Does ownership of shares by a company’s senior leadership actually align interests and drive better results? And what is a true measure of alignment anyway? In our experience, effective alignment actually goes beyond having financial incentives in place.

A true sense of alignment requires a mindset that engenders belief in the long term success of a company.

The words of Texas Instruments’ CEO last month are particularly poignant in this regard and characterise his inherent mindset.

“To me, at the highest level, it’s a philosophy or a belief of a couple of things. First it is act like owners, owners that are going to own the place for decades, and then when you get inside of that you start to look at and make sure you’re focused on getting stronger, and not just bigger … and in many ways. We spend a lot of time on this internally, if you’re focused on getting stronger and you’re aimed at the right markets, the result is you will get bigger”

Rich Templeton

CEO, Texas Instruments Inc

Source: Sanford C Bernstein Strategic Decisions Conference, New York, May 27th 2019

Although a company is never immune to the economic cycle, the Texas Instruments leadership team exhibit complete ownership of the business strategy to ensure it is able to ride through the difficult times.

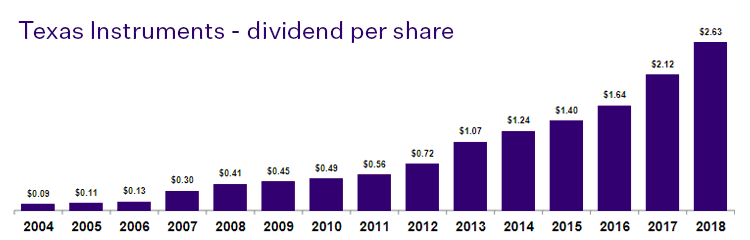

Texas Instruments is the world’s number one analogue semiconductor company which forms the nucleus of our many and varied connected devices. Its leadership offers a prime example of the owner-operator mindset we look for in company management.

One of the key tenets of our very different approach to investing is to apply this lens on a company’s management. Through time we have found a high degree of success in backing company management teams that exhibit an owner-operator mentality. This goes beyond any financial incentives in place as it is an indicator of a longer term sustainable growth mindset.

Texas Instruments is positioned for continued growth, with a highly diversified product mix skewed to the secular growth industries of automotive and industrial, where they operate across six and 13 sub-sectors, respectively.

For the past 15 years we have witnessed success in this management philosophy. Through this time they have delivered, on average, double-digit growth in free cash flow and a dividend which has increased each consecutive year.

This kind of stewardship is at the core of its success.

At a critical juncture in Australian monetary policy, Pendal Head of Bond, Income & Defensive Strategies Vimal Gor provided this in-depth interview to the AFR’s Sarah Turner on why he is so bullish on bonds, the RBA’s reluctance to ease and comparing the UK’s painful divorce from the EU to the decline of Rome.

View the AFR article

To date, a weaker Chinese Yuan has helped to offset a lot of the pain felt by China from US-imposed tariffs. In this interview with Bloomberg TV Pendal Portfolio Manager Amy Xie Patrick discusses the likely direction of the CNY versus the USD given recent additional tariffs imposed, rehetoric and general sentiment.

View the interview

More about our Bond, Income & Defensive Strategies team

– Conditions for emerging markets (EM) ex-China look better for the next few years than they have in recent years.

– Using IMF forecasts from April’s World Economic Outlook database, EM ex-China should grow at 3.7%pa from 2020-23, 2.3% faster than the developed world.

It has long been generally thought to be the case that two of the key drivers of the relative performance of EM equities versus developed world equities are the growth differential between emerging economies and developed economies, and the strength of the US dollar against other global currencies. These relationships can be made more meaningful by excluding China from the EM component of this model (for complicated reasons to do with China’s closed capital account, and more simple reasons to do with the quality of China’s GDP growth statistics).

Supporting this, JP Morgan has published research showing a fairly strong regression relationship between EM vs. DM growth differentials, the move in USD/EUR and capital flows to emerging markets (ex-China). Its research concludes: ‘robustness tests run with a diverse set of external and domestic variables regularly show EM-DM growth differentials and US dollar performance to be dominant drivers of capital flows.’

With this in hand, how do prospects stack up for the rest of 2019 and into 2020?

