The banking sector may no longer be the defensive investor’s place of refuge for relatively stable and reliable returns. But the Financials sector houses a range of opportunities beyond banks and insurers that may provide a different risk-return experience.

Pendal’s Ashley Pittard shares his thoughts on investing in the lesser observed constituents of the financial world – stock exchange operators.

Find out more about the Pendal Concentrated Global Share Fund.

Financial stocks made up 26%^ of the global share market index before the Global Financial Crisis.

That’s now down to around 15%* today thanks to a shake in the sector and ‘de-yielding’ of the global monetary system.

The sector heavyweights of the banking fraternity have experienced a general de-rating with many investors turning away from the sector.

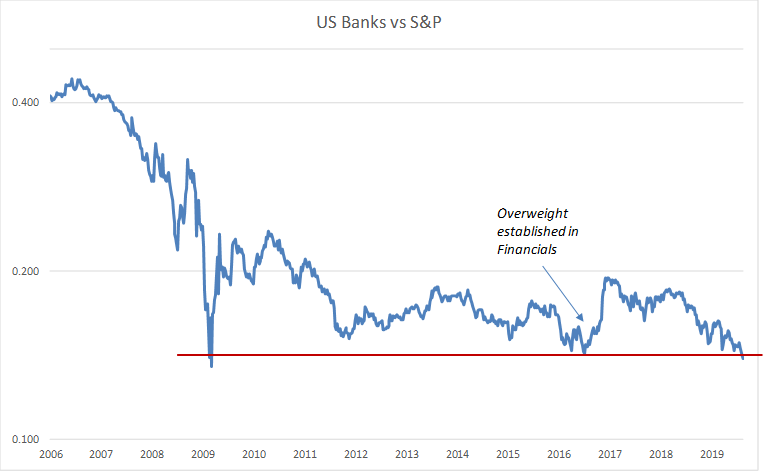

US banks — which form a large part of the global banking segment — have materially underperformed the market since the GFC.

They are now back to levels last seen in 2009 and 2016 as you can see in the following chart which tracks the relative performance of US banks against the broader US equity market.

US Banks now at pre-GFC levels

Source: Bloomberg, Pendal using representative exchange traded products

In mid-2016 at the inception on the Pendal Concentrated Global Share Fund we formed a view on a range of major influencing factors including Brexit, interest rates and inflation.

This led us to take a deeper review of the sector to identify areas of interest.

We already knew that many of the sector’s participants were well established with considerable economic moats and scale. This research culminated in establishing material positions across the financials sector.

Within the banks we favoured the regional players over the globally focused competitors which typically have significant investment banking exposures.

This led to positions being established in Wells Fargo, Lloyds Banking Group, Caixa Bank and KBC Group.

The banks we hold are of higher quality as they have generated higher returns than their peers through scale-driven cost efficiencies.

This has enabled them to build the capital required by regulators and be in a position to return the remaining free cash flow in the form of dividends and buybacks to shareholders during a tough environment.

Considering the regional nature of these businesses we expect this cohort will continue to exhibit a degree of resilience should the broader banking sector experience further de-rating.

However, if the broader environment does instead improve, we expect these companies to outperform the market much like they did following the dislocations in 2009 and 2016.

Stock exchanges – the forgotten financials

The other often overlooked segment of Financials are stock exchanges.

Stock exchanges generate revenue based on trading volumes, with an inter-related link to market volatility.

As market uncertainty develops, the derivative products issued by exchanges tend to generate higher revenues as a function of increasing spreads on pricing as well as through higher trade volumes.

Market volatility remains depressed and near historically low levels.

This negatively impacts revenue for companies like CME Group — operator of the Chicago Board of Exchange which holds a 90% market share in global futures trading and clearing services.

We launched the Fund with half of the financials exposure held in stock exchange operators.

This has made a strong contribution to the Fund’s returns over the period. Collectively, our investments in stock exchange operators have generated an average annual return of 23% (in Australian dollar terms).

In December 2018 we took profits on one of these businesses — Intercontinental Exchange — after the stock reached our valuation threshold of a 5% buyout yield.

