In this article, Greg Bright from Investor Strategy News pens “a potted history of the old BT and a view on its new expansion horizons.”

Read the full story

“Higher oil prices could be a game changer for Asia’s trade-gap trio”

Reuters, 26 April 2018

The first four months of 2018 have seen a more challenging global environment for emerging markets, notably a rising oil price alongside a strengthening US dollar and higher global bond yields. This combination of drivers exposes both countries with external financing needs, i.e. those with large and/or persistent current account deficits, and those with significant oil import bills. And the main way that those weaknesses come through is in currency movements. Emerging market currencies have generally been weak against the dollar so far this year, but an analysis of the two drivers mentioned above shows some distinct patterns. Overall, three groups of countries emerge.

The first, which have been the main point of focus in commentary, are the current account deficit oil importers. The Reuters article from which the above quote comes focuses on India, Indonesia and the Philippines, but the worst hit emerging currencies year-to-date have been the Turkish lira (down 11.0% against the US dollar at the time of writing), and the Argentine peso (down 17.9%). Both countries are expected to have current account deficits in excess of 5% of GDP this year and both are now facing the prospect of severe monetary policy tightening to limit currency weakness.

India, Indonesia and the Philippines also run current account deficits and are substantial net oil importers. In the first quarter of 2018, crude oil imports costs rose year-on-year in India by US$5b, in Indonesia by US$1b and in the Philippines by US$130m. Correspondingly, these countries have all seen currency weakness year-to-date, but so have several other emerging markets. Overall, the group of Argentina, Turkey, India, Indonesia, the Philippines, Pakistan, Brazil, Chile, Peru and South Africa have an average forecast current account deficit of 2.7% of GDP, will see that worsen by 0.4% of GDP for each US$10 increase in the crude oil price, and have seen average currency move of -5.9% against the US dollar year-to-date.

The second group are the oil importers whose current account balances are so strong that they are, for now, able to weather the rising oil price. Exclusively in emerging Asia, this group comprises South Korea, Taiwan, Malaysia and Thailand. These countries have an average forecast current account surplus of 7.1% of GDP, will see that worsen by 0.5% of GDP for each US$10 increase in the crude oil price, but have seen average currency move of +0.8% against the US dollar year-to-date.

The third group are the pair of Mexico and Colombia. Each produces about 600,000 barrels of oil equivalent per day more than they consume, and so although they run current account deficits, a US$10 increase in the crude oil price improves their current account balances by an estimated 0.2% and 0.7% of GDP respectively. Both currencies have strengthened against the US dollar so far this year as a consequence. Building on our comments of last month, this is another reason to be more positive about Mexican assets in the run-up to July’s presidential election.

Finally, the above analysis does not mention one important country: Russia produces an annual 2.9 billion barrel annual oil surplus, so oil’s move from the 2017 average of US$54 per barrel to the current US$77 is worth an extra US$67b to Russia, or 4.3% of GDP, while Russia’s forecast current account surplus is already 3.1% of GDP. At this oil price, Russian assets should be performing very strongly, yet the Russian ruble has fallen 7.8% against the US dollar year-to-date. Politics notwithstanding, if there is one emerging market that most benefits from this environment, it is Russia.

Recent market events have shown the continuing knock-on effects of US monetary policy normalisation. The reduction in US Dollars available onshore in the US, but more importantly offshore, is currently claiming its next victims in emerging markets. This is after pushing US short term money market rates higher in March and will continue as US monetary policy normalises. Quantitative tightening is a big part of it but the likelihood of positive real Fed Funds rates also sees US cash making a comeback as an asset class. This unravelling story has impacts across rates, currency, credit and equity markets and I will dive back into these next month. This month given there’s so much going on I wanted to take an in-depth look at Australia.

View the newsletter here.

Company and fund name changes

BT Investment Management Limited (BTIM) has changed its company name to Pendal Group Limited.

Since BTIM was listed in 2007, the business has transformed into an independent global investment management firm. In light of our growth and success, we believe now is the right time for our business to establish its own name and brand; one that reflects our independence, ownership and identity.

