Significant Features: The Pendal Active Balanced Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international listed property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a higher weighting towards growth assets than defensive assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium to long term.

Global energy and financial stocks have been unloved, but as inflation comes through it’s time to take another look. Pendal’s head of global equities Ashley Pittard explains why

- Financials and energy have been unloved compared to tech and healthcare

- But Inflation will provide an inflection point

- Find out about Ashley Pittard’s Pendal Concentrated Global Share Fund

IT’S A PERFECT time to be a contrarian investor.

If you ever wanted a reason for investing in global energy and financial stocks, have a look at their weighting in global indices relative to technology and healthcare stocks, says Pendal’s head of global equities, Ashley Pittard.

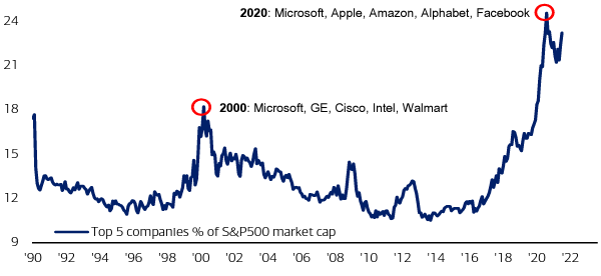

Not since the tech boom in the late 1990s and early 2000s have technology and healthcare stocks played such a dominant role in global indices — as you can see in the graph below.

The two sectors contribute about 43 per cent of the MSCI World index, led by Apple which recently passed the $US2.5 trillion market capitalisation point.

You have to go back even further to find a time when energy and financials have been so unloved, at least in a relative sense.

Even though the past six months have seen an improvement — due to upward revisions in earnings forecasts — the two sectors now make up just 18 per cent of global indices.

Extreme index positioning

“You’ve got people in extreme index positioning – index funds and active investors are in tech and healthcare, and extremely underweight energy and financials,” says Ashley Pittard, head of Pendal’s Global Equities boutique.

“It’s because no-one believes inflation is coming.”

Inflation is the critical factor going forward. It’s true that during the past decade, the lack of price rises has meant growth stocks were a good place to be.

“But now we are getting to an inflection point,” Pittard says. “Globally, earnings are beginning to broaden out.”

Find out about

Pendal Concentrated Global Share Fund

In the Unites States, there was earnings growth of nearly 100 per cent during the June quarter, led by basic materials, financials and materials.

It was even higher in Europe, with earnings growth of more than 240 per cent.

“And inflation is increasing. The argument is whether it’s transitory or structural — but we know there is inflation and it’s higher than it’s been over the past 10 years,” Pittard says. “Wage inflation is still compounding at around 3.5 per cent.”

Long term bond yields remain very low, supporting the argument for growth stocks like technology and healthcare companies.

“This is a timing issue. One day you’re going to get inflation that’s going to be more structural than transitory. It’s going to come via wages and commodity growth. And that will come back to money supply.

“Money supply is up 25 per cent year-on-year.” Pittard explains. “There was similar money supply growth after the global financial crisis. But back then the money stayed in the financial system and didn’t get in the mainstream because regulators increased banks’ capital ratios and buffers.

“To me this is a timing issue about when you see inflation coming through. That will feed back into this extreme index positioning of energy and financial being on their knees compared to healthcare and technology.”

Ashley Pittard, Pendal’s head of Global equities

“Fast forward to today, the money is going back into the real economy. And when you get that much money going into the money supply, you will see inflation.

“You are already seeing that in house prices and second-hand cars,” Pittard says.

“To me this is a timing issue about when you see inflation coming through. That will feed back into this extreme index positioning of energy and financial being on their knees, compared to healthcare and technology.

“When inflation does come back through, that’s when you want to be in financials and energy.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

As Portfolio Manager, Lewis co-manages our Australian smaller companies and micro-cap funds and conducts fundamental analysis on a range of smaller companies. Lewis joined the Pendal Smaller Companies team in 2013 as a small cap analyst, before being promoted to the role of Portfolio Manager in 2018. Lewis brings 20 years of industry experience with previous roles spanning equities research at boutique stockbroking firm, Taylor Collison, as well as commercial and investment banking roles at Westpac Bank and Commonwealth Bank. Lewis holds a Bachelor of Commerce (Corporate Finance) from the University of Adelaide.

Significant Features: The Pendal Australian Long/Short Fund is an actively managed portfolio of Australian shares investing in both long and short positions.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 200 (TR) Index over the medium to long term by taking both long and short positions in Australian shares.

Retail landlords have borne the brunt of lockdowns, but investor sentiment towards the sector is turning positive, say Pendal’s Pete Davidson and Julie Forrest

- Retail was improving ahead of current lockdowns

- Property investors not as shaken by closures

- WEBINAR: How far will listed property go and what’s its role in portfolios now

RETAIL landlords haven’t had a great time of late.