Growth differential: EM vs DM

The good news is that conditions for EM ex-China look better for the next few years than they have in recent years. During the ‘golden years’ of 2002-12, when the MSCI Emerging Markets index substantially outperformed the MSCI World index, EM ex-China (GDP-weighted) had average GDP growth of 4.6%pa, 3.2% faster than the developed world (source: IMF, for all GDP data here). The difficult period for EM in relative performance terms was 2013-2018, when the EM ex-China relative GDP growth gap was only 1.2 per cent. Using IMF forecasts from April’s World Economic Outlook database, EM ex-China should grow at 3.7%pa from 2020-23, 2.3 per cent faster than the developed world. This should support EM equity outperformance over the next few years.

Looking into what is driving this, two trends appear. The first is the key role of a few Asian economies in driving EM ex-Chinese GDP growth. India is the largest ex-China EM economy (2019 GDP: US$3 trillion) and is the fastest growing (2020-2024 average GDP growth forecast 7.7%), and the combination of these two means that India is expected to represent 35% of the total growth in EM GDP outside of China. As such, India is a key opportunity for EM equity investors, despite not being among the very largest markets by index weight). Smaller, but also key, are Indonesia (US$1.1 trillion; 5.3%) and Korea (US$1.7 trillion; 2.9%). Other markets are mostly too small (eg the Philippines, Egypt) or too slow growing (eg Russia, South Africa) to make a big contribution. Brazil is perhaps the one that might also make a big contribution, although regular followers will be aware of our concerns regarding the success or otherwise of social security reform there.

It should be noted, also, that the IMF forecast a steady slowing of Chinese GDP growth down to 5.6% in 2023, which will act as a headwind to wider EM growth. While that fits with our shorter-term expectations, any successful stimulus policy in China should lift the EM relative growth gap, improving the outlook for equity investors.

USD strength

So, a positive growth outlook, but a note of caution is the other half of the global macro environment: the US dollar. While we are not G7 currency experts, one trend in the IMF’s forecasts is that the US has had the largest increase in forecast 2020-23 GDP growth of any of the developed markets, which might point to renewed US dollar strength in the future. That would then put focus on inflation, current account balances and other macro-drivers of individual EM equity markets, which is why our process also looks not just at growth, but also the sustainability of that growth.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighborhood

Fund Manager commentary for the month and quarter ended 30 April 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

The market continues to price two rate cuts in Australia over the next twelve months as the RBA grapples with sluggish consumption and subdued inflation. This was evident in first quarter inflation data released last week. This quarter’s update was written before the release and in light of the softer picture, we have brought forward our RBA cuts from August and November to May and August. This is in spite of the current resilience of the labour market. In the April update we take a longer term look at the structural forces at work in the Australian economy and why rates will remain low into the next decade. Also in this update, we examine what has contributed to the recent strength in domestic credit, how we have positioned our credit funds and what dangers remain lurking on the horizon. In cash markets, very front-end rates recently fell to their lowest on record – our Cash PM, Steve Campbell explains why and what lies ahead. Finally, the quarter also featured International Women’s Day, which we thought would be opportune to educate investors on gender equality bonds, a growing segment of Responsible Investment.

We hope you find the piece useful and welcome feedback from readers.

View our Australian Quarterly Update

Fund Manager commentary for the month and quarter ended 31 March 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Quarterly commentary

Monthly commentary

What separates environmental, social and governance (ESG) investing; impact investing; ethical screening; and socially responsible investing (SRI)?

While they are all unique approaches to investment, there are some areas that overlap.

Susheela Peres da Costa shares insight on how to navigate this complex landscape and get responsible investment governance right.

View the article

It is clear to us that the domestic opportunity in Mexico has a better fundamental underpin than in South Africa, and we are positioned accordingly.

One of the defining characteristics of emerging markets (possibly even the defining characteristic) is that there are positive price (and liquidity) correlations between bond and equity markets. If you hit a crisis and your equity market sells off and bond yields spike, congratulations – you’re an emerging market.

