Regnan’s head of impact investment Tim Crockford interviewed by Investment Magazine (Nov 2020).

IMPACT investing — which aims to generate a financial return and a positive impact on society — is a fast-growing market.

The value of Australian impact investment products is expected to grow to $100 billion in the next five years — up from $20 billion in 2019, according to the Responsible Investment Association Australasia.

Impact investment manager Regnan — distributed in Australia by Pendal — is about to launch its Global Equity Impact Solutions fund.

Here is the fund’s portfolio manager Tim Crockford making his first Australian appearance live from London at Investment Magazine’s Fiduciary Investors Symposium on November 18, 2020.

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com or Regnan Chief Operating Officer Lisa Boyce at lisa_boyce@regnan.com.

Pendal Active High Growth Fund (APIR: BTA0488AU, ARSN 610 997 674)

Effective 25 November 2020, the buy-sell spread for Pendal Active High Growth Fund will increase as set out in the table below:

|

|

Old (%) |

New (%) |

|

Pendal Active High Growth Fund |

0.34 (0.17/0.17) |

0.38 (0.19/0.19) |

The buy-sell spread is an additional cost to you and is generally incurred whenever you invest in or withdraw from a Fund. The buy-sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy-sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy-sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Funds.

Pendal will continue to monitor market conditions and review and update the buy-sell spread regularly as required. You should therefore review the current buy-sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy-sell spread for each Fund.

Pendal’s head of equities Crispin Murray explains his vision for our newly renamed Pendal Horizon Fund (formerly known as Pendal Ethical Share Fund).

The year 2020 demonstrated some fundamental truths about the modern investment environment.

The world is vulnerable to shocks — from climate change to pandemics. Change is accelerating. Successful companies must confidently manage a wider set of risks than in the past, including environmental, social and governance (ESG) risks.

What are the implications for investors? What have we learned and how is Pendal responding?

We believe investors need:

• Strategies that can protect against unpredictable outcomes.

• Investments that benefit from and are leveraged to structural changes.

• Investments that can enable and facilitate positive change while avoiding harm.

• A high-conviction, all-weather, nimble portfolio.

Our approach to sustainable investing is grounded in these beliefs.

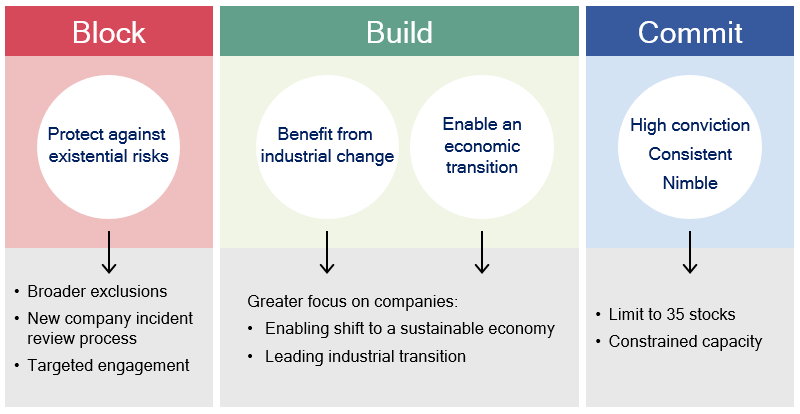

Block, build, commit … the foundations of Pendal’s Horizon Fund

Now we have taken the Pendal Ethical Share Fund, with its 19-year history, and re-engineered it for the next two decades as Pendal Horizon Fund.

This enhanced strategy is:

• Built for performance. It’s a concentrated, high-conviction strategy of 15 to 35 stocks that draws on the company insights and risk management underpinning Pendal’s long and strong track record in performance

• Actively invests in companies that enable a more sustainable and “future-proof” Australian economy. This allows the fund to benefit from trends shaping coming decades, from digitalisation to decarbonisation. We allocate capital to companies that directly contribute — or enable others to contribute — to areas such as:

Pendal’s Horizon Fund directs capital into these areas

• Avoids activities that undermine a more sustainable economy (see graph below). We screen out harmful industries such as fossil fuels, alcohol, gaming, tobacco, weapons, logging, predatory lending and companies that breach standards:

Pendal’s enhanced Horizon Fund operates exclusionary screens in these areas

• Uses Pendal’s deep responsible investment capabilities. This includes the advice of Regnan — our wholly-owned subsidiary — in assessing companies on their contribution to a sustainable, future-oriented Australian economy and their management of ESG risks.

• Prioritises active stewardship and engagement with companies to promote sustainable characteristics and minimise ESG risks. This leverages Pendal’s depth of corporate access and scale of funds under management, allowing us to be an effective agent of change.