Covid-inspired lockdowns hit shopping mall owners harder than most. Unlike banks which froze — but did not cancel — loan repayments, unpaid rent money mostly won’t be recouped.

Yet investor sentiment for the sector is turning positive.

The malls are losing about a third of their income “but retail is getting better — it’s finding a bottom,” says Pendal’s head of listed property, Pete Davidson.

Find out about

Pendal Property

Securities Fund

The latest lockdowns in New South Wales, Victoria and the ACT came at a time when the retail real estate investment trust sector was looking much healthier than early last year.

Not only were people returning to malls, they were also spending more.

“People had plenty of money to spend and they weren’t holding back. Turnovers were improving quite nicely. Then Delta came along to ruin the party,” Davidson says.

Retailers are effectively being subsidised by landlords, explains Forrest. “During the lockdowns, landlords have to foot the bill.”

A rule of thumb is that about one-third of retail A-REIT (Australian Real Estate Investment Trust) income comes from the majors like Woolworths and K-Mart — and they’re still paying rent, says Davidson.

“Another third comes from the large-scale national speciality stores. They are across the country and still paying rent. Generally, those stores are looking beyond Covid and they’re operating in the States that haven’t closed down.

“It’s the mum-and-dads third that are doing it tough. They’ve been impacted and are finding it hard to pay the rent,” Davidson says.

Confidence is emerging

Notwithstanding the lockdowns, there’s confidence about the sector’s prospects.

“In the last lockdown, no-one knew what would happen and there was no vaccine or cure,” says Pendal portfolio manager Julia Forrest.

“This time around there is a vaccine, and people are prepared to look through the trading valley.”

There is less fear about the unknown, says Forrest.

“Investors have seen the other side of the valley. After the lockdowns last time around, there was all this pent-up demand which unleashed spending.

“There were superannuation drawdowns, fiscal stimulus in the form of JobSeeker supplements and people had a high propensity to spend.

“And people just didn’t take holidays. There was $40 billion in cash that wasn’t spent on holidays.”

The experience of last year has mitigated negative sentiment about the sector this year.

“Investors saw this massive reopening last time,” Forrest says. “They know there will be an end because there’s a vaccine this time around.

“They are prepared to look through the current lockdowns, as opposed to last time when no-one knew what was going to happen.”

About Pete Davidson, Julia Forrest and Pendal Property Securities Fund

Julia Forrest has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pete Davidson is Pendal’s Head of Listed Property. Over the past 34 years Pete has held financial markets roles spanning portfolio management, advisory and treasury markets. he specialises in the property, retail, insurance and infrastructure sectors.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Significant Features: The Pendal Australian Equity Fund is an actively managed portfolio of Australian shares.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 300 (TR) Index over the medium to long term.

Climate change investing tends to focus on removing carbon from portfolios or helping companies decarbonise. But a third opportunity — investing in adaptation — is often overlooked. Regnan’s Alison George explains

- Climate-aware portfolios focused on divestment, decarbonisation

- Adaptation is a third opportunity often overlooked

- Irreversible climate change means adaptation is essential

CLIMATE CHANGE caused by past emissions is likely to be irreversible for thousands of years — even if emissions stopped today.

That was a finding in the latest major report from the United Nations Intergovernmental Panel on Climate Change released in August.

Despite this, climate-aware portfolio construction often focuses on decarbonisation by removing investments with high emissions; tilting to low-carbon stocks and investing in offsets; or by investing in solutions that help companies reduce emissions — such as green hydrogen or low-carbon transportation.

But there is another approach that is largely overlooked — investing in companies that are successfully adapting to climate change.

“Adaptation is always the poor cousin to decarbonisation,” says Alison George, head of research at global responsible investing leader Regnan.

Find out about

Regnan Global Equity Impact Solutions Fund

“But it’s a critical component of climate-aware investing given the amount of climate change already baked into the system from historical emissions.

Huge driver of investment

“Adaptation will be a huge driver of investment going forward, alongside transition.

“Climate-resilient infrastructure and water-efficiency solutions that respond to reduced water availability under climate change are two key opportunity areas.”

Adaptation has been discounted as a legitimate investment option due to two investment views that have dominated in recent years, says George.

The first factor is the group of people who did not believe in climate change in the first place. “For anyone who doesn’t think climate change is real, why would you spend money on adapting?”

The second, more important factor is a belief that focusing on adaptation is like giving up the fight against climate change.

In truth, transition and adaptation are both needed — and both offer investible solutions.

Find out about

Pendal Horizon Sustainable Australian Share Fund

Pendal Group’s responsible investing specialists note in a recent two-part climate-change investing report that the physical impacts of climate change will continue to materialise even in the best-case, low-carbon transition scenario.

The report discusses how permanent changes in rainfall patterns and increased temperatures have significant impacts on agricultural productivity. This means businesses that do not adapt — for example through geographic or product diversification — may see a permanent decline in profits.

“A changing climate also impacts consumer demand,” the report points outs.

