Pendal has appointed a London-based impact investment team to launch a Global Equity Impact strategy in late 2020.

The team will join Regnan, a leading provider of ESG research, engagement and advisory services, which is wholly owned by Pendal.

The appointment marks the expansion of Regnan’s capabilities into responsible investment funds management.

The four-person team will be led by Senior Fund Manager Tim Crockford working with Mohsin Ahmad, Maxime Le Floch and Maxine Wille.

The team previously managed the Hermes Impact Opportunities Equity Fund, which Mr Crockford co-launched in 2017.

The team will be based in the J O Hambro Capital Management office in London.

‘Global leader in responsible investment’

“One of our strategic objectives is to become a global leader in responsible investment,” said Pendal’s Chief Executive of Group, Emilio Gonzalez.

“The move to 100 per cent ownership of Regnan in early 2019, and now the appointment of a specialist impact investment team, demonstrates our commitment to delivering on this strategy.

“The impact investment market is currently worth over half a trillion US dollars and there is an obvious and growing demand from clients for this capability.

“Given our 35-year heritage in responsible investment, we believe we have an important role to play in delivering positive impact alongside strong investment returns for clients.

“Our combined deep knowledge and expertise in this area enables us to deliver innovative and credible Environmental, Social and Governance (ESG) and impact investment solutions that will meet client needs and grow funds under management.”

Late 2020 launch

Regnan’s Global Equity Impact strategy is expected to launch in late 2020 and be available across Pendal’s global distribution network.

The team will aim to generate long-term outperformance by investing in mission-driven companies that generate value for investors by providing solutions for the growing unmet sustainability needs of society and the environment.

The fund will use the United Nations Sustainable Development Goals (SDGs) as an investment lens:

“We are delighted to welcome Tim and his team to Regnan and the Pendal Group,” Mr Gonzalez said.

“The team hire expands our investment capability while enabling us to leverage Regnan’s ESG expertise.”

Background on Regnan

Regnan is a leading provider of ESG research, engagement and advisory services.

Its focus on environmental and social issues traces back to Melbourne’s Monash University in 1996.

Regnan was established to investigate and address ESG-related sources of risk and value for long-term shareholders in Australian companies.

It has evolved to become a global leader in long-term value, systemic risk analysis and responsible investment advisory.

Regnan’s in-house team of experienced analysts produce rigorous, relevant ESG investment analysis.

From this research and insight, the team tailors solutions to meet the specific needs of its asset-owner clients.

These clients use Regnan’s services for a range of purposes from stock selection, portfolio construction and stewardship, through to all aspects of responsible investment framework development and implementation.

Regnan also advocates for ESG considerations to become mainstream through contribution to the public policy debate, board and committee-level participation in industry bodies, and submissions to government.

Regnan staff recently co-authored a UN Principles for Responsible Investment report, Active Ownership 2.0: the Evolution Stewardship Urgently Needs.

Pendal Sustainable Balanced Fund – Fee Change

Pendal Sustainable Balanced Fund (Fund} APIR: BTA0122AU, ARSN: 637 429 237)

Reduction in management costs from 2 December 2019

From 2 December 2019, the issuer fee for the Fund will reduce from 0.90% pa to 0.80% pa

Pendal’s very own George Bishay has been awarded the Alpha Manager status of endorsement by Money Management’s parent, FE fundinfo. This accolade is in recognition of George’s career-long performance record in the asset management industry.

George was one out of 11 Australia-based investment professionals included in this list across multiple asset classes, after being assessed on his ability to create risk-adjusted alpha (outperformance) over his entire career track record.

FE Fundinfo, creators of the inaugural Alpha Manager award, determined this exclusive list by only focusing on the top 10% of Australia’s retail-facing portfolio managers and analysing their track record.

Shifting the short term focus

The Alpha Manager status has been intentionally designed to recognise career-long performance. Rather than just picking this year’s winners in the investment industry, the Alpha Manager status has been reserved for the select few who have demonstrated a compelling track record of performance throughout their career.

George’s investment management career spans over 22 years with Pendal and its predecessor firms. He is responsible for management of credit, fixed interest and enhanced cash portfolios, including Pendal’s highly regarded Enhanced Cash Fund and Sustainable Australian Fixed Interest Fund.

