– The outlook for emerging markets in the second half of 2019 and beyond has two main macro drivers: US rates and yields, and Chinese growth.

– While the expectations are for a slowdown in the future in the US, economic growth in China is unambiguously soft.

– EM equities remain in aggregate a highly cyclical asset class, but the first half of 2019 has shown that a slowing cycle still creates great opportunities within the asset class.

The outlook for emerging markets in the second half of 2019 and beyond has two main macro drivers: US rates and yields, and Chinese growth. This is obviously always the case, but these variables significantly surprised in the first half of the year and will remain of great interest ahead, unlike, say, the oil price (weakening demand but producer discipline), Asian and Middle Eastern geopolitics (both noisy but seemingly not yet at the point where any major player abandons the current system), or developments in Europe (messy politics should not distract from super-low bond yields).

The shift in the US yield curve, and the associated expectations for interest rates, has been dramatic. At the end of June 2018, the effective Fed Funds rate was 1.82% and the US 10-year Treasury yield was 2.86%; a year later, those rates were 2.40% and 2.01%, respectively. Even the 30-year Treasury, at 2.53%, is almost trading below the policy rate. This inversion of the longer end of the US yield curve has generally occurred before difficult times in markets, including the early 1980s twin recessions, the savings and loans crisis, the Asian crisis and end of the tech boom, and the global financial crisis. US data remains reasonably strong, but clearly US fixed income markets see the long economic boom that began in 2009 coming to an end.

Chinese slowdown

While the expectations are for a slowdown in the future in the US, economic growth in China is unambiguously soft. Recent disappointing data include a 49.4 reading for June’s manufacturing PMI survey and May’s industrial production number slipping to 5.0%, a 17-year low. Other related data such as Taiwan exports (-5.8% to May), Korea exports (-13.5% to June) and the copper price (down 7.9% in the second quarter of 2019) all show the endemic weakness in Chinese demand. While China notionally has a wider set of policy options than almost any other emerging market, internally imposed constraints mean there is no easy way to stimulate growth while also managing the Renminbi exchange rate.

In addition, trade tensions and related uncertainty may be partly to blame for this developing sense of slowdown. From an EM point of view it doesn’t matter if export demand is sliding because of the natural evolution of the economic cycle or because of a political overlay. It is clear that economic data, positioning in bond markets and revisions to forecasts point to an environment that is negative for the cyclical, export-driven part of EM. For countries, that means Taiwan, South Korea, China, Mexico, Malaysia and Thailand; for sectors, it means information technology and parts of the industrial, materials and consumer discretionary sectors.

At the same time, though, lower interest rates in developed markets mean the opportunity for lower rates in emerging markets. Year-to-date, various EMs, including Russia, Malaysia, India and Chile, have been able to cut policy rates, both in response to declining inflation and to reduced concerns about US monetary policy tightening.

EM winners in 2019

So, in this seemingly slower-growing world, what were the winning trades in the first half? From an EM country perspective, the best performing markets were Greece (MSCI USD price index +29.3%) Russia (+28.0%), Argentina (+27.2%) and Egypt (+24.9%). What these markets have in common is that they are generally very cheap (in each case because of some fairly obvious political and economic dysfunction), and their strong performance reflects investors increased appetite for risk as risk-free rates decline. If global rates and yields are to remain depressed, this rotation into risk is likely to endure, even if the headlines remain troubling.

This isn’t to make an argument for investing in the (long-underperforming) value style tilt in EM. Value may also capture many industries that are, at this point in time, strategically challenged by industrial and technological changes (such as retail, autos and telecoms). In addition, falling costs of capital should be proportionally more beneficial to companies with longer duration cashflows, i.e. growth companies. Rather, this is about the increased attractiveness of cheaper, riskier markets, both through value (to equity investors) and through carry (to bond investors).

Individual country opportunities despite a slowing cycle

We feel that this points to some markets that have lagged the rally in risk, year-to-date. Turkey remains very difficult from a political and policy standpoint, while the economy continues to work through the legacy of the strong credit boom that ended in mid-2018. Nevertheless, it is the emerging market that seems to be cheapest across the equity-rates-currency spread, with single-digit P/Es in the equity market, policy rates 830bp above trailing consumer price inflation and a currency far from its real effective exchange rate trend.