For us as equity investors it means we need to pay attention to bond markets, including credit ratings of emerging market sovereign issuers. That is where two interesting stories have been developing recently – South Africa (and its relationship with parastatal power company Eskom) and Mexico (and its relationship with parastatal oil company Pemex).

South Africa’s Eskom

South Africa (long-term foreign currency debt) is currently rated Baa3 by Moody’s and BB+ by Standard & Poors. These ratings are respectively just above and just below the critical investment grade threshold at which many investors will choose to disinvest. Key to this is the parlous state of South Africa’s state-owned electricity utility Eskom. Eskom has struggled for years with high operating costs and a steadily increasing debt burden. The costs are from a variety of problems, including poor choices for capital investment (specifically two of the world’s largest coal-fired power stations, both behind schedule and over budget), poor execution of those investment decisions (including serious operating problems at those power stations), low employee productivity and failure to collect receivables from local municipalities. Eskom currently has a total indebtedness of ZAR 420bn (US$29.6bn) and trailing 12-month EBITDA of only ZAR 44.3bn (US$ 3.4bn).

Without major financial support from the state, Eskom will be bankrupt. But this is simply not an option as the lights must be kept on. South Africa is already struggling with a series of crippling rolling electricity blackouts, and Eskom must be rescued both as a financial entity and as an operating concern. Analysts estimate that Eskom needs around ZAR 150bn of financial support, or ZAR 23bn per annum. Finance Minister Tito Mboweni’s maiden budget in February included a promise of ZAR 69bn of aid for the next three years, sparking statements of concern for South Africa’s sovereign credit rating.

Mexico’s Pemex

Mexico, despite better credit ratings of A3 (Moody’s) and A- (S&P), has also seen the ratings agencies express concern about state support for a huge parastatal. Pemex, the state-owned national oil company, has debts of MXN 2.1trn (US$ 106.7bn) and trailing 12-month EBITDA of MXN 494.8bn (US$ 25.8bn). Fifteen years of declining oil production and underinvestment have created a powerful short-term funding squeeze – a quarter of its debt matures in the next three years, which with capital expenditure requirements more than exceeds the company’s available financial resources. Meanwhile, oil output per employee runs at about 15 barrels per day (Colombian peer Ecopetrol manages 80).

We remain far more positive on the outlook for Mexico, however. The Mexican finance ministry has said it will exhaust its other options before offering an explicit guarantee of Pemex’s debt, while the unpalatable alternative of seeking foreign joint venture participation in Pemex is, at least, a possibility. The South African treasury is already bailing out Eskom, and the chances of attracting foreign capital into Eskom are nil. Finally, the Mexican economy (2019 forecasts: current account deficit 1.5%, fiscal deficit 2.5%) remains in fundamentally better shape than the South African economy (deficits forecast at 3.6% and 4.0%, respectively). Whatever opportunities may exist in exporters in these markets, it is clear to us that the domestic opportunity in Mexico has a better fundamental underpin than in South Africa, and we are positioned accordingly.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighborhood

Key highlights

• Home and personal care companies are relatively new entrants to the Fund.

• The Amazon onslaught provided a clear opportunity to buy into two industry leaders at depressed prices.

• Consumer goods companies are many and varied, but only some are actively investing in the brands which can underpin their continuing success.

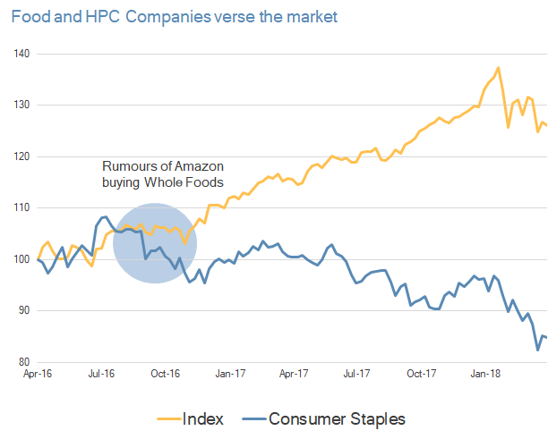

We identified food and home & personal care (HPC) companies as a key research focus in 2017 after Amazon’s $US13.7 billion acquisition of upmarket grocery chain Wholefoods.

