12/12/2018

Transactional and operational costs update

Pendal Active Growth Fund (APIR code: BTA0125AU)

Please note the estimated total transactional and operational costs for the year ending 30 June 2018 is 0.56%. Of this amount, we estimate 0.36% was recouped via the buy-sell spread and 0.20% reduced the return of the Fund.

These costs have been updated in the current PDS (dated 12 December 2018).

12/12/2018

Transactional and operational costs update

Pendal Asian Share Fund (APIR code: BTA0054AU)

Please note the estimated total transactional and operational costs for the year ending 30 June 2018 is 0.31%. Of this amount, we estimate 0.06% was recouped via the buy-sell spread and 0.25% reduced the return of the Fund.

These costs have been updated in the current PDS (dated 12 December 2018).

12/12/2018

Transactional and operational costs update

Pendal European Share Fund (APIR code: BTA0124AU)

Please note the estimated total transactional and operational costs for the year ending 30 June 2018 is 0.47%. Of this amount, we estimate 0.10% was recouped via the buy-sell spread and 0.37% reduced the return of the Fund.

These costs have been updated in the current PDS (dated 12 December 2018).

2018 has been a difficult year for the emerging equity asset class, as a challenging global environment has coincided with some country-specific challenges to see weakness in both equities and currencies. Chief among the global challenges has been the tightness in US dollar liquidity, higher US interest rates and a rising US dollar. These have all stemmed from two drivers: the US Federal Reserve’s reduction in the size of its balance sheet by rolling over fewer of its holdings of US Treasuries, and a substantial upturn in US Treasury issuance to pay for the Trump administration’s tax cuts. The effect of this on those emerging markets (EM) with current account deficits (ie those that depend on capital inflows to fund their growth) has been dramatic, with the equity markets in those countries generally underperforming, and those with the largest current account deficits (Turkey, Argentina and Pakistan) all seeing sell-offs that in another era might have been termed crises.

Other stresses on the asset class have included the ongoing slowdown in China as the economy there reacts to the substantial tightening of monetary policy that has accompanied the crackdown on shadow banking since 2017. Throughout the year steady evidence has emerged in both economic data and corporate results of reduced consumption and investment in China as a much slower rate of credit growth comes through. As well as seeing weakness in Chinese equities, other emerging markets with significant exposure to China have struggled. This weakness has been exacerbated by ongoing concerns about the outlook for global trade, with the tariffs and restrictions on US-China trade the focus.

Finally, 2018 saw a very busy political calendar in emerging markets, with elections in Brazil, Colombia, Mexico, Russia, Malaysia, Pakistan, Egypt, the Czech Republic and Poland, as well as unexpected changes in leadership in Peru and South Africa. Many of these saw volatility in financial markets during or after the electoral process.

So, with 2018 now drawing to a close, what can we expect for next year?

The external environment remains difficult at the time of writing, but one legacy of 2018 has been the extremely attractive valuations appearing in parts of the asset class, particularly in some parts of the asset class exposed to EM domestic demand. The MSCI Emerging Markets Index is about one standard deviation cheap relative to its history, despite the rise of the (comparatively expensive) internet sector in the index. Many parts of the asset class now trade at single-digit forward price/earnings ratios. We believe there is substantial opportunity in the asset class, but that this will need an improvement in the external environment before that opportunity can be realised.

“We believe there is substantial opportunity in the asset class, but that this will need an improvement in the external environment before that opportunity can be realised.” James Syme, Senior Portfolio Manager, JOHCM

The catalyst, we feel, will be the feedback of weak EM economic conditions back into the developed world (particularly the US), causing central banks there (again, particularly the Federal Reserve) to pause the monetary tightening process, allowing EM equity markets to rally, potentially quite powerfully. According to the IMF, emerging market and developing economies (including South Korea, Taiwan, Greece and the Czech Republic) represent 42.8% of global GDP, and weakness here will affect demand for US goods and services, ultimately influencing US monetary policy. A recovery in China would be an additional support, but we are less convinced that China will revert to credit-led growth in 2019. Finally, the political calendar looks far more benign in 2019, with Argentina, India, Indonesia, South Africa and Greece the key elections to look out for, although the effects of 2018’s elections must also be watched, notably in Brazil and Mexico.

Overall, we are very positive on the outlook for emerging market equities in 2019, as we feel the current negativity towards the asset class (as expressed through valuations) is unwarranted, but we feel the gains may be loaded into the back-end of the year.

