Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS continued to grind higher on limited news flow last week.

Improved sentiment on global growth pushed the energy sector ahead 8.5%, which led the S&P/ASX 300 to a 1.6% gain for the week.

There were several factors at play, including a sense that the worst overseas Covid outbreaks are coming under control. There are indications Europe will soon follow the US into a broader re-opening.

OPEC’s meeting was very short, signalling that its stance of restricted supply remains firm. Brent Crude rose 2.8%.

Covid and vaccines

Global cases continue to trend in the right direction in the US and EU — as well as some of the worst-hit countries such as India. Continued vaccine exports to under-supplied countries is boosting confidence.

US mobility levels have now passed pre-COVID highs. The EU is trending higher, which is helping improve sentiment on oil.

Economics and policy

US non-farm payroll data showed an additional 559,000 new jobs in May. This was better than April, but was still well below the jobs growth that many expected with the recovery.

There are still 7.6 million fewer jobs than before the pandemic. There is a view that on-going federal unemployment insurance top-up payments are discouraging people from job hunting. These payments are due to roll off in September.

A buffer of excess savings accumulated in the past year is also likely to be playing a role. The result is a falling workforce participation rate at a time of huge jobs supply.

Leisure and hospitality account for about 40% of the gap in jobs compared to pre-Covid. Education and health make up another 15% or so.

Wages are a big focus given latent concerns on inflation and people’s reluctance to return to work. Wages grew faster than expected in the latest data. But the year-on-year rate is still subdued at 2% growth.

The composition of wage growth is distorting headline figures to a degree. We have seen a faster return in lower-paid jobs which is depressing the headline figure.

Interestingly, leisure and hospitality is bucking this trend, with 8.8% wage growth. This highlights labour supply issues in the sector.

The debate is whether labour supply issues will be resolved relatively quickly or whether this will seed wider spread inflation.

Another point to note is that productivity is high.

The US has returned to pre-Covid GDP — with far fewer workers. This clear gain in productivity reduces the importance of unit labour costs.

These issues will play into the Fed’s policy deliberations. At this point most expect the Fed to start talking about tapering in the June meeting, without drawing any firm conclusions. The focus is on clear signalling to avoid a “taper tantrum” in markets.

We won’t return to the trend of long-term job growth until mid-2023 based on the current jobs growth rate. This is consistent with the Fed’s message of no rate tightening for two-to-three years.

This helps explain why bond markets have so far seemed comfortable with the Fed’s stance — and the benign reaction to signals around tapering.

This is supportive for equity markets, as is the ongoing growth pulse.

The US Composite Purchasing Manager’s Index (PMI) is well above its highest level in over a decade. The Global Composite PMI, while trending upward, is still below its highs.

There is scope for the Global PMI to follow the US, emphasising that there are several legs to the global recovery story. This can prolong it further than many are expecting.

Markets

Bonds remained largely unmoved last week and the broad environment was reasonably benign.

There was some movement in the commodity space. Brent crude rose 2.4%, passing a technical level that suggests it could head towards US$80. If that’s the case, it will be interesting to see what this means for bonds.

Elsewhere iron ore rose 10.8%. Copper and gold consolidated.

Overseas we started seeing gains in the Real Estate Investment Trust (REIT) sector, which has long languished. The main explanation is that it is a later cycle play on the re-opening.

In Australia the Energy sector rose 8.5% — though it’s still up only 6.8% for 2021 so far. REITs rose 2.6% domestically, but are also lagging for over the year to date (up just 6.4%).

Financials remain very consistent, up 1.6% for the week. There are some early signs of rotation from the banks (which are up 30.2% for the year to date) to the insurers.

Utilities (+5.8%) gained some respite, reflecting the local issue of higher power prices following a recent explosion at the Queensland coal-fired Callide Power Station.

Six of last week’s eight top performers in the S&P/ASX 100 were energy stocks. Origin (ORG, +15.7%) led the pack, a beneficiary of higher oil and power prices. Santos (STO) was up 12.2% and Oil Search (OSH) gained 11%.

Worley (WOR, +15.6%) had a fortuitously-timed investor day, which played to the theme of a rising oil price driving a recovery in capex in the sector. We are mindful that part of the reason oil is strengthening is a lack of new investment response.

The iron ore miners did not respond to the 10% gain in prices. This reflects some scepticism around the sustainability of price drivers, which is linked to the stimulus and economic recovery.

In contrast, sentiment remains bullish on the copper miners despite a 4.5% drop in the price last week. This is regarded as a longer-term theme related to renewable energy and electric vehicles.

Tech was the week’s loser, for no discernible reason. Appen (APX, -8.7%) was the worst performer. Altium (ALU, -3.5%) was also weak. There are signs of a base building in tech stocks in the US, although we do not expect sustained market leadership given the broader macro backdrop.

Gold stocks reflected the yellow metal’s 1.6% fall. Evolution (EVN) fell 4.9% and Northern Star (NST) was down 4.6%. We see the gold price as well supported.

About Crispin Murray and Pendal Focus Australian Share Fund

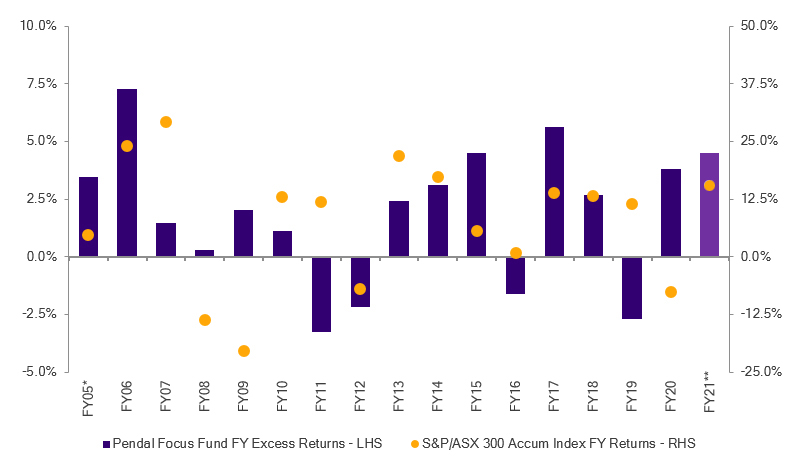

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia. Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Find out more about Pendal Focus Australian Share Fund here. Contact a Pendal key account manager here.

