The Pendal Defensive Equity Income Fund closed to applications and reinvestments effective 7 June 2018 and will terminate effective 17 July 2018, with the assets liquidated and the net proceeds returned to investors.

More information

The Pendal Balanced Equity Income Fund closed to applications and reinvestments effective 7 June 2018 and will terminate effective 17 July 2018, with the assets liquidated and the net proceeds returned to investors.

More information

Market headlines in the final week of May were dominated by developments in Italian politics. Uncertainty over which parties would lead the country’s government and what policies they would pursue drove some sizeable price swings that extended beyond Italian bonds. We will delve into the details and explore the situation in more detail in our upcoming newsletter. For now, we thought it would be timely to highlight some of the more noteworthy market movements and the relevance to broader risk-sentiment.

The most dramatic reaction to the Italian turmoil has arguably been witnessed in yields for Italian bonds, the fourth largest bond market in the world. As illustrated in Chart 1 below, the 2 year Italian yield spiked an alarming 304bps during the month. This benefited our positioning for a widening in the spread between Italian and German yields. Given the arithmetic of the election results in March, there was never a possibility of a market friendly outcome. The best outcome for the establishment parties was a second election, but in reality this would have just bolstered support for the populist parties. Moreover, while there were echoes of the French election worries that ultimately fizzled last year, as we explore later – the market environment has changed and risk sentiment is more vulnerable than 2017.

Chart 1: Italian 2 year yield

Beyond Italy, the sharp correction for risk appetite spread through the region with Spanish bonds suffering a smaller but still significant spike (2 year yields from -34bp to 7bp). Similarly, the region’s common currency endured a 3.2% slide, the largest monthly decline since November 2016. The spill-over effects were also felt in the credit arena, where the cost of protection on European high yield jumped 51bps. This accelerated the trend higher calendar-year-to-date as visible in Chart 2. These sizable moves served our short credit and short Euro exposure well.

Chart 2: European High Yield CDS Credit Spread

In terms of the economic landscape, we have previously pointed to reasons why we believe the European growth story has tired and has already turned a corner. This includes the gusting tailwind of strong export growth fading to a breeze as the surge in Chinese imports drops, coupled with the looming effects of trade wars.

While the situation in Europe is likely to continue capturing investors’ attention in the near-term, the real story is one that we have spoken of repeatedly this year, namely; the return of volatility. It is a story driven chiefly by the withdrawal of an unprecedented swell of liquidity in the financial system. A tide that had lifted all asset classes, but more importantly a force that had lured investors to those offering higher yields, which are now those that are the most at risk of an unwind. We won’t rehash all the implications here – our March newsletter discussed some of the dangers in more detail. What is worth emphasising is that the aforementioned moves across Italian bonds and high yield credit are part of this much larger story, which arguably has many more chapters ahead.

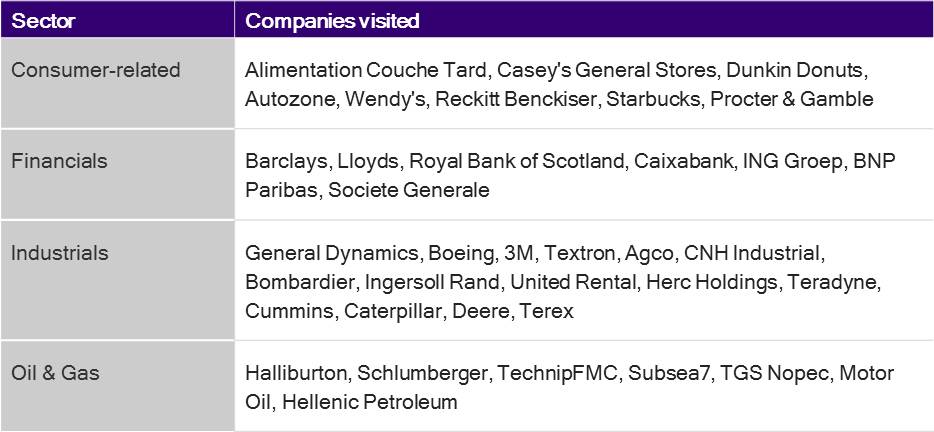

In the weeks leading up to Easter, the Pendal Concentrated Global Shares Team completed its latest round of due diligence which took the team to parts of Europe and the US to review companies involved in various industrial functions, energy, financial services, real estate, and consumer goods. This trip provided the team with the opportunity to identify new investments, stress test existing portfolio positions, and confirm the underlying tenet of our portfolio that the global economy has reached an inflection point remains intact.

