BT Concentrated Global Share Fund (APIR: BTA0503AU, ARSN: 613 608 085) – Important information

Reduction in management costs from 1 March 2018

With effect from 1 March 2018, the Fund’s management costs will reduce.

The management costs are currently made up of an issuer fee of 1.25% pa. The issuer fee will reduce to 0.90% pa from 1 March 2018.

Fund Manager commentary for the month ended 31 January 2018 covering market reviews, BT Investment Management fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Irony – A figure of speech in which the intended meaning is the opposite of that expressed by the words used; usually taking the form of sarcasm or ridicule in which the laudatory expressions are used to imply condemnation or contempt.

“The Walrus and the Carpenter were walking close at hand; they wept like anything to see such quantities of sand: ‘If this were only cleared away,’ they said, ‘it would be grand! If seven maids with seven mops swept it for half a year. Do you suppose,’ the Walrus said, ‘that they could get it clear? I doubt it,’ said the Carpenter, and shed a bitter tear.” Lewis Carroll, The Walrus and The Carpenter

Why we underperformed in 2017

2017 was a tough year for the Pendal Wholesale Asian Share Fund. I’ll recap the main reasons for the underperformance, not just so that I have it in one place (I’ve commented on some of the mistakes in my monthlies last year), but also for me to reflect on and explain what I’ve done to the portfolio since.

As you are aware, I do own cyclical businesses in our portfolio. However, compared to the index, which has perhaps a 40-45% weighting, I own no more than 25%. In 2016, I had started increasing my cyclical position closer to 20-22%, but in a year like 2017 with a huge cyclical-biased rally, I will underperform. The reason I own cyclicals is to lessen the underperformance during a cyclical recovery. Shares of quality and defensive-oriented businesses generally do not perform as well in a year in which we have cyclical rallies. Some clients have asked if I would increase the weighting in future to mitigate this risk. It’s unlikely for the simple reason that cyclical turns are macroeconomic events and therefore difficult for me to predict. In my opinion, cyclical stocks do well (most of the time) because of a change in risk perception, not because they are good businesses to own.

In my opinion, cyclical stocks do well (most of the time) because of a change in risk perception, not because they are good businesses to own. Samir Mehta – Senior Fund Manager, J O Hambro Capital Management

Unfortunately in 2017, the timing of my stock-specific mistakes in my core holdings coincided with the powerful cyclical rally. In the past when I’ve made mistakes, they were usually compensated by my other stock holdings performing equally well or better. That was not the case last year. Not just the cyclical rally but its narrowness played against me as an all-cap fund.

Tilting towards financials and materials

As to the current portfolio, you will observe that I made a reasonable tilt towards the financials and materials sectors in 2017. In the past, both were poorly represented in our fund. Financials should generally benefit from low valuations, falling risks on non-performing loan (NPL) provisioning, falling risk of regulatory fines, rising loan growth and possibly higher margins leading to sustained earnings growth. A sweet spot, if any could be defined. Materials, on the other hand, are benefiting from an anti-supply shock in China. In terms of countries, North Asia and select exposure to Malaysia and Indonesia reflect my confidence in the global economic recovery, as well as the possibility of this rally broadening out from the narrowness we experienced last year.

On the topic of materials, let me reflect on the events of the past two decades, which help put things in perspective. China’s accession to the World Trade Organisation in December 2001 was a watershed moment. Around that time, the US was dealing with the fallout of the internet bubble, while Asia was cleaning up after the Asian financial crisis of 97/98. The Greenspan-led Federal Reserve cut interest rates aggressively to counter slowing GDP growth. American corporates were keen to outsource to China in order to reduce costs. China’s vast land mass, cheap exchange rate and unlimited labour pool set in motion the long bull market in most assets from 2002/3 onwards.

