The Australian retail sector is facing two challenges: a cyclical challenge caused by a slowing economy and a long-term structural threat from digital disruption (ie Amazon). In this brief note we will leave the digital challenge for another day and take a look at the retail slowdown and its implications for the retail property sector.

The weakness we’re seeing in the retail property sector is reflective of some key underlying dynamics. It is therefore instructive to understand the background issues before discussing how to navigate this new slower environment.

Firstly, it is fairly intuitive to draw a link between the performance of retailers and consumer activity. There is a well-observed flow-on effect from changes in household incomes, inflation and consumer sentiment towards an individual’s future financial position. An environment where incomes grow, employment conditions remain stable and the price of goods and services grow at a moderate rate bodes well for spending. This was quite prevalent in the cyclical upturn following the GFC when retail sales in the malls accelerated to around 5% pa. However, retail sales growth is back to just below 2% pa. This slowdown is occurring despite a large uplift in residential property values, especially in Sydney and Melbourne.

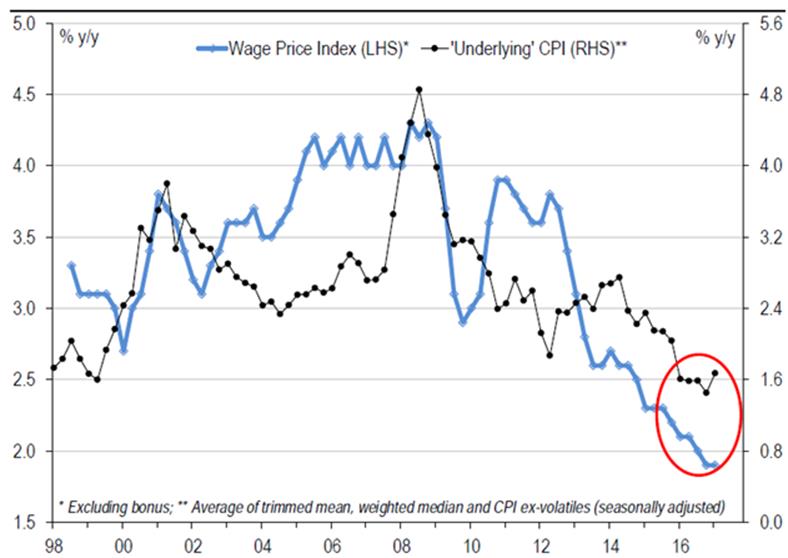

What is causing weakness in the consumer sector here in Australia? The following charts help to explain how the consumer feels. Firstly, there is very little wages growth; in fact the series is at its lowest level since 1997 and wages have been tracking below inflation for almost two years. In response to falling real wages, the consumer is hunkering down and devoting a greater proportion of household disposable income to servicing debt.

Australian wages growth is anaemic

Source: UBS

One of the reasons behind weak wages growth is simply that the workforce is more casualised and participation rates are falling. Not everyone who wants to work gets a job or gets enough hours when they are working. In fact, if you held participation rates and hours worked constant, the underlying unemployment rate would be almost 10%.

Australian underemployment is rising

Source: Macquarie Equities

Another background issue is the repricing of mortgage books by Australian banks. There is roughly $1.6 trillion of mortgage debt in Australia. Surprisingly, 40% of that debt is within interest-only loans. That high share of interest-only Ioan debt has caused concerns for the RBA and APRA which have those interest-only debt books firmly in their sights. In response, we have seen out-of-cycle rate hikes by the banks in an attempt to rebalance the books away from interest-only debt. The table below highlights the rate increases that have occurred over the past year. The interest-only book has increased by an average of 80 basis points. Based on $660 billion worth of interest-only debt, that equates to an additional $5 billion in interest costs per year. Putting that into perspective, the higher interest costs equate to 1.5% of retail sales, which goes some way to explaining the flow-on effect at the point of sale.