Company meetings – March-April 2018

Our meetings did very little to dispel our belief that the global economy remains on a path of growth. Interestingly, no group of companies were more positive than the industrials, despite President Trump’s tariff impositions, which evolved from rhetoric to reality during our trip. From the humble tractor maker to the builder of aircraft, confidence was shared by all and stems from the fact that much of the demand to date has related to replacement rather than expansion, with any over-enthusiasm being kept in check by a supply chain struggling to keep up. Quantitative measures such as equipment pricing, rental rates, and backlogs are all trending favourably and are supportive of the view that growth will extend beyond what is shaping up to be a very strong 2018. While a lot of the industrials space has already re-rated, opportunities remain and we look forward to sharing these in due course.

With regards to the businesses already in the portfolio, the trip left us comfortable with our ownership of Boeing, despite the value of the company having doubled over the past year. We believe the quality of the business continues to be underappreciated by many in the market which, under the leadership of CEO, Dennis Muilenburg, has been re-engineered to become a more responsible allocator of capital and generate persistent growth in free cash flow. Since our last update, Boeing has continued to make solid progress in its key aircraft program. The company is continuing to grow its order book and has committed to increasing the production of 787 aircraft from 12 per month currently to 14 per month. Boeing recently delivered the inaugural 787-10 to Singapore Airlines and continues to undertake due diligence on the much anticipated ‘middle of market’ airframe.

New portfolio investment

The latest addition to the Pendal Concentrated Global Share Fund is Seven & I Holdings. This Japan-listed company exhibits many of the characteristics favoured by the team and our process. In this edition of our Global Research Trip notes we share our insights from recent site visits to the company’s US outlets and the opportunities we see for investors.

—————————————————————————————————————————————————————

Who is Seven & I Holdings?

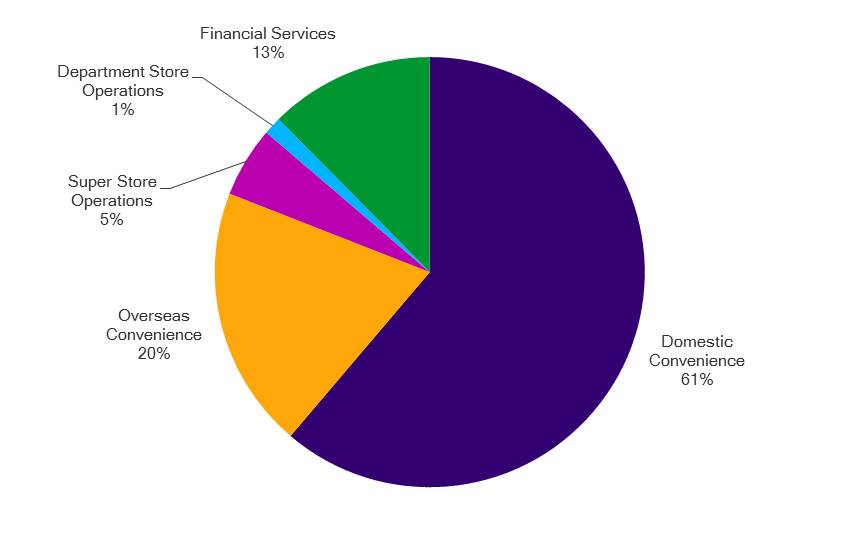

Seven & I Holdings (herein referred to as 7-Eleven) entered the team’s investment radar late last year during a research trip to Japan. The business operates/licenses/franchises stores under the 7-Eleven brand and is the leader in Japan’s convenience store (“C-store”) market. The company is building upon its 44% market share through a fresh food offering that resonates with the country’s demographic and lifestyle demands. Complementing the C-store business in Japan which makes up 61% of earnings is the overseas C-store business where 7-Eleven is a top player in the consolidating US market. The company also operates a profitable financial services business and a portfolio of shopping centres and department stores in Japan.