I attribute a demand shock from China to be one of the foremost reasons for that bull market in commodity prices. As China’s economy grew, capital flooded in, infrastructure investments picked up; cheaper and easier access to credit fuelled a concurrent rise in consumption as well. Some people compared it with Japan’s industrialisation, only much bigger in scale. In the early 2000s, as global growth went on steroids, commodity prices in particular rose very sharply. Of course, that was before it all nearly ended with the 2008/09 crisis.

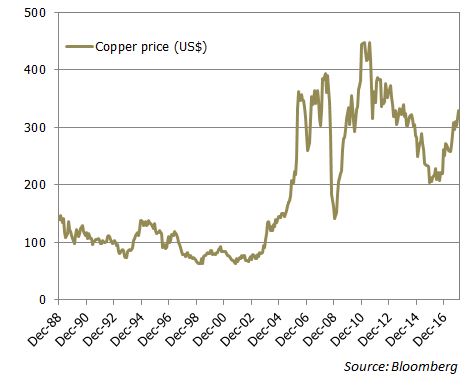

Copper is the new gold

Too much stuff

A supply response did emerge for commodities and metals. Most projects planned and implemented during the boom fructified between 2008 and 2013. Commodity prices remained elevated after the 2008/09 crisis, thanks in no small measure to the gigantic stimulus plan by China and the QE policies of central banks across the world. However, by 2013, as the Federal Reserve spoke about ‘normalising’ policy and the effects of the stimulus started to wear down, excess supply was in plain sight. What was once a demand shock was now blighted by supply excess. Everywhere you looked, just like the Walrus and the Carpenter, you could see just too much stuff. China’s severe downturn in 2015/16 gave rise to the possibility of widespread deflation. As industrial China floundered, the country’s banking system came under stress.

In my view, the Fed’s decision not to raise rates in March 2016 was in hindsight the pivotal turning point for China, the global economy and commodities in general. It allowed the Chinese authorities breathing space to deal with capital outflows that were snowballing into capital flight. Subsequently, a clampdown on outflows and a bit of economic stimulus helped stabilise demand. Regardless, the added positive for commodity prices has been a desire to control pollution in China and the associated supply side reforms. This has led to a significant shut down of capacities in steel, cement, coal and aluminium, in particular.

A Chinese supply-side shock

The dictatorial fiat – what in normal times is considered anathema to capitalism – was in this case a boon for capitalism. We know that in North Asia (Japan, Korea and China) businesses were driven more by market share ambitions rather than by generating the highest return on capital for their shareholders. This attitude, combined with cheap access to capital and the state’s desire to grow GDP at any cost, resulted in over-investment in several industries. If the Chinese government does maintain its focus on pollution, which then translates into more discipline on future expansion, the result will be lower GDP growth (as fixed asset investments grow at a slower pace) but much better cash flows and profits. A demand shock from China caused the first boom in commodities; ironically, an anti-supply shock from China is driving commodity prices higher now. So far, there is evidence that the clamp down on industries to reduce pollution, especially in and near the big cities, is genuine. Take the cement industry as an example.

Cement prices – at levels not seen for years

I started buying China’s Anhui Conch, one of the largest cement manufacturers, in March 2016 as part of our contrarian approach to cyclicals. As cement prices have climbed, profits for cement companies are running at levels not seen since 2011. Fear drove price-to-book multiples in 2016 to extremes; I’m hoping that greed will drive the price-to-book ratio to well above mean levels at a time of rising book values. If the government stays firm on capacity controls, that outcome is likely some time later this year, in my view. I’ll be happy to give the stock away to those who are fearless then.

Anhui Conch – fear no more

“Alibaba: We reiterate OW rating and raise our TP to USD 270”

Broker report, February 2018

Different perceptions of the value of an asset are at the heart of capital markets and are the key to active investment management. For any given investment process, there will be periods when the consensus view seems to be completely unjustifiable and must be opposed. For us, this is such a time. Here are three significant mispricings in the current emerging market asset class, all relating to the very largest stocks in the asset class.

