Fund Manager commentary for the month ended 31 January 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

“As US monetary policy moves through the stages of fewer hikes-pause-cuts, the prospects for economic growth and market recovery in emerging markets improve. We expect strong returns from some of these markets in 2019, and have seen a strong start to the year in some of them.” James Syme, Senior Portfolio Manager, JOHCM

Federal Reserve Board Chairman Jerome Powell

There are two powerful sources of qualitative information that can help investors in emerging markets assess how US monetary policy (which is one of the key global drivers of EM equity returns) might evolve. The first of these two is the quarterly results and outlook commentary from globally-facing US companies. These comments give an immediate view of the state of demand in various economies around the world, and how those demand conditions might be feeding back into the US economy (and, in turn, how US monetary policy might evolve). The second is from speeches and comments from the leadership of the Federal Reserve, particularly where those comments reference emerging markets.

Corporate reporting

It has been our view for over a year that the G7 policy-driven slowdown in emerging economies would feed back into the developed world through weaker orders and revenues for EM-facing companies, until either weakness in financial markets and/or weakness in economic statistics caused a policy re-think in G7 capitals. Over the last twenty years, sustained weakness in emerging market currencies has led, or been coincident with, a fall in US and G7 activity measures, such as industrial production and manufacturing PMI. We expect the EM sell-off in 2018 will show up in developed market corporate and economic data in 2019.

Looking at some of the company results published so far in 2019, there are certainly signs of weakness, with China very much a focus of it. This trend includes Apple (“while we anticipated some challenges in key emerging markets, we did not foresee the magnitude of the economic deceleration, particularly in Greater China. In fact, most of our revenue shortfall to our guidance, and over 100 percent of our year-over-year worldwide revenue decline, occurred in Greater China”), Caterpillar (“Construction activities remained at low levels in Latin America… weakness in the Middle East… sales in Asia/Pacific declined due to lower demand in China”), Nvidia (“deteriorating macroeconomic conditions, particularly in China”) and Disney, where a trend of very strong results from parks and resorts was broken by “lower operating income at Shanghai Disney Resort… primarily due to lower attendance”).

Fed commentary

We can also see the Federal Reserve paying increasing attention to emerging markets. Notably, Chairman Jerome Powell held the view in May 2018 that “the normalization of monetary policies in advanced economies should continue to prove manageable for EMEs”, but by September 2018 was claiming that “when our economy is strong and we’re raising rates, that puts upward pressure around the world and can affect countries, particularly countries that have external dollar borrowing… The performance of the emerging market economies really matters to us in carrying out our domestic mandate”, which pre-figured the move to the Fed being “patient” with rate hikes.

“The performance of the emerging market economies really matters to us in carrying out our domestic mandate.” Fed Chairman Jerome Powell

This growing evidence of weakness in the cyclical part of EM does not create an automatically bearish outlook for the asset class though. One of the key sensitivities in the asset class is to bond yields and the strength of the US dollar; markets more exposed to this tend to be the more domestically-driven, current account deficit markets such as India, Indonesia, Turkey and most of Latin America. As US monetary policy moves through the stages of fewer hikes-pause-cuts, the prospects for economic growth and market recovery in these markets improve. We expect strong returns from some of these markets in 2019, and have seen a strong start to the year in some of them. In addition, the more cyclical end of EM (predominantly Asian exporters) does contain some markets that are clearly already pricing in a sharp slowdown – we would highlight the strong performance (+21.7% at the time of writing) of Samsung Electronics since its “disappointing” results on 8 January as an example of a stock already pricing in the worst. We remain substantially overweight India and Korea and continue to rotate the portfolio into more domestically-driven markets that can benefit from the Fed’s new-found caution.

In this edition of The Business, Vimal Gor, Pendal’s Head of Bond, Income & Defensive Strategies featured in a panel discussion to share his insights into the outlook for interest rates, Australia’s economy and key offshore factors to watch in 2019.

View the video here.

Pendal Group Limited (ASX: PDL, ‘Pendal’), the co-founder of Regnan – Governance Research & Engagement Pty Ltd (‘Regnan’), today confirmed it will acquire the remaining 50 per cent stake in Regnan to bring Pendal’s ownership to 100 per cent. Co-founder Commonwealth Superannuation Corporation (CSC) will cease to be a shareholder.