The name Pendal has been chosen because of its link to the heritage and origins of the BT investment management business. Pendal was the name given to BT’s original nominee company, established in 1971 to hold assets on behalf of its first prospective client, the Dalgety Pension Fund.

Pendal preserves the strengths, values and culture of our business whilst moving forward as an independent, successful, international investment management company.

What does this mean for investors?

While we have changed our company name, it will be business as usual with no change to our investment management approach or the operations of the company. As Pendal, we will continue our focus on delivering superior investment returns for clients through active management.

To reflect our new brand, we have updated the names of our funds. Please click here to view a list of our funds’ new names.

The responsible entity and investment manager have also changed their names, as follows:

| Previous Name | New Name |

| BT Investment Management (Fund Services) Limited | Pendal Fund Services Limited |

| BT Investment Management (Institutional) Limited | Pendal Institutional Limited |

We have updated our fund product disclosure statements, application forms and website to reflect the Pendal name, with changes to some of our other systems and documents to be implemented over time.

Pendal Group starts trading on the ASX and new brand unveiled

Pendal Group Limited, formerly BT Investment Management, today unveiled its new brand and was welcomed to the Australian Securities Exchange (ASX) with its updated ticker, PDL. Pendal’s Chairman, James Evans, and Group CEO, Emilio Gonzalez, rang the bell to commence trading for the day.

Read more about the unveiling here.

Surprisingly, many investors are overlooking the mid cap segment of the Australian share market, which has delivered higher returns than the broader market over the past decade. In this video, Equities Portfolio Specialist Chris Adams looks at why mid cap stocks are attractive investments and explains how our experts add the best stock ideas to an investment portfolio.

Find out more about the Pendal MidCap Fund here.

“Mexico leftist Amlo vows no nationalisation, no expropriations”

Financial Times headline, 9 March 2018

One of the challenges in analysing the effect of political change on capital markets within emerging markets is the short history of the asset class. With 30 years of data at most, a country with a four-year electoral cycle will only have seven or eight electoral data points to consider and these must also be taken in the context of economic and market drivers at both the national and global levels.

And this matters in 2018 with a fully-loaded electoral calendar (notwithstanding the unscheduled transitions in power we have seen this year in Peru and South Africa). In particular, the two large Latin American markets, Brazil and Mexico, go to the polls in October and July, respectively, while Colombia also votes on its next president this month.

Brazil’s political disconnect

Since emerging market equity came to the fore as an asset class in the late 1990s, Brazil has seen seven presidential elections. The return from Brazilian equities in those calendar years (as measured by the MSCI Brazil Index in US dollar terms) has varied widely, from +63.8% in 1994 to -44.1% in 1998. Overall, the average US dollar return in an election year in Brazil is +8.7%, compared with an average of +9.4% in those same years for the MSCI Emerging Markets Index, suggesting a limited impact.

Where the Brazilian electoral experience gets more interesting is if we separate out the elections that returned generally centrist/conservative presidencies (1989, 1994 and 1998) from those that returned more left-wing/populist governments (2002, 2006, 2010 and 2014). The first set saw an average market return of +17.9% compared with +7.7% for the MSCI Emerging Markets Index in those same years, while the second set saw an average return of +1.8% compared with +10.7% for the same index. It seems the focus needs to be on the election result rather than the simple fact of an election. This is further supported by the sharply negative short-term market performance around the 2002 and 2014 elections, which were finely balanced but ultimately decided in favour of the left-wing candidate.

And south of the border….

A potentially similar pattern is also seen in the Mexican presidential elections (although these are held every six years, so there are even fewer data points). Mexico has elected presidents in 1988, 1994, 2000, 2006 and 2012. Despite a wide range of results (including the disastrous year of 1994 which saw a leading candidate assassinated in March and a sovereign debt default in December), the overall pattern is that the average market return in these years has been +15.2%, compared with +9.1% for the MSCI Emerging Markets Index. Significantly, in none of those five elections has the most left-wing candidate been victorious, suggesting a similar market dynamic to that seen in Brazil.