Firstly, the disconnect between Chinese internet company Tencent and its South African shareholder Naspers. We feel the Tencent business model is one of the strongest in the world. Whilst its total addressable market is smaller than Facebook’s, its core business continues to grow revenues successfully without overly relying on advertising. Against this, though, is the degree to which the share price has outrun earnings. Tencent reached over 40x 12-month forward consensus earnings, which is around the level that has historically formed the upper limit to the stock’s valuation range.

Tencent headquarters at Nanshan Hi-Tech

The valuation situation is different at Naspers, a South African holding company with a 33.2% stake in Tencent. Naspers trades at a very deep discount to its underlying net asset value. At the end of January, Naspers traded at an improbable US$62bn discount to its stake in Tencent alone. That negative US$62b covers US$3.8b of other quoted holdings, US$1b in net debt, and various media and internet assets in emerging markets, including pay television and e-commerce.

“We are as confident in these positions as in any we have ever held.” James Syme, Senior Portfolio Manager, J O Hambro Capital Management

Secondly, Samsung Electronics, which since 2015 has delivered incredibly strong operational performance across its business units and a highly positive set of corporate governance reforms. That performance might be expected to have been reflected in the stock’s valuation, especially with the run-up in the overall price/earnings multiple of the emerging market asset class, but that has not been the case. From 2010-2015, Samsung Electronics traded at an average price/12-month forward earnings discount to the MSCI Emerging markets index of 22.2%, but in the last year that has expanded to 46.8%, with Samsung Electronics at 6.9x 12-month forward earnings, and the index at 13.0x.

Thirdly, within the group of companies that constitute the Alibaba group, the cloud computing business is thought by other analysts to have a valuation that we cannot comprehend. The strong performance of Alibaba shares in 2016 and 2017, well ahead of the growth in underlying earnings, partly reflects increasing confidence in the newer business units the group has launched, including the cloud computing business. That unit had, in the fourth quarter of 2017, revenues of RMB 3.6b (US$553m), up 104% on a year earlier. Unfortunately, the growth was not accompanied by profitability. The reported operating margin for the quarter was -22.0%, down from -19.2% a year earlier. How much might a loss-making business with an annualised US$2b revenue stream be worth?

A review of published analysts’ estimates reveals some robust estimates, with an average valuation for the unit of US$60b. It is this approach to company valuation that has helped Alibaba reach a market capitalisation of US$523b. Our portfolio has benefited substantially from the run-up in Alibaba’s share price, but we cannot justify continuing to hold the stock and have sold our position.

The portfolio’s largest active positions are overweight Naspers and Samsung Electronics, and underweight Tencent and Alibaba. We are as confident in these positions as in any we have ever held. We are invested in our strategy alongside our clients. Nothing can out-run its fundamentals forever.

The year 2017 unexpectedly marked the end of Westfield – at least in relation to the corporate entity that carries the name of well-known shopping centres. On December 7th investors in Westfield Corporation (WFD) received a proposal to merge with the Dutch origin property giant, Unibail Rodamco (‘Unibail’). The deal was consummated by an in-principal acceptance by the Lowy family and directors which valued the company at $33 billion, a 32% premium to the prevailing share price. If the deal meets all regulatory hurdles and shareholder approvals, it will represent the largest corporate merger in Australia’s history.

Unibail itself has an illustrious history as a company. It was formed in 1968, initially as a finance leasing company before winding down this business in the 1990s to establish itself as a commercial property operator. In 2007 the company merged with Rodamco Europe to form a large regional player in European property, representing approximately 16% of the EPRA/NAREIT Developed European Index. The merger makes strategic sense, considering the complementarity of the respective Westfield and Unibail asset portfolios. Unibail’s footprint consists primarily of 71 shopping centres across the region together with 13 office buildings and 10 convention centres in Paris and surrounding areas. Retail property accounts for about 85% of its portfolio.

