Pendal has announced a new appointment to its Bond, Income and Defensive Strategies (BIDS) team.

Philip Treharne joins the team as a Quantitative Analyst from July 20.

Philip is a highly skilled quantitative researcher and investment analyst with extensive experience in portfolio management, research, modeling and trading.

In a previous role as a senior investment analyst at a systematic investment fund Philip specialised in strategy development and portfolio risk management.

Philip holds a PhD in Applied Maths from Cambridge University in England.

At Pendal Philip will reunite with another recent BIDS team appointment, volatility analyst Thomas Ciszewski.

The pair, who worked together at Deutsche Bank and SouthPeak Investment, will collaborate on key initiatives to ensure Pendal’s BIDS products are optimised for the new economic and market environment.

These appointments mean the BIDS team now operates with a dedicated equity volatility skillset.

Philip will report to Vimal Gor, Head of Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Which fiscal factors will impact investors in the months ahead? Here’s a quick snapshot from portfolio manager Tim Hext (pictured) of Pendal’s Bond, Income and Defensive Strategies team.

MELBOURNE’s second virus shut-down was the story of this week — and will no doubt cause slower-than-expected growth this quarter.

An increase in cases was expected as economies re-opened, but the speed with which this wave hit parts of the Victorian capital was a surprise.

Nevertheless, unlike the massive initial shock in March, markets barely skipped a beat.

Equities saw some moves within sectors, especially those exposed to the Melbourne economy. But overall equity and bond markets were almost unchanged.

The government will again play a key role in buffering the impact.

We have written a lot in recent months about the transfer of economic control from monetary to fiscal policy. Economists have turned their gaze from Martin Place in Sydney to Langton Crescent in Canberra.

A number of key markers will be laid in the months ahead. JobKeeper and JobSeeker are due to end in late September. We expect more colour in the weeks ahead on how they may be extended or adjusted.

Then a budget is due in October. The need to encourage investment should see more aggressive schemes and tax breaks introduced.

The big fiscal question is whether tax changes will be brought forward. The government has two big tax cuts scheduled for July 2022. The 19c tax cap is due to be raised from $37,000 to $45,000 and the 32.5c cap from $90,000 to $120,000.

This would bring significant tax relief to most taxpayers. Given the current environment these could be brought forward.

Another, more controversial tax cut is due in July 2023. This would establish a single tax rate of 30c for $45,000 to $200,000 — a massive cut for middle and higher income earners. Whether the Senate agrees to bring this one forward may be more controversial because it favours higher income earners.

Tax cuts would put more money in taxpayers’ pockets. But would they have the confidence to spend it rather than save it?

As always, lower income earners have a much higher propensity to spend — so it could be argued keeping JobSeeker at a higher level beyond September would be more help.

Other ways of injecting activity into the economy may be more difficult, short of handing out coupons rather than cash. Infrastructure is already operating at capacity and housing will not be helped by the static population.

Either way fiscal policy will be left doing the heavy lifting.

Graphic: Bloomberg

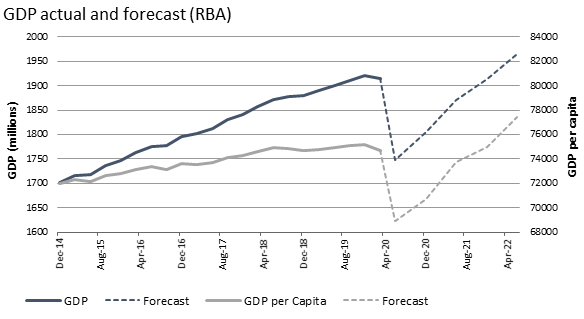

In regard to bonds, we continue to watch the massive excess capacity gap and attempts to close it.

The RBA expects GDP output to take until mid-2022 to return to pre-crisis levels — but even that looks optimistic.

