“We haven’t seen a trade war hit emerging markets. If it does I think it will be quite specific in terms of where it hits.”

James Syme, Senior Portfolio Manager, Pendal Global Emerging Markets Opportunities Fund

Investor caution towards emerging markets has increased this year as a strengthening USD creates real challenges for a number of EM countries. This caution has accelerated more recently with trade war rumblings and Turkey’s economic flashpoint.

In this quarterly update, Senior Portfolio Manager James Syme:

– explains, using Russia, Brazil and Turkey as live examples, why active top down country selection is so important in EM

– sets out the team’s rationale for key country-level overweight and underweight positions

– discusses the role the USD and oil prices will play in driving EM performance dispersion.

Further reading:

Be a part of the world’s fastest growing economies

Fund Manager commentary for the month ended 31 August 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

You’d be surprised how easy it is to take for granted the state of the world that you know.

You thought everything was fine, but then the GFC happened. Luckily, central banks covered up the mess with a put and plenty of liquidity.

You believed in the status quo, and then Brexit happens. Populism and nationalism have been ‘on trend’ ever since.

You never questioned the idea that global free trade is good, yet Donald Trump has started a trade war. He might just put the nail into the WTO coffin whilst he’s at it. Seismic shifts are happening right beneath our feet. Globalisation, it seems, can go no further in its current form.

Through all of this and more, China has remained the one constant. For all the talk of reform and economic transition, the recent shift towards domestic easing policies highlight that the old economic model remains dominant. This model has relied on a largely closed-economy system, with a currency that has been artificially kept weak over the last 30 years to support a flourishing manufacturing exports sector.

Cross-border capital flows have not been permitted, thus allowing the Chinese authorities fuller control over the financial system. This control has directed cheap credit to various industries from steel and cement to solar and high-speed rail. Debt-fuelled fiscal stimulus has been used to support growth at every turn.

What’s more, this model exists under a one-party socialist government. We in the West tend to view planned economies with disdain. There is a certain arrogance about governments who believe they can do a better job of allocating resources than the pure signal of market prices. The bad-debt problems now sitting with a swathe of zombie state-owned enterprises (SOEs) in China is case in point.

However, survival of the Chinese Communist Party and the political order that goes with it depends on continued economic progress, and its ability to carry the entire population along. This is a key point of difference between China and other socialist regimes such as Venezuela that have ended in suffering and demise.

Over the last 30 years, through its own poverty alleviation efforts, China has contributed as much as 70 per cent to global poverty reduction. Socialism with Chinese characteristics seems to offer a template for pragmatic implementation of the socialist agenda.

Since World War II, the US has tried to spread the liberal world order across the globe. By inviting China into the WTO, it was hoped that this spread could continue. Instead, whilst Chinese exports have hugely benefited from WTO membership, its industrial and political practices have moved even further away from liberal Western ideals.

The allure of the sheer size of the Chinese market has forced foreign firms to surrender their intellectual property. In return, they get to sell to and operate in China. Under the cover of subsidised cheap debt and de-facto protectionist policies that have limited the force of international competition on Chinese firms, ‘indigenous’ national champions have risen in various sectors across the Chinese economy (alongside many zombie companies to boot).

And if it can have its way, these continued practices to circumvent the spirit of international trade law would enable the success of its Made in China 2025 plan.

But the US has put its foot down. Among other things, Trump is viewed as the disruptor of global free trade. Tariffs and tweets are like hand grenades to him, thrown around to shake up the status quo, irrespective of how and where they land. Whilst his weapons are blunt, his motivations are widely echoed across party lines.

From China’s perspective, its industrial policies have been smart, but the US thinks they have been cheating. And if China’s rapid rise in the global pecking order is down to this type of behaviour, then Trump wants to fight fire with fire.

Theoretically, there is a high road that he could take, by engaging in the rule of law and soliciting support from its traditional allies. However, knowing that the law could never deliver any necessary punch, there really was no alternative for him than to get down and dirty with the same tactics as he’s witnessed from China.

If China’s $US3 trillion foreign reserve position is a symptom of unfair currency manipulation over the last two decades, then the least that Trump could do is talk down the US dollar. If China has been surreptitiously breaking WTO rules, then Trump will turn his back on the institution entirely. And if China has used fiscal stimulus funded by a ballooning debt stock to prop up growth and various industries, then Trump will unleash the largest fiscal package ever to be witnessed outside of times of war or recession.

Is this progress? It’s hard to recognise it as such when it spells the end of globalisation as we know it. Is this creative destruction? We will only know if these protectionist policies lead to a sustainable pick up in US industrial productivity – a tall order given that this declining trend has been impossible to turn for over a decade.

This article was first published by the Australian Financial Review on 26th August 2018.

Fund Manager commentary for the month ended 31 July 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Resilience: The ability to bounce or spring back into shape and position

There is always a debate in markets about what is the right price to pay for a good quality business. During this market cycle, since the 2008 lows in equity markets, businesses with growth characteristics have been rewarded with even richer multiples. Over the past nine years, with few exceptions, value as a style has remained unloved. On occasions, we did witness the value style outperforming growth (especially in times of macroeconomic stress or industry-specific worries), but that outperformance proved ephemeral. Despite an environment of reducing liquidity (central banks moderating QE) and rising interest rates, we have, so far, not seen any marked de-rating in valuation multiples for growth businesses. It is also a fair comment that in every market fewer businesses have delivered sustained growth in the face of several challenges, or are perceived to be in a position to do so.