Staying true to form

Stock exchanges remain a centrepiece of the Fund’s financials exposure and we expect these stocks to continue to re-rate as market volatility increases.

Our process is designed to identify fundamentally sound companies which have been flat or underperformed for a number of years.

Of course, the present environment is far from certain for banks in the short term amid the macro policy tensions but, from a long term perspective their valuations remain compelling to us.

At these levels history has shown it can be beneficial to look through the immediate market concerns and noise and invest in high quality companies wherein their intrinsic value is not being reflected in their current stock price.

^ Source: Bloomberg. Financials weight as represented within the MSCI World Index as at 31 December 2016.

* Source: Bloomberg. Financials weight as represented within the MSCI World Index as at 31 August 2019.

Ratchet: a device consisting of a bar or wheel with a set of angled teeth in which a pawl, cog, or tooth engages, allowing motion in one direction only; a situation or process that is perceived to be changing in a series of irreversible steps

At first, I mulled if ‘Treppenwitz’ is an apt word to describe President Trump’s comebacks to the tariff pronouncements by China. I have experienced this phenomenon before. When someone says something to me which overwhelms me, leaves me speechless, and I cannot come up with a snappy comeback on the spot. Yet once I have walked away from the situation, the perfect response suddenly pops into my head. Literally translated, Treppenwitz, a German word, means staircase joke, because the witty retort hits you in the stairwell on your way out. By then it is usually too late.

However, I quickly realised my folly. That is probably the opposite of how President Trump reacts. He is more off the cuff, speak your mind and ratchet. Since mid-2018, one of the risks markets have to contend with is whether this trade war will persist for a long time. If ever there was a doubt on that outcome, it was possibly snuffed out in August 2019. I think it is fair to say that decision-makers in China and companies on both sides of the tariff divide have decided that a resolution, if any, will at best be temporary in nature.

Then what about the other ratchets around the world? Prime Minister Johnson has engaged on a path that seems to indicate a very high probability of a no-deal Brexit. In Argentina, despite a US$57b bail-out by the IMF, we have capital controls, while Ms Legarde, the ex-IMF chief, will head the ECB. These different, seemingly unconnected events manifest themselves in the markets in one measure – the strong US dollar.

Source: Bloomberg

When risk aversion increases, the usual beneficiaries of the flight to safety trade reflect this angst. I have no clue whether we are in a phase of an even stronger or possibly weaker US dollar. History provides a reasonable guide to outcomes in markets in either case. However, in an era of nationalism, policy activism and intervention, it would take a brave soul to predict the future.

Luckily, I remember that fortune favours the brave. As the tiff with China has intensified, you might have noticed that we have ratcheted up our holdings in China, particularly the ‘A’ share market. At the end of last month, our holdings in ‘A’ shares represented approximately 10% of the portfolio. Our rationale is threefold:

1. Invest in quality businesses with high or rising margins/return metrics (with low volatility of those metrics) and a growing top line. In a world of low growth, it is a global phenomenon that higher growth companies are being rewarded more by the markets. However, these companies must have the ability to withstand disruption (whether online or policy) or benefit from it.

2. From 1978 until around 2015, China enjoyed almost uninterrupted high economic growth. In that environment, it is not easy to pinpoint businesses that have genuine resilience to economic cycles. Yet from 2015/16, we have witnessed a marked slowdown in growth, volatility in the renminbi and sharp policy zigzags in China. What is normal in any other emerging market companies in China are now facing with gusto. This provides a more fertile environment for companies that can manage better than the average ones. (Additionally, in the past, some of the best firms listed in either Hong Kong or the US, obviating the need to access the ‘A’ share universe).

3. With index providers increasing weightings for Chinese ‘A’ shares, there will be a trend over the long term towards the ‘institutionalisation’ of equity markets. Trading is currently dominated by retail investors, tends to be short term in nature and mostly, I hear (no pun intended), based on rumours and news flow. Over time, as larger pools of institutional capital pour in, it is reasonable to expect this to change. There is a caveat to this, of course. If most of the capital flows from index funds and ETFs perhaps that stream of capital might not focus on the quality names we have an interest in.

