Pendal’s Sustainable Australian Fixed Interest Fund invests in social bonds that help vulnerable Australians while also aiming to generate strong returns. This is the story of a family helped by Hume Community Housing, which is financed by those social bonds.

Rudy and Judith knew early on that something was different about their twins Steven and Kerry.

When they first took them to the doctor at 12 months of age, they still hadn’t shown any sign of trying to walk or stand up.

“I knew something was wrong,” says Judith.

Steven and Kerry had cerebral palsy: a permanent movement disorder that robs sufferers of the ability to live a normal life. It often requires constant, sometimes lifelong care — usually delivered by loving family members at considerable personal sacrifice.

“Steven and Kerry’s parents have done everything for them for 60 odd years and asked for nothing – asked for no help whatsoever,” says Angela, a direct care worker for the Cerebral Palsy Alliance.

As the years went on, Rudy had to retire early because it was getting too difficult for Judith to take care of Steven and Kerry on her own.

“I was 80 and Rudy was 83 – we knew we had to do something,” says Judith.

Heart-wrenching separation

The idea of being separated from the pair was heartwrenching.

The first time Judith took the twins to respite she admits she “cried her eyes out – it was hard to let go”.

But they knew they had to prepare for the future. It was most important that the twins could be looked after in comfortable accommodation built by someone they could rely on.

Pendal Sustainable Australian Fixed Interest Fund

An Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

More than anything Rudy and Judith wanted the twins to be kept together when they could no longer look after them, Angela says.

Angela, who has been a carer for Steven and Kerry for about 15 years, put the family in touch with Hume Community Housing.

Social bonds help vulnerable Australians

Hume is a Tier 1 Community Housing Provider (CHP) which develops affordable housing for vulnerable or low-income Australians with help from investors in Pendal’s Sustainable Australian Fixed Interest Fund.

Hume is well-known for its expertise in developing and managing Specialist Disability Accommodation that caters for extreme functional impairment or very high-support needs.

Hume’s funding comes partly from the federal government’s National Housing Finance and Investment Corporation (NHFIC), which raises money by issuing social bonds to investors such as Pendal.

NHFIC lends out the money raised (more than $2 billion so far) to CHPs at lower interest rates and on better terms than banks — while providing attractive returns to investors.

“NHFIC is very important for financing, because it’s possibly as low a cost for borrowing you could ever achieve,” says Wendy Hayhurst, chief executive of the Community Housing Industry Association.

“And it’s performed very well because it’s got a government guarantee.”

A new home for Steven and Kerry

With help from Angela the twins moved into a Specialist Disability Accommodation property purpose-designed by Hume to meet their high-support needs.

The Cerebral Palsy Alliance worked closely with Hume to ensure the fit-out was purpose-built for the twins’ evolving needs and staffed with familiar faces.

After walking through the Hume property in south-west Sydney – perfectly designed for wheelchair use and built to platinum-level Livable Housing Design Guidelines – Judith felt comfortable with the decision.

But it was still hard to let them go.

“I knew it would be hard to let go of my children,” says Judith. “I thought they’d be lost without me. I was certainly lost without them.”

“[But] I couldn’t be happier. It was perfect for the twins. It kept them together.”

Rudy and Judith could live peacefully knowing the twins were well looked after in “such a lovely place” close to their own home.

After decades of sacrifice, they have also been finally able to do something they have never done before – enjoy a holiday on their own – something Judith admits “they never would have considered if the twins were still at home”.

Pendal thanks Hume Community Housing for their co-operation in producing this article. Hume is a Community Housing Provider with more than 30 years experience in providing homes and services to more than 9000 customers in NSW. For more information go to www.humehousing.com.au

About Murray Ackman and Regnan

Murray is a Senior ESG and Impact Analyst with sustainable investing leader Regnan.

He also provides fundamental credit analysis on Environmental, Social and Governance factors for Pendal’s Income and Fixed Interest team.

Murray has worked as a consultant measuring ESG for family offices and private equity firms and was a Research Fellow at the Institute for Economics and Peace where he led research on the United Nations Sustainable Development Goals.

Find out more about Regnan here

Regnan Credit Impact Trust is an investment strategy that puts capital to work for positive change.

Pendal Sustainable Australian Fixed Interest Fund is an Aussie bond fund that aims to outperform its benchmark while targeting environmental and social outcomes via a portion of its holdings.