South Korea is a highly cyclical economy and equity market, with substantial exports to China, but extremely low valuations there (price/book value for the market of 1.0x) also reflect investors’ sense that governance risk in Korea is elevated. Followers of our strategy will be aware of our expectation that increasing payout ratios will add a carry opportunity to the existing value opportunity there. Korea is also attractive because it should provide a hedge in the event that there is a recovery in the global economy, with a resultant back-up in yields.

Some other EM assets should also benefit from the current environment. Although Pakistan continues to face multiple economic challenges, the market is cheap and the recent IMF loan deal underpins the policy environment. In addition, gold has performed well in this period of low cost of capital, driving strong gains from EM gold miners.

EM equities remain in aggregate a highly cyclical asset class, but the first half of 2019 has shown that a slowing cycle still creates great opportunities within the asset class.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighborhood

In May 2019 the Pendal Property Securities Fund was awarded Best Property Securities Fund at the Money Management Fund Manager of the Year Awards.

In announcing the award, Money Management and its research partner Lonsec stated:

The Pendal Property Securities Fund has a ‘core’ investment style with a ‘quality’ bias, and is managed by highly-experienced and long-serving Portfolio Managers Peter Davidson and Julia Forrest. The team benefits from extensive industry contacts and sharing of ideas and news flow ideas from Pendal’s other asset class teams. The Fund has an extensive track record of outperforming peers over multiple investment cycles.

Responding to the award, Pendal’s Head of Listed Property Pete Davidson addressed some key questions facing the sector:

1. What do you think drove your strong performance in the last year? How did the management of the Fund contribute to this?

• Our focus on having a valuation toolkit and using a variety of valuation measures meant we could identify value in stocks that had strong equity-style valuation.

• Traditional NTA based stock valuation lagged. Many NTA supported stocks became value traps rather than traditional value.

• There was a strong divergence in stock performance, which was better for active managers.

2. What asset allocations and/or market conditions did you find most advantageous?

• Our overweights in fund managers and industrial, logistics stocks supported our performance.

• Falling bond rates have supported fund managers.

• Underweights to traditional mall / retail assisted our performance. These stocks have been impacted by the weakening macro economic environment in Australia.

3. Do you anticipate continued strong performance?

• Yes, our portfolio is positioned in pockets of growth and good reliable cash flow, such as child care and traditional industrial property, which will outperform the slowing economy.

• Yes, we are now overweight the Perth and Auckland office markets which have very good and improving fundamentals.

• Our underweights to traditional mall retail should continue to perform. We believe asset values will decline in this sector over the coming year.

Read more about the Fund and our capabilities

Fund Manager commentary for the month and quarter ended 30 June 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

Engaging via social media has become an essential part of daily lives for people the world over. The deeply entrenched use of smart phones and other mobile devices has superseded the traditional computers experience for an increasingly mobile population who have gone from periodically ‘logging on’ to ‘always on’.

No company is benefiting more from this trend than Facebook. It has been successful in leveraging its platform to facilitate user interactions at scale in a myriad of different ways, at any time of the day. While the ‘always on’ user views, posts, likes and shares, Facebook is working away in the background collecting a share of the value created in the form of advertising.

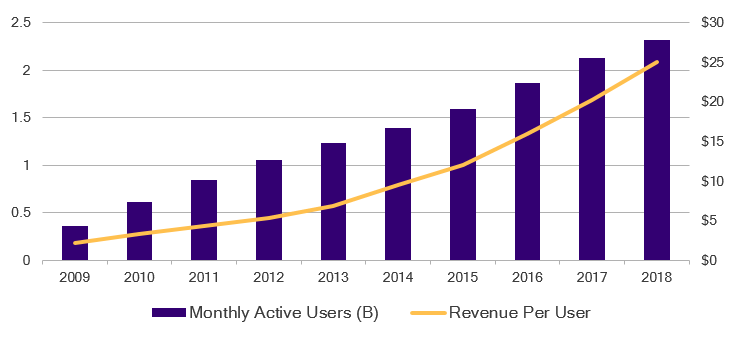

Today, 93% of its total advertising revenue is generated from mobile which is still growing north of 20% a year.

