Brazil may be attracting negative headlines, but 2021 looks set to be a period where the cyclical opportunity is strong.

Here James Syme and Paul Wimborne (pictured) — managers of Pendal’s Global Emerging Markets Opportunities strategy — explain why.

-

- Brazil shows a move away from liberalising economic reforms towards a more populist stance ahead of 2022 elections

- But by our reckoning the country’s fundamentals look very good indeed

- Find out more about Pendal Global Emerging Markets Opportunities Fund

THE BOLSONARO government in Brazil has taken decisive action after weeks of increasing tension with parts of the corporate sector.

Most coverage has focused on a decision to replace the CEO of oil company Petrobras (held in the Pendal Global Emerging Markets Opportunities portfolio) after the company decided to increase petrol and diesel prices in line with crude oil prices in the face of government criticism.

President Jair Bolsonaro instead suggested the company should cut fuel prices by 10 per cent.

This management change was poorly received by investors because it reduces headline profitability and calls into question the outgoing CEO’s shareholder-friendly operational and financial strategies.

This trend is not Petrobras-specific though. President Bolsonaro is also pushing utility companies to reduce electricity prices.

In addition, one of the major Brazilian banks, Banco do Brasil, has been under serious pressure to abandon its plans to rationalise its workforce.

Taken in the whole, this shows a clear move by the administration away from liberalising economic reforms, towards a more populist stance ahead of the 2022 elections.

What it means for investors

This has a number of implications for investors.

Coming at a time of rising US bond yields, the effect on the share prices of the companies concerned has been significantly negative. But at a wider level the stock market, local currency bonds and the currency have sold off and Brazilian Credit Default Swaps have increased.

This is partly because of the potential implications for fiscal and monetary policy.

As the Brazilian economy normalises post-Covid, the question as to how to (or even, whether to) end the worsening drift in the trajectory of public debt becomes more urgent.

There is a substantial domestic lobby arguing for prioritising economic support and it’s now more likely President Bolsonaro will move in this direction.

The key question for fixed income investors is the future of the fiscal spending cap.

The cap (given constitutional status in 2016) limits nominal growth in the primary (ex-debt interest costs) deficit to the rate of inflation. This would, over time, reduce the deficit as a proportion of GDP, and its existence anchors Brazil’s fiscal policy and contains bond yields.

In 2020, with serious pressure on government finances, the government was able to avoid the cap by using a parallel “emergency budget” for stimulus.

As that justification passes, pressure to return to a fiscal stance that complies with the cap will conflict with popular (and hence political) pressure to remain fiscally loose.

Impact of 2022 election

As we head into an election campaign (a Brazilian general election is due in October 2022) markets may assume the spending cap will be abandoned.

As fiscally loose, so monetarily tight.

The Brazil Central bank met in mid-March and lifted rates in response to a weaker currency and higher bond yields.

The old adage that elections are good for markets in emerging Asia but bad in Latin America may yet apply.

And yet, it is important not to be too bearish. Policy has to be viewed through the lens of fundamentals and, by our reckoning, fundamentals look very, very good indeed.

Barring a prolonged inflationary spike (end of December unemployment was 14.2%, pretty much the highest it has been in 20 years while capacity utilisation recovered to 80.5% in January, well below the 83-84% levels seen at cyclical peaks) Brazil’s enduring weakness is its balance of payments. This is in turn largely a reflection of trade-related and portfolio flows.

Right now both of those look great.

Brazil’s terms of trade (the ratio of export prices to import prices) are by far the best they have been in 25 years, far above the mid-90s or late-00s peaks.

A year ago soybean spot prices were BRL 40/bushel — they’re now BRL 84. Iron ore has moved from BRL 380/t to BRL 900/t. Sugar has gone from BRL 0.67/lb to BRL 0.92/lb.

This feeds right through to the trade balance.

Through 2015 and 2016 the Brazilian trade balance moved substantially into surplus with exports rising and import compression.

Last year 2020 there was volatility in trade flows as Covid-19 hit domestic and external demand and the past few months have seen economic recovery lift imports.

But there is a close historical relationship between terms of trade and exports, and this points to a substantial lift in exports as we move through 2021.

Meanwhile the non-goods component of the current account has compressed to a deficit of 1.4% of GDP compared with deficits of around 4% at cyclical peaks.

Portfolio flows

Portfolio flows are another driver of the Brazilian economy and Brazilian financial markets.

In mid-2020 we saw large capital outflows from riskier emerging markets, particularly Brazil.

Foreign holdings of Brazilian government debt fell from $US140 billion at the start of 2020 to $US101 billion in April.

But by the end of 2020 we saw strong capital inflows with a better cyclical outlook and a weaker

dollar.

International portfolio flows into Brazilian government debt were $US16 billion in Q4 2020, with half of that coming in December.

Anecdotal information suggests a continuation of that in January and February and a similar pattern in the Brazilian equity market (where trading volumes have shot up in the past year).

Foreign direct investment (FDI) is perhaps the laggard.

Net FDI into Brazil was down 50% in 2020 compared with the previous year. The main trend there is a reduction of large investment flows into sectors such as autos and steel and a pick-up in much smaller flows into sectors like fintech and education.

Political outlook

History suggests a sustained recovery will attract inflows — but the negative impact of President Bolsonaro’s actions must be noted.

Concerns around politics and policy have caused us to be cautious about adding exposure to Brazil. We will continue looking to add opportunistically while the macro environment remains so supportive.

It remains our view that Brazil is a market best seen as offering cyclical opportunities rather than a long-term buy-and-hold case.

There will be periods where the cyclical opportunity is strong — and we believe 2021 is likely to be one of them.

