Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

WHILE the NSW victory in the NRL State of Origin was impressive last weekend, another important interstate contest is now underway — the state budget updates.

We’ve had two states come in with their 2021-22 budgets in the past week — NSW and South Australia.

State budgets do matter to investment managers. But before we look at what they mean, it’s important to remind ourselves on one crucial and massive difference between the states and the federal government: the states do not have a printing press.

They cannot simply print money to meet a repayment. They must first earn or borrow money before spending it.

The federal government (thru the Reserve Bank) can simply create money with a keystroke. The only reason they tax is to drain money they have spent from the system, with the aim of limiting inflation.

This creates very different dynamics when building a budget for a state versus the federal government.

States should aim to run balanced operating budgets through the cycle. Like all of us they must “live within their means”.

For the federal government the notion of a balanced budget is irrelevant. The only question they should ask is: does the budget help produce full employment without inflation being too high? If this means creating and spending more money than is drained through taxes (a budget deficit), then so be it.

The budget position is merely an accounting result of attempting to strengthen the economy — or if inflation is too high, slow it down.

Therefore the federal government is to be applauded for finally catching on that they need to keep spending despite an improving economy — as they did in the recent budget. We are not yet at full employment and we do not have an inflation problem, so why would you stop?

The states in Australia are primarily public service providers – health, education, police and so forth. No income or company taxes and no (or few) welfare payments.

These services are less dependent on economic cycles, so the tax and spending base of states should also be less dependent on economic cycles. That’s one of the reasons taxes such as stamp duty and payroll are inefficient, while a land tax and GST are preferable. (Good luck with the politics though.)

Recent operating budgets are improving, but borrowing is going higher in NSW

That brings us to the state budgets.

The improving economy is seeing operating budgets improve. South Australia should win the race back to a balanced budget in 2022-23 (if we exclude Western Australia). NSW and Queensland are forecasting balanced budgets in 2024-25. Victoria will be the laggard, forecasting deficits over a four-year forecasting period.

Following recent elections Tasmania will come out in August and Western Australia in September. In Perth they are probably too busy counting all the cash to hurry with a budget that is already well into surplus and moving higher.

For bond investors the operating position is only part of the equation.

Rating agencies put a high importance on it because it shows the sustainability of debt. But it is infrastructure spending — in General Government and State Owned Corporations — that largely drives funding tasks.

On this account all states are still going hard. NSW alone is spending $27 billion this year and around $108 billion over four years. This should see public sector investment continue to grow at 5% a year, helping drive overall GDP growth.

The NSW funding task announced last week actually moved higher despite an improved operating position. It seems they are now borrowing to put money into the NSW Generations Fund (NGF), rather than merely using asset sales.

Given ratings agencies allow them to use the NGF to offset gross debt for their metrics, it seems like a free kick. Borrow at 2% and invest in riskier assets assuming a 6-7% return.

Like the federal government’s Future Fund this is essentially a credit arbitrage which should work through the cycle. However the federal government used the one-off windfall of Telstra and budget surpluses to seed the Future Fund, rather than current borrowings. If this pays off it is ultimately good for NSW. But it does increase the state’s exposure to the economic cycle and asset prices.

Wages are making a comeback

The other important change from the NSW budget is the reinstatement of the 2.5% wage increase.

This has been in place from almost day one of the LNP Government in 2011, but was put back to 1.5% last year. The NSW government is Australia’s biggest employer with more than 400,000 workers. Even the federal government has removed its 2% wage cap, now linking it to private sector outcomes.

This all leads us to think the RBA wage forecasts of 1.75% this year and 2.25% medium term are far too low —particularly as unemployment falls to 4%. We expect 2.5% wage growth this year and above 3% by 2023.

Risk reward remains underweight semis

Our portfolios are generally underweight semi (state) governments with a bias to holding West Australian and Tasmanian bonds.

Despite ratings pressures we never worry about getting repaid due to the federal government’s implicit support.

However two positive forces behind outperformance of semi governments in the last year – RBA Quantitative Easing and Bank Balance sheet Liquid Asset purchases – are likely to taper in the year ahead.

These factors, together with high borrowing tasks, mean the cost of borrowing relative to the federal government should move higher.

We expect semi-government spreads around 15 to 20 basis points higher in the medium term.

About Tim Hext

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

THE MARKET spent last week digesting the shift in Fed messaging.

The S&P 500 rose 2.8%, while the S&P/ASX 300 fell 0.8% as sentiment wavered in the face of the Sydney lockdown.

The US economy remains strong heading into its reporting season. We are also seeing economic and earnings momentum build elsewhere in the world.

Coupled with a stable bond market and receding fears of a policy mistake this bodes well for markets grinding higher.

Covid and vaccines

The key question is how the Sydney outbreak and the impact of the Delta variant will affect domestic economic re-opening.

Cases are likely to spike in the next few days while the lockdown takes effect. The lockdown in the Northern Beaches outbreak last Christmas led to a deceleration in case growth within a week.

The higher transmissibility works against containment. But on the positive side improved track-and-trace capability means there are fewer unknown cases leading to unexpected outbreaks than in previous instances.

Uncertainty remains elevated. But on balance we do not expect the overall market to fall on fear of the economic consequences of a more severe lockdown.

The regularity of these outbreaks prevents any earnings momentum building in the re-opening related stocks. We do not expect the most exposed re-opening trades to outperform until we are further along the vaccination path.