Inflation will see the first negative annual print since the 1960s in late July. It will bounce back, but when combined with wage freezes, low population growth and sluggish housing, the medium-term outlook is not promising.

We remain comfortable that bonds will continue to do their defensive job in portfolios.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Pendal’s head of equities Crispin Murray (pictured) outlines how the US experience with COVID-19 and the latest vaccine developments are impacting the outlook for Australian equities.

Quick take-outs

- Despite negative sentiment from increased COVID-19 cases, equity markets continued to rise

- Economic data has been supportive, but there are early signs of a slowing in the V bounce

- We’ve seen some positive vaccine news flow

- Locally it’s an important week for sentiment with the risk that stocks leveraged to economic recovery could be impacted by the Victorian lockdown

As bad as it feels with the negative news flow around rising COVID cases in Australia and parts of the US, the market hasn’t responded as some may have expected — and has continued to grind higher. We are now at a juncture where:

- We could see a more significant leg down if case load data continues to worsen;

- But if evidence emerges that virus management has improved, we could get squeezed higher — bearing in mind that overall market positioning has turned more defensive.

Our portfolios are positioned defensively — but not aggressively so. We have stated several times in this weekly Australian equities note that a balanced portfolio with a good mix of recession insurance and recovery plays is very important in this unpredictable and fast-moving environment.

US Economic data surprises to the upside — but there’s evidence of the V stalling and no improvement in US case numbers

Published economic data continues to be positive.

Jobs data is strong, which has supported the market. On the employment front “Hours Worked” (+8.3%) and “Household Employment” (+6.6%) surprised to the upside. Similarly, the PMI diffusion indices are heading in the right direction indicating a stronger growth momentum than many anticipated.

We are now looking at an 8% drop in US Q2 GDP versus an 11% to 12% drop — as most estimates suggested we were facing a few months back. Still a lot to make up, but significantly better. Clearly interest rates will continue to be supportive.

However there is still some evidence that things are slowing. Markets must gauge not only the economic effect of the lockdowns, but a perception of risk that is deterring consumer spending.

A recent University of Chicago study concluded that sentiment — rather than the lockdowns themselves — are the biggest headwind. We know that only around half of the stimulus has been spent so far. This is something to keep watching in the US and Australia.

There are signs of this slowdown coming through in the last week in the worst-affected states of Florida, Texas, California and Arizona — which make up about a quarter of the US population. Restaurant bookings in the Open Table app tapered off quite sharply last week after a post-lock-down recovery.

Cases in the US continue to rise and hospitalisations are increasing — though they remain below the previous peak and deaths are still low. In Florida overall numbers are worse, though there is less strain on hospitals. In contrast, Phoenix and Houston are close to ICU capacity. We are now seeing “surge plans” implemented in many of these cities such as LA, including the deferral of elective surgery.

The data shows some smaller US states have seen improvements — but not the major states such as Florida, Texas and California.

Vaccine news flow is positive

One positive consequence of rising cases is the acceleration of some Phase 3 trials. There is some talk of the first batches being available before year-end.

The three main trials are:

- Moderna

- Aztrazeneca (in partnership with the University of Oxford)

- Pfizer (four variants of a vaccine in development)

Pfizer has just released results of Phase 2 trials on one of its vaccines, which indicate a) the drug is safe to use and b) it is triggering an immune response. This means it can progress to the final Phase 3 trial, which will be 30,000 patients. The rate of new cases actually helps determine the efficacy of the vaccines.

In the best-case scenario, the drug will be approved by October. Pfizer estimates it could produce 1.2 billion doses in 2021, which would equate to 600 million treatments. This shows the problem likely will not be solved by a single vaccine. To meet demand we will likely need several vaccines to be approved.

Pendal portfolio manager Amy Xie Patrick outlines the outlook for bonds and explains where to look for fixed income opportunities in this interview with online business channel Ausbiz.com.au.

Watch the video above or read the transcript below.