At the time, the market’s reaction reflected concerns Amazon would disrupt the US retail and digital food landscape – and no brand would be safe.

Food and HPC companies underperformed after the Wholefoods deal as you can see here:

Source: Factset

But we saw an opportunity.

We intensified our research on the major food and HPC companies and soon came to a different conclusion to the market.

We believe global brands are still in demand. Those that can develop an effective and sustainable digital strategy will be able to drive traffic online as well as in store.

Many global brands have larger market shares online than they do in store, because online shoppers are time-poor and tend to be more brand conscious.

This research led us to initiate positions in two companies: Colgate-Palmolive (Colgate) and Procter & Gamble (P&G).

Both companies enjoy strong market shares, driven by management that understand the need to consistently invest in their brands to drive long-term sustainable growth.

Reviewing the thesis

To test our research and conviction in these names, we attended the Consumer Analyst Group of New York (CAGNY) conference in Boca Raton, Florida.

This industry conference is the largest of its kind, run by a not-for-profit group and designed to facilitate robust dialogue among investors, analysts and consumer industry executives.

The February event provides management the opportunity to discuss their new products and strategy for the coming year.

This year’s conference featured presentations by senior managers from 31 consumer companies, including Colgate and P&G.

A key theme was refocusing on investment and innovation to drive top-line growth, alongside the opportunity to drive online sales through targeted digital strategies.

This is very much a change from the last couple of years where the focus has been on driving margin improvements through cost savings.

Our process tends to de-weight companies with a binary focus on cost saving initiatives. From experience they tend to be unsustainable beyond the short term.

Many of the companies at CAGNY have come to the conclusion they were too aggressive in cutting costs as a means of driving sales growth – and now need sustainable investment behind their brands.

This was poetically demonstrated when Kraft Heinz — the epitome of this singular focus on margins — released their Q4 earnings results during the conference. (They were not in attendance).

The stock was down 27% the day after management cut the dividend and conceded the need to step up spending on their brands to reinvigorate revenue growth.

By comparison, the HPC companies we own have been consistent in their approach to brand management and investment. In 2019 they are focusing on the latest innovations and product launches.

Colgate-Palmolive – cleansing the market’s palate

In 2019 Colgate is embarking on one of the biggest projects in its 200 year history — a relaunch of its bestselling Total toothpaste.

The company already holds a dominant market share for its oral health care range across a number of countries, but there is little evidence of complacency when it comes to product development.

This new iteration of the classic Colgate product is the result of 10 years of research and development.

This depth of reinvestment into what is already a market leader is testament to the value Colgate places on its brand.

The financial pay-off comes in the form of improved price control. Developing core products like Colgate Total into a premium category can place HPC companies in a strong position to exercise pricing power and expand margins while still growing sales volumes and consumer loyalty.

The new Colgate Total is designed to provide even more benefits to the consumer including relief from sensitivity, stronger enamel and fresher breath.

The company’s other categories reflect effective innovation in targeting consumer preferences.

Colgate Naturals toothpaste — with ingredients such as lemon, charcoal and even seaweed — address a growing consumer preference for natural ingredients over manufactured alternatives.

The Palmolive purifying clay body wash is another example of innovation through using natural ingredients.

Intersecting innovation with distribution

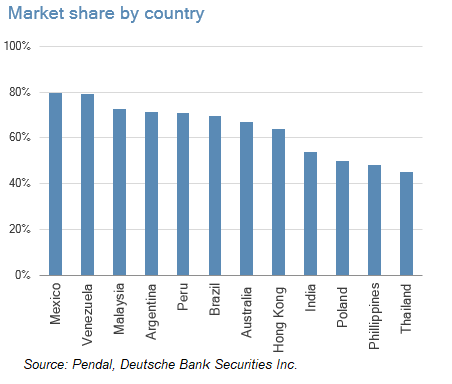

Addressing growth in emerging markets is another key feature of the company’s growth strategy. Colgate derives 50% of its sales in emerging markets, with leading positions in the following countries.

Colgate achieves this high market share through its price pack architecture which includes products for all income levels. As incomes rise in these markets, consumers can trade up to the higher priced products.