Resilience matters

In the past few months, as I rejigged our portfolio, one big challenge I have grappled with is the high multiples for good quality businesses. Do I just buy stocks which appear to be squarely in the momentum trade, for whom valuation multiples already trade at significant premiums to the market? What if I misjudge the growth trajectory or the risks of industry disruption, currency volatility or a slowdown in the economy? In addressing those questions, the one metric I decided to re-emphasise was resilience. Every business invariably goes through challenging times. When it does, it is either the inherent resilience of the business, or the ability of management teams to deal with and engineer the requisite change, that differentiates it from more pedestrian businesses.

The unwelcome Maggi gift

One such resilient business I have added to our portfolio is Nestlé India (NI). A subsidiary of the Swiss multi-national, NI has operated in India for over a century and built upon its iconic brands in milk, nutrition, beverages, prepared dishes, chocolates and confectionery.

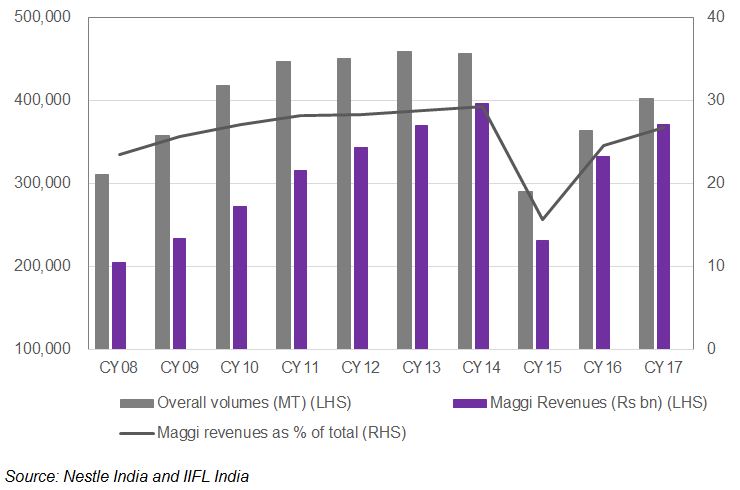

One of NI’s biggest sub-brands by far was and is Maggi Two-Minute Noodles. Between 2009 and 2014, NI aggressively expanded its factories to take advantage of potential growth in India. Yet, under the direction of its parent, NI shifted strategy to focus on improving margins at the expense of volume growth. It cut back on low-priced, lower margin products. That strategy may be appropriate in developed markets, but in a poor/emerging country like India, it made little sense, in my view, for NI to focus purely on enhancing margin at the expense of market share, growing the market and innovation. To an extent, that misstep by management led to lacklustre revenue growth in the past.

To add to this, in June 2015, one of the regulators in India banned NI from selling Maggi noodles due to food safety concerns. The food safety commissioner of Uttar Pradesh, the most populous state in India, claimed that a package of noodles contained seven times the permissible level of lead. Despite the fact that NI was convinced about its safety and quality record, NI decided to recall the product. All associated products, like Maggi jams, ketchups and beverages, were also badly affected, as consumers were naturally cautious. From a dominant 60-65% market share in noodles, NI’s market share almost halved overnight.

Nestle and Maggi Volumes

A fresh approach

But the brand was and remains iconic and NI had a lot at stake. Tackling the problem head on, NI appointed a new CEO, an old India hand. Under his direction, the management team and the company addressed the safety issue as a priority to regain trust. Simultaneously, it changed course and enhanced its innovation capabilities. In the subsequent couple of years, 42 new products were introduced. NI’s strategy turned 180 degrees, away from higher margins to growing volumes and market share with the help of innovation.

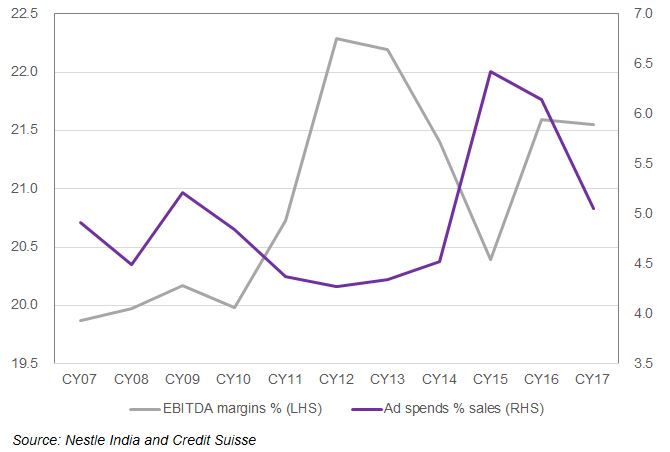

This new approach manifested itself in increased advertising and sale promotion spend. Just to put it in perspective, Nestlé globally has close to 2,000 brands; in India, it had just 20. India represents just 2% of global sales for Nestlé but has always remained a country that has great promise. There is an increased recognition by its parent that India needs to be run to meet the aspirations of Indian consumers; the local management team has been given the freedom to do so. Fortune favours the brave. This time around, NI has some tailwinds to aid what now seems to be a path towards sustained and highly profitable growth over the next few years.

