Fund Manager commentary for the month and quarter ended 30 June 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

“Inside Xi Jinping’s purge of China’s oil mandarins”

Reuters Special Report, 25 July 2014

A key component of our investment process is looking at how macro-level developments drive risk and opportunity at the stock level. One recent example of this is the Chinese state-owned oil companies, which we feel are a good-news story being overlooked by the market, and where we have been actively investing.

For background, the People’s Republic of China owns (via an entity known as SASAC) stakes in about 100 central state-owned companies. Three of these are China National Petroleum Corporation (CNPC), China Petrochemical Corporation (Sinopec Group) and China National Offshore Oil Corporation (CNOOC Group), all of which are among the world’s largest companies. Each of the three then has a listed subsidiary holding a large part of the operating assets of the parent. The listed companies are PetroChina (owned by CNPC), Sinopec Limited and CNOOC Limited.

As these oil companies became more commercial in the 1990s, CNPC was managed by a tight-knit group of officials under Zhou Yongkang and Jiang Jiemin, who each progressed from head of CNPC to senior political jobs such as Minister for Resources and head of SASAC. This period was characterised by rapid growth in all three of the listed oil companies, with heavy investment and aggressive acquisitions, many of which had poor financial returns. One of the last of these, as an example, was CNOOC Limited’s US$15.1b 2013 acquisition of Canada’s Nexen, which pushed CNOOC Limited’s costs up very substantially for limited additional production.

An aerial view of artificial islands on Kashagan offshore oil field in the Caspian sea, part of the assets purchased in China’s $5b investment in Kazakh oil assets in 2013.

2013 was also, however, when President Xi Jinping came to power. His programme to crack down on corruption and malpractice rapidly came to the oil companies, and CNPC in particular, with Zhou Yongkang and Jiang Jiemin among the many executives to be prosecuted. As the Reuters report referenced above notes, ‘investigators are scrutinizing offshore and domestic spending, including oil service contracts, equipment supply deals and oil field acquisitions.’

The resulting improvement in governance at the state-owned parents has had a very visible effect on the operating and financial metrics of the listed oil companies. The most dramatic improvement has come at CNOOC Limited, where all-in costs per barrel have declined from US$45 in 2013 to US$33 in 2017 (with the cash all-in cost per barrel falling even more sharply, from US$24 to US$12). Similarly, another key metric, the investment in production capacity, declined from over RMB 6,000/ton in 2012 to around RMB 3,000/ton in 2017. Crucially, discipline has not come at the cost of output – production actually increased from 411m barrels of oil equivalent in 2013 to 470m in 2017.

Sinopec Limited is a more downstream operation, with the world’s largest oil refining capacity and over 30,000 petrol stations. Improvements have come across the board, with lifting cost per barrel down, strong growth in the retail and marketing business, and a turnaround in the chemicals business from large losses in 2012 to healthy profits in 2017. Significantly for both companies, dividend payout ratios have risen substantially, from 42% in 2012 to 118% in 2017 at Sinopec Limited, and from 26% to 75% at CNOOC Limited in the same period.

We do not see this massive governance improvement as having been recognised by the market, with both companies trading at substantial EV/EBITDA discounts to both global and emerging peers. It is precisely this kind of macro-driven stock opportunity that our process is designed to identify. Consequently, we hold significant portfolio positions in both Sinopec Limited and CNOOC Limited.

In last month’s newsletter, I wrote about the pain points in global markets that were being revealed as a result of the roll-back in extraordinary central bank liquidity. Another pain point related to this is the availability of market liquidity. Since the GFC, market liquidity has changed structurally and for the worse. It has not been obvious in recent years because that liquidity, especially for exiting risk, has not been in demand. After all, what with global central banks pushing so much excess liquidity into markets in the last two years, any investor who has turned a blind eye to growing fundamental risks has been well rewarded.

As Australia’s past and present experience demonstrates, the smaller the market and the greater its reliance on global risk appetite, the more likely it will suffer from thinning liquidity. This month, I take a closer look at Australian cash and funding markets, how they have been impacted by the ongoing changes to global liquidity, and what that means for the opportunity set available to domestic investors.

View the newsletter here

Pendal Australian Long/Short Fund (APIR: RFA0064AU, ARSN: 121 948 810) – Important information

Reduction in management costs from 18 July 2018

From 18 July 2018, the issuer fee for the Fund will reduce from 0.85% pa to 0.50% pa and the hurdle used to calculate the Performance fee will increase from the Fund’s benchmark (S&P/ASX 200 Accumulation Index) to the Fund’s benchmark plus the issuer fee.

There has been no change to the performance fee percentage, which will remain at 15% of the Fund’s performance in excess of the performance hurdle.

In this Australian Quarterly Update we look at how the Australian economic landscape has been changing and why the RBA is becoming more optimistic on wage growth. We consider if the RBA is ever going to raise rates and look at why local credit markets have seemingly lost their Teflon coating as credit spreads widen. Finally, we emphasise the importance of ESG considerations in investing with a case study of how Coca Cola Amatil has lost its fizz.

