Headline earnings growth for Australian corporates reflects a continuation of favourable operating conditions, with aggregate results broadly in line with expectations and fewer negative surprises than usual. Forward earnings growth expectations are largely unchanged at around 6% and are well underpinned by the resources sector.

Key themes emanating from the results season include:

1. Stable earnings outlook which supports reasonable return expectations

2. A distinct lack of negative surprises

3. Earnings momentum is emerging in the cheaper sectors

4. Commodity prices provide a buffer for earnings growth

While the market’s valuation is above its long term average, it is not egregiously so and is entirely consistent with the low interest rate environment. However, conditions are differentiated at an industry level and we are cognisant of the ongoing wave of disruption to traditional business models and industry structures. Equally, we aware of earnings momentum gathering among previously unloved industrial cyclicals and these are presenting a range of compelling investment opportunities.

Access our full report

There are two attitudes you can take to the February 2018 “flash crash”. The first, and overwhelmingly the most popular, is that this was a technically driven correction in the markets, exacerbated by carry monkeys such as the short-VIX crowd, and that the pause since then has provided a refresh in a bull trend that remains well and truly intact. The second view, and much closer take to ours, is that the highs seen in the S&P 500 index on 26th January will be the highs of this cycle and the ensuing volatility marked the beginning of a protracted period of adjustments needed to realign asset valuations with a new reality. I suppose there could be a third attitude which is that the February crash signalled “game over” and equity markets are going to be taken round the back of the bike sheds for a kicking, and normally I would be the first to voice that position, but not right now. Not yet.

As Q1 drew to a close, we were hearing a mix of optimism and caution among our client base, with questions ranging from “shouldn’t you be less bearish given the tax deal struck in the US?” to “why has LIBOR-OIS widened to crisis levels and does this mean we’re on the doorstep of the next market melt-down?” Certainly a lot has happened over the last three months, some of which have been obvious (US tax reform) and others less so (LIBOR-OIS), and a lot is still going on (threat of trade wars, Facebook probes). In this month’s newsletter, I’ll try to piece together the bigger picture as we see it, what it means for markets and asset allocation, and how we’ll position for our views.

View the newsletter here.

“The luxury of today is the necessity of tomorrow. Every advance first comes into being as the luxury of a few rich people, only to become, after a time, an indispensable necessity taken for granted by everyone.” – Ludwig Von Mises.

Most of us can relate to that statement. The best manifestation of this societal norm is the smartphone. Perhaps the millennials of today might include ride-sharing and home-delivered food in that category. But could Von Mises have ever dreamt it could apply to policies by the central banks? As every major central bank talks about normalising monetary policy, all of us have to wonder whether asset markets and, in turn, the real economy are hooked on the necessity of quantitative easing.

Recent data indicates the global economy remains healthy with few clouds on the horizon. This naturally raises a question on the possibility of higher inflation across the world. Several data points suggest that inflation indeed is on the rise. If this portends a structural rise in interest rates, there will be an inevitable need to normalise monetary policy. At the same time, advances in AI, machine learning and robotics indicate a structural deflation, which could mean this nascent rise in inflation is just cyclical in nature.

Recent data indicates the global economy remains healthy with few clouds on the horizon. This naturally raises a question on the possibility of higher inflation across the world. Several data points suggest that inflation indeed is on the rise. If this portends a structural rise in interest rates, there will be an inevitable need to normalise monetary policy. At the same time, advances in AI, machine learning and robotics indicate a structural deflation, which could mean this nascent rise in inflation is just cyclical in nature.

Cleaner Chinese skies over chasing growth

Amidst this macro uncertainty, I do want to emphasise a distinct change for the better in the Chinese financial system. In no way do I suggest it is in pristine health. Accumulated debt from the stimulus-induced binge post 2009 and the spread of shadow banking to prop up the property markets very much remain a lurking risk. Yet, as I have mentioned before, the closures of capacity in several basic industries is a development worth noting. As a commentary from Gavekal Economics puts it: “There seems to be a change in the incentive system for the party officials and heads of governments across China.”

Personally, I still think that the improving global economic scenario and diminishing financial risks in China are bigger positives that outweigh the potential risk of trade war rhetoric. – Samir Mehta

In the past, every Chinese government official was measured by GDP growth they delivered, no matter the cost. If the by-product of that obsession with growth meant too much debt and rising leverage, or massive overcapacity, or pollution, so be it. But with President Xi Jinping now focused on reducing pollution, we have seen some drastic cuts in capacity in steel, coal, cement and maybe aluminium. If this change in focus is sustained, the new incentive system will mean that growth is subjugated to quality growth. The result will be better cash flows and healthier companies. This in turn helps the banking system, as the banks’ non-performing loans have in probably peaked for the moment. Simultaneously, the quasi-nationalisation of Anbang Insurance is evidence of the seriousness of the authorities to clamp down on debt accumulation. A company formed in 2004 as a motor insurance firm had accumulated USAUD$3080bn of assets by 2017 – most of them acquired from borrowed short duration money!