Nestle India – EBITDA margins and ad spend

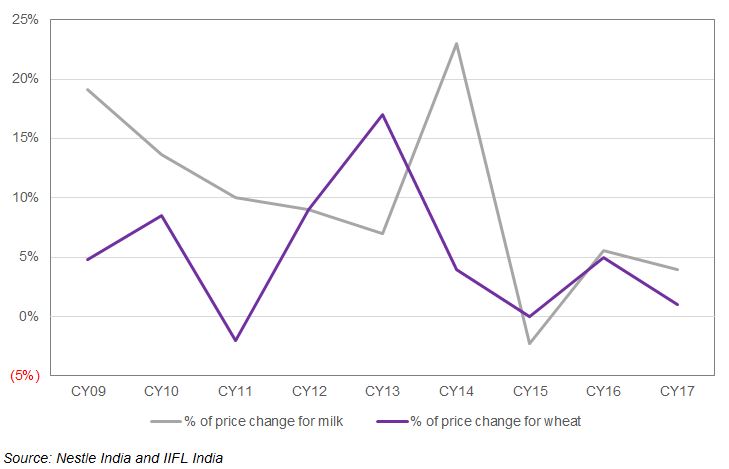

Commodity prices, particularly the ones most relevant to NI such as milk and wheat, have eased across the globe. This enables NI to take the higher costs from oil-related packaging products in its stride without feeling any pressure on margins. There is evidence of a recovery in consumer demand after two years of disruption post demonetisation and introduction of a Goods and Services Tax (GST). This nascent recovery could sustain as India heads into a general election, scheduled by May 2019 at the latest.

Milk and wheat price change

As is typical of governments when they approach elections, Prime Minister Modi’s administration has started to loosen the purse strings and hand out largesse to rural voters to appease them. As the rural economy starts to see better income growth, I do think NI will keep innovating and introduce more brands from the parent into the Indian market.

A rich valuation but consider the growth prospects

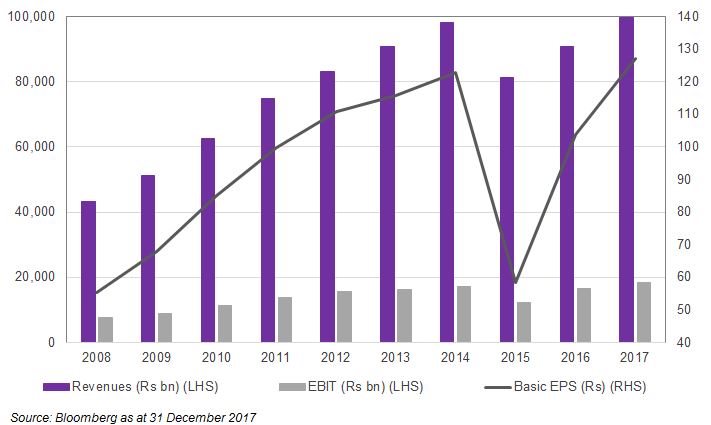

This leaves us with the question of NI’s valuation: the stock trades on a 50-52x multiple for 2019 earnings. For some, that’s a nosebleed-inducing valuation. On the face of it, that multiple does look rich. Yet I would suggest we put in perspective, looking at financials from 2013 onwards. In the past four years, NI’s revenues, earnings and earnings per share have barely budged.

Revenues, EBIT and EPS have flat-lined

There were genuine reasons for a below par performance. However, in my view, we are on the cusp of change. If the company does execute on its plans, it is quite feasible that in the next four years revenues and earnings double from where they were at the end of 2017. In what could be a turbulent period for macroeconomic reasons across the world, that kind of resilient sustained growth will deserve premium multiples. That’s why I am willing to take this positive view on Nestlé India.

Trade wars are front and centre for markets at the moment and no amount of ink is being spared writing about it. While many have tried to quantify the effects of trade wars on economic growth, it’s pretty much a waste of time as it is attempting to simplify the effect of a monumental change on the way that modern multinational corporates do business.

I am certain we are watching a key turning point in history unfold right in front of us. The way things have been done on the global stage over the last 40 years is changing at a lightning pace, as politics, diplomacy, immigration and trade relations are all in a state of transition. The dominant economic theory – commonly referred to as neoliberal economic theory – is no longer the playbook by which world leaders run their economies, and the new playback has many blank pages. This will have further significant effects on fiscal discipline and debt management as governments feel their way forward, obviously impacting economic growth and inflation. All of these factors will then have a subsequent effect on the role of the central bank, as the focus shifts from the independent and inflation targeting model that has been the status quo for the last 20 years. The rules of the game are changing.

View the newsletter here

The [IMF] also notes that current-account imbalances are increasingly becoming concentrated among rich nations, as surpluses shrink in China and among crude exporters.

Bloomberg, 24 July 2018

Turkish President Recep Tayyip Erdogan

Followers of our process and portfolio will be aware of the respect we have for the IMF’s annual External Sector Report, which focuses on IMF staff assessments of valuations of major exchange rates. This month saw the release of the 2018 report, which is generally positive about EMDEs (Emerging Markets and Developing Economies), identifying the major and riskiest imbalances as being the various large external surpluses (Germany, Japan, the Netherlands) and deficits (UK, US) in the developed world.

However, the report does also identify undervalued emerging market currencies. The report is focused on the end of 2017, but it is possible to adjust those valuations by year-to-date moves to arrive at current estimates of currency valuation. More interestingly, these can be combined with equity market valuations to identify areas of the emerging market universe that are cheap overall. Obviously our full country process considers many other top-down factors, including business and credit cycles, monetary policy, politics and governance, but this may point to areas of opportunity.