Dynamic loan pricing at Australia’s major banks – interest rate hikes in 2016-17

Source: BT Investment Management

Finally, the consumer also faces rising school fees, healthcare, electricity and gas prices (+20%), all of which will constrain spending at the malls.

Positioning for consumer weakness

Given the weak environment for retail, our portfolios have an underweight position in the sector, with exposure to retail focused on Scentre Group – the highest quality retail name in Australia. Scentre Group owns 14 of the top 20 shopping centres in Australia which includes prime Westfield malls like Bondi Junction, Sydney and Doncaster in Melbourne.

The vertically integrated structure of Scentre Group’s operating platform provides the business with a very strong competitive advantage. The company controls all elements of the asset operations development, design and construction, leasing, marketing and management. This has enabled the group to achieve development returns and operating metrics that are superior to its industry peers. The favourable development returns generated by Scentre Group in part reflect the quality of the assets, which forms a strong working model for generally high productivity in the existing centres and this experience is applied to new developments.

Trends in retail sales and consumer sentiment suggest the retail industry in Australia will be operating through a challenging environment in the months ahead. Our approach is to limit exposure to the retail sector to high quality names and weight our portfolios to towards other segments such as high grade commercial property.

14 June 2017

Notice of Termination: BT Australian Share PST (ABN: 40 573 184 010)

The BT Australian Share PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination.

14 June 2017

Notice of Termination: BT Conservative Outlook PST (ABN: 83 493 016 882)

The BT Conservative Outlook PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination.

14 June 2017

Notice of Termination: BT DIY Active Balanced PST (ABN: 90 963 319 535)

The BT DIY Active Balanced PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination

14 June 2017

Notice of Termination: BT Core Australian Share PST (ABN: 71 753 267 021)

The BT Core Australian Share PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination

14 June 2017

Notice of Termination: BT International Share PST (ABN: 40 573 184 010)

The BT International Share PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination.

14 June 2017

Notice of Termination: BT Property Securities PST (ABN: 80 182 972 170)

The BT Property Securities PST (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination.

14 June 2017

Notice of Termination: BT Super Trust – Capital Stable Fund (ABN: 77 143 880 163)

The BT Super Trust – Capital Stable Fund (Fund) will terminate effective Wednesday, 20 September 2017 following the required notice period set out in the trust deed of the Fund.

The Fund will be closed to any further investments or withdrawals from 14 June 2017. To allow us to make any final tax adjustments proportionally, investors will not be able to access their investment until termination is completed.

The Fund will terminate effective Wednesday 20 September 2017 and as soon as practicable, the remaining assets in the Fund will be realised and the proceeds distributed to all investors in proportion to their unit holding. This payment is currently expected to be made in early October 2017.

A letter has been sent to existing investors and advisers with clients invested in the Fund providing additional information regarding the termination.

There were clear winners and losers in 2016/17, both at an asset class and investment-specific level. Share investments were the place to be but badly timing when to buy and sell could have resulted in very different outcomes. Trump, Brexit, Frexit, Nexit and no exit (in the case of Italy’s constitutional referendum) proved to be powerful shorter term disruptors to the loosely defined normal conditions for investment markets. But all’s well that ends well appropriately characterises the year in investment markets. Here’s a summary of the key market developments over the past year together with insights from our investment teams.

*Asset class returns shown above are based on appropriate index returns. Australian Shares: S&P/ASX 300 Accumulation Index; Global Shares: MSCI World Total Return (A$) Index; Australian Fixed Income: Bloomberg AusBond Composite (0+yr) Index; Global Fixed Income: JP Morgan GBI Global Traded A$ Hedged Index; Australian Listed Property: S&P/ASX 200 A-REIT Accumulation Index; Global Listed Property: FTSE EPRA/NAREIT Developed ex Australia (A$ hedged) Total Return Index.

Australian shares

Australia’s share market marched ahead despite temporary rattlings from offshore. Share markets commenced the financial year in uncertain and unprecedented territory with the surprise outcome of the Brexit vote. Shares then staged a short term rebound and oscillated within a tight range before establishing a positive trend to end the year with a 13.8%1 return.