Time will tell whether this line of thinking is brave or foolhardy. Increasingly, there are signs that lower interest rates and looser monetary policy engineered by central banks are less potent than before. Some term it the ‘Japanisation’ of a world marked by disinflationary tendencies and beset with debt. Countries held hostage to external funding, like Argentina, pay a price in the US dollar value of assets. Those who have an ability to finance themselves with domestic debt pay a price in lower and faltering growth. If this indeed turns out to be the case, China might indeed be more like Japan. The probability that high growth domestic business make good long-term investments might be high. As insurance, we do hold some in the portfolio. Yet, as stated earlier, our attempt is to find and invest in more of the quality names in ‘A’ shares in China.

Fund Manager commentary for the month ended 31 August 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

We assess and score every country in the emerging markets index on a 5-point framework: growth, liquidity and monetary environment, currency, politics and governance, and valuation. We are investing based on where trends are going, not where they have been. In this latest piece James Syme assesses the currency situation particular to China and the flow-ons from the US-China trade war.

In August, the Trump administration formally designated China a “currency manipulator” (following a tweet to this effect from the presidential Twitter account). The term has formal meaning in US law, with the US Treasury required to produce an annual report identifying countries engaging in currency manipulation. China does not meet the technical criteria laid out in 2015 legislation (current account surplus, bilateral trade surplus and evidence of one-sided intervention), and, although legislation from 1988 does give more flexibility, the timing of this designation, away from the formal annual review, suggests a political rather than technical motivation.

China’s current account surplus is forecast by the IMF to be only 0.4% of GDP, which is effectively at balance. China does run a bilateral trade surplus with the United States (currently averaging US$ 27b/month), but there really is no evidence of ‘one-sided intervention’. Chinese foreign exchange reserves have been steady at around US$3.1 trillion for several years now, the currency moves broadly in line with the reference rate from a basket of currencies and, crucially, if the currency has deviated from the basket reference rate in recent months, it is to the stronger side.

Followers of our process will be aware of our view that a focus on currency valuation is a core part of the work when investing in emerging markets, as well as our preference for real effective exchange rate (REER)-based methods to do this. We are big fans of the IMF’s External Sector Report, in which every July, the IMF guides towards its views on the fundamental valuations of 26 leading currencies, focusing on how much a country’s REER would need to move to drive stability in that country’s current account balance. The 2019 External Sector Report concluded that “China’s external position was assessed to be in line with fundamentals and desirable policies, as its current account surplus narrowed further”. It also noted that “the identified policy gaps are small on net (-0.3%), reflecting largely mutually offsetting forces: loose fiscal policy and excessive credit growth on the one hand and inadequate health spending on the other hand.”

What is most interesting in the report is the consistent focus on policy-driven external imbalances in other economies: “In many countries with higher-than-warranted current account balances (Germany, Korea, Netherlands, Thailand), a tighter-than-desirable fiscal stance contributed to those external imbalances”. There is plenty of imbalance that the US Treasury could be focusing on given 2019 current account surpluses in those four countries are forecast by the IMF to be 7.0%, 4.6%, 9.3% and 7.1% of GDP, respectively. For the record, in the last three years the foreign exchange reserves of Thailand have increased by 23%, very much suggesting one-sided intervention there.

In a sense, China is merely the lightning rod for American perceptions that the US dollar is overvalued. The IMF’s report concludes that the dollar was 8% overvalued at the end of 2018, and the desire of US policymakers to have a more competitive exchange rate is clear. Unfortunately, the desire of other countries to accumulate US dollar assets is very rational. As Mark Carney, Governor of the Bank of England, noted in a speech in August, the US represents 10% of world trade and 15% of global GDP but 50% of global trade invoices, while two-thirds of EM external debt and global foreign exchange reserves are in US dollars.