Impact of the delta strain

The big issue is whether the delta variant changes the outlook for growth in Australia and globally.

Will there be more widespread outbreaks in Australia? Will this more contagious strain lead to a slowing of momentum in the US and Europe?

On the former, we think the speed of response means we’re unlikely to see a repeat of last winter’s Victorian experience. We are also better prepared medically.

Globally we are still tracking the effects of delta strain outbreaks. The UK continues to experience only limited growth in hospitalisations despite a surge in new cases. This reflects the effect of vaccinations, though it could still change.

New cases in the US have plateaued. The delta strain is likely to become dominant there in the next few weeks. It is particularly prevalent in areas of the mid-west and north where there are low vaccination rates. We will need to watch the impact on hospitalisations in the next few weeks.

The higher transmissibility of delta raises the threshold on herd immunity.

In the US it’s believed up to 20-25% of the population has already had Covid. With vaccinations at 53% we may still be quite close to herd immunity. This will need to be tracked.

Economics and policy

US economic data remains strong. Companies are running low on inventory and struggling to replenish in the face of strong consumer demand.

There are signs that excess savings are being put to work. Personal consumption has held up despite the end of fiscal aid. There is a rotation of spending from goods to services as mobility increases — and a great deal of scope for this to play out further.

All this should provide a good outcome in the upcoming earnings season in the US. Australia will be different due to the stop-start nature of our re-opening.

On the policy side key Fed members assuaged market fears on a pivot in policy. The key message last week was that having effectively achieved their goal on an inflation overshoot this year, they will not need to see inflation remain above target thereafter.

They also acknowledged they are factoring the risk of higher-than-expected inflation into their deliberations.

These messages reinforce the view that the Fed is not as potentially reckless as some had feared.

In this context speculative trades such as crypto could come under more pressure.

The counter argument remains that the Fed does not have the degree of control it currently believes, given the combined degree of fiscal and monetary stimulus. But this will not be apparent for some time.

Elsewhere in the US the odds of a bipartisan infrastructure bill are rising, however it is not expected until the Northern autumn.

The Australian labour market continues to do better than expected. Overall employment is back above pre-Covid levels. Full-time employment has rebounded better than casual labour. Regional areas are doing better than cities, which reflects the effect of lost tourism and a strong mining sector.

Slack in the labour market is becoming a lot more limited. Measures of “excess” workers — those working few hours due to economic reasons — have returned to pre-Covid levels. The number of jobless looking for work has also fallen to eight-year lows.

This makes it difficult to see how the RBA continues with the mantra of no rate rises for the next three years.

Markets and stocks

Markets remained largely benign. US bond yields rose a little following the strong rally. Commodities were generally stronger and growth sectors continued to lead US equities higher.

Last week we saw rotation to tech growth names and miners in the local market. Financials and health care were the weakest sectors. The latter was dragged down by CSL (CSL, -6.7%).

CSL was hit by a ruling in the US that Mexicans crossing the border to give paid plasma donations will be considered illegal work. This could have an impact of 5-8% of CSL’s total collections. Plasma collection recovery has been a key factor in the CSL’s bounce, so this sets back the company.

Oil Search (OSH, -5.5%) fell despite oil price strength as the Abu Dhabi sovereign wealth fund divested part of its stake. We continue to remain positive on the oil sector given very favourable supply and demand dynamics.

Banks underperformed, led by Bendigo Bank (BEN, -5.1%) and Commonwealth Bank (CBA, -4.3%), which reflected weakness in the US financial sector the previous week, in response to the Fed’s more hawkish tone.

Insurers were also weaker, with QBE (QBE) off 3.8% and IAG (AG) down 3.4%. This was partly in response to Victorian floods and news that the High Court had rejected the insurance sector’s appeal against having to pay out on Covid-related business continuity claims. This issue is not yet settled, given there are still very few test cases.

Afterpay (APT, +12.8%) continued its run. This was partly given its high leverage to the rotation to growth. It also announced the launch of a “shop anywhere” option which will allow some customers to pay in instalments at non-affiliated merchants in the US. This is initially limited to 11 retailers including Amazon and Nike, with Afterpay benefiting from referral fees. The market also liked Paypal’s decision to increase prices 25% for their buy-now-pay-later service in the US. This only applies to a small percentage of their gross merchandise value (GMV) — mainly small businesses who do not have a negotiated price. The true impact is debatable, but it does reduce one of the competitive risks for APT.

Boral (BLD, +8.3%) announced the sale of much of its North American business at a higher price than most expected. We also saw the next act of the Seven Group (SVW, -5.8%) takeover offer play out. SVW raised its offer price for BLD stock (to $7.30 or $7.40 depending on the take-up) and extended the offer period.

Mining stocks bounced back as commodity prices rebounded. Independence Group (IGO, +5.6%) did best, followed by South32 (S32, +5.4%). Other deep cyclicals such as BlueScope Steel (BSL, +5.0%) did well on this trend.

Woolworths (WOW, -0.1%) de-merged its liquor and hotel business Endeavour Group (EDV, +1.3%) without triggering much of a stock response. We remain cautious on EDV — capital intensity and regulation both loom as potential headwinds. WOW now trades on about 28x price to earnings, which is high given the limited growth.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

The US Federal Reserve hit back last week against the view that they were complacent on inflation.

There was no explicit message on tapering out of the latest meeting of the Fed’s monetary policy arm, the Federal Open Market Committee.