If the deal meets all regulatory hurdles and shareholder approvals, it will represent the largest corporate merger in Australia’s history.

Westfield’s offshore asset base consists of large shopping centres in the US and the UK, along with development opportunities for new and existing centres, as well as residential apartments. Bringing these entities together will result in a largely retail property behemoth representing US$72 billion (A$96 billion) of assets.

The deal is unlikely to face any material resistance. Westfield’s shareholders will be furnished with independent valuation reports prior to voting on the proposal and can be expected to support the combined scrip and cash offer. There remains a chance that another party could show its hand and conduct a raid on the register, although we see this as a relatively low probability event. The sheer size of the transaction limits the potential bidders to a small handful of property companies with the requisite balance sheet strength. This list of potentials would realistically be limited to the largest US REIT and sovereign wealth funds. With all hurdles being met, the merger should be completed by mid-2018.

The choice for shareholders

The next question on the minds of existing Westfield shareholders is whether their Australian-listed holding will be subsumed into an offshore listing. Under the terms of the offer, existing shareholders will receive around 35% of the value as US$2.67 in cash for each Westfield share held together with the option of receiving the remainder as Unibail Netherlands-listed stock or Chess Depository Interests (CDIs) which will be tradeable on the ASX. It is likely that the majority of Australian domiciled investors would opt for the latter and retain exposure to the enlarged entity. Existing shareholders may hold some concerns over the value of the deal, given that Westfield’s share price has remained below its post-announcement level. However, this is largely a reflection of US dollar weakness and the translation of value for its underlying assets rather than a concern over the deal’s intrinsic value.

Index implications

Despite the loss of an iconic name and major component of the Australian REIT Index, the sale is a net positive for investors as it will reduce the size of the retail sector and improve diversification. Westfield’s representation within the Index under the combined CDI security will fall from around 15% to 5% and the retail sector will fall from 44% to 35%. There is also likely to be some re-weighting into office, industrial and logistics assets from proceeds of the sale. The aggregate cash component is the equivalent of about two years’ worth of capital raisings across the sector, so we’re likely to see a bolstering of capital accounts within the majors like Stockland, Dexus, GPT and Goodman Group.

The aggregate cash component is the equivalent of about two years’ worth of capital raisings across the sector

REIT opportunities abound

Beyond Westfield and the other major REITs there are a number of good opportunities in new segments such as childcare, retirement living and storage. Demand for such assets in Australia is growing along with the well-publicised shortages of child care and accommodation needs associated with demographic shifts. Supply of these assets remains short and the release of Westfield capital will benefit these areas of the market.

Storage is another area with growing demand credentials. This sector’s growth is being driven by issues like cybersecurity and shifts to cloud data storage. An example of operators in this space is Iron Mountain. Our fund recently invested in the company, which provides a range of data storage and document management services. The operational leverage of companies like this is substantial, with limited incremental capital spend required to expand capacity. In simple terms, the company is able to lease out eight cubic metres of lettable space for each single square metre of floor space. Fundamentally, success in property investment is a function of acquiring quality assets and generating productivity and operational efficiency. Iron Mountain clearly fits those criteria.

Investors may look at Barangaroo and associate these mega towers with compensating supply, but over 90% of the three towers is already leased.

The office sector represents another area of interest. Office space in Sydney and Melbourne – the vast majority of index exposure – is operating at supply-constrained levels not seen for many years. Take a close look at Sydney’s CBD and you see a considerable loss of office space, courtesy of some large office buildings being torn down in Martin Place and Hunter Street to make way for the Metro and alternate uses. Investors may look at Barangaroo and associate these mega towers with compensating supply, but over 90% of the three towers is already leased.