What does the latest GDP data mean for investors? Pendal portfolio manager Tim Hext (pictured) explains in our weekly Bond, Income and Defensive Strategies wrap.

Find out more about Pendal’s fixed interest strategies

THE WEEK’s headline act was the Q1 GDP result.

It marked the first full year since Covid-led changes, restrictions and lockdowns altered our economic landscape (and lives).

What a comeback. Most importantly, Australia’s economy has expanded as we emerge from the shadow of 2020.

Australia’s GDP is now 0.8% higher than it was in December 2019. This was driven by the 1.8% GDP growth in 2021 Q1.

It’s a strong result across most sectors and states even though pockets of the economy have not yet recovered.

Comforting: consumer spending

Sustainable economic growth always stems from a strong and stable consumer spending base. Therefore it was wonderful to see consumer spending as the biggest driver of growth in 2021 Q1.

Even better, this time around in 2021 we are spending on services instead of just goods. This is the opposite of 2020 when we were in the midst of an online spending frenzy.

Goods spending held steady with a decline of only 0.5% — instead of falling off a cliff — despite concerns about post-Covid spending patterns.

This was a case of retail services roaring back to life. Just when we thought the gift would not keep giving.

Not surprisingly, the main retail services sectors benefitting from an uplift in consumer spending were those held back during lockdown. Hotels, cafes, restaurants, recreation, culture, transport have all taken off.

Hello domestic tourism

Elsewhere in the economy the Q1 results showed that building programs already in place worked. Building approvals rose with higher levels of new building, which will feed into inflation.

The biggest upside surprise came in business investment.

After lacklustre business investment over the past decade it became easy to write off this section of the economy. But thanks to new measures allowing unprecedented property, plant, and machinery (PPE) tax write-off, private business investment rose by 4% — with 11.6% in new PPE spend alone.

This is a level of growth not experienced in more than 10 years (since Q4 2009).

Troubling: Victorian lockdown

Even as Victoria extends lockdown by another week there is no need to hit the panic button. The economy will not hit the brakes — as long as this lockdown does not extend to the same length as last year.

Experience has taught us this is not lost spending but delayed spending. Once the economy re-opens it will recover lost ground.

Furthermore, Australians now have the habit of saving for a rainy day. Household income continued to rise in Q1. Though the savings rate has eased from pandemic levels, it is still above 11%.

This is more than double the pre-pandemic, five-year average savings range of 5-6%. These savings will serve Victorians well through this lockdown and support them in the re-opening, as will the new federal support measures.

Strong tax receipts from the increase in nominal GDP driven by commodity prices and economic expansion will fund those measures. This ensures we are seeing a mere storm in a teacup.

Implications

Given the strength of Australia’s economic growth we expect the Reserve Bank of Australia (RBA) to announce in early July that it will not extend Yield Curve Control (YCC) beyond the April 2024 bond.

This supports our portfolio positioning. Kinks in the yield curve will be ironed out as the three-year futures basket sets to roll off the yield curve-controlled bonds.

Continued economic growth will support the federal budget bottom line through stronger tax receipts.

This will result in favourable demand-supply dynamics of Australian Commonwealth Government Bonds (ACGBs).

Meanwhile the eventual RBA tapering of Quantitative Easing will see Semi-government bonds underperform from current levels.

In the medium term, we favour being overweight ACGBs and underweight Semis.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

IT WAS relatively quiet on the macro front last week.

Signs that the Fed was “thinking about thinking about” tapering were absorbed without any ructions in the bond market.

It seems the local market is also content to look through the Victorian Covid outbreak and lockdown. The S&P/ASX 300 gained 2.17% last week, with good market breadth. The S&P 500 was up 1.2%.

Covid and vaccines

It’s too early to make a call on whether the Victorian shutdown will contain the latest outbreak. At this point the market seems sanguine. Travel and casino stocks have not been punished.

Overseas the biggest outbreaks appear to be improving. New case numbers continue to decline in India, the EU and the US. Brazil may also have turned a corner.

New daily cases have been ticking up in the UK where the Indian (B.1.617.2) variant is becoming the dominant strain.

We are watching new outbreaks in Asian countries such as Taiwan and Vietnam which had previously kept the virus under control.

There is some talk of a new variant emerging there, which has elements of both the Kent and Indian strains. But it is too early to be clear on this.

Macro and policy

There was little news last week. Anecdotal evidence from the US continues to demonstrate the strength of recovery and pent-up demand.

There is a growing focus on recent developments in China and the implications for resource demand. Beijing has made efforts to talk down commodity and crypto prices in recent weeks. It has also sounded warnings against speculation in property.

Data suggests Chinese credit growth is decelerating, which is seen as an important indicator for commodity demand. This issue needs to be watched.

While credit growth is slower than this time last year, the base effect of stimulus in 2020 needs to be considered. Credit growth remains ahead of 2019.

Meanwhile 10-year bond rates remain very low and the RMB has been appreciating, which helps purchasing power. The global economic recovery will boost the Chinese manufacturing sector.Despite some restraining measures at the margin, we think Chinese policy remains supportive and is unlikely to be the catalyst of a significant correction in commodities.

There have been notable developments regarding oil — all of which are likely to constrain medium-term supply and support prices.

The International Energy Agency published a roadmap for the industry to achieve net zero emissions by 2050. The projections will be difficult to achieve, but this sends a strong signal that energy companies should not be investing in new green-field projects.

Last week a small US hedge fund successfully gain institutional support to force three new directors onto the board of Exxon.

At this point there is no specific plan for change — the move stems from desire to drive a share price re-rating rather than ideological motivations.

But it relates to a view that Exxon has been dragging the chain when it comes to pivoting its portfolio towards renewable sources.

This highights a shift against new investment in oil and gas.

Elsewhere a Dutch court ruled that Shell’s plans to cut emissions were not stringent enough. The energy and petrochemical giant was told to cut emissions by 45% before the end of 2030. The ruling will be appealed — a process that could take several years. But it places more pressure on the company to act.

