Markets have not priced in the possibility of a large, uncontrolled Covid outbreak in mainland China, argues Pendal senior credit analyst TERRY YUAN. Here Terry outlines how that scenario would impact investors

CHINA’S zero-Covid policy is one of the most important under-the-radar issues facing investors.

While most countries have accepted the need to live with Covid, China has decided that uncontrolled spread within its borders is too dangerous.

The impact of China’s Covid policy on markets over the next few years could be widespread, affecting inflation, interest rates, currencies and equity sectors.

Given the extreme transmissibility of Omicron (and potential future variants) as well as the outbreak in Hong Kong, we believe the market has not priced in the possibility of a large uncontrolled outbreak in mainland China.

If there is a big outbreak China’s reaction will likely be swift and heavy handed, including lockdowns, mass testing and stimulus:

- Travel restrictions would remain tight, limiting immigration and associated capital flows into Australia and the rest of the world. The more successful the zero Covid bubble, the more likely Chinese citizen would stay at home for tourism and education (much as Australians did over the past two years). We can assume this would limit supply of labour and put upward pressure on wages, inflation and interest rates.

- A bounce-back among Australian travel and immigration companies could be delayed given the dollar-weighted importance of Chinese immigration

- Lockdowns, quarantines and hospitalisations would impact Chinese workers at factories, services firms and infrastructure providers. This would create bottlenecks in shipping and production, leading to more inflation.

- Stimulus via fiscal and monetary easing — while the rest of the world was doing the opposite — would put pressure on Chinese interest rates.

China’s zero Covid policy could put upward pressure on wages, inflation and interest rates — and negatively impact sectors reliant on tourism and immigration over the next few years.

This means Australian investors should keep a close eye on airport, airline, hotel and education-related related companies in their portfolios.

Another consideration might be staying away from companies that lack pricing power.

At Pendal, we are carefully weighing this as one possible future scenario.

After navigating the initial Covid sell-off, post-pandemic rally and recent inflation spike, we are constantly looking for the next thing flying under the radar.

We are carefully selecting exposures to companies that have less exposure to China’s zero Covid policy, but have strong earnings stability, balance sheet strength and sustainability credentials.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Why China persists with Covid-zero

Why does China refuse to let Covid like the rest of the world?

The answer seems to be a combination of issues:

1. China is more vulnerable

Most of the Chinese population has been vaccinated with lower efficacy traditional inactivated viruses, rather than newer, higher efficacy MRNA vaccines.

Higher population density compared to the rest of the non-Asian world could increase the speed of transmission and more quickly overwhelm the Chinese hospital system.

Healthcare infrastructure in China, even in urban areas, is inferior to Australian standards, notes Pendal’s head of income Amy Xie Patrick

Even if Omicron infections result in a lower rate of hospitalisation relative to prior variants, the absolute numbers would likely overwhelm the hospital system.

Meanwhile, China does not want to rely on US vaccines given geopolitical tensions and potential for the US to threaten a ban on exports of MRNA vaccine supply (as it did with computer chips).

China wants to foster a successful domestic COVID vaccine and pharmaceutical industry for domestic security and a future international export avenue.

2. Political stability and timing

The Omicron wave hit at a particularly sensitive time for China — just before the Beijing Winter Olympics and Chinese New Year, the biggest holiday of the Chinese calendar.

Uncontrolled spread in Chinese cities would have captured global headlines as a failure of the Chinese government.

This would be playing on Chinese leader Xi Jinping’s mind as he approaches the Communist Party National Congress later this year, where he will seek an unprecedented third five-year term.

The last two leaders (Jiang and Hu) only had two terms before being forced to retire.

Positions on various Chinese ruling bodies will also be up for grabs. Uncontrolled Covid would likely hurt the incumbent.

3. Social contract

Without elections, China’s top leaders understand they must deliver a growing standard of living for most citizens.

Otherwise, the recent Hong Kong riots could spring up all over China. Ubiquitous camera phones would likely capture any heavy handed crackdown by the government.