Firstly, we have the complicated case of Turkey. After several years of being assessed as overvalued, the IMF 2018 External Sector report sees the lira as about fairly valued as at end-2017, which means it is substantially undervalued after the fall in the exchange rate year-to-date. We estimate the lira to be 9.0% undervalued as at end-June 2018 and 14.2% undervalued as at 6 August 2018*. Meanwhile, Turkish equities are priced at 5.8x forward earnings. The IMF sees Turkey as needing to “adopt a credible policy package involving growth-friendly fiscal consolidation” as well as reining in easy credit, and there is no doubt that the implementation of orthodox policies in Turkey would produce a very powerful rally in Turkish assets. However, we can see no sign that policymakers are considering such steps, and remain negative on Turkey.

Next up is Brazil, where the IMF assessed the real as 2% undervalued at the end of 2017, and subsequent weakness suggests a current undervaluation of 3.5%, while the equity market is cheap at 10.5x forward earnings. The IMF’s view is that, in Brazil, “lower-than-desirable credit, amid weak investment, pushed up current account balances, masking underlying competitiveness problems that pushed the current account in the opposite direction.” This fits with our view, and must be taken in the context of a fiscal problem that may, or may not, be addressed at the forthcoming October 2018 election (which we see as an absolutely key driver of Brazilian markets). Indeed, the IMF report notes that “fiscal consolidation [in Brazil] should be met with reforms to boost investment.” We remain cautious on Brazil but are monitoring developments around the election.

Finally, Korea. With its large external surplus, Korea has a very different profile to most emerging markets. There are a number of drivers of Korea’s undervalued currency (4.5% as at end 2017; 4.7% at present) and persistent current account surplus identified in the report. Overall, the IMF report sees Korea as having a higher-than-desired current account surplus, with the remedies involving a stronger currency and looser fiscal policy. We believe that the policies of the more left-wing Moon administration will achieve both of these aims, resulting in stronger domestic demand growth and an upward lift to returns from a stronger currency. Meanwhile, Korean equities are priced at just 7.7x forward earnings. Korea is one of our favourite markets.

We believe that both currencies and equity valuations are critical components of assessing the investment opportunity in emerging markets but, as can be seen in these three cases, one can ignore neither the political and policy environment, nor the credit and demand cycles, in emerging markets.

* The Turkish Lira fell a further ~24% against the USD from 6 to 13 August 2018.

The 2017/18 financial year saw a return to more normalised conditions in global share markets. By ‘normal’ in this sense we refer to the levels of volatility and dispersion in stocks, sectors and countries that are historically more typical of markets. The post-GFC phase of ultra-low interest rates across the major economies came to a close and so began the process of structural adjustment from the ‘lower for longer’ disposition that has supported valuations for risk assets and kept sovereign bonds in the unloved basket.  The task ahead for investors was to position portfolios for the inevitable unwinding of policy support and accurately predict the trajectory of interest rates and inflation. History has also shown that this is an imperfect science, fraught with variability.

The task ahead for investors was to position portfolios for the inevitable unwinding of policy support and accurately predict the trajectory of interest rates and inflation. History has also shown that this is an imperfect science, fraught with variability.

Adding to the uncertain course for markets were disruptions to the political landscape. Investors were considerably influenced by Trump tweets, the emergence of populist power and trade war rhetoric as well as the more structural shifts relating to US tax policies, energy prices and household balance sheets. Developments in these areas frequently dominated the news headlines and generally left investors uneasy. But the underlying stories provided for a more sanguine assessment of capital markets and an important reminder for investors to buy the fundamental story of the asset and apply an active and focused approach to selecting investments.

Australian shares

The Australian share market certainly proved to be fertile ground for active decision makers. In aggregate, the market delivered a gain of 13.2% for the financial year, although there was considerable dispersion in the winners and losers at the stock and sector level. At the broadest level, Resources (+40.3%) considerably outpaced Industrials (+8.1%). The Materials sector (+29.9%) was a beneficiary of strengthening demand for bulk commodities such as iron ore. The Energy sector (+41.9%) was a standout performer, supported primarily by a 61% increase in the crude oil price. Such a rise proved fruitful for energy companies such as Santos (+106.9%) and Beach Petroleum (+217.1%) but acted as a tax on other companies, given the flow-on effects for input costs or consumer responses to discretionary spending.

“The spread of winners and losers over the past year reflects the multi-layered impacts of disruption, regulation and innovation. We’re likely to see these themes persist for some time, which is exactly the environment that will reward active, research-driven company selection.”

Crispin Murray

Head of Equities, Pendal Group

Big was not necessarily beautiful in 2017/18. Smaller companies (+24.4%) outperformed their large cap counterpart, in part reflective of the relatively high resources exposure. The prospect of tightening monetary conditions hampered the bond-sensitive sectors, which collectively rose by an uninspiring 0.7%.

Within the Industrials segment, Health Care (+27.7%) outperformed, although in common with the divergence in performance across the market, fortunes were mixed. At one extreme was Sirtex Medical (+97.9%) which benefitted from a bidding war for the company between US-based Varian Medical Systems and China-based alternatives fund manager, CDH Investments. In contrast, the laggards in this sector were Monash IVF (-35.6%) and Impedimed (-47.7%).