![]()

Diving deeper generates true rewards

While being highly appreciative of the award, George puts his results down to a “fastidious approach” to assessing information and constantly rejecting the human tendency to accept information at face value. “You can’t underestimate the value of digging deeper when it comes to assessing issuers and security structures”. Also critical to his success is the team’s top down process that utilises a quantitative model backbone, qualitative overlay and technical analysis.

A similar mindset applies to holistically integrating ESG and impact investment analysis. Although it is very topical these days to espouse the virtues of sustainability, George and the Pendal Bonds, Income & Defensive Strategies team argue the importance of authenticity when it comes to delivering long term results within a sustainability framework. “Long before sustainability was in vogue, we have been focused on delivering tangible rather than tokenistic outcomes.” George has managed dedicated Sustainable (ESG) fixed interest portfolios since 2009.

Click to view the media release and feature article in the latest Money Management publication.

Investing to take account of humans’ impact on the environment has garnered even greater attention over the past several months and its importance for our clients continues to grow.

As Pendal’s Portfolio Specialist, David De Ferranti outlines, there are now opportunities for investors to make a real difference to the lives of everyday people, while also earning a financial return.

Take a two-minute read on the evolving area of impact investing and the positive contributions it can make to the environment and broader society.

View the article here.

The inexorable drift towards lower and lower interest rates is upending many assumptions; from the role of monetary policy in lifting the economy through to where investors look for yield. Australia and the US have positive rates for now. However, as growth slows further, inflation persistently undershoots central banks’ targets and governments prove unwilling to lift spending, rates are being forced closer to zero. This has raised speculation over non-traditional measures like negative rates, as already in place across Europe, as well as quantitative easing in order to move central banks’ key objectives back towards their targets. At Pendal’s recent Lighthouse event, the Bond, Income & Defensive Strategies (BIDS) team shed some light on the conundrum facing policymakers and what the future may look like when monetary policy is no longer effective.

Monetary means at their limits

Central banks around the world have been progressively targeting inflation since 1989, with our friends across the Tasman at the Reserve Bank of New Zealand the pioneers of its modern form. Over this time the policy setting boards have presided over the structural shift to lower interest rates, lower inflation and considerable economic expansion.

Since the 1990s we have seen a few economic cycles, with each changing the nature of policy effectiveness. Our Australian rates manager, Tim Hext, has experienced many over his career and notes every cycle has lower and lower interest rates. In Europe, several countries now have negative interest rates, led by Denmark, Switzerland and Sweden. They have joined Japan, where interest rates hit zero two decades ago, before turning negative.

The issue now is increasing risk aversion resulting from negative rates. Central bank tools are relatively blunt, so to obtain the desired economic response, even deeper negative interest rates will be required for Europe. This is the problem with blanket policy targeting through interest rates. When you’re a hammer, everything looks like a nail.

As such, to address the failures of the current regime there is growing recognition of need for a different policy approach. Enter Modern Monetary Theory (MMT). The thinking around this form of economic management was pioneered by American economist, Professor Bill Mitchell along with a cohort of academics and finance practitioners. MMT directly repudiates the thinking around government budget constraints which form the basis of the ideologically opposed Keynesian school of thought for economic management.

Breaking from tradition

The chorus is growing as central bankers increasingly appeal for help in the unruly task of economic management. In his last meeting at the helm of the ECB, Mario Draghi called again on greater support from the fiscal arm of policy. RBA Governor Lowe has echoed these calls amid the frugality that has characterised government spending at home, driven by a seeming obsession with obtaining a surplus.

Ultimately, if an economic crisis and recession eventuates it will drive radical political change, forcing governments to boost spending, cut taxes and pursue deeper structural reform. This may include elements of MMT, which we can interpret more as a framework, than a set of individual policies.

At the core of MMT is an ideology that upends the traditional view that considers the economy as separate from individuals, who seek to maximise their utility from it. Rather, MMT essentially sees the economy as the people and in turn, works for us as a collective.

Another conventional perspective which is uprooted by MMT is that governments should operate like households. This is an idea perpetuated by our personal experience with budgeting and debt. Simply, if we live beyond our means, there is a deficit which requires debt to finance. We then project this idea onto how governments should operate. As such, we have the notion that governments must raise revenue through taxes in order to spend, otherwise they will run a deficit and accumulate debt.

