Here’s the latest outlook for Australian equities from Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

EQUITIES continue to surge, driven by optimism over the pace of economic recovery.

The rotation away from defensives and growth to deep cyclicals and value continues. This is providing better breadth to the market as previous laggards start to catch up. It also continues to squeeze a market which has been defensively positioned.

Last week the S&P/ASX 300 gained +4.2%.

Economy and policy

The equity market seems to be disregarding earnings on the basis that everyone knows the current period will be woeful, while one year into the future is impossible to predict.

As a result, the delta on economic news flow is driving returns – and this remains better than expected.

Last week’s US payrolls are a case in point. Non-farm payrolls rose by 2.5 million in May – versus a consensus expectation of a 7.5 million fall. Unemployment fell from 14.7% to 13.3% versus a consensus of 19%. There is debate around the numbers and classifications used. However, the underlying signal is that re-hiring is better than expected.

While fiscal stimulus is driving better outcomes, monetary policy also remains very pro-cyclical as we are effectively at the zero bound.

A strong recovery leads to less fear of deflation, which means lower real rates, which helps further stimulus and higher valuations, creating a virtuous circle. This could of course turn vicious if we start to see economic expectations deteriorate – however for the moment the fiscal backstop appears sufficient.

The combination of these two effects is driving equity markets and squeezing the broadly consensus bearish positioning in terms of sector allocation.

Digging into the US job data, leisure and hospitality saw the best results, with an increase of 1.2 million jobs in May. However this was against 8.3 million lost in the previous two months. While the delta is good, this sector is still well below its high-water mark. There were an additional 400,000 jobs in construction, which has recovered almost half the jobs lost to Covid-19.

While unemployment is a lagging indicator, more real-time indicators are also constructive. PMI numbers are stabilising. While still signalling a contraction, the market is focused on the positive trajectory versus recent results.

Elsewhere US auto production estimates for Q3 are almost back to the pre-Covid levels. This has a positive read-through for supply chain inputs such as steel and components. Mobility data and trends such as AirBNB searches are likewise painting a picture of an economy recovering faster than many predicted.

The US FOMC meeting this week will shed light on their rate of asset-buying going forward and how they are seeing the economy. The next US fiscal package is expected to be announced in July at US$1 trillion to US$1.5 trillion – with a focus on helping the re-start rather than income support. This will be a more contentious process and could represent a risk to the market.

Markets

There is a view – backed by data on brokerage account openings – that retail money is driving this rally, supported by various government cheques.

We are mindful this market has shrugged off lot of bad news and uncertainty in the form of tensions with China and US civil unrest. ETF flows have been to defensive assets such as bonds and gold – while equity ETFs remain in material outflow since late March. The market is climbing the proverbial wall of worry, which is a constructive factor.

The reflation trade of the past few weeks continues to dominate price action. In equities, we see it in the continued rotation from growth to value, which is broadening the market’s rally. This can continue while the economic data remains supportive.

In other assets it is seen in US 10-year bond yields rising, credit spreads narrowing, a higher copper/gold price ratio and a stronger AUD.

There are a number of near-term issues to be mindful of:

- Valuation: P/E valuations have surged. Many see P/Es as meaningless given uncertainty over earnings and at this point the market does not seem concerned. However, this could change.

- Technicals: The market’s recent momentum has only been equalled 10 times in the last 30 years and suggests we might see some near-term consolidation.

- Put/call ratio: The case for near-term consolidation is supported by a shift in put/call ratios from super-bearish to a more optimistic stance.

The balance of probabilities suggests we might see consolidation – but not necessarily a material fall. But there are two issues that could potentially de-rail the market and need to be watched closely:

- A second wave of infections: The market’s concern here seems to be diminishing – which does leave it vulnerable to any resurgence. In this vein, it is important to understand the improvement in US case numbers is driven by the hardest-hit States of the north-east. Other States are showing flat-to-rising trends, albeit at low levels. Given we are seeing genuine second waves in places like the Middle East – particularly in Iran and Saudi – this needs to be watched.

- US Presidential Elections: Trump has seen support ebb and Biden is now the favourite for November’s election. The odds that Democrats win five seats to take control of the Senate appear even at this point. This raises the possibility of Democrat control of Washington – with policy implications in areas such as tax which could present a risk to equity markets.

Fixed income impact investment is a fast-growing but still relatively new segment of capital markets. Here Pendal portfolio manager George Bishay (pictured above) takes a deep look at impact bonds and answers questions we often hear from our clients.

EACH year, more and more sustainable bond investments become available, covering all aspects of the environmental and social spectrum.

There are bonds where companies in underlying projects reduce their carbon footprints and bonds that help finance companies with strong gender equality records.

Some bonds finance governments to build railroad and solar power plants, others help build affordable housing.

As the market rapidly grows, debate is intensifying about pricing and returns and how these bonds are trading in high-demand secondary markets.

More than $US465 billion of sustainable debt was issued globally in 2019 — a new record and up 78 per cent from the previous year. More than $US1 trillion in sustainable debt has been issued since the market began.

This growth is driven by soaring demand as investors seek ways to “do good” with their investments amid growing concern about climate change and social issues.

At the same time, corporations and governments are becoming ever keener to behave responsibly and to be seen doing so.

Types of impact bonds

There are two main types of impact bonds:

– Environmental bonds which finance projects that benefit the environment

– Social bonds which address a social need or improve an outcome for underprivileged people

Issuers are usually certified by an independent organisation such as the International Capital Market Association or the Climate Bonds Initiative.