Facebook – user revenue growth (US$ millions)

While Facebook is the type of business we love to own in the Fund, we had been cautious on buying it. Recall our prior discussion on the rationale for details on our view.

Our investment process favours companies with dominant market shares and a growth profile capable of sustaining a competitive advantage over peers. We then look for an opportunity to invest in these companies. This usually occurs after they have experienced a substantial drop in their share price or have had flat earnings for an extended period of time.

As such, our investment in this area thus far has been limited to Alphabet Inc. (Google’s parent entity). We haven’t seen value in most of the other names, that is until recently.

Facebook’s share price underperformed the market from mid-2018 following news that confidentiality of its user data had been compromised. It traded below levels last reached in 2016, prompting a deep dive review of the company.

Facebook – share price performance vs S&P 500

The digital difference

Facebook and Google collectively account for 75% of all global (ex-China) online advertising spend. Such is the powerful combination of digital advertising and a captive, engaged user base. For advertisers the potential return on investment offers a distinct advantage over traditional forms of advertising.

Large, well curated social platforms offer advertisers the ability to have much more bespoke, targeted ad campaigns that can be enhanced and re-channelled through the course of the campaign, thanks to clever analytics that can be extracted to inform success or otherwise of the campaign. Unlike ads on TV, radio or printed materials, the advertiser doesn’t know who is watching TV, who lives in the house, what goods they’re buying online and at what time of day.

Considered together, Facebook and Google represent a powerful market share which provides clear competitive advantages.

Monetising the monopolies

Within its stable, Facebook owns and operates Instagram which was acquired in 2012. Within six years Instagram grew to amass one billion active users. Facebook is now in the process of ramping up monetisation of this asset which has become the largest growth driver for the company. The key medium of video presents a richer platform for both creators and advertisers to become more creative with their interactions.

This is similar to the opportunity we see with our investment in Google and its under-monetised Google Maps and YouTube assets.

Platform risks abate

The key concern for us with owning Facebook in the last two years has been their ability to control and monitor the content on their platform following a series of scandals. With our conservative approach we felt we needed to wait until we had clarity on the eventual new cost base and likely regulatory impact before investing.

Two recent developments have supported a change in our view:

1. Cost growth peaking – The company has had to significantly increased its expenditure on content control in 2018 and 2019. Given the direct impact on its margins and earnings we were happy to wait for signs that cost growth has peaked. In its most recent earnings update, Facebook reduced its expectations for capital expenditure in 2019 by US$1b. This means capital expenditure requirements will no longer continue to erode margins which will provide a base for profitability.

2. Regulatory impact not as bad as feared – Analysis of the company’s first quarter results showed a US$3b expense accrual based on expectations of a fine from the FTC in the range of US$3-5b. From our perspective, we could not forecast this potential outcome with any certainty, but comparing it to similar fines levied against Alphabet in the past couple of years gave us confidence Facebook won’t be penalised at a significantly higher level.

News reports in July indicate a Facebook has reached a settlement with the FTC of US$5b for the privacy breaches, which is within the company’s earlier guidance. The market has responded positively to the news, which was reflective of our premise on this issue.

We believe that the regulatory scrutiny will continue for some time and there will be associated costs. However, we also believe company management have acknowledged the reality of the situation and are driving operational change to reduce such risks and improve profitability.

Giving Facebook a ‘like’

We have held a favourable view on Facebook’s fundamentals for some time, but its valuation, unquantifiable regulatory risks and uncertainly of its ultimate profitability had precluded an investment. With an improved valuation (cash adjusted price-earnings multiple of 16x and a buyout yield — our preferred whole-of-company valuation measure — of 8%), greater clarity on the aforementioned costs and importantly, management’s actions to ameliorate operations for the platform, we have been able to improve our conviction.