The move higher in bond yields, reflecting a stronger global economy, is causing a drag on Brazilian financial markets in the short-term.

But that doesn’t remove the strong fundamental case for the medium-term.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

One year after the market low, here’s how head of equities Crispin Murray (pictured) drove outperformance for Pendal Focus Australian Share Fund during the pandemic. Chris Adams reports.

THIS week marks one year since the market’s low point during the pandemic.

Since the pre-Covid peak on February 21, 2020, Pendal Focus Australian Share Fund has returned 2.9% after fees (to Mar 19, 2021).

The benchmark ASX 300 lost 2.2% over the same time according to Morningstar.

A key factor in the fund’s 5.11% outperformance against the benchmark has been its ability to perform through each phase of the market last year. This is driven by our approach to portfolio construction.

Pendal Focus Australian Share Fund does not rely on a certain set of macro variables to be in place to perform. This has enabled the fund to deliver outperformance while other more thematic approaches have not performed as well.

A market of rapid rotations

The world has run out of clichés to describe the past 12 months.

We had the impact of lockdown policies, supply chain disruption, fiscal stimulus, monetary policy, China-Australia trade tension, the shift of consumers to online, increased focus on ESG and US Presidential elections.

It’s fair to say we have never seen such a material change to so many structural factors in such a short space of time.

Swift changes in key macro factors prompted often-sudden rotations in market leadership.

Defensives did well in the initial market slump. Though the nature of the crisis meant some sectors previously considered defensive – such as A-REITS – were anything but.

The policy response of slashed interest rates helped growth companies renew their pre-Covid surge.

In November, news of successful vaccines drove a swift rotation to cyclicals and value.

Meanwhile entire industries and business models were structurally disrupted in a matter of weeks. Other companies encountered a once-in-a-generation opportunity.

As a result it’s been an incredibly challenging period for investors.

It has also been a period in which the Pendal Focus Fund showed its mettle.

How our portfolio construction drove outperformance

Relying on one “style” of investing can lead to prolonged periods of underperfomance — as value investors have seen for many years.

Trying to “time” swings in style involves anticipating changes in macro variables and investor sentiment — something that’s incredibly hard to get consistently right.

We address this issue by building portfolios based on company insight. We want a portfolio that can perform regardless of the environment, driven by stock selection.

Our aim is a portfolio that is not hostage to one style or a theme playing out in a certain way. In environments of heightened uncertainty, we want to avoid heroic calls on binary outcomes.

Under our approach we created different segments in the portfolio that worked together, allowing it to perform in different scenarios. Key segments last year included defensives, growth stocks, policy beneficiaries, quality franchises and recovery plays.

The key is to find companies with attractive fundamental features that can help limit the downside if the macro factors are not supportive, while delivering the potential for large upside gains in the right environment.

This requires an understanding of companies and industries drawn from access to management that comes with our 18-strong, highly experienced Australian equity team.

2020 provides a strong case study of why we do it this way:

- We were able to move quickly to identify and avoid companies facing existential threats.

- We were able to take opportunities in companies where we anticipated a better outcome than share prices implied – such as Nine Entertainment and Qantas.

- Pendal Focus Australian Share Fund’s outperformance in periods of negative sentiment was driven by defensive holdings such as Metcash (MTS) and by the portfolio insurance provided by gold miners such as Evolution (EVN).

- Falling bond yields helped our growth exposure via Xero (XRO) – which has then held up well due to company-specific fundamentals as other growth stocks sold off.

- Recent outperformance has been driven by recovery-linked exposures such as Qantas (QAN), Santos (STO) and Westpac (WBC).

- Throughout the period there has been a strong tailwind from policy beneficiaries such as Fortescue Mining (FMG) and JB Hi-Fi (JBH).

- We have also done well as the market recognised the value offered in long-term winners such as Aristocrat (ALL), James Hardie (JHX) and Nine Entertainment (NEC).

The outcome is a portfolio that has outperformed through each phase of the market in 2020.

Outlook

The world is now in a better place than many expected a year ago.

The economic rebound has been strong, helped by a surge in monetary and fiscal policy support. Vaccines are arriving. The world is getting better at living with the virus and mitigating its economic damage.

Nevertheless, risks remain.

The risk of premature policy-tightening cannot be ruled out. Vaccinations are working, but efficacy against new strains must be monitored. Geopolitical risk – particularly around the relationship between China and Australia – is higher than usual.

There has been a rotation from growth to value and cyclicals, but the reality is far more complex than broad style labels.

Within value there are plenty of companies that are structurally challenged and are cheap for very good reason.

Growth stocks may have lost the tailwind of falling real rates, but plenty of growth companies remain attractive long-term investments. It’s interesting to note the market seems to be starting to differentiate between profitable growth companies with cash flow and more speculative, long-duration stocks.

Given heightened macro risk, we believe a strategy that is not reliant on a certain macro outcome offers the best chance for consistent performance.

If value, recovery-related stocks continue to outperform, that part of our portfolio will benefit.

If inflation starts to creep up we have exposures with pricing power that will do well.

If we see a hit to sentiment – either from tighter policy or a deterioration in Covid – then the defensives should step up.

We continue to have exposure to carefully selected growth stocks, where we see fundamental valuation support on the basis of earnings visibility and realistic expansion opportunities.

The upshot is that we believe our balanced approach remains as valid now as it did a year ago. It has served our investors well in the sell-off and has worked in the rebound.

No-one knows what will come next. But we believe our portfolio construction, underpinned by our company knowledge, should give investors confidence that their portfolio is well positioned regardless of the next phase of the Covid saga.

