Pendal Group (ASX:PDL) has announced the completion of its acquisition of US-based value-oriented investment management company, Thompson, Siegel & Walmsley LLC (TSW).

Highlights:

- 96% of TSW client consent to the acquisition secured and expect to achieve 100% consent shortly after close.

- Early completion achieved – reflecting the cultural and commercial alignment of both teams and the strong mutual commitment to realise the growth opportunities ahead.

- John Reifsnider, TSW CEO, to lead Pendal’s consolidated US business and joins the Pendal Group Global Executive Committee.

- Step change in Pendal’s FUM: more than doubling US FUM to A$62.5 billion (US$47.0 billion)* and increasing total Group FUM by 31% to A$139.3 billion.

- Expected to be double digit EPS accretive in the first full year, post completion.

PENDAL Group CEO, Nick Good (pictured), said: “We are thrilled to welcome the TSW team and its clients to Pendal Group.

“Client support has been incredibly strong, with 96% TSW client consent received in just 11 weeks. It is testament to the compatibility and drive of the two organisations and their teams that we have completed the acquisition well ahead of original expectations.

“As a result of the acquisition, we will double our addressable market in the US and extend our ability to generate new FUM through the distribution of both TSW and JOHCM products across an expanded global network.

“Today, John Reifsnider becomes the new leader of the combined US business. John and I have worked closely together to complete the transaction expeditiously, cognisant of the importance of client and team support for the go-forward proposition. I am very pleased that John will be taking on this key role.”

Mr Reifsnider said: “The team and I are more convinced than ever of the merits of bringing together these two culturally aligned and forward-looking businesses.

“We believed from the outset that both organisations are a natural fit with compatibility in investment philosophy, client service and our entrepreneurial approach.

“The teamwork in delivering early completion and client consent is validation of this view and bodes well for future success.”

Broader range of product solutions

Mr Good commented: “This acquisition significantly broadens the range of product solutions we can offer clients via an expanded distribution network, and we are focused on providing our combined investment strategies to our enlarged client base as soon as possible.

“Both organisations share a core belief in investment team autonomy, and TSW’s investment autonomy will be preserved, an important consideration for our clients.

“As complementary businesses, with almost no overlap of investment strategies, together, we will be better placed to take advantage of the growth opportunities we see in the US market.”

There was strong support for the acquisition from Pendal’s institutional and retail shareholders and as a result, the successful Placement and Share Purchase Plan raised A$380 million in total.

This equity raising reduced the debt and balance sheet funding which was required to complete the transaction to A$57 million (US$44 million). This outcome provides additional balance sheet strength and capacity for Pendal to accelerate its growth opportunities.

Mr Good concluded: “The acquisition has delivered immediate value for our shareholders and a step change in Pendal Group’s diversification, scale and client offering.

This creates enhanced opportunities for growth, particularly with increasingly positive investor sentiment, a flourishing US economy and the global economic rebound.”

* Includes TSW FUM of US$24.6 billion (A$32.6 billion). Based on exchange rate of AUD:USD of 0.7518 at 30 June 2021.

Visit Pendal’s shareholder website for more information.

About Pendal

Pendal Group (“Pendal”) is an independent global investment manager focused on delivering superior investment returns for clients through active management. Pendal manages A$106.7 billion in FUM (as at 30 June 2021) in client assets through J O Hambro UK, Europe & Asia; JOHCM USA; Pendal Australia and Regnan.

Pendal operates a multi-boutique style business delivering superior results across a global marketplace through a meritocratic investment-led culture. Its experienced, long-tenured fund managers have the autonomy to offer a broad range of investment strategies with high conviction based on an investment philosophy that fosters success from a diversity of insights and investment approaches.

Listed on the Australian Securities Exchange since 2007 (ASX: PDL), the company has offices in offices in Sydney, Melbourne, London, Prague, Singapore, New York, Boston and Berwyn, Pennsylvania in the US.

