China has emerged quickly from zero-Covid, but its property industry is holding the economy back. What does that mean for investors? Here’s a view from Pendal’s head of income strategies AMY XIE PATRICK

You can also listen to this podcast on Apple or Spotify

An excerpt from this podcast

Amy Xie Patrick, Pendal’s head of income strategies:

The dropping of zero-Covid measures largely means that the huge restrictions on mobility no longer exist in China and you can go about living life as you wish.

Post Covid we saw in Australia a massive lift in the demand for services, a massive lift in the desire to go traveling, and a shift in consumption towards services.

That’s exactly what’s happened in China in the first few months of re-opening.

The difference with the China story though, is that a large part of the economy is still on its knees – and that’s the property part of the economy.

When the property sector is in a slump, it means that confidence from the private sector generally is in a slump as well.

That’s what’s is leading to a lot of the recent data showing that the initial momentum from China’s reopening story seems to be petering out.

The longer-term structural story for property in China is not a good one.

The Chinese inflation picture – and especially its Producer Price Index (a leading indicator of inflation) –will continue to drag more on the global inflation story – which is good for bonds, argues Amy.

We think there are many strong reasons both cyclically and structurally to be favoring fixed income and bonds in portfolios right now.

The way the China growth story is shaping up for 2023 presents as one of the top five reasons to be buying bonds right now.

Find out about

Pendal’s Income and Fixed Interest funds

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

With inflation still high but ‘sufficiently well-behaved’, the factors influencing recession are now unemployment and wages. Pendal’s TIM HEXT explains in this fast podcast

You can also listen to this podcast on Apple or Spotify

An excerpt from this interview with Pendal’s head of government bond strategies Tim Hext:

Consumers are feeling gloomy but are we still headed for recession?

With inflation “sufficiently well-behaved”, the main factors are now unemployment and wages, says our head of bond strategies Tim Hext.

“I think in the US it’s still the case that we are going to have a very mild recession at some point.

Whie it’s taken longer than expected, the impact of 5.25% of rate hikes in just over a year are starting to show through among consumers.

“The one thing that’s keeping the US economy ticking over still quite well is employment.

Jobs and wages should remain “not strong, but well-behaved” this year, which should stop any chance of near-term rate cuts, says Tim.

In Australia the chances of recession are far lower due to population growth, says Tim.

“But there is definitely a possibility we’ll have a GDP per capita recession. In other words, the economy will be better off but individually we may not feel that way.

Tim goes into detail here

Find out about

Pendal’s Income and Fixed Interest funds

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

How should fixed interest investors think about the turmoil among US regional banks? In our latest fast podcast, Pendal assistant portfolio manager OLIVER GE gives a plain-language explanation

You can also listen to this podcast on Apple or Spotify

An excerpt from this podcast with Oliver Ge, an assistant portfolio manager with Pendal’s Income and Fixed Interest team

“The problems with First Republic and SVB are not unique,” says Oliver.

“There are potentially cracks opening up in the 5th, 6th, 7th, and 13th largest banks.”

If further failures occur, investors may be over-confident that the Federal Reserve wil continue to launch rescue missions, says Oliver.

The relatively mild market response could suggest “a disconnect between what investors are pricing in and what’s actually happening”, he says.

In this podcast, Oliver explains what that could mean for investors – and why he believes cash and government bonds are an important consideration for portfolios right now.

Find out about

Pendal’s Income and Fixed Interest funds

About Oliver Ge and Pendal’s Income and Fixed Interest boutique

Oliver Ge is an Assistant Portfolio Manager with Pendal’s Income and Fixed Interest (IFI) team.

Oliver works on developing and running key quantitative investment models, and acting as trading support for the Income & Fixed Interest team. Oliver received his Bachelor of Commerce (Finance) from the University of Sydney and is also a CFA Charterholder.

Pendal’s IFI boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The invests across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

It’s become increasingly important for equities investors to understand how companies in their portfolios are protected from data breaches, says Pendal’s SUE SCOTT

- Increased focus on cyber security

- Investors need comfort from cyber policies

- Find out about Pendal Concentrated Global Share Fund

AFTER the recent Optus and Medibank data breaches, stockmarket investors may be wondering what to look for when assessing how vulnerable a company is to a hack attack.