Most of these bonds also adhere to the UN Sustainable Development Goals.

Why do companies issue impact bonds?

A key question we get asked is why corporations and governments issue impact bonds instead of traditional issuances. In our experience, they are issued for a number of reasons.

One reason is to signal confidence in the sustainability of a wider business.

Corporations issuing impact bonds are implicitly inviting scrutiny of their wider business practices and signalling they are confident in their sustainability credentials. This also leads to future benefits.

More and more traditional fund managers are incorporating Environmental, Social and Governance (ESG) factors into their investment processes.

This is partly because ESG risks genuinely affect performance and partly at the behest of end investors such as superannuation funds.

Companies that issue impact bonds are stamping their ESG credentials, which can ultimately be supportive of credit spreads they have to pay down the track.

A third reason is simply to cater for market demand.

Across the world investors are seeking access on behalf of clients to investments that are sustainable or make a positive change in the world.

Issuing impact bonds can also help diversify an issuer’s funding by attracting new types of investors.

Research also shows green bonds get the tick of approval from equity holders.

They can trigger a positive stock price reaction as markets react to expectations the bonds will improve long-term shareholder value by lifting company performance.

Examples of recent impact bonds include a $400 million, five-year bond issued by supermarket giant Woolworths to improve carbon emissions from refrigeration and lighting in its stores.

NSW TCorp, the bond issuer for the NSW state public sector, issued a $1.8 billion bond to further public transport projects and fund a sustainable water project.

Queensland’s QTC allocated bond proceeds to light and heavy rail projects, cycleways and a solar farm.

How do impact bonds perform?

It is true that impact bonds tend to perform well in the secondary market — but the reasons for this are nuanced.

We often say there is excellent secondary market liquidity for impact bonds if you’re looking to sell — but not so much if you’re looking to buy!

There should of course be no difference in pricing between impact bonds and their vanilla counterparts. This is true because the same credit risk applies to non-green bonds issued by the same issuer.

The credit risk is that of the issuer, not the underlying green or social projects.

This is most pronounced in bonds issued by supranationals such as the World Bank. The collapse of an underlying project has no effect on bond holders, who are assured by the triple-A rating of the World Bank itself.

Fundamentally, this also means investors are not penalised for investing in green bonds.

Investors in impact bonds get the same credit spread as if they invested in an equivalent vanilla bond from the same issuer.

Nevertheless, a “greenium” — a premium paid for green bonds — can be observed from time to time in the secondary market.

Often the explanation for the premium is simply an excess of demand over supply.

When Woolworths issued its first green bond last year it found demand five times stronger than its issue size and priced better than initial guidance. It traded even more strongly in the secondary market.

Whether this was demand for the green aspects of the bond — or simply demand for exposure to Woolworths — is difficult to determine.

But this differential can be a benefit for dedicated sustainable fixed income funds buying in the primary market. They are often handed a better allocation than a competing vanilla fund, putting them in an advantaged position in the secondary market.

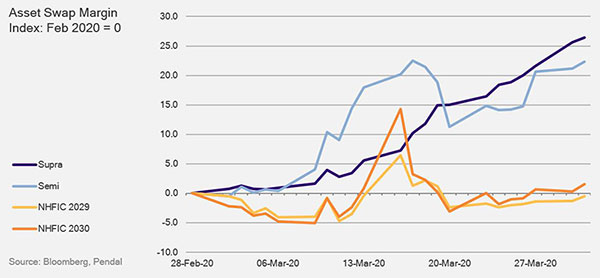

During increased volatility at the end of the March 2020 quarter we saw one of our impact holdings do very well relative to a similar non-impact bond.

The bonds were issued by the National Housing Finance and Investment Corporation (NHFIC) — an independent Commonwealth entity that operates the Australian Affordable Housing Bond Aggregator.

This organisation provides cheap, longer-term secured finance for community housing providers by issuing bonds in Australia’s debt capital markets.

The funds raised by the bonds were loaned to community housing providers to help finance more than 2000 properties in Victoria, NSW, Queensland, Western Australia and South Australia.

This included supporting the supply of more than 360 new social and affordable dwellings.

The bonds, which typically trade in line with other supra nationals and semi-government bonds, outperformed in March 2020 as can be seen in the chart below.

Looking ahead

The truly dedicated sustainable funds are not yet big enough to soak up all the impact bonds issued in Australia.

Some $6 billion of impact bonds were issued in Australia last year and the pure impact funds accounted for only a sliver of that supply.

This has the effect of keeping pricing in line with non-impact bonds.

Vanilla funds are required to fill the book and need to be offered at the same pricing as they would get in an equivalent non-impact bond.

Only when the dedicated sustainable sector is big enough to take out whole books will we start to see some difference in pricing.

Right now, that looks to be some way off.

George Bishay is a portfolio manager in Pendal’s Bond, Income & Defensive Strategies team.

George has managed dedicated Sustainable fixed interest portfolios for a decade. He has also worked across numerous fixed income, credit and money market portfolios in portfolio management, credit analysis and dealing roles for over 20 years.

In 2019 he was awarded the Alpha Manager status by Money Management’s FE fundinfo, in recognition of his career-long performance in the asset management industry.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Our Pendal’s Chief Executive Officer, Australia, Richard Brandweiner discusses why the way we invest can make a big difference to the world around us.

Watch the video above or read the transcript below.

TRANSCRIPT

My name is Richard Brandweiner, and I’m the Chief Executive of Pendal in Australia.

These are very challenging times, but they remind us of just how interconnected our world is, how our economy and our financial markets are intrinsically linked to our human ecosystem.