- Retailers are resetting business models, adapting to online shopping

- E-gaming, gyms and childcare to boost shopping malls

- Property investors should take a closer look at the once-maligned sector

A SURPRISING resurgence in retailing is underway in the real estate industry as shopping malls reset around food and entertainment, fending off the threat of online vendors.

E-sports computer gaming, gyms, childcare centres and even car dealerships are driving a renaissance at shopping malls, which are emerging strongly from 18 months of pandemic restrictions and lockdowns.

Pendal’s Julia Forrest, a portfolio manager specialising in property for the Australian equities team, says during the reset forced on the sector by COVID-19 retailers closed unprofitable stores and optimised staffing levels.

It also forced landlords to the negotiating table to reset rents at lower but more sustainable levels for the long term.

“The retail sector is probably in a better position now than it was at the beginning of 2020,” says Forrest.

Amid further lockdowns across the country and the threat of a resurgence of the pandemic, the strong outlook for retail is an important and unheralded theme for portfolio construction.

Before the pandemic, the retail sector was under pressure. Sales growth was falling, shops were cutting shifts, discounting was on the rise and some retailers were closing or going into administration.

“We went into 2020 expecting rents to fall but for completely different reasons than COVID,” says Forrest.

“But the rental reset in 2020 was somewhere between 12 and 15 per cent lower.”

“You can be more certain about the cash flows with retailers going forward.”

Julia Forrest

The lower rents, coupled with government subsidies for wages, the closure of less profitable stores, higher productivity as staffing levels were reset and a move to online and omni-channel retailing, has put the sector in a better position than many expected.

At the same time, strong demand for other property assets like office and industrial has improved the relative attractiveness of malls for investors.

“You can be more certain about the cash flows with retailers going forward.”

Omni-channel approach

Forrest says shopping malls are adapting well to the threat of online shopping, moving to an omni-channel approach and lifting the experiences available at a mall.

“There’s e-gaming that has opened in one of the centres in Victoria that’s drawing in young teenage boys, which isn’t the typical target market for malls.

“They are adding childcare centres to the periphery. They’re starting to add car dealerships and things like car care and parts – the kind of thing that you’ve seen in the bulky goods category or large format retail are now moving into malls.”

Forrest says investors should keep an eye on the big asset sales in the pipeline to gauge how valuations are changing.

“The AMP assets, Pacific Fair and Macquarie Centre will probably trade, and they’ll probably trade close to book value.

“That’s a reflection of capital seeking best quality assets with good locations and optionality from repurposing.”

About Julia Forrest and Pendal Property Securities Fund

Julia has managed Pendal’s property trust portfolios for more than a decade. She has 25 years of experience spanning equities research and advisory, initial public offerings and capital raisings.

Pendal Property Securities Fund invests mainly in Australian listed property securities including listed property trusts, developers and infrastructure investments.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

SYDNEY’S LOCKDOWN dominated local news last week, but the S&P/ASX 300 fell only 0.5%.

The takeover bid for Sydney Airport (SYD) reminded us of the abundant liquidity — and propensity among long-term investors to look through Covid-related earnings issues, supporting market sentiment.

At a global macro level we saw bonds rally for the first four days of last week. This reinforces the narrative that we are through peak growth and the delta variant is exacerbating a global slowdown.

Sentiment reversed on Friday, perhaps suggesting that sentiment had turned too negative. We expect more sentiment swings through the northern summer as we wait for data on the economy and the effect of the Delta variant.

There are signs of a potential stimulatory shift in Chinese policy. This could be a positive development that supports resources in coming months.

Outlook for Covid and vaccines

The Sydney outbreak has taken a turn for the worse, breaking containment lines. We are now looking at a far longer period of restrictions.

While Covid remains contained to Greater Sydney the economic impact will be material, though not severe for the broader domestic economy.

Growth in new case numbers is tracking worse than Victoria’s second wave last year. On the plus side tightened lockdown measures, higher testing numbers and the ability of contact tracers to identify exposure sites should help. But the higher transmissibility of the Delta variant is an offsetting factor.

The Delta variant is now dominant in the US, prompting further scrutiny. At this point it appears cases will start to rise materially. The key variable is what this means for hospitalisations. Until we have greater visibility the market may continue to worry about the potential for restrictions to return.

