Followers of the Pendal Global Emerging Markets Opportunities Fund will be aware of our belief that one of the most exciting stories in the emerging market world right now is the ongoing corporate governance revolution in South Korea, and the resultant unlocking of the extreme value that exists in the Korean equity market.

A number of factors have combined to drive this revolution, including an ageing population, low returns from Korean and global fixed income markets, and the intervention of activist investors. Now, the social pressure for governance reform is slowly turning into political pressure.

At stake is the one of the world’s lowest dividend payout ratios, and the web of interlocking and circular shareholding structures that enable it. As we wrote in 2017, ‘The behaviour of corporate Korea and the related lack of dividends has become an increasing issue in Korean politics, as an ageing population needs income from its investments. We feel that both the Korean public’s response to the corruption scandal, and the resulting election of a left-wing administration, will put huge pressure on Korean companies to reform.’

We have since highlighted the steadily increasing dissent rate of the National Pension Scheme (NPS, the largest investor in Korea and the third largest public pension fund in the world), as further evidence of the widespread demand for change. From a normal level of about 10%, the rate at which the NPS has voted against Korean corporate management rose to 12.9% in 2017 and 20.5% last year. We have also seen wide reform of Korean corporate structures, partly driven by shareholder pressure and partly by the increasingly shareholder-friendly regulations brought in by the Korea Fair Trade Commission (FTC).

This process will have milestones. One was reached in October 2015 when Samsung Electronics reformed its shareholder return policy. Another was reached on Wednesday (27 March 2019), when Cho Yang-ho, the chairman of Korean Air, lost his position at the head of his own board, as the NPS voted against Mr Cho’s reappointment.

Mr Cho failed to receive the required two-thirds majority of shareholders’ votes to retain his position, with the NPS joined by some of Korean Air’s largest foreign institutional shareholders in voting against him. While by international standards this may not seem controversial (Mr Cho is accused of embezzling company funds and unfairly awarding contracts to family members, while his daughters have also been caught up in several scandals at the company, including the ‘nut rage’ incident that readers may recall), the outcome of the vote has shocked the generally conservative Korean business community.

The Cho family will retain their control position at Korean Air, and only the week before the NPS had voted with company management and against foreign activist shareholders at the Hyundai Motor annual general meeting.

This revolution will not arrive everywhere at once, and not all cheap Korean companies will see value unlocked in the near-term. But we are confident that Korean corporate governance is undergoing irreversible and revolutionary change and the NPS rejection of Mr Cho is a powerful symbol of that. We remain overweight Korea in the portfolio.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighbourhood

The following speech was delivered by Richard Brandweiner, CEO of Pendal Australia, at the KangaNews 2019 Sustainable Debt Summit on 18 March 2019.

From fringe to foreground – the evolution of sustainable investing and the opportunity for investment management

In the beginning of our modern sensibility, there was only one axis.

Returns.

Investment returns, company profits, GDP growth.

As individuals, we would go to a stock broker to invest on our behalf and outcomes were judged solely on returns.

In the 1960s and 1970s, the investment industry discovered it was able to measure a second axis. With the advent of modern portfolio theory, we came to understand that there was volatility which could be measured which was inherent in achieving those returns. We pretended we could forecast it, and risk became the second axis. Now many generations later, no self respecting professional investor would ignore volatility in making an investment decision. In fact, we have become obsessed with it, almost as if it’s the fulfilment of our craft.

So, is that where it ends?

Is the entirety of the purpose of investment management encapsulated in getting as far to the top left of that neat two dimensional chart?

Where does our role as an intermediary fit?

An allocator shifting capital from savers to borrowers or businesses. Determining, as part of a supreme collective, what deals live or die, where profits are to be made and how the users of capital should behave.

All the while, contributing towards externality after externality, both positive and negative.

There is, in fact, a third axis. But we are only just starting to become aware, and we are certainly a long way away from being able to measure it.

The third axis is impact.

Glenn Stevens put it neatly – “For finance is not, for the community, an end in itself. It is a means to an end. Ultimately it is about mobilising and allocating resources and managing risk. Finance matters. Its conduct can make a massive difference to economic development and to ordinary lives – for good or ill.”

“There is, in fact, a third axis. But we are only just starting to become aware, and we are certainly a long way away from being able to measure it.

The third axis is impact.”

Maybe, the third axis doesn’t matter.

Maybe if we just allocate to the most profitable enterprises and leave them be – as specialists in what they do – the world will continue to become a better place.