Also how important it is, the decisions that we make, and how we treat other people, what the ramifications are. That’s perfectly true with our capital and our wealth as well.

The way we invest can make a big difference to the world around us and importantly the world into which we, or our children, are going to retire.

And that’s one of the reasons why we’re seeing such extraordinary growth in sustainable and ethical investing.

Consumers are increasingly demanding different things from their service providers. It’s no longer just about what product or service you provide, it’s also important how you go about it.

Impact investing, in particular sustainable and ethical investing, has become the fastest-growing part of the investment management industry.

Pendal has been in this space for a long time. We launched our first ethical fund back in 1984 and more recently we fully acquired a business that we helped establish called Regnan.

It’s one of the leading institutional providers of ESG research, engagement services, and advisory work.

We’re very keen to support you in the journey towards an increasingly sustainable capital system and towards empowering your clients to invest in positive ways that make them proud, together with growing their wealth and their family’s wealth.

Thank you.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities.

Regnan is a global leader in long-term value, systemic risk analysis and responsible investment advice. Last year Pendal appointed a London-based impact investment team to launch a Global Equity Impact strategy in late 2020.

Regnan is wholly owned by Pendal Group.

Here’s the latest outlook for Australian equities from Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

STOCKMARKET sentiment has been buoyed by a roll-back of restrictions and anecdotal evidence that some parts of the economy are recovering faster than expected – possibly as the result of pent-up demand.

That helped the S&P/ASX 300 to a gain of +1.9% last week. A second wave of infections remains the key risk – however this is too early to call.

The Australian equity market has consolidated earlier gains from the low and has effectively traded sideways over the last 30 days – albeit with material volatility.

It has also seen significant rotation within the market – this is driving investment opportunities.

Economic re-start

The market is now in an optimistic mood around economic recovery as restrictions are rolled back.

There has been talk of V-shapes, U-shapes and L-shapes in terms of recovery. We see a strong possibility of a “reverse square root shape” – a sharp drop and then strong initial recovery, levelling off at a lower range than the initial point.

We are seeing demand recover faster than many expected in several sectors. But there’s a risk that after an initial surge it then falls short of expectations and we see a more protracted economic slowdown.

The key factor is that the recovery is not evenly spread. Sectors such as durable goods, autos, take-away restaurants and housing are proving more resilient here and in the US. Other areas such as tourism and entertainment are likely to face stiffer headwinds.

Some key observations on sectors:

• Traffic data is very strong in the US as people avoid public transport. We are seeing this start to feed through to auto demand as ride-sharers now opt for their own vehicle. This may have implications for steel.

• Homebuilding seems to have held up much better than people expected. In the US new orders are stepping up and prices remain resilient. It is important to remember both the US auto and housing sectors were coming off relatively subdued bases, which helps in the pace of recovery.

• There are signs that retail is quickly bouncing back. Some 75% of Australian retailers have re-opened their doors and, anecdotally, are seeing decent sales. It will be important to see how much of this is an initial surge of pent-up demand.

All this has important implications for the portfolio.

If we return to 90-95% of the pre-COVID-19 economy, there will be some parts at 80% and some at 100% or even higher. It will be important to identify the outlook for each individual company or industry and position accordingly.

We also need to remain mindful that, despite current optimism, the economic data will be awful. The hit to Global GDP, ex-China, in 2Q 2020 could be somewhere in the vicinity of 40% – even with the current bounce.

While the market seems well-supported at the moment, there are medium-term risks.

Longer term we remain mindful of the consequences of current policies and the potential for deflation.

Health outlook

It is too early to draw conclusions about the risk of a second wave of infections. In coming weeks we need to remain focused on case loads as countries open up.

High levels of testing and awareness of social distancing may help alleviate some risk. Warmer weather in the northern hemisphere may also help.

(continued below)

VIDEO: Crispin Murray explains the current market environment

(continued from above)

A surge in optimism over the Moderna vaccine trial may have been premature, but expert opinion seems positive about discovering a vaccine.

A coronavirus vaccine for humans has not previously been found, however focused efforts and widespread use of modern technology platforms are encouraging.

More trial results are expected in June.

Policy

China’s leadership avoided the traditional GDP target at the annual National People’s Congress last week.

Some took this as a bearish signal, on the view that authorities will not feel compelled to stimulate to hit a target. However it also probably has a lot to do with the degree of uncertainty around global demand for Chinese exports.

There is also some disappointment at the scale of bond issuance to fund growth projects – also seen as suggesting less stimulus. We believe Chinese authorities remain focused on job creation and social stability.

The Chinese economy has seen a decent recovery. The smaller scale of stimulus perhaps reflects a desire to pause until some evidence of the effect of global demand comes through before enacting new measures.

Some of the initial US fiscal program are nearing expiry. However there is scope for extension of the Paycheck Protection Program – one of the more important packages – which is critical for small businesses.

Politicians continue to wrangle over the form of the next US fiscal package. The market expects up to a further $US1 trillion in spending – though this may not be until late June.

A key debate here and in the US is how to incentivise workers who may feel better off on government support. This may result in changes to the structure of government programs.

Markets

Looking at some of the key indicators we flagged last week, gold and the USD were largely unchanged last week, while US 2-year yields rose a little.

The latter remains an important indicator of the market’s expectation of negative rates.

The Australian equity market has been effectively trading sideways since April 13.

This is constructive in the sense that it has held onto gains from the March 20 low and has managed to consolidate. However there has been a material rotation within the market.