Every Chinese leader has studied how and why dynasties and governments failed in China’s 2000-year history.

Confucian society centres on the family unit and respecting elders. An elevated hospitalisation or death rate for the elderly would leave a deep scar and resentment for the government.

Find out about

Regnan Credit Impact Trust

When might China abandon its zero COVID policy?

China could abandon its zero-Covid policy when a domestic pharmaceutical champion successfully develops a higher efficacy vaccine or treatment and begins manufacturing the product at scale.

Alternatively, after Xi Jinping’s re-election China could authorise foreign-produced vaccines with higher efficacy (eg Pfizer or Moderna) for a mass domestic booster campaign.

This would allow China to abandon its zero-Covid policy and gradually reopen to the world in 2023.

About Terry Yuan and Pendal’s Income & Fixed Interest boutique

Terry is a senior credit analyst with Pendal’s Income and Fixed Interest team

Terry has extensive experience in buy-side and sell-side fixed income, consulting and accounting. He has previously worked at Antares Fixed Income and Morgan Stanley.

He is a Chartered Financial Analyst (CFA) and has been admitted as a solicitor in NSW, Australia.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

The team won Lonsec’s Active Fixed Income Fund of the Year award in 2021 and Zenith’s Australian Fixed Interest award in 2020.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Businesses exposed to coal face real credit risks as well as decreased demand due to ESG concerns, writes Pendal ESG credit analyst MURRAY ACKMAN

WHAT can we learn from the AGL takeover bid by Brookfield Asset Management and Mike Cannon-Brookes’s Grok Ventures?

Anyone with a charcoal barbeque has some sense of the challenge facing coal as a power source.

Coal takes a while to heat up and you need to keep adding more to keep it hot.

Historically, this wasn’t much of a burden. Steam-powered locomotives worked fine as long you had someone shovelling more coal in.

Why is it a problem now?

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Health and economics.

Coal is one of the dirtier ways to produce energy. Burning coal releases a lot of carbon emissions as well as air pollution in the atmosphere.

Coal will need to be phased out to reduce emissions and prevent the extreme consequences of climate change.

But there’s also economics at play. With the rapid increase in renewables, the economics of energy has changed.

It’s far too simple to say renewables are cheaper than fossil fuels, especially accounting for transmission costs. But the way the wholesale electricity market works, when renewables are available, they are often the cheapest bids and get dispatched for use in the grid.

Gas can be turned off when the sun is shining and the wind is blowing. Coal stays on, so there are times when it’s burning and making no money.

Find out about

Regnan Credit Impact Trust

These are also the issues behind the news that the coal-fired Eraring power station will close seven years earlier than planned.

AGL, as the country’s biggest emitter, has announced plans to split up its coal and renewable assets into separate businesses.

The Cannon-Brookes/Brookfield takeover bid can be viewed as a challenge to management’s plan.

The consortium doesn’t believe the business should be split up, but it should more aggressively phase out coal.

What does it mean for investors?

For investors, the changing economics means businesses exposed to coal face real credit risks as well as decreased demand due to ESG concerns.

We also need to consider a range of flow-on effects to understand credit risks for investments and asset allocation.

There’s been a lot of focus on stranded assets such as coal-fired power plants which won’t be economically viable for their originally planned lifespan.

But we’ve also been divesting from coal-adjacent businesses such as coal transportation railways due to fears they won’t be able to generate revenue when coal ends.

Concern about climate change is changing the way our energy system operates.

The flow-on effects aren’t restricted to takeover bids.

It’s become a vital part of credit analysis.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

THE rapid growth of government-backed impact bonds is creating new opportunities for investors to earn stable, safe returns while doing good, says Pendal’s Murray Ackman.

- Find out about Regnan Credit Impact Trust

- Find out about Pendal Sustainable Australian Fixed Income fund

IMPACT bonds are designed to make attractive returns by financing solutions for the world’s most pressing problems.

They remain a small part of the global financial system but interest is growing strongly as more investors discover the potential to direct their capital to social and environmental outcomes.