Except for two things….

1) Firstly, time horizons and incentives are not aligned.

In terms of time horizons, as we know, the big things that really matter move more slowly than the impact of short term financial returns.

And in terms of incentives, given the opaque industry of agents within financial services, with its specialised expertise and discretion to act on behalf of others, unless it recognises a bigger purpose, it has considerable opportunity to act in ways that are not in the interests of the outside world that it is there to serve. I no longer think this is a controversial statement.

Yet, the externalities generated by allocating capital are real. Markets generate economic value, and there is little that can match their ability to allocate goods and services and encourage innovation and technological improvement. The allocation of capital impacts employment, infrastructure, productivity, taxation and, of course, our society and our environment more broadly.

I suspect, as I’m sure many of you do, that the impact of these externalities far outweigh anything else and are much bigger than we generally realise. Like an iceberg. What we don’t’ see because we can’t measure it, in all likelihood dwarfs our simple view of the world.

Of course, a proper market and effective competition, like Adam Smith envisaged, requires companies to bear their real costs and not leverage asymmetries of information and power.

And fortunately, as each day turns into the next, and time horizons evolve from one to another, externality after externality gets priced in. We can see consumer behaviour shifting as we speak.

2) Secondly, the size of the financial system – its volume – is too significant in our small world, and so the responsibility becomes too real.

Over $7 trillion turns over in capital markets globally every single day. That’s equivalent to about 10% of annual global GDP.

The financial services sector comprises between 15 and 20% of the global economy, and has doubled over the last fifty years.

The Willis Towers Watson Pension Fund Survey puts the total capital controlled by asset owners and fund managers globally as $131 trillion, equivalent to almost twice the annual production of our entire world.

The financial system controls the assets of the world.

Whether you’re more interested in the Gospel of Luke – “from everyone who has been given much, much will be demanded” or simply Uncle Ben from Spiderman, “with great power comes great responsibility” – it is impossible not to recognise the immense responsibility that comes with power of allocating such vast volumes of capital in the world.

The world into which we retire will in no small part be a function of how we invest. Those who invest for short term profits and ignore the impact of their allocations of capital are not creating real value.

I’m reminded of a famous sermon by John Wesley in the nineteenth century:

“And it is our bounden duty to do this: We ought to gain all we can gain, without buying gold too dear, without paying more for it than it is worth. But this it is certain we ought not to do; we ought not to gain money at the expense of life.”

Altogether, this is about the third axis, the third dimension. Perhaps not the fulfilment, but a step towards a greater understanding of investment decision making. Our challenge is to improve measurement in the third dimension, to make it real for all agents and to institutionalise it in the way that modern portfolio theory changed our profession.

Now, it is debt that brings us together today –

ESG was all about the equity gang, partying, as they do down at the bottom of the capital structure, blindly holding on to their ‘first loss’ pieces of paper.

In the ecosystem of sustainable investment, equities investing is like the showy spring flowers: – flashes of newsworthy colour, high profile divestment announcements and all the drama of activism and only seasonal proxy voting.

Yet the reality is that most of the equities action is taking place in secondary markets – at least a step removed from the processes that direct funds to the real economy.

Debt, of course, is far more cool.

– the proportion of new issues to debt traded in secondary markets dwarfs that of equities

– the need for borrowers / issuers to come back to the market regularly (this is the exception in equities, not the rule)

– and, of course, debt’s depth of penetration into economies. At any moment, it creates exposure to many more segments, asset sizes (right down to microfinance) and organisational structures.

It is uniquely placed to meet the vast challenges we face in the 21st century, because our very model of sustainable development– the one the world has agreed on in the form of Sustainable Development Goals – focus on issues that are more frequently handled by the entities that issue debt rather than equity – banks, governments, corporates of course, but also many unlisted assets and enterprises.

The annual SDG financing gap in developing countries is estimated at approximately USD 2.5 trillion, and although this seems huge, it constitutes only 3% of GDP, 14% of global annual savings, or 1.1% of the value of global capital markets.

There is a role for all of us to play to galvanise debt markets to fulfil the challenge, opportunity and responsibility of investing. Whether we are Issuers, Arrangers, Fund Managers, Asset Owners or Ratings Agencies.

Or Private Investors, themselves.

I’m here to ask you to come with us, a fund manager, on this journey

– to be mindful of externalities and seek out investments that create positive outcomes

– and to continue to call for more accountability and for more transparency.