But the “dot plot” of the committee’s rate expectations — and the language in an accompanying statement — were clearly more hawkish than the market expected.

The US yields curve flattened in response. Two and five-year yields rose, while 10-year yields were flat and 30-year yields fell. This also triggered a rally in the US dollar.

In the equity market we saw a sharp rotation out of cyclicals and commodities and into technology. Overall the S&P/ASX 300 was up 0.7% and the S&P 500 was down 1.9%.

Economics and policy

The key point in the Fed release was a shift in the FOMC “dot points” — a chart that outlines interest rate expectations of the 12 FOMC members.

The median view of the committee shifted from zero to two expected hikes by the end of 2023. The three senior committee members are all apparently expecting at least one hike.

The median inflation forecast for 2021 shifted up markedly from about 2.2% to about 3%. This is still considered transitory. Fed chair Jerome Powell noted the recent retracement in the lumber price, for example.

As a result expectations for 2023 CPI remained constant at about 2.1%.

This suggests average inflation will return to where the Fed wants to see it earlier than they previously thought, which explains a shift in the first expected rate hike.

All this should be considered in the context that the Fed has been as inaccurate as anyone else when it comes to forecasting the path of rates, based on its historical predictions versus actual outcome.

There was also a change in the wording of the release, which suggested the tapering decision was no longer more than six months away.

The Fed’s hawkish tone gave the market more confidence that inflation will be contained. Break-even inflation expectations fell, which prompted flattening in the Treasury yield curve.

Yield curve shift

The shift in the yield curve was material, which probably reflects the strength of the consensus position towards inflationary trades.

The debate now is whether this is just an adjustment in signalling or a more significant pivot in the Fed’s stance. Statements this week will be important to watch.

The Fed is unlikely to want any further flattening in the yield curve. So we would not be surprised to see the messaging shift subtlety back to promoting growth.

The US dollar rose along with the short end of the yield curve. This shift in Fed signalling probably means the USD will remain well supported for a period.

This weighed on commodity prices, particularly in crowded trades such as copper, which fell 8.3%. Gold was off 5.8%.

The fundamental supply-and-demand equation remains favourable for commodities. Our medium-term view remains positive, but we may see some near-term weakness as the consensus inflation trade is washed out.

Impact on portfolio construction

This all led to the inevitable rotation towards growth stocks, notably technology.

For the moment the strong rotation from growth to value that began in November looks to have played out.

Instead, in recent months we have seen momentum swing between the two. This emphasises the need to remain balanced in portfolio construction.

We have been adding to our growth exposure in recent weeks to hedge such a policy risk. But we remain underweight more traditional rate sensitives such as REITs.

In commodities we prefer energy to metals at this point. We see fundamentals in energy as a bit more supportive, while it has also been a less crowded trade.

Covid and vaccines outlook

We continue to monitor developments around the Delta variant of Covid, given its potential for larger outbreaks and a higher vaccination threshold for herd immunity.

The UK is the bellwether in this regard. So far a rise in cases has not fed through to higher hospitalisations. This is potentially due to Delta being more benign than the original strain. The level of vaccinations may also be playing a role.

The latest Australian outbreak needs to be monitored, given the slow rollout of vaccines.

The risk of further restrictions has risen. Domestic re-opening trades are struggling to perform in this context. There is a clear divergence from global re-opening exposures. But we are mindful that sentiment can swing quickly in this regard.

Markets

It is important to emphasise that the Fed’s hawkish bent does not mean markets have peaked for this cycle.

First, the broad policy environment remains supportive. We are still looking at two years of near-zero rates and monetary policy has a large lag. Fiscal policy also remains high stimulative.

Second, we can be guided by history. The first hike in a cycle normally prompts a market correction. However the actual peak tends to occur after rates have risen a number of times.

Some speculative excess has been cleared out and the rotation is significant. However equity markets overall seem to have digested the Fed’s shift quite comfortably so far.

US 10-year Treasury yields fell by a basis point last week, while two-year yields rose 11bps to 0.26%.

The divergence between oil and copper is interesting. Copper is off 11.1% for the month while Brent crude is up 6%. Again, this probably reflects consensus positioning in recent months.

The Australian market was dominated last week by thematic rotation. Technology (+12.4%) and Health care (+6.2%) led, while resources dragged down Materials (-4.7%).

Banks (+2.2%) held up reasonably well, in contrast to overseas markets. There may be some near-term vulnerability here.

Gold miners led the underperformers. Northern Star (NST, -13.9%) was the worst in the ASX 100, followed closely by Newcrest (NCM, -8.4%) and Evolution (EVN, -8.1%).

Copper miner Oz Minerals (OZL, -12.2%) also lagged.

Contractor Downer (DOW, -7.2%) also fell, following a broker note which highlighted wage pressure in the contracting space. We do not agree with the conclusion that wage pressure seen in the Pilbara can be applied to expectations for other industries and locations across the country. DOW continued with its stock buy-back, which also suggests this is not the issue some fear it to be.

ResMed (RMD, +12.5%) was the best in the ASX 100. In this case the growth rotation was augmented by news of a product recall from a competitor.

Afterpay (APT, +10.5%) is the most leveraged to the growth trade at the moment. Xero (XRO, +6.1%) also benefited.

A stronger US dollar is beneficial for Ansell (ANN, +9.4%), Cochlear (COH, +4.8%), James Hardie (JHX, +3.6%) and RMD, among others.