So what is the prognosis for 2018? The Mexican election is likely to be won by a populist left-wing candidate, Andrés Manuel López Obrador (normally known as Amlo). This implies significant risk to Mexican equities heading into the election, and despite other attractive features of the market, we retain our neutral position because of political risk. Although, we would note that as per the quote above, Amlo has sounded far more centrist in recent weeks, and significant weakness in Mexican assets around the election may offer an exciting buying opportunity, as was seen in Brazil in 2002 when Lula was first elected.

The Brazilian election is complicated. With Lula (the left-wing Partido dos Trabalhadores (PT) party’s preferred candidate) potentially facing jail for corruption, the leading candidate is abrasive far-right politician, Jair Bolsanaro. If he is to be Brazil’s next president, the better comparison may be the present-day Philippines under President Rodrigo Duterte. Since President Duterte assumed office in June 2016, the MSCI Philippines Index has returned -10.6% (in US dollar terms), compared with a return of +46.5% from the MSCI Emerging Markets Index. We consequently remain underweight Brazilian equities.

The BT Wholesale Enhanced Cash Fund shifted to a neutral stance on investment grade (IG) credit at the start of February after being positive on the segment for a number of years. A number of the positive tailwinds that have supported IG credit are becoming less clear, with monetary stimulus being removed globally and signs of inflation and wage growth, at least in the US. We believe this concern over where inflation is moving to will continue to see bouts of volatility in bond and equity markets in the near term.

Concerns around levered corporates in the high yield space having to pay higher interest rates in the future are at the core of this change in strategy. Higher borrowing costs will pressure corporate profitability and credit metrics. In turn, this should drive credit spreads – which represent the additional cost of borrowing over the relevant government bond yield – to a wider margin, which has a negative impact on the value of these securities. We believe IG credit will outperform the high yield market, although credit spreads will be pushed wider in both IG credit and high yield markets. The risk-reward trade-off that often favours being overweight investment grade credit is no longer there in the near-term. Trade war developments add to our concerns here.

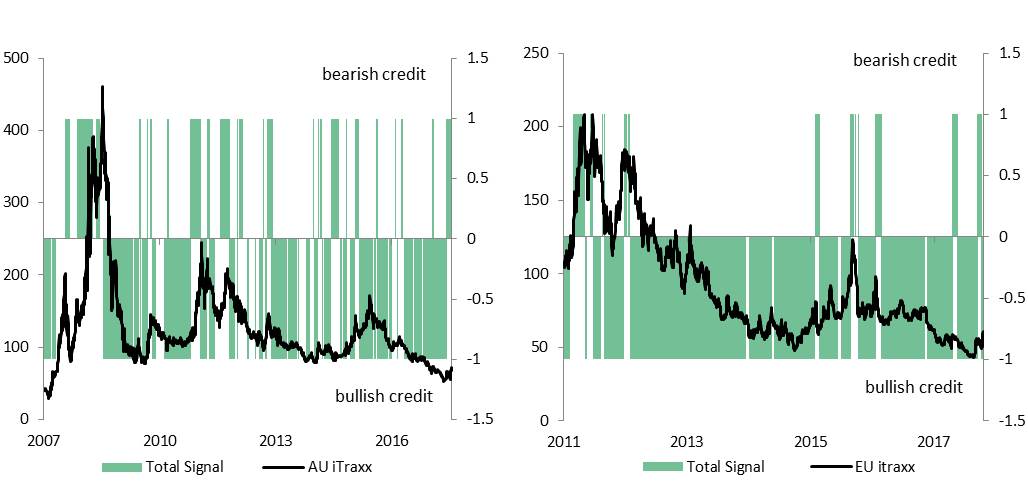

Our quantitative credit model scorecards, which use economic and market data factors to provide indications for future market directions, have also recently shifted from a bullish to a more neutral bias for investment grade credit. This has been echoed in our technical analysis scorecard signals, which have also turned bearish.