“Businesses that don’t pay attention to emerging trends from changing seasons and weather patterns may risk being caught out.

“For example, shorter winters can leave retail businesses with surplus winter stock, while wetter summers may reduce demand for outdoor entertainment.”

The report provides the example of a salmon farming business investing in cooler water offshore pens and ways to lift water oxygen levels.

Download: Pendal’s two-part guide explaining the impact of climate change on business and investing.

About Alison George

Alison George is Regnan’s head of research. She has deep experience in ESG, responsible investment and active ownership. Alison oversees Regnan’s research frameworks, processes and outputs, ensuring it remains at the forefront of industry practice and meets evolving clients needs.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

As Portfolio Manager, Patrick co-manages our Australian smaller companies and micro-cap funds and conducts fundamental analysis on a range of smaller companies. Patrick has been part of the Smaller Companies team for a collective period of eleven years. Patrick initially joined the company in 2005 and developed his career as a highly regarded small cap analyst. Patrick worked at a small cap boutique as a portfolio manager for 3 years before re-joining Pendal’s Smaller Companies team in January 2018. Patrick holds a Bachelor of Commerce (1st class Honours) from the University of Queensland and is a CFA Charterholder.

Significant Features: The Pendal Active Conservative Fund is an actively managed diversified portfolio that invests in Australian and international shares, Australian and international listed property securities, Australian and international fixed interest, cash and alternative investments. The Fund has a significant weighting towards defensive assets.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the Fund’s benchmark over the medium term.

Investors expect China may turn its regulatory spotlight on property after tightening industries such as education. Pendal’s Samir Mehta explains the outlook

- China seeking to reduce cost of living pressures on families

- Property industry may be next in Beijing’s sights

- Slowdown would have global ramifications

CHINA’s regulatory tightening of industries such as education, ridesharing, games and food delivery has sent shudders through global investment markets in recent weeks.

The policy changes — which aim to improve quality of life, redistribute income and relieve cost-of-living pressures among China’s most disadvantaged people — may go further with the giant property industry next on the list of investor concerns.

A tightening of property regulation leading to a slow-down in China’s real estate industry would pose a real risk for Australian investors given our commodity exposure to Chinese growth.

How might a China property slowdown play out?

What should investors be looking out for as they weigh these issues?

A real risk

Pendal’s Samir Mehta, who manages Pendal Asian Share Fund, says investors face a real risk that property is next in Beijing’s policy sights.

“There has been chatter around property, because buying a property or renting one remains one of the biggest outlays for an average family,” says Mehta.

“Disparities of income have led to significant real estate price appreciation, particularly in cities like Shanghai, Beijing and Shenzhen.

“There have been a few local articles that have talked about the rising multiples of annual income now required to buy an apartment.”

Find out about

Pendal Asian Share Fund

Regulatory intervention in China’s real estate market could take a number of forms such as:

- Mandating affordable housing as part of new property developments

- Restrictions on investment properties

- New property taxes

- Changing the way capital gains are taxed

Each of these could have serious ramifications for economic growth.

“This is a very tricky part of the economy because of the interactions between construction, property price appreciation and the way provincial and city governments raise revenue through land sales,” Mehta says.

“If China adjusted its policies there would be a noticeable impact down the whole chain.”

Residential property construction is an important component of China’s GDP, “so if property does come under the microscope, you should expect further slowdown.”

“Then there is mounting burden of debt in the system; a fair bit on the balance sheet of property developers and individual mortgages for residence or investment purposes.”

Impact ‘way beyond stocks’

“The impact could be way beyond stocks. Because you’re talking about a system that is built on GDP growth, built on construction, built on debt for that sector and revenues for the government. It’s across the board.”

As a major supplier of building materials including iron ore, Australia could endure the biggest impact of policy changes on China’s real estate.

Iron ore prices fell by a third in recent weeks as China slowed steel production to curb carbon emissions.

Changes to the Chinese property industry would put further pressure on the iron ore price.

What are the signs an investor should look out for?

Investors should watch Chinese retail sales, sales of property and credit growth as leading indicators of a Chinese downturn, Mehta says.

If there is evidence of slowing, investors should watch how China’s central bank responds.

The People’s Bank of China has been winding back stimulus — but they may change tack if Beijing’s policies start to affect property process and weaken the economy too much.

“The ramifications of a slowdown in China are going to be global in nature, and therefore it’s very important for the next three-to-six months to observe how the economy in China fairs,” says Mehta.

About Samir Mehta and Pendal Asian Share Fund

Samir manages Penda’s Asian Share Fund, an actively managed portfolio of Asian shares excluding Japan and Australia. Samir is a senior fund manager at UK-based J O Hambro, which is part of Pendal Group.

Pendal Asian Share Fund aims to provide a return (before fees, costs and taxes) that exceeds the MSCI AC Asia ex Japan (Standard) Index (Net Dividends) in AUD over the medium-to-long term.

Find out about Pendal Asian Share Fund

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.