Deeds not words

The risk of a trade war and imposition of tariffs is a real risk for economies across the world. Yet, similar to much that comes from this White House, I would rather wait and see how much of what is said is finally implemented. I recollect in the early days of the Trump administration talk of levying an import tax. Analysts worked on various scenarios and modelled spreadsheets with ‘what if’ scenarios. Ultimately, this talk came to naught. With a return of volatility, markets are bound to gyrate around worst-case scenarios of possible tariffs and extrapolate them to infinity. Personally, I still think that the improving global economic scenario and diminishing financial risks in China are bigger positives that outweigh the potential risk of trade war rhetoric.

19 March 2018

Changes to the BT Wholesale European Share Fund (APIR: BTA0124AU, ARSN: 087 594 429) – Important Information

What is the change?

Following a review, J O Hambro Capital Management Limited (JOHCM) will replace MFS International (U.K.) Limited (MFS) as the investment manager of the Fund. This change will take place on or around 23 April 2018.

The Fund will continue to be an actively managed portfolio of European shares investing in companies listed in countries within the MSCI Europe (Standard) Index and opportunistically in companies domiciled outside Europe, from time to time.

Whilst both MFS and JOHCM utilise a bottom up, fundamental stock selection process with a focus on value and high quality businesses, JOHCM adopts a more active approach to portfolio construction. JOHCM’s investment process for European shares is a high conviction, contrarian approach that seeks to identify companies they believe to be undervalued in the near term but offer long term capital growth.

The JOHCM strategy is also benchmark agnostic, meaning that the benchmark’s weights are not used as a reference point during portfolio construction. With JOHCM’s investment approach being less constrained by the benchmark than MFS, they are able to focus on risk-adjusted returns rather than benchmark relative returns. As a result, JOHCM will build a more concentrated portfolio (typically between 20-25 stocks) reflecting their best investment ideas.

Why do we think the change in manager will be a better outcome for investors?

We believe that JOHCM’s more active and benchmark agnostic approach to portfolio construction will deliver an improved investment outcome to investors compared to the more benchmark aware approach of MFS.

What will be staying the same?

The Fund’s investment return objective will stay the same: ‘The Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI Europe (Standard) Index (Net Dividends) in AUD over the medium to long term.’

We believe it is important for investors to be able to continue to measure and compare the Fund’s performance against the market even though the JOHCM strategy is benchmark agnostic.

There will also be no changes to the Fund’s management costs of 1.00% pa and buy-sell spread of 0.30%.

About J O Hambro Capital Management Limited

JOHCM is a boutique investment firm with investment offices in London, Singapore, New York and Boston and is a wholly owned subsidiary of BT Investment Management Limited.

JOHCM actively manages a range of different global and regional equity investment strategies. As at 31 December 2017, JOHCM has £31.3bn of assets under management across 23 equities strategies covering UK, US, Europe, Japan, Asia ex Japan, global and emerging markets. Over 85% of JOHCM’s strategies are currently ranked within the top quartile of their respective industry peer groups.

A letter has been sent to existing investors and advisers, with clients invested in the Fund, providing additional information regarding the change of investment manager.

Equity markets, particularly in the US, have been in a well-established bull run accompanied with very low levels of volatility. In fact, the S&P 500 had not experienced a greater than 5% drawdown over the 18 months to January 2018. This bull market has been facilitated by concerted efforts from central banks to provide freely flowing liquidity. After such a long cycle it is not unusual to see a spike in market volatility as investors’ sensitivity is heightened in anticipation of a change. We saw this in early February, with the catalyst being a jump in inflation expectations in the US.

The following provides thoughts from each of our investment boutique heads on the implications for markets and how they are responding.

Australian equities

The Australian market’s fall in early February reflected an adjustment in relative valuations with the US, rather than concerns specific to our market. There are also signs that the selling was exacerbated by some investors scrambling to unwind their low-volatility positions. Despite this, the size of the decline was lower than for the US, given Australia’s more defensive character. These falls were followed by a reasonable rebound, resulting in a 0.3% return from Australian shares for the month of February.

The recent company reporting season revealed quite a different scenario. Earnings growth for industrial companies, in aggregate, was around 9% which exceeded market estimates and we have seen a net upgrade to consensus forward earnings expectations. It is earnings growth that has driven the market’s returns over the past year. A number of companies have reported resilient operating conditions and we expect earnings growth of mid-single digits this year. Add the return from dividends and we can expect to so total returns in the high single digits for the year.

We believe the market’s rating will be supported at current levels, which is underpinned by several factors:

• Valuations are not excessive. The 12-month forward P/E for the S&P/ASX200 is slightly higher than its historical average, but consistent with the low interest rate environment with the RBA showing no indication of a material policy shift in the near term.