Also weighing on the industrials grouping were Telecommunication Services (-30.9%) and Financials ex-Property Trusts (+1.6%). Telstra was the major source of weakness for its sector, falling 34.4% on the back of its declining earnings growth and a cut to its dividend. Meanwhile, the major banks were dealt their fair share of challenges a Royal Commission, higher funding costs and regulatory imposts to name a few. ANZ Banking Group (+3.9%) was the pick of the big four banks, while Commonwealth Bank (-7.0%) was best avoided for banking exposure.

Listed property

The domestic listed property sector matched the performance of the broader share market in 2017/18. The sector benefitted from some supportive macro factors, primarily the pushing out of expectations for interest rate rises and a benign inflationary environment. In contrast to the dispersion theme across industry sectors, the property sectors exhibited considerably less deviation in performance. In aggregate, 33 out of the 34 A-REITs generated a positive return, with 23 of these being in excess of 10%. The big news influencing the sector was in retail land, with investors concerned about the impact of online competition. The exit of sector heavyweight, Westfield Group, following the takeover by European property giant Unibail Rodamco as part of a A$32b deal which completed at a substantial premium, saw around A$7b of cash proceeds out to find a new home. Across the sector, industrial property REIT, Property Link Group (34.4%) topped the table, while Stockland (-3.6%) dipped into negative territory.

“Fundamentals for the Australian property sector remain sound, but not uniform. We expect to see greater distinction between the quality and sub-par operators and across sectors over the year ahead as valuations are more closely scrutinised.”

Peter Davidson

Head of Listed Property, Pendal Group

Global shares

Global shares delivered a strong return for Australian investors, although a weaker Australian dollar limited the gain to 10% for investors that hedged the currency. US stocks continued to gather momentum against a favourable macroeconomic backdrop. Global markets suffered a temporary correction in February, triggered primarily by the latest US labour market data and fears of prospective inflation and uncertainties over Trump’s ‘policy on the run’ approach to resetting the global trade landscape. But where investors are concerned, America may already be great again – as indicated by the 14.4% total return from the S&P 500 Index in 2017/18.

US corporates also responded favourably to President Trump’s corporate and personal tax cuts. This, coupled with a resilient economy that now boasts annual GDP growth of 2.8%, solid jobs growth and unemployment at a 48-year low of just 3.75%, provide meaningful justification for double-digit returns from US shares. These data points supported decisions by the US Federal Reserve (Fed) to progress its monetary unwind, raising the Fed Funds rate on three occasions over the course of our financial year.

“Trump tantrums are actually helpful for us as investors. They distract those who follow the headlines and allow investors focused on fundamentals to hone in on the company narratives.”

Ashley Pittard

Head of Global Equities, Pendal Group

President Trump’s mantra on global trade led to ramifications for markets in Europe, the UK and Asia. The first in a series of tariff imposts against China came into effect in January, with ensuing measures levied on around US$50b worth of high tech and industrial imports from China. China’s own economy continued to grow, albeit at a declining rate of expansion as growth stabilised at a 6.8% annual rate. Shares listed on the mainland underperformed the Hong Kong bourse, while other emerging Asia markets were somewhat impacted by weakening sentiment from the trade rhetoric and higher oil prices. Japan continued to diverge in performance, delivering a return of 11.3%.

European markets had their own share of challenges, ranging from political destabilisation and the European Central Bank (ECB) continuing to pursue a gradual unwinding of monetary stimulus, through to consternation over the shape and form of Brexit. Returns from the region were an uninspiring 4.3%, even less for investors in the share markets of Spain and Germany.

Fixed income

It was a year of two halves for bond markets. Early in the period, further signs of growth taking hold in the major economies led to expectations of inflation returning in the near term, sending government bond yields higher. A change in the guard at the Fed was accompanied with the market’s notion that incoming Chair, Jerome Powell, would pursue an aggressive tightening agenda. This also coincided with the sell-off in equity markets and bonds also sold off, sending yields higher. The market has moderated fears since this time as the Fed progressed with its program of normalising interest rates. The European Central Bank (ECB) also progressed along a similar path of reducing stimulus, albeit at a more measured pace. In contrast, the Reserve Bank of Australia has retained its cash rate at 1.5% for a record length of time. A confluence of low wage growth, household indebtedness and benign inflation has kept the board from acting in concert with its global peers.

“The return of volatility was a significant shift in the market environment over the past year. As a defensive manager, our funds were well-positioned to benefit from the opportunities presented. We expect volatility to persist as markets continue to feel the effects of an ongoing liquidity drain and elevated political uncertainty.”

Vimal Gor

Head of Income & Fixed Interest, Pendal Group

The result was a very moderate return from fixed income. Global bonds returned 2.1%, while Australian bonds fared somewhat better with a 3.1% return. Credit spreads on Australian corporates tightened in the second half of 2017 alongside healthy risk appetite. This was driven by accommodative global central bank monetary policy settings, the much-anticipated US tax reform and better-than-expected reporting sessions out of the US and Europe. However, credit spreads subsequently reversed moves for the entire second half of 2017 in the first six months of 2018 as volatility increased on the back of fears over higher US inflation and geopolitical risks. Meanwhile, the Australian dollar weakened against the major counterparts over the year, down 3.7% against the US dollar, 5.9% against the euro and 5.2% against the British pound.

Investment implications

The normalisation process for monetary policies across the globe will erode progressively the valuation support that unilaterally low risk-free rates have provided to growth assets. This changing environment should also increase the level of dispersion in returns both within and across asset classes as focus returns to fundamental rather than market momentum drivers. That said, the speed and nature of this adjustment is uncertain and further complicated by more esoteric forces like global trade, political brinkmanship and structural changes in the shape and composition of industries.

