view.

Among other stocks we invest in, Metcash (MTS, +6.6%) was one of the quality defensives to catch some interest last week.

James Hardie (JHX) rose 5.7% as bond yields stabilised. Anecdotes from US homebuilders remain supportive, suggesting sales could double current levels if supply was available. At this point the prospect of higher mortgage rates is not having a negative impact on demand. Builders are also signalling an opportunity to raise prices further.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.