An increasing sophistication in the way governments are approaching the sector — including by providing backing for a bond’s coupon — is making the concept even more attractive for investors.

“Instead of a government donating $100 million to finance a project, they can lend their credit rating and back the coupon rate of a bond that is then sold into the private sector,” says Murray Ackman, a credit ESG analyst who works across funds including Pendal’s Australian Sustainable Fixed Interest Fund.

“For governments and international organisations like the World Bank, you get much bigger bang for buck because the private sector is funding the project. Governments lend their credit rating and don’t front the full costs.

“And its win-win for investors who get exposure to projects that generate real impact and returns without credit risk — these are triple A rated.”

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Impact bonds are used to fund an important range of projects across the planet.

In India, impact bonds have funded the development of better road networks in West Bengal where access to essential services like banking and healthcare can take days.

In Fiji, an impact bond has provided resourcing to women significantly affected by COVID-19.

You can read more about these examples here (PDF).

Closer to home, impact bonds also fund the development of social and affordable housing, not only funding the buildings but also the solar panels and batteries that make the communities sustainable.

Regnan’s Credit Impact Trust and Pendal’s Sustainable Australian Fixed Interest Fund have invested in a range of green and social bonds including those issued by the federal government’s National Housing Finance and Investment Corporation.

NHFIC offers low-cost funding to community housing providers such as Argyle Housing, which puts a roof over the heads of single mums like Stacey and her daughter Luna.

“We have invested in these bonds which direct money to social housing providers. And the government guarantee means we do not have exposure to the risk of the underlying projects,” says Ackman.

Find out about

Regnan Credit Impact Trust

The trend to governments guaranteeing the payments on a bond provides a multiplier effect for foreign aid by harnessing the private capital markets to provide the bulk of funding for projects, says Ackman.

The UN estimates an additional $2.5 trillion a year of investment is required to deliver the 17 Sustainable Development Goals agreed to in 2015, indicating the size of the opportunity available for impact investors.

Impact bonds are particularly attractive to investors approaching retirement who are seeking stable income and preservation of capital, says Ackman.

“You can get social returns and also financial returns.

“It’s not philanthropy — that’s the whole idea.

“It’s using capitalism for good.”

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Fixed interest funds dedicated to impact investing can delivering strong performance while also making the community a better place, says Pendal senior credit analyst TERRY YUAN

- Returns in impact credit funds outperforming other bond funds

- Look for a funds with arbitrage advantage and portfolio management skills

- Find out about Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund

INVESTING in equities with an ESG or Impact bent is proving fruitful for many investors, but fixed income strategies with similar attributes are also becoming popular in Australia.

In fact, green, social and sustainability bonds make up the vast majority of “impact investing” — where investors aim to generate positive, measurable social and environmental impact along with a strong financial return.

Impact investment in Australia increased by 46% to $29 billion in 2020 — mostly due to growth in green, social and sustainability bonds which made up 88 per cent of the total, the Responsible Investing Association Australasia reported in its most recent benchmark report.

“The 2020 results indicate that responsible investments perform consistently in the short term, even though they are historically expected to yield long-term benefits,” the report says.

“As responsible investing becomes the norm, and an ever-increasing proportion of Total Managed Funds become managed to responsible investing approaches, RIAA anticipates the performance of responsible investment funds and mainstream funds … will ultimately converge.”

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Pendal senior credit analyst Terry Yuan says: “Traditionally the view has been that ESG or impact or sustainability investments don’t improve returns.

“But there is an outperformance benefit in investing in a dedicated Impact fixed interest fund.

“You can do something good and you don’t have to sacrifice returns for it. You can say ‘I’m helping take cars off the road or aiding disadvantaged families and helping people get back on track with their lives’.

“A lot more companies are issuing green bonds or impact bonds and they tend to be sought-after once they are issued [and traded in the secondary market]. There is normally a new-issue rally after they issue.

“Dedicated impact funds tend to get better allocations, and so take advantage of the bump,” he says. “And that advantage compounds over time.”

Arbitrage opportunity

The popularity of fixed income ESG or impact investments creates an arbitrage opportunity for big investors already in the market. And that’s likely to continue for a number of years.