Over this period small caps (+13%), resources (+11%) and discretionary (+8%) have all outperformed, reflecting an improvement in sentiment.

Defensive names that did well in the early phases of the crisis – such as health care (-6%) and staples (-3%) – have underperformed.

Financials have underperformed right through the crisis. We have been broadly underweight and have benefited from this.

However we are mindful of the degree to which they have lagged. We remain cautious on the banks, but insurers are starting to look interesting as we think the market is over-discounting the risk of pandemic-linked claims.

REITs (+4.4%), Resources (+6.4%) and Small Caps (+4.4%) all outperformed last week as sentiment remained positive. The banks (-1.3%) dragged.

Crispin Murray is Pendal’s Head of Equities. Crispin has more than 27 years of industry experience in equities and a strong track record leading Australian and European equities funds.

He is responsible for managing a number of our flagship funds and leads one of the largest equities teams in Australia.

Pendal’s Head of Equities Crispin Murray outlines his thoughts on the current market environment.

Watch the video above or read transcript below.

TRANSCRIPT

Hello everyone. My name is Crispin Murray from Pendal Group. I thought I’d take the opportunity today to share with you our thoughts on the current market environment and how we at Pendal invest and manage money on behalf of clients.

One of the attributes we believe in is being upfront and transparent in our views.

If I was to summarise the current situation, I think it represents perhaps the greatest challenge for investors in many years, but also it presents some of the greatest opportunities we have seen.

This is because we’ve got a combination of a really bad economic situation with perhaps the greatest policy stimulus we have seen — and overlaying this, a huge health challenge and substantial technological change.

In combination this is changing the way consumers and businesses operate.

This leads to three levels of uncertainty — economic, industrial and corporate. We believe the more uncertainty there is, the more mispricing in the market there is, and that is what creates the opportunity.

We also believe this environment plays to our strength. We have a strong organisation. We have a real breadth of resources, a lot of experience across many cycles and strong corporate relationships.

Two key questions for investors

When it comes to investing, there are two key questions to answer.

The first is how you make money for your investors and the second is what is your competitive advantage.

When it comes to making money, we believe that anticipating change is the key. Investing is about what happens next.

When it comes to competitive advantage, ours comes from an information advantage.

We have a large team with a real focus gathering primary information. We think of the team as being similar to investigative journalists. We have a lot of meetings, gathering information we use to make good investments. We believe in a culture not of commentating, but of actually thinking and investing.

Three pillars

There are three pillars to delivering this:

1. The first is the business model.

We are an Australian listed company. We are independent. All the staff are shareholders and we’re very much aligned to our investors. In addition, we have a dedicated management team, which means there are no distractions for those investors. They can get on with the job of identifying good ideas.

2. The second pillar is the team.

We’ve got 18 people in our Australian equities team — 22 years average [industry] experience, 14 years within the group. This means they understand market cycles, they understand the industries they’re looking at and they have a huge list of good contacts.

It’s that experience and understanding that is critical at these types of points in the cycle.

Because it’s remaining calm, focussing on the controllables, identifying opportunities that comes from that, that is the thing that will make a difference.

3. The third pillar is process.

We’ve spoken about the philosophy of identifying what’s going to happen next. We believe that you make money when something is changing for the positive in a business — and [when] the market’s not realised that and it’s not yet in the price.

When we do this, we need to then drill down into five key factors that we watch incredibly closely.

I want to highlight two of these.

1. The first one is business innovation.

Take a company like Xero, which is the cloud-based accounting software for small businesses. This is a company that has really been a leader in the industry in driving penetration globally. We believe it’s got a product suite that is still not fully appreciated by the market, that will allow it to drive penetration and increase their revenues from their customers.

That’s a good example of where innovation can drive opportunity.

2. The second category that I’d highlight is the self help category.

These are companies that are doing something themselves to improve their position. Often it comes in the form of cost and productivity.

Santos is a great example of this. They’re in a tough business — oil prices are very low, but they are a low-cost player with a good balance sheet.

They’re very proactive in terms of how they manage capital. We believe that will hold them in really good stead, particularly if you start seeing the economies improve.

So it’s a combination of these factors that we believe have allowed us to deliver strong performance over the long term.

And we highlight our Focus Fund performance. This is our concentrated best ideas portfolio and the basis of the SMA.

Not only has it been able to deliver very strong performance, but it’s also been very consistent performance and it’s been doing it for a long time.

It’s been through many cycles. It’s been able to be very consistent. Even when there’s been periods of underperformance, they have tended to be limited in terms of the drawdown and the recovery of that performance has happened quickly.

Market outlook

If I turn now to our view on the market. We believe we are in the fourth phase of this market environment.

We’ve gone from the focus just being on China, to an indiscriminate sell-off, followed by strong bounce. Now we’re in what I would call a protracted discovery phase.

How bad will the economies be? How will companies fair? This is a time when information and insight can add a lot of value. You’ll see that we identified the key swing factors.

The critical issue is the ability to restart the economy and how quickly and sustainably it recovers.

Four scenarios

To better assess this, we’ve presented four scenarios.

The first scenario to consider is the potential for a rapid medical breakthrough whether that be a vaccine or antiviral treatment.

If there was a dramatic breakthrough it would clearly be very positive for the market — and that would happen well before the availability of those treatments because it would impact on confidence.

This is a-low probability scenario, but it does have a very significant potential effect on the market. So it’s something that needs to be aware of.

The other three scenarios are less constructive but are more likely in terms of outcomes.