About Thompson, Siegel and Walmsley (TSW)

TSW is a US-based value-oriented investment management and advisory company, operating primarily in the long-only equity (International and US) and fixed income asset classes with US$24.6 billion (A$32.6 billion) of FUM as at 30 June 2021.

Established in 1969 and headquartered in Richmond, Virginia, the company has a well-known record in attracting and retaining investment talent, with an average tenure of 12 years among the investment team members.

Roshni works as a portfolio manager with the Pendal Global Emerging Markets Opportunities strategy. She is based in our London office with affiliate fund manager J O Hambro. Prior to joining JOHCM, Roshni worked for Kintbury Capital for two years as an investment aAnalyst. Prior to this, Roshni spent four years at JOHCM as an analyst on the UK Opportunities fund. Roshni holds a degree in Economics from the London School of Economics and is a CFA Charterholder.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

GLOBAL equities have struggled to push higher recently under the weight of several factors.

US inflation data was again stronger than expected last week, while concern lingered over the impact of the contagious Delta Covid variant.

Global equities dropped — the S&P 500 gave up 0.96% — but the Australian market bucked the trend, rising 1.05%. Merger and acquisition activity and a stronger resource sector continued to lend support.

Markets are in something of a holding pattern while investors look for visibility on a number of unresolved issues.

These include:

- Economic growth: How much is it slowing? To what extent is this about temporary supply-related issues? Or is it a signal that pent-up demand is less than expected?

- Inflation: How transitory will this be?

- Covid: To what extent will Delta or other variants affect the recovery and re-opening of economies?

- Central bank policy: How quickly will they need to reduce balance sheet expansion and begin to raise rates?

- Fiscal policy: Do we see more stimulus coming through in the form of infrastructure and other social investment programs?

- China: To what extent is the economy slowing and how material a shift in policy will we see?

- Corporate earnings: How much leverage to re-opening, the impact of rising cost pressures and the ability to raise prices?

These issues are inter-related. Some such as inflation and fiscal policy may take a long time to become clear.

However we should get a good read on most factors through this quarter. This will play into how bonds and the US dollar perform, which will in turn affect the performance of commodities, as well as cyclicals and defensives in the equity market.

We expect markets to consolidate in the near term. Domestic cyclicals are likely to struggle. But we expect concerns around most of the factors above to ease, potentially creating opportunities.

COVID and vaccines

South East Asian countries with low vaccination rates are reporting a surge in new Covid cases. Malaysia, Thailand and Indonesia are running at their highest daily case numbers so far.

But we are also seeing surges in countries such as the UK and the Netherlands, where vaccination rates are high. Rising cases in France, the US and Israel have prompted a return to restrictions.

In Malta 80% of the population is fully vaccinated and a further 5% have had a single dose — yet it is seeing a sharp rise in new cases. There are still questions to be answered — is the spread primarily among the unvaccinated for example? But places like Malta will be important in understanding whether the new wave of Covid will lead to a more restricted re-opening.

The UK remains something of a bellwether. New daily cases are running within 15% of the highs of the previous wave, but hospitalisations are 80% lower.

This suggests vaccines are helping prevent people from getting very sick. But it’s not yet clear if new cases are predominantly unvaccinated people or “breakthrough infections” among those who are vaccinated.

We can also gain insight from the US. There is a clear link between rates of vaccination and infections by county. Counties with vaccination rates of 50-59% have half the infection rate of counties with less than 30% vaccination.

The US is also publishing reassuring data on breakthrough infections and hospitalisations. So far this year vaccinated patients account for only 0.4% of Covid-related hospital admissions. That is running at about 1% more recently, which reflects the Delta strain. Some 75% of recent admissions have been people over 65.

We can make a couple of observations about Australia in light of this.

First, it is difficult to envisage us remaining Covid-free even with high vaccination rates, without keeping international borders shut. This necessitates some shift in policy approach, which will be more complex than first thought. This will be an important factor in elections.