Read more

Be a part of the world’s fastest growing economies

Pendal Global Emerging Markets Opportunities Fund

Key highlights

• Global Industrials have provided great investment opportunities in recent years, fuelled by buoyant market conditions and valuation support through the ultra-low interest rate environment

• Picking the right industrial companies at appropriate valuations has been challenging but rewarding.

• New technologies further up the production line are driving a resurgence in the Industrial Robotics segment, prompting us to consider if the time is right for investment.

The global Industrials sector provides a highly diverse and fertile ground for selecting companies to invest. This segment features companies across a range of disciplines, ranging from manufacturers of capital goods such as aerospace, heavy machinery and building products through to human services, research and facilities management, and extending to transportation companies in rail, road and airline industries. It is common to see disparities in valuations within the sector through time as markets tend to follow short term trends in narrow segments. As such, we have seen significant performance dispersion across Industrials over recent years. Since the launch of our Concentrated Global Share Fund, returns from the 292 names in the Industrials sector have ranged from +57% (Boeing) to -56% (Capita Plc). Consistent with our discipline towards only buying industry leaders trading below their intrinsic value, we have only invested in seven industrial companies. Two of these investments – Boeing (+57% local currency return) and CSX Corporation (+50.0%, also in local terms) – have been the highest performers within the sector.

While it is disappointing to not have held a few more Industrials amid the sector’s overall strong performance, spectating the rally from the sidelines did reveal a number of gems to consider when sentiment turns and valuations come back to more sensible levels. One such area we have been looking at with deepening interest is robotics/factory automation companies, many of which have experienced de-ratings in excess of 50% in 2018.

So why the interest in Robotics/Factory Automation amidst a sea of red?

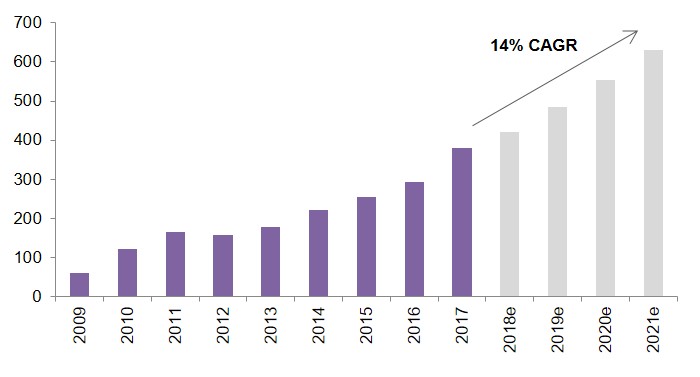

The robotics/factory automation space is highly investable, with the annual demand for industrial robots forecast to grow by 14% pa, according to the International Federation of Robotics. This growth is being driven by the rising cost of labour, which has improved the payback period on investments in robotics from five to less than two years. Growth is also being promoted by new industrial applications as well as significant subsidies from various levels of China’s Government. Growth aside, the industry also features a number of companies that hold dominant market share (>50%) and a track-record of sustaining extraordinary margins. These companies are well placed with scale and earnings leverage to invest further in automation.

Forecast annual worldwide supply of industrial robots

Source: International Federation of Robotics

These attractive characteristics coupled with the sector’s valuation de-rating since the start of the year led us to undertake significant research into the sector, which included visiting companies located in Japan, China and the US.

Robotics / factory automation related company meetings – 2018

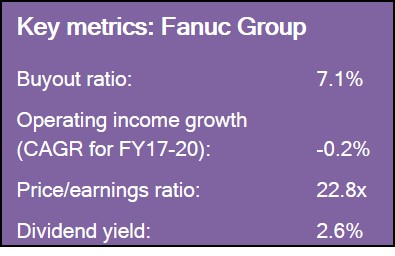

Our meetings revealed very little to dispel our positive impression of the sector and confirmed much of the de-rating has been due to transient concerns over the automotive and semi-conductor capital investment cycle, together with slowing activity due to uncertainties over cross-border trade policies. That said, there was some concern over supply/competition dynamics as new companies emerge in China which can be expected to aggressively roll-out capacity. They seek to offer competitive technology priced around 30% cheaper than the incumbents along with attractive ‘pay when satisfied’ trading terms. The logical conclusion here is profitability for the incumbents is at risk. However, history tells us this isn’t necessarily the case. One such incumbent is Fanuc, a Japan-based global manufacturer of factory automation technologies, which presents an interesting case study in the face of emerging competition.