The UK continues to run the gauntlet on new cases. So far a surge in infections has not translated into hospitalisations.

There is a growing debate about the effectiveness of vaccines and the need for boosters. Early studies on Delta indicated the mRNA vaccines were very effective — well into the 80% range in preventing Covid.

But data from Israel is concerning. It indicates the effectiveness of Pfizer in preventing Delta infections is in the mid-60% range. This is from a larger sample set than previous studies.

This could be due to the fact that Israelis had their injections four-to-five months earlier, which may suggest waning immunity and a lower efficacy in preventing infection.

The vaccines are still highly effective against severe infections. But this shows why a debate over the need for booster shots is gaining impetus.

Economic outlook

We have had a series of weaker data points for the first time in months. US unemployment, PMI data, unemployment claims and vehicle sales have all softened and money supply growth has slowed.

Much of this can be explained by holidays, shortages of certain products or labour and some hot weather. But it is a trend that needs to be watched. Along with the increasing prevalence of the Delta strain this has triggered a further flattening of the yield curve on concerns for near-term economic growth.

We need to bear in mind the link between market price action and policy.

There is a view that if inflation and growth expectations soften sufficiently – and the yield curve flattens below 100bps – we could see the Fed delay tapering. This moderating factor suggests we may be near the end of the recent rally in bonds, although a move higher is unlikely in the next few months.

In China the State Council signalled a shift in policy to be more supportive of growth. A cut in the reserve requirement ratio (RRR) for banks followed, which can help credit growth.

This is most likely in response to weak consumption. But China faces a similar challenge to Australia: low levels of immunity and a reliance on vaccines that may have limited effectiveness against the Delta strain. This could force the Chinese to maintain restrictions for longer.

Beijing’s move to prop up growth via traditional investment-related stimulus would be supportive of commodities.

Meanwhile the European Central Bank announced its policy framework.

The ECB is taking a less activist approach to inflation than the Fed. They will tolerate an overshoot of inflation targets, but won’t actively try to generate inflation. The wash-out is no real shift in Europe’s more conservative approach.

Markets

Bond yields fell for much of last week on concerns over the economic outlook, before reversing on Friday.

As a result the US 10-year Treasury yield fell only 6 bps to 1.36%. The Australian equivalent fell 12 bps to end at the same yield.

Brent crude fell 2.7% despite the lack of a deal between OPEC and its partners on increasing supply. Concerns over growth — coupled with speculation that OPEC’s cohesion may be waning — are probably at play.

Most sectors in the S&P/ASX 300 fell last week, though the index was propped up by the bid for Sydney Airport (SYD, +33.4%). Otherwise there was a relatively small spread across sectors, with growth lagging after a good run.

The bid for SYD by a consortium of pension funds was last week’s big news. The offer of $8.25 per share was a 40% premium. It values the stock at 25x EBITDA based on post-Covid FY23 earnings, versus a historical trading range of 18-21x.

This represents an enterprise value of $30 billion versus the previous peak of $29 billion. We see this as a very competitive bid in the wake of an uncertain rate of recovery in international travel and the impact of the Western Sydney Airport. There may be a higher offer to follow, but the increase is likely to be small. The bid is conditional on board approval and Unisuper agreeing to roll its 15% holding into the venture.

Tabcorp (TAH, -8.1%) announced a plan to demerge its Lotteries and Keno business by June 2022, effectively rejecting offers for its wagering business. The stock’s fall reflects the high cost of the demerger – a $225 million to $275 million one-off and $40 million ongoing.

Crown (CW, -7.8%) delivered a market update that was softer than expected. Market attention remains fixed on the Victorian Royal Commission, which has now ended and will report in October. The risk of losing its licence – as well as the potential impact on revenue from upgraded compliance procedures – will have an impact on valuations from potential bidders.

Ramsay Health Care (RHC, +0.7%) raised its bid for UK-listed private hospital group Spire. This is unlikely to change the minds of big shareholders who hold a blocking stake to prevent the deal. This leaves the company back where it started, but in a bit of strategic bind, which is reflected in the price.

A2 Milk (A2M, +10.4%) has rebounded on signs of an improvement in volume and pricing in China’s infant formula market. We remain wary. China’s low birth-rate will likely result in lower demand, while local providers continue to gain market share.