The most positive scenario one of these is the potential for certain countries such as Australia and New Zealand to actually eliminate the virus and then effectively close down their borders and remain separate until a vaccine was available.

The middle scenario is a more managed mitigation, which allows your economy to ramp up, though perhaps not to where it was before.

The third scenario is the most negative one, if we get waves of re-infection, which really impact on the economy.

Recently I was talking to some of the academic experts who’ve been working with the government. It’s worth noting that the difference between an elimination strategy in Australia, and a managed mitigation one, could be worth $2 billion to 8 billion a month just for our economy.

So it does highlight the variety of outcomes that we could see.

While we spend a lot of time understanding the developments and risks on the medical and economic front, the reality is we know it is really impossible to predict what’s going to happen.

What we need to do is weigh up these different scenarios and position the portfolio for that.

It’s important to stress as investors, we’re not going to be taking binary risks with our clients’ money.

We invest where we have insight and where we expect to get a good return. So we’re positioning our portfolios to find the best stocks for those different outcomes.

The categories of stock that we’re considering:

Firstly, recession protection; stocks that are policy beneficiaries; companies that are good businesses which we expect us to bounce back strongly when the recovery occurs; and finally, recovery plays and stocks that have been discounted the most heavily because they’re most immediately affected by the crisis.

We’re looking for different attributes in each of these categories in terms of the best stocks. But ultimately they do boil down to those factors we identified earlier — which reflect in terms of the quality of the industry structure, but also the quality of the management and their ability to respond to the environment we’re in and their ability to allocate capital well.

I hope that’s given you a taste of how we invest at Pendal.

Yes, this is a really uncertain time for investors, but that also means it is a time where there are a huge number of opportunities.

I believe the experience that the team at Pendal has can deliver on those opportunities for you and your investors.

Thank you for your time and I wish you all the best.

Crispin Murray is Pendal’s Head of Equities. Crispin has more than 27 years of industry experience in equities and a strong track record leading Australian and European equities funds.

He is responsible for managing a number of our flagship funds and leads one of the largest equities teams in Australia.

Find out more about Pendal’s investment capabilities

How will deflation impact investors in a low-rate environment?

Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor (pictured above) explains in this plain language keynote presentation from the Conexus Fiduciary Investors Symposium on May 19, 2020.

TODAY I want to run through some of the unprecedented numbers we’re seeing and outline how this economic environment could play out.

What is the economic outlook?

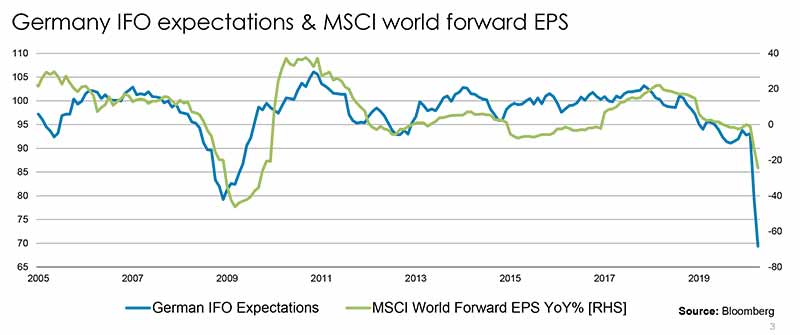

Let’s put the current situation in perspective. Take the non-farm payrolls number (see below). This graph, which goes back to 1940, puts into context how monumental this slowdown has been.

It’s becoming more of a consensus view that the size of the lockdown — and the commensurate policies that have come with it — have largely been the wrong ones.

We arguably shouldn’t have stopped the economies as quickly as we did. We should have followed a different model and now we’re trying to pull ourselves out of this massive economic contraction we are experiencing.

There is no getting away from the fact that this is a massive shock.

Shocks historically have started in the financial system, for example the dot-com and GFC crises. This one started as a health crisis which flowed into economics then through to financial assets. So it’s a very different beast than the crises we have seen before.

That is why the authorities have had so much trouble dealing with it.

This chart below shows Germany, but I could have used pretty much any country.

I’ve used the IFO expectations which is a PMI and I’ve just put it up against MSCI world for EPS. We can see how the situation is going to get worse before it gets better.

Global data is awful. The April US retail sales number was down 16% — which puts it down about 30% since February (excluding food).

It is quite clear many businesses will not survive this crisis. High-end restaurants run with a margin of around 5% to 8% and they’re going to be running at 10% to 30% capacity.

Yes, we have dealt with the liquidity issue but we’ve got a solvency issue which is going to come up and hit us later. Do we have enough firepower to deal with that?

We’re going to see a tsunami of bankruptcies — there’s no other way to think about this.

The reason we’re not seeing these bankruptcies already is the government lockdowns and life-support mechanisms are delaying the process.

We can see here that earnings are going to be terrible. But we know the S&P is down only marginally from the levels we came into the year — so what’s happening?

It’s about multiple expansion. P/E multiples expanded on the back of liquidity, but earnings have been decimated — and it’s very clear earnings are going to get hit further.

Central banks responded very quickly. They did the usual: conventional monetary policy, cutting rates to zero. This was followed by unconventional monetary policy, yield curve control and more quantitative easing at a size we’ve never seen before.

Quantitative easing in the US is five times the size of all the quantitative easing we’ve seen in the last 10 years put together — unbelievably large.

The Fed and other central banks then started going into the fiscal policy area — somewhere they’ve not normally gone before.

They start supporting the markets and the economy directly, bypassing the banking system.

The Fed and central banks around the world have thrown every measure they possibly can to get rates down and flood the system with liquidity.