Here’s an overview of Pendal Focus Australian Share Fund performance at February 28, 2021:

Source: Pendal. *Benchmark: S&P/ASX300. Past performance is not a reliable indicator of future performance

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

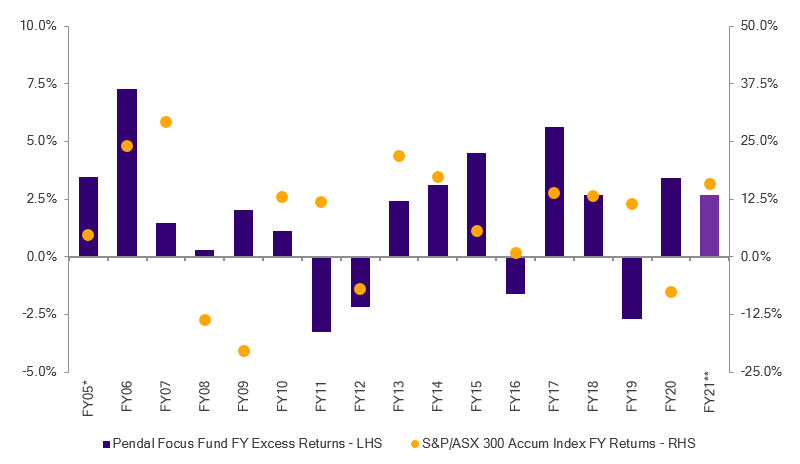

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

TWO concerns emerged last week. Both bear close watching.

First was the emergence of another wave of Covid cases in Europe. The pace of vaccination has been too slow and Covid variants have taken hold, driving an increase in new daily cases across the EU. There are some emerging signs that the early removal of restrictions in the US may see growth in new cases in some states.

The second issue is growing scepticism over the Fed’s ability to keep rates low for an extended period, despite its reiterated stance. The risk here is of a sharp bond sell-off which contaminates equities.

At this point global equities continue to hold up well. But we note the oil price fell 7% last week. There is a risk this is the first sign of this year’s winning trades rolling over.

On the positive side, earnings continue to support markets. The US economy is taking off, while the Australian economy is doing better than expected — as evidenced by last week’s employment data. This can help sustain equities through a consolidation phase while the market adjusts to higher bond yields.

The S&P/ASX 300 fell 0.8% last week, while the S&P 500 was off 0.7%.

Covid and Vaccines

Overall new daily cases in the US continue to fall — but there are states such as Michigan and Florida where cases have turned higher. The arrival of Spring and the removal of restrictions is expected to lead to a new wave in cases. The issue is how material this will become given the level of vaccines and high levels of prior infection. Very high vaccination rates among the more vulnerable parts of society may mean far less pressure on hospitals.

Europe is more of a concern and a significant new wave is possible. There are renewed lockdowns in Poland and France. Non-essential businesses in Paris have been closed. Growth in concerns here are likely to have played a part in a weaker oil price over the week.

Economic and policy

The market’s essential paradox is that two-year inflation expectations in the US are nearing 3% — beyond the Fed’s 2% target — but the Fed’s guidance is for continued loose policy. The market is increasingly uncomfortable with this notion.

The Fed meeting this week reinforced this paradox with a message of more of the same. It re-affirmed a dovish perspective, with the majority of the FOMC seeing no rate hikes in CY22 and 23. The rationale is they expect strong near-term growth to fade, easing inflationary pressures. Their expectation is 2% inflation for CY22 and only marginally higher in CY 23.

The Fed appears to be comfortable with bonds finding a new long-term equilibrium and do not want to get in the way of it. The Bank of England also met this week and indicated comfort on rising bond yields.

The risk is that this process is not smooth and the sale of bonds becomes disorderly, given the unprecedented coincidence of strong pent-up demand driven recovery, fiscal stimulus and loose monetary policy.

The disconnection in expectations can be seen in the large spread between the Fed’s guidance and the market expectation of hikes implied in overnight index swaps (OIS). By the time the first rate hike is officially expected in Q4 2023, the market implied expectations are for three 25bp rate hikes — the first coming in early 2023.

This can also be seen within the FOMC itself. Five members are expecting three-to-four rate hikes by end CY23 — ie believing what the market is saying — while 11 see no such increases. The fact that this dichotomy exists even within the Fed suggests the market’s current expectation is plausible.

Economist and former US Treasury Secretary Larry Summers provided an interesting perspective last week. He repeated his observation that the US was plugging a 3-4% gap in GDP with 14% worth of stimulus.

He also noted a contradiction in the narrative that this is a new paradigm for progressive policies which will deal with structural challenges such as inequality and addressing climate change – but that the effects of the fiscal stimulus are transitory and will fade in CY22, meaning inflation is not an issue.

The key to this is how well inflation expectations are anchored. The Fed believes they are well anchored. The risk is that this belief is undermined and they are forced to re-anchor through a policy pivot.

This will be the key debate for the next six months. It could make for some choppy moments and heightened sensitivity to near-term signals. The strength of recovery in the US economy will be the key issue to watch.

We note that the basing out of the US dollar index may help with the management of inflation expectations. There are a lot of sectors correlated with the USD, notably resources. Recent USD strengthening partly explains the sell-off in resources stocks and remains an important factor to follow. We expect the USD can remain supported given challenges facing the EU. This could be a headwind for resources, but could also help check the worst fears on inflation and bonds yields.

On the US fiscal side, the focus is shifting to the tax increase which will come as part of the infrastructure bill. The Bill itself is still expected to be about US$2 trillion, with half towards hard infrastructure and the remainder to healthcare, education and research and development.

Half the funding is intended to be from net tax increases, including 28% corporate tax. There will be a lot of disagreement over tax rates within Congress, which may impede progress. But the headlines are likely to add to market concern.