The outcome is a fund that is built for performance while also acting as a force for positive change in Australia’s future. The fund is aligned with developing trends while benefiting from Pendal’s proven capability.

Click here for more information about the Pendal Horizon Fund (formerly Pendal Ethical Share Fund).

Contact Us

For more information, please contact Pendal’s Head of Responsible Investment Distribution Jeremy Dean at Jeremy.Dean@pendalgroup.com.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Here’s what’s influencing Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS were mixed last week. On one hand there were fears the US Covid-19 surge could prompt restrictions that weigh on growth. On the other, we saw further positive vaccine developments.

The S&P 500 fell 0.73%, but Australian equities rose 2.11% (S&P/ASX 300) as the virus remained under control domestically.

The risk to growth from the current US Covid wave must be watched. However we still see plenty to support equity markets through to the end of the year, including policy stimulus, economic resilience, strong liquidity and the prospect of good corporate earnings growth as previous weakness is cycled.

Vaccine news

There was positive news on the vaccine front last week, with Moderna’s interim results showing 94%+ effectiveness. Pfizer also updated their results to show a similar outcome.

This is good news for the economy and markets.

From here, several factors need consideration:

• Side effects: Initial data looks reassuring on this front, particularly for Pfizer. A small subset of trial patients report some minor irritation, but at this point there seems nothing too serious.

• Impact on older patients: Data indicates that older cohorts are so far responding well to vaccines.

• Durability: This is still to be determined. Time will tell, but indications on immunity thresholds suggest it should work for at least a year.

• Manufacturing and distribution: The combined expectation is that Moderna and Pfizer will have 70 million doses available by the year, which can be used on 35 million people (each vaccination requires two doses). About 70% of these doses are expected to be used in the US. The area to watch is the production ramp-up. Moderna are saying they will ramp from 7 million doses per month now to between 50 million and 80 million by mid-2021. This means widespread vaccination will be possible by the June quarter.

• Take-up of vaccine: Surveys indicate the high vaccine efficacy rate is increasing the propensity for people to take it.

• Virus changes: The potential for new strains of Covid – and the impact on vaccines – remains a key unknown.

The next expected developments include emergency approval for Pfizer’s vaccine – anticipated by end of the year. AstraZeneca’s interim results are also expected in the next two to three weeks.

Covid outlook

The focus is on how things play out in the US. Rolling average daily new cases continue to climb, but at a declining rate — up 25% week-on-week versus 40% the previous week.

However bottlenecks are emerging in testing capacity, which is reflected in case numbers and in a continued increase in the proportion of positive test results.

US hospitalisations increased 20% week-on-week — a marginally slower rate than the previous week. Patients remain spread out geographically and we are still seeing spare capacity in the system.

The next two weeks will be critical. Some modellers are predicting an acceleration in cases and hospitalisations, partly due to the Thanksgiving holiday.

Case trends continue to improve in Europe. At this point Europe seems to have avoided a crisis in the hospital system. France appears to be turning around, which supports the case that better treatments and protocols are helping manage the scale of the crisis.

Policy outlook

The Trump administration’s treasury secretary last week declined to approve beyond January 1 the facilities that have been the back stop of credit markets.

This means the Fed will no longer be able to buy corporate credit, provide main street loans or municipal loans. The Treasury is also asking for the return of unused capital.

Originally the Cares Act pledged $454 billion to the Fed, which could be leveraged up. To date they have received about $100 billion.

While the extension can be re-approved under Biden’s administration, the bigger issue is that the returned funds would not be immediately available. They would remain locked up until Congress authorised them.

The Fed has some access to other funding sources via the Exchange Stabilisation Fund. But this is in the region of $70 billion – far less than the existing package.

While markets continue to function normally this should not present a major issue. But it adds to the downside risk of negative events emerging. It is also likely to encourage the Fed to do more Quantitative Easing.

Another negative on the horizon is a further step down in fiscal support as jobless benefits expire for another 7 million to 12 million workers. This equates to $35 billion to $70 billion less fiscal stimulus in the first half of 2021.

The last step down was relatively benign, as households drew on elevated savings rates to smooth the effect. Any fiscal deal may also restore some version of these payments. However this risk needs to be watched in the near term.

Economy outlook

Rising cases and shifting behaviour are having some effect on US economic indicators. But activity is so far proving more resilient than many had feared.

The Atlanta Fed’s GDPNow real GDP estimate is improving. It’s most recent prediction is 5.6% GDP growth in Q4 – well above consensus – driven by strength in housing, retail sales and industrial production.

Elsewhere, the weekly US Consumer Comfort index rose to a new post-pandemic high, probably helped by the election and vaccine news.