Regnan is Australia’s leading provider of ESG research, engagement and advisory services. Regnan’s focus on environmental and social issues can be traced back to Monash University in the late ‘90s.

Closer alignment with Regnan will support Pendal’s objectives to improve investor outcomes through a continued focus on stewardship.

Further, making Regnan part of Pendal will enhance Regnan’s capability and service proposition to its clients by enabling it to leverage the fundamental insights of a highly regarded investment management organisation, across equities, fixed income and multi-asset portfolios.

Richard Brandweiner, CEO of Pendal Australia, said: “Full ownership of Regnan will allow us to further support our clients on their journey to fully embed ESG into their frameworks, and also improve our ability to be a more active steward of their capital across all our investment capabilities.”

“Delivering evidence-based, multi-asset ESG research and stewardship is a unique value proposition, which supports our goal to deliver sustainable, risk-adjusted out-performance for our clients.”

Pendal has a strong heritage in responsible investing, dating back to 1984 with the launch of the BT Australia Charities Trust*. Today Pendal manages approximately $2 billion in dedicated sustainable and ethical strategies on behalf of its clients.

Our responsible investing journey**

About Regnan

Regnan – Governance Research & Engagement was established to investigate and address ESG-related sources of risk and value for long term shareholders in Australian companies. Regnan has evolved to become a global leader in long term value, systemic risk analysis and responsible investment advisory.

Regnan’s in-house team of experienced analysts produce rigorous, relevant ESG investment analysis. From this research and insight, the team tailors solutions to meet the specific needs of clients who include asset owners, fund managers, wealth managers, endowments, retail and investment banks. Clients use Regnan services for a range of purposes from stock selection, portfolio construction and stewardship, through to all aspects of responsible investment framework development and implementation.

Regnan engage directly with leading ASX-listed companies, on behalf of its institutional investor clients, to drive improved ESG governance and long term thinking needed for stocks to yield higher quality returns. Regnan also advocates for ESG considerations to become mainstream through contribution to the public policy debate, board and committee-level participation in industry bodies, and submissions to government.

Read more about Regnan

Read the ASX Release

* This fund was launched when the Pendal business was part of the Bankers Trust Australia Group.

** Notes on Pendal Group heritage:

1 This fund was launched when Pendal was part of the BT Financial Group. Pendal Fund Services Limited (previously known as BT Investment Management (Fund Services) Limited) became the responsible entity of this fund in 2007.

2 Formerly the BT Sustainable Conservative Fund

3 Formerly the BT Ethical Share Fund

4 Formerly the BT Sustainable Australian Share Fund

5 Formerly the BT Sustainable Australian Fixed Interest Fund, BT Sustainable International Share Fund and the BT Sustainable International Fixed Interest Fund

6 PRI signatory when Pendal was part of the BT Financial Group

7 Formerly the BT Sustainable Balanced Fund

8 RIAA membership commenced when Pendal was part of the BT Financial Group

9 Founding Member of the IGCC when Pendal was part of the BT Financial Group

The market is now expecting a greater chance of a cut by the RBA than a hike over the next year. At the same time the central bank has held firm in its bias to leave rates on hold. In this quarter’s update our Australian rates PM, Tim Hext, offers his views on the outlook for 2019 and what could move the dial. We also assess the prospects for the local credit market, where macro risks have weighed on investor appetite and liquidity has become increasingly scarce. Meanwhile in cash markets, funding cost increases have fuelled out-of-cycle mortgage rate hikes. Our Cash PM, Steve Campbell takes a deeper dive into the causes and also examines issues in the RMBS market. Finally, we discuss new developments in the ESG arena including NSW TCorp’s first green bond issuance.

We hope you find the piece useful and welcome feedback from readers.

View our Australian Quarterly Update here.

