Robust succession plan … Mr Nicholas Good (left) will succeed Mr Emilio Gonzalez (right) as Pendal Group CEO

Pendal Group (ASX: PDL) today announced that Group CEO Mr Emilio Gonzalez will step down after 11 years in the role, and Mr Nicholas Good, currently CEO of the J O Hambro Capital Management (JOHCM) operations in the USA, will be Mr Gonzalez’s successor.

The Chairman of Pendal Group, Mr James Evans, said: “The Board sincerely thanks Emilio for his contribution, constancy, and commitment for over a decade and recognises his significant achievements, particularly the successful acquisition of JOHCM in 2011 that transformed the company into a global funds management business.

“Our robust succession plan has enabled the Board to appoint Nick as the new Group Chief Executive Officer of Pendal Group.

“Nick is a global leader in the funds management industry with a strong track record of building and growing businesses. He is an impressive strategist and has an inspiring leadership style.

“Importantly, the biggest future potential for the Group is in the USA. With Nick on the ground there, and with the support of the talented Global Executive Team, including the regional CEOs, Pendal Group will be well-positioned and equipped as it transforms its business to take advantage of future growth opportunities.”

Mr Gonzalez has a six-month notice period and is committed to ensuring a smooth transition.

Mr Evans said: “Under Emilio’s leadership the business underwent a step-change in funds under management, scale, distribution, product offerings to clients, and importantly, shareholder returns.

“Since Emilio’s appointment in January 2010, Total Shareholder Return (TSR) has been 322.9 per cent, compared to the 130.1 per cent return of the Standard and Poor’s ASX200 Accumulation Index over the same period.

“Emilio truly diversified the business across geographies, asset classes, and channels. He successfully oversaw the gradual sell-down of Westpac’s ownership and a broadening of the share register, a change in brand to Pendal that represents our heritage and navigated the business through the global credit crisis and the current global COVID-19 pandemic.

“Emilio will leave Pendal with acknowledgement and thanks for a job very well done and our best wishes for the future.”

Mr Gonzalez said, “With the multi-year investment program announced in November 2020, it is timely and important that my successor has a clean run to drive this program. It will require a long-term commitment, and after 11 years as CEO, it is the right time for a new Group CEO to step in.

“It has been a privilege to lead the company and transform it from a domestic equity fund manager, with $41.9 billion under management, to a diversified global fund manager with $97.4 billion in FUM.

“I would like to thank all of my colleagues at Pendal Group who I have worked with over the years. It has been a team effort and I leave knowing the business is in a strong financial position and well placed for the future.”

Mr Good commented: “I would like to acknowledge the outstanding contribution of Emilio to the Pendal Group. It has been a privilege and pleasure to work with him, and I am honoured and excited to have the opportunity to lead this great company.

“Pendal is recognised for its talent, diversified business model and strategic global footprint. It has long-tenured, highly regarded fund managers and has consistently delivered long-term outperformance.

“I am confident that there is a very bright future ahead as we position to take advantage of the fast-paced changes, and inherent opportunities, in global funds management.”

Mr Good will remain based in Boston, USA.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Contact a Pendal key account manager here.

Pendal has today launched our first Responsible Investment and Stewardship Annual Report for Australia. Here Pendal Australia’s chief executive Richard Brandweiner (pictured) explains what it means

I AM pleased to introduce our inaugural Responsible Investment and Stewardship Annual Report for 2020.

This is a new initiative to summarise the responsible investment practices — including environmental, social and governance (ESG) integration and stewardship activities — we undertake on behalf of our clients.

As an active investment manager, we are truly stewards of our clients’ capital. We believe we have a role and responsibility to deliver sustainable returns for them, as well as influence sustainability practices more broadly.

We do this as part of our fiduciary duty to clients, but also in recognition of our position as one of the largest allocators of capital in the Australian ecosystem.

This means we need to influence positive change by taking a constructive and forward-looking approach to supporting companies improve their ESG credentials.

Long-term value creation

As society evolves and consumers and regulators increasingly look towards organisations to be mindful of their social licence to operate, we believe attention to ESG factors leads to better informed investment decisions and can improve the quality and consistency of long-term value creation.