“There is a role for all of us to play to galvanise debt markets to fulfil the challenge, opportunity and responsibility of investing. Whether we are Issuers, Arrangers, Fund Managers, Asset Owners or Ratings Agencies.”

For us, at Pendal, it reinforces what we believe is the critical importance of active management. We see our role as stewards of capital – generating returns while being mindful of externalities, and holding issuers and management to account.

This is something that passive or algorithmic strategies simply cannot do.

Active managers bring a unique analytical discipline to the task of sifting the value from the noise and being able to identify debt instruments that contribute to the solutions.

One part of it is very much about understanding the fundamentals of the contract – there’s good evidence, at least on the equities side, that focussing on the sustainability issues that intersect with business fundamentals can deliver meaningful alpha.

And furthermore, demand based on these fundamentals will impact the cost of capital over time and ensure markets do their thing, with the right information.

But we need to go further than returns, even over the medium to longer term.

We need to understand how efficient capital allocation gets the non-financial environment and social outcomes we need. It boils down to a commitment to – at least considering – ‘what needs funding?’ in the mix of questions about what assets we seek out as we build a portfolio.

And this can provide some counterintuitive results for those who hear ‘sustainability’ and think ‘ethical screening’ – but it can prompt a rich dialogue with clients as well as issuers. For instance

– It might be more sustainable to finance a company with a high CO2 emissions profile so that it can invest in new technology that lowers those emissions.

– It might be more ethical to fund a bank that needs to invest in changes to its systems, governance structures and its people, rather than to divest at just the time they need support to make changes.

– Controversially, it might be better to invest in a tobacco company and push them through engagement to cease their cynical marketing to young people in the developing world.

Thinking about ‘what needs funding’ is most relevant when it comes to ‘impact’ investments – many of which are green bonds or social impact bonds.

The role for asset managers in this space is significant. There are thousands upon thousands of genuinely useful, sustainable activities and enterprises out there that need funding and these are of such great interest to our clients, that it’s fair to say that demand for quality offerings exceeds what we would describe as investment-grade supply.

One of the most important things we can do is to educate the market on what ‘good’ looks like. We just released a paper on gender bonds with our Responsible Investment Research boutique – Regnan, which took a look at what next generation gender bonds could look like, based on would be attractive to our funds and clients.

And of course, there is a critical role for us to play in demanding greater transparency and improved measurement. As we have invested in more and more green and social bonds, we note the market has some way to come. There is a parallel in terms of corporate sustainability reporting (lots of push back, slow up take and difficulty in sourcing information). We recognise it’s an evolution – the first step is the hardest – but with guidance, ‘leader transparency’ and experience this steep learning curve should flatten out over time. There is already plenty of evidence that better corporate sustainability reporting tends to be ‘rewarded’ over time.

“The role for asset managers in this space is significant. There are thousands upon thousands of genuinely useful, sustainable activities and enterprises out there that need funding and these are of such great interest to our clients, that it’s fair to say that demand for quality offerings exceeds what we would describe as investment-grade supply.”

The recent Climate Bonds Initiative’s report into post-Issuance reporting practices globally in the green bond market found that, of the 367 issuers in the CBI research universe only 53% provided impact reports. Interestingly, these CBI findings are in line with our own analysis across our holdings of Australian Green Bond issuers.

Impact reporting aims to provide insights into the environmental or social benefits of Green, Climate, Social or Sustainability bond financing. Best practice is evolving to incorporating the quality of the E or S outcomes that are part of the underlying projects as part of the security selection process. We need this to improve over time.

Ladies and gentlemen,

Investors and allocators of capital are, in no small way, the architects of our future. All of us here are at the drawing board. We have the unique power that comes with a privileged position in our society. Please, let us act together to create the future that we want.

Because the future is worth investing in.

Read more about Pendal’s responsible investment capabilities

The Australian Sustainable Finance Intiative – helping steer the Australian economy through a critical decade

A sustainable and resilient economy – one that prioritises human well-being, social equity and environmental protection – is the foundation for ensuring Australia’s prosperity throughout the 21st century. That’s why the leaders and senior executives of Australia’s major banks, superannuation funds, insurance companies, financial sector peak bodies, civil society and academia are coming together to set out a roadmap for realigning the finance sector to support greater social, environmental and economic outcomes for the country.