Big, listed companies can make attractive targets for hackers.

“The larger the company, the more data it has and the more critical it is to society,” asks Sue Scott, a senior analyst in Pendal’s global equities team.

“These companies are more likely to be targeted for a cyber-attack,” Scott says. “Given our investment philosophy, it’s a particular risk for several of our portfolio companies.

“Understanding the risk, and what is being done by management to mitigate the associated with a cyber-attack on that business is critical.”

Scott use the example of Spanish financial services giant CAIXA, which Pendal has assessed for cyber-security risks.

Find out about Pendal Concentrated Global Share Fund

CAIXA has the largest IT platform in Spain and processes some 30,000 transactions per second.

“They receive 74 attacks every hour and the number of attacks has increased 2.6 times in 2022 compared to 2021,” Scott says.

Yet CAIXA hasn’t experienced a successful critical attack, says Scott.

What to look out for

Before investing, Pendal scrutinised the policy framework CAIXA has in place to understand preparedness for cyber-attacks and mitigation efforts.

“Importantly we saw that there are very clear roles and responsibilities defined within CAIXA.

“It has a cyber policy that’s corporate wide and mandatory for everyone to comply with.

“They have a specialised Cyber Security Committee which includes executive management representation; an audit team which presents to the board regularly; and three board members with specific technical expertise.

“Board members receive training and it’s reflected in the KPIs of management.”

An important addition at CAIXA is the Cyber Risk and Compliance role, separate from the Chief Technology Officer role.

“CAIXA felt when tackling cyber security, it’s important to have someone with a technical focus, and someone focused on governance.

“It also undertakes independent assessments of their cyber security capabilities twice a year, as well as complying with all European regulation regarding cyber safety,” Scott says.

Danger from within

Risks can also come from staff — whether intentional (such as a dissatisfied employee) or unintentional.

CAIXA monitors unusual behaviour among staff and their use of data.

“If there’s any abnormalities exposed then they investigate further,” Scott says.

“For non-intentional risks CAIXA has comprehensive training programs for staff and customers.”

One challenge is the ability to attract the relevant talent into a cyber security division.

“Everyone wants technical talent now to negate cyber risk. The fact that CAIXA has scale and is heavily resourced has helped attract people and keep the attrition rate very low,” Scott says.

“It gives us a lot of comfort talking to them, helping us understand what good looks like in terms of a cybersecurity policy and implementation of that policy.

“While good policy and technical expertise aren’t enough to prevent all attacks, they do mitigate the risk of an attack where critical business functions are affected, and reputational damage is inflicted.”

About Sue Scott

Sue joined Pendal in 2016 as a senior investment analyst for the global equities team. She is responsible for global sector coverage of the technology, consumer discretionary and materials sectors.

Sue has more than 24 years of experience in the finance industry. Before Pendal she advised global and Australian investors in Morgan Stanley’s Institutional Equity Division.

Pendal Concentrated Global Share fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

- Find out about Regnan Global Equity Impact Solutions Fund

REGNAN portfolio manager Tim Crockford spends most of his time searching for companies with an innovative edge in solving the world’s biggest problems.

Right now the opportunities lie with smaller companies, he argues

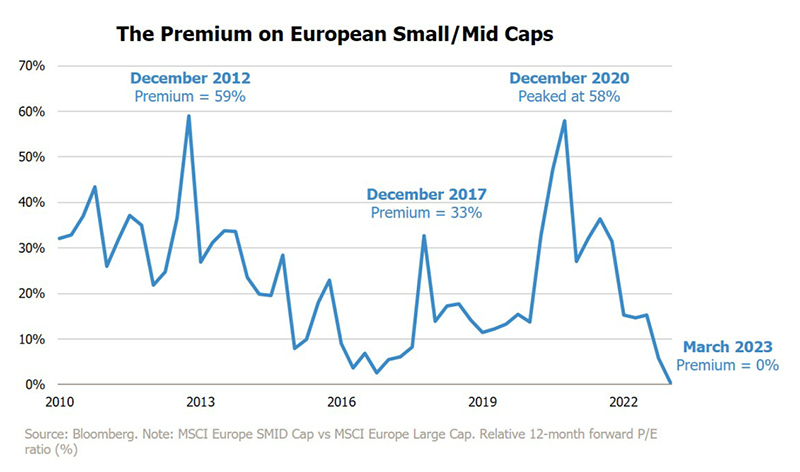

IT would take nerves of steel to write-off US large-cap equities.