It’s my strong belief they will have to take rates negative. They don’t want to take rates negative — Powell talked about that last week about the fact that they don’t want to do it.

We know operationally the US isn’t ready yet and there is very strong resistance from the lobby groups and the banks.

But when nominal interest rates are 50 basis points in the US and you’re going to get a big wave of deflation, you’ll have real interest rates rising — which is just going to crunch the US economy further.

So, we believe the only material thing the Fed will be able to do is cut rates to negative with a short, sharp shock the way Kenneth Rogoff has recommended.

They clearly don’t want to. But I think there’s no choice — which would mean bond yields across the world would go negative as well.

What are defensive assets today?

While yields are already low, you can very clearly own 10-year Treasuries until they’re at -1%. I think they’ve got a lot of juice left in these markets. People don’t want to be owning them here but they should be.

The more bonds rally, and the lower yields go, the more people will need to buy them.

The Fed has done everything — conventional monetary, unconventional monetary and now they’re doing fiscal policy.

This chart shows investment grade spreads relative to non-manufacturing PMIs:

You can see we’d be off the scale if the Fed wasn’t artificially supporting credit spreads — we’d be at 600 to 700 given the non-manufacturing PMI.

The slowdown in the economy should lead to much wider spreads — but it hasn’t because of the backstopping by the Fed.

Not only is the Fed backstopping investment grade corporates via ETFs, they’re now doing high-yield fallen angels.

They’re effectively doing everything they possibly can to stop the markets dislocating and to plug this hole. But what they’re doing is plugging a solvency hole with liquidity, and ultimately it will fail.

We know the size of the central bank response has been massive, but then we had this coupled with the response by the governments as well.

This chart below shows the change in cyclically adjusted primary fiscal balance, this measure will give you an idea of how big the government fiscal response has been.

You need to think about this in terms of the US.

I’ll put it in perspective in terms of the US.

We came into this crisis with a fiscal deficit around 5% in the US. That’s ridiculously large on the back of the longest expansion in history. Plus we’re at full employment.

We came into COVID in the worst situation. We had very high debt levels in both government and corporate debt, and investors had portfolios which were pushed out the risk curve as they stretched for yield

So the virus hit us at exactly the wrong time.

Coming into this crisis the US was running a 5% fiscal deficit, we’ve now had support packages in the region of 15%. The economy has slowed dramatically which will lead to a drop in tax revenue of about 3% to 5%.

Nominal GDP is also going to detract about 5% over the calendar year, so we’re looking in the US for a fiscal deficit somewhere 20% and 25% of GDP.

This next chart shows you how unsustainable this is. The US Congressional Budget Office (CBO) estimates below show numbers back to 1790.

There’s zero chance they’re going to be able to pay this money back. Zero chance.

So how will they close the hole?

They have to defaults — either implicit default through inflation (the preferred course of every central bank and government in the world) or explicit default (restructuring, tax rises and spending cuts).

We talk about rebuilding the budget in Australia and trying to pull things back.

But there is zero chance across the world this money’s being paid back, so we need to engineer inflation or we need to do some type of debt jubilee, or a combination of the two.

The outlook for inflation

Lots of things drive inflation over the long run.

Factors that have kept inflation down over the last 30 years include the three Ts — trade, tech companies and titans.

Up until recently we had free and growing trade; we’ve had the influence of the tech companies (eg Amazon and its pricing power and ability to push prices down); and the titans (the rise of massive companies with oligopolistic or monopoly positions).

You’ve also had the two Ds — debts and demographics.

All these factors have been weighing on inflation. It’s quite clear here in the next chart showing M2 minus real GDP — but you can put any measure of money supply for any country in the world and the US is the poster child for this.

Money supply is absolutely ballooning.

Initially, the run-up in the money supply was unexpected as corporates drew on their revolving lines of credit.

That increased money supply as the banks were forced to lend to them. Then the Fed began pumping money in the system.

The three-month change in M2 in the US shows it is running at over 100%.

These are numbers you couldn’t even imagine. At some point that will start feeding through to inflation.

When you think of Irving Fisher’s theory of money, on one side you’ve got money supply and on the other side you’ve got velocity. Multiplying the two together gives you nominal GDP.

But the velocity of money’s been falling since 2006-07 because the economy’s been slowing, nominal GDP is coming down and nominal interest rates have been falling.

Now it’s been falling off a cliff because there are no transactions happening in the economy.

The government’s trying its best to slow down the velocity of money by throwing all of these fiscal packages at it. At some point, whether it’s six months or a year when we start coming through this, we’ll see velocity of money stop falling and then probably start rising.

That means you’ve got this massive money supply up against the velocity which isn’t falling. That has to lead to higher nominal GDP and nominal inflation.

There is no question in my mind that we will be hitting an inflationary episode in the US over the coming medium-term — one to three years out.

I think that’s what the governments want. They want to deflate the debt away.

Even before the virus, the Fed told us they wanted to move to average inflation targeting — running inflation above the target to get the 15-year average up.

Now they might have to run this at 3% to 5% — so you’re talking some quite big numbers. The problem is we’re going to hit deflation first, then inflation after.

In the long run you get these structural forces — monetary policy, fiscal policy, demographics, debt, trade, etc — which influence a long-term inflation rate.

In the short run inflation is largely driven by the business cycle. It’s quite clear we’re going to hit GDP growth of minus -5% in the US this year, which will give you a deflationary environment.

The thing that really worries me in the US is the fact that shelter inflation — the part of inflation that has been holding up the inflation rate in the US — is now flat and starting to fall.