MMT takes an alternative view under a few assumptions, including that governments have control over their currency. This means a government could create money to finance spending, rather than raise it through taxes or a combination of deficits and debt. Such an approach can be followed when there is excess capacity in the economy and the need for stimulus.

What creates inflation?

The notion of creating money for spending may raise some eyebrows, given concerns over the idea of money printing resulting in inflation running out of control. However, such worries require consideration of the force behind money creation. As has been proven by the recent era of massive central bank stimulus efforts, inflation is not purely supply-driven. It does not matter how cheap money is to borrow or how much is available, ultimately it depends on demand and a borrower’s ability to borrow.

Government spending can stimulate this demand and taxes can reduce it. In the MMT world, a key policy that can be used as part of this mechanism is a job guarantee program. If economic activity is weak with low inflation, jobs can be created to absorb idle capacity, and as capacity becomes stretched, inflation will rise. True inflation can only emerge once full capacity is reached. As inflation rises, the government can cut spending and raise taxes to bring the economy back towards balance. In this way the policy acts as an automatic stabiliser.

Such a job guarantee program also supports an idea that anyone who wants to work will work. If the private sector can’t absorb them, then the government will. It will guarantee you a job. There are plenty of public services that are needed – building public facilities, cleaning community spaces or whatever host of other productive activities.

A new New Deal

In the US a similar style policy was implemented in the form of the Civilian Conservation Corps – one of the most successful New Deal reforms introduced by Roosevelt in the 1930s. Looking at the debate in the US now, Tim believes it is not a matter of when a form of MMT arrives, but who will move first – when will they do it, how they do it, and who will then follow.

“For example, you could have a 50-year infrastructure project, which you break down into 5-year, short term projects. This can be slowed as inflation rises. And if inflation rises too far, taxes can be hiked”, he says. “The currency may take a hit, initially, but as growth kicks in, that will flow through to the currency.”

Tim highlights the case of Japan, which has struggled to stimulate growth, but boasts one of the lowest unemployment rates in the world; “everyone’s got jobs, everyone is happy. Why do you need GDP growth if everyone is happy? It begs the whole question of why do you need GDP growth for GDP growth’s sake.”

Looking elsewhere, the UK is likely growing closer to adopting some form of MMT. Their economy is really weak now. And once you see job guarantees coming, then others will follow. Tim notes “You won’t announce we’re doing ‘modern monetary theory’, but you will announce job guarantees. The first implementation will be the UK. The US will follow at some point.”

Investing in an MMT world

With significant experience in rates markets as Head of the boutique, Vimal Gor believes secular stagnation is a problem that is likely to persist for a long time to come. In the medium-term and for the practicalities of investing, the baton of policy stimulus will likely not be passed completely from the current hands of central banks to governments. Arguably, even within an MMT world with more of the heavy lifting done by government spending, we will remain in an environment of structurally lower yields over the long-term. The need for rates to remain low or lower represents further opportunities for bonds as we see the race to the bottom continue. Bonds will also continue to offer investors the important safe-harbour that is critical when risk-assets like equities suffer and as such, will remain a vital part of an investor’s portfolio.

Changes to the Pendal International Share Fund (APIR: BTA0056AU, ARSN 087 593 299)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal International Share Fund | Pendal Concentrated Global Share Fund No.3 |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50%1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

Distribution frequency

The Fund’s distribution frequency will change from quarterly to annual. Effective 21 February 2020, the Fund will generally pay distributions at the end of June each year.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund/.

[1] The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Changes to the Pendal Core Hedged Global Share Fund (APIR: RFA0031AU, ARSN 098 376 151)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal Core Hedged Global Share Fund | Pendal Concentrated Global Share Fund Hedged |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50% 1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) hedged to AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

The Fund’s foreign currency exposure will continue to be fully hedged back to the Australian dollar to the extent considered reasonably practicable.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund/.

1 The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Changes to the Pendal Core Global Share Fund (APIR: RFA0821AU, ARSN 089 938 492)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal Core Global Share Fund | Pendal Concentrated Global Share Fund No.2 |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50%1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund

[1] The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Cast back to the year 1998 when Paul Wimborne, co-manager of the Pendal Global Emerging Market Opportunities Fund started looking at Emerging Markets, and the world was a different place: the US was impeaching its President, Argentina was heading towards default and we had a big tech bubble forming on the NASDAQ with unsustainable returns, and of course the Australian cricket team retained The Ashes. Unprecedented times indeed!