Fanuc – maintaining a competitive advantage

Fanuc holds a somewhat mystical status amongst investors due to its secretive nature, its charming obsession with the colour yellow and the location of its headquarters in the idyllic forests at the base of Mt Fuji in Japan. These are characteristics many associate with a religious cult rather than a leading industrial company with over 60 years’ experience and renowned for the big yellow robots found in the world’s most advanced car manufacturing facilities. However, the company’s roots are actually not in robots but the somewhat less glamorous field of computer numeric control (CNC) systems (i.e. computers and motors that control machining tools). Fanuc holds a 50% market share globally (70% in Japan) in CNC systems and is a key driver of its 30-40% earnings (EBIT) margins.

Fanuc CNC System |

Fanuc Industrial Robots |

|

|

Like any other company with a dominant position, Fanuc has met its fair share of challenges. In the 1980s its share in Japan fell to a low of 50% compared to a peak of 80% during the 1970s. Technology played a part in Fanuc’s decline in the 1970s, with the company’s electro-hydraulic stepping motor technology superseded by the faster and operationally simpler DC Servo Motor. Fanuc pulled out all stops to not only catch up but exceed its competition through technology partnerships and aggressive technology implementation, guided by feedback from its customer service network.

The technology threat of the 1970s was followed by a competitive threat with the major machine tool makers boycotting Fanuc for its refusal to allow them to customise the numeric control module. Products from Yaskawa and Mitsubishi were introduced but were eventually marginalised due to end-user preference for Fanuc’s superior aftermarket support.

In both instances, it was Fanuc’s extensive service network that helped protect the company’s market position. This service network goes far beyond being a piece of infrastructure to keep customer equipment in working order; it also serves as a sounding board to help capture customer feedback and direct product development. The network is as valuable today as it was in the 1970s and 1980s as Fanuc face-off against a new generation of competitors and undertakes a sizeable research and development program, amounting to 7% of its sales revenue.

Keeping a close eye on the robots

The robotics/factory automation sector is home to a number of companies that harbour significant competitive advantages which facilitate a profitable ride on the industrial automation tailwinds. That said, we don’t currently hold positions in the afore-mentioned names on valuation grounds. Despite the significant valuation de-rating, companies in the robotics/factory automation space remain expensive, offering less than an 8% buy-out yield based on mid-cycle earnings which offers limited upside. A clear valuation discipline within our process is to buy companies with an 8-15% buy-out yield.

The robotics/factory automation sector is home to a number of companies that harbour significant competitive advantages which facilitate a profitable ride on the industrial automation tailwinds. That said, we don’t currently hold positions in the afore-mentioned names on valuation grounds. Despite the significant valuation de-rating, companies in the robotics/factory automation space remain expensive, offering less than an 8% buy-out yield based on mid-cycle earnings which offers limited upside. A clear valuation discipline within our process is to buy companies with an 8-15% buy-out yield.

By way of comparison, the Fund holds investments in other major industrials such as Boeing, Analog Devices Inc. and Texas Instruments. These companies are industry leaders with less competitive threats. We purchased these names when they were comfortably within our target valuation range and have since performed well. The industrial robotics sector has very real prospects and we are maintaining a watching brief until we see an entry point where the risk/reward balance is more favourable. As investors we are spoilt for choice with 200-plus industrial companies to buy, should Fanuc and its peers fail to meet our hurdles.

Click here to find out more about the Pendal Concentrated Global Share Fund.

“Emerging markets remain in a much better position…but it is important to monitor where value is developing”

James Syme, Senior Portfolio Manager, Pendal Global Emerging Markets Opportunities Fund

A number of emerging markets have felt the impacts of a strong US dollar, volatility in the oil price and a tightening of the reins on US trade policy so far in 2018, resulting in varied performance across different countries.

In this quarterly update, Senior Portfolio Manager James Syme:

– explains the role of major policy decisions in driving performance dispersion across emerging markets

– highlights the key markets which are in fundamentally better shape; and

– sets out the team’s rationale for key country-level overweight and underweight positions

Further reading:

Be a part of the world’s fastest growing economies

Fund Manager commentary for the month ended 31 October 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Settle down, calm down — a change is taking place in the country

Mexican President-elect Andres Manuel Lopez Obrador, 30 October 2018

The global environment continues to pose challenges for emerging markets, with tight US dollar liquidity, a slowdown in China and stresses about the global trade system all acting as headwinds. However, emerging markets will continue to also be driven by country-specific factors, very much including changes in the outlook for politics and governance, and this has very much been the case in both Brazil and Mexico in the last few weeks.