Disrupt: to break apart; split up; rend asunder; to disturb or interrupt the orderly course

It is easy to pinpoint or lay blame upon the rapid evolution of the internet and the shift online across most businesses for the tectonic disruption across the world. The likes of Tencent and Alibaba in Asia or Facebook, Netflix and others in the US are testament to the forces of structural change. Yet I do think it is as important to recognise the spark to it all: cheap and abundant capital over the past decade. A range of unconventional ideas (in the traditional sense) which would have never got off the ground a decade ago have accessed immense amounts of capital. That ability to raise capital was not a validation of these business ideas per se. Yet, in a perverse logic, raising larger amounts of capital in order to attain scale at any cost, shake out incumbents and prevent similar competitive business ideas was, by its nature, the biggest barrier to entry that could be built. Fracking for shale gas and oil is an example that comes to mind here. For those keen to learn about the intersection of raw ambition, cheap money, transformation through the geopolitics of oil, and colourful entrepreneurs, “Saudi America” by Bethany McLean is an easy and entertaining read.

When I talk about unconventional ideas scaling up at any cost, one of the extreme cases we have observed in Asia is the independent bicycle hire companies. The concept which started in China and expanded globally — based on flooding the streets of a city with millions of bicycles for exceptionally cheap rental rates — sounded bizarre at first. Companies raised several million US dollars in capital and collected deposits from customers to help them acquire more bicycles in a never-ending cycle (no pun intended). Rental income was not the main revenue source. It was all about gathering data and monetising that resource later. Never mind the mounting losses, the cash burn or the cost to cities from abandoned, vandalised cycles and unpaid creditors and employees. Last week, Ofo Bikes — one of the bike-sharing firms from China — admitted bankruptcy. The company had raised US$2.2b, yet left behind a flawed and broken business. It should be little surprise that these kinds of capital-guzzling businesses will face difficulties as interest rates and the cost of capital rises. Unsurprisingly, peers like Uber and Lyft, having remained private for some time, are now contemplating an IPO to capture as much public capital as they can and provide an exit for the early investors. Time will tell if they manage to pull it off.

When viewed over the past couple of decades, the LIBOR rate still looks reasonable in an historical context. Yet it has almost doubled in 2018, and we are now at levels last seen in 2008.

London Interbank Offered Rate – A decade is a long time

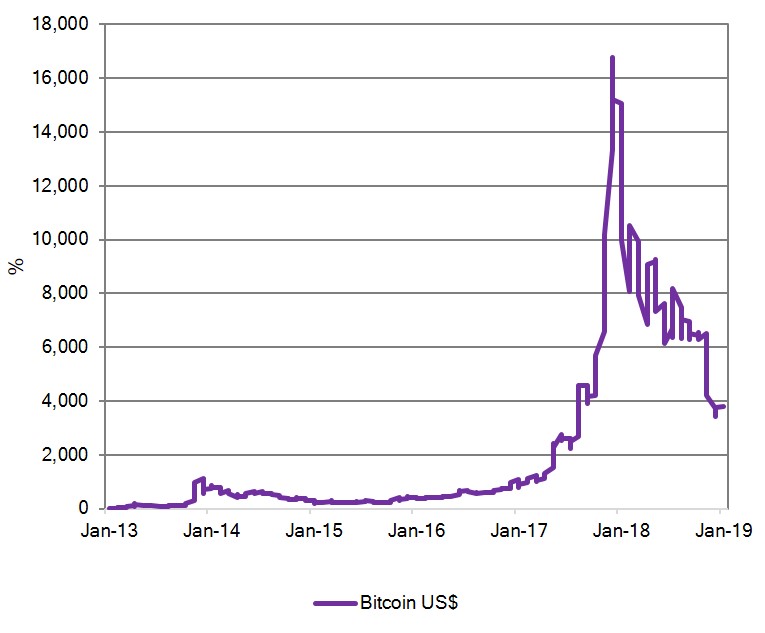

For the first time in a decade, interest on cash is greater that the yield of almost 60% of the US stock market. Any asset that looked sensible for speculation when cash paid close to zero is now clearly at risk. Bitcoin is an example of an asset which generated a lot of hype but has seen its allure falter. In my opinion, Bitcoin is another victim of rising interest rates.

Bitcoin – Just one of the victims of normalising rates

Rising rates and quantitative tightening are clearly headwinds for economic activity (which in Asia is already challenged by the trade war), as well as valuation multiples. Asia has borne the brunt of the de-rating but earnings downgrades are still coming through. Yet I do see some positives from rising rates. Disruptive businesses like the Ofos of the world should find it more difficult to access capital. Venture capital and private equity firms might also find it prudent to pull back from indiscriminate funding. In time this should lead to a more benign environment for incumbents as they have to worry less about competitors who did not focus on profits or cash flows. Speculative excesses are being curbed and genuine, well-run businesses will likely stand apart.