Investors are likely to experience temporary bouts of volatility and greater dispersion between the performance of different asset classes, sectors, industries and companies over the next few years. Despite the uncertainties, this is very fertile ground for investors to take active, research based decisions on where and how to allocate capital. While some of the imbalances across markets may persist and warrant a degree of caution, we believe the greater risk would come from taking a set-and-forget approach to allocating capital.

Pendal continues to apply its multi-faceted approach to generating excess returns by looking through the headline factors that regularly skew market valuations and risks. Our focus is maintained on ensuring investments are actively managed to reflect the underlying stories that are driving risks and returns. Investors should also maintain an allocation to the Alternatives sector within a multi-asset portfolio. Through an appropriate selection of strategies, this sector offers diversification benefits with the potential to enhance returns.

Click here to download a copy of this article.

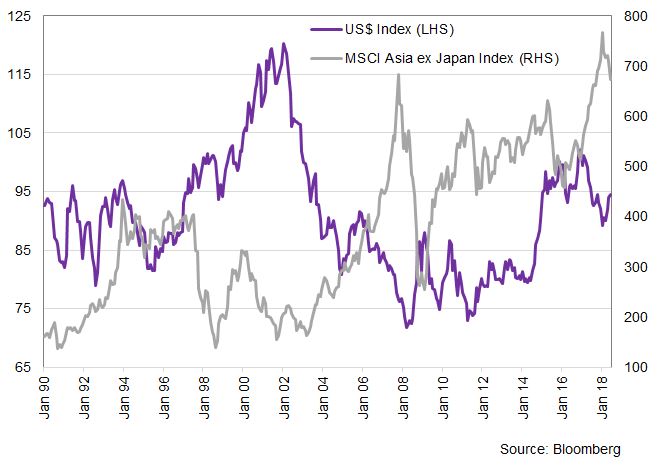

Emerging markets, including within Asia, have recently seen a torrent of selling. Several factors may have contributed to this negative turn of events: trade tensions; creeping protectionism; and political change in several countries, to name just a few. Yet a change in liquidity is, in my view, probably the main variable behind the weakness of emerging and developed Asian stock markets, and broader EM, in the first half of the year.

A lurch in liquidity

The trade-weighted US dollar index, as the simplest proxy for liquidity in all risk assets, provides a snapshot of changing conditions in financial markets. Whether in times of risk aversion or in periods of rising US interest rates, a strengthening dollar funnels liquidity away from non-US countries and assets. Apart from expectations of interest rate increases, a planned reduction in the size of central bank balance sheets (quantitative tightening) has also played a big role in contracting liquidity.

The mighty greenback – the dollar remains the reserve currency

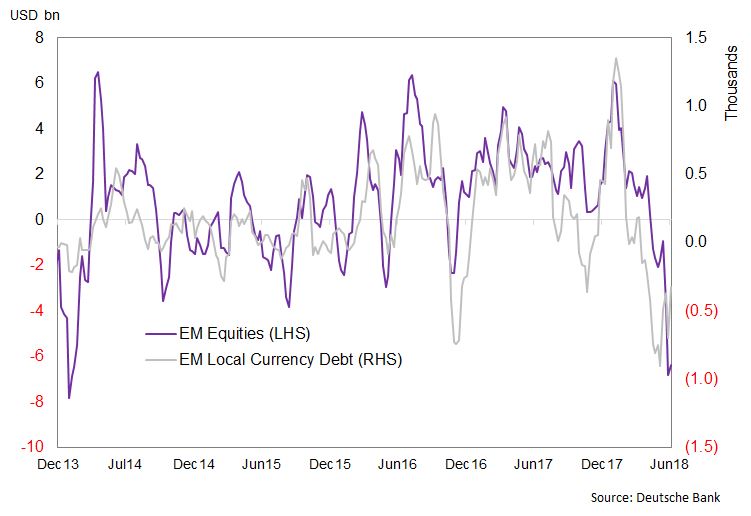

Unlike in previous occasions of dollar strength, this time around the oil price has climbed quite sharply. Besides tighter liquidity and rising rates, higher oil prices are acting as another drag on economic conditions across Asia. Most countries are dealing with a hike in petrol and diesel prices, leading to lower disposable incomes. Current account positions have come under stress in some countries, as the region is a net importer of oil and refined products. These conditions are applicable to emerging markets in general, hence the reaction in terms of fund flows has been vicious. There is no better way to see this than to look at ETF flows in both emerging equities and debt markets.

EM investors abandon ship

The good thing about economic and liquidity cycles is that they repeat themselves. The painful part, though, is the downturn, which can hit very hard and very fast when it happens.

Remedial action

In the face of what appear to be challenging conditions for Asian economies, the stocks that I have bought lately broadly share the same characteristics: a strong balance sheet; high cash flow-generating abilities; a domestic business orientation; and, finally yet importantly, signs of a turnaround from the effects of idiosyncratic slowdowns that each of them has had to deal with.

The repair work is, I believe, done. It is time for the recovery, even if that may well only be on a relative basis given prevailing headwinds for the asset class.