Property managers have been reporting buoyant conditions on the leasing side, to the extent that tenant incentives typically associated with long term leases like rent-free periods and fit-out contributions are no longer being offered to entice new tenants. Melbourne’s CBD office space is showing similar space constraints, reflecting a combination of both gains in white collar employment and centralisation of businesses from suburban markets to the CBD. Vacancy rates in the CBD have fallen to close to 6%. Melbourne is seeing a boom in construction activity and while this will ease supply constraints, the lead time to completions is significant. A similar dynamic applies to the Sydney office market.

Value across the REIT sector

The property securities sector has been exposed to the headwinds of interest rate markets, with the US having passed three rate rises since it began the tightening cycle. Further unwinding of monetary stimulus is likely in the US, followed by Europe at a later stage, which casts a shadow over the sector’s relative valuation metrics. Inflation expectations are also starting to reflect in valuations, while a soft domestic retail sector reflects the impacts of household leverage and stagnant wages growth. These amount to notable risks for the sector, but pricing dynamics within the sector sound a more positive tone. In the private markets for direct property, recent transactions have been completed at cap rates – a measure of prospective cash flow yield for the capital outlaid – close to 4%. Cap rates in private markets should translate to support for valuations in public markets.

The Westfield merger is part of a broader global thematic that reflects strong appetite to acquire public market assets. UK-listed property company, Hammerson, launched a bid in December for a smaller UK property rival, Intu, at a 28% premium to its prevailing share price. In the US there will be potential corporate activity in other large mall owners – Taubman, General Growth and Macerich – with activist shareholders on their registers. The operators of large property portfolios are clearly keeping bond market movements in perspective and see longer term value in prime property assets. These dynamics suggest that opportunities for investors are significant, both within and beyond the big names.

We believe that good corporate governance and sustainability is a central factor to a company’s long-term success. To support our investment decision making processes we have developed a comprehensive Responsible Investment philosophy statement to provide guiding principles for our investment teams.

Responsible Investment Philosophy Statement

2018 has started with a bang. First we saw the melt-up and then we saw the crash down. The S&P is virtually unchanged from year-end levels, but the volatility has been massive. To put it in perspective, this was the strongest January performance the S&P has seen since 1989, which was then followed by a brutal selloff which saw cryptocurrencies slammed and the VIX jump from 10 to 50.

In this Newsletter I have a look at the leverage in the system and why volatility is suddenly spiking now.

There is also an addendum where I remember the similarities of these markets to 1994.

View the newsletter here.

One of the most common questions that we get from our investors is why do we not have more exposure to China? We answer investors by saying that while we may not be directly invested in any Chinese listed stocks we do have exposure to China through our investment to Hong Kong Stock Exchange and the US-listed Chinese search engine, Baidu. We also have significant indirect exposure to China through our holdings in technology, beverage, fast food and casino companies. This leads to the second most common question asked by investors: Are you concerned about the high risk of owning casino companies in Macau?

Our Concentrated Global Share Fund is actually invested in two US-listed companies, Las Vegas Sands (LVS) and MGM Resorts International (MGM). Both companies develop and operate a suite of world renowned resorts. They also own a majority stake in Hong Kong-listed Macau casinos, as well as casinos within their US properties. In the case of LVS, they also own the Marina Bay Sands resort in Singapore. Whilst we refer to these companies for simplicity as casinos, in reality this is a misnomer given that both companies are owners and operators of integrated resorts that offer five star hotel accommodation, numerous food and beverage options, retail, convention facilities and entertainment venues, as well as casino facilities.

Both LVS and MGM hold indirect exposure to Macau’s hotel and leisure establishments. LVS’ Macau exposure is through a 70% holding in the HK-listed Sands China Ltd, which accounts for around 50% of total earnings (EBITDA). Sands China has a large market share of around 23% and holds the number-one position in terms of gross gaming revenue (GGR), mass-market gross revenue share (29%), and share of total Macau resort earnings (approximately 35%). MGM, who have the largest market share on the famous Las Vegas Strip, derive their Macau exposure through their 56% holding in HK-listed MGM China Holdings Ltd, which currently accounts for 13% of MGM’s total revenue. This is set to grow after MGM China open their second casino in Macau at the end of January 2018.