• There is no sign of a recession. Australian growth remains muted, however tailwinds are emerging, such as the rise in corporate capital expenditure and the large pipeline of infrastructure. In combination with a small pick-up in mining investment and a housing slowdown which remains moderate and controlled, we think the Australian economic outlook remains reasonable.

• Inflation in Australia remains benign. The monetary conditions in the US do not reflect the situation in Australia, where inflation remains muted and the RBA has given no indication of aggressive hiking.

• Liquidity withdrawal remains modest. The withdrawal of liquidity from the equity market as a result of central bank actions does present a risk to valuations over the medium term. However, we expect this trend to be moderate globally. The US economy has displayed a historical sensitivity to bond yields and we would expect the Fed to temper their tightening efforts if there are signs of an inordinately adverse effect on growth.

“Bouts of volatility can provide the opportunity to pick up stocks we like at an attractive buying point.”

Crispin Murray, Head of Australian Equity Strategies

As active managers, market volatility creates mis-pricing – and more mis-pricing means more opportunities. Any change in volatility does not typically change our fundamental view of the market and where we see compelling investments. For example, at the moment we see the disruption of long-standing industry structures and business models as a key area of opportunity. Likewise, we also hold some previously unloved stocks where we think the market has not yet appreciated a turnaround in earnings. We also see some opportunity among those growth stocks which have not been pushed to challenging valuations. Bouts of volatility can provide the opportunity to pick up stocks we like at an attractive buying point and our large and experienced team looks to take advantage of these moments as they occur.

Global equities

The US earnings season commenced in late January and indications to date show no material shift in the operating environment for industrial companies. According to data based on 90% of S&P500 companies that reported quarterly earnings, 79% of those exceeded the market’s consensus estimates. The group has on average delivered 14.9% earnings growth over the prior period and commentary from management has been generally favourable. Against this backdrop it is difficult to call the February correction in share prices as anything other than a realignment of valuations. The fundamentals of a bear market are just not there.

“Rather than be concerned over higher future interest rates, we would seriously question the quality of companies that have not taken advantage of ultra-low interest rates.”

Ashley Pittard, Head of Global Equities

We take the proposition of higher interest rates in the US this year as a given, and inflation will find its way in a lagging fashion. Returns from global equities are likely to remain positive this year, although we expect a greater degree of divergence in fortunes across markets and geographies. In broad terms we expect:

• A story of two halves – Global equity markets are likely to experience a strong first half, buoyed by strengthening economies and the broad-ranging boost of Trump’s corporate tax cuts and incentives. These conditions are likely to force the hand of the Fed and interest rates will rise ahead of market expectations for the year and weigh on equities. Hence, returns should be similar to their longer term average.

• US and European companies are well placed to continue to do well – Earnings reports are continuing to show that companies are operating well. Europe has entered their earnings season and given the synchronised growth globally for the first time in a decade, European corporates should deliver similar aggregate results to their US counterparts.

• Aussie dollar stability – The Australian dollar is likely to be range-bound in the US$0.75-80 band as we have seen over the past five years, which shouldn’t have a material impact on returns from global equities.

• Market valuations in select areas to remain attractive – Although the market has rallied, certain industries remain fundamentally attractive. Consider that US banks are trading below 1.3x book value, while pharmaceuticals are on an unchallenging PE ratio of 10x.

What is more of interest to us is balancing the assessment of companies that are achieving operational excellence and are using the buoyant economic conditions to generate strong cashflow. Rather than be concerned over higher future interest rates, we would seriously question the quality of companies that have not taken advantage of ultra-low interest rates to skilfully deploy capital and grow their businesses. We give merit to companies that have shown the ability to command a dominant position in their industry. They are much better placed to show resilience in varied market conditions.

Bond markets

Over the past year the market has been focusing on forward indicators of consumer sentiment and US economic growth such as manufacturing and services sector outputs to support expectations of economic growth. These have been in a generally positive trend over the past few years, however, consensus expectations of higher inflation have failed to materialise. We think that inflation will surprise on the upside this year but we are weary of expecting too much of a rise until we see sustained wages growth coming through. Pent-up expectations to seize upon the first signs of inflation was taken by the market as a precursor to inflation rising from stagnant levels.

“We are cautious of expecting any meaningful pick-up in inflation until we see the whites of its eyes.”

Vimal Gor, Head of Income & Fixed Interest

Whether a benign inflation outcome can continue is the subject of much debate. We are cautious of expecting any meaningful pick-up in inflation until we see the whites of its eyes. What is of significance to markets is if central banks expect inflation to pick up and continue to unwind their unprecedented monetary stimulus. This is a real possibility in the US given that there are two major fiscal forces now in play – company tax cuts and an extension of the debt ceiling. It is exactly the wrong time to be adding stimulus when the economy is running at near full capacity. We believe this will force the hand of the Federal Reserve to counter the inflationary impact, which will be negative for bond yields as the yield curve steepens. The risk then arises that this compensatory tightening will lead to recession in late 2018 or in 2019.