Ironically, investors have Donald Trump to thank for some of the market’s gains this financial year. Despite mixed views on his candidacy, the notion of an expansionary policy agenda provided markets with renewed belief in future growth and helped the market to advance in a less volatile manner.

Within the major sub-components there was a fair degree of dispersion. Resource shares outpaced their industrial counterparts, supported by a strong rise in the iron ore price. However, the rising trend ended in March when this key component of steel manufacturing began a precipitous decline. Growing concerns over China’s true economic health and hence the underlying demand for Australia’s key commodity eased the enthusiasm for resources.

Industrial shares as a group lagged the resources sector, although there was a wide range of winners and losers. Among the best performers were Qantas (+111%) and BlueScope Steel (+109%) while specific stocks to avoid included Ten Network (-82%), Vita Group (-78%) and Reject Shop (-64%).

“The market overall is fairly valued but there are still very attractive stock specific opportunities. These include ResMed with its new product releases, JB Hi-Fi and its successful integration of the Good Guys business which will deliver synergies and margin expansion, and Metcash which is well placed with strong management, a clear turnaround strategy and solid free cash flow that underpins a strong dividend.”

Andrew Waddington

Portfolio Manager – Australian Equities

Listed property

Constant murmurs of bubble, bust and burn for Australian residential property persisted through the year, although this had little bearing on the A-REIT market. Many of the established names in this sector did well, with retail property companies the notable exception. Scentre Group (-14%), owner and operator of Westfield stores in Australia and New Zealand, its US and UK stores equivalent, Westfield Corporation (-22%) and Vicinity Centres (-18%) were the stocks to avoid. The direct link to a lacklustre consumer weighed down by debt and low wage growth had a material impact on the sector.

The broader A-REIT sector remains attractive, offering a solid yield of 4-5% and earnings growth of 3-4%, making it a valuable component of diversified portfolios.

Global shares

In the US, share market returns were largely driven by the so-called FANG stocks – Facebook, Amazon, Netflix and Google. Add Apple and Microsoft to the mix and these stocks have each delivered returns ranging from 28% to 58%.

While the big tech and media stocks drove the US market higher over the past year, there are great opportunities at the moment outside of the mega cap stocks. The 10 largest stocks in the US only represent only about 15% of the US$28 trillion US stock market.

“Always look beyond the popular stocks, there are a plethora of quality companies with the potential to become ‘the next leaders’. Find them, assess them…and invest with patience.”

Ashley Pittard

Head of Global Equities

Elsewhere, most major European and Asia-Pacific markets delivered healthy double-digit returns, aided by the low interest rate environment and recovering economic fundamentals. Market valuations may appear to be extreme but we argue there is still good value in many companies and investors need to be very selective.

Fixed Income

Despite widespread expectations of negative returns, Australian fixed income posted a small positive gain in 2016/17, with a 0.25% return. Globally, central banks have kept interest rates low and flushed the market with liquidity. Returns across the major overseas bond markets ranged from -1% to -4.5%, with the global fixed income asset class as a whole returning -1.3% . The Australian dollar was a relatively strong performer, appreciating against the US dollar, euro, British pound and Japanese yen over the year. Although returns were muted across the government sector, credit investments performed well as they benefitted from strong share market performance.

“Fixed income is a core asset class and will continue to play an important role within a diversified portfolio, particularly in the event of increasing volatility in the share markets, which shouldn’t be discounted in the current environment.”

Vimal Gor

Head of Income & Fixed Interest

1. S&P/ASX 300 Accumulation Index

2. Bloomberg AusBond Composite (0+yr) Index

3. JPMorgan GBI Global Traded A$ Hedged Index

BT Investment Management (Fund Services) Limited ABN 13 161 249 332, AFSL 431426 (BTIM) makes the following irrevocable election, with effect from 1 July 2017, for the funds listed in this notice that a period of one month will be the maximum period (elected period) for providing a periodic report being an exit statement (periodic report) when a person ceases to hold a managed investment product as required by the provisions set out in the Schedule (see below). BTIM acknowledges that the periodic report must be provided as soon as practicable and in any case within the elected period.