We are proud to work with many clients who have additional ethical and sustainability-related objectives, in addition to generating returns. For these reasons, we integrate financially material ESG factors across all Pendal funds, as well as offer dedicated investment solutions to meet our clients’ additional priorities.

At Pendal we have a multi-boutique structure, with four distinct investment teams: Australian Equities, Global Equities, Multi-Asset Strategies and Bond, Income & Defensive Strategies.

Each boutique integrates ESG and undertakes stewardship in a way that makes sense for their respective strategies and asset classes.

In other words, we don’t have a single way of investing responsibly at Pendal, although our dedicated Responsible Investments team does bring a common thread across the firm by supporting all boutiques and helping to define quality.

Regnan: Sustainable and impact investing

As many of you will be aware, in early 2019 we assumed full ownership of Regnan, bringing the team in-house to be Pendal Group’s specialist sustainable and impact investing business unit.

Regnan’s experienced team of experts have been a great addition, supporting our engagement and research activities and the continued development of our investment products.

Excitingly, 2020 saw Regnan’s capabilities expand to investment management.

Pendal Group secured a specialist global impact investment team to join the Regnan ecosystem and we launched two products under the Regnan brand.

We look forward to the expansion of the Regnan business, further enabling the purposeful allocation of capital.

Learning and growth

While 2020 in many ways went down as a year most would rather forget, for Pendal it was also a year of learning and growth.

It was a year of paradoxes: a reminder that not every situation is an “either/or”, and not every decision can be bound by the immediate environment or issues at hand.

The year saw, for example, corporate management held to account for more than just the maximisation of short-term shareholder profit in ways we have not seen before.

As we turn our attention to the future and “building back better”, we expect the topics of climate change and inequality will gain importance in the year ahead — and beyond.

The COVID-19 pandemic laid bare many underlying inequalities in societies around the world. Women, elderly and vulnerable communities were disproportionately represented in the hardest hit sectors of the economy.

Encouragingly we are seeing investor action already and we share in this report some of the ways we are working with our clients and investee companies to address this rising inequality.

Tranformation through collective action

The pandemic has also shown us that collective action can drive transformative policies and deliver break-through technologies that seemed unthinkable before the crisis.

Through our engagements and advocacy efforts we will seek to ensure the advances witnessed in 2020 continue.

How else can we ensure that our health, political and economic systems can be resilient in the face of a pandemic, or other form of crisis in the future?

We are thrilled with some of the things we achieved in responsible investment and stewardship in 2020.

These efforts are detailed in this report which I hope you enjoy reading.

We look forward to reporting annually on the ways in which we continue to enhance our approach, responding not only to the ever-changing investment environment but to the evolving needs of our clients.

— Richard Brandweiner

Pendal Chief Executive Officer, Australia

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Download Pendal’s Responsible Investment and Stewardship Annual Report 2020 (PDF)

Contact a Pendal key account manager here.

As part of its approach, Pendal Horizon Fund invests in companies that enable and lead in the transition to a more sustainable and future-ready Australian economy, while avoiding those that cause significant harm.

An example is business software innovator Xero, a leader in the trend to digitalisation which is changing the way we work.

Pendal equities analyst Elise McKay explains in a short video above.

ASX-listed technology stocks — particularly so the so-called WAAAX stocks Wisetech (WTC), Afterpay (APT), Altium (ALU), Appen (APX) and Xero (XRO) — have been favourites among many investors in recent years.

A key part of this has been the benefit of low-bond yields, which have lifted valuations for growth companies — including many tech names — worldwide.

This tailwind has receded in recent months as yields have begun to rise. Meanwhile vaccines have provided a pathway to re-opening, boosting sentiment around more cyclical stocks. As a result market leadership has shifted from growth stocks to cyclical and value.

In our view this does not mean a shift to a stance of “sell growth, buy value”.

There are plenty of value stocks that are structurally impaired. At the same time, we think there are compelling opportunities in tech stocks. Stock selection is as critical as ever.

In the tech sector we think the market will start to discern between companies with less tangible prospects that are not delivering cashflow — and those that are profitable with good earnings visibility.

We see accounting software provider Xero as one of the latter. It is our top pick in the ASX tech sector.