Our fundamental signals have shifted….

BTIM Credit Model Scorecard – Australian and European Investment Grade Credit

Source: BTIM

However, given the extended period of low inflation in the US, it is difficult to determine when and to what extent inflation will rise and the impact on bond yields and corporate interest expenses and their ability to refinance. Given this uncertainty, we prefer to hold a neutral stance towards investment grade credit while we wait for more economic data to establish direction.

Volatile times call for caution

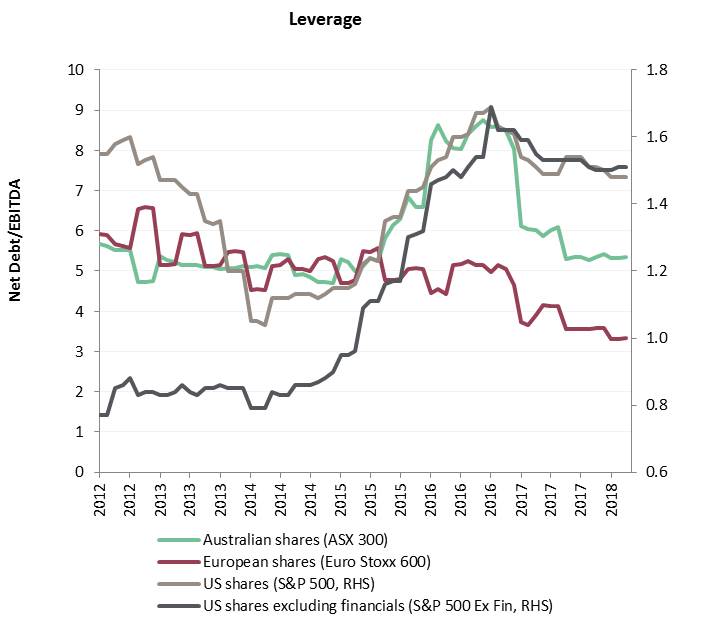

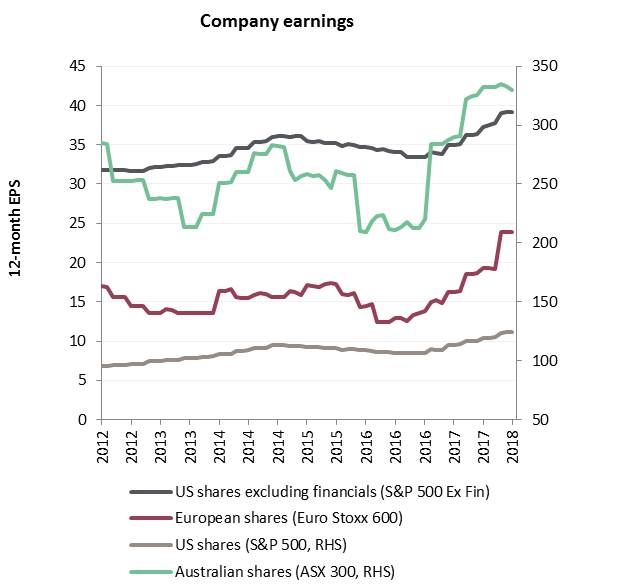

Increasing share market volatility remains a significant negative for credit markets, given their linkage to broader risk sentiment. However, the corporate fundamentals which we regularly monitor remain healthy, as illustrated in the charts below.

Corporate fundamentals remain healthy… …while debt levels remain low…

Corporate earnings per share expectations – one year forward (select markets) Corporate balance sheet leverage – select markets

Source: Bloomberg

In summary, corporate balance sheets are strong and earnings growth is solid within the major developed markets. This balances the perceived macro risks to IG credit and in the present environment, warrants a neutral stance.

This article appears in the BTIM Australian Quarterly Update (April 2018) which provides a broad collection of views from BTIM’s investment professionals on the local economy, bond yields, credit markets and the importance of sustainability analysis.