I hope you find the piece useful and we welcome feedback from readers.

View our Australian Quarterly Update here.

“US consumer staples plunge as bond yields rise”

Financial Times, 24 May 2018

We wrote last month about the negative effect of rising US bond yields on some emerging economies (and their currencies). The sharp sell-offs in Argentina and Turkey in May support our views, but there are also some key sector effects in this environment.

So far 2018 has seen ample evidence of a strong global growth environment, but with gently building inflationary pressures putting upward pressure on bond yields. From a starting level of 2.4%, US 10-year Treasury yields reached 3.1% in mid-May. The increase in risk-free bond yields puts pressure on other income-generating assets around the world, including emerging market bonds, but also including low-beta, dividend-paying stocks, the so-called ‘bond proxies’. These stocks, principally in the consumer staples, telecom and utilities sectors, have generally performed well in recent years, but now face a less favourable environment.

This has been the case in emerging markets year-to-date. With the MSCI Emerging Markets price index down 1.0%, MSCI EM indices for consumer staples, telecoms and utilities are down 3.2%, down 9.8% and up 1.5% respectively. The portfolio is significantly overweight consumer staples (in India, Mexico and Russia, which provide exposure to domestic demand; in South Korea, China and Brazil as more defensive positions), and broadly neutrally-weighted in telecoms and utilities.

The consumer staples position has been a negative contributor to the portfolio’s performance year-to-date, but within the sector there has been a broad range of returns. The investments with exposure to China include Tingyi (noodles) and South Korea’s LG Household & Health (cosmetics), which have both performed well after a strong 2017, and also Hengan International (infant care), which has lagged year-to-date after a strong 2017. We see continued strong growth in the Chinese consumer sector in 2018, despite monetary tightening, with companies holding strong brands able to push through earnings-enhancing average-selling price increases in 2018. Also generating positive performance despite a weak country performance has been retailer Walmart de Mexico (Walmex).

India’s ITC (tobacco) and Russia’s Lenta (retail) are about flat year-to-date. Both countries are seeing a pick-up in economic growth, but the higher oil price is a tailwind for the Russian consumer and a headwind for the Indian consumer. Tax increases have also been a drag on ITC’s operational performance. Also in Russia, retailer Magnit has been weak this year, as investors wait to see the effects in a change of corporate leadership.

Our process remains assertively top-down, but stock selection also remains a key part of the process, as can be seen in recent performance.

The bulk of our underperformance in consumer staples has come from Brazilian food producer BRF, which has underperformed even a generally weak Brazilian equity market. It has struggled to maintain margins despite lower input prices and the weakness in the Brazilian real. As it the case with Magnit, there has been a change in management, the effects of which are yet to be seen.

Nonetheless, the positive contribution of telecoms and utilities has more than offset the drag on performance from consumer staples. In each case we have a single Chinese holding. China Mobile reported impressive 2017 results but declined slightly, in line with the MSCI EM Telecommunication Services Index, but our utility investment, ENN Energy, performed very strongly (+46.3% in US dollar terms), on continued strong demand for natural gas in Chinese urban areas.

Overall, the portfolio has seen a positive contribution from its investments in bond proxies. While some of this came from good top-down calls, it was principally through stock selection. Our process remains assertively top-down, but stock selection also remains a key part of the process, as can be seen in this case.

This case study on Pendal’s credit risk assessment based on ESG factors was published by the PRI — the world’s leading proponent of responsible investment — as part of their ESG in credit ratings initiative which aims to enhance the transparent and systematic integration of ESG factors in credit risk analysis.

In this case study, George Bishay, Portfolio Manager of the Pendal Sustainable Australian Fixed Interest Fund, shares his insights into the rationale for limiting exposure to credit issued by Coca Cola Amatil. The decision reflects long-held concerns over the social risks associated with high sugar and the consequences of structural shifts in consumer behaviours. This case study provides a timely illustration of the impact on corporate profitability from non-financial considerations and the value that can be added through integration of ESG assessments in credit analysis.

Click here to view the case study.

This case study is included in Appendix 2 (pages 56-57) of the ‘Shifting Perceptions: ESG credit risk and ratings‘ report which explores the disconnects encountered when integrating non-financial risk assessments. The report delves into PRI’s findings on the challenges encountered by credit practitioners in integrating ESG-related risks, together with practice guidance on the implementation of risk assessments and engagement with credit ratings agencies.

Fund Manager commentary for the month ended 31 May 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Infrastructure develops at a glacial pace in Manila. On a short visit, you would hardly notice any meaningful change in this often chaotic city. Bumper-to-bumper traffic, it took us almost 25 minutes to exit the airport and traverse 500 metres across a traffic junction.