In the Pendal Asian Share Fund, I have reduced the weighting to cyclical stocks. With so many macroeconomic variables at play, the old school valuations of standard deviations around a mean seem less potent. When there is a return to the mean, it happens far too quickly and the reversals are equally dramatic. I will try to limit the cyclical element of the portfolio to no more than 10-15%, compared to the 20-25% I have maintained in the past. It is an acknowledgment not just that the macro environment is getting tougher, but that a rising rate environment might throw up better opportunities in the core side of the portfolio.

“While we anticipated some challenges in key emerging markets, we did not foresee the magnitude of the economic deceleration, particularly in Greater China. In fact, most of our revenue shortfall to our guidance, and over 100 percent of our year-over-year worldwide revenue decline, occurred in Greater China.”

Apple Q4 2018 results commentary

Since the middle of 2018 we have been expecting US corporate results to reflect the broad slowdown in many emerging markets (including China), and Apple has very much met our expectations with its latest quarterly commentary. However, at the same time there has been much media commentary about various stimulus policies being enacted in China, creating mixed news flow regarding the economic outlook in China.

As a starting caveat, we feel that Apple may be overstating the degree to which the Chinese economy is the cause of its disappointing results. Market share data has shown strong growth in Chinese smartphone sales by local producers, particularly Huawei, while Apple has struggled. This is because the dominance of integrated multi-purpose platforms (WeChat, Taobao) which reduce the costs of switching from iOS to Android for Chinese users. As always, it is important not to read too much into a single data point and explanation.

But there is plenty of other evidence of a deep slowdown in China. In the first nine months of 2018, domestic consumption tax revenues averaged RMB109.8b per month, however October saw revenues of RMB32.1b and November was only RMB17.0b. Car sales in October were down 13.0% from a year earlier. More industry-linked measures (e.g. rail freight turnover, cement consumption) look healthier but the trend is certainly down. Finally, stock markets are not economic data, but the Shanghai Stock Exchange Composite Index fell 28.7% in US dollar terms in 2018, reflecting the extent of negative domestic investor sentiment.

“Credit is now growing more slowly than the economy”

None of this particularly surprises us. We believe China remains an essentially domestically-driven economy (exports as a proportion of GDP is about 20%, compared with 40% for South Korea; we feel this also makes concerns about the impact of tariffs overstated), and that growth in domestic demand (and hence, economic growth) is substantially driven by the change in credit. That change in credit has been slowing since 2016 and increasingly hurting the wider economy.

Following the stimulus in 2015, the year-on-year growth in the financial system (we track all-system claims, including shadow banking products such as bankers’ acceptances and trust loans) peaked at +22.2% in the year to January 2016, but that growth rate has steadily declined. The increase for the year to November 2018 was only 8.0%; with real GDP growth for the year estimated at 6.6% and the latest CPI print of 2.2%, credit is now growing more slowly than the economy. This negative credit impulse is a significant drag on economic activity in China, and a very different environment to that which has existed since the renminbi was floated in 2005.

Various stimulus packages have been announced, with an alphabet soup of lending programs from the People’s Bank of China (SLF, MLF and PSL were recently joined by TMLF). However, the reality that we believe matters, as seen in the data, is that monetary policy in China is tight, fiscal policy is broadly neutral, and there is no immediate reason to expect a turnaround in the economy. We remain cautious on Chinese equities (especially A-shares, where we remain zero- weighted), cautious on commodities and commodity economies, and continue to expect disappointment from global companies that sell into China. At some point, probably given the weakening renminbi, Chinese policy will turn more stimulative, but we believe it will pay to wait until that turn is tangible.

Fund Manager commentary for the month and quarter ended 31 December 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

Oxford Dictionaries, the world’s leading authority on English linguistics, has judged the word ‘toxic’ to best “reflect the ethos, mood, or preoccupations of the passing year”. It’s an appropriate word to describe many of the alarming developments across the world – and their impact on investment markets. With the S&P500 down over 5% so far in December, the seasonal phenomenon of a ‘Santa rally’ – which has prevailed in 64 of the 89 December periods since 1929 – looks set to be an anomaly in 2018.