In this video above Pendal Research Analyst Elise McKay shares insights into XERO, the ASX tech sector and the five-factor framework by which we assess companies.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

“We use this framework to find those companies like Xero that are generating strong, sustainable returns on the capital that they’re investing today in unlocking a large global addressable market and creating significant value in the future,” says McKay.

In Xero’s case:

- The industry structure and competitive landscape is favourable and there is a large global addressable market

- Xero is well placed in the cycle as secular trends drive the adoption of cloud accounting products

- It’s investing heavily in innovating the next generation of products.

- The culture of the company is strong, and it’s able to internally create the products it needs.

- And finally, the capital return and unit economics of the business are attractive.

“One of the great things about Xero is that it has accelerated digitalisation of the economy, particularly for small businesses.”

Digitalisation refers to the use of digital technologies “to change a business model and provide new revenue and value-producing opportunities” according to research house Garnter. (It’s distinct from digitisation, which simply means converting things such as bank accounts or books from analog to digital.)

“This platform opportunity allows Xero to be the plumbing into so many more solutions being offered to this community.”

Digital tools are rapidly becoming essential for small business in Australia, according to McKay, who says businesses adopting digital are on average able to save 10 hours a week and generate 27 per cent more revenue.

She believes the fast-growing cloud accounting provider is at the start of a multi-year journey to unlock an enormous global market and become a platform for transforming small business.

XERO is included in Pendal Horizon Fund (formerly Pendal Ethical Share Fund) and Pendal Focus Fund.

About Elise McKay

Elise is an investment analyst with Pendal’s Australian equities team. Elise previously worked as an investment analyst for US fund manager Cartica where she covered a variety of emerging market companies. She has also worked in investment banking and corporate finance at JP Morgan and Ernst & Young.

About Pendal Horizon Fund and Pendal Focus Australian Share Fund

Pendal Horizon Fund (formerly Pendal Ethical Share Fund) is a concentrated, high-conviction portfolio aligned with the transition to a more sustainable, future-ready economy.

Pendal Focus Australian Share Fund is an actively managed, concentrated portfolio of 15 to 30 of our best investment ideas across the Australian share market.

Both funds are led by one of Australia’s most experienced portfolio managers, Crispin Murray. Crispin is backed by one of the largest, most experienced Australian equity teams.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Contact a Pendal key account manager here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

- Crispin Murray names the big policy shifts driving equities

- Find out about Pendal’s Focus Australian Share Fund here

OPTIMISM over stimulus and the rate of economic re-opening in the US has continued to drive equity markets higher.

The US$1.9 trillion American Rescue Plan Act was signed into law last week, while the EU increased its bond purchase program.

Locally the federal government announced its “PlaneKeeper” program to support the tourism industry. It was met with mixed reviews. The headline figures do not seem to match the details revealed so far and market impact was muted.

The S&P/ASX 300 rose 1.03%. Most sectors were up, although real estate and energy lost a little. The S&P 500 gained 2.69%.

Covid and vaccine outlook

The US retains positive momentum. New daily cases are down 73% from their peak while hospitalisations have fallen 71%.

Mobility data is picking up quickly, reaching its highest level since March last year. This is undeniably good for economic recovery.

About 21% of the US population have had a single dose and 11% have had two. This raises the risk of a second wave given the speed of re-opening.

The vaccination rate is closing on 3 million people per day as the broader supply arrangements take effect. Vaccine supply was up 140% in March versus February. April is expected to be up another 60%.

At these rates the US could reach herd immunity in June as long as demand for vaccinations exists.

The UK is experiencing similar trends in new cases and hospitalisations. Europe’s sluggish program remains a concern with a pick-up in new cases in Italy and part of Eastern Europe. The divergence between the US and EU is helping support the US dollar.

Economics and policy outlook

The big news from the US was the passing of the $1.9 trillion stimulus Act.

Some $400 billion worth of $1400 cheques will be disbursed by the month’s end. This is the single biggest weekly surge in stimulus spending so far — almost double the previous high in April 2020.

We expect some of this cash to find its way into the stock market and — if history is a guide — into the more speculative tech names.