In the shorter term, we expect:

• Higher volatility for both equity and bond markets – Historically, heightened inflation expectations have been followed by a pattern of higher market volatility.

• Investment grade credit to outperform sovereign and high yield debt – Segments that benefitted strongly from the global wave of liquidity are now the most vulnerable areas of the credit world. This includes certain emerging market sovereigns and high yield corporates. An unwinding of favourable market conditions may be particularly unkind to these areas versus more structurally resilient investment grade credit.

• Australian inflation to lag the US – Inflation in Australia will surprise on the downside. Hence, the RBA will need to closely watch unemployment and wages growth before it can consider any pre-emptive strike against inflation. We find it difficult to build a scenario where the cash rate rises while wages languish and spare capacity remains.

Looking more broadly, the easy financial conditions and fiscal support from the past decade have left a legacy of debt, which raises concerns over financial stability and ultimately results in higher levels of market volatility going forward. We are positioned to capitalise on this environment with tactical exposures to investment grade credit.

Asset allocation

It is important to put bouts of market volatility into context. Markets have experienced strong gains in the last few years so a correction like the episode in February was inevitable. However, what market volatility does illustrate is the importance of a well-diversified portfolio. While equities are a critical component in delivering long-term growth to a portfolio, this exposure needs to be balanced by assets that are diversifying – bonds, foreign exchange exposure and alternatives can all help to stabilise returns.

“One interesting feature of the recent sell-off is that bonds, in general, failed to provide a cushion against market volatility.”

Michael Blayney, Head of Multi Asset

Each episode of market volatility is different. For example, in the global financial crisis the correction was led by credit, with equities following and government bonds providing capital gains to help insulate portfolios. One interesting feature of the sell-off (although a very small correction compared to the GFC) is that bonds, in general, failed to provide a cushion against market volatility.

In a “normal” equity market sell-off, government bonds benefit from a ‘flight to quality’ effect, as investor demand for bonds increases. As the most recent volatility was initially triggered by fears of inflation and rising interest rates (poor conditions for bonds) this caused US bonds to sell off (with Australian bonds mixed depending on the term). The reaction in credit markets lagged equities, and while spreads widened, eventually there was no sign of panic, with investors exhibiting greater focus on strong underlying corporate fundamentals than shorter term equity market volatility.

While we believe that bonds are an important component of a portfolio, this instance of market volatility also illustrated the importance of holding both foreign currency and alternative assets – when one of your stabilisers fails to provide the desired protection it is important to have others. Currency exposure was particularly valuable in this instance, with the recent fall in the Australian dollar from US$0.81 to below US$0.78 providing a cushion to market volatility. When the Australian dollar falls in value, assets denominated in foreign currency become more valuable for Australian investors.

Recognising the inherent uncertainty of financial markets, we continue to hold a broad range of diversifying exposures to seek to smooth out inevitable bumps in the road.

Fund Manager commentary for the month ended 28 February 2018 covering market reviews, BT Investment Management fund performance and outlook for the period ahead.

Access the commentary here.

The February flash crash served as a warning shot to the market to expect further volatility ahead. The goldilocks narrative of strong growth with benign inflation morphed into ugly inflation and deficit concerns in the US, driving bond yields higher which dragged equity markets lower. Within five trading sessions, the S&P 500 index undid the melt-up of the first three weeks of the year, and by the close of the 8th of February, the market was down over 10% from the peak.

In this Newsletter I take a close look at how global FX markets have been behaving and delve deeper into the prevailing narratives currently underpinning a bidless environment for the US dollar.

View the newsletter here.

“Ramaphosa inherits stagnant economy and divided party”

Financial Times, 15 February 2018

One of the unfortunate facts of emerging market investing is that emerging market political leaders who come to power with promises of much-needed reforms tend to disappoint. Even in the last few years, leaders from Jokowi in Indonesia to Enrique Peña Nieto in Mexico have started their leaderships with significant progress but subsequently disappointed (“Jokowi’s 35,000MW electricity program only reaches 3.8% progress” – Jakarta Post, 4 March 2018; “Release of jailed union boss reveals Mexican president’s empty promise” – Guardian, 21 December 2017).

The latest new national leader to promise a break with the past is South Africa’s Cyril Ramaphosa, elected the country’s president in February following the resignation of Jacob Zuma after a raft of corruption allegations. From the December 2017 confirmation that Cyril Ramaphosa would replace Jacob Zuma to the February 2018 transition of power, the South African rand rallied 14.0% against the US dollar, reflecting optimism for political and economic reforms under a Ramaphosa administration. In particular, his decision to recall previous ministers Nhlanhla Nene and Pravin Gordhan (both sacked by Zuma) suggests improved prospects for economic policy and governance.