The story of 2018

After a reasonably strong January effect – another well-observed phenomenon of general optimism on stock markets to commence the year – positive sentiment quickly gave way in February to concerns over inflation coming back with a vengeance, coupled with aggressive monetary tightening which sent the US stock market to a 10% correction. Other developed and emerging markets followed to varying degrees before a relatively stable period ensued. October came and volatility returned, US treasury yields peaked and bellwether commodities including crude oil and iron ore fell prey to sellers.

Naturally, the story of 2018 goes much deeper, with multiple dynamics at play across asset classes and industries. In this article we delve into the minds of Pendal’s portfolio managers to attain their thoughts on the year, and more importantly, insights into what investors need to be aware of for 2019 and beyond.

Australian Equities

The Australian share market has experienced its most volatile year for some time. The correction we saw in February was followed by a reasonable recovery from March through to August, pushing the S&P/ASX 200 back above the 6000 mark, only to decline again in September. The market has de-rated to its longer term average price-earnings valuation of 14 times, with many good companies trading now below that level. Crispin Murray, Head of Equities, has regularly spoken about the need to focus on company fundamentals to identify catalysts for re-rating. With the market’s growing divergence we posed a few key questions to Crispin.

Q. How are you viewing the market’s recent action?

A. 2018 has ended on a note of increased volatility, with the subsequent de-rating driven by fears over the potential impact of global monetary tightening and trade wars on economic growth. This has weighed particularly on cyclicals and growth names. However, data indicates that the underlying US economy remains robust and domestic earnings estimates are not showing material deterioration. We have been using the recent weakness as an opportunity to buy some new positions and add to some existing ones. But we are being judicious as growth and defensives are still looking expensive versus the rest of the market and their own history.

Q. Much of the market’s macroeconomic concern is focused on China. What is your high-level outlook here?

A. Economic growth in China remains a key factor for commodity prices and therefore prospects for the Australian mining sector in 2019. Growth has been decelerating on the tightened credit that came with the Government’s clamp down on the shadow banking sector. Markets fear this will see a significant decline for demand for commodities, particularly if exacerbated by ongoing trade frictions. While this is a risk, we need to remain mindful that supply-side discipline remains supportive for commodity priced and China would probably move to stimulate an overly weak economy and not sit idle.

Australian miners remain cash generative and disciplined in their capital allocation. We remain cautious in the near term given the risks but are keeping a close eye on the sector, ready to take advantage if we see sentiment turn too negative. In the interim, we have been building a position in mining services as we reach that point in the cycle where miners need to replace and expand mines and maintain their equipment.

Q. You have been talking about corporate disruption for the past two years, does this trend continue into 2019?

A. Several sectors of the economy and market continue to face challenges to traditional business models and industry structures from technology, competition, and government/regulatory intervention. It is the latter which is looking likely to shape up as the key disruptive element in 2019. Not only do we have the Royal Commission final report due in February, but in recent weeks APRA’s action on IOOF and the ACCC’s initial response to the TPG/Vodafone deal suggests regulators will be increasingly inclined to flex their muscles. Banks, wealth management and power generation have all been hit hard by government intervention in 2018. There are signs that both insurance and aged care may be under scrutiny in 2019, however we would not be surprised to see the effects of this trend manifest in other parts of the economy. As with all disruptive forces, this can provide a challenge for companies – but also opportunities for active investors as heightened uncertainty leads to the chance of mis-pricing risk.

Fixed Interest & Cash

Over the year, Australian bond yields were relatively range-bound and the yield curve flattened in sympathy with its global peers. This was alongside swings in risk sentiment that revolved around geopolitical risks, with changes in US Federal Reserve (Fed) and European Central Bank (ECB) policy expectations also playing a part. Following the latest rate hike by the Fed in December and a tempering of market expectations for further hikes in 2019, we asked Vimal Gor, Pendal’s Head of Bonds, Income and Defensive Strategies for his thoughts on how rates and credit are likely to play out.

Q. Australian bond yields have traded lower this year, while US bond yields look set to finish 2018 higher. Is this divergence expected to continue in the period ahead?