To provide some context around the scale of stimulus, the US cumulative response stands at 36% of 2019 GDP. Europe has done 30% but with greater skew to loans rather than fiscal transfers.

This is driving the debt/GDP ratio back to levels not seen since World War II.

Expected nominal GDP growth in the range of 10% this year will help alleviate some of this. But the government remains vulnerable to any spike in bond yields. This is why the market remains focused on the outlook for inflation.

This stimulus package was in reaction to the depths of the crisis in December and January, but it comes as real-time economic indicators are recovering.

Company surveys are already picking up and the lead indicators for jobs growth are strong. Rising house prices are also supportive, judging by the surge in equity being cashed out of homes.

There are some concerns over the supplementary leverage ratio (SLR) in the US, which dictates the amount of capital large banks must hold against their loans.

Last year the Fed allowed the temporary exclusion of US treasuries and deposits held at the Fed from the ratio’s calculation.

This exclusion is due to expire at the end of March. This could potentially become a binding constraint on capital and distributions, which could see banks selling treasuries and being unable to make markets as efficiently.

This is a risk to watch, although the expectation is for some sort of transition period which would mitigate any near-term effects on the bond market.

Elsewhere, the EU announced it would significantly increase Quantitative Easing purchases in the next quarter to offset higher moves in the yield curve. However they did not raise the overall amount planned through to March 2022.

This helped improve EU bond yields, but leaves a confusing policy conundrum later this year if growth doesn’t accelerate materially.

Markets and stocks outlook

The key issue in markets is the degree to which concerns over bond yields offset huge cyclical tailwinds.

Moves were generally subdued last week, though a sell-off in bonds at the end of the week pushed US 10-year treasury yields up 6bps. This did not have an impact on equities.

The US dollar is at an interesting juncture. The dollar index — which measures the USD versus a basket of currencies — slumped over the second half of 2020, but has risen since January.

There is debate as to whether recent strength is a temporary rally, followed by more weakness — or whether the strength in the US recovery will see the greenback rally further. A stronger US dollar could prove a headwind for commodities.

Comments on bond yields from this week’s Fed meeting will be a key signal for currency.

There is an interesting trade developing within the broad rotation from value to growth. In growth, large-cap tech stocks are outperforming smaller, more speculative names for the first time since April last year.

It is important to remain mindful that today’s market is not just a case of simply “buy value, sell growth”. Plenty of value companies are structurally challenged.

There are also signs of a divergence between profitable growth companies with strong cash flow versus the longer duration, more speculative names.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

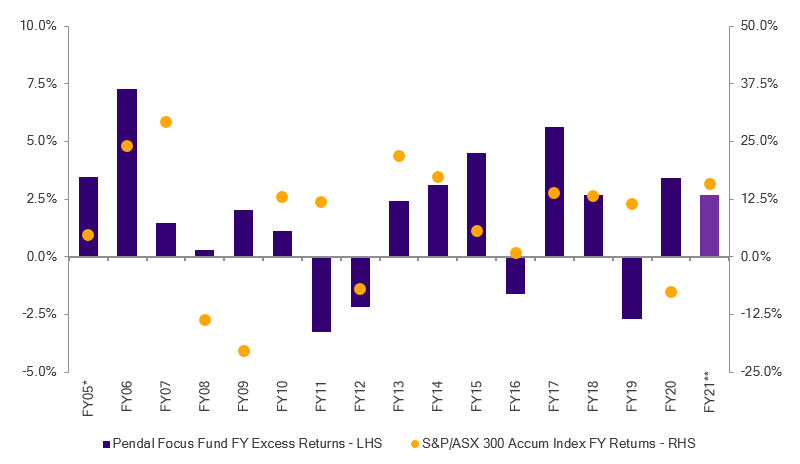

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Major shifts in policy-making — driven by the Covid crisis and a desire to correct GFC-era mistakes — can drive equities higher despite pockets of excess, says Pendal’s head of equities Crispin Murray (pictured).

Here are some insights from reporting season, drawn from Crispin’s bi-annual Beyond The Numbers presentation.

Watch the presentation here (registration required).