Finally, Coles (COL, -1.9%) held a strategy day which flagged that capex will need to rise to compensate for under-investment in recent years. Capex will rise from 2% to more than 3% of sales per year.

This raises questions for the supermarket sector as rising capital intensity may dilute returns. COL also signalled that they are seeing the trend to more neighbourhood style unwinding, although in the current environment we doubt this is material.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

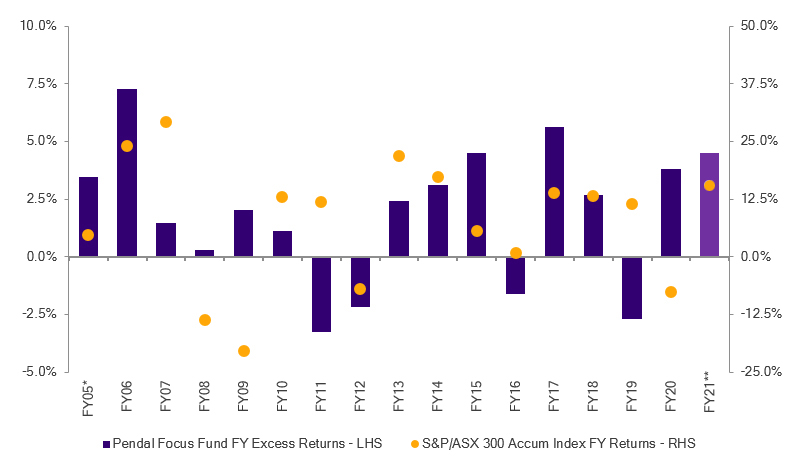

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Increase to the Fund’s management fees and costs

The Fund’s financial year 2022 (FY22) estimated management fees and costs are 1.41% p.a. of the assets of the Fund. The estimated management fees and costs have increased from 1.28% p.a. of the assets of the Fund in financial year 2021.

The increase is due to the fund experiencing higher estimated transaction costs. The Fund’s FY22 estimated transaction costs net of any amount recovered by the Fund’s buy-sell spread increased by 0.13% p.a. to 0.17% p.a.

Transaction costs are incurred when buying and selling the Fund’s underlying securities and are paid out of the Fund’s assets. These costs are reflected in the daily unit price and are not charged to you as an additional fee. Transaction costs and buy-sell spread may vary from year to year depending upon market conditions, the market impact of transacting and volumes traded.

There has been no change to the Fund’s management fee of 1.22% p.a. or estimated expense recoveries of 0.02% p.a..

Key points

- Paul Hannan and Noel Webster will step down as Senior Portfolio Managers of Pendal’s Smaller Companies team from today.

- Over 17 years Paul and Noel have together built a well-respected and highly successful franchise. The Smaller Companies Fund has delivered 11.55% pa after fees since they took over management on April 1, 2004. The Microcap Opportunities Fund has returned 23.87% pa since its launch in March 2006. Both have significantly outperformed their benchmark, the S&P/ASX Small Ordinaries index (source: Pendal at Apr 30, 2021).

- Pendal’s emphasis on team development and a disciplined process has laid a strong foundation for the next stage in the franchise’s evolution.

- After more than three years as Portfolio Managers, Lewis Edgley and Patrick Teodorowski take over full management of the Pendal Smaller Companies and Pendal Microcap Opportunities portfolios from today.

- Paul Hannan will continue as an analyst until the stock coverage transition is completed. This is expected in 2022.

- Noel Webster will step down from the team as soon as the handover of his stock coverage is completed within the next two months.

- Edgley and Teodorowski also become Co-Heads of Smaller Companies in Pendal’s Australian equities boutique, reporting to Head of Australian Equities, Crispin Murray.

TODAY Pendal announces the next stage in a Smaller Companies portfolio management transition which began in 2017.

From June 21, Lewis Edgley and Patrick Teodorowski take over full management of Pendal’s Smaller Companies team.

Edgley and Teodorowski have been Portfolio Managers for the fund since early 2018. Over the past three years they have taken increasingly greater responsibility for the portfolio’s trading, position weightings and construction. They now take full responsibility of the team and portfolios.

Pendal’s Australian equities team has a culture of accountability, granting team members the opportunity to prove themselves.

Paul Hannan and Noel Webster successfully executed this approach, focusing on development within the Small Cap strategy. Edgley and Teodorowski have been with Pendal for eight and 11 years respectively. Their progression reflects our focus on development.

This transition is the next stage of the smaller companies evolution and demonstrates Hannan and Webster’s focus on succession planning and their confidence in leaving management of the funds in the hands of Edgley and Teodorowski.

The Smaller Companies team is a vital part of Pendal’s broader Australian equity boutique – in terms of the portfolios they run and the company research that feeds directly into the midcap and broadcap funds.

Edgley and Teodorowski will work closely with Crispin Murray and other portfolio managers in the boutique, building on a long track record of success and excellence in our small cap capability.

The team will continue to be assisted by analysts Rachel Cole and Damien Diamant. Another analyst is expected to be appointed shortly.

A monthly insight from James Syme and Paul Wimborne (pictured), managers of Pendal’s Global Emerging Markets Opportunities Fund

- There are three broad drivers of the recent commodity boom: a natural demand bounce-back after 2020, US economic stimulus, and Chinese economic stimulus.

- Here we review the prospects for each and discuss our portfolio positioning around the commodity rally.