We initiated a position in Facebook for the Fund in April and will look to add to our exposure as we see further evidence of the company sustaining its operating margins and containing costs.

What happens when a straight ‘A’ student starts bringing home ‘Bs’? We discovered one outcome of this report card for the Australian economy with back-to-back rate cuts from the Reserve Bank in June and July. In this quarter’s update we discuss why such easing was required, but more importantly what lies in store for future policy in Australia, including the possibility of quantitative easing. We also assess the outlook for Australian credit, which remains a balancing act between the global forces of trade war concerns and speculation of central bank action. Finally, we discuss a moving firsthand experience with responsible investing and how it has improved the outcomes for housing the homeless and victims of domestic abuse.

We hope you find this piece useful and welcome feedback from readers.

Australian Quarterly Update

Amy Xie Patrick, Portfolio Manager, Bond Income & Defensive Strategies:

It is our belief that the world has moved past the peak of globalisation, and now begins the messy and drawn-out process of individual actors working out the next-best way in which to interact with each other, be they friend or foe.

In this paper, we visit the key issues surrounding ongoing US-China tensions, including offering a perspective of the conflict from both sides. We provide our view of what drives continued tensions, as well as an analysis of the likely scenarios going forward and their potential impact on growth and policy responses.

Read more

Convulsion: a sudden, violent, irregular movement of the body, caused by involuntary contraction of muscles and associated especially with brain disorders such as epilepsy; a violent social or political upheaval

Our long-planned trip to visit companies in China could not have been better timed. A breakdown of negotiations between the US and China prompted President Trump to impose higher tariffs on a wider range of product imports from China. Combined with the imposition of sanctions on Chinese telecom and technology giant Huawei, this has convinced almost all seasoned observers of geopolitics that the ‘genie is out of the bottle’. The posturing and counter-moves by the two global economic giants is just the start of what could be a long lasting ‘economic war’ for ideological dominance in the decades to come. It is beyond my remit to posit on this development, yet suffice to say all countries will need to rethink and adjust as we undergo a massive change to the current global political and economic order.

“Overall the mood in China was combative and downbeat”

Most of the companies we met were cautious to downbeat. To generalise, as industrial profit growth in China slows sharply and export orders come under a cloud, almost every firm is understandably affected. There was a common thread running through most companies’ future expectations: government policies will save the day. I met a few companies which rank very high on the quality and growth score (in the health care and consumer space) but valuations reflect a lot of positivity. Those are on my radar to buy in case markets face further challenges, but overall the mood in China was combative and downbeat.

Our working assumptions are that growth rates (in China and globally) will moderate while volatility of growth will increase. In what is not just a case for China, governments and central banks across the world will increasingly try to cushion negative outcomes for growth in almost every country. Hence, risk of policy mistakes – knowable only in hindsight – will exacerbate asset price moves. Corporate capital expenditure and consumer spending might reflect a high degree of caution as confidence and clarity is diminished.

Pumping life through the economy

In other news, election results in Indonesia and India have given an increased mandate to incumbents. Both leaders face similar challenges: revitalising growth, job creation, growing income levels and infrastructure investment are the priorities. These challenges have no immediate solutions. In a challenged external environment bordering on protectionism, government subsidies will play an increasing role to help the lower strata of society. The constraint will be the fiscal deficit of both countries, but, from what I have read, the initial thrust of both governments will be on devising strategies towards this end. By way of example, Indonesia’s actions of the past few years may be indicative of policy direction for its peers.

Indonesia: Purse wide open

Source: CLSA Securities

Despite these efforts, growth has been difficult to come by. In Indonesia’s case in particular, there is an urgent need to address relatively inflexible labour laws. This has been the most cited reason for the lack of significant relocation of manufacturing at a time when firms are looking for alternatives to China.

Cautious, yet confident

From a portfolio standpoint, there is a fair bit of defensiveness through most of our holdings. I have tried to focus on companies that have managed the disruptive forces of online commerce and stand a better chance of success. With uncertainty emanating from restrictive trade policies, vigilance on monitoring second order effects (like moderation of consumer demand) will be important. There is genuine concern over the economy in China, yet even in these times there are pockets of growth. With this in mind I am keen to add to a couple of names in the ‘A’ share market if there is a further sell-off.