Key points

- Equities to benefit from major shifts in policy goals

- A number of factors are driving rotation from growth to value

- Performance is not simply “buy value, sell growth”

- Find out about Pendal Focus Australian Share Fund

INVESTORS may see pockets of excess in markets at the moment — but that’s not necessarily a sign that we’ve reached a top in equities, says Pendal’s Head of Australian Equities Crispin Murray.

These are symptoms of a policy agenda designed to avoid the mistakes of the Global Financial Crisis era.

That era resulted in fiscal austerity, pre-emptive monetary tightening and a focus on economic goals to the exclusion of other factors.

Today policy makers are thinking more about reducing inequality, building economic resilience and a greater role for clean energy.

This means bigger fiscal spending and very accommodative monetary policy.

Coupled with the impact of pent-up demand amid a re-opening economy and the return of fund inflows, this should combine to drive the stock market higher, Murray believes.

But he cautions investors to watch for additional complexity in markets.

For example Covid has accelerated structural trends such as the transformation of work via digitalisation and the impact of Environmental, Social and Governance factors when scrutinising companies.

Growing concern about inflation can also trigger bond market sell-offs which can have varying impacts across equity market sectors.

“We think equity markets will be resilient in the face of rising bond yields,” he says. “[But] they do have a big effect on what’s going to actually perform in the market.”

Higher inflation expectations and bond yields are seeing market leadership shift away from growth to cyclicals with pricing power. This suits the Australian markets, he says.

But future outperformance is not a simple matter of buying value stocks and avoiding growth stocks.

“There are still going to be companies in the value sector that are structurally disadvantaged.

“And you’re going to find companies in the growth sector that still have incredibly strong franchises. So, you need to be nuanced about your stock selection.”

The environment is ripe for an active, style-neutral approach focused on company specifics.

Four components of a well-constructed equities portfolio

Murray says a well-constructed portfolio should have four components:

- First, defensive stocks are needed to protect against risk and the chance of policymakers changing their minds.

- Second, a portfolio should have exposure to stocks that are leveraged to the potential inflationary pressures coming through.

- Third, investors should hold companies that used the crisis to improve their position and are ready to benefit from the release of pent-up demand.

- And finally, investors should consider the companies hit hardest by the pandemic who will see a material shift in fortune once the vaccines roll out.

“When we think about our portfolio, we think about the different roles stocks play. Like a football team, you need the defence, you need the midfield, and you need the attack.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions, as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21.

Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Find out about Pendal’s Focus Australian Share Fund here.

MARKETS rallied last week as the sell-off in bonds slowed down and data suggested the US economy was about to kick into a phase of strong growth.

The rotation to value continued. However on Friday we saw some signs of a rebound in tech names from a significantly oversold level.

The S&P/ASX 300 rose 0.98%, while the S&P 500 was up 0.84%

Covid and vaccine outlook

The rate of decline in new cases in the US slowed last week, but this likely reflects a lag in reporting after winter storms.

Hospitalisation rates continue to improve substantially, prompting speculation that restrictions in some countries may be eased sooner than expected.

The vaccine roll-out continues to accelerate in the US. It’s now reached 2.3 million per day. This will rise with greater supply. The number of people who have been vaccinated now exceeds the total number of reported cases in the US.

The gap in vaccination rates between the US (and UK) versus Europe continues to widen. This has implications for the economic outlook and may account for some of the strength in the US dollar last week.

Novavax released data from a trial in South Africa. Placebo group results revealed that people who had previously caught the original strain of Covid were just as likely to catch the new South African strain – and to become as sick.

This is an issue to watch. It may have implications for where and when international border restrictions are eased.

Economics and policy outlook

The US payroll data was very strong for February. It is likely to be the first of a number of strong data prints as the economy begins to reopen and the next wave of stimulus kicks in.

There is nevertheless a lot of slack left in the economy. The payroll data is still 10 million jobs below the previous peak. At the worst point of the GFC the payroll data had fallen by 9 million. This excess capacity is why policy makers believe they can stimulate and keep rates near zero for an extended period without triggering inflation.

Many of these lost jobs are in leisure and hospitality, which still has a long way to recovery. As the economy re-opens this sector could see a lot of job growth in the next few months. We are seeing signs of a potential breakout in mobility data above its range of the last nine months.