Existing house prices rose 15% in October, implying a US$10 trillion gain in consumer net worth. In combination with increasing money supply (still up 25% year-on-year), tight credit spreads, stronger copper prices and the scope for better corporate earnings, it suggest that while sentiment is nervous, there are plenty of supportive factors at play in markets and the economy.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. Crispin manages a number of our flagship funds and leads one of Australia’s biggest equities teams.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Looking at tech stocks in emerging markets? Take care to consider investments with a catalyst to unlock a company’s potential and share price. Global Emerging Markets Opportunities portfolio managers James Syme and Paul Wimborne (pictured above) explain

TECHNOLOGY companies generally face an extremely supportive operating environment at present.

Covid-19 has hugely accelerated online migration. Along with the rise in artificial intelligence and machine learning this requires massive investment in new hardware.

Pendal’s Global Emerging Markets Opportunities portfolio has significant exposure to companies that are benefiting from these trends.

But we retain a preference for investments that also have a catalyst to unlock the company’s potential and its share price. This includes some of the largest holdings in the fund.

Naspers, Prosus & Tencent: Twin discounts

One of our largest aggregate portfolio positions is in the related companies of Naspers (a South African holding company), its subsidiary Prosus (a Dutch media conglomerate focused on the internet in emerging markets), and Prosus’s biggest investment, Tencent (a Chinese internet giant).

One of the oddities about the listings of these three is that Naspers trades at a discount to the market value of its shares in Prosus; and Prosus trades at a discount to the market value of its stake in Tencent (let alone the value of Tencent and Prosus’s other listed and unlisted investments).

Naspers has a market capitalisation of US$85 billion (all data as at October 31, 2020 unless otherwise indicated). Almost all of the Naspers balance sheet consists of its 72.5% stake in Prosus. Prosus has a market capitalisation of US$162.7 billion, making that 72.5% stake worth US$117.9 billion.

There are various explanations — mostly around the gap in liquidity, index membership and investor market access between South Africa and the Netherlands.

Sitting behind that valuation anomaly is another, more complicated and potentially larger one.

Prosus owns 28% of listed Russian internet company Mail.ru, 22% of German-listed food delivery company Delivery Hero and 6% of US-listed Chinese online travel retailer Ctrip. These three holdings are worth US$7.7 billion.

Crucially, it also owns 30.9% of Chinese social media and gaming behemoth Tencent. That stake has a market value of US$225.8 billion.

A long tail of unlisted emerging market online companies in classifieds, food delivery, payments, travel, education, and social media has a value (while harder to assess) conservatively estimated at more than US$20 billion.

At its December 2019 capital markets day, Prosus management indicated a desire to create at least US$100 billion in shareholder value over the medium term.

As a step towards achieving that, in October 2020 Prosus announced a US$5 billion buyback, consisting of US$1.37 billion in Prosus shares and US$3.63 billion in Naspers shares. This sits alongside a commitment to increase Prosus’s free float by reducing the Naspers stake to below 70%.

The really big step, however, would be Prosus selling some of its stake in Tencent to do further buybacks.

There are no immediate indications that this is about to happen, but it should be noted that the last such sale (in March 2018) followed a very strong share price run in Tencent, as we have seen year-to-date.

Through these twin discounts in the group’s market capitalisations, there exists very substantial potential for gains to shareholders from proactive steps to buy back shares. We have seen a concrete step towards this in October and expect further steps in current months.

Samsung: Reform in the chaebol sector

Another one of the portfolio’s largest positions is Samsung Electronics (SEC) in South Korea. SEC is a multi-faceted conglomerate operating across various consumer electronics and IT products.

Using its last four quarterly results as a guide, the biggest division by revenue is IT & Mobile, which produced US$9.7 billion in operating profits on US$85.4 billion in revenue with a margin of 11.4%.

The next biggest (but most profitable) division is semiconductor products, which produced US$15.4 billion in operating profits on US$59.8 billion in revenues with a margin of 25.8%. There are also smaller units producing display products and consumer electronics which together produced US$4 billion in operating profits.

This operational profit translated into US$21.3 billion of free cash flow for the period.

SEC has a market capitalisation of US$297.8 billion. But crucially, its balance sheet is extremely cash-heavy.

At the end of September SEC had US$105.2 billion in cash and only US$17.5 billion debt. The company has tended to grow organically, and does not use its cash for acquisitions, making this essentially surplus cash able to be returned to shareholders.

Since 2015 SEC has had a far more positive approach to dividends and share buy-backs, currently operating a shareholder return policy of paying out KRW 9.6 trillion (US$8.7 billion) in dividends each year.

It is seeking to return a minimum of half of free cash flow over the three-year period 2018-2020 through dividends or share buy-backs.