Tainted perceptions of Macau

We believe that the perception of Macau’s inherent “risk” by some investors dates back to the significant share price declines experienced by the six HK-listed Macau casinos in 2014. This followed the introduction of smoking bans and a country-wide corruption crackdown in China which saw GGR fall from around US$44 billion in 2014 to US$28 billion in 2016. However, our view is the latter initiative will result in an industry that is able to sustain greater long term growth with higher margins, whilst the former will no doubt result in healthier patrons and staff. In assessing the risks and opportunities in Macau, investors need to look through the lens of the Chinese Government’s underlying agenda for the island to appreciate the context.

Macau’s European heritage

Up until 1999, Macau was a Portuguese colony which was renowned for organised crime, illegal gambling and prostitution. In 1999, Macau was handed over to the People’s Republic of China, and like Hong Kong, became a Special Administrative Area (SAR) of China. In 2000-2002 the Macau Government, under the control of the Chinese Government, issued what resulted in effectively six gaming licenses with 20-year terms.

Today, the only real form of legal gambling in China takes place in Macau. Although there was no exclusivity placed on the six licenses, the Chinese Government has been resistant to issue any further gaming licenses given lack of land availability and a focus on developing additional non-gaming attractions. The tax rate was set at a relatively high 39%, and was reviewed ten years later although no changes were made. Hence, the licensing arrangement for the six concessions has remained consistent since China established control.

Macau consists of three distinct land masses – Macau Peninsula, Coloane and Taipa – connected by bridges and covers 30,000 square kilometres. Macau shares a border with the Chinese province of Guangdong. The Peninsula of Macau was the first area to be developed following the handover to China and today accounts for approximately 40% of Macau’s total GGR and about 30% of property earnings.

Sands China was the first to develop the reclaimed land bridge between Coloane and Taipa called Cotai. They were also the first to develop an integrated resort in Macau, the Venetian Macau in Cotai. Sands China now owns close to 13,000 hotel rooms , four theatres with total seating capacity of over 5,000, an arena with a total seating capacity of 15,000, as well as two million square feet of retail facilities and another two million square feet of conference, exhibition and meeting space. MGM, with only one casino and 580 hotel rooms on the Peninsula, will open their second casino in Cotai with an additional 1,400 rooms. Cotai itself has since become home to numerous integrated resorts and now accounts for about 85% market share of the casino-owned hotel rooms and the bulk of the non-gaming facilities, creating a cluster effect not unlike the Las Vegas Strip.

Changing the Macau tourist dynamic

VIP gambling became a feature of Macau and has certainly been a driver of GGR growth from the time the first casino licenses were issued. The VIP business is divided into direct VIP and junket VIP sources. Direct VIP tours are arranged directly by the hotel, while in the third party model, the junket acts as a ‘middle man’, promoting relationships with wealthy individuals in China, organising their visits to casinos in Macau and extending credit. Both forms involve the extension of credit by either the casino in the case of direct VIP, or the junket for the latter. The junkets are paid a handsome commission for their services by the casinos which equates to around 40-45% of net casino revenue from the group. As a result, VIP earnings margins are around 10% and a lot lower than mass market margins which average 35%.

“The Chinese Government’s longer term agenda is to promote Macau as a family-friendly tourist destination”

The Chinese Government wagered a crackdown on VIP gaming in 2014 to control the illegal flow of money from mainland China and address corruption among the junket operators. At its peak, VIP business accounted for 73% of Macau’s gaming revenue. Today, in large part as a result of the corruption crackdown and the introduction of anti-money laundering regulations, VIP revenue is closer to 50% and the number of VIP tables has been reduced by 35% since 2013. Through this curtailing, the Government has facilitated growth in the mass-market segment, which forms part of the longer term agenda to promote Macau as a family-friendly tourist destination.