Seven & I Holdings (herein referred to as 7-Eleven) entered the team’s investment radar late last year during a research trip to Japan. The business operates/licenses/franchises stores under the 7-Eleven brand and is the leader in Japan’s convenience store (“C-store”) market. The company is building upon its 44% market share through a fresh food offering that resonates with the country’s demographic and lifestyle demands. Complementing the C-store business in Japan which makes up 61% of earnings is the overseas C-store business where 7-Eleven is a top player in the consolidating US market. The company also operates a profitable financial services business and a portfolio of shopping centres and department stores in Japan.

Seven&I Holdings – business overview

Why we invested in Seven & I Holdings?

We initiated a position in 7-Eleven at the start of 2018 after our initial due diligence revealed a business where the troubled performance of its non-core assets (i.e. department stores, supermarkets and shopping centres) was overshadowing the dominant position held by the Japan-based C-store business and the opportunities within a consolidating US market. The non-core assets of the business have been so overbearing that there is now a significant valuation disparity compared to C-store operators both in Japan and North America.

Japan retail sales growth by segment: 1998-2016

Source: Japan Ministry of Economy, Trade and Industry. Growth has been indexed; 1998 = 1.00

Under the leadership of CEO Ryuichi Isaka, we have confidence that the significant value we see in the business will be unlocked. Appointed in 2016, Isaka-san’s approach to the business can be summarised as one of capital discipline, having outlined a strategic mandate that has demanded smarter investments in the Japan C-store business, improve in-store execution in the US C-store business, and close or divest department stores and shopping centres. In his first year, Isaka-San closed four department stores and 11 shopping centres/general merchandise stores, with more to come under his five-year plan. Over time, the rightsizing of non-core assets will help further de-risk the business and re-focus investor attention to the company’s core competencies. In the interim we are paid to wait through a circa 2.5% dividend yield.

What we learned about the business from our US trip

As part of our initial due diligence it was suggested to us that the US C-store market is primed for consolidation, with more than 150,000 stores of which, 65% are owned by operators of fewer than 10 stores. The two biggest operators, 7-Eleven and Alimentation Couche-Tard, have less than 10% market share each and were expected to be benefactors of the impending consolidation.

Our visits to numerous C-store operators in the US confirmed the validity of the consolidation thesis. We observed a significant gap in execution between the independents and chains a gap that will only get wider as the chains make investments to differentiate and enrich their food offerings and improve their technology capabilities. With some independents already struggling to fund working capital (e.g. empty shelf slots), it’s likely they’ll be left behind in the current investment push.

Conclusion

Overall, we left the US confident of 7-Eleven’s strategy in the US. The growth trajectory is significant as the independent operators, who are struggling for capital, act as market share donors for the chain operators for decades to come, either organically or through mergers and acquisitions. Since buying the stock, it has outperformed the MSCI AC World ex-Australia (A$) Index by nearly 7% as it continues to gain market share from Japan convenience store peers, execute on cost efficiencies, and return non-core businesses to profitability. Continued execution on these fronts should help reverse the valuation discount to peers, which is in excess of 20%. Having served 7-Eleven in a range of roles since 2009, Isaka-san knows the convenience store business well and exhibits the commercial acumen to drive organic growth in a strident, yet sensible manner.

Fund Manager commentary for the month ended 30 April 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

*Of the book series ‘Lemony Snicket’s A Series of Unfortunate Events’, by Daniel Handler

It has been a challenging period, as evidenced by the performance of the Fund. Last year’s underperformance was more ‘explainable’ – the big cyclical rally combined with a couple of stocks that did not work for me on a relative basis. Yet I felt the outcome last year was in the range of expectations. This year to date has been just plain frustrating.

We came into 2018 with a few working assumptions. Global economic growth trends were strong and gaining momentum. In emerging markets (EM), after periods of varying headwinds there was evidence of stability and growth. Inflation particularly across EM seemed very benign.

If you recollect, China had been the vortex of financial instability in 2015 and 2016. There was an explosion of debt, especially off-balance sheet debt, slowing GDP growth and a changed management of the currency. Capital outflows at a time of rising US interest rates had pressured the Chinese economy even further. In 2017, the authorities did clamp down on rising debt levels. Specifically, they first regulated the peer-to-peer lending schemes. They also nationalised Anbang Insurance while curtailing operations of the HNA group – both these being the most egregious of firms that borrowed short-term capital to make acquisitions outside China.