“Ten or more years is a fair assumption for how long this arbitrage may last for,” Yuan says.

If you pick the right fund, you can also benefit from a portfolio manager’s skills in the fixed income market. “It’s about knowing when to de-risk, and then put risk back on.”

Find out about

Regnan Credit Impact Trust

Yuan uses the period of mid-December 2019 to mid-April 2020 to demonstrate his point.

The Covid outbreak began and there was a rapid rise in new cases. While the Pendal team became bearish on the outlook for credit markets, the fixed income market itself was complacent, spreads were tight and risk wasn’t well priced, Yuan says.

“There were also quantitative signals to sell credit. Technical analysis was giving sell signals. So, our fund began selling down in the last week of February and the first week of March,” Yuan says.

“Then by mid-April last year, our outlook of credit markets was improving given new Covid cases were flat-lining globally and governments and central banks were co-ordinating fiscal and monetary stimulus.

“Spreads were much wider and at attractive levels. Quantitative signals showed neutral-to-slightly-bullish credit. Technical analysis was giving buy signals. And so, we began buying back credit in mid April.”

Akin to equity markets, fixed income investing in ESG and impact funds can provide better outcomes than vanilla bond alternatives, Yuan says.

“Investors in fixed incomed ESG or impact investing need to be looking for funds that have this arbitrage advantage…and portfolio management skills.”

About Pendal’s Income and Fixed Interest boutique

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

Regnan Credit Impact Trust is a defensive investment strategy that puts capital to work for positive change

Pendal Sustainable Australian Fixed Interest Fund is a defensive Australian bond fund that delivers market-leading performance with positive environmental and social outcomes.

A new kind of bond offers features based on whether an issuer achieves sustainability goals by a deadline. Pendal Credit ESG Analyst Murray Ackman explains the pros and cons

EVERY YEAR we get asked “what are your New Year resolutions?’” Every year I come up with a few, but they tend to fade before the change of season.

When Sydney went into a Covid lockdown at the end of June I decided to try a few new self-improvement goals. As lockdown stretched on (and after some feedback from my mother) I gave up on my “no shaving” goal.

But other goals were more sustainable.

After another day of meeting goals, I got to thinking about why I’d had more success during lockdown compared to my New Year’s resolutions.

A few things came to mind. I told people about them. And I actually wanted to achieve them, rather than it being an arbitrary decision based on the end of the calendar year.

The goals had a deadline and were easily measurable. And I had skin in the game by way of a friendly wager.

How might that apply to a business?

If a business wanted to change, would a New Year’s resolution pledge be enough? Or would it need more incentive to succeed?

Can capital markets encourage businesses to become more sustainable?

This is how I think about a recent change in capital markets: the sustainability-linked bond.

What are sustainability-linked bonds?

Sustainability-linked bonds are a bond instrument where certain features vary based on whether the issuer achieves pre-defined sustainability goals within a timeframe.

Like my lockdown goals, this is an issuer making a statement that they will achieve something by a certain time, such as reducing emissions.

If they fail they have to pay up.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

This generally takes place though a coupon step-up. An issuer will have to pay investors more if they don’t achieve specific environmental or social goals.

Unlike green, social and sustainability bonds, these are not use-of-proceeds bonds earmarked for specific purposes. They fund general corporate purposes.

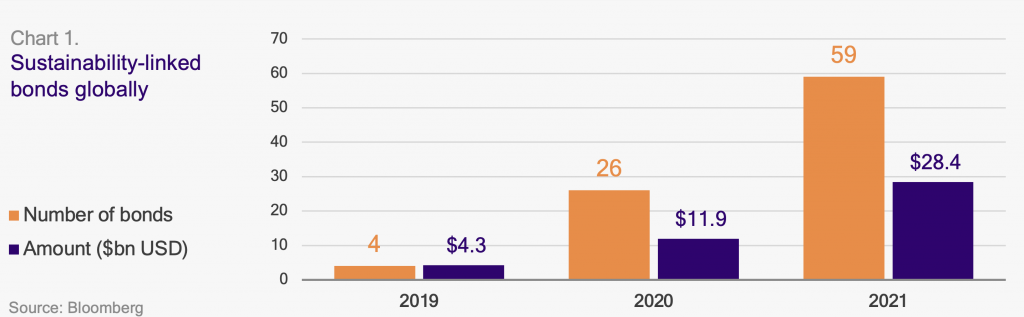

These are relatively new instruments. Globally, there have been a few issuances of sustainability-linked bonds and only one in Australia by Wesfarmers in June.