One potential resolution may see the Bill broken up into a bi-partisan infrastructure Bill and then a second one that is more progressive and partisan incorporating tax increases.

We also got important Australian data last week. Employment data was very strong. The unemployment rate fell to 5.8% — 0.5% below expectations. This supports the view that any set-back from the end of JobKeeper will be limited and short lived, as long as no more lockdowns occur. The employment / population ratio is 62.3%, versus 62.7% pre-Covid.

The unemployment rate remains a little higher due to participation rates actually rising. Nevertheless Australia has effectively recovered all jobs and is well ahead of other countries in this regard.

Retail sales data was more subdued following a very strong run. It is a reminder that it is vulnerable to normalisation as opportunities emerge to direct spending to other areas such as domestic travel. The softness was more in the area of food sales, indicating people may be beginning to eat out of home more.

We also had population growth data for end of September which, unsurprisingly, has slowed dramatically. This will eventually begin to cause issues for economic growth and housing demand. But for now it will perhaps allow the unemployment rate to fall further and quicker than expected. We expect immigration will be high on the government’s agenda – and that the last 12 months have probably increased Australia’s attraction to potential migrants.

Markets

Equities continue to be resilient in the face of the bond sell-off. 10-year government bonds are on track for their worst quarter for returns in 50 years. Despite this equities in US are up 4.5%, helped by strength in corporate earnings.

The Australian market fell last week, mainly due to resources stocks falling in sympathy with commodity prices. There was a rotation to more defensive names. Over the calendar year to date resources are now underperforming. Banks are the clear lead sector, while tech is worst.

We saw some of the more speculative tech names affected, which is understandable given the rise in bond yields.

The market was led by stocks that had lagged more recently. Some of the US dollar-sensitive stocks did well. Retailers also recovered, as did gold miners.

There was some news flow on key positions in the portfolios.

Metcash (MTS, -2.5%) delivered a constructive strategy day. The IGA franchise has won market share as a result of changing shopping habits to more regional and neighbourhood centres. They have now moved back into store expansion, rather than closures, while Aldi’s roll-out has ended. This suggests they can hold share in this space.

Meanwhile hardware offers a decent growth opportunity in a consolidated industry. The stock fell in reaction to increased capex in this space, but we see the plans as sensible and likely to produce a reasonable return.

The company upped its payout ratio from 60% to 70%, which can be funded despite the capex and means the yield is running at 5%.

Gold miner Evolution (EVN, +5.1%) announced a mid-sized debt-funded acquisition of a Canadian gold company which is adjacent to their existing Red Lake mine. This and allows them to bring forward production and reduce capex, so was well received.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

The pandemic reminded us that you can never truly know the future. But with the right strategy investors can come out the other side well positioned.

Here Pendal’s Head of Global Equities Ashley Pittard (pictured) explains why his Concentrated Global Share Fund has outperformed the index since the market’s pre-Covid peak. Reported by portfolio specialist Chris Adams.

- Our Concentrated Global Share Fund process is conceptually simple: we buy great companies when they are out of favour

- This works particularly well in market slumps. The fund has outperformed the index since the market’s pre-Covid peak.

- Now it is ideally positioned to benefit from the current change in market leadership.

AT THE end of February the Pendal Concentrated Global Shares (COGS) Fund is up 10.14% (after fees) for the previous 12 months. This is 2.36% ahead of the index.

We are pleased with the COGS fund’s outcome in an environment of such high uncertainty. We believe it is very well positioned to perform in the current investment environment.

Dealing with uncertainty

Uncertainty is a given in investment. We do our best to understand the outlook for companies, industries and the global economy. But we are also mindful that you can never know what truly lies around the corner.

The market crash in 2020 was an extreme reminder of this. But as with previous episodes such as Brexit, the Euro Crisis, the GFC and the Asian Crisis, the strategy behind COGS ultimately used the market impact to the advantage of investors.

We deal with uncertainty by buying the very best one or two companies in industries where we have confidence in the long-term fundamentals.

While it sounds simple, this approach offers two important aspects:

- It’s a great way to make money in global equities. These companies and industries periodically fall out of favour due to short-term headwinds or the market focusing elsewhere. If you’re paying attention and know the companies well, at times you get the chance to buy them at material discounts to long-term intrinsic value. Over time this drives outperformance.

- It gives you confidence in times of uncertainty. The companies we own are the largest in their industry with dominant competitive positions and the strongest balance sheets. When macro stress arrives these companies are best set up to survive. Smaller competitors can falter, which means our companies often emerge in an even stronger position in a consolidated industry.

Investing in the epicentre of 2020

Several of our companies were in the epicentre of the crisis, including casinos (MGM, Las Vegas Sands), energy (Total, Exxon), regional banking (Lloyds, Wells Fargo) and aircraft manufacturing (Boeing, Airbus).

We did the work and concluded that these companies could weather an extended downturn and emerge on the other side. This gave us the confidence to add selectively to these great companies at bargain prices.

We also moved quickly to identify the companies facing the highest levels of balance sheet risk. As a result we sold the position in Eurotunnel operator Getlink and property developer Howard Hughes.

Growth stocks outperformed as bond yields fell in the early stages of the crisis. We took some profits here, notably pharma (Pfizer, Merck) and we lightened the position in tech (Facebook, Alphabet). This freed up more capital to take advantage of depressed prices.

We added new positions in several companies with compelling assets which we have been tracking for a while and were now available at attractive prices. These included Zurich Flughafen (Zurich Airport) and Japanese office property play Mitsubishi Real Estate.