Trading at just below 20x price/earnings, the S&P 500 can be seen as either over-valued or under-valued, depending where you think the world is going.

Given the rally in Big Tech through the first quarter, quite a few investors would seem convinced that there’s life — and value — left in long-duration, large-cap growth.

But this feels like a belief that the future will replay the past.

Are there alternatives?

The chart shows the premium on European small and mid-cap relative to their large cap peers.

It is now approaching zero — the lowest it has been since the aftermath of the Global Financial Crisis.

We wouldn’t like to call the market.

But what we can do is identify opportunities in the European small and mid-cap area that we feel deserve serious consideration.

Here are two.

Alfen is a manufacturer of smart grid solutions that accelerate the energy transition.

It’s the only company in Europe combining smart grids, energy storage systems and electric vehicle (EV) charging systems into a single integrated approach.

A key growth market for the business is its range of smart-connected EV chargers, enabling the broader adoption of electric vehicles.

The prospective growth of EV hardly needs to be emphasised.

Ford Europe, as one example, expects to switch completely to electric vehicles in just two years.

Find out about

Regnan Global Equity Impact Solutions Fund

Stevanato Group has been operating for 70 years, most of that time manufacturing basic glassware.

Its current — and future — strength lies in “containment” technology.

This involves machinery that greatly accelerates the production of sterile medical equipment, particularly pre-filled syringes and vials used in high-growth biologic therapeutics.

About Tim Crockford

Tim Crockford leads Regnan’s Equity Impact Solutions team and is senior fund manager of Regnan Global Equity Impact Solutions Fund. Tim previously managed the Hermes Impact Opportunities Equity Fund after co-founding the Hermes impact team in 2016.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Perpetual Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change. Both funds are distributed by Perpetual Group in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

It’s back to the future for investors with 2023 looking like a “normal financial crisis”, says Chris Lees, co-manager of Pendal Global Select Fund

- Opportunities in technology and consumer staples

- Exporters in UK, Europe and Japan are favoured

- Find out about Pendal Global Select Fund.

IT’S back to the future for investors with 2023 looking like a “normal financial crisis”, says Chris Lees, co-manager of Pendal’s Global Select Fund.

“The classic 60/40 asset allocation model is working again,” says Lees in a recent quarterly webinar.

Scroll down to watch the full presentation.

Inflation remains the big unknown — specifically whether we’re facing a 1970s-style scenario when rates rose and then were cut too early, triggering a second round of price rises.

Or a 1980s-type scenario where rates stayed higher for longer and inflation was killed off.

Or should investors expect an injection of liquidity – the so-called ‘Greenspan put’ – if markets fall sharply?

Lees and fellow co-manager Nudgem Richyal have not bought any western banks for the fund in about 15 years. “The banks are not as cheap, and not as safe, as many investors and depositors think.”

“We don’t find them particularly attractive at 0.5 to 1.5 times book [value],” Lees said.

“We do however own as couple of emerging market banks which are very profitable, with 300-to-500 basis points of net interest margin spreads. They are growth stocks in emerging markets.”

“We still think the short-term risk to interest rates is still probably on the upside, and the short-term risk to earnings is probably on the downside,” Lees says.

“The investment environment is clearly changing from last year’s inflation and interest rate shock to this year’s banking shock,” he says.

This means sectors such as financials and energy have deteriorated, from an investor’s viewpoint. Technology and consumer staples have improved, he says

Pendal Global

Select Fund

Something very

different in

global equities

“At the regional level, we’ve seen the UK, Europe and Japan improve at the margin, and specifically the exporters in those markets,” Lees says.