Second, it highlights the difficulty in achieving eradication in NSW. Even if you get cases very low, the latest Victorian wave shows how quickly the variant can spread.

Policy makers will need to decide whether to extend restrictions to contain case numbers until we reach warmer months when the vaccine program can be accelerated. This could take us through to October or November.

If so, we would expect significant offsetting stimulus. Nevertheless it would weigh on the domestic economy and have a negative impact on more cyclical stocks. Given the lack of visibility, we are wary of re-loading on this part of the market despite recent weakness.

Economics and policy

There are some real-time indicators. The Atlanta Fed’s GDPNow estimate suggests economic growth has fallen below market consensus levels for the first time this year, while still remaining strong in absolute levels. This is why bonds have rallied and cyclicals have fallen.

We believe much of this reflects supply bottlenecks in certain areas which — alongside labour constraints — is preventing some businesses from operating or producing as much as they would like. We still expect the effects of pent-up demand, excess savings, low inventories and high wealth effect to help fuel an on-going strong recovery.

That said, the risks to this scenario are rising.

US inflation data surprised to the upside for the third month in a row. Material elements of this – such as used car and holiday accommodation prices – reflect some supply disruptions and a bounce back from last year’s deflation.

But there is also evidence of increases among some longer duration inflation factors. For example there is a pick-up in rents with the ending of restrictions on evicting non-paying tenants. These factors could persist even as more transitory effects roll off.

This is why we believe it is too early to make the call on inflation being temporary — despite the bond market suggesting it is.

Markets

Markets remain in something of a lull due to the Northern hemisphere summer.

Last week we did see the start of what could be a correction in global equities, with higher beta growth names underperforming.

The current equity market rebound differs from other post-crisis environments – particularly the post-GFC experience — since we haven’t had any real correction so far.

This is likely due to the degree of liquidity added by central banks. It would be entirely plausible to see a correction given current uncertainty. However the US earnings season which has just kicked off promises to be quite strong, potentially providing support.

Brent Crude fell 2.6% as the OPEC deal came through, even though this assuaged the previous week’s concerns over OPEC breaking down. We expect the oil market to remain tight. Extra OPEC supply is necessary to prevent a dislocation in the market.

The Australian market played catch-up from previous week, although the gain came almost entirely from resource stocks, while tech and banks sold off. The effects of lockdowns hasn’t really hit sentiment yet. But late last week we began to see domestic cyclicals lag the market.

Infrastructure M&A dominated newsflow for the second week in a row. This time it was Spark Infrastructure (SKI, +17.4%) receiving a bid. The 20% premium offered by Ontario Teachers and private equity firm KKR was less than that offered for Sydney Airport. SKI owns only minority stakes in assets and is more heavily regulated.

Sydney Airport (SYD) gained 2.1% last week. While the board rejected the bid and struck a negative tone to selling, there were also some signals that an offer over $9 might be considered. This is steep, but the bidders have deep pockets and a very long duration timeframe in assessing return. They may well move, although the market is not convinced.

Mining and steel stocks generally outperformed on the combination of Beijing’s policy shift, some better data out of China and the prospect of large capital returns in upcoming results. Fortescue (FMG) was up 8% and BlueScope Steel (BSL, +7.48%).

Rio Tinto’s (RIO, +2.23%) quarterly report was disappointing on the production front and highlights on-going supply issues facing many metals. Nevertheless, strong iron ore prices are likely to underpin a very strong result.

Gold stocks were generally better as the gold price recovers. Northern Star (NST) gained 6.24%. Evolution (EVN, +2.63%) lagged as its quarterly highlighted near-term lower production and higher capex as they scale up the plans for their Red Lake asset.

Tech stocks were weaker, led by Afterpay (APT, -12.17%). We saw further evidence of increasing competition in the buy-now-pay-later space as Paypal entered the Australian market with a product that had no late fees.

This comes as no surprise. Rumours that Apple will enter the BNPL space with an extension of Apple Pay is potentially a much bigger threat to the sector.