COMMODITY price moves have been one of the most significant parts of markets pricing in a post-Covid global economic recovery.

As we’ve mentioned before, commodities are a major driver of returns for emerging market (EM) equities as a whole. They’re also a major differentiator of returns among different parts of the asset class.

We feel there are three broad drivers of the recent commodity boom: a natural demand bounce-back after 2020, US economic stimulus and Chinese economic stimulus.

Here we review the prospects for each and discuss our positioning around the commodity rally.

Demand bounce-back

Pent-up demand during lockdowns created a huge demand shock as restrictions and trade interruptions began to ease.

This was particularly noticeable in the housing and construction industries with long lead-times and big price increases on products such as construction lumber, windows and bricks.

One trackable index for this is the US CME lumber future, which rose from US$400/lot at the start of 2020 to more than US$1600/lot in May.

There’s also been a surge in demand for smart, programmable or connected devices, leading to real pressure on the availability of some semiconductor components.

One benchmark, DRAM memory chip, climbed to US$4.60 from US$2.60 in August 2020.

US and Chinese economic stimulus

US and Chinese economic stimulus is the other driver of the commodity boom.

Investors face a complicated world. The biggest economy has broken with 40 years of generally deflationary fiscal and monetary restraint, just as the second-biggest economy has significantly tightened policy.

The Biden administration moved quickly to pass a US$1.9 trillion stimulus package, and is now preparing a US$6 trillion budget that will very substantially increase the rate of investment by the government sector in the US economy.

Meanwhile, as we noted in December, China has moved to end an acceleration in money supply growth and credit growth that began in mid-2020.

Fiscal policy was tightened, which naturally reduces credit growth. We also saw a disappointing Q1 GDP growth rate of 0.6% quarter-on-quarter and a decline in shorter-term bond yields as markets priced in the slowdown.

In this environment it is hard to see where commodity prices might go from their current elevated levels.

Historically a slower China is bad for commodity prices. But this has always been in an environment of tight US fiscal policy.

In terms of where commodities might go — and how to manage exposure in emerging markets — we make the following observations:

1. China’s dominant role in commodity demand

The dominant role of China in terms of global commodity demand and its historical importance to commodity prices should not be dismissed.

When taken alongside the ability of market systems to increase supply in the face of high prices, we would not be surprised to see a meaningful pull-back in commodity prices at some point this year.

2. Not all commodities are the same

It’s important to note that not all commodities are the same. Agricultural products in particular can display a very strong supply response to high prices as farmers’ planting decisions are affected.

In addition some commodities are more exposed to Chinese end demand (steel, coal) and some more to US end demand (particularly oil).

The oil price has risen strongly in the past year. As oil companies struggle to add production capacity — in light of Environmental, Social and Governance (ESG) restraints — we feel there is probably more upside to the oil price than to industrial metals from this point.

3. Correlation between equity and commodity prices

Although the share prices of most commodity-producing companies in emerging markets have risen strongly, there remains a high correlation between those share price moves and moves in the prices of the respective underlying commodity products.

These shares offer exposure to commodity prices, but nothing more.

We have exposure to commodity-producing companies in sectors such as oil/gas, wood pulp, cement and gold. But in every case we have a clearly identified additional catalyst that we expect to come through — as well as the supportive environment for commodity prices.

For example, for Brazilian oil and gas producer Petrobras we believe the market has mispriced when (and even if) domestic product prices deviate from import parity prices. Meanwhile in the first quarter of 2021 the company had free cash flow equal to 10% of its market cap.

At Brazilian pulp and paper company Suzano, we feel the company’s substantial progress in ESG has not been recognised by analysts yet. At Mexican cement maker Cemex we feel the rapidly improving European operating environment is not yet in consensus estimates or priced into the share price. And so on.

4. Opportunities in other sectors

Fourthly, the macro-economic impact of commodity prices creates opportunities in other sectors in certain countries.

Followers of our strategy will be aware of our increased allocation to Brazil and South Africa. Recent economic data and corporate results show robust demand growth there — particularly from South African financials and retailers.

We also note that strong economic recoveries are underway in the UAE (where we have maintained our position) and potentially in Russia (where we are currently underweight).

One of the great attractions of emerging market equities is the global macro exposures the asset class offers. One of the great strengths of a top-down approach is an ability to find preferred opportunities within this view.

The overall environment for cyclical assets remains robust, both for commodities and emerging market equities.

But as always we feel it pays to be selective.

Download this article as a PDF.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

Find out more about Pendal’s fixed interest strategies

THIS week we saw strong economic numbers — here and in the US — turbo-charged by fiscal stimulus.

Australia’s May employment update reported 115,000 new jobs created, including 97,000 full-time. Jobs are now 1% higher than before the pandemic.

Unemployment fell from 5.5% to 5.1% despite a rise in participation. Importantly underemployment (part-time workers looking for full time hours) fell to 7.4%. This level was last seen in January 2014.

Underemployment has had a stronger correlation to wages in recent times so it lifts the chances of decent wage gains.

On the topic of wages the Fair Work Commission this week passed down a 2.5% increase to the minimum wage —from $19.84 an hour to $20.33 an hour.

This affects about 2.2 million workers. They must have gotten the decision about right as employer groups and unions seemed as unhappy as each other. There was a tip of the hat to Covid impacts with delays on the increase until November for some industries.

The pace of the recovery continues to catch the RBA by surprise.