In 2016, Macau welcomed 31 million visitors and recorded a higher number of overnight visitors than day trippers for the first time. For the casinos, this is important as the average overnighter spends about four to five times that of a day tripper. Of these, 66% of the visitors were from mainland China and 20% from Hong Kong. Given the proximity, 44% of mainland China visitors come from the neighbouring Guangdong Province, and arrive by ferry.

Yet, penetration of Macau tourism in China is only 2-3% of the 1.4 billion population, significantly lower than Las Vegas’ penetration of 13% of US resident visitors. We believe there are a number of reasons behind the relatively low penetration, including lower average personal income, restricted travel, limited hotel capacity and transport infrastructure bottlenecks. Over time, we expect these issues to present less of a barrier to entry.

Major investments to expand capacity

Today, Macau’s aggregate hotel capacity is 36,000 rooms, with typical occupancy of 85% (>90% on weekends and holidays). Based on current development proposals, we expect this number to rise to more than 40,000 by 2020. In addition, more than US$22 billion of transport infrastructure is also expected to reach completion by 2022 which will significantly change the current tourist dynamic. The new transport links will allow more mainland Chinese from further afield to travel to Macau more efficiently, which will encourage longer stays.

One of the flagship infrastructure projects is the Hong Kong-Zhuhai Bridge, a 55-kilometre link due to open in early 2018 which will be among the world’s largest sea-crossing roads. This will allow passengers flying into Hong Kong Airport to arrive at the Macau border by road in 30 minutes. The same journey currently takes an hour by ferry, which operates infrequently.

Expansion of the five airports that serve Macau and development of the National High Speed Rail Network should also drive increased visitation. Cotai, which currently appears as a giant construction site, will be linked by the Macau Light Rail to allow easy access to all the integrated resorts on Cotai. The growth in tourism will take time, however the Chinese Government has made it clear that transportation infrastructure and the development of the Greater Bay Area (which encompasses mainland China, Hong Kong and Macau) is a priority.

Easing the barriers to entry

Chinese visitors currently require a visa to enter Macau. They can either enter Macau on a Group visa as part of a group tour, or under the individual visitor scheme (IVS). Only the residents of 49 cities within China (21 of which are in the Guangdong province) are eligible to enter through the IVS. With the implementation of new technology at border gates, increases in hotel capacity, expansion of non-gaming facilities and infrastructure improvements, we expect that the IVS will be extended to some of the other 650 cities in China over time. China continues to transform into a consumer-driven economy with a burgeoning middle class and we expect those second and third-tier cities to benefit. The World Travel & Tourism organisation is expecting 200 million Chinese to travel outside the mainland by 2020, up from 135 million in 2016. We expect Macau to benefit from the above-mentioned improvements to capacity which will increasingly attract a Chinese population that is more able to travel and has more money to spend. The Macau Tourism Industry body shares this view, with forecasts suggesting “under a modest growth scenario, visitation should range between 38-40 million by 2025”.

Shifting the focus away from casinos

The recent development of Macau has been closely overseen by the Chinese Government. The corruption crack-down is not going away, nor will Chinese officials tolerate illegal activity. They have also made it clear through the Government-sponsored Macau Tourism Industry Development plan, that the goal is to develop Macau into a world “Centre of Tourism and Leisure” and brand it as a “multi-day destination” that offers diversified tourist products and services.

The Government expects the six existing gaming concessions to generate at least 9% of their earnings from non-gaming activities by 2020. LVS already generate more than 30% of earnings from non-gaming revenue streams, with non-gaming and mass gaming accounting for close to 90% of Sands China’s profits in the most recent quarter. MGM China’s new Cotai resort will include a spa, retail, theatre and convention facilities to target non-gaming revenues, which are expected to account for between 12-15% of total revenues by the end of next year.