All of the above highlights the forces being applied to oil supply growth.

Meanwhile volume decline rates are rising, given the increased share of shale in total supply. Demand is likely to be maintained for much of the decade, leading to a potential future squeeze in oil prices.

Markets

We are seeing some rotation back to growth leaders in the global equity market, following underperformance for much of the past three months. This is broadly supportive of market breadth.

Merger and acquisition (M&A) activity is proving to be supportive in 2021 — driven by low funding costs, improving economic fundamentals and substantial fire power in private equity.

There have been US$1,266 bilion in M&A deals in the US so far this year. The previous record was US$861 billion at the same point in 2019.

Commodities generally bounced back last week. Brent crude rose 4.8% and copper gained 4.1%. Iron ore bucked the trend to end 4.3% lower.

Costa Group (CGC, -23.7%) fell last week as management downgraded EPS guidance by about 30% for the current year and by 10-20% for FY22. Several factors were at play — all in the domestic market — off-setting strength in the international segment. Pricing in avocados wass weaker than expected. A fruit fly issue in South Australia and higher labour costs in a mushroom facility have also dragged. These issues were previously flagged, but the impact was far greater than expected.

Fortescue Metals (FMG, -0.81%) was also among the laggards after confirming a cost uplift for its Ironbridge project. The increase from $2.6 billion to $3.3-3.5 billion is significant, but it’s in line with the market’s current expectation.

There was relief in the market as the potential investment from Domain Group (DHG, +14.8%) in PEXA looks set to be a lot less than many feared. Underlying trends in housing also remain supportive.

Testing company ALS (ALQ, +11.3%) delivered a strong result with margins higher in its commodity and life sciences divisions. Management delivered a positive outlook, helped by strong exploration activity from smaller miners. Earnings expectations were upgraded by 10-15% for out-years.

Carsales.com (CAR, +10.4%) bounced back from last week’s sell-off. Management made an effort to put the acquisition in the US — which has not been well received — into the context of an overall healthy business.

Tabcorp (TAH, +3.6%) received a bid for it wagering business from Betmakers Technology (BET). This is effectively a proposal for TAH to buy BET and the dynamics of the deal do not look particularly appealing. But it adds an extra layer of competitive tension into the battle for control of TAH’s wagering business.

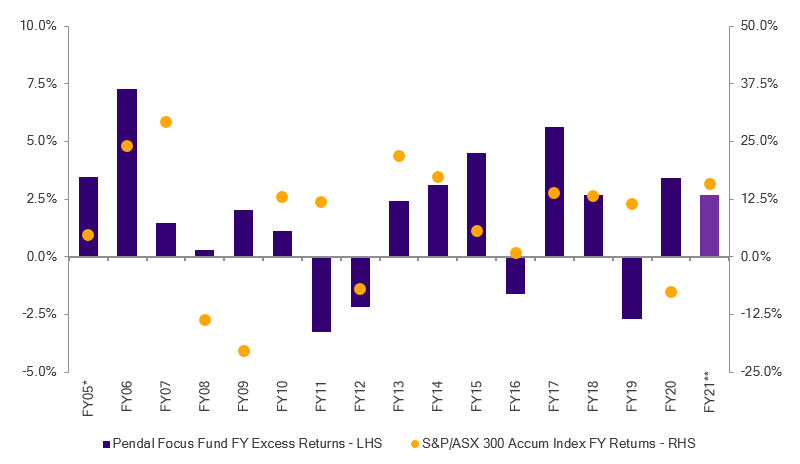

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

We heard a lot of t-words this week — particularly “transitory” and “tapering”. Pendal portfolio manager Tim Hext (pictured) explains what it all means in our weekly Bond, Income and Defensive Strategies wrap.

Find out more about Pendal’s fixed interest strategies

TWO THEMES dominated bond and equity markets this week.

The first was the Fed’s plan to label the latest inflation surge as “transitory”.

Although US Federal reserve speakers are allowed to speak their views, they generally follow the party line. Right now the party line is that the recent surge in inflation “largely reflects transitory forces”.

The implication is: all will soon be fine if the cycle plays out as usual.

Those Fed speakers were out in force this week — Evans, Barkin, Clarida, Quarles, Daly — and we may see similar sentiments from the RBA next week.

There is some truth to this.

Commodity prices always surge coming out of a recession. Firms generally cut back supply in a recession and are slow to react to stronger demand.

This causes shortages that last about two years before supply catches up with demand. Last week we included a graph that shows this.

However another story coming out of recession is that monetary and fiscal policy are tightening in line with stronger demand.

Equilibrium at lower prices is reached by both expanding supply and contracting demand. This time around governments and central banks globally are very happy to be way behind the curve.

Massive stimulus will stay in place and it is therefore likely commodity and goods prices will be higher for longer.

Transitory perhaps. But when measured in years — not quarters — the risk of embedding inflation in the system is much higher.

Tapering

The second theme for markets this week was tapering — in particular signs that the idea is slowly entering the minds of central bankers.

At many central banks tapering initially means reducing the size of Quantitative Easing (QE) programs.

US Fed minutes reveal that while there will be no change for now, they will soon be talking about reducing the size of purchases. It’s a similar story with the ECB.

And the Reserve Bank of New Zealand went a step further on tapering, reinstalling its OCR (cash rate) track. This shows potential for rate hikes beginning late next year and into 2023.

RBNZ governor Adrian Orr did provide some fresh honesty for a central banker by reminding everyone this was an educated guess and who really knew the future.

In Australia the RBA has signalled July as a crunch time for tapering, of sorts. They are unlikely to extend their yield curve control beyond the current April 2024 bond, if that can be called tapering.

They are also likely to announce whether QE will be extended beyond September. Here consensus is they will — but perhaps reduced from the $5 billion per week.

The Australian Office of Financial Management recently announced $130 billion of issuance for 2021-22.

The RBA is now buying $4 billion per week (plus $1 billion of state debt). At the current rate this means the RBA will finance the government in seven months.

Of course the RBA is keen to separate its QE (the purpose of which is driving down term rates) from government financing, but by buying the bonds they are financing the government.

We expect a halving of the QE program to $50 billion, reflecting reduced issuance and likely tapering offshore.