A. There are two forces that should continue to direct US yields in 2019. The first is the outlook for the US economy. We believe the US is still mid-cycle and has the potential to remain relatively strong in the near-term. This is reflected in leading indicators like manufacturing surveys. While this would point to higher yields, the Fed has also acknowledged that rates are now closer to their neutral level and expectations for hikes next year have moderated significantly. As such, the potential for yields to increase may be limited.

The second force remains risk appetite, where an increase in broader market volatility and geopolitical concerns could put pressure on yields. Australian yields should take some guidance from the US, but our view that the RBA will remain on hold for at least the next year will likely see them remain range-bound and below their US counterparts.

Q. The ECB recently announced the end of its quantitative easing program. Do you see them raising rates in 2019?

A. We believe the ECB will not raise rates in 2019, which has been a non-consensus call until recently. Economic activity for several of the Eurozone’s largest members has deteriorated this year including Germany, France and Italy. Additionally, all three will face political uncertainty that may compound over the next year. Italy will also face fiscal constraints, which maybe a drag on economic growth and could cause GDP to contract further. At the same time, the end of the ECB’s asset purchases will remove a degree of support for both sovereign and corporate bonds in the region, which supports our negative bias for European credit and the euro.

Q. Is market volatility expected to rise, fall or do both, and how does volatility impact your investment strategies?

A. The ongoing liquidity withdrawal from the global financial system points to higher volatility going forward compared with previous years. Globally, central bank balance sheets will shrink for the first time in a generation. With tighter availability of credit comes more stringent pricing of risk. It also brings a less-forgiving market as illustrated by the reaction to bouts of geopolitical uncertainty over the year. We expect such an environment to persist in 2019 and our funds are positioned to benefit accordingly.

Global Equities

As expected, market volatility increased this year in response to largely macro and geopolitical issues. Prime among these were Trump’s policy agenda, US-China trade, Brexit machinations and monetary tightening. We also saw significant sector rotation as Financials rallied on expectations of aggressive Fed tightening before reversing late in the year. The US technology heavyweights – Facebook, Apple, Amazon, Netflix and Google’s parent entity Alphabet – or ‘FAANG’ stocks, were key drivers of the market’s gains during the first half before suffering a reversal when softer earnings expectations spooked the market. Ashley Pittard, Portfolio Manager of the Pendal Concentrated Global Share Fund, lends his insights into how the team navigated the year.

Q. You have not invested in FAANGs this year aside from Google and remain positioned that way. What is the team’s rationale for this position?

A. Our discipline of buying high quality, industry leaders that meet our valuation hurdles led us to steer clear of the FAANGs except Google. There is no dispute they are great companies operating world-leading platforms and product suites, but their valuations left little to gain and importantly, some of these names carry nascent regulatory risks. We wrote about this at length earlier in the year when we saw better value in other areas of the US tech sector such as semiconductor manufacturers like Analog Devices and Texas Instruments.

Q. How were you positioned in financials?

A. Based on our expectations of rising interest rates in the US and monetary tightening elsewhere, we saw great potential in operators of stock exchanges. There are listed companies like CME Group, Deutsche Boerse and Japan Exchange Group which are direct beneficiaries of higher market volatility and therefore, higher trading volumes. These companies delivered impressive returns for our clients this year of around 41%, 20% and 15%, respectively.

Q. Given stock exchanges and semiconductor names have done well this year, what areas do you expect to find interest in 2019?

A. We’re long term investors and rely on our valuation discipline to guide our research focus. The stock exchange and semiconductor names above are great businesses and remain attractive based on our metrics. The heavy macro influences this year have driven the share prices of some great industry leaders to attractive levels and we’re closely monitoring companies within the infrastructure, pharmaceuticals and consumer-related industries and expect to see additions next year. During the year we reduced our technology weight in the Fund from 20% to around 12% and increased the exposure to pharmaceuticals to 11%. We’ve also held a higher level of cash over the past few months (up to 11%) and we expect to reinvest as opportunities arise.

Listed Property

The A-REIT market has delivered a positive return for the year to date, surpassing the negative returns from share markets in Australia and around the globe. We asked Pete Davidson, Head of Listed Property at Pendal for his thoughts on the sector.