Both LVS and MGM have fostered strong relationships with the Chinese in order to gain a deep understanding of the Government’s objectives for Macau. By way of example, LVS appointed Wilfred Wong as President of Sands China in 2015. Wong is an experienced and extremely well connected former construction and property executive, who is active in the Hong Kong arts scene. Prior to his private sector work, Wong was also an elected member of the National People’s Congress of China and was involved in the restructuring of Hong Long into a Special Administrative Region. The Co-Chair and Executive Director of MGM China is Pansy Ho, who also owns a circa 22% stake in MGM China. Ho comes from a prominent Hong Kong family with a long history in the Macau gaming industry and has been instrumental in developing Macau as an exhibition space for fine art. MGM have also further engaged with the Chinese through a hospitality joint venture with the State-owned Diaoyutai Guest House. The business has developed hotels in Sanya and Shanghai and is in the development stages for hotels in Beijing and Frankfurt.

Future growth is not in gaming

We believe the future growth drivers of Macau will be the completion of transport infrastructure projects, expansion of hotel rooms, additional non-gaming attractions, and a rapidly expanding Chinese middle class. The Chinese will come from further, stay longer, and spend more in Macau than is practically possible today.

The growth prospects of both Sands China and MGM China are closely aligned with the Chinese Government’s objectives for growing Macau over the next five years. With the opening of MGM Cotai, we do not think earnings growth of 30% in 2018 for MGM China is unrealistic. As capital expenditure recedes, the growth in earnings are likely to be used to pay down debt and allow management to increase the dividend payout ratio from 35% in 2017 to closer to 100% by 2019.

The companies we own have diversified revenue streams that are less dependent on the lower margin and higher risk VIP revenue. As owners of MGM China’s major shareholder, MGM Resorts International, we expect our investors to benefit from these changing dynamics. With the dominant market share that Sands China has in the Macau mass market, we also think it is uniquely positioned to benefit from the longer term growth in Macau. The company has a strong balance sheet and we expect management to remain committed to returning capital to shareholders, namely LVS, their 70% shareholder. Both the Chinese Government and the resort operators are aligned in the transformation agenda which bodes well for more profitable and socially desirable patronage in the years ahead.

Fund Manager commentary for the month and quarter ended 31 December 2017 covering market reviews, BT Investment Management fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

Ebullience: An issuing forth in agitation, like boiling water; overflow; enthusiasm, extravagance.

What a difference a year makes. Gloom enveloped equities in Asia at the beginning of 2017. This year could be hardly different. There is a general sense of optimism as global economic growth shows signs of acceleration. China, at least in the near term, neither faces a capital account crisis nor deflationary bust. China and other related North Asian economies are recovering from a deep slowdown of 2015/16. While debt still is the elephant in the room, incremental cash flows and earnings for old stack companies display robust positive trends. Stock prices are made at the margin; with data looking positive to distinctly bullish, equities are responding to this fundamental evidence. This chart of China’s foreign exchange reserves China captures the dynamic very well.

China’s improving foreign exchange reserves

You would be excused in feeling ultra-bullish on markets. Several sell side strategists have increased their targets for returns and pronounced this uptrend in its second or third innings. Even the dreaded geopolitical issue of North Korea and the spectre of a nuclear war have receded. Last week there were indications of a potential conversation between South and North Korea, and this week the cameras flashed as dignitaries met in the DMZ to confirm North Korea will send a team to the upcoming Winter Olympics in South Korea.

I do not have much to add to the comments in the press, whether on economics or geopolitics. Stars seem to be aligned at the moment; our job is to monitor developments and watch for risks. Apart from the company-specific risks that are asymmetric in nature, the ones that I think we still need to keep a watch on are: protectionism for general trade; regulation for the tech sector (internet companies in particular); rising inflationary pressure forcing the Federal Reserve to hike more than expected; and a sudden shake out of liquidity as central banks reverse their QE policies.

Learn more about the BT Wholesale Asian Share Fund