“And that’s the type of stock that we’ll be looking to add to the portfolio next – some world class champions in the UK, Europe and Japanese technology or consumer staples sectors.”

About Chris Lees and Nudgem Richyal

Chris Lees co-manages Pendal Global Select Fund with Nudgem Richyal. The pair have been working together in global equities investing for more than 20 years.

Chris has more than 32 years of investment industry experience. He joined Pendal Group’s UK-based asset manager J O Hambro Capital Management (JOHCM) in 2008 after spending 19 years at Baring Asset Management, ultimately as head of its global sector team.

About Pendal Global Select Fund

Pendal Global Select Fund is a global equities portfolio with a distinctive, yet proven approach.

Fund managers Chris Lees and Nudgem Richyal have worked closely together for more than 20 years.

They manage a portfolio of 30-60 stocks using quantitative analysis and fundamental research based on decades of experience.

The team draws on the expertise of 40-plus investment professionals at JOHCM and Regnan.

Pendal equities chief Crispin Murray and bonds boss Tim Hext discuss the big issues facing investors right now

THERE are a mind-boggling number of issues investors need to stay on top of in 2023.

The potential for recession, government intervention, China outlook, wages growth, consumer confidence, inflation and rates to name a few.

And there are differing views on each of these issues across the investing spectrum.

To cut through the noise and find some answers, our latest podcast brings together two of Pendal’s top investment managers: our head of equities Crispin Murray and head of government bond strategies Tim Hext.

You can also listen to this podcast on Apple or Spotify

Here’s an excerpt:

Are we heading for a recession in the US and Australia?

Tim Hext: I think we’re clearly heading for a slowdown. No one is disputing that.

Does the slowdown take us through zero growth, in other words into negative territory? It may for one quarter. It may even for two quarters, which is technically a recession, but I doubt it.

The important point is when most people think of recession they’re thinking about jobs and they’re thinking about major job losses.

I think in Australia we are going to have a rising unemployment rate. It’s probably going to go from 3.5% up towards 4.5%.

But I’m a little bit more optimistic that it will be in a context of an increasing workforce rather than necessarily large-scale job losses.

For Australia I would say chances are against a recession, although we may go close.

I’m a little bit the other way around in the US, where I think the chances are it does happen, but not with high probability.

Crispin Murray: I share a similar view to Tim on this one.

In Australia we haven’t dipped down into those excess savings as much as they have in the US.

We’ve got population growth. The stats came out for Q3 and we’re at 1.6% population growth, probably heading towards 2%. Just by bringing in more people, you help prop your economy up.

It doesn’t stop the fact that it’s a slowdown — and the big debate is about the consumer.

What you’ve got is this big headwind from the mortgage cliff as people refinance their fixed-rate mortgages into much higher variable rate runs in the next six months.

That acts as a pretty major headwind for the household income budget and that’s where we’ll see the weaknesses in the consumer.

The investing part of the economy, particularly with the public sector and with resources still going well, that probably just gets us over the line. As Tim said, it will be close, but probably not a recession.

In the US there’s two schools of thoughts.

We’ve probably got as wide a spread in terms of potential outcomes as we’ve seen for many years.

One school of thought is a soft landing where you get a pickup in participation that allows unemployment to rise without major job losses and therefore we avoid recession.

Then other people are saying: “Look at these high rates, falling money supply, less liquidity. All of those things are creating tension and strains in the financial system and you don’t know how they manifest.”

Listen to the full podcast above

Find out about

Pendal’s Income and Fixed Interest funds

Find out about

Pendal Focus

Australian Share Fund

Crispin Murray,

Head of Equities

About Tim Hext and Pendal’s Income & Fixed Interest boutique

Tim Hext is a Pendal portfolio manager and head of government bond strategies in our Income and Fixed Interest team.

Tim has extensive experience in banking, financial markets and funding including senior positions with NSW Treasury Corporation (TCorp), Westpac Treasury, Commonwealth Bank of Australia, Deutsche Bank, Bain & Co and Swiss Bank Corporation.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia.

Find out more about Pendal’s fixed interest strategies here

About Pendal

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

In 2023, Pendal became part of Perpetual Limited (ASX:PPT), bringing together two of Australia’s most respected active asset management brands to create a global leader in multi-boutique asset management with autonomous, world-class investment capabilities and a growing leadership position in ESG.