TRANSCRIPT

AUSBIZ.COM.AU INTERVIEWER: In the never-ending chase for yield, our next guest Pendal portfolio manager Amy Xie Patrick, is warning investors not to get spooked. She joins us live in the studio. Great to have you here. It’s a really interesting spot that we find ourselves in right now. We know of all the potential dangers, all the potential risks out there. But it’s as if is if there’s FOMO forcing people into equities as people are looking for a return that is hard to find.

AMY XIE PATRICK: Absolutely. I think you’ve hit the nail on the head. Is it because people want all this extra risk in their portfolios right now? I don’t think it is. The risks are well known, but the outcomes of those risks are still highly uncertain as it’s to do with the fact that we’re in a zero-interest rate world.

For most major jurisdictions in this world, policy rates are as low as those policy-makers feel they can go. In the search for return income yield, you have to grab whatever you can. I don’t think it’s so much that people want to go further out the risk curve, but we’re being forced to. When you come out of a crisis, you tend to be more risk-averse and thinking about saving for the future.

But when I put my savings in term deposits or my savings account, it gives me nothing. And I’ve got to think about my children, right? So how do I get some return out of that saving? I’m pushed further out the risk curve and the savings glut that the world was facing before.

AUSBIZ.COM.AU INTERVIEWER: Amy, the fixed income world is large and very wide. Where would you be investing in this type of market at the moment? Corporate bonds and investment-grade high yield, how would you be playing them?

AMY XIE PATRICK: There’s a great range of thought on this. The majority of the consensus seems to be that you need to chase more yield and government bonds simply don’t give you that much yield anymore.

You need to turn your back on them and go further out the risk curve — especially with the fed buying not only investment-grade debt, junk-rated debt and fallen angel debt. People feel safer going down the risk curve that way.

I would just caution against chasing risk too much down the quality ladder because, at the end of the day, the economic crisis and health crisis is still in full swing. It may mean chasing good headline income now, but what if those bonds default and they don’t pay you any income at all in the future?

You only need to look as far as Japan and Europe to see that just because yields start from a low point, doesn’t mean that they can’t go lower. The power of duration in fixed income means that if you buy longer-dated bonds, you get that beautiful multiplier effect as yield goes lower as well.

AUSBIZ.COM.AU INTERVIEWER: When it comes to Aussie 10-years now we’re seeing record lows. It’s trading at 0.9, 0.92%. Can it go lower?

AMY XIE PATRICK: A year ago, two years ago, the exact same conversations were being had right at 1.5%. Can they possibly go lower? You know, at 1%, can they go low? Well, they did go lower, so we’re just back around that one percentage level. A lot of people’s arguments with longer-dated bond deals and the reluctance to chase them because they think they can’t go lower.

It’s purely because a lot of central banks rightly or wrongly feel that at the zero bound that’s enough, they can’t deliver any more rate cuts. But if you compare the current episode to what happened in the global financial crisis, this hit to economic activity has been far worse than what happened in the GFC.

And yet the number of basis points of cuts that central banks have delivered have been so little compared to what they were able to deliver in the GFC.

Even though zero cash rate sounds like a really easy monetary policy setting. Actually, it might not be that easy. It might actually still be quite tight. And as long as policymakers don’t want to inject extra fiscal stimulus we’re locked at this zero lower bound at the front. How can long end yields really sell off meaningfully?

And then what if we get another shock? Even though lots of people say with yields so low, the asymmetry is actually that yields go higher. With all these risks, the asymmetry is probably still lower.

AUSBIZ.COM.AU INTERVIEWER: I’m curious to know when it comes to central banks when you hear the FOMC when you get minutes from the RBA, what is it that you zone in on to help form your view of where bond opportunities could go and where opportunities in fixed income could lie?

AMY XIE PATRICK: I think you just have to take them at face value. The consensus is deafening right now especially with the market rebound, equities are roaring up.