But consider the structure of today’s emerging markets and its clear there have been some more permanent changes. Emerging economies are a fairly disparate group, with many barely recognisable to the asset class that existed in the 1990s and 2000s, where a crisis in one particular market usually spread rampantly across many others.

In the past three decades, many of these countries have embarked on monetary and fiscal reforms, building defences against such external shocks. This difference was evident through the past year when the US dollar strengthened, prompting investors to exit emerging markets. Countries with these policy defences escaped relatively unscathed, while others like Argentina and Turkey showed their vulnerability.

Leading investment research firms like Lonsec argue that today’s emerging markets warrant a dedicated place in an overall global equity portfolio. While emerging markets only represent around 10% of the MSCI All-Country World global share index, they are materially underrepresented based on their true share of the global economy. Today, emerging markets account for 59% of global GDP. There are now more than 120 companies that have joined the Fortune 500 which are facing into emerging markets.

So why does this discrepancy in recognition persist? There are a few reasons but the prime explanation is found in the underlying structure of share market indices. They are generally based on market capital weightings, which essentially represents the total value of a company’s shares on issue. Take the global technology behemoths for example — Apple, Microsoft, Google and Amazon — their collective representation in the index accounts for around 8% of the developed markets index, not far from the total index weight of all emerging markets.

Valuations now attractive

China epitomises the extent of this discrepancy. Despite its status as the world’s second-largest economy, China is still defined as an emerging market due to low household income levels, which are just 15% of what they are in the United States.

“Valuations look attractive, even in spite of trade wars …”

Veronica Klaus, Head of Investment Consulting, Lonsec

And the US-China trade war and associated rhetoric has played its part in driving lacklustre returns from emerging markets in recent years, leading many investors to write off the asset class.

“Valuations look attractive, even in spite of trade wars …” according to Veronica Klaus, Head of Investment Consulting at Lonsec.

Lonsec believes many of the fears are overdone, although this is not a blanket statement to cover all 1,149 stocks in the emerging market index as they’re not without risks. Klaus refers to the volatile nature of parts of the emerging world. For the year to date, Chile’s share market has declined by 7%, while Russia is up 32%, precisely why Lonsec impresses upon the importance of active management for the asset class.

Lonsec argue for an active, selective approach to emerging markets for clients with a long term growth horizon. Klaus says “What is important is to look for active management, and look to a manager and a strategy that is moving away from these higher risk scenarios and looking towards the long term valuation opportunities.”

Lonsec sees value stocks within emerging markets as being particularly cheap, “trading at their largest discount since December 2001”.

“It’s much more attractive compared to US shares and Australian bonds.”

Lonsec holds an overweight stance in emerging markets across their suite of balanced or growth oriented model portfolios.

Click here to download the complete article

Importance of the country’s business model

Paul Wimborne, co-manager of the Fund concurs on the point of being selective. We are not compelled to buy any stock; regardless of what is or isn’t in the benchmark, the investment has to measure up on our country-level macro assessment and the bottom-up fundamentals of a company.

“The key question you have to ask yourself is, do I want to be invested in that country…or not?”

Paul Wimborne, Senior Fund Manager

We don’t say bottom-up analysis isn’t important in emerging markets, but we are very different to the conventional approach. Our bottom up analysis recognises that the key factors we put into our company analysis models are actually top-down in nature. Our process is inherently designed to reflect the belief that emerging markets go right or wrong at the country level.

Take Argentina’s 45% stock market crash in August this year; it didn’t matter if you were in the best Argentinian company that day. The business model of that company is not going to help you out. “The key question you have to ask yourself is, do I want to be invested in that country…or not?”

In emerging markets there are always countries that go wrong. We need to satisfy ourselves with regard to what we like about the macroeconomic environment that means the equity market is going to do well. Then we find the companies that will benefit from the macroeconomic environment and avoid companies that are susceptible. It is vital to understand the country’s operating model in all of its guises, as it is intricately linked to the success of a company.

Unlike in the developed world where there is a greater degree of synchronicity in economic factors between countries, emerging markets feature a much more diverse group. Variables like GDP, interest rates, inflation, regulation, cost of capital and terminal growth rates can be materially different and much less correlated relative to developed markets.