So the message from central bankers is clear: “Trust us. Relax on inflation. If it does get too high we’ve got this.”

The market reaction over the past two weeks indicates this is believed. We can see this in the chart below.

The market was gradually pricing in the rising inflation in a steady manner from around October last year.

It got a massive spike upwards in February but since then has consolidated and started trending down.

The question now is which direction will this head.

For now though some of the pain experienced in February is starting to be reversed for bond holders.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

This month’s Emerging Markets Spotlight demonstrates why we believe country-specific factors are critical when assessing EM investments. James Syme and Paul Wimborne (pictured), managers of Pendal’s Global Emerging Markets Opportunities Fund, explain:

FOLLOWERS of our views will be aware we’ve held a significantly positive tilt towards some Latin American equity markets since the third quarter of last year — including several new names and increased weightings in Mexico and Brazil.

Latin America has historically shown a strong relationship between GDP growth and commodity prices — and also between US dollar equity returns and commodity prices.

Commodity prices remain extremely strong by recent standards. After starting 2020 at about US$100/t, iron ore sits at around US$200/t. Copper has moved from US$2.80/lb to around US$4.50/lb; soybeans from US$9.40/bu to above US$15/bu.

These moves in export prices feed through to commodity-based economies in many ways. Trade balances and current account balances strengthen, tax revenue rises, corporate wages and investment can rise.

This upward pressure on currencies, corporate earnings and liquidity creates a potentially very attractive opportunity for equity investors like us.

Yet we remain zero weight Argentina, Chile, Colombia and Peru.

Why? In a word, politics.

Every unhappy country is unhappy in its own way. So what are the specifics in each of these cases?

Argentina

Argentina has the least functional politics of the four. The populist government of president Fernandez and vice-president Kirchner has struggled repeatedly with indebtedness (mostly to the IMF), inflation and a weak economy.

It has been illegal for companies to fire workers since last year, the private sector is subject to arbitrary price controls (which has caused output to slump), citizens have very limited access to foreign exchange, aggressive wealth taxes are being imposed (with the promise that they are one-offs) and almost every economic statistic is horrendous.

Consensus economic forecasts for 2021 are for CPI inflation at 45% and unemployment at 11.5%.

Until there is prospect for a change of political leadership, Argentina is effectively uninvestable in our eyes.

Chile

Chile has two major political problems.

Firstly, president Pinera is highly unpopular and the right-wing coalition he heads seems to be collapsing. This has allowed the Opposition to pass several populist bills largely seen as negative for the private sector and financial markets.

These include a new mining royalty Bill that will be a significant negative for the critically-important resources industry. The Bill has been approved by the energy and mining committee in the lower house of parliament and is likely to pass the Senate as early as this month.

The government is unlikely to be able to stop it. It similarly failed to stop three Bills allowing the public to draw down assets from their private pensions.

Unhappiness with the government and with the state of the economy and society has led to a second important development in Chile.

In October 2020, following mass protests against inequality, Chileans voted overwhelmingly to replace the constitution implemented during the military rule of General Pinochet.

The new constitution will almost certainly create expanded rights to healthcare, education, housing and welfare — and consequently will require significantly higher taxation.

It may also constrain the private sector in other ways, and may restructure the relationship between commodity producers and the state. These are not automatically negative outcomes, but the uncertainty clearly creates significant risk for investors.

Colombia

Unlike Argentina and Chile, the problems in Colombia stem from an attempt by the government to maintain orthodox fiscal policy.

Colombia has had an investment grade credit rating since 2011, but the fiscal deficit has expanded from 1.9% of GDP in 2019 to 8.9% last year and an estimated 8.2% this year.

Tax revenues have to be increased. Analysts estimate 1% of GDP in additional revenue is the minimum required to maintain the credit rating. The proposed budget would increase taxes on middle-class Colombians, and has proved wildly unpopular.

Previous finance minister Alberto Carrasquilla first withdrew the budget — and then resigned — when violent demonstrations broke out across the country. Protesters blocked roads and fought with the police.

New finance minister Jose Manuel Restrepo has instead sought a national consensus around a budget based on alternate taxes and spending cuts — but protests have continued.

This is not the first violent demonstrations that the Duque government has faced. A collision between bond markets and the Colombian people makes for a difficult environment for equity investors.

Peru

Peru is in the middle of its presidential election. The first round took place in April and the second round is expected on June 6.

Hard-left populist Pedro Castillo of the Free Peru Party won the most votes in the first round and is leading in polls ahead of the election run-off.

His opponent, conservative candidate Keiko Fujimori of the Popular Force Party, is enjoying a lot of political support from other right-wing parties. But allegations of corruption, money-laundering and obstruction of justice are weighing heavily on her campaign.

Castillo is a radical, anti-establishment candidate who has said he does not plan to nationalise private companies in Peru. But he plans an increase in government spending of 10 percentage points of GDP and has hinted at extremely high corporate taxes to help fund this.

Polling suggests a landslide win for Castillo. The prospect of this is placing significant stress on financial markets.

Conclusion

The pick-up in capital flows to emerging markets, a global recovery, higher commodity prices and the steady roll-out of vaccination are all powerful positive drivers for higher-risk, commodity-exporting EM countries.

We are overweight Mexico, Brazil and South Africa in the portfolio.

But we have avoided the smaller Latin American markets for these generally political, but country-specific, reasons.

Download this article as a PDF.

About Pendal Global Emerging Markets Opportunities Fund

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities Fund.

The fund aims to add value through a combination of country allocation and individual stock selection.

The country allocation process is based on analysis of a country’s economic growth, monetary policy, market liquidity, currency, governance/politics and equity market valuation.

The stock selection process focuses on buying quality growth stocks at attractive valuations.

Find out more about Pendal Global Emerging Markets Opportunities Fund here.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS were broadly flat last week — the S&P/ASX 300 returned 0.35% and the S&P 500 fell 0.39%.

However we did see material rotation: tech rallied and the high-momentum areas of commodities and crypto fell — in some cases sharply.

A combination of factors were behind this:

-

- A sense that concerns over inflation were at a crescendo, which was not translating into a significant bond yield spike. This suggests the market is very long on the inflation trade.