The Biden stimulus package is set to go ahead – US$1.9 trillion is more than most expected. This underpins our expectation of support for higher corporate earnings – and equity markets – as some 9% of annualised GDP is injected into the market in the next few months.

Focus now shifts to the infrastructure bill. Consensus is a US$2 trillion package, though there is chatter of something up to US$4 trillion.

We see indication of enormous pent-up demand globally, though the US stands out. Once the latest US$1400 stimulus cheques go out, the US savings rate is expected to hit 18%. That compares to 7% pre-Covid. This is supportive of economic activity, as are surveys suggesting a material pick-up in corporate capex later in the year.

Market outlook

Bonds yields continued to move higher last week, though in a more orderly manner.

Comments from the Fed suggest it’s comfortable with yields gradually rising towards 2%, given they reflect a better outlook for growth. The Fed is unlikely to move pre-emptively to control yields unless they start to break out in a disorderly manner and threaten to choke off growth.

US 10-year yields rose 16bps to 1.57% for the week. The Australian equivalent fell 8 bps to 1.83%.

Brent crude rose 4.9% on the OPEC decision to extend restrictions on production. Other commodities consolidated as the US dollar bounced.

We started to see a bounce in some growth names late last week. They may make a recovery form oversold levels from here. That said, we may see divergence between the larger cash-generating plays and the loss-making, higher-growth sub-sectors.

The Top 20 stocks drove the Australian equity market higher. The ASX 20 gained 1.8% versus a 1.5% fall in the Small Ordinaries. The banks played a key role, up 6.6% as the effect of higher bond yields flowed through. ANZ (ANZ, +10.2%) was the best performer in the ASX 100.

Resources (-0.6%) saw some consolidation as commodities softened, although Energy (+3.3%) saw the benefits of a higher oil price. Gold miners were among the worst performers in the market.

There was limited company news in the wake of reporting season.

Xero (XRO, -4.4%) announced its $280 million acquisition of Planday, a cloud-based workforce management solution based in Copenhagen. This extends XRO’s product suite, potentially helping further its expansion into Europe. The shares were caught up in a rotation away from growth, but we believe the deal is a good one. XRO remains among our preferred exposure in tech.

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21. Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Environmental, Social and Governance factors are now critical in asset allocation decision-making says Pendal’s Head of Multi-Asset Michael Blayney.

THE BIGGEST secular shift over the next decade is arguably the continuing emergence of — and demand for — Environmental, Social and Governance (ESG) factors in investment portfolios.

In the past ESG may have been considered, but it seldom had a meaningful value ascribed to its risk and wasn’t thought of in terms of asset allocation.

But ESG has emerged as a secular theme, alongside demographics, debt levels and productivity — and investors must think more deeply about how it fits into a portfolio.

“In the past, when an investor put together an ESG-focused portfolio, it would basically have the same asset allocation as a conventional fund,” says Michael Blayney, who head up Pendal’s multi-asset investment team.

“Now it’s essential to think about how we can incorporate ESG and sustainability factors into both strategic and active asset allocation decisions.”

Critical big-picture factor

ESG has not only emerged as a long-term secular consideration, it’s becoming the most critical “big picture” factor for the next decade.

“The time between a scandal breaking out and a CEO being shown the door has shortened considerably,” says Blayney. “Community expectations have shifted, particularly on the environmental side.”

Find out about

Pendal Multi-Asset Funds

“We’re seeing it in Europe with the new Green Deal. With the change in the White House, the US economy will shift that way too. There’s clearly a long-term thematic going on. People are focused on how they can contribute to – and benefit from — long-term, positive solutions.”

Of the different ESG factors, the environment provides one of the clearest links to economic growth factors.

“If you take Australia, we actually look a lot worse on environmental performance because we dig a lot of fossil fuels out of the ground and still use a lot of coal for our energy,” Blayney says.

Because the Australian economy and market is more exposed to environmental issues, it creates a secular headwind. About three quarters of Australia’s energy mix is from coal and we are the world’s third biggest fossil fuel exporter according to recent research by the Australia Institute.