We remain, then, in a position where structural economic imbalances are driving global geopolitical tensions, and the potential exists both for an escalation of US-Chinese conflict as well as an extension of these stresses to other countries, both developed and emerging. Someday, this war’s going to end. That would be just fine for emerging market investors. Until then caution is warranted.

About the Pendal Global Emerging Markets Opportunities Fund

Be a part of the world’s fastest growing economies

With just over 12 months to go before the Americans return to the polling booths, Pendal Head of Bond, Income & Defensive Strategies Vimal Gor published his thoughts in the AFR on why the US economy is on a near-certain path to recession, and why President Trump’s new world order on trade is a success in the making.

View the AFR article

Global asset manager Pendal Group has announced the appointment of Nick Good as chief executive of the J O Hambro Capital Management (JOHCM) operations in the US.

This follows a decision to appoint dedicated CEOs for the JOHCM business in UK, Europe and Asia and a CEO for the US business to support growth in offshore markets.

Alexandra Altinger was appointed CEO of JOHCM’s UK, Europe and Asia business in July. Ms Altinger starts September 9.

“The US region is a key growth engine for the Pendal Group,” said Pendal’s Group Chief Executive Officer Mr Emilio Gonzalez.

“Building on our success to date we believe there are significant opportunities to continue to materially grow our funds under management in the region.

“Nick’s leadership and success with leading global asset managers made him the prime candidate to lead our business in the US.

“He is recognised for his achievements in building and growing successful businesses, his deep knowledge of the market, and track record of delivering results.”

Mr Good was most recently Executive Vice President, Chief Growth and Strategy Officer at State Street Corporation.

In this role, he has been responsible for setting overall business strategy and leading corporate development for State Street.

Prior to this role he was co-head of State Street Global Advisors Global ETF Business, with primary responsibility for the North America and Latin America regions.

During his tenure, the Global ETF business grew assets under management by 50 per cent between the end of the 2015 and 2017 financial years.

Prior to joining State Street Mr Good worked at Blackrock (initially Barclays Global Investors), including five years as Head of the iShares ETF business in Asia-Pacific based in Hong Kong, where he led the rapid growth of the iShares business in the region.

Strong position

Mr Good said: “The strong position JOHCM has carved out in the US in such a short time is impressive and I see the real potential to accelerate that growth.

“I am excited by the opportunity presented by JOHCM’s US business and attracted by the firm’s investment-led pedigree and entrepreneurial culture.

“I look forward to joining the global leadership team and helping to grow the US business.”

Mr Gonzalez said: “Since the JOHCM business was acquired in 2011, Pendal’s offshore presence has grown significantly and provided an increasing contribution to the Group’s Funds Under Management (FUM) and profit.

“Pendal Group had closing FUM of $101.3 billion as at 30 June 2019, of which $22.0 billion is managed on behalf of US clients.

“Nick’s appointment reflects the importance of the US business to the Group and its future potential.”

Mr Good has a Master of Arts in Biochemistry from the University of Oxford. After graduating in 1996, he started his career in management consulting including five years at Boston Consulting Group.

Mr Good will report to Pendal Group CEO Emilio Gonzalez.

He will be a member of the Pendal Group Global Executive Committee.

His appointment is effective December 2 and he will be based in Boston.

Regnan has released its annual report on ESG Engagement and Advocacy activity throughout FY19. Climate risk remains an ongoing engagement theme with ASX200 companies and Regnan has increased engagement on climate related issues through the year. Human capital management and ethical conduct has been another key area of focus and Regnan has undertaken increased levels of engagement in this area. Full details are available in the report.

Download Regnan’s Annual Engagement and Impact Report here:

About Regnan

Regnan – Governance Research & Engagement Pty Ltd was established in 2007 to evaluate the relationship between environmental, social and corporate governance (ESG) factors and investment value. Regnan has evolved to become a global leader in long term value, systemic risk analysis and responsible investment advisory.

Regnan provides ESG integration, advisory and stewardship services on behalf of institutional investors including asset owners, fund managers, wealth managers, retail and investment banks to drive improved ESG performance in S&P/ASX200 listed companies. Regnan meets with directors and senior company leaders, in a constructive manner, to influence change on issues with the potential to impact value over the long term.