- Early signals that the Fed may kick off the debate over tapering a couple of months earlier than expected.

- Comments from Beijing on an excessively rapid rise in commodity prices raised concerns they may act to curb prices. There was also a warning on the surge in Chinese interest in cryptocurrencies. This is a reminder of Beijing’s desire to retain control of its financial system and launch its own digital currency.

So far equities have held up well, consolidating in a range rather than correcting like other risk assets. In our view equities remain well supported by corporate earnings, driven in turn by the strong economic recovery.

Macro and policy outlook

The market latched onto a number of potential signals out of the Fed last week:

- Minutes from the Fed’s recent meeting noted that if the economy continued to make rapid progress towards its goals, it may be appropriate at some point to begin discussing a plan for adjusting the pace of asset purchases.

- Other comments such as a need to be “nimble on policy” reinforced this change in tone regarding tapering.

- Federal Open Market Committee member Richard Clarida maintained a line of current inflation as transitory. But he went on to say the Fed was “attuned and attentive to incoming data” and “monetary policy is as much about risk management as it is about the baseline”.

All this was accompanied by dovish comments regarding timelines. But it may represent an adjustment in the Fed’s tone, signalling a focus on ensuring that inflation expectations remain under control.

So the tapering debate has potentially begun. The real question is ‘will this end the equity rally?’ We remain of the view that it will not.

The reasons for inflation concerns are clear: strong demand, supply-chain bottlenecks and surveys showing companies feel they have cost pressures coming through.

We agree the risk of inflation is higher than it has have been for some time. But it is not a forgone conclusion.

There is an alternative perspective which may yet come to pass. There are a number of arguments supporting the case against widespread inflation, including:

-

- Supply bottlenecks may quickly be unwound. We are seeing a demand spike with supply still lagging. But there is evidence the supply response is coming, for example in export data from Taiwan and Korea.

- Commodity prices have not been a good lead indicator for broader inflation for the last 25 years.

- Productivity: Wages can go up without a big shift in core inflation if productivity is also rising. We have just seen the US GDP recover to pre-Covid levels with 8 million fewer jobs — an indication that productivity has surged.

- Supply of labour: This is likely to rise, particularly in the US after September as benefits return to pre-Covid levels, alleviating wage pressure.

- Plateauing demand: We may have reached peak levels of demand in a number of key segments. Durable goods, housing and auto sales are at levels that are likely to plateau. This would lead to inflationary pressures easing.

- Debt levels: The US has record debt just shy of 380% of GDP, although it has shifted from households to the government. History suggests high debt levels lead to declining velocity of money. M2 money velocity ratio in the US is sitting at just over 1.1 compared to 1.4 pre-pandemic. US bank results suggest they are still not extending credit — a necessary pre-requisite to see some inflation.

- Household spending: A third of US stimulus payments are paying down debt rather than increasing spending. This is a sign that people are wary of overall debt levels, which may subdue spending.

- Tax: The prospect of tax increases may reinforce caution among consumers.

- Demographics: Populations are aging and older people tend to spend less — so ageing can be deflationary.

- Technology continues to provide opportunities to deliver services and products more efficiently.

There is anecdotal evidence of wage pressures, but so far nothing is showing up in the data.

A lot is made of the rise in the breakeven inflation rates. But the inflation sceptics point out that this is highly correlated to commodity prices. They cite the Cleveland Fed’s long-term expected inflation measure as a better historical indicator of wage pressure and inflation. This has barely risen, suggesting no sign of wage-push inflation.

In conclusion there are many reasons to be wary about building inflation and rising bond yields. This seems to be the consensus view and reflects broad market positioning.

But it is not certain that we are seeing a secular shift in inflation. There are good reasons to argue against betting the farm on an inflationary outcome.

This goes to the issue of managing for different scenarios in our portfolios.

We have exposure to stocks that will benefit from higher inflation. But we also see the need to maintain some hedges on low inflation — notably quality growth names such as Xero.

COVID and vaccine outlook

Here there are two areas of notable risk:

-

- A continued spread of Covid in emerging markets and countries without access to vaccines

- Effectiveness of vaccines against new variants.

On the first issue we are seeing more positive trends in India as new cases and positivity rates continue to fall. (Although there are still questions about the accuracy of data.)

Overall new case numbers are dropping globally.

One key concern for Australia is that countries with strong track records such as Taiwan and Vietnam are seeing new waves of cases higher than any before. This is leading to lock-downs and dramatic reductions in mobility.

This brings the focus onto vaccine provision.

Global doses are approaching 30 million per day but only about 8% of the global population has been vaccinated.

The US is making more vaccines available (20 million doses by the end of June). The WHO approved the Sinopharm vaccine, allowing it to be exported.

On the issue of efficacy we had positive news this week from the UK. Due to detailed genomic analysis British scientists are now able to assess effectiveness of vaccines against the more infectious Indian B.1.617.2 strain.

In the UK those with two doses of vaccine are showing a high degree of protection against the Indian strain. Those who catch it are not getting as sick.

Health trends in the US remain positive, supporting the re-opening trade. As consumer confidence begins to rise significantly we are seeing clear signs that the next leg of recovery is kicking in.

Travel interest has returned to pre-Covid levels, according to data from travel-related apps. We are yet to see this translate materially in improved airline demand, but we suspect this could shift quickly.

Markets

Equity markets held up well last week despite a sell-off in commodities and the cratering of crypto.

Gold continued to rebound, resuming its status as a defensive asset class. Brent crude was off 3.3% on rising expectations of an Iranian deal which would allow more supply into the market.

The Bitcoin sell-off looks like the last domino to fall among the proxies we have been tracking for excess liquidity. Other indicators such as renewable energy ETFs, IPO ETFs and speculative technology stocks have also had significant corrections. This is a healthy sign for markets, suggesting speculative froth has receded.

The Australian market has held up well in face of a sell-off in cyclicals. It has consolidated over the last month, following a 15% move from early November.

The liquidity supporting the market is evident as banks continue to grind higher. We note that Commonwealth Bank is now about 21x next-12-month price/earnings, suggesting people are looking to park cash in safe-haven equities due to low rates.