Performance in 2020

Our holdings in the epicentre stocks fell and this weighed on performance for a period. The rebound was driven by richly-valued tech growth stocks, where the COGS fund was underweight. This weighed on the fund’s performance in the second quarter of 2020.

But then the market began to look through the near-term uncertainty to recognise longer-term fundamentals —particularly late in the year as vaccine optimism rose.

This has driven a surge in the COGS fund’s performance and it has now outperformed over the entire Covid period.

The key element here is maintaining discipline and trust in the process. This trust is grounded in the success we have seen in previous environments.

Outlook

We believe the Pendal Concentrated Global Share Fund is well positioned to continue its recent strength. Investors are looking for companies with pricing power, earnings visibility, strong balance sheets and cash flow.

This is in our wheelhouse. These are the kind of companies we buy — and there are many examples of them at very attractive valuations.

Several of the COGS fund’s epicentre stocks have strongly rebounded in recent months. But unlike the broader market, many still remain well below their pre-Covid levels.

Boeing, for example, is still 22% below where it was trading in mid-February 2020. Oil producer is Total is 18% below. Wells Fargo is 16% below.

The portfolio has many positions that have lagged considerably during the rebound — but conditions are now in place for them to catch up. In the context of our process, several of our stocks have more than 100% upside to reach our intrinsic valuation.

Rising bond yields and higher inflation expectations are seeing multi-year tailwinds for large cap growth stocks recede. Instead we are seeing a rotation to cyclicals and financials.

We do not see this as a matter of simply buying value and selling growth.

Plenty of value companies remain structurally challenged. We see signs that the market is differentiating between profitable growth companies with good cash flow — and longer-duration, more speculative names.

This trend helps a strategy that is grounded in idiosyncratic stock risk rather than betting on the macro environment.

We do not hold speculative growth stocks. Where we have growth exposure, it is in dominant cash-generative companies. Meanwhile some of our more cyclical exposures are well positioned to capitalise on pent-up demand as economies re-open.

Our ability to maintain discipline during crises and market volatility is a key part of our strategy’s long-term success. This has typically led to strong performance in the period that follows.

This time we expect the same result.

Pendal Concentrated Global Share Fund has done well in recent months. Macro headwinds have faded and our companies are primed for current conditions, with significant valuation upside to drive outperformance from here.

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

What’s likely to happen next in bond markets and how important are they in a portfolio right now? Here’s a quick overview from Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor (pictured)

- There are opportunities in bonds after the recent sell-off

- Vaccines, stimulus and inflation are the factors to watch

- Exposure to bonds is something investors shoud be thinking about

THE big question in financial markets now is what will happen to bond markets and how important are they in a portfolio today.

The sell-off in bond markets was quick – more so than after the global financial crisis of 2007-8 or the 2015 economic slowdown.

US 10-year Treasuries are yielding close to 1.55 per cent. Six weeks ago they were yielding scarcely over 1 per cent. Bond holders are suffering capital losses.

Is it time to cut and run? No, says Vimal Gor, head of bond, income and defensive strategies at Pendal.

“The markets are focused on three things,” Gor says. “The roll-out of the COVID vaccine, the size of the stimulus package in the United States and whether nascent inflation will pick up.”

Investors’ views on these three factors will determine how many bonds to hold.

“There’s a strong argument that the reflation trade is fully priced in,” Gor says. The reflation trade refers to investing on the basis that the economic cycle is in an upswing, where both growth and inflation are accelerating.

“You can see this. Equities have done well and bonds have suffered,” he says.

He points out that central banks around the world are determined to keep a lid on yields at the short end of the yield curve, even if many investors aren’t quite as confident.

“The Reserve Bank has pre-committed to three years of low interest rates. The Fed’s actions have been similar. The European Central bank CB has taken action. Most central banks have given up on forecasting inflation,” Gor says.

In fact the market may turn, and the sell-off in bonds could well reverse.

“There are now opportunities in bond markets. They’ve been oversold … so bond yields should fall,” Gor says.

Outlook for inflation

Gor is not worried about the outlook for inflation, even though many investors are less sanguine about future price rises.

“If it picks up, it’s supply-side related,” he says, referring to potentially higher energy and raw material costs and supply bottlenecks.

“Also, inflation data this year is up against deflation last year, so any headline number will be relatively larger.

“We will get a bout of short, sharp inflation but as for sustained price rises – well we’ve been waiting for that for years and it hasn’t come,” Gor says.

He notes the wrinkle in the bond market currently. The Reserve Bank says it will keep bond yields at 0.1 per cent. But local three-year bonds have been yielding more than that in recent weeks.

“It’s very difficult to lose money buying three-year bonds at the moment given what the Reserve Bank has said,” he says.

At this point, playing the reflation trade is much better done in commodities or equities, not bonds.

“There was a strong argument that government bonds would play much lesser of a role given the sell-off. But now, after the sell-off, exposure to bonds in portfolios is something that every investor should be thinking about.”

Taking advantage

Gor says Pendal has been “taking advantage of these attractive yields in our Australian bond portfolios.

“Markets are looking for cash rates to rise to 2% in five years time — a level last seen in 2015. This is highly unlikely and therefore bond markets are cheap.

“We are happy to look through the current volatility to take advantage of these opportunities.”

About Vimal Gor and Pendal’s Bond, Income and Defensive Strategies (BIDS) boutique

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

With the goal of building the most defensive line of funds in Australia, Vimal oversees A$22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Vimal sets the strategy, processes and risk management for the boutique and all funds managed within it.