Mexico is the latest emerging market to undergo volatility as a result of politics-related trade uncertainty. As we are currently overweight Mexico in the Pendal Emerging Markets Opportunities Fund, we wanted to provide an update on our views.

For context, Mexico is one of the more stable and institutionally robust emerging markets, with an established democracy, OECD membership and an investment-grade credit rating. That is not to downplay some of the country’s challenges (such as violence and crime, or corruption, or the standard of the education system), but Mexico has smaller challenges than those faced by newer democracies such as South Africa or Russia.

The Mexican economy has performed moderately well since the Tequila Crisis of 1994/5, with real GDP growth averaging 2.6% pa, with the benefits of exports via NAFTA membership being a key driver. Despite this modest economic performance, Mexican equities have performed relatively well, with the MSCI Mexico index averaging 9.1% pa in US dollar terms from December 1995 to December 2018, ahead of both peer Brazil (the MSCI Brazil index has annualised 8.6% over the same period) and the broad MSCI Emerging Markets index (up 6.0% pa). This outperformance of equities relative to the economy is among the best in emerging markets; we attribute this to the competitive strengths of many large Mexican companies, from both good corporate management and also a less competitive structure to many key industries.

We have held a modest overweight position in Mexican equities since May 2017. At that time, we felt that the constructive approach of US Trade Representative Robert Lighthizer was indicative of easing external geopolitical risk for Mexico. We also felt that external demand from exports to the US was strong, domestic demand conditions were reasonable, and that the valuations of both the equity market and the Mexican peso were attractive. Since we initiated that position, our Mexican holdings have contributed positively to performance.

Notwithstanding recent announcements, we have to recognise that the threat by President Trump to impose steadily increasing import tariffs on Mexico is a significant change in the opportunity. Over 75% of Mexico’s exports go to the US and the degree of integration of the two economies means there will be a meaningful impact on both if the threat is carried through. More importantly, the change of direction in the Trump administration’s policy must cast doubts about the final form of the USMCA trade agreement that replaced NAFTA, and was previously thought settled following the signing in November 2018. For ratification, the agreement must gain legislative approval in both in the US and Mexico. The Democratic majority in the US Congress was already a challenge to overcome, but with President Trump seemingly also opposed to free trade with Mexico, it would seem that USMCA enjoys little support in the US and may well be in doubt, despite a continuing constructive approach from the Mexican government.

Political risk has just stepped up in Mexican assets, but we are not immediately turning bearish for a number of reasons. Firstly, Mexican equities look extremely cheap against their history (generally down to levels previously seen in the Global Financial Crisis), in a world where many asset classes look historically expensive. Secondly, real interest rates are historically fairly high and interest rates should follow inflation lower over the next year, providing further support to equities. Thirdly, we own a set of high quality, defensive stocks with very limited exposure to either exports or exporters. It has mostly been the good results from these companies that have supported returns over the last two years.

Finally, and with bigger implications, we believe that trade enables countries to exploit comparative advantage and seek larger markets than their own domestic base. The US protectionist turn is negative for US growth, and financial markets have moved to rapidly price in US interest rate cuts. Any such cuts are likely to drive US investors towards higher carry, higher growth and cheaper valuations, which will benefit emerging markets, including Mexico. It may be that more compelling country opportunities appear, and our process is designed precisely to identify those opportunities, but for now we retain confidence in the part of the Mexican equity market we are exposed to.

With responsible investing continuing to rise in popularity and importance among investors, Richard Brandweiner, CEO of Pendal Australia, joins netwealth’s Joint CEO Matt Heine as part of netweath’s Between Meetings podcast series to discuss:

– intermedation

– peak employment in funds management (vs asset owners)

– the evolution of impact investing and ESG

– philanthropy vs impact investing

– creation of the Pendal brand and taking full ownership of Regnan

– the role of active management and the concept of stewardship

Listen to the podcast

Fund Manager commentary for the month ended 31 May 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.