Stock news

Carsales.com (CAR, -8.2%) was the worst performer in the ASX100 after announcing a deal to buy 49% of a US online caravan site in the US. There was a degree of market scepticism over this strategy.

Concerns over tapering dragged on cyclicals. BlueScope Steel (BSL, -6.6%), Santos (STO, -5.7%) and Alumina (AWC, -5.3%) were hardest hit.

James Hardie’s (JHX, -2.6%) result was complicated. North American volumes disappointed, although this was offset by better pricing and demand in Europe.

Technology stocks benefited from the rotation.

Appen (APX, +19.4%) was the strongest performer in the ASX100. Management announced an organisational restructure and confirmed its recently downgraded guidance which helped the bounce. It is still down about 70% from its August 2020 peak.

Xero (XRO, +13.1%) bounced back strongly after last week’s reaction to its result. It seems the focus has shifted to potential growth in FY22 and FY23 as the UK pushes more small businesses onto cloud accounting through the “making tax digital” program.

Ampol (ALD, +9.2%) and Viva (VEA, +2.5%) benefited from a long-awaited government fuel security package. This provides scaled support for sector-based refiner margins for six years (and potential for nine years). The government will pay for 50% of capex needed for upgrades to improve fuel standards. This is supportive for the long-term rating of both companies.

Aristocrat (ALL, +8.9%) upgraded earnings ahead of today’s result. Its gaming and digital businesses are going well. The former reflects the US re-opening.

Qantas’s (QAN, +6.5%) quarterly update indicated that cash flow is now positive.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 30 Apr 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s our weekly Bond, Income and Defensive Strategies wrap from Pendal portfolio manager Tim Hext (pictured).

Find out more about Pendal’s fixed interest strategies

THERE were plenty of positive signs this week.

Despite a slight pull-back in the latest job numbers and consumer confidence, we’re seeing wage inflation recover from a down-trend that was underway before the pandemic shock.

April was expected to be more subdued than earlier months because the data now reflects the full impact of JobKeeper ending.

There were plenty of worries that hard won post-Covid gains would be lost as talks of tapering accelerate overseas.

But now there is a difference.

Before the pandemic the RBA acted as a lone wolf, tackling unemployment with monetary expansion, while the federal government kept a lid on spending due to its budget surplus obsession.

Now the RBA and federal government are in lock step as Team Australia.

Fiscal policy is the main game

The pandemic crisis finally freed the Liberal government from the shackles of dogma — Budget surplus at all costs.

The transformation is now complete with the release of the federal Budget.

Employment is now above its pre-COVID level and GDP is expected to soar this year. But the government continues to plough more into the economy, presumably to secure a full employment victory this time.

New stimulus initiatives are worth 4.1% GDP over four years. This compares to the paltry 2019 budget spend worth 0.5% of GDP when unemployment was drifting north of 5%.

These are good signs indeed — not just for the Australian economy but also for the Liberal government.

As the saying goes, fortune favours the brave.

They may learn that not all spending is bad. The good news this time is that the strategy is affordable.

A continued surge in commodity prices — as well as tax receipts from growth instead of higher taxes — will make this a “self-funded” expenditure.

Monetary policy

We anticipate the RBA’s monetary response will remain expansionary to support the federal government’s fiscal response.

That will involve keeping the cash rate target and the interest rate of RBA Exchange Settlement account balances low. It’s also highly likely there will an extension of the Quantitative Easing (QE) program as part of the toolkit.

The incredible rebound in the Australian economy has given the RBA a shot in the arm.

These complementary actions between the monetary and fiscal policies make full employment a goal rather than a dream.

The implications

Despite the stimulatory Budget surplus, a massive increase in supply of Australian government bonds (CGLs) is not anticipated, because the spend can be largely funded through economic growth.

An extension of the RBA’s QE program will continue to provide support.

We therefore continue to favour CGLs versus semi-government bonds as the economy recovers.

We’re also keeping a watchful eye on inflation to see if it will turn structural this time or remain transitory — as was the case in historical post-crisis periods.

As highly expansionary fiscal and monetary policies remain in place after the economy hits full capacity next year, we suspect inflation will stick above target for another few years at least.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here

Many US and European stocks are reporting strong earnings. Pendal’s Head of Global Equities Ashley Pittard (pictured) explains what this means for global equities portfolios.

- US and European companies post better-than-expected earnings

- Stronger macro environment to drive growth

- Ashley Pittard: How to position a global shares portfolio for the recovery

- Find out more about Pendal Concentrated Global Share Fund

STOCK SELECTION is the key to successful portfolio management in 2021 as a booming earnings season in the US and Europe indicates the broader global economy is roaring out of its COVID-induced coma.

In the US, S&P 500 stocks grew earnings by 47 per cent in aggregate year-on-year in the first quarter, on the back of sales rising more than 10 per cent.

European companies did even better with a 153 per cent lift in earnings and a 3.2 per cent rise in sales.

Pendal’s head of global equities, Ashley Pittard, says the strong performance is a result of pent-up consumer demand, the rebuilding of corporate supply chains and immense government stimulus.

But he says investors should be cautious about the index dominance of America’s big tech stocks — the so-called FAANGs of Facebook, Amazon, Apple Netflix and Google-owner Alphabet — which can give a misleading impression of the market’s overall prospects.

“How you wanted to be positioned the last few years, it was all in the FAANG stocks,” he says. “The market was very narrow because the US tech sector were the only companies that could grow their earnings.

“Now, it’s not going to be as narrow because earnings growth is going to be broader.

“The earnings today due to a stronger macro environment means that the market will be more broad, which therefore should mean that we will get higher equity markets.”

Portfolio construction perspective

From a portfolio construction perspective, Pittard says investors should move to a concentrated stock-selection stance and avoid shadowing the tech-dominated indexes.

“The S&P is near an all-time high valuation at 24 times earnings, but if you strip out the top ten stocks, the market is still very compelling. That’s why I believe that over the next three years, as long as you’re a stock picker or you’re very selective or very concentrated you will do very, very well.

“But if you shadow the index — you just mirror the market — and you’re going to do poorly.”

One reason the big tech companies did so well in the Covid recession was they brought forward demand — they were able to service households in lockdown that were unable to travel, visit the shops and eat out, Pittard says.