“As a result, the home bias in asset allocation should be reduced from historical levels and more so for sustainable funds,” Blayney says. “The Australian economy scores very well on the S and G factors of ESG, but the equity market is let down by our high carbon intensity.”

Governance and social issues matter as well, and are particularly critical considerations in emerging markets.

“There have been studies that show well-governed businesses tend to perform better,” Blayney says. “But there are nuances in that. The rate of change of governance can be very important too.

“We’ve invested in Korean and Japanese equities at times in the last couple of years and a key element of the investment thesis has been improved governance in those countries.”

Opportunity for better returns

ESG is moving beyond risk management. “Previously investors tended to focus on the bad stuff, and how that could trigger a fall in a share price,” Blayney says.

“It’s obviously still important … but nowadays we also think about ESG and sustainability in terms of the opportunity to generate better returns from the portfolio.

“It’s very much a big shift in thinking and it’s coming into the mainstream. But it has evolved more in some markets around the world, notably Europe. There’s a bit of ground to make up in the United States, Australia and parts of Asia. That provides opportunity,” Blayney says.

“When you consider how some big investors allocate their assets, there’s still quite a lot more that can be done to better align with both ESG risks and opportunities. Many investors know about ESG, but they’re not sure if it’s already factored into the price [of an asset]. That’s where we can help.”

There’s a pressing need for investors to consider ESG factors when allocating assets.

“In our research, the integration of ESG risks added weight to decisions to decrease exposure to Australian shares,” he says. “It also indicated investors should increase weightings to some offshore opportunities.”

“While a lot of environmentally aligned assets have had a strong run, we still think there’s good opportunity in the longer term.”

About Michael Blayney and Pendal’s Multi-Asset capabilities

Michael Blayney leads Pendal’s multi-asset team.

Michael has more than 20 years of investment management and consulting experience. He was previously Head of Investment Strategy at First State Super and head of Diversified Strategies at Perpetual.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The team — which includes Stuart Eliot, Allan Polley and Rita Fung — manages our multi-asset portfolios with a focus on strategic asset allocation, active management and tactical asset allocation.

Pendal Horizon Fund (APIR: RFA0025AU, ARSN: 096 328 219)

With effect from 15 March 2021, the “Pendal Ethical Share Fund” will be renamed the “Pendal Horizon Fund” (Fund).

The change of name will more accurately reflect the investment framework and responsible investment priorities of the Fund which extend beyond just ethical screens being applied.

The investment processes of the Fund (including new and tighter screens and a framework that places a greater focus on selecting stocks and industries that meet our investment criteria, responsible investment priorities and philosophy) were implemented in October 2020.

The responsible investment priorities of the Fund centre on a future-ready Australia, by participating in and supporting the transition to a more sustainable economy.

There will be no changes to the investment strategy, objective or distribution frequency of the Fund.

An updated Product Disclosure Statement (PDS) will be issued on 15 March 2021 and made available on www.pendalgroup.com.

Our head of equities Crispin Murray makes the case for a continued rise in equity markets in a presentation to Portfolio Construction Forum’s Markets Summit. Here’s a quick summary.

Key points

- Government stimulus and accommodative monetary policy driving stock markets

- Policy push to lift wages and reduce inequality

- Focus on clean energy and economic resilience

A DESIRE to correct the policy mistakes of the post-GFC era should underpin a continued rise in equity markets as the global economy recovers from COVID-19, believes one of Australia’s most experienced portfolio managers.

A unique combination of supportive government policy and the re-opening of the global economy should unleash of a wave of pent-up demand for consumption and investment, driving stock markets to new highs, believes Crispin Murray, who heads up one of Australia’s biggest equities teams at Pendal.

Unlike previous booms, this time governments will tolerate excesses in some parts of the market in the hope of improving wages, reducing inequality and building the infrastructure to support a clean energy future, he believes.

“There’s been a fundamental shift in the motivations and mission of policymakers,” says Murray in a presentation to the Portfolio Construction Forum Markets Summit 2021.

“They have observed what’s happened with the rise of populism, they’ve seen what happened as a result of COVID and they’ve looked back at what happened in the post-GFC era and there are a number of wrongs – a number of policy mistakes – that they are now addressing.