However, it is our view that South Africa faces serious economic challenges with no obvious solutions, while the broad political grouping that is the ANC will further constrain the new Government’s ability to act.

We regard all incoming EM political reformers as ‘show-me’ stories, but this is particularly true of Cyril Ramaphosa, as we cannot even see the reform path that would turn South Africa around.

The most serious problem for South Africa is its failure to generate economic growth. The National Development Plan requires a 5.4% economic growth rate to make a serious dent in the country’s 27% unemployment rate. Growth in the last five years has averaged 1.4%, and consensus expectations are for 1.5% in 2018 and 1.7% in 2019. There are various reasons for the poor growth rate, but South Africa’s failures in the last 20 years to support both infrastructure and education are particularly to blame. While the recent water supply shortage in Cape Town has attracted the most news coverage, a chronic undersupply of electrical power has had far worse effects on business and the economy. To address either the infrastructure or education problems will take large sums of state investment as well as considerable time, which make improvements seem simply impossible.

The South African fiscal budget remains materially stretched. The fiscal deficit is estimated to have been 4.3% of gross domestic product (GDP) in 2017, Fitch and S&P cut South Africa’s sovereign credit rating to junk last year, and Moody’s put the country on review for a credit downgrade in November 2017 (which is expected to be confirmed later this month). Meanwhile, parastatals like electricity power utility, Eskom, face financial distress. Eskom has recently sought ZAR20 billion (AUD$2.15 billion) in emergency credit from the Government just to remain operational. The higher education sector needs an additional ZAR 12 billion (AUD$ 1.3 billion) in financing this year.

In addition, the good news of the appointments of Nene and Gordhan is balanced by the problematic appointment of David Mabuza as Deputy President. Being an old ANC party insider from the struggle against apartheid, Mabuza has been the subject of very serious allegations in the last few years, including links to corruption and violence. The Ramaphosa administration is emphatically not a clean break from the Zuma years.

We regard all incoming EM political reformers as ‘show-me’ stories, but this is particularly true of Cyril Ramaphosa, as we cannot even see the reform path that would turn South Africa around. We remain cautious on the South African economy and currency, and prefer to invest in South African companies doing most of their business in other emerging markets.

Each year on the 8th of March, women the world over commemorate International Women’s Day. This year marks the 110th anniversary of the movement, and the fundamental reason for its existence is just as relevant today. Gender equality has long been an issue facing society and progress has been iterative. Pendal’s Head of Responsible Investment, Edwina Matthew, provides a detailed insight into not just the social imperative, but the economic value to corporations in adopting a broader focus on diversity that actually extends beyond the gender divide.

Diversity is an issue with growing prominence across corporate enterprises. Although the issue most readily raises a connection with gender equality, the concept of diversity has broad-reaching demographic variants that cover gender, age, ethnicity, religion, and much more. Collectively, these form a nucleus of economic value for a business that leverages diversity from the board level right through the company’s organisational structure.

Widening the lens

Historically, diversity within the business community has tended to be thought of as an “insurance policy” against brand or reputation or operational risk. More recently, diversity has become an important social and governance issue, heralding an era of closer scrutiny by customers, shareholders and other stakeholders on behaviours and actions of corporate leaders. Increasingly, companies need to earn a social license to operate from both internal and external sources.1

From an investor perspective, the focus on diversity may be linked to management quality, to others it may represent awareness of particular stakeholder priorities, while for others it may be associated with expected benefits related to fewer instances of bribery and corruption . Regardless of the motivation, recent trends across the investment industry have helped to widen the lens on diversity.

Building the (“smart”) business case for diversity

There is a growing body of industry reports and academic research supporting a connection between diversity and shareholder value. A 2016 Credit Suisse study found a positive relationship between gender diversity and return on equity. Their research suggests companies with at least one female board member earned an annual excess compound return of 3.5% over the MSCI All Country World Index since 2005.2

Looking at diversity from another direction, studies have also found a positive link between increasing participation of women in labour markets and a sizeable improvement in GDP and world leaders are taking note. Canadian Prime Minister, Justin Trudeau, has spoken strongly on the need to address the gender imbalance “not just because it’s the right thing to do, or the nice thing to do, but because it’s the smart thing to do.”3

In Japan, Prime Minister Shinzo Abe introduced a program (“womenomics”) incentivising Japanese companies to hire more women, especially at levels of leadership in an effort to alleviate pressures on the Japanese economy in relation to the nation’s aging population.

Diversity and the generational dollar

Another demographic influence supporting the business case for diversity is the growing influence of the millennial generation as consumers and members of the workforce. By 2025, millennials are set to make up 75% of the global workforce, revolutionising businesses from both an employee and consumer perspective.4 A number of studies report that millennials place a higher value on diversity than older generations and they actively look for diversity and inclusion programs in their prospective employers before making a job decision.5 This and other studies highlight the imperative for businesses to cater to the expectations of this generation, not only as employees, but as customers.6

Diversity and disruption

Today’s rate of technological change is a form of disruption and is challenging many business models. Advances in technology can ironically introduce the potential for unintended bias, including gender bias. For example, despite the technology intensity and specialist skills deployed in developing Artificial Intelligence, there is actually a role for corporate governance and ethics-based oversight. Companies need to better understand consumer patterns and need to design gender-neutral products that also work for 50% of the population.