The Australian Sustainable Finance Initiative, launched on 27 March, is an unprecedented collaboration to help shape an Australian economy that prioritises human wellbeing, social equity and environmental protection, while underpinning financial system stability, in what it says is a ‘critical decade’ ahead.

Pendal is proud to represent the investment management industry on this critical initiative. Over the past decade we have seen growth in a number of groups individually advocating for greater cohesion with business, financial, social and environmental imperatives. Bringing the wider financial industry together through the Australian Sustainable Finance Initiative means we will now have a truly collective approach to developing a comprehensive roadmap that will address the many present and future challenges.

The Roadmap development process will be overseen by a Steering Committee consisting of senior financial services, academic and civil society representatives. Richard Brandweiner, CEO Pendal Australia, has been appointed to the Steering Committee. Richard is looking forward to contributing to this important initiative, drawing upon his deep experience in the fields of impact investing and responsible investment practices.

Richard is a passionate advocate for responsible investment and delivering societal outcomes. He shares his expertise through current appointments on the NSW Social Impact Investment Expert Advisory Group and as Vice-Chair of the Australian Advisory Board on Impact Investing.

Find out more about the Australian Sustainable Finance Initiative.

In this second of our two-parts series, Samir Mehta looks at the oligopolistic paints industry as an example of disruption risk and continual reinvestment to support future growth.

In Asia, there is one difference when compared to developed markets. Good long-term growth opportunities for several companies are still robust, albeit frequently interrupted by macroeconomic challenges. Take India as a case in point. After disruptions due to demonetisation and the introduction of a GST, we now confront geopolitical tensions. I have no opinion of how this situation will resolve, but suffice to say that in the past, saner heads have prevailed. Results for the quarter ending December 2018 are almost through. Companies that managed the disruption of GST and demonetisation well were rewarded handsomely by the market; P/E multiples for the better-managed firms remain high.

Take Asian Paints (AP) for example. On the face of it, the stock has always appeared expensive on both an earnings as well as price-to-sales multiples. In my opinion, there is a logical reason for this: the structure of the paint industry. The world over, the paints industry is an oligopoly. Even in America it has yet to be disrupted by the internet giants. In India, too, the industry is a cosy oligopoly, with AP the clear market leader. As of March 2018, total industry revenues were estimated at approximately Rs500bn (US$7bn), of which AP reported revenues of Rs166bn (US$2.3bn). The unorganised sector (small mum-and-dad chemical plants that have low-end paints with no brand resonance and poor distribution) still account for 30-35% of total sales. That share is likely to fall over the next decade, in my view. This will partly be driven by trends of rising incomes and aspirations of customers who gravitate to branded offerings, but moreso due to the introduction of the GST in 2017 and lowering the GST slab to 18% compared with 28% in prior years.

The world over, the paints industry is an oligopoly. Even in America it has yet to be disrupted by the internet giants.

To illustrate the hold the four big companies AP (52,000 dealers), Berger (23,000), Kansai Nerolac (21,000) and Akzo (14,000) have on the market, it is instructive to look at the progress of a couple of firms that entered the industry early this century. Indigo Paints started in 2000 and Kamdhenu Paints opened in 2008. It is difficult to get exact data of these unlisted firms but, from public data sources, Indigo has approximately 12,000 dealers while Kamdhenu has 4,000. After 18 years in the business, sales for Indigo are approximately Rs5-6bn pa. To put that in perspective, the top four firms collectively spent Rs13bn in advertising and promotions in 2018.