Learn more about the Pendal Asian Share Fund

Learn more about the Pendal Global Emerging Markets Opportunities Fund

One of the things our team most enjoy about the research process is the opportunity to go out into the field and visit the operations of our investee companies in person. There is nothing like putting a hard hat or a lab coat on and getting a hands-on perspective to visually comprehend the scale and quality of an operation or asset. It also affords an opportunity to converse with management and employees in the comfort of their own operating environment where they are happy to demonstrate their passions. For our approach it is imperative that each team member conducts research trips through the year to update our knowledge of the company and its operating environment. On our latest trip to the US, Paul Gyenge – Senior Investment Analyst within the team – took the opportunity to visit the Howard Hughes-developed South Seaport District. In this latest edition of our global research trip notes, Paul shares his thoughts on the asset and the rationale for our long term investment in the company.

Howard Hughes Corporation (HHC) is a mid-cap company we have followed since it was spun out of General Growth Properties in 2010. As a standalone entity, HHC has been able to develop and monetise its assets with the freedom and flexibility that would not have been possible as part of a larger property group. We have held a consistent position in HHC since the Pendal Concentrated Global Share Fund’s inception when the opportunity arose to purchase the company at a discount to our assessed intrinsic value. It was still recovering from demand concerns in its key state of Texas after the oil price decline in 2014/15. This is a typical and favoured scenario for our process, which sees short term issues that lead to stock price weakness as an opportunity, given our long term investment horizon.

At the time of launching the Fund we were looking for businesses with leading market positions and assets valuations that are out of step with the share price. The prevailing market environment resulted in a number of real estate companies being sold down on premature concerns over monetary tightening (recall the taper tantrum?) and instinctively we knew that some of these companies had become oversold. We assessed the sector and developed a positive view on HHC. We liked the business model and the board structure, with individuals holding material equity in the company. We also valued the company’s strong development pipeline which notably included the South Seaport District development in Lower Manhattan, which was expected to drive earnings in the Strategic Development segment. The stock was trading at a discount to NTA which also warranted attention and we decided to initiate a position. Nearly two years later, we thought it was an opportune time to visit the site, assess the operating aspects and the potential for growth in free cash flow.

At the time of launching the Fund we were looking for businesses with leading market positions and assets valuations that are out of step with the share price. The prevailing market environment resulted in a number of real estate companies being sold down on premature concerns over monetary tightening (recall the taper tantrum?) and instinctively we knew that some of these companies had become oversold. We assessed the sector and developed a positive view on HHC. We liked the business model and the board structure, with individuals holding material equity in the company. We also valued the company’s strong development pipeline which notably included the South Seaport District development in Lower Manhattan, which was expected to drive earnings in the Strategic Development segment. The stock was trading at a discount to NTA which also warranted attention and we decided to initiate a position. Nearly two years later, we thought it was an opportune time to visit the site, assess the operating aspects and the potential for growth in free cash flow.

The Manhattan Transfer

The South Seaport District is located on the East River in Lower Manhattan, New York, not far from the Brooklyn Bridge. Over the past few years Lower Manhattan has seen a significant transformation following hurricane Sandy of 2012. The city has been progressively shifting from a financial services hub to a precinct for media, advertising and technology companies. This development has been attracting young, affluent, well-educated New Yorkers with a median age in the low 30’s and an average household income exceeding US$200,000. Today, the residential population has grown to over 60,000, with plans under development for the construction of a further 4,000 apartments.

In order to get to the Seaport District I used the new Fulton Transit Centre, from which the precinct is a five-minute walk and serves as a key access point alongside the World Trade Transportation Hub which opened in 2016. These two links serve more than half-a-million commuters daily and provide easy access to the district alongside the ferry terminal and the New York ring road.

The Seaport District comprises eight buildings on several city blocks with a ground lease in place until 2072. The area has a rich history as a bustling port and fish market. HHC has endeavoured to incorporate this history in its redevelopment by bringing the old Tin Building back to its 19th-century glory. Once fully restored by 2020, the Tin Building will operate as a 4600 square metre food market. This is being developed under the guidance of famed American-French chef, Jean-George Vongerichten.

Pier 17 with the Brooklyn Bridge and

New York skyline in the background.

Source: Howard Hughes Corporation.

The jewel in the crown of the project is the new Pier 17. The site encompasses 18,500 square metres of lettable floor space that is spread over four levels, offering views of the Brooklyn Bridge, Statue of Liberty and the city skyline. The rooftop provides an extra 6,000 square metres of space which transforms into an ice skating rink. In the summer the space is purpose built to hold concerts for 3,500 standing or 2,400 seated patrons. The first summer concert series is set to open on 28 July with a diverse line up including Amy Schumer, Kings of Leon, Slash (of Guns’n’Roses fame), Diana Ross and even legendary crooner, Paul Anka, who will perform renditions of Frank Sinatra’s songbook presumably featuring an encore of the heartfelt New York, New York!

High profile tenants move in

In April this year ESPN moved into the fourth floor and is occupying close to 1,800 square metres of space under a long-term lease. EPSN currently broadcast eight shows a day using both their internal space as well as external locations on Pier 17 as a backdrop to their programing. The lower two floors of the building will feature six dining concepts, including David Chang’s newest Momofuku and Jean-George’s Vongerichten, set to open later this year.

ESPN’s Get Up! filmed from their new studios at Pier 17.

Source: Howard Hughes Corporation.