Regnan is also a regular contributor to the public debate on long term value and sustainability, and is an active commentator in the media and at corporate and financial industry events. Regnan also provides submissions to government and other policy makers to improve both sustainable investment and the identification of systemic risks.

Regnan’s research insights are applied to Pendal’s Sustainable, Ethical and mainstream funds where relevant, as well as enabling us to work with other institutional investors in meeting their sustainability objectives.

DISCLAIMER

This document has been prepared by Regnan Governance Research and Engagement Pty Limited (ABN 93 125 320 041), (“Regnan”) and is republished with Regnan’s permission. It is for general informational purposes only and should not be relied upon in making a decision to invest or a decision in relation to an existing investment. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information relates only to Regnan’s assessment, based on its research and the information available to it, of the performance of a company in relation to environmental, social and governance issues and should not be regarded as a recommendation or statement of opinion by Regnan on:

i. any other aspect of the company’s performance;

ii. the prospects of the company; or

iii. the company’s suitability or attractiveness from an investment perspective.

The views expressed in this document are exclusively those of Regnan and the information contained within is current as of the date of publication. Pendal Group is the owner of Regnan and commissioned the company to provide research and engagement services for use as inputs into the decision making processes for Pendal’s investment activities. The views of Regnan expressed in this article may differ from those held by Pendal Group.

Fund Manager commentary for the month ended 31 July 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Ashley Pittard, Head of Global Equities at Pendal recently presented his thoughts on the extent of risk that has developed in global equity markets at the Portfolio Construction Forum’s Strategies Conference 2019 – “20/20 Vision” . This article outlines the insights shared around why investors need to adopt a different mindset when it comes to investing in global equities in the 2020s.

Today global equities investors are facing into markets where the risks go well beyond trade wars and currency tantrums.

I’m proud of the first quartile performance Pendal’s Concentrated Global Share Fund has achieved since we commenced.

But it’s now more important than ever for investment managers in the global equities sector to have the right active strategy for the 2020s.

The extreme risk in global equities right now requires a different mindset as we enter the new decade.

September 15 marks the 11th anniversary of the Lehman bankruptcy and Global Financial Crisis (GFC).

That event sparked one of the greatest credit and equity bull markets in history as central banks adopted extreme and unprecedented monetary policies.

Along with conventional monetary policy actions including 735 interest rate cuts around the world, central banks took unconventional actions such as $US13 trillion worth of quantitative easing which essentially refers to “printing money”, preventing debt default and deflation.

End of the post-GFC era

Over the past ten years broad investment in global equities has been a great investment decision.

Investing in an index fund, exchange traded fund or a growth theme such as tech stocks would have done very well for your retirement savings instead of holding money in the bank.

After the GFC investors benefited from tail winds that drove share prices higher – such as falling interest rates, lower volatility, a declining Australian dollar and quantitative easing.

But that’s now changing.

The 2020s will be very different to the past decade.

In the new environment investors will need to be very selective rather than pursuing broad market exposure for their portfolios.

Macro supports such as cheap money and big government balance sheets won’t provide a blanket for all listed companies.

At Pendal we are contrarian, long-term fundamental stock pickers when it comes to global equities — so this environment plays to our strengths.

Markets in the new phase

Why am I so confident that these 10-year tail winds will become headwinds – even when volatility measures suggest risk is low in global equities?

It’s a hard ask for market valuations to be compelling when the market is trading at all-time highs. Price-to-Earnings ratios are over 17x and the S&P500 Index has grown to nearly four times its value since its GFC lows.

Bifurcation in the market is extreme and distortions are occurring within equity markets. We have a handful of mega cap technology-related stocks that have carried the market higher, while at the other end of the spectrum sectors deemed to be eternally disrupted have languished.

Growth sectors are significantly over-valued on traditional historical measures while value sectors are shunned.

This year just 6 % of the MSCI World Index stocks have accounted for 53% of the return for the global equity index.