All sustainability-linked bonds have been oversubscribed and there is growing investor appetite for this type of bond.

Sustainability-linked bonds make public a company’s intention to achieve certain goals by tying financing to sustainability.

For current issuers, they offer a different list of investors and are easier to issue rather than transition or use-of-proceeds bonds.

Only a handful of corporates can do the ring-fencing required for green or social bonds.

Most of these sustainability-linked bonds have featured goals relating to emissions reductions, renewable energy generation, recycling and better waste practices. These are challenges that every business has.

These bonds are a welcome inclusion for capital markets.

They can provide a way for issuers to put something on the line to demonstrate they are serious about targets regardless of the business environment or the energy of specific champions within a business.

Potential concerns

As a new instrument, there are still some outstanding issues, particularly for sustainable investors.

Firstly, these bonds are easier to issue than other sustainable bonds. That means potential uncertainty about whether an issuer cares about sustainability or if they are using the instrument as a way to get cheap debt.

Find out about

Regnan Credit Impact Trust

Secondly, there can be doubts about whether the targets stretch a company beyond what they were planning to do anyway.

There will likely be a “first-mover” benefit whereby company targets become less aggressive compared to peers as more bonds are issued.

Thirdly, there are idiosyncratic concerns for sustainability funds. If an issuer doesn’t hit their step-up, this can potentially hurt an investor. Then it’s no longer a sustainability-linked bond and may need to be sold to comply with the mandate of a fund.

If there is a mass exodus, a step-up of 25bps — the amount generally seen in the international market — won’t necessarily compensate a forced sell-off by a sustainability fund that is not looking to hold more vanilla issuances.

The right direction

This is an evolving market.

Through greater engagement among issuers, arrangers and investors, there is hope that sustainability-linked bonds can improve sustainability offerings in debt markets.

It’s one of many initiatives for helping issuers become more sustainable.

This is about making a public statement with intent, measurable goals and putting something on the line.

It’s working for me.

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

Significant Features: The Pendal Wholesale Plus Active Balanced Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a higher weighting towards growth assets than defensive assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium to long term. The suggested investment timeframe is five years or more.

Brenton manages the Pendal MidCap Fund and natural resources portfolio, drawing on over two decades of expertise across precious metals, derivatives, investment banking, and private equity to invest in large and small cap mining companies.

Brenton has worked with Randfontein Estates Gold Mine & Harmony Gold as a mine geologist and Executive, and at JP Morgan, Deutsche Bank, Craton Capital, Macquarie Funds Group, and Taurus Funds Management in research and asset management roles.

Graduating with honours, he holds a Bachelor’s degree in Science (Geology) and a Master’s degree in Science from the University of Johannesburg. He is a member of the CFA Institute and has previously served on the International Accounting Standards Board.

The headlines have focused on Beijing’s regulatory changes, but the bigger issue for investors may be China’s economic slowdown. Here’s more from James Syme, co-manager of Pendal’s Global Emerging Markets Opportunities Fund

- China economic growth slowing

- Impact on commodity-exporting emerging markets

- Brazil, South Africa still investment opportunities as domestic demand recovers

BEIJING’s wide-ranging policy changes have rocked confidence in markets in recent weeks, but all the noise about internet regulation and video games is masking an even deeper problem for investors — a rapidly slowing Chinese economy.

That’s the view of James Syme, who co-manages Pendal Global Emerging Markets Opportunities Fund.