Significant Features: The Pendal Geared Imputation Fund is an actively managed fund that invests in a geared portfolio of Australian shares.

Fund Objective: The Fund aims to provide a return (before fees, costs and taxes) that exceeds the S&P/ASX 300 (TR) Index over the long term.

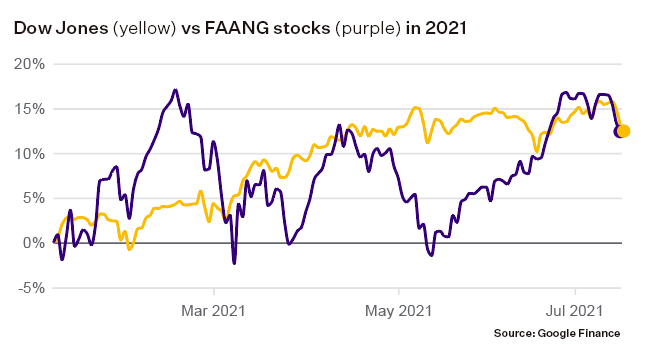

This year the Dow Jones has been keeping pace with the FAANG tech stocks — and even outperforming them. Pendal’s Ashley Pittard explains why global equities investors are looking further afield.

- Investors are looking to broaden their horizons beyond FAANG stocks.

- Inflation and wages are the critical variables.

- The world is normalising and that provides opportunities.

ASHLEY Pittard thinks the 2020s are a bit like the late 1960s and early 1970s. At least in equity market terms.

“Back then there were nice returns in equities. Inflation was increasing but it wasn’t out of control,” says Pendal’s head of global equities. “A limited number of stocks dominated the market.”

As equities appreciated in the late 1960s, and economies grew, there was a broadening out of the market, and investors looked further afield.

“The equivalent in recent years was the FAANG stocks. Everyone wanted them. But why they’ve underperformed over the last year is that growth has expanded into other areas. Commodities, for example,” Pittard says, likening the expansion to the movement beyond the “nifty 50” stocks of the late 1960s.

“What you are seeing now is that people want to own the growth stocks and rent cyclical stocks … but as the world normalises, people will be forced to own the cyclical companies.”

The big change over the past month was triggered by the US Federal Reserve.

“The Fed made it pretty clear that rates will go up and the market read that the risk of overheating had dramatically changed,” Pittard says.

It all evolves around the long-term dynamics of the market, Pittard says. Will inflation be higher over the next three to five years, than the last three to five years?

“I think it will. Interest rates are significantly lower than they have been over the past decade. Wage growth is now recovering and compounding at three to five per cent per annum,” he says. “In fact, you are seeing some fast-food companies paying up to $1,500 sign on bonuses for staff.”

“And if you look at house prices in the US, they’re at 30-year highs. House price growth is at 14.5 per cent.”

“It appears that things are getting in place for inflation to be over the Fed’s two per cent target number, and it won’t be transitory,” Pittard says.

Pittard’s fund on average only turns over 20 per cent each year. The fund managers spend time for looking for undervalued assets and waiting for them to appreciate.

“We like to buy the waterfront property when its trading at a discount and then we’ve got the patience to let things play out.”

– Ashley Pittard, Pendal’s head of global equities

Pittard gives the example of his fund increasing positions in Boeing following a series of accidents involving the 737 Max, and Airbus during the COVID crisis when airlines were on their knees.

“Today, the airlines have gotten rid of many of their old 747s, and the older pilots got axed. Now the US domestic capacity is back at 80 per cent, and recently United Airways said it wanted to buy 250 planes.”

The anecdote highlights that there are opportunities available if you are patient and can find assets that are under-valued because of the abnormal world in which we’ve been living.

“Our core tenant … is that the world is beginning to normalise. Around the world, people are starting to go out. There are fewer lockdowns and as a result people are spending more money on travel and eating out. Wage growth is getting back to normal. And that means there’s opportunities.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.