In February the Reserve forecast unemployment to reach 5.25% by June 2023. Given an opportunity for revision in May they predicted 5% by December 2021. They effectively reached it in the same month as the re-rating.

While forecasts are playing catch up the RBA seems more than happy to leave the narrative way behind. In a speech this week From Recovery to Expansion, Governor Philip Lowe noted the improvements but held the line that “inflation pressures remain subdued and are likely to remain so”.

Time will tell, but after hearing the central bank tell me consistently for 30 years that inflation has a long lag to activity it’s hard to see how today’s low inflation is a good predictor of inflation a year from now.

Strong US inflation numbers

Late last week the US printed another series of strong inflation numbers.

Year on year CPI is now 5% and 3.8% ex food and energy. There are some base effects from this time last year but the moves were broad-based and finally seemed to catch the Feds’ attention.

The previous set of numbers brought out a round of Federal Reserve speakers talking about “transitory” inflation.

This time the Fed seemed to be paying attention.

In a press conference Fed chairman Jerome Powell said: “as the reopening continues, shifts in demand can be large and rapid, and bottlenecks, hiring difficulties and other constraints could continue to limit how quickly supply can adjust, raising the possibility that inflation could turn out to higher and more persistent than we expect”.

To paraphrase, as we said earlier “transitory” will be measured in years, not months.

Markets were quick to price in earlier rate hikes in the US, helped by the Fed dots predicting earlier hikes.

Terminal rates were less affected as the yield curve flattened. It seems the Fed narrative has changed from being way behind the curve to maybe keeping up with it — limiting the chance of a major policy mistake unleashing longer-term inflation.

For now the US dollar is rallying because it seems the Fed may be well ahead of the rest of the world in tightening. Only New Zealand might beat them to it in the developed world.

The RBA has a chance for a reset in early July, although the capping of Yield Curve Control at April 2024 now seems a foregone conclusion.

Overall it is negative for bonds, but February saw the major re-rating and the surprise factor is diminishing.

We expect rates to gradually climb while not moving higher than what we saw in late February.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

BONDS continue their counter-trend rally despite US inflation data again coming in higher than expected last week.

US 10-year yields fell another 10bps to 1.45% — down 30bps from their highs. The Australian equivalent fell 20 bps to 1.49%.

Falling yields saw growth stocks resume leadership in equities last week. The S&P/ASX 300 gained 0.3% while the S&P 500 was up 0.43%.

Macro and policy

Many reasons are offered up for the recent bond price rises:

- Economic growth slowing after the peak of April/May

- Softer-than-expected employment data

- The “fiscal cliff” of 2022 as stimulus rolls off, dampening recovery and subduing inflation

- Potential for the Fed to discuss tapering in its next meeting

- Belief that supply disruptions will be temporary

- Covid resurgence holding back Asian and emerging market recoveries

- Monetary tightening in Beijing

- Carry trades from other currencies supporting bond demand

All these factors are likely playing a role to some extent. The employment data in the US is particularly important, as an exemplar of a string of economic data that has surprised on the downside.

Though perhaps the most important factor is little-discussed: the demand and supply of Treasury bonds.

In Q1 2020 the US Treasury issued US$342 billion in bonds. Of this the Fed purchased US$254 billion as part of Quantitative Easing (QE). In Q2 Treasury issued only US$70 billion since they had effectively drawn down on the cash balances built in Q1 to fund stimulus.

However the Fed’s QE has continued at the same rate of about US$250 billion for the quarter.

This has effectively engineered a strong bid in the Treasury market, in an environment where many had positioned away from bonds.

The danger could be in reading higher bond prices as a macro signal that inflation concerns have been tamed.

We do not agree.

The technical supply/demand factors may be clouding the signal from bond prices. But the underlying economy remains strong. We see the debate around inflation as still very much alive.

US CPI data

In this vein, US CPI data for May was again stronger than expected. Headline inflation was 5% year-on-year and +0.6% month-on-month. Core inflation was 3.8% and +0.7% respectively.

The market took this in its stride, mainly because price growth was concentrated in transient areas such as air fares, used cars and apparel.

There were less benign components as well.

For example total rent ticked up. This is relevant because it tends to be a longer cycle part of inflation. It had been running at 2%, but is expected to rise to 4% as the surge in house prices feeds into the owner’s equivalent rent part of the equation.

Fast food prices also rose. Although it’s not a big part of the basket, this reflects higher input costs and labour costs passing through to consumers. It’s another thing to keep watching.

Investor and Home Depot co-founder Ken Langone said last week that a number of his businesses were battling the worst labour shortages in 50 years.

The costs of equipment, labour, spare parts and fuel were all rising, he said. His businesses were demonstrating pricing power but it wasn’t having any negative effect on demand.

Against a backdrop of near-zero rates, there is an argument we may not get a natural petering out of activity and easing on pricing pressure to subdued levels before 2024.

This could particularly be the case when factoring pent–up demand, excess savings and wealth increases.

Capex investment

Meanwhile we need to watch investment in capex, which has the potential to surprise on the upside.

Surveys suggest a surge in capex plans in the US. Part of this is tied to investment in clean energy. But companies will also need to spend on capacity to replace Chinese supply of products such as steel and aluminium as Beijing shifts from its role as the world’s provider of energy-intensive products.