Excluding shelter, the CPI number we saw last week was 0.6% and this is falling rapidly.

So we’re going into a deflation episode in the US. I think the Fed has to counter that with negative interest rates.

Then when we start coming back to work and hopefully get a vaccine, that point is going to be super inflationary because I cannot see an environment where the central banks of the world pull back monetary policy anywhere near the pace they need to.

It’s quite clear they and the governments have over-delivered. They’ve filled a solvency issue with massive short-term liquidity.

When we talk about the deflation-inflation picture we can’t forget about the US Dollar’s role as the reserve currency. They call it the exorbitant privilege.

This shows you what that privilege is worth. You can see on this next chart as currencies weaken you tend to see bond yields fall.

The US can get bond yields falling while the currency strengthens and that’s a massive advantage.

The world certainly doesn’t like that advantage. China, Russia and Europe don’t like it. There will be a move away from the dollar standard at some point — it’s just a question of how long it takes.

I think that will go hand in hand with some kind of debt jubilee over the medium term and some greater role for crypto currencies.

The focus of the crypto world is Bitcoin for me. You can like it and not be part of the shiny hat brigade. All you have to do is accept the fact that crypto is going to be a much greater part of the financial markets going forward.

Most of the world’s central banks are currently working on crypto and some kind of stable coin right now. These are the equivalent of IMF SDRs — there is no doubt it will become more mainstream.

American billionaire Paul Tudor Jones had a note out just a couple of weeks ago expounding the benefits of Bitcoin. Literally, it’s the only tradable asset in the world where there’s a known fixed maximum supply.

You’re buying it because you don’t trust in central banks and governments. You’re buying it because they can’t deflate its value away — they can’t devalue your Bitcoin.

Whether you like Bitcoin as a construct or not, I think you have to accept the fact that the world is moving away from allowing the US to be the reserve currency.

We’re moving to a new regime. How we move away from a US reserve currency and how crypto impacts the long-term inflation-deflation dynamics have yet to be determined, but they will be material.

Vimal Gor leads Pendal’s Bond, Income and Defensive Strategies team.

Find out more about Pendal’s investment capabilities.

Important Updates

Pendal Dynamic Income Fund (APIR: BTA8657AU, ARSN 622 750 734)

Pendal Enhanced Credit Fund (APIR: RFA0100AU, ARSN 089 937 815)

Pendal Fixed Interest Fund (APIR: RFA0813AU, ARSN 089 939 542)

Pendal Monthly Income Plus Fund (APIR: BTA0318AU, ARSN 137 707 996)

Pendal Sustainable Australian Fixed Interest Fund (APIR: BTA0507AU, ARSN 612 664 730)

Effective 22 May 2020, the buy-sell spread for a number of Pendal funds (the Funds) will decrease as set out in the table below:

|

Fund Name |

Old (%) |

New (%) |

||

|

Buy |

Sell |

Buy |

Sell |

|

|

Pendal Dynamic Income Fund |

0.07% |

0.36% |

0.07% |

0.23% |

|

Pendal Enhanced Credit Fund |

0.07% |

0.32% |

0.07% |

0.23% |

|

Pendal Fixed Interest Fund |

0.06% |

0.12% |

0.06% |

0.10% |

|

Pendal Monthly Income Plus Fund |

0.07% |

0.25% |

0.07% |

0.20% |

|

Pendal Sustainable Australian Fixed Interest Fund |

0.05% |

0.13% |

0.05% |

0.09% |

Table 1: Old and New Buy-Sell Spreads

The buy-sell spread is an additional cost to you and is generally incurred whenever you invest in or withdraw from a Fund. The buy-sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy-sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy-sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Funds.

The further reduction in buy-sell spread reflects continuing improvement in market liquidity for Australian issued investment grade securities.

Pendal will continue to monitor market conditions and review and update the buy-sell spread regularly as required. You should therefore review the current buy-sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy-sell spread for each Fund.

The COVID-19 crisis underlines the importance of considering Environmental, Social and Governance factors when investing. Regnan’s head of advisory Susheela Peres da Costa expains why in this interview with online business channel Ausbiz.com.au.

Watch the video above or read this transcript:

AUSBIZ.COM.AU INTERVIEWER: We were speaking earlier about Environmental, Social and Governance (ESG) and it was pointed out that in this crisis ESG is still front of mind — perhaps more for the social impact than the environmental impact. Is that how you see it?

SUSHEELA PERES DA COSTA: Absolutely. Often during more ordinary times it’s the social factors that get short shrift. But as a result of this pandemic we’ve become very alert to things like the working conditions in factories that might be making our protective gear or protective equipment in factories far away.

We’ve become quite alert to the working conditions for people who are essential workers in the community, who we need to be healthy, and be able to be willing to continue to put themselves at the service of the community in times that are quite difficult.

These are just some examples of social issues.

INTERVIEWER: Do you see a real opportunity when it comes to ESG principles and gauging a company’s compliance when it comes to supply chains? Most people say supply chains are not going to look anything like they did pre-COVID.

SUSHEELA PERES DA COSTA: Yes, one of the really interesting things is that in boom times we tend to see efficiency as a good in itself.

Very often the idea of just-in-time inventory or very short supply chains where we’ve taken as many costs as possible out of the ultimate cost of a product is seen as a good thing.

But really efficiency comes at the expense of resilience and a little bit of redundancy is often a good thing.