Yet there is change. ‘Entertainment City’ houses three of the four newly-built integrated resorts and casinos, the first of which opened in 2013. That whole area is wide open with broad boulevards, a sea-facing frontage and swanky new buildings. A new expressway, completed in 2016, connects the airport to these casinos and has cut travel time to just 20 minutes from more than an hour prior to 2016. It is no wonder that tourism to Manila, in particular from China, has started to pick up, as has the revenue of those casinos. Several large areas that are converted townships are witnessing a boom in property construction. Even outside Metro Manila, in Visayas and Mindanao, there are new roads and airports under construction.

Effective January 2018, Filipinos had a relatively big change in their tax policies. Under the first part of the reform process, income tax for low and mid-level salaried employees was substantially reduced. However, taxes were raised on a host of items, including petroleum products, cars, tobacco and sugar-sweetened beverages. In the next stage, the government wants to reduce corporate taxes from 30% to 25% while simplifying the myriad of incentive schemes given to states.

During a time of rising oil prices and a weakening peso, these changes in taxes are affecting several parts of the economy. For one, costs have increased across the board as petroleum prices have risen. In general, inflation is rising and the pernicious effects are being felt by the most vulnerable and poor sections of society. Companies which cater to the low income part of society, such as Universal Robina, have seen sales slowdown while companies like Robinson Retail, which cater primarily to middle income families, have seen a bump up in sales. The middle-income cohort seems to be in a much better position, especially as they benefit from the income tax reduction. Yet, so far, overall consumption is relatively benign.

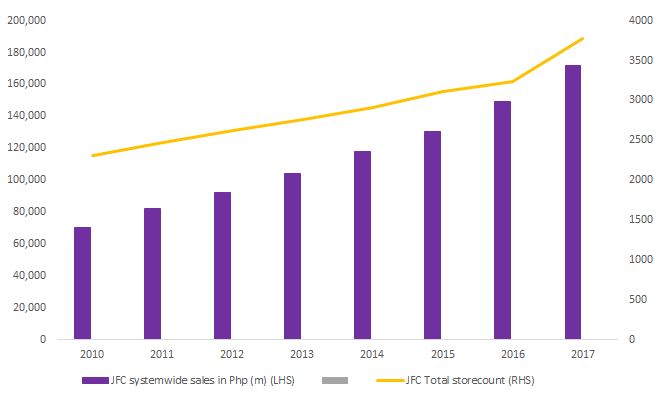

We spent a fair bit of time with Jollibee Foods (JFC), the only Philippine stock we currently own in our portfolio. It is a leader in the quick service restaurant (QSR) business in Philippines, with an expanding footprint around the world. If done right, QSR businesses can be very profitable and scalable. American chains such as McDonald’s or Chipotle are prime examples of the model. I’ve seen analysis on QSR models where the EBITDA returns on total investment per store can range from 18-30% pa. In JFC’s case, their main brand Jollibee earns returns per store upwards of 35%.

Over the years, JFC has expanded its offerings of different cuisines in the Philippines. One brand they acquired in 2010, ‘Mang Inasal’, has expanded its store network from 345 to 495 stores in the past seven years. However, by improving sales per store by almost three times, total revenues for that brand increased from Php2.3bn in 2010 to Php17bn in 2017. Once a concept is successful, JFC expands to destinations abroad where there are Filipino nationals.

JFC ventured into China in 2005 and for a long time after that the China business was a struggle. Intense competition, rising wage costs, and lastly a structural shift to online ordering of food have tested its Chinese business. After stagnating for almost three years as management figured out a way to deal with challenges, 2017 has seen a low double-digit same-store-sales growth.

Jolly steady growth at Jollibee Foods

JFC recently took over Smashburger, a burger chain in the US, and increased its existing stake in a company that is expanding in Vietnam to a majority. In the past couple of years, the management team has invested a fair bit, expanding new stores and acquiring new formats. Given their past record of accomplishment, I have reasonable confidence in their ability to execute on this expansion. It is a challenging time for the business: peso depreciation, rising inflation, tax changes and structural changes to the restaurant industry from online food delivery businesses. Yet with a 16% growth in system-wide outlets, a healthy balance sheet and the ability to increase prices and maintain margins over time, JFC should be able to grow through these tough times.

Well that was certainly fun. Over recent months we have been making the strong case that as a result of the normalisation of global monetary policy, global liquidity will recede and market volatility will rise. Well it certainly did in May as Italian yields puked and global asset markets reacted. The era of Quantitative Easing (QE) boosted asset prices and bought forward future asset returns to today. We expect that in a period of Quantitative Tightening (QT) the reverse is going to happen. To be crystal clear, a normalisation of the QE experiment requires adjustments, and those asset prices that have benefited the most from the abundance of liquidity are likely to be the ones that will require the greatest of adjustments.

This month, I focus on the current key events, the casualties of May and how markets will continue to unfold.

View the newsletter here.