In this environment we continue to see appeal in commodities. The sector can benefit if inflation recedes, allowing policy to stay loose and growth strong. Alternatively, it should be a beneficiary if stronger inflation starts to emerge.

Several commodities have already run hard, so it is important to be selective. We still see opportunity here.

This week the Fed meets amid speculation about its approach to tapering QE bond purchases. We suspect some indication that it will start investigating the possibility of tapering, in keeping with recent signals.

COVID and vaccines

The overall environment continues to improve. New daily cases in India have dropped to about 20% of peak levels. Europe and the US remain low. Numbers in Brazil and Asian nations with recent outbreaks appear to be stabilising.

The main concern is spread of the Delta variant in the UK which could be a lead for other countries. This more transmissible version has seen a tripling of cases from the lows and will likely delay the final stage of reopening on June 21. It is raising the threshold for vaccinations to reach herd immunity.

Markets

After a strong run equity markets have been broadly consolidating since mid-April. Bond yields have fallen, commodity markets risen, earnings revised higher and liquidity remains abundant.

New Covid variants are causing significant concerns. But vaccines remain very effective and supply is increasing.

We would not be surprised to see markets move higher through the northern summer.

The Australian bourse saw a rotation to growth names last week as bond yields fell.

Information Technology rose 6.9%. Bond-sensitive sectors such as REITs (+2.2%) and Utilities (+2.9%) outperformed to show some signs of life.

This rotation came at the expense of Financials (-1.9%), which led the market in the last six months.

Last week’s move closed the gap in performance between Financials and Technology. But the former is still about 27% ahead in 2021 and there is potential for more.

AUSTRAC announced investigations into Star Entertainment (SGR, -4.5%) and Crown Resorts (CWN, -3.7%) for alleged breach of anti-money laundering regulations. The Victorian Royal Commission inquiry into Crown was also extended.

The potential for more onerous regulation is rising. But a push for cashless casinos, which can help combat money laundering, is complicated by the presence of slot machines in pubs and clubs.

AUSTRAC also launched a formal enforcement investigation into National Australia Bank (NAB, -3.8%).

This appears to be a case of the regulator losing patience after long negotiations. The issues do not look as serious as those at Westpac (WBC, -2.2%) and there are currently no civil penalty proceedings. Nevertheless this could lead to a significant step-up in compliance costs.

The rotation to tech saw the rest of the banking sector fall. Bendigo and Adelaide Bank (BEN) was down 4.1%, ANZ (ANZ) lost 3.3%, Bank of Queensland (BOQ) fell 2.6% and Commonwealth Bank (CBA) dropped 1.1%.

Altium (ALU, +28.6%) was the best in the ASX 100 last week. The rotation to tech was augmented by a takeover bid from US company Autodesk. This highlights a strong environment for mergers and acquisitions (M&A) amid cheap funding, a strong economic outlook and a market rewarding earnings growth. The bid was rejected.

M&A activity in the US data centre sector prompted local play NextDC (NXT) to rise 7.7%.

Afterpay (APT, +9.6%) and other buy-now-pay-later stocks benefited from the latest fund raising by Swedish competitor Klarna. It raised US$639 million from Softbank at a valuation of US$45.6 billion. This is roughly 40x its 2020 revenue.

When Klarna raised capital in March it was valued at US$31 billion. In September 2020 it was $10.3 billion. This highlights heady valuations in the sector and the amount of capital being deployed in a land grab.

Ultimately we think this will impact on margins.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Find out more about Pendal Focus Australian Share Fund here. Contact a Pendal key account manager here.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

Find out more about Pendal’s fixed interest strategies

THIS WEEK we saw rallies everywhere.

Massive fiscal and monetary stimulus continues to support “risk-on”. Bonds shared in the rally, breaking through recent ranges and increasing their recent positive correlation with equities.

It is generally difficult to isolate a single reason for market movements. Sometimes we just guess — and this is one of those times for bonds.

The best explanation I can find is the continued massive weight of money. This is creating a positive loop from very strong equities into bonds via pension fund reweighting — especially in the US.

A recent Milliman article shows that the 100 biggest US corporate-defined benefit pension plans overall are nearly fully funded (98.8% in May). This is an incredible result given they were funded near 70% on average a decade ago.

Amazing what a tripling in your equity market can do.

The opportunity to lock in a fully funded plan is not going missing this time. Last time they got there was early 2008 — so lessons have been learnt.

In Australia of course we are largely a defined-contribution retirement market. Unlike defined benefits plans, no one tracks or measures a liability.

We talk in general terms about funding retirement and we publish statistics about what is needed for a basic or comfortable retirement. But the concept of locking in risk market gains is more gut feel than defined levels.

Central banks continue to reward asset owners.

Even though we are now well past the depths of the Covid crisis, stimulus continues to ramp up.

This month banks will draw down around $80 billion of funds under the Term Funding Facility promised by the RBA last year. At 0.1% cost of funds for three years, the gifts keep giving well beyond when they were most needed.

Next month the RBA will likely begin signalling a back-off in stimulus by not extending Yield Curve Control. But importantly it will stay in place until April 2024.

Fortunately fiscal policy this time around has also helped wage owners with few assets. The past decade saw tight fiscal policy and loose monetary policy.

Not surprisingly capital boomed while wages stagnated. To paraphrase Midnight Oil, “the rich got richer, the poor got the picture”.

Finally it seems the message is getting through that fiscal policy is a far more targeted and effective means of stimulus than monetary policy.