Yet the bigger and more significant policy move was the focus by the authorities on pollution in China. As one commentator opined, there is a complete shift in the incentive system for the authorities at the national, provincial and city levels. Since the 1980s, as the economy opened up, growth was the only metric to assess performance for various government authorities. Growth led to increased employment and rising per capita incomes. The cost of achieving that growth – pollution, high debt and overcapacity (through misallocation of capital) – did not matter. That changed in 2017. Recognition by the highest levels of authority, now conveyed down the chain, that pollution control and citizen health needs to be as much a priority as growth, has redefined the way governments approach growth. There have been shutdowns of capacity in the steel, coal, cement and aluminium sectors. This has resulted in higher commodity prices, which in turn have improved cash flows for the remaining firms in those industries. Consequently, China’s banks witnessed a reduction in potential bad debt cases within the ‘old’ economy of China.

The stakes are high for negotiations between China and America: both sides know that trade barriers are not good but domestic political compulsions will dictate events.

Valuations for cyclicals in general had risen from the depths of 2016, yet they were far from stretched. Our expectation was that continuing economic growth combined with capacity controls in China would lead to better cash flow/profit growth and this would sustain for much longer. On a relative basis, cyclicals could grow faster and were cheaper than the market in general. Even though we had considered the rhetoric of trade tensions as a risk, the passing of the tax cuts in the US meant that growth there could be stronger, in effect necessitating higher imports and possibly higher deficits for the US. We kept our exposure to cyclicals at the higher end of my allocations, adding to financials in 2017.

Since February/March of this year, the imposition of sanctions by the US on steel and aluminium sectors seems to be the turning point for sentiment towards Asian markets. Subsequent sanctions on Chinese technology and telecom companies (particularly Huawei and ZTE), in my opinion, are more consequential for future growth expectations. In 2017, Huawei’s turnover was approximately US$95b while ZTE’s was approximately US$16b. These are large companies dealing with several customer bases and component suppliers across geographies. Apart from technology, some other sectors have come in for specific targeting. This has resulted in a retaliation from China on US exports from corn to wastepaper. In my view, it’s not relevant to analyse which particular sectors might be targeted; it’s the uncertainty this creates about the future path of friction-free trade that matters.

The stakes are high for negotiations between China and America: both sides know that trade barriers are not good but domestic political compulsions will dictate events. There is still a chance that a compromise might be reached. That is our hope, but the reality is that we have to be prepared for a tougher trade environment. At the start of the year, from our projections for profit and cash flow growth in Asia, we felt comfortable about prospects in 2018. I have had to temper those expectations a bit.

From our regular screenings and our shortlist of prospective investments, we invariably find some good quality businesses that I am very comfortable owning through tough times. In the past two months, I have been adding some new stocks into the portfolio. Last month I mentioned LG Household as one example. Another stock I have been adding to is Philippine-listed Jollibee Corporation. It is the largest quick service restaurant (QSR) firm in Asia, with a small footprint in the US as well. Jollibee derives almost 80% of revenues from the Philippines by serving customers across five different brands. In the second week of May, after meeting with management in Manila, we will be able to provide a bit more colour regarding the stock. The other positions are not yet at their full weights, but should be over the course of the next month or so. The common characteristics in all these companies is that they are relatively more insular, with decent growth prospects in the face of the challenging macro-economic environment that we might face across our region. The risk at this point is whether the trade frictions escalate and whether that results in a rally in the US dollar as investors look for safety above all else. I am reasonably confident that the businesses we own can survive a downturn and that if stocks do sell off, this will give us opportunities to add to them.

In this article, Greg Bright from Investor Strategy News pens “a potted history of the old BT and a view on its new expansion horizons.”

Read the full story

“Higher oil prices could be a game changer for Asia’s trade-gap trio”

Reuters, 26 April 2018

The first four months of 2018 have seen a more challenging global environment for emerging markets, notably a rising oil price alongside a strengthening US dollar and higher global bond yields. This combination of drivers exposes both countries with external financing needs, i.e. those with large and/or persistent current account deficits, and those with significant oil import bills. And the main way that those weaknesses come through is in currency movements. Emerging market currencies have generally been weak against the dollar so far this year, but an analysis of the two drivers mentioned above shows some distinct patterns. Overall, three groups of countries emerge.