I think there’s a lot to hold central banks back right now. Not to say that they’ll always be held back, but for me, the more medium-term risk is not so much what the central bank says, but what our governments say.

Will this fiscal stimulus be with us for as long as the economy needs or will there be this urgency to claw back to some kind of fiscal discipline again? Will all that fiscal stimulus get withdrawn right before the economy gets traction in the recovery trajectory? And what happens then?

So it’s not so much reading what the central bank has said, because quite frankly what they say right now is fairly boring. They’re saying that we’re at zero, we’ve done as much as we can. Fiscal, please take over.

Amy Xie Patrick, Portfolio Manager – Bond, Income, and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

What is the outlook for retail REITs in a post-COVID world?

Should retail landlords charge rent based on a tenant’s turnover?

Pendal portfolio manager Julia Forrest tackled this hot issue at The Australian Financial Review’s Retail Summit on June 26, 2020.

Watch the video above.

Julia Forrest is a portfolio manager with Pendal’s Australian Equities team. Julia has managed Pendal’s property trust portfolios for more than a decade and has 25 years of experience in equities research and advisory, initial public offerings and capital raisings.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

INVESTORS are advised of the following change to the September 2022 distributions. This change is being made for operational reasons.

The funds set out below will pay their distribution (if any) for the September quarter in the week commencing September 26, 2022 for the period ending September 20, 2022. This change will be for September 2022 only.

Investors will receive distribution statements in accordance with our usual process.

Please call our Investor Services support line on 1300 346 821 if you have any questions.

Pendal funds impacted if paying a September distribution:

| Fund Name | APIR Code | ARSN |

| Pendal Active Conservative Fund | BTA0805AU | 087 593 100 |

| Pendal Active Growth Fund | BTA0125AU | 087 593 682 |

| Pendal Active High Growth Fund | BTA0488AU | 610 997 674 |

| Pendal Active Moderate Fund | BTA0487AU | 610 997 709 |

| Pendal American Share Fund | BTA0100AU | 087 594 509 |

| Pendal Asian Share Fund | BTA0054AU | 087 593 468 |

| Pendal Australian Equity Fund | BTA0055AU | 087 593 191 |

| Pendal Australian Share Fund | RFA0818AU | 089 935 964 |

| Pendal Australian Share Trust | RFA0004AU | 089 939 453 |

| Pendal Balanced Returns Fund | BTA0806AU | 087 593 011 |

| Pendal Diversified Global Equity Fund | BTA0316AU | 134 214 618 |

| Pendal Dynamic Income Fund | BTA8657AU | 622 750 734 |

| Pendal Dynamic Income Trust | BTA3816AU | – |

| Pendal European Share Fund | BTA0124AU | 087 594 429 |

| Pendal Fixed Interest Fund | RFA0813AU | 089 939 542 |

| Pendal Government Bond Fund | BTA0111AU | 098 011 048 |

| Pendal Horizon Sustainable Australian Share Fund | RFA0025AU | 096 328 219 |

| Pendal Imputation Fund | RFA0103AU | 089 614 693 |

| Pendal Japanese Share Fund | BTA0130AU | 090 666 621 |

| Pendal MidCap Fund | BTA0313AU | 130 466 581 |

| Pendal Multi-Asset Target Return Fund | PDL3383AU | 623 987 968 |

| Pendal Property Investment Fund | RFA0817AU | 089 939 819 |

| Pendal Property Securities Fund | BTA0061AU | 087 593 584 |

| Pendal Pure Alpha Fixed Income Fund | BTA0441AU | 161 859 936 |

| Pendal Short Term Income Securities Fund | WFS0377AU | 088 863 469 |

| Pendal Short Term Income Securities Trust | PDL8847AU | 645 793 862 |

| Pendal Sustainable Australian Fixed Interest Fund – Class R | BTA0507AU | 612 664 730 |

| Pendal Sustainable Australian Fixed Interest Fund – Class W | PDL3438AU | 612 664 730 |