The main way monetary policy helps is by boosting asset prices and hoping it somehow filters down. Fiscal policy can target where needed — importantly those with a capacity to spend rather than save.

For now though, central banks are keeping a foot to the floor, hoping they can pull off the Goldilocks trick of boosting asset prices and growth without too much inflation.

A difficult balancing trick — but one for now the market is happy to believe.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS continued to grind higher on limited news flow last week.

Improved sentiment on global growth pushed the energy sector ahead 8.5%, which led the S&P/ASX 300 to a 1.6% gain for the week.

There were several factors at play, including a sense that the worst overseas Covid outbreaks are coming under control. There are indications Europe will soon follow the US into a broader re-opening.

OPEC’s meeting was very short, signalling that its stance of restricted supply remains firm. Brent Crude rose 2.8%.

Covid and vaccines

Global cases continue to trend in the right direction in the US and EU — as well as some of the worst-hit countries such as India. Continued vaccine exports to under-supplied countries is boosting confidence.

US mobility levels have now passed pre-COVID highs. The EU is trending higher, which is helping improve sentiment on oil.

Economics and policy

US non-farm payroll data showed an additional 559,000 new jobs in May. This was better than April, but was still well below the jobs growth that many expected with the recovery.

There are still 7.6 million fewer jobs than before the pandemic. There is a view that on-going federal unemployment insurance top-up payments are discouraging people from job hunting. These payments are due to roll off in September.

A buffer of excess savings accumulated in the past year is also likely to be playing a role. The result is a falling workforce participation rate at a time of huge jobs supply.

Leisure and hospitality account for about 40% of the gap in jobs compared to pre-Covid. Education and health make up another 15% or so.

Wages are a big focus given latent concerns on inflation and people’s reluctance to return to work. Wages grew faster than expected in the latest data. But the year-on-year rate is still subdued at 2% growth.

The composition of wage growth is distorting headline figures to a degree. We have seen a faster return in lower-paid jobs which is depressing the headline figure.

Interestingly, leisure and hospitality is bucking this trend, with 8.8% wage growth. This highlights labour supply issues in the sector.

The debate is whether labour supply issues will be resolved relatively quickly or whether this will seed wider spread inflation.

Another point to note is that productivity is high.

The US has returned to pre-Covid GDP — with far fewer workers. This clear gain in productivity reduces the importance of unit labour costs.

These issues will play into the Fed’s policy deliberations. At this point most expect the Fed to start talking about tapering in the June meeting, without drawing any firm conclusions. The focus is on clear signalling to avoid a “taper tantrum” in markets.

We won’t return to the trend of long-term job growth until mid-2023 based on the current jobs growth rate. This is consistent with the Fed’s message of no rate tightening for two-to-three years.

This helps explain why bond markets have so far seemed comfortable with the Fed’s stance — and the benign reaction to signals around tapering.

This is supportive for equity markets, as is the ongoing growth pulse.

The US Composite Purchasing Manager’s Index (PMI) is well above its highest level in over a decade. The Global Composite PMI, while trending upward, is still below its highs.

There is scope for the Global PMI to follow the US, emphasising that there are several legs to the global recovery story. This can prolong it further than many are expecting.

Markets

Bonds remained largely unmoved last week and the broad environment was reasonably benign.

There was some movement in the commodity space. Brent crude rose 2.4%, passing a technical level that suggests it could head towards US$80. If that’s the case, it will be interesting to see what this means for bonds.

Elsewhere iron ore rose 10.8%. Copper and gold consolidated.

Overseas we started seeing gains in the Real Estate Investment Trust (REIT) sector, which has long languished. The main explanation is that it is a later cycle play on the re-opening.

In Australia the Energy sector rose 8.5% — though it’s still up only 6.8% for 2021 so far. REITs rose 2.6% domestically, but are also lagging for over the year to date (up just 6.4%).

Financials remain very consistent, up 1.6% for the week. There are some early signs of rotation from the banks (which are up 30.2% for the year to date) to the insurers.

Utilities (+5.8%) gained some respite, reflecting the local issue of higher power prices following a recent explosion at the Queensland coal-fired Callide Power Station.

Six of last week’s eight top performers in the S&P/ASX 100 were energy stocks. Origin (ORG, +15.7%) led the pack, a beneficiary of higher oil and power prices. Santos (STO) was up 12.2% and Oil Search (OSH) gained 11%.

Worley (WOR, +15.6%) had a fortuitously-timed investor day, which played to the theme of a rising oil price driving a recovery in capex in the sector. We are mindful that part of the reason oil is strengthening is a lack of new investment response.

The iron ore miners did not respond to the 10% gain in prices. This reflects some scepticism around the sustainability of price drivers, which is linked to the stimulus and economic recovery.

In contrast, sentiment remains bullish on the copper miners despite a 4.5% drop in the price last week. This is regarded as a longer-term theme related to renewable energy and electric vehicles.

Tech was the week’s loser, for no discernible reason. Appen (APX, -8.7%) was the worst performer. Altium (ALU, -3.5%) was also weak. There are signs of a base building in tech stocks in the US, although we do not expect sustained market leadership given the broader macro backdrop.

Gold stocks reflected the yellow metal’s 1.6% fall. Evolution (EVN) fell 4.9% and Northern Star (NST) was down 4.6%. We see the gold price as well supported.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Find out more about Pendal Focus Australian Share Fund here. Contact a Pendal key account manager here.