In Brazil…

In Brazil, the political order has been shaken by the election as president of the right-wing populist Jair Bolsanaro, who stood on a platform of generally liberal economic policies and illiberal social policies. His economic policy ambitions include proposals to reduce both state spending and state intervention in the economy, although he has sent mixed messages regarding the privatisation of large state-owned companies such as oil producer Petrobras and electricity utility Eletrobras. The prospect of the adoption of these policies has been well-received by financial markets.

Brazilian President-elect Jair Bolsonaro

As followers of our views will be aware, though, we believe that the critical policy measure for Brazil is pension reform. It is generally accepted that Brazil needs to run a primary fiscal surplus (ie before paying interest on government debt) to achieve economic stability. Brazil has been running a primary deficit since 2014, largely because of uncontrolled growth in social security expenses, the majority of which is related to pensions. As an example, 10 years ago, in September 2008, the Brazilian federal government had revenues of BRL 50.7bn, expenses of BRL 44.6bn (of which BRL 20.9bn were for social security), a primary surplus of BRL 6.1bn and interest costs of BRL 4.1bn. Ten years later, revenues have grown to BRL 96.7bn, but expenses to BRL 119.6bn, with BRL 61.5bn of that being social security costs, leaving a primary deficit of BRL 22.9bn before interest costs estimated at BRL 49.2bn. We believe that for Brazil to avoid a fully-fledged sovereign debt crisis, the social security system must be reformed within the next few years.

“We remain in a wait-and-see mode on Brazil, with the portfolio holding a small underweight position relative to benchmark.”

James Syme, Senior Portfolio Manager JOHCM

To do this, President-elect Bolsonaro must get a reform bill approved by a three-fifths super majority twice in each of the chambers of Congress. In the lower house, that requires at least 308 votes of the 513 members. While more right-wing parties did well in the Congressional election, it will be very difficult to pass pension reforms, particularly if illiberal social policies alienate more centrist politicians. We remain in a wait-and-see mode on Brazil, with the portfolio holding a small underweight position relative to benchmark.

Mexico, meanwhile…

Mexico, meanwhile, has seen financial markets react negatively to one of the first major policy steps of President-elect Andres Manuel Lopez Obrador (known as AMLO), which will be to cancel the controversial new airport for Mexico City. The decision, legitimised by a chaotic referendum, has been taken particularly badly by bond markets (where US$6bn of airport bonds are now at risk), with a concurrent sell-off in equity markets. Investors are particularly concerned that the AMLO administration will continue to enact populist policies via direct democracy.

Returning to the global environment, though, we continue to find a lot to like about Mexico. Mexico exports US$300bn of goods and services to the US, 81% of its total exports, and is also a beneficiary of the strong US economy through remittances (about US$28 billion in 2017, the vast majority of which came from the US). The renegotiation of NAFTA removes key risks to the Mexican economy, while Mexico is among the few emerging markets to be a net oil exporter. As with Brazil, we remain in wait-and-see mode, with a broadly neutral position relative to the benchmark, but do wonder if Mexico will prove the better medium-term investment.

Read more

Be a part of the world’s fastest growing economies

The script gaining popularity this year is that Australia’s housing bust is finally coming. From 2013 to 2017 foreign buyers and local investors pushed up prices to levels that were unaffordable for local owner occupiers but very profitable for developers, spurring on supply which only now is hitting the market. Government policy meanwhile has put the screws on foreigners and investors, meaning there is a long way to fall before new buyers step up. A Labor government potentially banning negative gearing outside of new developments suggests further downward price pressure.

This script has a lot going for it, but many people have been calling the death of Australian property since 2009.

In our six page Australian Housing Review, Pendal Portfolio Manager Tim Hext takes a dispassionate look at the underlying data and potential tax changes to draw conclusions on the prospects for residential property prices.

Read our Australian Housing Review

If my daughter wins a hundred-metre dash by hiding the other kids’ runners whilst giving herself a pair of jet-powered wheelies, I’d credit her cunning and ingenuity, but I’d hardly applaud her sprinting skills.

That kind of winning also describes what’s currently fuelling the narrative of US “exceptionalism”. By itself, the fiscal stimulus that the US has been enjoying since the end of last year doesn’t make a whole lot of sense.

Not only has it been a pro-cyclical use of fiscal policy, but outside times of war and recession, this is the largest stimulus the country has seen in its economic history.