“And in doing that, they’re actually helping to support the equity market.”

Murray identifies three key policy mistakes that governments are seeking to correct:

- The first is inequality, which intensified post-GFC as policymakers kept tight hold of fiscal and monetary policy, while globalisation and the growth of the technology industry kept a lid on real wages.

- The second is a growing fragility in the world economy produced by global supply chains, just-in-time production and finely tuned corporate balance sheets.

- And the third is policy complacency about the environment and the need to move to clean energy, with little urgency to meet carbon emissions targets.

“COVID showed that existential threats can happen and they can happen very quickly.

“These things focus policymakers’ minds. They had to respond to a cyclical issue, but it also focused their minds on these structural issues.”

Policy changes underway

Murray says policy changes are occurring in three areas.

A new era of monetary policy has abandoned containing inflation as a short-term goal in favour of driving social cohesion and full employment.

Real interest rates have been negative for some time and will stay lower over the course of this cycle, says Murray.

Monetary stimulus is also causing money supply growth that has not been seen since after the war.

“When you’ve got that level of stimulus coming into the economy, it has to go somewhere. This is why you’ll see equities benefiting from that sort of monetary policy environment.”

Fiscal policy is also supportive.

“I’d have to go back to World War Two to see anything like this level of fiscal deficit, this fiscal stimulus.

Uniquely, fiscal and monetary stimulus is occurring simultaneously as a decade of fiscal austerity comes to an end.

“It will be supportive for the economy, and for earnings.”

Until now, expansionary policy has been held back by the headwind of the COVID-19 pandemic and its associated government shutdowns.

“But now what we’re seeing is those headwinds turning to tail winds. We’re going to see the excess savings, the benefit of pent-up demand as vaccines are rolled out, you’re going to see continued loose monetary policy and fiscal policy.”

Murray says the stimulus has produced close to US$3 trillion of excess savings in the US alone, equivalent to more than 16 per cent of actual consumption which is the major driver of the US economy.

Meanwhile, available capital in private equity funds and special purpose acquisition companies is at record levels.

As this excess cash starts to find its way into the economy it will drive both higher consumer spending and higher investment.

“There’s going to be an underlying support for the market because of that level of liquidity.”

About Crispin Murray and Pendal Focus Australian Share Fund

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Source: Pendal. Performance is after fees and before taxes. *From 01 Apr 05; **as at 28 Feb 21.

Past performance is not a reliable indicator of future performance.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about Pendal Focus Australian Share Fund here.

Regnan’s impact investment team … (l-r) Mohsin Ahmad, Maxine Wille, Maxime Le floch and Tim Crockford

Regnan’s impact investment team has released its maiden quarterly impact report for the Regnan Global Equity Impact Solutions fund.

It’s the first report since senior fund manager Tim Crockford and his impact investment team moved to Regnan — a global leader in responsible investing. Regnan is part of Pendal Group.

In the report, which can be downloaded here, Crockford and his team demonstrate how innovation in agriculture is “spawning a multitude of new technologies and business models, providing attractive investment opportunities”.

The report also outlines investments in German recycling innovator Befesa and Brazil-based educator YDUQS.

“The team and I are excited to be up and running again, having successfully launched the Regnan Global Equity Impact Solutions strategy in October 2020 in the UK, and more recently in Australia,” Crockford says in the report.

Impact investing aims to generate both a financial return and a positive impact on society.

It’s the latest stage in the evolution of responsible investing, which began in the 1980s with the emergence of ethical funds created by faith-based groups looking to align their investments with their values.

Ethical funds were originally about screening out companies such as tobacco growers, casinos and weapons makers. But impact investing goes further, recognising that portfolios can be biased towards companies that generate positive outcomes for the world, while also delivering strong returns.

“This is the evolution of the project we started together back in early 2016,” Crockford says in the report.

“Our ambition has always been to create an exciting, differentiated core global equity solution for our clients… A solution that allows investors to deliver a genuine positive impact by investing in mission-driven companies that create the environmental and social solutions which drive the advancement of our productive systems.”

Download the Regnan Global Equity Impact Solutions Fund Quarterly Impact Report (Q1 2021)

Who is Regnan?

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.