There is anger among Credit Suisse bondholders who’ve been wiped out as part of the bank’s rescue plan. But there are also important lessons for Australian fixed income investors. Pendal’s AMY XIE PATRICK explains

- Fast podcast: Prepare for likely recession with long-duration bonds

- Find out about Pendal fixed interest funds

SOME $A25 billion worth of Credit Suisse “additional tier one” (or AT1) bonds have been written down to zero value as part of a rescue deal that favoured equity shareholders.

That’s caused anger among bondholders who have lost their money – and fears of wider fallout among investors around the world.

Are broader fears justified? What can Australian fixed income investors learn from the crisis?

Murky at the bottom

AT1 bonds – also known in Europe as CoCos (contingent convertible bonds) and in Australia as bank hybrids – were created in response to previous financial crises, including the European debt crisis in 2011.

They are a type of bond that can be converted into shares if a certain event happens – and are often used by banks to meet their capital requirements.

The bonds can be converted into either common equity or written down to help absorb losses.

All 13 of In Credit Suisse’s outstanding CoCos – worth a combined face value of US$17.3 billion ($A 25.7 billion) – are of the write-down variety.

It isn’t unreasonable that these bonds are now worth zero. This part of the capital stack was designed to provide a buffer when the going gets tough.

But bondholders are outraged because equity holders will get paid more than CoCo holders on the bottom rung of the bond ladder.

That hasn’t always been the case.

In 2017, Spanish lender Banco Popular SA suffered a loss of some 1.35 billion euros

Regulators forced the bank to write off its CoCos – as well as its equity.

The Swiss regulator’s decision to write down a far larger amount of Credit Suisse CoCos — while retaining some (albeit small) value in its stock — sends a signal that things are murkier than we thought further down the capital structure.

Revaluation risks

The European CoCo market has a face value of $US275 billion. The instruments are perpetual in nature and have no maturity date.

Instead, they have call dates when issuing banks may choose to buy them back.

A “call” is financial jargon for having the option to buy a security at a pre-set price.

In the case of CoCos, it’s the issuing banks that have this option, not the bond holders.

The issuing banks should only want to buy back these CoCos at the call dates if they can do so below the prevailing market price or issue new CoCos at a cheaper level.

A “gentlemen’s agreement” between banks and investors means call dates are usually honoured (typically five to 10 years from the issue date) — and the securities are valued as if those call dates are hard maturity dates.

As recently as October 2022 we have seen in Australia’s bank T2 market that those call dates shouldn’t be viewed as maturity dates.

The Australian regulator was keen to remind issuers and investors alike that the economics needs to make sense for banks to call existing T2 paper.

While APRA has allowed T2 and AT1 bonds to be called since then, the immediate aftermath in Q4 2022 was a revaluation of existing low-coupon, subordinated bank paper to new and longer assumed maturity dates.

The time value of money dictates that when you get your principal back later than you originally thought, the value of that investment in today’s terms has to fall.

Australian T2 bank bonds had a volatile fourth quarter last year.

European bank debt traders are faced with a revaluation exercise this week as they try to factor in an increased write-down risk across the asset class, while also reassessing the value of the “gentlemen’s agreement” on call dates.

Since these CoCo bonds can also skip or defer coupon payments, their utility in providing steady income streams will also come into question.

What it means for Australian portfolios

Australian bank hybrids are designed to do the same job as European CoCos.

They are close to the bottom of the capital stack (next to equities) and are there to absorb losses for banks when they get in trouble.

The terms and conditions on our hybrids are a little different than CoCos. Most of our hybrids are convertible into common shares.

The big difference is the investor base that holds Australian hybrids.

AT1 bonds issued by European and US banks have large minimal parcel sizes for investors.

This is the regulators’ way of acknowledging the highly risky nature of these securities.

Only large wholesale or institutional investors are able to invest in hybrids offshore.

If mums and dads want exposure, they’ll likely have to invest in a fund or ETF that targets investing in hybrids.