| Pendal Sustainable Balanced Fund – Class G | PDL4756AU | 637 429 237 |

| Pendal Sustainable Balanced Fund – Class R | BTA0122AU | 637 429 237 |

| Pendal Sustainable Balanced Trust | PDL1098AU | 647 479 598 |

| Pendal Sustainable Conservative Fund | RFA0811AU | 090 651 924 |

| Pendal Sustainable International Fixed Interest Fund | BTA0509AU | 612 664 945 |

| Pendal Sustainable International Share Fund | BTA0568AU | 612 665 219 |

| Regnan Credit Impact Trust | PDL5969AU | 638 304 220 |

Pendal Stable Cash Plus Fund (APIR: BTA0459AU)

Increase to the Fund’s management fee effective 1 October 2022

Effective 1 October 2022, the management (issuer) fee for the Pendal Stable Cash Plus Fund (Fund) will increase from 0.15% p.a. to 0.18% p.a.

Why is the management fee increasing?

Since 2020, Australia has experienced historically low official cash rates due to the economic impact of Covid-19. On 1 July 2020, Pendal temporarily reduced its management fee for this Fund from 0.18% p.a. to 0.15% p.a. Although originally intended as a 12-month fee reduction, the lower management fee has continued to apply in light of the continued lower cash rates.

The management fee will increase to its original rate of 0.18% p.a. effective 1 October 2022.

There are no other changes to the Fund.

An updated Information Memorandum was issued for the Fund on 26 August 2022. Please contact us for a copy if required.

Pendal Stable Cash Plus Fund (APIR: BTA0459AU)

Important information

Reduction in management costs from 1 July 2020 to 30 June 2021

Due to the economic impacts of Covid-19, the RBA reduced the official cash rate from 0.50% to 0.25% on 20 March 2020.

With the cash rate likely to remain at a record low of 0.25%, the Pendal Stable Cash Plus Fund (Fund), currently offered to investors with a minimum initial investment of $500,000 at an issuer fee of 0.18% pa will be reduced to 0.15% pa effective from 1 July 2020, for a period of 12 months. Over this period, the Fund’s issuer fee will be reviewed and any changes will be communicated to investors prior to 1 July 2021.

Pendal Managed Cash Fund (APIR: WFS0245AU, ARSN: 088 832 491)

Increase to the Fund’s management fee effective 1 October 2022

Effective 1 October 2022, the management (issuer) fee for the Pendal Managed Cash Fund (Fund) will increase from 0.12% p.a. to 0.22% p.a.

Why is the management fee increasing?

Since 2020, Australia has experienced historically low official cash rates due to the economic impact of Covid-19. On 1 July 2020, Pendal temporarily reduced its management fee for this Fund from 0.22% p.a. to 0.12% p.a. Although originally intended as a 12-month fee reduction, the lower management fee has continued to apply in light of the continued lower cash rates.

The management fee will increase to its original rate of 0.22% p.a. effective 1 October 2022.

There are no other changes to the Fund.

An updated Product Disclosure Statement (PDS) was issued for the Fund on 26 August 2022 and is available on www.pendalgroup.com. If you would like a hard copy of the PDS, please contact us.

Pendal Managed Cash Fund (APIR: WFS0245AU, ARSN: 088 832 491)

Important information

Reduction in management costs from 1 July 2020 to 30 June 2021

Due to the economic impacts of Covid-19, the RBA reduced the official cash rate from 0.50% to 0.25% on 20 March 2020.

With the cash rate likely to remain at a record low of 0.25%, the Pendal Managed Cash Fund (Fund), currently offered to investors with a minimum initial investment of $25,000 at an issuer fee of 0.22% pa will be reduced to 0.12% pa effective from 1 July 2020, for a period of 12 months. Over this period, the Fund’s issuer fee will be reviewed and any changes will be communicated to investors prior to 1 July 2021.