The company was due to announce an update to this policy in the fourth quarter of 2020. However, Samsung group chairman KH Lee passed away on October 25, having been unwell since a heart attack in 2014.

Mr Lee had led the Samsung Group since 1987 following the death of his father, Samsung founder BC Lee. He had transformed Samsung into a world-leader in multiple sectors, with SEC at the heart of the group.

Mr Lee’s son JY Lee has been acting chairman of SEC since 2014 and drive the change in shareholder return policy.

JY Lee is set to inherit stakes of major Samsung group companies, including SEC, and we expect SEC to continue to improve its shareholder return policy.

The Lee family’s control over SEC may decline as it sells down stakes in related group companies to meet inheritance tax obligations, while the Moon government’s pressure on chaebol holding structures continues to increase.

(Chaebol refers to a business conglomerate structure that originated in South Korea in the 1960s, creating global multinationals with big international operations. The Korean word chaebol means business family or monopoly.)

This is likely to increase the role of minority shareholders in major decisions at SEC, which should drive an improving shareholder return policy at SEC. As a result, the announcement of the new shareholder return policy has been moved to late January.

This will be a key moment for SEC.

The buy-back program has been on hold since mid-2018 because a capital expenditure bulge meant the KRW 9.6 trillion dividend payment commitment met the free cash flow return commitment.

However the last four quarters have seen free cashflow run at an annualised level of around KRW 25.6 trillion (US$21.6 billion).

This suggests that either the commitment to pay dividends increases, or the buy-back program resumes.

In conclusion, we certainly find many opportunities in the broader technology space, but prefer to focus our larger positions on those with strong operating momentum and an additional potential driver of returns from restructuring and the unlocking of value.

We are particularly excited about potential newsflow for these holdings in the next few months.

James Syme and Paul Wimborne are senior fund managers and co-managers of Pendal’s Global Emerging Markets Opportunities fund.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Here’s what’s influencing Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Equity markets experienced strong gains last week as positive news on the Pfizer vaccine outweighed a continued surge in US Covid cases.

Real-time data indicates higher US case numbers are starting to have an economic impact. There is a risk this could accelerate.

Lead indicators point to a rapid increase in hospitalisations next week, which could lead to renewed lockdowns in the US.

At this point investors continue to focus on the vaccine and potential for policy support to offset the impact of lockdowns. The S&P/ASX 300 gained 3.6% and is now down only 1.43% year-to-date. The S&P 500 was up 2.21%.

There was a significant rotation from momentum to value last week.

Latest vaccine developments

Pfizer announced interim results of its vaccine trial which show an efficacy rate of 90%. This means the number of infections in the vaccine group was 90% different to the placebo group.

This is much better than expected and has material implications for the time it could take to effectively suppress the virus. A 75% efficacy rate could take 6-to-12 months to see suppression, while this could be cut to a couple of months with a 90% rate.

Questions remain. We do not know how it performs on more severe infections. We also don’t know how long the vaccination remains effective — although observations of the immune response suggest it should work for at least a year.

There is some concern about distribution given the vaccine needs to be kept cold. Pfizer plans to retain control of the distribution process. They will make and freeze the vaccine at -70 degrees Celsius and ship it in dry ice, keeping it stable for 15 days. Once at a destination it can be stored at 2-8 degrees, keeping it stable for five days.

This is a positive development. There are expectations the data could be ready for emergency FDA approval by the end of November.

Expect Moderna to report its trial interim results early this week. They have already said the threshold of infection numbers in their vaccine group has been met. Moderna’s vaccine could trigger a more durable immune response than Pfizer’s.

Covid outlook

The vaccine news was critical because it appears the US is facing a surge in hospitalisations and deaths.

Daily new cases rose 40% last week versus a 20% gain the previous week. Given a sharp drop in daily new cases in places like France, where lockdowns are in place, the US is now in line with the EU in these terms.

Total US patient count is now above the peak during the summer wave, although cases are more evenly distributed across the country this time. The test positivity rate has climbed above 10% for the first time since May.

There are reports of issues with testing capacity, which can lead to delays in turnaround time and an under-reporting of case numbers.

Hospitalisations typically lag case number trends by a week, suggesting we could see a surge in the next few days. Some 26 States are now at their highest levels of hospitalisations and 17 are at their peak level of Covid-related ICU patients. ICU capacity remains reasonable in most States. This must be watched in coming weeks.

Localised restrictions are in place in Chicago and in Utah. A number of States have reduced bar opening hours and the size of gatherings. Any signs of capacity strain are likely to trigger more restrictions.

There is concern about the potential impact of Thanksgiving-related travel.

With the rise in cases, the US is seeing early signs of activity slowing — notably in retail and preparedness to leave home. Company and retail surveys have ticked down in recent weeks, as have consumer sentiment indicators.