Meanwhile, interest rates are down a long way. We have had 29 cuts from central banks in 2019 and government bond yields for the largest economies are at a 120-year low.

It is hard to say they will be going significantly lower. Consider the US 10-year bond as a proxy. In 2012 when the market believed the euro would break up and European banks would be nationalised, the US 10-year bond touched 1.36%. In 2016 when the ‘Brexit’ vote occurred, it touched 1.36%. In August it has drifted past the 1.75% level.

The Aussie dollar has collapsed from $1.10 over the last decade to hover around the US$0.70 level within a small range. Currency volatility for the major economies is at the lowest level since 1992.

But we have just started to see the US officially label China a currency manipulator.

It is timely to recall the 1995 Plaza Accord, a joint-agreement between France, West Germany, Japan, the United States and the United Kingdom, to depreciate the US dollar in relation to the

Japanese yen and German Deutsche Mark by intervening in currency markets. This event turned currencies upside down at the time and placed Japan into its lost decade. This event turned currencies upside down at the time and placed Japan into its lost decade.

It’s interesting that many economists saw this accord as a direct response from the US to the threat from Japan’s growing status as an economic superpower.

In my view equity risk is the highest in more than 20 years – regardless of what traditional volatility measures suggest.

When you have $US13.7 trillion of negative yielding debt globally investors have been pushed up the risk curve to chase ever decreasing yields.

And when you fundamentally change the value of cash massive distortions occur. We are seeing this on many levels.

Global debt is now 3.2 times the size of global GDP – again at an all-time high.

We have been here before

The tech sector – especially the FAANGs (Facebook, Amazon, Apple, Netflix and Google)- have been the darlings of the bull market for the last 10 years.

Real estate and utilities stocks have also been drivers of market returns, thanks largely to declining interest rates.

But the elephant in the room is the tech sector.

It has tripled its index weight since the GFC and doubled its index weight in the US market over the past five years.

Tech has been at the epicentre of this self-fulfilling circle — declining interest rates, exploding debt and rampant passive investing have helped to triple its representation of the market.

No doubt these are great businesses but it’s amazing how big their market capitalisations are — especially when compared to the GDP of some countries.

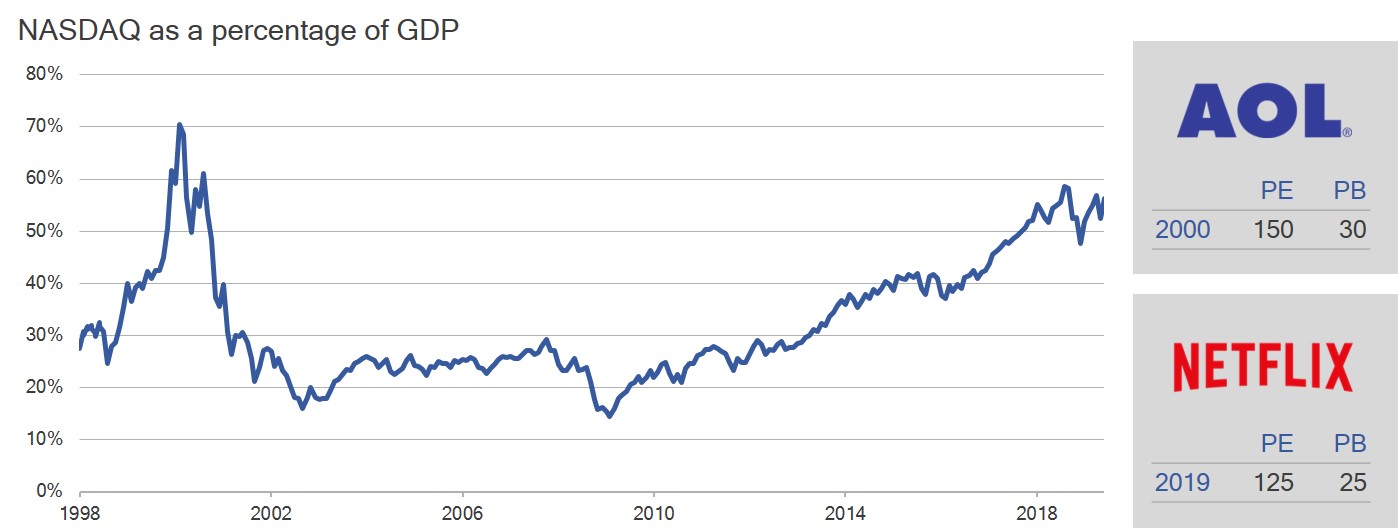

If we use the 2000 technology bubble as another proof point, the valuations again are stark.