Q. What’s driven A-REIT returns this year?

A. We’ve seen four main themes driving returns for the listed property sector in Australia:

1. lower Australian bond yields

2. limited new equity issuance

3. some merger and acquisition activity; and

4. very strong office and industrial markets.

Lower Australian bond yields reflect the fact that after 27 years of uninterrupted growth, the Australian economy is slowing. Our economic growth rate is now below the US for the first time ever, with Australian bond yields around 0.40% below the equivalent US bond yield.

A-REITs are very sensitive to Australian bond yield movements, so lower bond yields have served to underpin A-REIT valuations. Equally, slowing economic growth has encouraged many investors to rotate back to defensive asset classes such as A-REITs over the course of 2018.

Another factor is simple supply and demand. The table below highlights just how little fresh or new equity has been raised this year. Low capital raisings translates into good demand for existing assets.

A-REIT capital raisings

Q. It was a big year for property portfolio M&A activity. Where was the appetite and what was the impact?

A. We’ve seen significant corporate merger and acquisition activity in A-REITs this year, much of it acting as equity withdrawals. Notable takeovers included Investa Office, Gateway Lifestyle, Propertylink and the gargantuan takeover of Westfield – the largest takeover in Australian corporate history. Looking forward to next year there is likely to be further activity in the market.

The direct commercial property market was strong in 2018. Bidding activity for Investa Office (two direct investors competing to buy a $4b premium office portfolio) highlights strong demand for office assets. Equally, investors are keen to buy logistics and industrial assets. In 2018 we saw competing bids for Propertylink, an industrial A-REIT, while Goodman Group, a global logistics owner, was the best performing A-REIT over calendar 2018. The rising asset values in the office and logistics sectors helped to underpin returns for A-REIT investors.

Looking ahead, a delicate balance of the above forces should help underpin the sector’s outlook for 2019.

Emerging Market Equities

2018 has been a difficult year for emerging markets (EM), as a challenging global environment has coincided with some country-specific challenges to see weakness in both equities and currencies. James Syme, Portfolio Manager of the Pendal Global Emerging Markets Opportunities Fund recently visited Australia to provide some perspective on developments this year.

Q. After a tumultuous year for the asset class, what can we expect to see in 2019?

A. The external environment is likely to remain difficult, but one legacy of 2018 has been the extremely attractive valuations appearing in parts of the EM equities universe, particularly within those countries reliant on domestic demand. The MSCI Emerging Markets Index is cheap relative to its history, despite the rise of the (comparatively expensive) internet sector in the index. Many parts of the asset class now trade at single-digit forward price/earnings ratios. We believe there is substantial opportunity in the asset class, but there will need to be an improvement in the external environment before that opportunity can be realised. Overall, we are very positive on the outlook for emerging market equities in 2019. We feel the current negativity towards the asset class is unwarranted, although gains may be loaded into the back-end of the year.

Read more of James’s 2018 review of emerging markets

Multi Asset

Considering all the challenges in 2018 we asked Michael Blayney, Pendal’s Head of Multi Asset, to makes some observations with a longer term context.

Q. How have the dislocations in markets this year affected your return expectations for diversified funds?

A. Rather than dislocations, we see the market gyrations this year as more of a return to normal conditions after nearly a decade of artificially low volatility. It is our view that central bank support for markets since the GFC has led to unusually-low realised volatility since the start of Quantitative Easing in 2009. As central banks reverse this policy, we see the potential for markets to return to their core function of price discovery in order to facilitate the efficient allocation of capital. This is a good thing.

Our assumptions have changed somewhat in response to recent market declines: for Australian equities our long-term return forecast has increased to 8.75% pa, up from 8.25% a year ago. Interestingly, market moves of around 10% that we’ve seen this year don’t change the long-term expected return by as much as might be expected. Let’s say your investment horizon is 10 years and your expected return for a given investment over that time is 8% pa. If the market price of that investment falls by 10% then your expected return rises to only 9.1%, all other things being equal. If your investment horizon is 30 years then the expected return increases to only 8.4%. Hence, moves of the magnitude we’re seeing are more noise than a valuable signal in the context of long-term wealth creation. Of greater importance is to ensure that you’re invested in the right asset mix and risk profile so that you can both handle inevitable declines in market prices as well as growing an adequate nest egg over the long-run.