The impact of greater restrictions is a key risk. As it stands today, markets seem of the view that lockdowns can quickly control the spread and that policy measures and an imminent vaccine can smooth the economic impact.

Markets outlook

The vaccine announcement lifted equities last week alongside oil, iron ore and copper. Bonds and gold sold off.

The US equity market is now up just shy of 10% for the month and is looking over-bought on some measures.

There is potential for some volatility or a technical correction brought on by rising case numbers. Last week there was a strong rotation away from momentum to value – by some measures the biggest ever intra-day move in that regard.

The Australian market is almost back to flat for 2020. We remain positive on the domestic outlook, given the combination of stimulus and border re-opening.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

US election. Rates. Covid. China. Last week was busy one. Here’s what it means for ASX investors according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

WE SUSPECT the removal of uncertainty would have prompted a relief rally regardless of the US election outcome.

But the market seemed especially positive at the prospect of divided government in the US — with a Democrat White House and Republican Senate limiting scope for dramatic policy changes such as higher corporate taxes.

Further monetary stimulus from the Reserve Bank of Australia and Bank of England also helped markets last week.

The S&P/ASX 300 gained 4.45% for the week, while the S&P 500 was up 7.43%.

A Republican Senate would mean smaller fiscal stimulus, reducing the chance of a strong rotation to value within the market. Growth stocks tended to outperform during the week.

US election

The likely outcome seems to be a Democrat in the White House, notwithstanding talk of legal challenges.

The “blue wave” did not emerge. The Democrats have done worse than expected in the House of Representative, losing nine seats so far. They should retain a (smaller) majority.

The Democrats also underperformed expectations in the Senate. Current projections suggest a 52-48 majority to the Republicans.

Georgia may not get to the 50 per cent threshold needed for one candidate, which means both seats go to a run-off election on January 5. This will become a major focal point of campaigning.

History indicates the side not in the White House tends to do better in a run-off. Republicans were already leading — and votes for the Libertarian candidate are likely to break their way — indicating they are more likely to win.

Questions remain about the current administration’s next steps. These include potential legal challenges before the Electoral College meets on December 14 and any other actions President Trump may take before he relinquishes the office next year.

These issues cannot be ignored, but we are mindful of checks and balances that may limit risk.

The prospect of divided government likely means lower stimulus, but also less chance for some of the more contentious policy changes such as higher taxes.

Without the control of Congress Biden is likely to plump for a more centrist cabinet, potentially taking some of the more left-wing agenda off the table.

Biden has a strong relationship with Republican Senate Leader Mitch McConnell, which may be constructive for a degree of co-operation.

The main short-term issue is the reduced expectation of a fiscal package, with $US1.5 trillion to $US2 trillion now possible by the end of Q1 2021. There is potential for the Senate to get this done while Trump is still president if it’s a smaller number.

Covid outlook

Cases continue to deteriorate throughout Europe and the US. Increased positive test numbers indicate a continuing rise in momentum.

Total US hospitalisations are at 50,000 versus a previous peak of 60,000. They are now spread over a wider geography but there are no signs of strain on the system yet. This remains a key factor to watch with an additional 100 new hospitalisations per day.

The market seems to be taking a sanguine view of lockdowns at this point and appears to be looking through this wave of Covid due to:

– A better understanding of the virus

– Improved healthcare system preparation

– A view that lockdowns work within a reasonable time frame

– Policy ready to plug the economic gap

– Liquidity so prevalent any sell-off can be quickly supported

– We may be weeks away from a vaccine

There was news of a new COVID strain emerging in Denmark. This highlights one of the potential risks to vaccine effectiveness.

There were also positive signs for a new therapeutic – Humaningen’s anti-GM-SF antibody – which showed 37 per cent improvement in outcomes in a hospital study. The trial is expanding, with a potential filing for approval in Q1 2021.

Economic outlook

Backward-looking jobs data in the US is positive. There was another step up in total jobs in October, driven by a recovery in leisure, hospitality and retail.

Aggregate signals on ISM data paint a positive picture for industrial activity. Most countries are tending to the expanding/strengthening quadrant. Australia was particularly strong in this regard.

Short-term retail survey data in the US was a bit weaker. This may be partly related to the election, but rising cases may be beginning to have some effect.

Last week’s Chinese plenum — a meeting of the Central Committee of China’s Communist Party — was broadly in line with expectations.

There was a focus on growing new industries, encouraging more self-sufficiency and more emphasis on consumers.

Markets

Last week there was a reversal of the previous week’s risk-off trade — equities, bonds, commodities and gold all rallied.

The USD weakened despite the issues in Europe. This is supportive for commodities, gold and risk markets generally.