When will emerging markets turn?

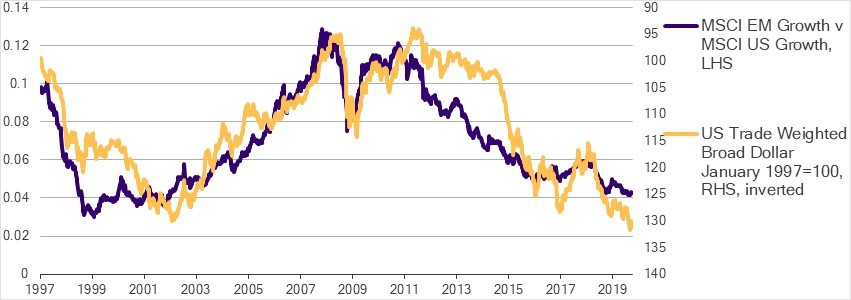

Our team believes there are two key conditions conducive to delivering strong performance in emerging markets: robust global growth and a weak US dollar. Clearly neither of those factors are in place – and until they are the team are being very selective and taking advantage of idiosyncratic opportunities in the asset class.

We do think the second of these catalysts may come through. When that does happen we should see emerging markets begin to outperform developed markets, in keeping with their historical relationship.

Weaker dollar to drive EM recovery

Source: Pendal, Bloomberg as at 4 October 2019

The rationale for this to occur at some point is fairly clear. First, the US dollar retains its reserve currency status. This means the US can borrow lots of money at cheap rates, and they are certainly borrowing plenty and driving up the deficit. Heading into the US election year, all signs are there for whoever takes office, that spending will all but continue and add to the deficit. The question will be who is going to finance the fiscal deficit? Over the last few years it has been the Fed and sovereign investors like China that have been buying US treasuries and adding to their expansive reserves.

Evidence is now emerging that China is increasingly moving to price commodity contracts outside of the US dollar payments system. At the margin, this means there is less rationale for holding all of your reserve assets in US dollars. So if it’s not foreigners buying as many US treasuries, and it’s not China or the Fed, who will be financing the deficit?

Evidence from prior crises shows that typically when currencies blow out, it’s driven by financing of enlarged fiscal deficits. When they can’t get foreigners to finance it, the Government turns to the local banking sector and you get a crowding-out effect. Essentially this means the banking sector becomes constrained with less money to lend to the domestic economy. The recent spike in US repo rates may have something to do with this dynamic.

When and how this happens can’t be predicted with certainty, but when it does we’re likely to see growth-focused investors switch preferences from NASDAQ tech stocks to emerging markets. But until this occurs we remain focused on country-specific, self-help opportunities through countries like India, Korea and Turkey.

The team believes India has the strongest growth potential over the next few years. Among the many differentiators, it is one of the only countries in the world which hasn’t had an increase in the credit-to-GDP ratio since 2008.

One reason is a number of loans made in the banking system went bad prior to 2008. The Modhi-led Government has made a concerted effort to redress shortcomings of the previous Bankruptcy Code. They have strengthened the banking sector with fresh capital and we should see a credit-driven recovery for the banking sector. There has been a delay in this cycle as credit growth has fallen in response to the collapse of a non-bank lender. However, we believe the recovery should eventuate, bolstered by a series of other reforms implemented under the Modhi Government.

Then there’s Korea, a very different opportunity. Korea has been one of the cheapest markets historically, largely due to its poor governance record. This is changing as political and social pressure is driving different behaviour in the ‘chaebol’ conglomerates which dominate Korea’s corporate landscape. One key, tangible benefit is an increase in payout ratios, helping lift Korea’s traditionally poor dividend yield. We see this trend continuing, which will likely lead to a substantial re-rating of Korean equities and potentially, its eventual graduation into the developed markets category.

Source: MSCI, Bloomberg as at 31 December 2018. Free cashflow is cashflow from operations less capex

Other bright spots in the emerging market world are Russia, Mexico and Turkey — all for very specific reasons. Turkey serves as an example of how quickly conditions can turn positive. With 2019 GDP growth revisions of -1.5%, Turkey was until recently the second-weakest of all emerging economies this year. However, the pricing of that forecast slowdown became wildly excessive, and the Turkish stocks we bought in May have outperformed substantially. Interestingly, Turkey’s 2019 GDP growth estimate has since been revised upwards, suggesting that the worst of the selling pressure (and the greatest opportunity for investing) was right before the turn in May.