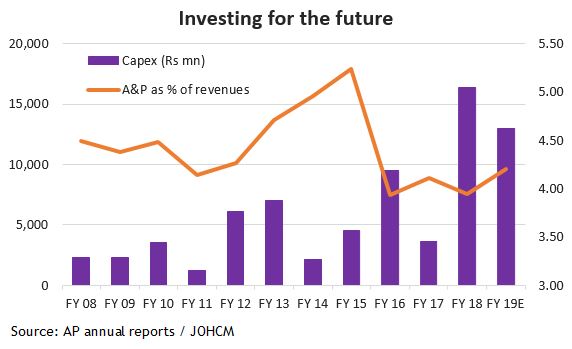

The cost of painting an apartment varies from 1-3% of the cost of purchasing the apartment. Paints are integral to decoration and aesthetics of the house. There is an umbilical link to the health of the real estate industry. In the past 7-8 years, home prices in India have, on average, remained flattish. A big bull market in property prices, which began in 2001/2, created an overhang of supply. Even in tough years, paint volumes have averaged growth of 6-8% pa. Fortunately in the past couple of years, the Indian government has refocused its efforts on the housing sector. Providing subsidised rates of interest for affordable housing, changing GST rates for finished and unfinished homes and recognising that building and construction industries can provide ample employment opportunities. The industry is working with the National Skills Development Corporation to impart skills in its effort to train painters and increase engagement with architects. Current penetration levels of paints in India is low. Housing demand in India is likely to grow steadily as income levels grow and joint families splinter over time. As the industry leader, AP is using its cash flows to create capacity well in advance of anticipated demand. In the past five years, AP has invested Rs46bn in capex compared with just Rs20bn in the five years prior. Its A&P spend remains around 4% of sales, even on a much higher sales base.

“My view on the persistence of industry growth and confidence in Asian Paint’s industry positioning and execution abilities overcomes the concerns that the company has always appeared expensive on both an earnings as well as price-to-sales multiples.” Samir Mehta, Senior Portfolio Manager

Given this dynamic, my view on the persistence of industry growth and confidence in AP’s industry positioning and execution abilities overcome the concerns about valuation. Unlike Heinz, this company’s focus remains on the growth potential that lies ahead in the decades to come. It has invested in distribution, brand and capacity and is continually increasing its lead over competitors. The free cash flow for the firm in the next five years could possible double (or more) if demand for property starts to pick up in India. Even when the economy was slowing and inflation was high, AP demonstrated it had pricing power. It continues to toggle between retaining margins and reinvesting in the business. Overall, I do not foresee a fate similar to Heinz. On the contrary, AP’s approach to business might be one that Heinz is forced to veer back towards.

Read more about the Pendal Asian Share Fund

Fund Manager commentary for the month ended 28 February 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Our investment process is designed to exploit what we believe is a market inefficiency that results from the structure of the emerging market equity investment community. Specifically, we believe the dominance of bottom-up, company-focused investors in the space creates an effect where markets alternatively ignore, and then over-react to, top-down developments. That creates shorter-term over – and under – valuations that are powerful opportunities for top-down focused active investors.

In this instance, us.

The sell-off and selective recovery in emerging markets in 2018 has created, we believe, multiple instances of this that we are actively rotating capital into. One of those instances is Dubai in the United Arab Emirates (UAE). The UAE is a federation of seven Emirates, with the two largest, Abu Dhabi and Dubai, dominant. The two are very different in nature: Abu Dhabi, backed by its hydrocarbon exports, has a conservatively managed, twin-surplus economy, with an expensive and low-beta equity market; Dubai, lacking hydrocarbons, relies on trade, tourism and investment, which makes the equity market high-beta, with close links to the local real estate market.

Dubai has had a series of real estate booms and busts in the last 20 years and is undergoing a slowdown at present. Through its currency peg, the UAE effectively imports US monetary policy, which has coincided with oversupply of development properties to push both real estate prices and related stocks down significantly. Even with a more benign US monetary outlook, the residential property market may take some time to recover. However, property companies exposed to the tourist trade through retail, entertainment and hospitality assets have similarly de-rated.

Emaar Malls

Dubai-listed Emaar Malls is a unique retail property operator, with one of the highest quality portfolios in the world. The company is the owner (not leaseholder) of a variety of retail properties in Dubai, most notably the Dubai Mall. The Dubai Mall is the largest and most-visited retail and entertainment destination in the world and is located right in the centre of downtown Dubai. Emaar Malls also operates four other large malls and some other smaller retail properties in the Emirate. In 2018, Emaar Malls’ 6.7 million (!) square feet of gross leasable area attracted 136 million (!!) visitors, a 5% increase on 2017, which in turn drove an 8% increase in EBITDA and a 7% increase in net earnings. Meanwhile, despite the super high-quality nature of its asset portfolio, Emaar Malls is surprisingly under-levered, with a net debt/EBITDA of 1.4x (peers are typically levered anywhere from 3x to 12x).

So, have investors over-reacted to the slowdown in the Dubai economy? In our view, absolutely. At the time of writing, Emaar Malls is on an operating yield of 12.5%, (compared to a typical level for global peers of 5-9%). From another viewpoint, Emaar Malls had, at 31 December 2017, independently-valued investment properties worth AED 54.0 billion, new assets coming into operation in 2018 and net debt at 30 September 2018 of AED4.0 billion, but a market capitalisation at the time of writing of only AED 22.8 billion. It is our strongly held opinion that there is no sense to these valuations, and we have accordingly been building a portfolio position in Emaar Malls.