Find out about

Pendal’s Income and Fixed Interest funds

This, at least, would get them some diversification benefit versus putting all their eggs in one basket.

In Australia, retail investors are the primary audience for hybrids.

Minimum investments for CoCos are small, to allow mums and dads to directly access this asset class.

The CoCo protestors in the Credit Suisse case are banks, hedge funds and big private wealth clients all chasing yield over the last decade.

The ones left holding the bag if any of our Aussie banks get into trouble would be retirees thinking they had bought “safe” bonds.

A wake-up call for Australians

Fortunately, the Australian financial system and banks are in rude health, thanks to the relatively risk-averse nature of our banking and regulatory institutions.

Our regulator and central bank have a huge library of “dos and don’ts” to draw upon from offshore crisis experiences.

That was one of the reasons the RBA was able to pull out the stops of quantitative easing and the term funding facility so quickly in the initial throes of the COVID pandemic.

Nevertheless, the wiping-out of Credit Suisse AT1 bondholders will be a wake-up call for parallel assets in Australia.

In coming days, the market will be rightly asking whether the risks have been adequately priced in to domestic subordinated bank bonds.

Is the market making the right assumptions about call dates and maturity dates?

Do hybrids pay enough extra coupon for the risk that those coupons might be switched off?

Are there ways to construct portfolios that offer better sleep at night?

At the very least, the premium investors will demand of the next hybrid bond to be issued in Australia ought to be higher.

Hybrid bonds are not fixed income

At Pendal, we’ve long maintained that hybrid bonds are not fixed income.

Fixed income investors demand stable and reliable income streams, with the benefit of diversification.

Diversification counts the most when the system is under stress.

Hybrids may look like fixed income when markets are calm. They look like equities (or worse!) when volatility picks up.

The worst part? By the time this becomes obvious, hybrid investors may not be able to find an exit.

More than ever, we believe it is time to take fixed income back into portfolios and scrutinise its true-to-label behaviour.

Pendal’s income strategies have never relied on hybrids for additional income, even when yields were glued to the floor.

That means today, our strategies don’t have to worry about the potential revaluation hole that awaits the asset class.

Instead, these strategies have been employing a highly active approach to managing interest rate risks around a safe and liquid core investment grade portfolio. That’s exactly what’s been needed as bond volatility reaches decade-highs.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

There is anger among Credit Suisse bondholders who’ve been wiped out as part of the bank’s rescue plan. But there are also important lessons for Australian fixed income investors. Pendal’s AMY XIE PATRICK explains

- Fast podcast: Prepare for likely recession with long-duration bonds

- Find out about Pendal fixed interest funds

SOME $A25 billion worth of Credit Suisse “additional tier one” (or AT1) bonds have been written down to zero value as part of a rescue deal that favoured equity shareholders.

That’s understandably caused anger among bondholders who have lost their money – and fears of wider fallout among investors around the world.

Are broader fears justified? What can Australian fixed income investors learn from the crisis?

Murky at the bottom

AT1 bonds – also known in Europe as CoCos (contingent convertible bonds) and in Australia as bank hybrids – were created in response to previous financial crises, including the European debt crisis in 2011.

They are a type of bond that can be converted into shares if a certain event happens – and are often used by banks to meet their capital requirements.

The bonds can be converted into either common equity or written down to help absorb losses.

All 13 of In Credit Suisse’s outstanding CoCos – worth a combined face value of US$17.3 billion ($A 25.7 billion) – are of the write-down variety.

It isn’t unreasonable that these bonds are now worth zero. This part of the capital stack was designed to provide a buffer when the going gets tough.

But bondholders are outraged because equity holders will get paid more than CoCo holders on the bottom rung of the bond ladder.

That hasn’t always been the case.

In 2017, Spanish lender Banco Popular SA suffered a loss of some 1.35 billion euros

Regulators forced the bank to write off its CoCos – as well as its equity.

The Swiss regulator’s decision to write down a far larger amount of Credit Suisse CoCos — while retaining some (albeit small) value in its stock — sends a signal that things are murkier than we thought further down the capital structure.

Revaluation risks

The European CoCo market has a face value of $US275 billion. The instruments are perpetual in nature and have no maturity date.