The Schedule

The Corporations Act and Corporations Regulations 2001 (Cth) (Corporations Regulations) and in particular to comply with Schedule 10 of the Corporations Regulations as amended by Class Order 14/1252, ASIC Corporations (Amendment and Repeal) Instrument 2015/876 (ASIC Instrument 2015/876), ASIC Corporations (Amendment) Instrument 2016/1224 (ASIC Instrument 2016/1224), ASIC Corporations (Amendment) Instrument 2017/065 (ASIC Instrument 2017/065) and any subsequent ASIC Instrument amending any of those items in a manner intended or designed to give effect to the irrevocable election referred to in this document.

Funds for which this election is made:

BT Balanced Equity Income Fund (ARSN 159 947 270)

BT Concentrated Global Share Fund (ARSN 613 608 085)

BT Defensive Equity Income Fund (ARSN 159 947 298)

BT Diversified Global Equity Fund (ARSN 134 214 618)

BT Dynamic Global Equity Fund (ARSN 140 921 311)

BT Global Emerging Markets Opportunities Fund – Wholesale (ARSN 159 605 811)

BT Pure Alpha Fixed Income Fund (ARSN 161 859 936)

BT Sustainable Conservative Fund (ARSN 090 651 924)

BT Wholesale Active Balanced Fund (ARSN 088 251 496)

BT Wholesale American Share Fund (ARSN 087 594 509)

BT Wholesale Asian Share Fund (ARSN 087 593 468)

BT Wholesale Australian Long/Short Fund (ARSN 121 948 810)

BT Wholesale Australian Share Fund (ARSN 087 593 191)

BT Wholesale Australian Sustainable Share Fund (ARSN 097 661 857)

BT Wholesale Balanced Returns Fund (ARSN 087 593 011)

BT Wholesale Conservative Outlook Fund (ARSN 087 593 100)

BT Wholesale Core Australian Share Fund (ARSN 089 935 964)

BT Wholesale Core Global Share Fund (ARSN 089 938 492)

BT Wholesale Core Hedged Global Share Fund (ARSN 098 376 151)

BT Wholesale Enhanced Cash Fund (ARSN 088 863 469)

BT Wholesale Enhanced Credit Fund (ARSN 089 937 815)

BT Wholesale Ethical Share Fund (ARSN 096 328 219)

BT Wholesale European Share Fund (ARSN 087 594 429)

BT Wholesale Fixed Interest Fund (ARSN 089 939 542)

BT Wholesale Focus Australian Share Fund (ARSN 113 232 812)

BT Wholesale Future Goals Fund (ARSN 087 593 682)

BT Wholesale Geared Imputation Fund (ARSN 102 970 089)

BT Wholesale Global Fixed Interest Fund (ARSN 099 567 558)

BT Wholesale Global Property Securities Fund (ARSN 108 227 005)

BT Wholesale High Growth Fund (ARSN 610 997 674)

BT Wholesale Imputation Fund (ARSN 089 614 693)

BT Wholesale International Share Fund (ARSN 087 593 299)

BT Wholesale Japanese Share Fund (ARSN 090 666 621)

BT Wholesale Managed Cash Fund (ARSN 088 832 491)

BT Wholesale MicroCap Opportunities Fund (ARSN 118 585 354)

BT Wholesale MidCap Fund (ARSN 130 466 581)

BT Wholesale Moderate Fund (ARSN 610 997 709)

BT Wholesale Monthly Income Plus Fund (ARSN 137 707 996)

BT Wholesale Property Investment Fund (ARSN 089 939 819)

BT Wholesale Property Securities Fund (ARSN 087 593 584)

BT Wholesale Smaller Companies Fund (ARSN 089 939 328)