The first, which have been the main point of focus in commentary, are the current account deficit oil importers. The Reuters article from which the above quote comes focuses on India, Indonesia and the Philippines, but the worst hit emerging currencies year-to-date have been the Turkish lira (down 11.0% against the US dollar at the time of writing), and the Argentine peso (down 17.9%). Both countries are expected to have current account deficits in excess of 5% of GDP this year and both are now facing the prospect of severe monetary policy tightening to limit currency weakness.

India, Indonesia and the Philippines also run current account deficits and are substantial net oil importers. In the first quarter of 2018, crude oil imports costs rose year-on-year in India by US$5b, in Indonesia by US$1b and in the Philippines by US$130m. Correspondingly, these countries have all seen currency weakness year-to-date, but so have several other emerging markets. Overall, the group of Argentina, Turkey, India, Indonesia, the Philippines, Pakistan, Brazil, Chile, Peru and South Africa have an average forecast current account deficit of 2.7% of GDP, will see that worsen by 0.4% of GDP for each US$10 increase in the crude oil price, and have seen average currency move of -5.9% against the US dollar year-to-date.

The second group are the oil importers whose current account balances are so strong that they are, for now, able to weather the rising oil price. Exclusively in emerging Asia, this group comprises South Korea, Taiwan, Malaysia and Thailand. These countries have an average forecast current account surplus of 7.1% of GDP, will see that worsen by 0.5% of GDP for each US$10 increase in the crude oil price, but have seen average currency move of +0.8% against the US dollar year-to-date.

The third group are the pair of Mexico and Colombia. Each produces about 600,000 barrels of oil equivalent per day more than they consume, and so although they run current account deficits, a US$10 increase in the crude oil price improves their current account balances by an estimated 0.2% and 0.7% of GDP respectively. Both currencies have strengthened against the US dollar so far this year as a consequence. Building on our comments of last month, this is another reason to be more positive about Mexican assets in the run-up to July’s presidential election.

Finally, the above analysis does not mention one important country: Russia produces an annual 2.9 billion barrel annual oil surplus, so oil’s move from the 2017 average of US$54 per barrel to the current US$77 is worth an extra US$67b to Russia, or 4.3% of GDP, while Russia’s forecast current account surplus is already 3.1% of GDP. At this oil price, Russian assets should be performing very strongly, yet the Russian ruble has fallen 7.8% against the US dollar year-to-date. Politics notwithstanding, if there is one emerging market that most benefits from this environment, it is Russia.

Recent market events have shown the continuing knock-on effects of US monetary policy normalisation. The reduction in US Dollars available onshore in the US, but more importantly offshore, is currently claiming its next victims in emerging markets. This is after pushing US short term money market rates higher in March and will continue as US monetary policy normalises. Quantitative tightening is a big part of it but the likelihood of positive real Fed Funds rates also sees US cash making a comeback as an asset class. This unravelling story has impacts across rates, currency, credit and equity markets and I will dive back into these next month. This month given there’s so much going on I wanted to take an in-depth look at Australia.

View the newsletter here.

Company and fund name changes

BT Investment Management Limited (BTIM) has changed its company name to Pendal Group Limited.

Since BTIM was listed in 2007, the business has transformed into an independent global investment management firm. In light of our growth and success, we believe now is the right time for our business to establish its own name and brand; one that reflects our independence, ownership and identity.

The name Pendal has been chosen because of its link to the heritage and origins of the BT investment management business. Pendal was the name given to BT’s original nominee company, established in 1971 to hold assets on behalf of its first prospective client, the Dalgety Pension Fund.

Pendal preserves the strengths, values and culture of our business whilst moving forward as an independent, successful, international investment management company.

What does this mean for investors?

While we have changed our company name, it will be business as usual with no change to our investment management approach or the operations of the company. As Pendal, we will continue our focus on delivering superior investment returns for clients through active management.

To reflect our new brand, we have updated the names of our funds. Please click here to view a list of our funds’ new names.

The responsible entity and investment manager have also changed their names, as follows:

| Previous Name | New Name |

| BT Investment Management (Fund Services) Limited | Pendal Fund Services Limited |

| BT Investment Management (Institutional) Limited | Pendal Institutional Limited |

We have updated our fund product disclosure statements, application forms and website to reflect the Pendal name, with changes to some of our other systems and documents to be implemented over time.