In leasing the properties Howard Hughes has taken a partnership approach, whereby leases are structured to incentivise tenants through variable rent schemes linked to revenue generation. This approach is designed to build long term commitments with the right tenants and promote low tenant turnover in the future. Advertising also provides a meaningful opportunity, with sponsorship agreements in place with Lincoln, Heineken, and Ticketmaster, representing more than US$2.5 million in annual revenue. The rooftop naming rights are still to come.

Real estate development with a difference

Total construction cost for the entire project is expected at around US$800m. HHC is targeting a stabilised annual return of 6-8% plus any revaluation if and when they choose to sell the asset. It would not be out of the question to expect a sub-5% cap rate valuation for such a unique asset in a prime location. In our view, development of the Sea Port District demonstrates the pragmatic long term mindset that HHC takes to extracting the most value from its assets.

Other assets within the HHC business include master plan communities (MPCs) in Las Vegas, Texas and Columbia, and commercial assets in Hawaii and Chicago. The MPCs are large parcels of land where the company manages the development of entire new communities over decades. HHC sell blocks of land to homebuilders while developing the retail and commercial real estate to service those newly created communities. By controlling the supply of new homes tightly they are afforded the luxury of managing their assets through the cycle rather than for the cycle, as is more typically the case for most real estate development companies.

Management also takes a conservative approach to the balance sheet by keeping leverage low, with a debt to enterprise value in the mid 30s and two-thirds of its debt under non-recourse terms. The company is now reaching a point where it should be able to self-fund its future developments through a mix of cash and liquidity on its balance sheet, continued land sales at MPCs and the sale of non-core assets. This represents a key de-risking event for the company’s equity.

Source: Howard Hughes Corporation.

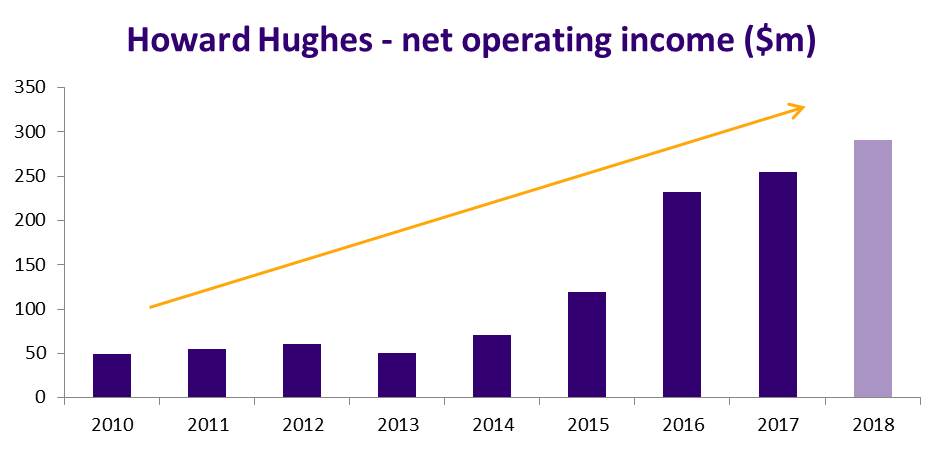

The stock remains largely unfollowed by the investment and broking community as it does not fit neatly into most ‘cookie cutter’ analysis due to its business model that combines development and management of mixed-use real estate. The financials are lumpy in the short term due to the land and asset sales but the underlying operating income continues to grow as the assets are developed and leased. The appropriate way to value such a company is to distinguish between their stabilised net operating income (NOI) and the remaining value of their land. Management’s most recent target for stabilised NOI was US$291m (which does not include the potential US$50-65m a year from the Seaport District) while the remaining land bank and assets under development are worth US$3-4b. All things considered, our analysis suggests the equity in HHC is conservatively worth US$180 per share, which is around 35% higher than its recent trading range.

The stock remains largely unfollowed by the investment and broking community as it does not fit neatly into most ‘cookie cutter’ analysis due to its business model that combines development and management of mixed-use real estate. The financials are lumpy in the short term due to the land and asset sales but the underlying operating income continues to grow as the assets are developed and leased. The appropriate way to value such a company is to distinguish between their stabilised net operating income (NOI) and the remaining value of their land. Management’s most recent target for stabilised NOI was US$291m (which does not include the potential US$50-65m a year from the Seaport District) while the remaining land bank and assets under development are worth US$3-4b. All things considered, our analysis suggests the equity in HHC is conservatively worth US$180 per share, which is around 35% higher than its recent trading range.

Future share price drivers

The Pendal Concentrated Global Share Fund has earned a return of 7% from HHC since inception. While it has been a relative underperformer for the Fund, the company’s intrinsic value has continued to grow. As projects reach completion and leases are secured the execution risk is reduced and value is created through the sustainable growing income streams generated. At the same time, the remaining land value increases through the combined influence of increased demand and reduced supply. Management is of the same mindset and is committed not only to managing the assets correctly but also to increasing awareness in the investment community of the HHC story. They are aligned with shareholders through a mix of direct equity ownership and incentive structures – a key factor we look for when investing.

HHC provides the Fund with exposure to an expanding US economy and an undervalued yet diverse asset base managed by a leadership team with strong credentials and skin in the game. As such, we are happy to hold our position even if it takes time for the market to appreciate the true value of the company. We continue to believe the development and management initiatives, current growth trends and management tenacity will create substantial value for shareholders. And I’m sure Sinatra is looking upon this evolving precinct of New York with a sense of pride, and perhaps regret that he’s not around to “be a part of it” and own some HHC scrip.

Click here to download a copy of this article