Emaar Properties

Similarly, Emaar Malls’ parent, Emaar Properties, has also sold off to an extent that seems irrational. As well as its stake in Emaar Malls, the other key subsidiaries are also listed, allowing a valuation to be calculated for Emaar Properties’ core hospitality and entertainment assets. At points in recent weeks, the implied value of the core assets has been negative.

With these two holdings we acquire both a highly defensive and a more cyclical holding, both at valuations that imply company-level distress or national crisis. We feel there is nothing happening in Dubai beyond a downturn in the property market, and have a high degree of confidence that both these investments will, in time, prove to be highly profitable as the emotions of the Dubai-facing investor community inevitably swing from excessively negative to overly positive.

No use buying the best house in a bad neighborhood

Be a part of the world’s fastest growing economies

The 8th of March each year marks International Women’s Day and today we take the opportunity to delve into a growing segment of the Responsible Investing market – gender equality bonds. With the teams at Regnan and Pendal coming together following Pendal taking full ownership of Regnan, we are pleased to provide a collective review of this emerging area of the bond market.

This article provides an update on the gender bonds market and considers what the next evolution might hope to achieve in advancing women’s equality and empowerment.

View the article

Pickle: any brine, vinegar or spicy solution used to marinate food; synonym – predicament: a condition or situation that is difficult, unpleasant, embarrassing or comical.

The annual results of Kraft Heinz and the commentary on what has happened to its business in the past couple of years has several lessons for those who invest in quality businesses.

With the imprimatur of Mr Buffet, the deal to combine Heinz and Kraft was a landmark transaction. An almost ruthless approach to cutting costs by the new owners was the new mantra for managing businesses with moats and steady revenues. In February 2017, it even made a hostile bid to acquire Unilever; today Kraft’s market cap is less than Hindustan Lever, its Indian subsidiary.

So what went wrong?

– To start with the easy part: leverage. It is one of the defining moves employed by private equity firms – financial engineering (in the garb of attaining the ‘right’ debt:equity mix). This led a stable business to take on significantly more debt. In itself that might not be wrong, but when a business faces challenging conditions, management teams face mounting pressure to remain within debt covenants to the detriment of investments in the future.

– Second, was the zero-based budgeting approach to cost cutting. Popular at one time amongst business consultants, it drove management by the mantra of ‘why should you spend?’ Perhaps that question is justifiable for administrative costs, but if applied to all costs this might defeat the purpose of managing and rejuvenating a steady cash-generative business.

– Finally, disruption in business conditions. The world over, retail chains were the first to feel the impact of online disruption; food and staple brands are increasingly feeling the effects now. The changing tastes of millennials, niche new brands that can scale thanks to influencer endorsement marketing strategies and help from online platforms for nationwide delivery are challenging incumbents.

It is critically important to reinvest continually into the business to maintain existing brands and create new ones. That ultimately is the crux of the ‘moat’ of quality branded businesses. In Kraft’s case, perhaps the high debt and focus on cost cutting left management with little room to focus on what should have been the core capital allocation decision.

In next week’s edition Samir compares the Kraft Heinz experience with India’s paint industry, to show the importance of balancing cost cutting initiatives and investing for the future.

Read more about the Pendal Asian Share Fund

Vimal Gor, Pendal’s Head of Bond, Income & Defensive Strategies, says there’s just one fundamental driver of all asset prices: liquidity. In this exclusive interview with Livewire Markets, Vimal discusses:

– liquidity and the implications of a tightening credit cycle

– why the US / China relationship has become too much of a focus

– a slowing global growth outlook and how this is feeding into his bearish outlook

– why the world simply can’t handle higher interest rates

– the asset class most likely to deliver a positive return in 2019

– the asset class most likely to deliver a poor return in 2019.

Watch the full interview

Read more about the team and our capabilities

“They don’t ring a bell at the top of the market…they don’t ring a bell at the bottom either”

James Syme, Senior Portfolio Manager

2018 was a difficult year for emerging markets, with a number of country-specific challenges leading to weakness in both equities and currencies.

In this quarterly update, James Syme reviews the Strategy’s performance over the past quarter and provides:

– a perspective on country-specific impacts from US economic policies;

– the underlying dynamics in China beyond the trade narrative; and

– the signs to look for ahead of a upturn in emerging markets

View the video here.

Further reading:

Be a part of the world’s fastest growing economies