Find out more about Pendal’s fixed interest strategies here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Robust succession plan … Mr Nicholas Good (left) will succeed Mr Emilio Gonzalez (right) as Pendal Group CEO

Pendal Group (ASX: PDL) today announced that Group CEO Mr Emilio Gonzalez will step down after 11 years in the role, and Mr Nicholas Good, currently CEO of the J O Hambro Capital Management (JOHCM) operations in the USA, will be Mr Gonzalez’s successor.

The Chairman of Pendal Group, Mr James Evans, said: “The Board sincerely thanks Emilio for his contribution, constancy, and commitment for over a decade and recognises his significant achievements, particularly the successful acquisition of JOHCM in 2011 that transformed the company into a global funds management business.

“Our robust succession plan has enabled the Board to appoint Nick as the new Group Chief Executive Officer of Pendal Group.

“Nick is a global leader in the funds management industry with a strong track record of building and growing businesses. He is an impressive strategist and has an inspiring leadership style.

“Importantly, the biggest future potential for the Group is in the USA. With Nick on the ground there, and with the support of the talented Global Executive Team, including the regional CEOs, Pendal Group will be well-positioned and equipped as it transforms its business to take advantage of future growth opportunities.”

Mr Gonzalez has a six-month notice period and is committed to ensuring a smooth transition.

Mr Evans said: “Under Emilio’s leadership the business underwent a step-change in funds under management, scale, distribution, product offerings to clients, and importantly, shareholder returns.

“Since Emilio’s appointment in January 2010, Total Shareholder Return (TSR) has been 322.9 per cent, compared to the 130.1 per cent return of the Standard and Poor’s ASX200 Accumulation Index over the same period.

“Emilio truly diversified the business across geographies, asset classes, and channels. He successfully oversaw the gradual sell-down of Westpac’s ownership and a broadening of the share register, a change in brand to Pendal that represents our heritage and navigated the business through the global credit crisis and the current global COVID-19 pandemic.

“Emilio will leave Pendal with acknowledgement and thanks for a job very well done and our best wishes for the future.”

Mr Gonzalez said, “With the multi-year investment program announced in November 2020, it is timely and important that my successor has a clean run to drive this program. It will require a long-term commitment, and after 11 years as CEO, it is the right time for a new Group CEO to step in.

“It has been a privilege to lead the company and transform it from a domestic equity fund manager, with $41.9 billion under management, to a diversified global fund manager with $97.4 billion in FUM.

“I would like to thank all of my colleagues at Pendal Group who I have worked with over the years. It has been a team effort and I leave knowing the business is in a strong financial position and well placed for the future.”

Mr Good commented: “I would like to acknowledge the outstanding contribution of Emilio to the Pendal Group. It has been a privilege and pleasure to work with him, and I am honoured and excited to have the opportunity to lead this great company.

“Pendal is recognised for its talent, diversified business model and strategic global footprint. It has long-tenured, highly regarded fund managers and has consistently delivered long-term outperformance.

“I am confident that there is a very bright future ahead as we position to take advantage of the fast-paced changes, and inherent opportunities, in global funds management.”

Mr Good will remain based in Boston, USA.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Pendal has today launched our first Responsible Investment and Stewardship Annual Report for Australia. Here Pendal Australia’s chief executive Richard Brandweiner (pictured) explains what it means

I AM pleased to introduce our inaugural Responsible Investment and Stewardship Annual Report for 2020.

This is a new initiative to summarise the responsible investment practices — including environmental, social and governance (ESG) integration and stewardship activities — we undertake on behalf of our clients.

As an active investment manager, we are truly stewards of our clients’ capital. We believe we have a role and responsibility to deliver sustainable returns for them, as well as influence sustainability practices more broadly.

We do this as part of our fiduciary duty to clients, but also in recognition of our position as one of the largest allocators of capital in the Australian ecosystem.

This means we need to influence positive change by taking a constructive and forward-looking approach to supporting companies improve their ESG credentials.

Long-term value creation

As society evolves and consumers and regulators increasingly look towards organisations to be mindful of their social licence to operate, we believe attention to ESG factors leads to better informed investment decisions and can improve the quality and consistency of long-term value creation.

We are proud to work with many clients who have additional ethical and sustainability-related objectives, in addition to generating returns. For these reasons, we integrate financially material ESG factors across all Pendal funds, as well as offer dedicated investment solutions to meet our clients’ additional priorities.

At Pendal we have a multi-boutique structure, with four distinct investment teams: Australian Equities, Global Equities, Multi-Asset Strategies and Bond, Income & Defensive Strategies.

Each boutique integrates ESG and undertakes stewardship in a way that makes sense for their respective strategies and asset classes.

In other words, we don’t have a single way of investing responsibly at Pendal, although our dedicated Responsible Investments team does bring a common thread across the firm by supporting all boutiques and helping to define quality.

Regnan: Sustainable and impact investing

As many of you will be aware, in early 2019 we assumed full ownership of Regnan, bringing the team in-house to be Pendal Group’s specialist sustainable and impact investing business unit.

Regnan’s experienced team of experts have been a great addition, supporting our engagement and research activities and the continued development of our investment products.

Excitingly, 2020 saw Regnan’s capabilities expand to investment management.

Pendal Group secured a specialist global impact investment team to join the Regnan ecosystem and we launched two products under the Regnan brand.

We look forward to the expansion of the Regnan business, further enabling the purposeful allocation of capital.

Learning and growth

While 2020 in many ways went down as a year most would rather forget, for Pendal it was also a year of learning and growth.

It was a year of paradoxes: a reminder that not every situation is an “either/or”, and not every decision can be bound by the immediate environment or issues at hand.

The year saw, for example, corporate management held to account for more than just the maximisation of short-term shareholder profit in ways we have not seen before.

As we turn our attention to the future and “building back better”, we expect the topics of climate change and inequality will gain importance in the year ahead — and beyond.