What the current situation (ie more extreme market movements combined with a move towards markets functioning more normally after a decade of central bank intervention) provides is the potential to increase returns via active management. To provide an example, during November our dynamic asset allocation (DAA) process identified US large-cap equities as being sufficiently expensive to warrant an underweight over the medium-term (1-5 years) while Korean equities are cheap enough to justify an overweight over a similar investment horizon. The respective entry points for these portfolio tilts create an attractively-skewed distribution of future returns, giving the high probability of adding value. US equities have subsequently fallen further than Korean equities, thereby generating a positive active return for investors in a number of Pendal’s actively managed multi asset products. We view several other equity markets in Asia as being modestly cheap, but not yet cheap enough that the probabilities are sufficiently compelling.

Q. The average super fund has delivered annual returns of 7-8%pa over the past few years. Are these returns achievable in the current environment?

A. I would expect passively managed balanced funds to struggle to meet these return targets. The reasons here are fairly intuitive. Consider the forecast return for the strategic asset allocation (SAA) of the Pendal Active Balanced Fund which is around 6.5% (comprised essentially of CPI+4 to 4.5%), with the balance of the return contribution sourced from active management and risk reduction. Through this approach, total gross returns of 7-8% are theoretically achievable. For the average passive balanced fund which is essentially premised on no contribution from actively selecting investments and managing risks, the likely returns would be closer to the 6 to 6.5% mark, before fees.

For further insights from Pendal’s portfolio managers please visit the education & resources section of our website.

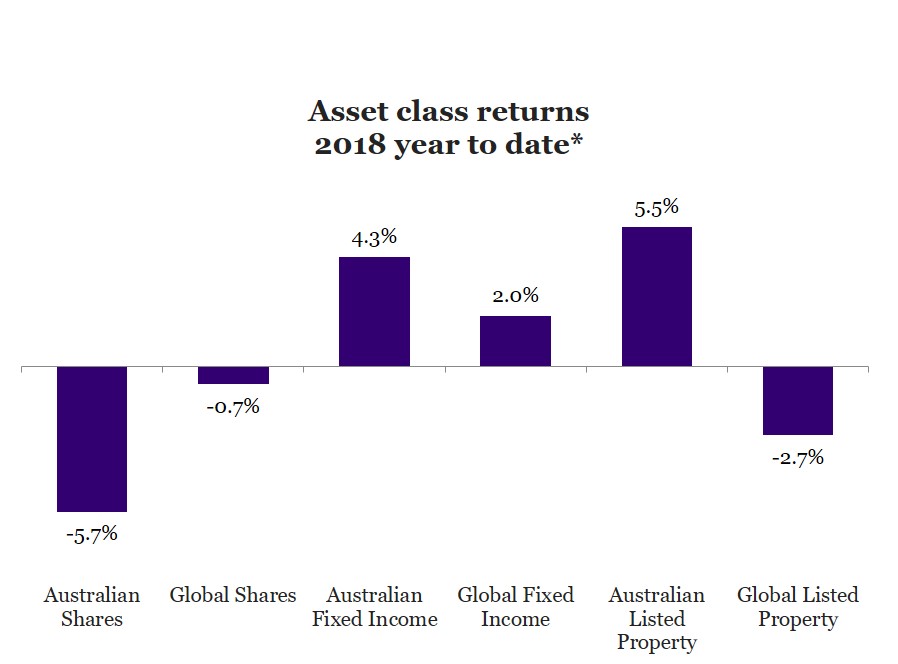

* Asset class returns are based on appropriate index returns for the calendar year to 20 December 2018. Australian shares: S&P/ASX 300 Accumulation index; Global shares: MSCI World ex Australia Total Return (AUD) index; Australian fixed income: Bloomberg AusBond Composite (0+yr) index; Global fixed income: JP Morgan GBI Global Traded A$ Hedged index; Australian Listed Property: S&P/ASX 200 A-REIT Accumulation Index; Global Listed Property: FTSE EPRA/NAREIT Developed ex Australia (A$ hedged) Total Return Index.

Fund Manager commentary for the month ended 30 November 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.