For the sceptics, there are plenty of examples through history of what can happen in technology when homogenous working environments fall prey to group think. Take the example of the early incarnations of air bag design for automobiles. Researchers suggest a fundamental lack of diversity goes some way to explaining failures of the technology which resulted in casualties. Consider that the engineering and automotive design professions were heavily dominated by males, who only consulted height, weight and body structure metrics for the average male. This approach overlooked suitability for females and children who are naturally different in stature.

Diversity applies beyond the board room

Diversity is becoming an important attribute for analysing the effectiveness of boards and senior leaders of companies. Bringing a team together with differing views and experiences can and should lead to rigorous debate and stress testing of proposals at the board and management level. Leaders need to be conscious of their own biases and demonstrate objectivity in making decisions.

“It’s the combination of diversity and inclusion initiatives that drive sustainable organisation change and thus deliver the diversity dividend”

Edwina Matthew, Head of Responsible Investment, Pendal Group

However, to be successful, a diversity policy needs to go beyond the boardroom. Without education and reinforcement on the value to the company it merely forms a discretionary guideline and can be tokenistic in nature. A company that fails to empower people to share ideas and debate initiatives risks failure in innovation. In other words, it’s the combination of diversity and inclusion initiatives that drive sustainable organisation change and thus deliver the diversity dividend.

Asset owners share the prerogative

The growth trend of adopting responsible investing principles is promoting a focus on diversity within company engagement and proxy voting activities. In its analysis of the 2017 proxy voting season, PRI noted diversity-related shareholder resolutions as one of the three key global environmental, social and governance (ESG) themes in 2017. Regnan (leading Australian ESG data, research and engagement service provider) also notes growing attention to diversity as an engagement theme locally.

This week (8th of March) the world celebrates 110 years since the campaign behind International Women’s Day began. This year’s theme is #PressforProgress in support of gender parity. However, this call to action could also apply to a broader definition of parity. Attitudes are shifting as companies, policy makers, asset owners and consumers all come to understand the negative effects of a diversity deficit. All along the investment chain we are witnessing a greater sense of shared responsibility for ESG issues, and pressing for progress on diversity is a priority.

The bottom line

A company’s approach to diversity can be an important indicator of overall business resilience and management quality. In this new era of heightened stakeholder scrutiny, combined with the growing social conscience of the younger generation, means that explicit attention to ESG issues such as diversity will continue to increase in importance. Organisations that pursue diversity-smart leadership, operations, product design and technological innovation and take the steps to capture the opportunities it offers, will be better placed to understand the world in which we operate, better able to identify the risks and opportunities, and ultimately achieve better business outcomes.

This article is an extract of a more in-depth discussion on the social and economic value of broadening diversity practices.

1. In October 2017 the European Securities and Markets Authority (ESMA) announced new diversity disclosure requirements for large, listed companies in the European Union. In Australia the ASX Corporate Governance Council requires explicit disclosure on progress towards achieving measurable diversity objectives for all Australian listed companies. The United Nations supported Principles for Responsible Investment (PRI) is actively working in partnership with a number of other UN initiatives to assist stock exchanges around the globe enhance the quality and quantity of reporting on gender-related factors.

2. Credit Suisse, “CS Gender 3000: The Reward for Change”, 2016.

3. World Economic Forum, “Justin Trudeau’s Davos address in full”, Davos, 23rd January, 2018

4. Catalyst, “Generations: Demographic Trends In Population and Workforce”, 20th July 2017

5. PwC, “Millennials at work: Reshaping the workplace in financial services”. A survey conducted in the US by the Institute for Public Relations in 2016 found that nearly half (47 percent) of the millennials surveyed actively look for diversity and inclusion programs in their prospective employers before making a job decision.

6. Macquarie Research, “Millennials – more to invest in than avocados”, 19th June 2017

We often like to highlight our “common sense business person’s approach” to investing. We are contrarian by nature and focus on the leading businesses in areas that are out of favour, facing change, or are depressed in the near term. Since the launch of our Concentrated Global Share Fund in 2016, no industry sector represented this better than the old media pay television space in the US. The sector serves as an interesting case study on the merits of buying quality assets at or below their replacement value.

We have all read the doom and gloom about “cord cutting” and millennials preferring Netflix over traditional cable and satellite services. But what some may not be aware of is the rich hunting ground this industry has been for our Fund, with two takeover offers within the last year. When we launched the Fund, our thesis was clear: Pay TV content channels need to consolidate as scale is becoming more and more important.