Growth recouped all the under-performance in the week ahead of the election, on reduced fiscal hopes and lower bond yield.

The vaccine is the next hope for the value bounce. This will need to be compelling to drive a significant reversal.

More cases, lockdowns, less stimulus, and a slow vaccine roll-out all suggest rates stay lower for longer, reducing impetus for a strong near-term value rotation.

The market was supported by what’s starting to shape as a good US earnings season. Expectations have been soft and a stronger recovery in Q3 GDP has flowed through into corporate earnings.

Among S&P 500 companies, 86% beat their quarterly earnings estimates, versus a long-term average of 65%.

Australia had a strong week led by REITs, industrials, and discretionary stocks, while defensives lagged.

Our market got an additional kicker when the RBA cut rates 15bp to 0.1%. Perhaps more importantly the Reserve cut the target level for 3-year bonds, launching a $110 billion six-month Quantitative Easing program, reinforcing the message that rates will stay effectively at zero for three years.

The prospect of further trade friction with China remains a risk. There has been speculation of additional measures on some goods – for example low-grade iron ore.

At this point Beijing may be happy to keep additional threats in the conversation without acting on them. But this issue must be watched.

Several positives are lining up that can support the market into the year’s end. These include:

1. Supportive global markets

2. Fiscal stimulus from Budget flowing through

3. Melbourne re-opening, perhaps more quickly than hoped

4. Borders re-opening

5. Pent-up demand as Australians stay home for Christmas

6. More stimulus from the RBA

7. Cautious positioning from investors

8. Potential for mergers and acquisitions (M&A)

We have seen results from three of the banks in the past fortnight, and the outlook remains unconvincing.

Revenue trends remain challenged. Credit growth, while stabilising, is still low. Margins remain under pressure and any tangible benefit from cost-out is an FY22 story.

However, they remain propped up by the likelihood of lower bad and doubtful debts (BDDs), which supports the capital position and headline earnings, bolstering the dividend yield.

Without BDD deterioration it is hard to see the sector underperform materially. But neither is there much catalyst for outperformance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Here’s the bond market outlook from Pendal portfolio manager Tim Hext ahead of this week’s interest rate decision and US election. Reported by portfolio specialist Dale Pereira

It’s all about this week.

Quantitative Easing and Blue Waves. Two expressions seldom mentioned — let alone together in a sentence. But Tuesday and Wednesday all will be revealed.

The RBA has been talking about rate cuts and likely Quantitative Easing (QE) for several months. Now it’s delivery time.

Yield Curve control, cash rates to 0.1% and Exchange Settlement to 0.01% look likely. QE of $100 billion in bonds and semis out to 10 years also seem likely.

Soon after polls will open in the US. By lunchtime Wednesday in Australia results will be flooding in.

The presidential race is critical and the US Senate may be on a knife’s edge.

A Joe Biden victory will mean massive stimulus with a Democrat Senate but major blocking if the Republicans hold it.

A Donald Trump victory would likely pave the way for decent stimulus because both a Democrat and Republican Senate would likely support it.

With new waves of Covid in Europe and the US, there is little doubt that extra fiscal and potentially monetary stimulus is needed.

Markets are largely priced for it. Only a contested election or a hostile senate can block it because both presidential candidates will want to start a term with a massive boost.

The balance of probabilities should be risk friendly, with only contested outcomes a landmine in waiting.

By Wednesday evening we should know where investment markets are headed for the next few months.

As always markets will move fast and we have our plans in place to adjust positioning for the outcomes. We want to make sure we are proactive — not reactive — to the news, a mistake many made in 2016.

Even as the US election result eventually becomes yesterday’s news, whoever is in power will face the tough task of rebuilding the US economy.

There may be some very short-term wobbles, but bonds should still perform. The main data point in Australia last week was the September quarter CPI.

A childcare-led bounce-back from the June quarter meant a 1.6% headline number or 0.7% Yearly. Underlying was 0.4% or 1.2% yearly.

All in all inflation has held in well this year. Goods prices are going up while services flat line — the reversal of a near 30-year trend.

While Covid is partly behind this — and it’s too early to call a trend — we will be keeping a close eye on how this unfolds in the quarters ahead.

Massive fiscal stimulus and the re-emergence of demand and supply could see prices tick higher in 2021 — a welcome development for the RBA but not the current market view.

And did we mention the Melbourne Cup? Avilius at $40 is a good outsider but this does not constitute a trade recommendation.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

It’s a busy week. Here are the key factors ASX investors need to look out for, according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

LAST week was eventful and this week promises to be the same.

The surge in new US and European Covid cases led to the start of lockdowns in Europe. In the US we also saw speculation that the election may be tighter than people expected a few weeks ago, while results season has been a touch disappointing.