It’s uncanny how AOL at its peak traded at similar levels to Netflix today.

Look at the metrics on the right hand side of this graph:

* Source: Bloomberg, Pendal. PE refers to price-earnings ratio, PB refers to price-book ratio.

You could argue about the relevance of using a price-book ratio for these tech names but as a long term valuation tool across different sectors, price-book is still a clean gauge of value.

And Nasdaq as a percentage of GDP is near historical bubble levels.

The extreme size of valuation premiums is a key risk driver.

Passively fulfilling a virtuous cycle

Here’s another aspect of the self-fulfilling circle. Passive and index-hugging strategies are reinforcing these valuation trends.

Over the past 10 years $US4.1 trillion has gone into passive investment funds versus outflows of $US1.5 trillion out of active.

In the year-to-date we have seen 65% of stocks in the MSCI World proceed into bear markets as passive inflows top $US7.4 billion and outflows from active strategies top $US22.4 billion.

The issue here is index and traditional strategies — by their inherent design — see more and more investors bet on higher growth for what has already risen.

This creates distortions in the market as passive ETFs focus on the largest companies in a sector, not the best companies.

Why we’re different

At Pendal, we are clearly very different.

We don’t look at the largest companies — just the best companies.

We focus on leading number one or number two franchises in their space when they are out of favour — regardless of size.

That is the lowest cost producer if it’s a commodity or largest market share if it’s a bank. We like monopoly assets.

We look at industries horizontally — not vertically as do many traditional index strategies.

We focus on fewer higher quality businesses and build a deep understanding of them like a business owner would.

We launched our Concentrated Global Share Fund three years ago and we have been very happy with the 1st quartile performance over the three-year period which reflects this very different approach compared to passive index following strategies.

Our philosophy and process has been the same since I started at BT Australia (the former entity name of Pendal) more than 20 years ago.

We have a universe of about 500 leading businesses that we follow.

We spend a lot of time focusing on disruption in industries. Usually we are buying businesses when we think they are cyclically depressed — while the market may think they are structurally impaired.

In our experience, only 15-20% of the market is attractive at any point in time.

You need to be very selective to grow wealth over the long term. Our top 10 holdings (see table) are very different to the index. We have a very large active positions.

We hold specific industry leaders such as Anheisser Busch Inbev – a leader in the beverage market.

We hold Colgate – makers of toothpaste around the world. We hold Total – Europe’s leader in oil and gas production.

We don’t hold these companies because they’re included in the Index or have driven returns. We hold them for very different reasons.

Consider the recent Amazon Wholefoods acquisition as an example.

The consumer staples sector shows how we like to research, stay patient and use disruption to our advantage.

We focus on the best businesses, understand fundamentally how they work, then stay patient and wait until they are out of favour.

There is no doubt the Amazon Wholefoods deal will change food distribution globally.

As a result of this disruption the market discounted the sector as they questioned the brand value longer term post the deal.

We looked at the industry differently and focused on market share and their return on investment (ROI).

It was clear you only wanted to focus on P&G and Colgate with greater than 60% market share and 100% ROI.

We never wanted to own Kraft Heinz, Campbell soup or Kellogg’s due to their lower market shares — even though they were larger in the index.

Think differently to drive different results

Overall I believe you need to think differently, have a concentrated highly active and very selective stock picking approach,

Think like an owner in a group of #1 unique premium assets, be patient on valuation and get paid a dividend to wait while the business normalises.

This will serve you well as we enter the next decade.