The COVID-19 pandemic laid bare many underlying inequalities in societies around the world. Women, elderly and vulnerable communities were disproportionately represented in the hardest hit sectors of the economy.

Encouragingly we are seeing investor action already and we share in this report some of the ways we are working with our clients and investee companies to address this rising inequality.

Tranformation through collective action

The pandemic has also shown us that collective action can drive transformative policies and deliver break-through technologies that seemed unthinkable before the crisis.

Through our engagements and advocacy efforts we will seek to ensure the advances witnessed in 2020 continue.

How else can we ensure that our health, political and economic systems can be resilient in the face of a pandemic, or other form of crisis in the future?

We are thrilled with some of the things we achieved in responsible investment and stewardship in 2020.

These efforts are detailed in this report which I hope you enjoy reading.

We look forward to reporting annually on the ways in which we continue to enhance our approach, responding not only to the ever-changing investment environment but to the evolving needs of our clients.

— Richard Brandweiner

Pendal Chief Executive Officer, Australia

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Download Pendal’s Responsible Investment and Stewardship Annual Report 2020 (PDF)

Contact a Pendal key account manager here.

As part of its approach, Pendal Horizon Fund invests in companies that enable and lead in the transition to a more sustainable and future-ready Australian economy, while avoiding those that cause significant harm.

An example is business software innovator Xero, a leader in the trend to digitalisation which is changing the way we work.

Pendal equities analyst Elise McKay explains in a short video above.

ASX-listed technology stocks — particularly so the so-called WAAAX stocks Wisetech (WTC), Afterpay (APT), Altium (ALU), Appen (APX) and Xero (XRO) — have been favourites among many investors in recent years.

A key part of this has been the benefit of low-bond yields, which have lifted valuations for growth companies — including many tech names — worldwide.

This tailwind has receded in recent months as yields have begun to rise. Meanwhile vaccines have provided a pathway to re-opening, boosting sentiment around more cyclical stocks. As a result market leadership has shifted from growth stocks to cyclical and value.

In our view this does not mean a shift to a stance of “sell growth, buy value”.

There are plenty of value stocks that are structurally impaired. At the same time, we think there are compelling opportunities in tech stocks. Stock selection is as critical as ever.

In the tech sector we think the market will start to discern between companies with less tangible prospects that are not delivering cashflow — and those that are profitable with good earnings visibility.

We see accounting software provider Xero as one of the latter. It is our top pick in the ASX tech sector.

In this video above Pendal Research Analyst Elise McKay shares insights into XERO, the ASX tech sector and the five-factor framework by which we assess companies.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

“We use this framework to find those companies like Xero that are generating strong, sustainable returns on the capital that they’re investing today in unlocking a large global addressable market and creating significant value in the future,” says McKay.

In Xero’s case:

- The industry structure and competitive landscape is favourable and there is a large global addressable market

- Xero is well placed in the cycle as secular trends drive the adoption of cloud accounting products

- It’s investing heavily in innovating the next generation of products.

- The culture of the company is strong, and it’s able to internally create the products it needs.

- And finally, the capital return and unit economics of the business are attractive.

“One of the great things about Xero is that it has accelerated digitalisation of the economy, particularly for small businesses.”

Digitalisation refers to the use of digital technologies “to change a business model and provide new revenue and value-producing opportunities” according to research house Garnter. (It’s distinct from digitisation, which simply means converting things such as bank accounts or books from analog to digital.)

“This platform opportunity allows Xero to be the plumbing into so many more solutions being offered to this community.”

Digital tools are rapidly becoming essential for small business in Australia, according to McKay, who says businesses adopting digital are on average able to save 10 hours a week and generate 27 per cent more revenue.

She believes the fast-growing cloud accounting provider is at the start of a multi-year journey to unlock an enormous global market and become a platform for transforming small business.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

About Elise McKay

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies. She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

About Pendal Horizon Fund and Pendal Focus Australian Share Fund

Pendal Horizon Fund (formerly Pendal Ethical Share Fund) is a concentrated, high-conviction portfolio aligned with the transition to a more sustainable, future-ready economy.

Pendal Focus Australian Share Fund is an actively managed, concentrated portfolio of 15 to 30 of our best investment ideas across the Australian share market.

Both funds are led by one of Australia’s most experienced portfolio managers, Crispin Murray. Crispin is backed by one of the largest, most experienced Australian equity teams.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

OPTIMISM over stimulus and the rate of economic re-opening in the US has continued to drive equity markets higher.

The US$1.9 trillion American Rescue Plan Act was signed into law last week, while the EU increased its bond purchase program.

Locally the federal government announced its “PlaneKeeper” program to support the tourism industry. It was met with mixed reviews. The headline figures do not seem to match the details revealed so far and market impact was muted.

The S&P/ASX 300 rose 1.03%. Most sectors were up, although real estate and energy lost a little. The S&P 500 gained 2.69%.

Covid and vaccine outlook

The US retains positive momentum. New daily cases are down 73% from their peak while hospitalisations have fallen 71%.

Mobility data is picking up quickly, reaching its highest level since March last year. This is undeniably good for economic recovery.

About 21% of the US population have had a single dose and 11% have had two. This raises the risk of a second wave given the speed of re-opening.

The vaccination rate is closing on 3 million people per day as the broader supply arrangements take effect. Vaccine supply was up 140% in March versus February. April is expected to be up another 60%.

At these rates the US could reach herd immunity in June as long as demand for vaccinations exists.

The UK is experiencing similar trends in new cases and hospitalisations. Europe’s sluggish program remains a concern with a pick-up in new cases in Italy and part of Eastern Europe. The divergence between the US and EU is helping support the US dollar.