Meanwhile Pfizer announced that the interim results of its vaccine trial would be delayed.

Domestically, the Queensland government announced its intention to maintain restrictions on travellers from Sydney.

The upshot was softer markets. The S&P/ASX 300 fell 3.87%, while US equities were off 5.62% (S&P 500).

The next few weeks will be important in terms of overall market performance and whether we see a rotation to value within equities.

The key issues:

• Will rising Covid cases stress healthcare systems in Europe and US?

• The degree to which containment measures drag on these economies

• The outcome – and timing – of the US election results

• The timing of relaxed interstate restrictions in Australia

• Any meaningful initiatives from the Chinese 5th plenum

Covid outlook

There was a clear deterioration in new case trends last week, driven by a surge in Europe which is now running at double the daily new case load of the US.

Governments have imposed lock-downs. The most draconian measures are in France and the UK. Without new measures modelling in the UK and France signalled that the number of deaths was set to exceed previous peaks.

The rationale seems to be that sharp lockdown now – before pressure builds in hospitals and colder weather arrives – may mean restrictions can be eased before Christmas.

One key difference this time around is that schools will remain open. The hospitalisation rate remains manageable in the US.

This will be the critical issue to watch in Europe, with the swift rise in cases and onset of colder weather two key risk factors.

Hospitalisation rates in France are showing some signs of a plateau, although it is too early to call. This will be a significant test of whether new therapies and treatments, improved protocols and better protection of vulnerable people leads to a more manageable health outcome.

An absence of community support for lockdowns is evident with substantial backlashes in the UK and Italy.

There is a glimmer of hope. Case numbers appear to be falling in some of the worst-affected countries such as Czech Republic and Switzerland, albeit from very high levels. But the outlook for Europe is concerning, given the rapid spread of the virus.

Pfizer did not provide interim results for its vaccine trial. There were too few cases to report statistically significant results. The trial is ongoing.

US Election outlook

This remains a key factor in near-term market performance, as well as the potential to trigger a rotation to value within equities. There is a strong view that a Democrat clean sweep would see outperformance from the value names, given the scale of the fiscal package that would result.

There are estimates this could run to the tune of US$2.5 trillion versus something in the order of US$1 trillion under the Republicans.

There are three issues to focus on:

The Result

At this point national polls place Biden’s lead at 8.0%, versus a 2.9% lead for Clinton in 2016.

Most polling experts put the probability of a Biden win at mid-80%. One exception is Plural Vote which has shifted from mid-70% to 62%. It is worth remembering that pollsters adjusted their methods after 2016. The chance that they have over-compensated and Biden does better than expected can’t be ruled out.

Betting odds are 65:35 to Biden. There is little evidence of a strong late movement to Trump. But there are wildcards which mean the result is not a foregone conclusion:

• Scale of turnout may be a factor. Turnout was 55.5% in 2016. The last time 60% turned out was in 1968, and there has not been a 65% turnout since 1908. There are potentially 20 million additional votes to be cast over 2016.

• There are some signs that Republican pre-voting is higher than expected. There are also signs of movement in expectations in key swing states. For example Trump is closing the gap in Florida and Iowa, while Arizona may be closer to swinging Trump’s way. These must-win states for Trump would get him to 244 Electoral College votes, 26 short of the 270 needed. He would still need North Carolina and Pennsylvania to swing his way, or one of those plus Wisconsin or Michigan

• Pennsylvania remains critical for Trump’s chances. Despite a huge campaign focus he is still behind by a wide margin. In 2016 the polls here were wrong by 2.6%. This time he needs an error of 4.2%

Timing

The situation is complicated due to the scale of pre-voting and the fact that different States count these in different ways.

Results in key southern states such as Florida will likely be known earlier, while northern states (where there is less pre-counting) will come later. Pennsylvania could take a week. If it is a close result we could be in for a long wait, with both sides heavily lawyered up.

Super-forecasters have a 31% probability of the result being known by November 8 and 47% by November 26.

The Senate

The Senate will be major factor for potential fiscal stimulus size and the degree to which Biden could enact his policies.

The race has become tighter, with a Democrat senate now at 55% probability.

The close States to watch are Georgia, South & North Carolina, Iowa and Arizona. In Iowa and Arizona polls are now moving the Republican way in the Presidential race, which suggests the prospect of a 50/50 or 49 Dem / 51 Rep Senate is now possible.

On election day Virginia could be a bellwether. It should be a comfortable Democrat win, but can provide early sign of turn-out levels and a possible signal for trends in North Carolina – a key swing state for the Republicans.

Economic outlook

Australian monthly credit data was in line with expectations at +0.1% month-on-month and +2.0% year-on-year.