Instead, they have call dates when issuing banks may choose to buy them back.

A “call” is financial jargon for having the option to buy a security at a pre-set price.

In the case of CoCos, it’s the issuing banks that have this option, not the bond holders.

The issuing banks should only want to buy back these CoCos at the call dates if they can do so below the prevailing market price or issue new CoCos at a cheaper level.

A “gentlemen’s agreement” between banks and investors holds that call dates will be honoured (usually between five and 10 years from the issue date) — and the securities are valued as if those call dates are hard maturity dates.

As recently as October 2022 we have seen in Australia’s bank T2 market that those call dates shouldn’t be viewed as maturity dates.

The Australian regulator was keen to remind issuers and investors alike that the economics needs to make sense for banks to call existing T2 paper.

While APRA has allowed T2 and AT1 bonds to be called since then, the immediate aftermath in Q4 2022 was a revaluation of existing low-coupon, subordinated bank paper to new and longer assumed maturity dates.

The time value of money dictates that when you get your principal back later than you originally thought, the value of that investment in today’s terms has to fall.

Australian T2 bank bonds had a volatile fourth quarter last year.

European bank debt traders are faced with a revaluation exercise this week as they try to factor in an increased write-down risk across the asset class, while also reassessing the value of the “gentlemen’s agreement” on call dates.

Since these CoCo bonds can also skip or defer coupon payments, their utility in providing steady income streams will also come into question.

What it means for Australian portfolios

Australian bank hybrids are designed to do the same job as European CoCos.

They are close to the bottom of the capital stack (next to equities) and are there to absorb losses for banks when they get in trouble.

The terms and conditions on our hybrids are a little different than CoCos. Most of our hybrids are convertible into common shares.

The big difference is the investor base that holds Australian hybrids.

AT1 bonds issued by European and US banks have large minimal parcel sizes for investors.

This is the regulators’ way of acknowledging the highly risky nature of these securities.

Only large wholesale or institutional investors are able to invest in hybrids offshore.

If mums and dads want exposure, they’ll likely have to invest in a fund or ETF that targets investing in hybrids.

Find out about

Pendal’s Income and Fixed Interest funds

This, at least, would get them some diversification benefit versus putting all their eggs in one basket.

In Australia, retail investors are the primary audience for hybrids.

Minimum investments for CoCos are small, to allow mums and dads to directly access this asset class.

The CoCo protestors in the Credit Suisse case are banks, hedge funds and big private wealth clients all chasing yield over the last decade.

The ones left holding the bag if any of our Aussie banks get into trouble would be retirees thinking they had bought “safe” bonds.

A wake-up call for Australians

The Australian financial system and banks are in rude health, thanks to the relatively risk-averse nature of our banking and regulatory institutions.

Our regulator and central bank have a huge library of “dos and don’ts” to draw upon from offshore crisis experiences.

That was one of the reasons the RBA was able to pull out the stops of quantitative easing and the term funding facility so quickly in the initial throes of the COVID pandemic.

Nevertheless, the wiping-out of Credit Suisse AT1 bondholders will be a wake-up call for parallel assets in Australia.

In coming days, the market will be rightly asking whether the risks have been adequately priced in to domestic subordinated bank bonds.

Is the market making the right assumptions about call dates and maturity dates?

Do hybrids pay enough extra coupon for the risk that those coupons might be switched off?

Are there ways to construct portfolios that offer better sleep at night?

At the very least, the premium investors will demand of the next hybrid bond to be issued in Australia ought to be higher.

Hybrid bonds are not fixed income

At Pendal, we’ve long maintained that hybrid bonds are not fixed income.

Fixed income investors demand stable and reliable income streams, with the benefit of diversification.

Diversification counts the most when the system is under stress.

Hybrids may look like fixed income when markets are calm. They look like equities (or worse!) when volatility picks up.

The worst part? By the time this becomes obvious, hybrid investors may not be able to find an exit.

More than ever, we believe it is time to take fixed income back into portfolios and scrutinise its true-to-label behaviour.

Pendal’s income strategies have never relied on hybrids for additional income, even when yields were glued to the floor.