These and other examples serve to validate our view that success in emerging markets relies on a balanced assessment of fundamentals and valuation. We look to use both to identify top-down, country-level opportunities in emerging markets, irrespective of how good or bad the global environment is perceived or otherwise at that moment. We see the key macro catalysts for re-rating as likely as conditions in the global economy evolve. When they do arrive, it will likely add to success for our country-specific investment decisions.

We think the challenges and opportunities in emerging markets underpin the importance of our country-driven approach. We continue to identify opportunities — such as those discussed — which exist despite the headwinds to the asset class more broadly. Meanwhile, we monitor the landscape for signs of a change in those headwinds, positioning the portfolio to benefit at the point when the tailwinds return to emerging markets.

Thai capital Bangkok is known for vibrant street life and the boat-filled Chao Phraya River… but is it a good investment?

One of the reasons we believe it’s crucial for Emerging Market (EM) investors to be knowledgeable about the history of the asset class — and the countries in it — is the dynamic nature of different emerging markets as they grow and develop.

There is possibly no country in the EM universe that has undergone a greater shift in its macroeconomic fundamentals — and the relationship of its capital markets to those fundamentals — than Thailand.

The Asian crisis of 1997 was one of the great landmark events in the history of EM.

Whereas the 1994-95 Tequila crisis in Latin America was confined to a group of countries with a history of economic volatility (see: Latin American debt crisis, 1982), the Asian crisis tore through a regional economic miracle.

First domino to fall

Thailand was the first domino to fall in 1997, with the default of major property developer Somprasong marking the beginning of the crisis.

Looking back, in the late 1990s Thailand was as capital-deficient, liquidity-driven and high-beta as Turkey, Argentina or Russia. The turn in global liquidity in 2002 would set in motion an economic and stock market boom of similar magnitude to those other countries.

However, a genuine transformation of the economy occurred at this time, with Thailand developing deep and widespread capability in exports of electronic products and processed foodstuffs, as well as a highly successful tourism industry.

As well as driving GDP growth, this shift massively strengthened the Thai current account balance, which has moved from a deficit of over 8% of GDP in 1995 and 1996 to a surplus that has averaged nearly 9% of GDP in the last three calendar years.

This has in turn led to a 180-degree turn in the policy objectives of the Bank of Thailand (BoT), which went from holding the baht up (to keep imports cheap and hard currency-denominated debt affordable), to holding the baht down (to maintain export competitiveness).

The BoT has pursued the latter strategy as single-mindedly as any other mercantilist EM.

Challenges ahead

What is more, Thailand is approaching some challenges as the limits to conventional interventionist-mercantilist policy are reached.

These include disquiet among trading partners at the suppressed valuation of the currency, and the zero lower-bound to policy (policy rates in Thailand were recently cut to 1.25% but are likely to continue to fall).

Unconventional monetary policies such as asset purchases, directed lending and negative rates could be employed, but the large current account surpluses will continue to pose a problem for Thai policymakers.

The upward pressure on the baht does not make Thailand particularly attractive for equity investors.

The hit to competitiveness from the stronger currency has an overall drag on the economy, while the central bank’s sterilisation of capital inflows limits liquidity growth.

Domestic demand in other late stage-mercantilist-interventionist Asian economies like South Korea and Taiwan has consistently disappointed, while returns on capital (particularly in the financial system) have trended lower and lower.

This also has echoes of the Eurozone, which has also chosen to suppress demand in order to run huge current account surpluses. Indeed, a current account surplus can be thought of as representing a country’s deficiency of demand relative to productive capacity.

Equity market opportunities

As we have seen in Europe, South Korea and Taiwan, equity market opportunities tend to be concentrated in export sectors during global upswings.

We continue to see the potential for US Federal Reserve accommodation to improve global US dollar liquidity and weaken the dollar in the coming year.

This has the potential to drive very strong economic uplift and equity market returns in the capital-deficient, liquidity-driven and high-beta emerging markets.

Thailand was one in 1999; it isn’t 20 years later.

James Syme is a London-based senior fund manager with Pendal subsidiary J O Hambro.