This was the first increase in five months. Mortgage credit grew 0.4% month-on-month. This was the highest level since August 2018, highlighting better performance in the housing sector.

Owner-occupier credit was up 0.5% m/m (+5.4% y/y) and investor loans were up 0.1% m/m (-0.4% y/y).

Globally, European economic trends are softening as Covid cases rise, but we are seeing policy easing. Asia and the US continue to hold up well, while globally capex is generally doing better than expected.

Global Q3 GDP played out better than anyone hoped, but Q4 is now seeing downgrades.

We continue to remain relatively confident in economic recovery despite Covid’s resurgence, driven partly by the previous stimulus which has helped build a buffer supporting growth.

US personal income levels have dropped as support packages have rolled off, but still remains higher than at the start of the crisis.

The jobs recovery is holding income levels at reasonable levels despite a lack of stimulus. Savings rates remain elevated providing a buffer for the consumer. This is also the case in Australia.

The latest Covid surge does not appear to be affecting activity levels in the US. But it’s clearly starting to have an impact on European activity according to the latest mobility data.

The challenge here is that the policy response in Europe is complicated due to ECB limitations on funding to countries to provide additional stimulus.

There is a clear risk that European economic signals will deteriorate meaningfully in the next few weeks.

News out of China’s plenum will be important this week. Currently Chinese economic indicators continue to go reasonably well.

Markets outlook

The key issue is how the combination of the pandemic, US election and policy responses will impact on the potential for rotation in the market.

We are at historical extremes when it comes to the outperformance of growth over value and also on the latter’s valuation premium. A relatively benign outcome and removal of uncertainty could trigger a rotation to underperforming value stocks.

In terms of performance last week was a big risk-off week – with nothing other than bitcoin working.

There were several concerns (detailed above) but the fact that gold also underperformed suggests the market is cutting positions and awaiting outcomes in key issues over the next few weeks.

US results season kicked off with big tech broadly in line with high expectations, but subsequently selling off.

So far we have seen materials and industrial earnings perform best versus expectations.

Last week Australian sectors were down across the board. Staples fell only 0.15% while Energy shed 6.71% as a proxy for global growth sentiment.

We saw domestic industrials affected by a further delay in re-opening borders. But we believe this will be short-lived and an opportunity to add to positions.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

BT Balanced Returns PST (ABN: 90 492 550 926) Termination

The BT Balanced Returns PST (ABN: 90 492 550 926) (PST) will be terminated on 29 January 2021.

Since the BT Balanced Returns PST was closed to new investors in 2012, there has been decreased demand from investors for the fund. In a recent review, the Trustee1 noted that the fund’s small number of investors and low funds under management means it is becoming less viable and, as a result, a decision has been made that it is in the best interests of investors for the fund to be terminated.

What does this mean for investors?

From 29 October 2020 any request for an application or withdrawal from the Balanced Returns PST will be assessed by the Trustee on a case by case basis and will depend on whether the price would be fair and reasonable for unit holders. If this cannot be satisfied, then the Trustee of the PST may not be able to process your request. If you have arranged regular scheduled contributions to be made into your investment, they may be returned to you.

Payment of the proceeds of your investment holding will be made by the end of February 2021 and credited to the nominated bank account we have on file for your superannuation account. A separate notice confirming this payment will be sent to the registered unit holder.

A small proportion of your holdings may be withheld to meet outstanding tax payments. If there are residual amounts owed to you after any outstanding taxes are paid, we expect to pay these to you by October 2021.

We understand that this is an important change and encourage you to seek independent financial advice from your financial adviser and specific tax advice from a registered tax agent.

What do investors need to do?

To ensure that the proceeds of your investment are credited to your preferred bank account, and that you don’t miss out on important communications about your investment(s), please contact us if your bank account or mailing details have changed. To do this, you can write to us at the following address:

BT for Pendal Fund Services Limited

Attn: Corporate Accounts Team

GPO Box 2675

Sydney NSW 2001

Your letter should include the following details:

− Your investor number: the C number found at the top of this letter

− Your investment name: BT Balanced Returns

− What you would like to change e.g. your address or bank details

− Authorised signature(s) for your account: this has to be what was nominated at the time of your investment application (i.e. authorised signatories must sign either individually or any two jointly)

We’re here to help

We can also help if you need historical transaction, to assist your financial adviser or tax agent to determine your taxation position (e.g. any likely capital gain impact) resulting from the termination.

If you have any questions about the PST termination, and your investment with us please call our Customer Relations team on 1800 813 886 between 8.00am and 6.00pm (Sydney time) Monday to Friday – we’d be happy to help.

[1] The Trustee of the Fund is BT Funds Management Limited (BTFM) ABN 63 002 916 458