Now, as the pandemic lifts, household spending will resume normal patterns.

“It’s like coming out of prohibition. People are going to go nuts. You can already see it and we don’t even have full vaccinations.”

Businesses are also lifting spending. In past recessions, inventories build up as demand reduces, leaving businesses with surplus stock to run through as the economy recovers. This time, inventories were run down as global supply chains reeled.

“So, what has to happen? They get everybody in, everybody’s doing overtime, everybody’s getting paid more and they’re rebuilding inventories,” says Pittard.

Underpinned by government spending

Government spending is underpinning the boom.

“It’s more than double what they did in the global financial crisis,” says Pittard.

In terms of regional allocation, Pittard advises being underweight US stocks and investing instead in Europe and the UK.

“You’re getting broader earnings growth, and you don’t need to be in those top 10 stocks that have had their day because they brought forward demand.”

Pittard says the main risk to portfolios is inflation resulting from central banks keeping interest rates artificially low as they seek to drive the economic recovery.

“Over time, every government that has tried to control prices has failed,” he says. “What governments are doing now are controlling the bond rate… in a normally functioning market the bond rate is at or higher than the inflation rate.”

The best asset allocation to deal with that risk?

“You want to be more concentrated, you want to be more stock specific, you want to have a higher active share, you want to have a long-term view and you want to have quality stocks.”

About Ashley Pittard and Pendal Concentrated Global Share Fund

Ashley Pittard leads Pendal’s Global Equities investment boutique. He is responsible for setting the strategy, processes and risk management for the boutique and its funds including Pendal Concentrated Global Share (COGS) Fund.

Ashley has more than 24 years of finance experience, including roles in petroleum economics, global energy investment analysis and 20 years as a global equities fund manager.

Pendal COGS Fund is an actively managed, concentrated portfolio of global shares diversified across a broad range of global sharemarkets.

Find out more about Pendal Concentrated Global Share Fund

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

LIKE A horror movie where you get a fright — even though you already know something bad’s about to happen — the markets last week experienced a mini-panic after the first signs of inflation.

We won’t know for a year or so if this inflationary pulse is transitory or more structural. In the interim, debate is likely to ebb and flow between fear and ambivalence.

The key question is: what does it mean for markets and portfolio positioning?

We are still in the camp that markets can rise.

But we think this will be driven by earnings growth rather than valuation expansion — a reversal of the past decade’s trend.

Governments and central banks are focused on generating growth to address social issues such as inequality and to underwrite investment in resilient supply chains and infrastructure for energy transition.

This should support earnings, which can in turn support markets — as long as there is no significant policy tightening.

Without the broad tailwind of valuation re-rating, earnings become a key differentiator of stocks in the market. Picking cyclical winners or improving structural growth stories will be key.

Last week saw the S&P 500 sell off 1.35% and the S&P/ASX 300 lose 0.71%. But there was significant underlying volatility in a knee-jerk reaction to inflation data.

Most sectors sold off. Growth sectors such as Technology (-6.46%) sold off the most, but traditional inflation hedges such as Resources (-1.72%) were also down. This is creating opportunities.

Economics and policy

US inflation data came through much stronger than expected. The consumer price index (CPI) was up 3% year-on-year in April and 0.92% ahead of March. A surge in prices is evident in areas related to re-opening such as airline tickets, travel lodging and used cars and trucks.

The CPI is expected to peak next month at +3.6% year-on-year before the base effect starts to moderate.

The market’s reaction was exacerbated by the Fed’s response. A number of Board members quickly characterised the data as transitory and emphasised that policy will remain loose.

The market is adjusting to the risk of inflation after decades without it. Its key question is the credibility of a commitment to keeping rates steady as inflation rises. This will continue to impact the US dollar and bond yields.

We wouldn’t be shocked to see inflation surprising on the upside over the year. It would be a natural outcome from an economy doing better and the increasingly co-ordinated nature of the global recovery as vaccines roll-outs progress.

But we emphasise that this does not have to be negative for equities overall because it’s likely to coincide with better earnings.

Over the medium term wage growth will be the key factor. There is already evidence in the US that tighter labour markets in certain sectors along with the effect of higher unemployment benefits, is leading to wage growth. Amazon and McDonalds have both announced 10% wage increases covering some 600,000 workers.

We do not expect a wage-price spiral to form. There is still a lot of capacity in the economy and structurally deflating factors. But given that governments are looking for higher wages to help address social issues (particularly in lower-income work) this will remain a key macro factor to monitor.

In the US the odds are growing of a bipartisan “traditional” infrastructure bill of $800-900 billion — funded by tax enforcement rather than tax increases to get Republicans over the line.

A bi-partisan bill could be ready by mid-August. This emphasises that there is more stimulus to come, albeit spread over a number of years.

There is some risk to this. Democrats are concerned it may make subsequent, more progressive policy bills harder to pass.

In Australia the federal budget sent an important signal that growth is the goal. For now traditional Liberal policies such as fiscal conservatism are in hibernation. Increased spending on areas such as infrastructure helps the underlying economy and corporate earnings.

COVID and vaccines

There is incremental improvement in global case numbers. The Indian data is difficult to interpret due to measurement challenges. But the rolling over of the daily new positive test rate is a small sign of hope.

Europe continues to progress. There is increasing focus on European re-opening and economic recovery, which is supportive for global cyclicals.

The US is approaching the point where Israel experienced a substantial shift down in new Covid cases.

This is leading to a real shift in re-opening momentum. Surveys suggest a dramatic change in sentiment towards participation in public activities such as movie-going, eating out and air travel. This is a pre-cursor of the release of pent-up demand.

There are some concerning developments we need to keep an eye on.

The UK is beginning to see the spread of the Indian variant despite a high level of vaccinations (55% vaccinated and 30% with two doses).

There are concerns around the variant’s transmissibility. Modelling suggests a 10-20% transmissibility rate is manageable but more than 30% is a problem. No one knows the transmissibility of the Indian variant, but experts suggest there is a 35-50% chance it is more than 30%. This could delay a roll-back of restrictions.

The other issue is the effectiveness of vaccines on this variant.

Early signs are positive. In areas of the UK hit by the Indian variant there are fewer cases among over-60s (where the vaccination rate is higher).