Viva Energy (VEA, +5.9%) delivered a well-received update. EBITDA was well ahead of consensus and the non-refining business is back to its previous peak profit level, despite a decline in the aviation business. This demonstrates the industry structure is helping support margins, while the company is also controlling costs. Government moves to protect refining have also removed a great deal of uncertainty.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

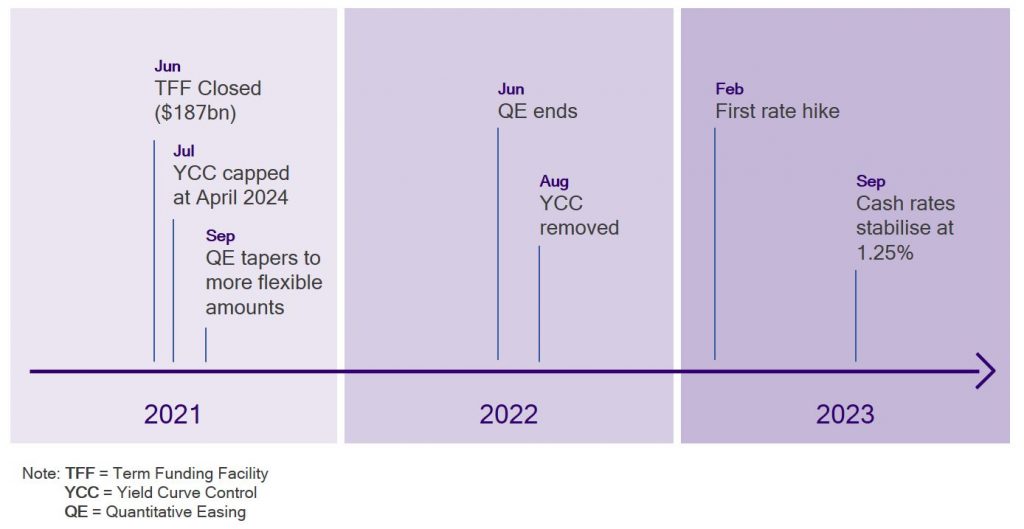

THE RESERVE BANK last week started the slow unwind of extraordinary monetary policy.

In recognition of the overall stronger economy, Yield Curve Control will not extend beyond the current April 2024 bond.

When the current $100 billion of Quantitative Easing (QE) ends in September, the pace will fall from $5 billion a week to $4 billion a week. It will be reviewed again in November.

Together with the closing of new borrowing from the Term Funding Facility (in total $187 billion lent) this represents the first steps back toward conventional monetary policy.

In our view the timeline looks something like this:

QE will likely taper further once the US Fed starts its own taper later this year.

The end of QE is probably brought forward by recent AUD weakness, relieving RBA concerns that higher rates here would push the AUD above 80c.

Of course there are a number of clear criteria laid out by the RBA to actually hike cash rates.

Inflation must be sustainably within the 2-3% band. For that to happen they believe wages need to be at least 3%, which in turn requires full employment.

The view is full employment is nearer 4% than 5%. We wrote extensively about employment and wages in our last newsletter. (Contact a Pendal key account manager for a PDF copy).

Given our views on inflation and wages we expect rates to lift-off in the first half of 2023. We expect them to stop around 1.25% to 1.5% before staying there for some time.

Of course this is a view into the future. In a week dominated by lockdowns and US bond rallies, bond markets here saw lower yields.

There is a lot more to play out in US employment markets in the months ahead.

Unlike Australia where jobs are now higher than before Covid, the US still has 8.5 million jobs “missing”.

The bulls blame higher welfare payments discouraging people from returning to low-paying jobs. The bears suggest COVID has shown the way for businesses to permanently operate with fewer staff.

The truth is likely a bit of both.

How this plays out in the months ahead will set the tone for bonds markets and eventually equity markets.

We will dive deeper into this topic in the weeks ahead.

About Tim Hext

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Alex is responsible for credit research coverage of Infrastructure, Utilities, and Financials.

Before joining the team, Alex spent seven years as a Primary Analyst at S&P Global Ratings, focusing on infrastructure, utilities, and general corporate issuers in Australia and New Zealand.

Prior to his role at S&P, Alex worked for three years as a Senior Analyst in the Audit Division at Deloitte Australia.

He holds a Master of Philosophy in Economic History from the University of Oxford and a Bachelor of Commerce from Monash University.

Alex is also a CFA Charterholder.