On Friday 27 April 2018, BT Investment Management’s shareholders voted to approve a change of company name to Pendal Group Limited.

We are currently working to legally change the name of the company with the Australian Securities and Investments Commission. To reflect our new name, we will also change the names of our funds and the names of the responsible entity and investment manager of these funds. We expect these name changes to be effective by Friday 4 May 2018.

Whilst our name is changing, it remains business as usual with no changes to our relationships or contractual arrangements. Importantly, our investment teams also remain the same, with no changes to their structure or investment approaches.

We will be updating our website with more information In the next week, as we transition to our new name and brand.

Read the ASX announcement here.

What has happened?

In 2014, as the military conflict in Ukraine escalated, the EU and the US (and various other nations) imposed a series of economic sanctions on Russian individuals and entities. From an equity investor’s point of view, the key components of the sanctions were a ban on buying and issuance of new equity for four large listed Russian companies: energy firms Rosneft and Novatek and banks Sberbank and VTB Bank. The securities of all four remained tradeable, as long as they did not issue new equity, which they have not done. There was also a ban on the provision of technology, equipment or assistance by Western firms to Russian offshore, deepwater or shale energy projects.

With further concern about the actions of the Russian government and/or entities connected to Russia’s Government, on 6 April 2018 the US Treasury department announced a new suite of measures, which has had a significant effect in Russian capital markets.

A series of Russian private citizens and government officials (including, importantly, Oleg Deripaska), and firms connected to those individuals, have been designated for sanctions. Crucially, these specifically bar the trading in securities of designated companies as well as limiting those companies’ access to the US dollar payments system. The listed companies designated were mostly unlisted, but did include Rusal (primary listing in Hong Kong) and EN+ (listed in Moscow, London and Paris in depository receipt form).

This had two immediate effects: the two main clearing houses for security transactions moved to immediately limit trades in the securities of Rusal and EN+ (Clearstream has said it will not process trades at all, and Euroclear will only process sales). Additionally, Rusal warned of potential credit defaults and asked its customers to suspend payments while it finds a way to be paid without breaching sanctions.

Market impact

The initial impact of this latest round of sanctions was severe. Perhaps with the US$8.9 billion fine levied on BNP Paribas for breaching sanctions on Iran in mind, there was a broad sell-off in Russian assets, and a very severe sell-off in the shares of the most affected companies, Rusal and EN+.

Rusal and EN+ fell over 50% in US dollar terms, with broad declines in other large cap stocks. The large energy names fell around 10%, Norilsk Nickel fell 18.7% and Sberbank fell 21.6%. Overall, the MSCI Russia US$ Index fell 12.4%, driven partly by a 4.2% fall in the Russian rouble to 62 to the dollar, while Russian sovereign CDS (5-year US$) moved from 120 to 140 (and subsequently widened further). Clearly, these are very substantial moves, and far greater than seen with previous rounds of sanctions.

Top-down implications

Whilst the stock-specific implications could be disastrous for the designated companies, the overall economic effect is likely to be more limited. As an exporter of US$-priced commodities, Russia is vulnerable to disruptions to its use of the US dollar payments system, but elsewhere Russia has considerable strengths. Crucially, Russian exports are commodities and essentially fungible. Barring world-wide sanctions, Russia can supply energy and bulk commodities to other parts of the world (crucially China) and be paid in an alternative currency (probably Chinese renminbi). Furthermore, Western and Central Europe depend on Russia for natural gas, with Gazprom representing a 40% share of supply in 2017.

Additionally, Russia runs a current account surplus (forecast at 3.0% of GDP in 2018) and a very limited fiscal deficit (forecast at 0.3% of GDP in 2018), thereby reducing vulnerability to reduced exports or financing.

The last year has also seen a steady rise in the oil price, which is ultimately the key driver of the Russian economy. With Brent crude currently trading at over US$70 per barrel, the Russian economy will continue to strengthen. A comparison of the oil price with the rouble, or with Russian sovereign CDS, shows the anomaly of the last week’s market moves.