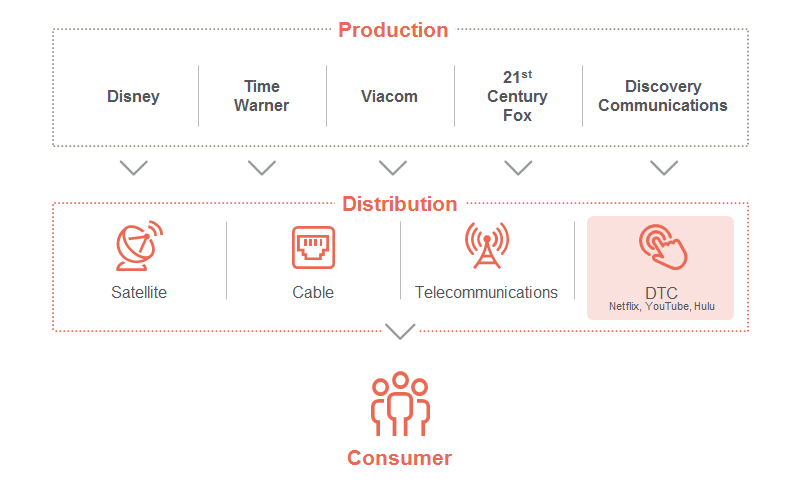

The value chain of the media industry below highlights the shifting balance of power between the content generators and distribution platforms to the consumer, with the Direct-to-Consumer (DTC) paradigm providing opportunities for the content producers to encroach on the platform territory and better target content to the end consumer’s preferences. Historically, consumers paid a premium to access bundled channel content through distributors. With the DTC model and disruptors like Netflix and YouTube coming to the fore, the distributors are progressively dismantling their ‘fat’ bundles to offer ‘skinny’ packages that are more tailored and competitively priced. This dynamic naturally has implications for the content generators, which is playing out through a wave of merger and acquisition activity.

Media value chain – content is king!

This consolidation dynamic is true not just in television but across many sectors. We have witnessed significant consolidation themes play out over the past two decades across different industries which we have held in our portfolios. But what has remained constant is our focus on identifying unique, high quality assets and then having the patience to let our thesis play out. This is the core foundation of our contrarian philosophy.

Our journey through media ownership

At the time of our Fund launch we only held one investment in Media, being Time Warner Inc. (TWX). We loved Time Warner’s unique asset base, with one of the world’s leading news channels (CNN) and premium drama content via HBO. It was no wonder that in July 2014 Rupert Murdoch tried to purchase the business but was rebuffed. Time Warner is more than just CNN and HBO, the company has a suite of fully scripted channels that include TBS, TNT Sports, Cartoon Network, and a blockbuster movie studio centred on the Warner Bros and DC Comics franchise.

Time Warner – operating divisions

In October 2016 AT&T made a $107.50 share offer for Time Warner which valued Time Warner shares at a multiple of 19.5 times (x) its 2016 earnings per share and a 12.4x enterprise value multiple (EV/EBITDA). The consideration was an equal proportion of shares and cash representing a premium of 40% to the prevailing share price at the time. On completion, Time Warner shareholders would own 15% of the combined company.

Following the bid, we used the strength in the stock price to sell our entire position in Time Warner. We believed the bid fully valued Time Warner and also held the view that AT&T could face an uphill battle with the Department of Justice (DOJ) Antitrust division to obtain requisite approval for the merger. As an aside, the DOJ has recently filed to stop the bid and now it is heading to the courts for resolution.

The proceeds we realised from the sale of Time Warner were redeployed into 21st Century Fox. This is a common theme in our Fund whereby we look to realise investments that have reached their intrinsic value. We then look for other opportunities within the industry with similar unique premium assets that are hard or impossible to replicate and are trading below their replacement or build value. 21st Century Fox (“Fox”) fit that criteria and we invested.

Consistent with our prior media investments, we place considerable value on the Fox assets. The company was formed through the spin-off of News Corporation’s publishing assets in 2013 and operates a broad collection of businesses across cable network programming, filmed entertainment, television, and Direct Broadcast and Satellite TV. The company’s television assets are primarily focused on news and sports content, together with entertainment programming through FX Networks and non-fiction science and exploration content through the National Geographic channel. The prime assets of the company are its Fox News and regional sports networks, which hold leading positions in their categories in North America. Outside of its home region, Sky Plc holds the number one position in the UK; Star India distributes content through over 40 channels across India and more than 100 other countries; and National Geographic is a global leader in its space, reaching over 440 million homes in 171 countries and broadcasting in 45 languages.