Economics and policy outlook

The big news from the US was the passing of the $1.9 trillion stimulus Act.

Some $400 billion worth of $1400 cheques will be disbursed by the month’s end. This is the single biggest weekly surge in stimulus spending so far — almost double the previous high in April 2020.

We expect some of this cash to find its way into the stock market and — if history is a guide — into the more speculative tech names.

To provide some context around the scale of stimulus, the US cumulative response stands at 36% of 2019 GDP. Europe has done 30% but with greater skew to loans rather than fiscal transfers.

This is driving the debt/GDP ratio back to levels not seen since World War II.

Expected nominal GDP growth in the range of 10% this year will help alleviate some of this. But the government remains vulnerable to any spike in bond yields. This is why the market remains focused on the outlook for inflation.

This stimulus package was in reaction to the depths of the crisis in December and January, but it comes as real-time economic indicators are recovering.

Company surveys are already picking up and the lead indicators for jobs growth are strong. Rising house prices are also supportive, judging by the surge in equity being cashed out of homes.

There are some concerns over the supplementary leverage ratio (SLR) in the US, which dictates the amount of capital large banks must hold against their loans.

Last year the Fed allowed the temporary exclusion of US treasuries and deposits held at the Fed from the ratio’s calculation.

This exclusion is due to expire at the end of March. This could potentially become a binding constraint on capital and distributions, which could see banks selling treasuries and being unable to make markets as efficiently.

This is a risk to watch, although the expectation is for some sort of transition period which would mitigate any near-term effects on the bond market.

Elsewhere, the EU announced it would significantly increase Quantitative Easing purchases in the next quarter to offset higher moves in the yield curve. However they did not raise the overall amount planned through to March 2022.

This helped improve EU bond yields, but leaves a confusing policy conundrum later this year if growth doesn’t accelerate materially.

Markets and stocks outlook

The key issue in markets is the degree to which concerns over bond yields offset huge cyclical tailwinds.

Moves were generally subdued last week, though a sell-off in bonds at the end of the week pushed US 10-year treasury yields up 6bps. This did not have an impact on equities.

The US dollar is at an interesting juncture. The dollar index — which measures the USD versus a basket of currencies — slumped over the second half of 2020, but has risen since January.

There is debate as to whether recent strength is a temporary rally, followed by more weakness — or whether the strength in the US recovery will see the greenback rally further. A stronger US dollar could prove a headwind for commodities.

Comments on bond yields from this week’s Fed meeting will be a key signal for currency.

There is an interesting trade developing within the broad rotation from value to growth. In growth, large-cap tech stocks are outperforming smaller, more speculative names for the first time since April last year.

It is important to remain mindful that today’s market is not just a case of simply “buy value, sell growth”. Plenty of value companies are structurally challenged.

There are also signs of a divergence between profitable growth companies with strong cash flow versus the longer duration, more speculative names.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Major shifts in policy-making — driven by the Covid crisis and a desire to correct GFC-era mistakes — can drive equities higher despite pockets of excess, says Pendal’s head of equities Crispin Murray (pictured).

Here are some insights from reporting season, drawn from Crispin’s bi-annual Beyond The Numbers presentation.

Watch the presentation here (registration required).

Key points

- Equities to benefit from major shifts in policy goals

- A number of factors are driving rotation from growth to value

- Performance is not simply “buy value, sell growth”

- Find out about Pendal Focus Australian Share Fund

INVESTORS may see pockets of excess in markets at the moment — but that’s not necessarily a sign that we’ve reached a top in equities, says Pendal’s Head of Australian Equities Crispin Murray.

These are symptoms of a policy agenda designed to avoid the mistakes of the Global Financial Crisis era.

That era resulted in fiscal austerity, pre-emptive monetary tightening and a focus on economic goals to the exclusion of other factors.

Today policy makers are thinking more about reducing inequality, building economic resilience and a greater role for clean energy.

This means bigger fiscal spending and very accommodative monetary policy.

Coupled with the impact of pent-up demand amid a re-opening economy and the return of fund inflows, this should combine to drive the stock market higher, Murray believes.

But he cautions investors to watch for additional complexity in markets.

For example Covid has accelerated structural trends such as the transformation of work via digitalisation and the impact of Environmental, Social and Governance factors when scrutinising companies.

Growing concern about inflation can also trigger bond market sell-offs which can have varying impacts across equity market sectors.

“We think equity markets will be resilient in the face of rising bond yields,” he says. “[But] they do have a big effect on what’s going to actually perform in the market.”

Higher inflation expectations and bond yields are seeing market leadership shift away from growth to cyclicals with pricing power. This suits the Australian markets, he says.

But future outperformance is not a simple matter of buying value stocks and avoiding growth stocks.

“There are still going to be companies in the value sector that are structurally disadvantaged.

“And you’re going to find companies in the growth sector that still have incredibly strong franchises. So, you need to be nuanced about your stock selection.”

The environment is ripe for an active, style-neutral approach focused on company specifics.

Four components of a well-constructed equities portfolio

Murray says a well-constructed portfolio should have four components:

- First, defensive stocks are needed to protect against risk and the chance of policymakers changing their minds.

- Second, a portfolio should have exposure to stocks that are leveraged to the potential inflationary pressures coming through.

- Third, investors should hold companies that used the crisis to improve their position and are ready to benefit from the release of pent-up demand.

- And finally, investors should consider the companies hit hardest by the pandemic who will see a material shift in fortune once the vaccines roll out.

“When we think about our portfolio, we think about the different roles stocks play. Like a football team, you need the defence, you need the midfield, and you need the attack.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions, as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21.

Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.