This ties into a second area of concern related to the Seychelles. Despite vaccination rates above 70%, cases have surged in this island nation off the African east coast. A third of new cases are among people who have already been vaccinated (using the Sinopharm and Astra Zeneca vaccines).

It is too early to make a call, but this highlights potential issues around the effectiveness of certain vaccines to Covid variants.

This highlights the importance of booster shots and complicates the re-opening of borders.

Markets

The inflation data prompted a risk-off move in markets. Equities and commodities fell, while the US dollar held firm.

We have been discussing the notion of market consolidation for a few weeks now. It feels like this is playing out with the crescendo of the inflation print. But the market is proving broadly resilient.

The VIX Volatility Index spiked last week. Though over the past year spikes have come at progressively lower levels with quicker reversions — a positive sign.

The US earnings season has been very strong. Earnings for Q1 were revised up 29% (and FY22 up 8%). This has alleviated pressure on P/E ratios and brought the S&P 500 back towards 20x earnings.

This valuation rating is very much in line with the laxity of monetary conditions.

A key risk to rating is any sign of tighter policy. At this point the Fed’s guidance is for a gradual tightening. But higher market rates, credit or bonds may challenge this. The key point is that a re-rating is unlikely, leaving earnings as the key factor for stocks.

The ASX’s sell-off last week was broad-based. Staples (+0.98%), Health Care (+0.73%) and Financials (+0.63%) eked out gains, but all other sectors lost ground.

A2 Milk (A2M, -21.2%) was the worst performer in the ASX 100 after management issued yet another earnings downgrade. It feels like the company is getting close to new base in terms of margins and market expectations. We think there need to be signs of material operational improvement to see opportunity emerging.

Xero (XRO, -15.9%) sold off along with other tech names, but the market was also disappointed with its earnings result. EBITDA came in below market expectations as the company invested more in R&D and customer acquisition. Previously, the market has welcomed further investment by tech growth companies, but the mindset has shifted in the current environment. The market no longer assumes incremental benefit to revenue growth.

XRO remains our pick in the sector. Its rating is in line with comparable, cloud-based companies. Our positive thesis is built on a growing appetite among governments and companies for digitally-enabled businesses. Xero continues to grow its subscriber base. We expect average revenue per user to benefit from product development and bolt-on deals enabling provision of new services.

Most other tech names fell on back of the inflation data last week. Afterpay (APT) was down 10.5% and Wisetech (WTC) fell 7.9%.

Chemical company Incitec Pivot (IPL, -10.41%) was among the weakest. It revealed more operating issues at its US ammonia plant, which led to another downgrade. Commodity price increases are ameliorating a lot of the earnings pain.

Crown (CWN, +7.59%) was the best performer as Star (SGP, +3.84%) tabled a bid to rival Blackstone’s, raising some competitive tension in the takeover process.

Treasury Wine Estate (TWE, +6.69%) delivered a well-received strategy update. The key factor was a continued turnaround in the US business as the economy recovers and some oversupply issues start to recede. This is helping offset a hit to its Chinese business from tariffs on Australian wine.

Boral (BLD, +5.12%) received a no-premium takeover bid from Seven Group (SVW,-5.16%), creating uncertainty over the latter’s intentions.

Finally Commonwealth Bank (CBA, -2.83%) rounded out the bank updates. It was a positive quarter, reflecting broad trends seen at the other banks.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

The next five years will see inflation significantly higher than the past decade. We should be alert to this but not alarmed says Pendal portfolio manager Tim Hext in our weekly Bond, Income and Defensive Strategies note.

Find out more about Pendal’s fixed interest strategies

THE two big highlights of the week were the federal budget and US inflation numbers — and they are more closely linked than it might seem.

Federal Budget

The RBA and Treasury now forecast GDP and employment at full capacity for next year.

That means no slack left in the economy. Normally this would signal a tightening of monetary and fiscal policy. But times have changed.

Invoking the continuing transition from the crisis, the RBA and government are both firmly foot-to-the-floor.

For the government a looming federal election translates to “why not keep handing money out?” After all no one seems too troubled.

Even the usual crowd of economists who warn of impending doom from too much debt have gone quiet. The only ones who can hold their heads high are proponents of Modern Monetary Theory. They understand better just how government debt works.

The RBA seems to have gotten itself in a corner. Like the rest of us they expected the health crisis to be far worse. Unlike us they made commitments (or guidance in some cases) out to 2024 based on that expectation.

The RBA is more oil tanker than speedboat when it comes to turning around. For now they remain committed to Quantitative Easing, Yield Curve Control and no rate hikes.

This is now based solely on benign inflation and wage forecasts — not growth and employment, which are strong.

Future RBA statements will be watched closely for watering down of rhetoric.

US inflation

That leads us to this week’s US CPI numbers. CPI was 0.8% for April and 4.2% year-on-year.

Extraordinary numbers.

Economists and no doubt the Federal Reserve will be quick to reassure us this is transitory.

Supply bottlenecks in the auto industry have prompted a spike in used car and rental car prices. Hotel rooms, airfares, sporting events — most things have spiked as the economy reopens.

These spikes won’t repeat but other spikes are coming. Rents are creeping up and wages are already rising. Commodity prices are taking off.

If there is excess capacity in labour markets perhaps the Fed can get away with the idea of ignoring these transitory factors and we can return to business-as-usual low inflation.

I suspect though with ongoing massive fiscal and monetary stimulus the inflation genie is out of the bottle.

Low inflation expectations may become, if not unhinged, at least challenged in the years ahead. Wages could well follow. Inflation in Australia will also follow.

Eventually technology and demographics will keep a lid on inflation becoming a massive problem.

But the next five years will see inflation significantly higher than the last 10 — something we should all be alert but not alarmed at.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies (BIDS) team.

Led by Vimal Gor, Pendal’s BIDS boutique is one of the most experienced and well-regarded fixed income teams in Australia. In 2020 the team won the Australian Fixed Interest category in the Zenith awards.

The team oversees $22 billion invested across income, composite, pure alpha, global and Australian government strategies with the goal of building Australia’s most defensive line of funds.

Find out more about Pendal’s fixed interest strategies here