Fast forward to December 2017 and another stalwart of the media world, Disney, launches a bid to buy the majority of Fox’s assets in an all-stock transaction for US$66.1 billion (A$88.0 billion) including debt of $13.7 billion. The deal represents an 11.9x calendar 2018 EV/EBITDA valuation for the assets sold, leading the stock to rally more than 40% from its recent November 2017 low. The assets to be sold include Fox’s Film and TV studio, FX Networks, National Geographic, Fox Sports Region Networks, Fox Networks Group International, Star India and Fox’s interests in Hulu, Sky, Tata Sky and Endemol Shine. Prior to acquisition, Fox will spin-off its remaining assets into “New Fox” including the Fox Broadcast Networks and TV Stations, Fox News Channel, Fox Business Network, FS1, FS2 and the Big 10 Network.

Time once again to take profits

Following the Disney bid we reviewed our thesis and decided once again to use the strength in the stock price to sell our whole position in Fox. We believed the bid fully valued the business and longer term, we believe that New Fox, which will be effectively run by Rupert and Lachlan Murdoch, will merge this entity into News Corp’s newspaper businesses. We believe that such an entity does not represent a premium unique asset as newspapers today are a highly commoditised business, heavily disrupted by digital formats and have little or no pricing power. The sale represented an average holding period gross return of 18.5% (before fees and taxes) for our investors.

The realised proceeds from the sale were once again redeployed into the sector, this time Discovery Communications (DISCA) was the recipient. Discovery operates a portfolio of premium non-fiction, lifestyle, sports and kids programming brands. Content is distributed to more than three billion cumulative viewers across pay-TV and free-to-air platforms in more than 220 countries and territories through highly recognised and endorsed channels.

Discovery Communications – brands suite

Source: Slideshare

We have been closely following Discovery Communications for some time as it also offers a unique set of assets, difficult to replicate and occupies the number one position within the non sport male demographic within the US pay television market. The company has engendered some strong leadership positions in distinct segments, such as the Oprah Winfrey-lead OWN Network with a strong following within the female African American demographic, and Europe-focused sports programming and broadcasting through its Eurosport business.

Apart from Discovery’s unique content, its share market valuation is compelling. Discovery Communication trades at a current PE of 9x, has significant excess depreciation and trades on an 8x 2018 EV/EBITDA, which represents a 50% discount to the two most recent private market takeover prices. Additionally, the synergy benefits from their recent acquisition of Scripps Network, which operates the HGTV, Food Network and Travel Channel subscription offerings, would represent an additional 15% of their total cost base and contribute double-digit earnings over time. We believe there are no competitors capable of replicating their library or asset base at such extreme valuations, even though we do acknowledge that it does face headwinds with consumers cancelling subscriptions and becoming more selective about the content for which they pay. They are losing traditional pay television subscribers and need to get into a ‘skinny’ lower priced bundle package. But beyond the short term, we believe if you have superior content, media companies will go direct to the consumer, similar to what Netflix have done with their original “House of Cards” content.

Discovering value

Part of our investment philosophy is to look for businesses that have an owner-operator management mentality. They are in tune with commercial and operational facets of the company and hold significant financial stakes in its success. John Malone — a pioneer in the US cable business and the largest owner of US private land — is Chairman of Discovery’s board and is its former CEO and founder. Malone has visibly backed his convictions through doubling his stake in Discovery in December, increasing his share in Discovery by 30% to become the largest individual shareholder. His combined stake in the company is now worth in the vicinity of US$400 million. Malone’s position clearly fits our criteria which adds to our conviction in Discovery.

It is worth recalling comments from a November 2017 interview with CNBC where John Malone articulated his views on the media industry which aligns with our longer term view. According to Malone, “Scale [is] even more important in a media business where scale always was important. So it’s all about scale … can Netflix get enough scale that nobody really can challenge them?”

BT Concentrated Global Share Fund – media sector investments

Source: BTIM, Bloomberg

Re-shaping the media landscape

It is still too early to speculate how the remaining assets in the media landscape will play out, but it is obvious to us that superior content will increasingly be delivered direct to consumers via an app on multiple devices, and failing this, takeovers will increase over the coming decade. Viacom will most likely merge back with CBS and Discovery may find a home with a larger content provider. Ultimately, the cable distribution providers are likely to converge with the telecommunications providers as 5G spectrum deployment quickens.

Across our investments in media content generators, a common rationale for the purchase decisions was the ability to buy these assets at prices below the replacement value of their content library.

“[Discovery] have good brand recognition globally and he owns all of his content. He doesn’t just license it, he actually creates it, produces it and owns it, all rights in all markets”.

John Malone, Chairman of Liberty Media entities and board of Discovery Communications

We have bought different viewership segments that are leaders within their category and have allowed the time for their value to be appreciated. Our latest investment in Discovery Communications continues that theme. It is a leader in the non-fiction 18-40 year viewership bracket and despite its below-par valuation, is generating a return on equity of over 130%. We recognise the intrinsic value of the growing content library which, once created, becomes an asset that can be syndicated through other platforms or via DTC approaches to generate additional revenues for little further outlay. The same dynamic doesn’t apply to the platform providers who are increasingly reliant on the content kings.