Educating customers is of paramount importance for Colgate and offers further opportunity.

Educating customers is of paramount importance for Colgate and offers further opportunity.

In Colgate’s markets, 68% of the population brush their teeth less than once per day. Greater education on the importance of brushing morning and night can double consumption.

The company’s education programs begin in schools through the Bright Smiles, Bright Futures program, which provides dental care resources to teachers.

The program has been in operation since 1991, reaching more than 850 million children in 80 countries. The company has ambitions to reach 1.3 billion by next year.

In developed markets they introduced Colgate Magik, a tooth brush that uses augmented reality to teach kids how to brush their teeth. Take a look at the promotional video.

Programs like these exhibit the long-term power of capturing and nurturing customer loyalty from a young age — an approach often overlooked by companies.

In our view, Colgate stands out for its leading brands and a strong management team willing to operate the company for long term value creation.

A long term approach

Similar to Colgate’s management approach, we also apply a long term approach to investing and take the required time to build conviction.

We purchased Colgate for the first time in June 2018 when it was trading at a buyout yield (our preferred valuation measure) of 8%.

The stock had traded sideways for around five years so the burden of proof for the upside potential was squarely with the company’s management team.

We then waited another six months before adding to the initial investment, which was further complicated by short-term impacts from foreign exchange fluctuations, rising commodity input costs and a trucking strike in Brazil which weighed on market sentiment and the stock price.

Notwithstanding these externalities, we have confidence in the company’s ability to capitalise on its investments in the brand and deliver above-market growth over the longer term.

Procter & Gamble – harnessing environmental and digital dividends

We made an initial investment in P&G in December 2018 at the time when its share price reached a buyout ratio of 8%.

The updates from P&G at CAGNY were particularly insightful and in time may provide a useful case study on the synergies of innovation, operational leverage and ecological awareness.

P&G showcased its new waterless soap DS3 Clean brand at CAGNY.

Established as an incubator brand, DS3 is sold on the crowdfunding and product innovations digital platform, Indiegogo. DS3 Clean has a multi-faceted approach to delivering value:

1. Addressing environmental concerns about water use and packaging waste.

2. Reduced emissions through reduced transport costs.

3. Increased customer convenience by shifting the final stage of production to the household. DS3 products are delivered to the customer in solid form and convert into a liquid when exposed to water, allowing for less packaging and easier shipment.

DS3 cleaning products include laundry detergent, toilet cleaner, surface cleaner, hand wash and even shampoo and conditioner. Take a look at the DS3 demo.

Expansion of the brand will benefit P&G margins because products are priced at a significant premium to the innovative pods product under the Tide brand.

Tide pods are a unit dose product designed for convenience and efficiency over the liquid detergent variant. US household penetration of pods grew from 16% in 2016 to 26% in 2018, highlighting the growth opportunity that still exists for this product and also the potential to grow the DS3 brand.

The Tide pods product is driving growth in the US laundry category and has allowed P&G to build a greater share of that market (US market share of tide pods is 80%).

As customers gravitate towards e-commerce, P&G is looking for innovative packaging solutions that delight the customer – and save costs.

The Tide Eco Box liquid laundry detergent pack is one example. It doesn’t require additional boxing for online sales, takes up less space due to the box design and uses less water.

In addition to innovation drivers, P&G is undergoing a five-year $US10 billion cost reduction program (2017-2021). Some of the savings will inevitably be reinvested in the business. We believe a proportion will translate to the bottom line.

This, combined with the diverse portfolio of products and a focus on innovation, makes P&G an attractive investment.

The company is valued on an 8% buyout ratio and is generating substantial free cash flow to support an attractive 5.1% dividend and buyback yield.

A key philosophical principle of our investment approach is to only invest in companies that command leading positions in their respective markets and actively invest in their brands.

Invariably this is a function of a company’s brand strength and longevity in the market.

Attending CAGNY reinforced our belief that companies which are able to consistently reinvest in their brands will drive long-term value creation for shareholders.

We see Colgate and P&G as industry leaders with a strong trajectory of sustainable growth ahead.

Click here to find out more about the Pendal Concentrated Global Share Fund.