It allows you to make changes as you need and to modify areas of risk that might come offline. That goes for pandemic conditions, but it applies equally to a flood or a fire or even a trade embargo that happens in different parts of the world and can affect supply chains that we’ve come to rely on.

These types of trade-offs are parts of ESG that are typically under-appreciated. We get headlines around things like climate change and modern slavery — ESG issues that the community is aware of — but they are the tip of the iceberg.

There’s a significant amount that’s less amenable to media interest during good times, but very, very apparent when anything goes awry.

The ultimate goal of ESG is to look a little bit further ahead and a little bit wider in your field of view than what’s typically in focus for business and investment.

Being able to widen that view and lengthen that horizon allows you to make better investment decisions for the long term.

INTERVIEWER: That’s a really good point. Even ESG as it stands — the E being first — [means] everyone talks about the environment as if that is front and center. But … where is that [capital] being deployed? Which part of that ESG is it trying to move to?

SUSHEELA PERES DA COSTA: It’s more about taking everything into account. One of the interesting things about ESG is we’re quite focused on labelling categories within ESG, for example the environment or supply chains.

But actually a lot of these issues interact with each other. Understanding how that can alter the shapes of economies, alter business profits and alter investment returns, is some of what ESG seeks to highlight.

To give an example, we might commonly hear about things like a business being a heavy emitter of carbon. But that may ignore the fact that it is also exposed to physical risks of climate change.

When you put those together, you can see how they might interact.

For instance, it might be after a season of bushfires that the community is more alert to climate change and more ready for regulation that limits carbon emissions.

The contingency plans a company makes to deal with one of those possibilities could be derailed by the other.

It’s really the interaction of many of these kinds of risks that form some of the biggest areas of potential risk for ESG. And of course also the biggest opportunities in addressing them.

INTERVIEWER: Are you seeing lots of positive forward momentum on this front in Australia? Are there plenty of opportunities, plenty of companies that you can hitch your bandwagon to because you truly believe they’re getting it?

SUSHEELA PERES DA COSTA: Momentum has been really strong. We’ve been talking to companies at Regnan since the early 2000s. The degree to which they are understanding and impounding the ESG ideas into their own business strategies and business models has never been swifter.

It’s actually quite an exciting time for people to be working on those projects inside companies and investors.

There are always pockets of laggards and that’s a reality that investors need to work with. But there are some interesting opportunities out there too.

Susheela Peres da Costa is head of advisory at Regnan, a global leader in long-term value, systemic risk analysis and responsible investment advice. Last year Pendal appointed a London-based impact investment team to launch a Global Equity Impact strategy in late 2020.

Regnan is wholly owned by Pendal Group.

Pendal Sustainable Conservative Fund (APIR code: RFA0811AU, ARSN 090 651 924)

Effective 21 May 2020, sustainable and ethical investment practices in the Pendal Sustainable Conservative Fund (Fund) will be broadened to also include a portion of the Fund’s investments in alternative investments. Sustainable and ethical investment practices are currently incorporated into the Fund’s Australian and international shares and Australian and international fixed interest allocation.

Alternative investments sustainable and ethical screens

For a portion of the Fund’s alternative investments component, the Fund will not invest in companies or issuers directly involved in the following two activities:

• tobacco production; and

• controversial weapons manufacture (such as cluster munitions, landmines, biological or chemical weapons, depleted uranium weapons, blinding laser weapons, incendiary weapons, and/or non-detectable fragments).

For a portion of the Fund’s alternative investments component, the Fund will also not invest in companies or issuers directly involved in the following activities, where such activities account for 10% or more of a company’s or issuer’s total revenue:

• the production of alcohol;

• manufacture or provision of gaming facilities;

• manufacture of non-controversial weapons or armaments;

• manufacture or distribution of pornography;

• direct mining of uranium for the purpose of weapons manufacturing; and

• extraction of thermal coal and oil sands production.

Investments will be reviewed regularly to ensure they remain within the sustainable and ethical screens of the Fund. If the review process identifies that an investment ceases to comply with the screens, the investment will usually be sold as soon as reasonably practicable having regard to the interests of investors, but this may vary on a case by case basis.

Pendal Sustainable Balanced Fund (APIR code: BTA0122AU, ARSN 637 429 237)

Effective 21 May 2020, sustainable and ethical investment practices in the Pendal Sustainable Balanced Fund (Fund) will be broadened to also include a portion of the Fund’s investments in alternative investments. Sustainable and ethical investment practices are currently incorporated into the Fund’s Australian and international shares and Australian and international fixed interest allocation.

Alternative investments sustainable and ethical screens

For a portion of the Fund’s alternative investments component, the Fund will not invest in companies or issuers directly involved in the following two activities:

• tobacco production; and

• controversial weapons manufacture (such as cluster munitions, landmines, biological or chemical weapons, depleted uranium weapons, blinding laser weapons, incendiary weapons, and/or non-detectable fragments).

For a portion of the Fund’s alternative investments component, the Fund will also not invest in companies or issuers directly involved in the following activities, where such activities account for 10% or more of a company’s or issuer’s total revenue:

• the production of alcohol;

• manufacture or provision of gaming facilities;

• manufacture of non-controversial weapons or armaments;

• manufacture or distribution of pornography;

• direct mining of uranium for the purpose of weapons manufacturing; and

• extraction of thermal coal and oil sands production.

Investments will be reviewed regularly to ensure they remain within the sustainable and ethical screens of the Fund. If the review process identifies that an investment ceases to comply with the screens, the investment will usually be sold as soon as reasonably practicable having regard to the interests of investors, but this may vary on a case by case basis.