But as Donald Trump turns up the heat on Sino-US trade relations and China scrambles for ways to offset the effects, it becomes apparent that this Republican fiscal reform was designed to build a fortress around US growth, from which an attack could be launched. This was cunning, and may eventually prove ingenious.

China’s biggest miscalculation was to underestimate Trump. Through waging an ideological war against China via the proxy of trade imbalances, he saw clearer than anyone the path along which this war would unfold, and the inevitable casualties that the US would also have to suffer along the way.

With third-quarter earnings season under way, the impact of US trade tariffs on Chinese goods are already being felt across American industries, from automakers to farmers, from Fortune 500 companies to “mom and pop” shops.

Ironically, as the tariffs currently stand, finished goods imported from China that have not yet been touched by US tariffs may enjoy an advantage over US-made goods with Chinese components. The inevitable conclusion there, would be to ensure tariffs expand to cover all Chinese imports to the US.

Knowing the pain that would accompany the process of on-shoring production back to the US, Trump effectively delivered a pre-emptive “whatever it takes” fiscal package.

Tax cuts ensure that corporate profitability is bolstered ahead of a likely period of margin erosion. Corporate repatriations ensure that liquidity conditions stay protected in the US whilst the rest of the world feels the drain. And stimulating the economy past full employment should put even more money into the pockets of the average American.

China’s changing approach

Trump certainly wasn’t kidding when he said “America first”.

As the path has become clearer, the focus has to now shift back to China’s reaction function. The tit-for-tat strategy engaged by China this year is no longer deemed to be appropriate now that the full extent of the threat has been recognised.

Rather than provoking more attacks by Trump, attention is now centred on boosting domestic demand. China’s tolerance for hard landings remains limited, less so due to a desire to save face, but more for reasons tied to the root of its ideological difference with the US.

Socialism under a one-party system needs buy-in from its people. China’s Communist Party may exert an authoritarian grip over the nation, but this can also be undermined by falling living standards and growing unemployment rates. Especially for a nation addicted to a near-doubling of per capita GDP every decade since the late 1970s.

In sharp contrast to last year’s resilience, trade wars have barely scratched the surface and yet the world’s second-largest economy is showing signs of greater damage.

The contraction in shadow banking that was kick-started by the deleveraging campaign has gathered internal momentum. Corporate defaults are piling up, both onshore and offshore, and that’s not even counting the ones saved or postponed by takeovers by state-owned companies.

Local governments are being asked to spend again, but until now have been fearful of the conflicting deleveraging agenda pushed by Xi Jinping. The fiscal lever is being pulled, but the transmission mechanism seems busted. Against this backdrop, the certainty of trade war escalation makes Chinese leadership all the more determined to underwrite economic growth.

‘Whatever it takes’

It is meaningful that in a letter to private entrepreneurs this month, Xi vowed his “unwavering support” for the country’s private sector. Such support will come in the form of tax cuts, liquidity back-stops, bond raises and likely even stock market support (a method of intervention that met with much controversy in 2015-16).

At the same time, private enterprises are being urged to focus on innovation. Sounds like a leaf from the Republican tax plan, taken one (or 10) steps further. Sounds like “whatever it takes” with Chinese characteristics.

Unfortunately, the results thus far have been disappointing. Economic activity continues to slide, led by the old economy. Given China’s importance in providing a safety harness for major parts of the global economy at every key juncture over the past decade, many still await the reflationary pulse to be delivered by China’s stimulus measures.

This is the biggest miscalculation the world can make about China. Just as US stimulus is more self-contained, it would be wrong to expect that China’s can save one and all.

Not only would broad-based Chinese stimulus undo much of the hard work of the past two years, it would also stall the growth engine of China’s new economy. It is no coincidence, for example, that consumers have remained resilient, and industrial upgrading continues to bolster the manufacturing sectors.

Through the US initiation of deglobalisation, a number of tough choices now lie ahead. China must choose quickly and strategically those allies most needed for her future. Luckily for Australia, China still needs to build more railways and to seek out high-quality education for its students.

For now, China also needs high-end imports from Japan, South Korea and Europe. Unfortunately Australia and much of Asia will all be forced to pick a side somewhere down the line.

If China’s Made in China 2025 plans are successful, high-end imports will eventually be displaced by domestically produced Chinese goods. Just because they’ve stopped bragging about it doesn’t mean they’ve abandoned this strategy.

Quite the opposite.

This article was first published by the Australian Financial Review on 29 October 2018