That means today, our strategies don’t have to worry about the potential revaluation hole that awaits the asset class.

Instead, these strategies have been employing a highly active approach to managing interest rate risks around a safe and liquid core investment grade portfolio. That’s exactly what’s been needed as bond volatility reaches decade-highs.

About Amy Xie Patrick and Pendal’s Income and Fixed Interest team

Amy is Pendal’s Head of Income Strategies. She has extensive expertise and experience in emerging markets, global high yield and investment grade credit and holds an honours degree in economics from Cambridge University.

Pendal’s Income and Fixed Interest boutique is one of the most experienced and well-regarded fixed income teams in Australia. The team oversees some $20 billion invested across income, composite, pure alpha, global and Australian government strategies.

Find out more about Pendal’s fixed interest strategies here

About Pendal Group

Pendal is a global investment management business focused on delivering superior investment returns for our clients through active management.

Should Australians be alarmed about Labor’s plans for Super? Pendal’s RICHARD BRANDWEINER believes not

AN essay by Jim Chalmers backing a “values-based approach” to capitalism last month triggered a flurry of positive and negative reviews.

This week a political battle over the role of Super escalated after Labor’s decision to cap concessions for people with more than $3 million.

Should Australians be worried about their Super?

What does the federal treasurer’s essay infer about his view on superannuation – and how the $150 billion or so annual new flows into the APRA-regulated, multi-trillion-dollar system should be managed?

Is there room for government intervention?

The Chalmers essay can be seen as a government’s reflection of the well-acknowledged excesses of neo-liberalism, says Pendal’s Richard Brandweiner.

Chalmers believes in the free market, Brandweiner says. But he also knows that unchecked neoliberalism creates market failures and distortions, such as worsening inequality.

“Markets ultimately exist to improve well-being and to enable organisations, corporations and governments access to capital to grow, and for others to be able to share their capital to save,” says Brandweiner, who also chairs Impact Investing Australia.

Left completely unchecked, markets can generate negative outcomes. But the treasurer doesn’t want to attack markets, Brandweiner believes.

“Chalmers is arguing to help create the infrastructure that will actually help the market play a role in solving some of the very real social and environmental problems we face.

Collaborate and co-invest

“He is asking: is there a scenario where not-for-profits, market participants and governments can collaborate and co-invest on market based parameters in order to help solve these problems.

“He is pointing to the Clean Energy Finance Corporations as an example where government did not direct capital, but there was a collaboration,” Brandweiner says, adding the public-private partnerships are examples of successful co-investments to support infrastructure needs.

“In PPPs, the government is playing a role directing the investment, but private capital is bidding for that and making a market-based decision on where it wants to allocate capital,” Brandweiner says.

“At the end of the day, the thing that matters in the long term is improved well-being for all.

“Markets are a very powerful tool to ensure an efficient allocation of resources, but they can create failures.

Find out about

Regnan Global Equity Impact Solutions Fund

“So how should we think about squaring this circle?

“How can governments, non-government organisations and markets leverage what they bring to the table most effectively to achieve the mission of improving well-being across the board?” Brandweiner asks.

He doesn’t believe Treasurer Chalmers is intending to direct superannuation funds where to invest.

Nor does he believe there is any desire or expectation for returns to be compromised.

“But he does want to create infrastructure that will support return-driven investment into areas which could lead to better environmental and social outcomes.”

“The way the capital in our super system is deployed will impact the world we retire into, and there’s no way around that.”

Given that, Chalmers policies could be critical for all our futures.

About Richard Brandweiner

Pendal’s Richard Brandweiner has more than 20 years of experience in investment management. He is the chair of Impact Investing Australia.

Pendal offers a range of sustainable and impact investing strategies, including:

Regnan Global Equity Impact Solutions Fund, which invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

Pendal Sustainable Australian Fixed Interest Fund, a defensive Australian bond fund that delivers market-leading performance with positive environmental and social outcomes.

Regnan Credit Impact Trust, which invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

For more information on these and other responsible investing strategies, contact our head of responsible investment distribution, Jeremy Dean at jeremy.dean@pendalgroup.com.