That anomaly represents increased political risk, especially both the wider and more severe nature of the latest sanctions, the risk of Russian retaliation, and the consequent potential for even harsher sanctions. Markets are discounting the world’s cheapest equity market even further in a classic fear-driven, risk off move.

For comparison, the 2015 peak in CDS was 628 and the 2016 low in the rouble was 82.45 to the US dollar. Underpinned by a strong oil price, it is hard to see current risks in Russian equities as comparable with those that existed when the oil price traded below US$45 per barrel.

Portfolio changes

At the start of the month, our portfolio held four Russian stocks: larger positions in Sberbank and miner Norilsk Nickel, and smaller positions in retailers Lenta and Magnit. We have sold our entire position in Norilsk Nickel. The company has a superb operating asset, with large by-product credits giving an effective negative cash cost of production for nickel, while nickel prices remain over US$13,000 per tonne. The stock has fallen to 8x consensus 12-month forward earnings, and could potentially have a 10% dividend yield in the next year. However, Norilsk’s largest shareholder is Rusal, with a 27.8% stake. Rusal has been sanctioned along with its parent EN+ and Oleg Deripaska, EN+’s controlling shareholder. Norilsk Nickel has not been designated as the US Treasury applies a 50% control rule and Rusal owns less than 50% of Norilsk. However, there is a very clear risk that a further round of sanctions could result in Norilsk being designated. This risk is further increased as Oleg Deripaska has recently been nominated to Norilsk’s Board of directors. We consider this stock-specific risk to be unsuitable for our strategy, especially given the attractive valuations available elsewhere in the Russian equity market.

We have increased our position in Sberbank to around 3.0% of the portfolio. Sberbank is a parastatal, with a control stake owned by the Central Bank of Russia; Sberbank’s bonds trade approximately in-line with the sovereign. Sberbank has had strong operational performance in 2017, with a 38% year-on-year increase in net earnings, balance sheet growth with good cost control and some impressive developments in using technology to service both retail and corporate customers. 2017 return on equity was 23.8%, the balance sheet is strong with a Tier 1 capital ratio of 11.4% and a trailing non-performing loan ratio of 1.8% (and a loan loss reserve multiples of the non-performing loans). As such, the decline to a trailing price/book ratio of 1.3x and a 12-month forward price/earnings ratio of 5.2x seems excessive given where the oil price and Russian CDS are (and given the parastatal status of Sberbank). Sberbank is one of our highest conviction stock ideas and we have invested accordingly.

In the mid-cap space, we have maintained our positions in the retailers, and also added a position in a high quality industrial name, GlobalTrans. GlobalTrans is the leading rail freight transport company in Russia, specialising in bulk transport of commodities. GlobalTrans’ controlling shareholder, Konstantin Nikolaev, has not been designated for sanctions. Recent results have been very strong, as the company’s investments in both its fleet and its logistics capabilities have come through – the industry is one with very strong network effects, as minimising the proportion of empty runs is the key operational edge. H2 2017 earnings (EBITDA) growth was 35% year-on-year, with a 51.4% EBITDA margin and a 20% return on invested capital.

One of the reasons we are very positive on GlobalTrans is the management’s excellent capital discipline. Having invested in the fleet, strong free cash flow is being returned to shareholders, with special dividends bringing the trailing dividend yield to 6.5%, and there is a commitment to maintain the dividend policy unless attractive acquisitions become available. The company’s recent investments in its own locomotive fleet for rail tank traffic has been paying off, and we find the combination of a highly profitable business with excellent capital management, good growth prospects and a 12-month forward price/earnings ratio of less than 10x very attractive.

Political risks have undoubtedly increased in Russia in recent weeks, but a strong oil price is a very substantial offset, as is the strong current account and fiscal position. Where valuations are attractive, we will look for opportunities. We always prioritise stock-specific ownership and corporate governance matters in our bottom-up research process, as demonstrated by our sale of Norilsk Nickel and investments in Sberbank and GlobalTrans.