A slowing China has serious ramifications for emerging markets, with many economies reliant on Chinese demand for their commodities and goods, says Syme.

China’s most recent economic indicators paint a picture of a sharply deteriorating economy. Indicators as wide-ranging as retail sales, property investment, industrial production and money supply are all weaker and below expectations.

“Normally when you have a set of economic data that’s trending one way, there are a few outliers,” says Syme.

“What’s quite surprising about the Chinese data through July and August is its consistency.”

How should emerging markets investors react?

“We’ve consistently been saying that we should expect a Chinese slowdown given the tightening of monetary and fiscal policy in the first half of 2021, and we continue to have that kind of cautious stance with China,” says Syme.

“You can definitely say that the Chinese economy now is weaker than it was at the start of the year.

“The real implication is what does this mean for emerging markets that are dependent on China?”

Two important China-dependent emerging markets are Brazil and South Africa.

Find out about

Pendal Global Emerging Markets Opportunities Fund

Perhaps surprisingly, Syme maintains a relatively positive views on both.

“How can you have that view on China and yet still be positive on Brazil and South Africa? The answer is domestic demand,” he says.

Syme says GDP growth in Brazil is forecast at 2.2 per cent for 2022, while South Africa is forecast to grow 2.3 per cent, “so we’re not talking about strong growth”.

But the normalisation of domestic demand as the economies emerge from the COVID pandemic should underpin the local stock markets and provide opportunity for investors.

“That’s the general pattern that we’re focusing on even if commodity prices come down,” he says.

Risks to watch

Still, there are domestic risks to watch.

Brazil goes to an election next year which brings the threat of a market unfriendly outcome echoing political instability elsewhere in Latin America.

Meanwhile South Africa is struggling with social unrest and violent protests.

“It’s likely to encourage the government to provide more support to people in distress, which would be positive for domestic demand. But you have to be aware that the longer conditions remain difficult the more there is political risk.”

Among other markets, Syme says Taiwan and South Korea face risk from the Chinese slowdown as they export to China and will suffer slowing demand. Indonesia will bear lower commodity prices for its exports.

India will be a net winner as the Chinese slowdown reduces the prices of commodities that India imports. Russia will lose some pricing on its metals exports but remains largely a play on the oil price.

Syme cautions against conventional wisdom that Beijing will step up with stimulus as the slowdown continues.

“If you think about what Beijing is trying to do, it’s to rebalance the economy. That means more consumer spending and services, and less construction,” says Syme.

“It’s hard to put an exact number on it but construction is about 20 per cent of GDP in China, and including related industries, it’s probably more like 25 to 30 per cent.

“There’s this focus on internet and education stocks and video games, but the copper price is at a record $9400 a tonne – that just does not make sense in the light of where the economy is at.”

About James Syme and Pendal Global Emerging Markets Opportunities Fund

James Syme is a senior portfolio manager of Pendal’s Global Emerging Markets Opportunities Fund with Paul Wimborne.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Pendal Wholesale Plus Active Moderate Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a similar weighting towards defensive assets as it does towards growth assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium to long term. The suggested investment timeframe is five years or more.

George’s investment management career spans over 30 years with Pendal and its predecessor firms. He is responsible for management of credit, fixed interest and short term income portfolios, including Pendal’s highly regarded Sustainable Australian Fixed Interest Fund, Short Term Income Securities Fund and Credit Impact Trust.

George holds a wealth of experience in portfolio management and credit analysis. He has also worked across numerous fixed income, credit and money market portfolios in portfolio management, credit analysis and dealing roles for 27 years. Prior to this George worked in an accounting role for three years.

In 2019 George was awarded the Alpha Manager status by Money Management’s parent, FE fundinfo, in recognition of his career-long performance in the asset management industry. George was one out of 11 Australia-based investment professionals included in this list of esteemed professionals across multiple asset classes, after being assessed on his ability to create risk-adjusted alpha (outperformance) over his entire track record.

George obtained a Master’s degree in Business (Finance), a Bachelor’s degree in Business (Accounting & Finance) and a Graduate Diploma in Applied Finance and Investment.