Where are the opportunities for investors as trade re-opens post-pandemic? Here’s a quick overview from Pendal’s head of multi-asset Michael Blayney (pictured).

EQUITY markets in developed economies have run hard. Wall Street is trading close to record highs.

The local S&P/ASX200 is heading the same way. European share markets have been trending higher since November last year.

So where are the opportunities for investors? Is the bull run petering out, or is there still plenty of steam?

“Obviously markets have run incredibly hard and the recovery has been fast,” says head of Multi-Asset at Pendal, Michael Blayney.

“And there’s still lots of positive cyclical factors. There’s all this massive fiscal spend. You’ve got easy monetary policy and there’s a boost to confidence from vaccines and the potential reopening of economies.”

But — and it’s a big but — valuations are nowhere near as attractive today as they were a few months back, Blayney says.

“Some things are getting quite expensive. Australian equities are on the marginally expensive side.

“There’s always a margin of error so we’re not at the point where we’d do any serious underweighting. But the opportunity to buy things cheap is behind us.”

It’s the same story in many developed markets.

“US large caps have been expensive for a while,” Blayney says. “They have been the clearest beneficiary from the stay-at-home trade. It will take time, but as the economy reopens and the recovery picks up, you might see a bit of a rotation [into US equities] but the starting point is quite expensive.

“A lot of the European markets have rallied pretty hard as well,” he says. “The United Kingdom still stands out as the value market in that region.”

Opportunities in Emerging Markets

There are a handful of opportunities in emerging markets, such as Mexico, but the gorilla amid those economies is China, accounting for close to 30 per cent of the emerging markets index.

“It’s run pretty hard and starting to look pretty expensive as well. There’s not as many opportunities in China as in other emerging economies,” he says.

The Shanghai Composite has easily matched the performance of most of the major equity markets in 2021 and is trading around five-year highs. Robust economic data is underpinning the investor buying.

With opportunities harder to come by, it might be time for investors to rethink their allocation to equities, Blayney says.

“We are not at a point where people should run for the hills and sell everything. It is nothing like that. But it is appropriate for people to start thinking about lightening up, particularly from equities that have run hardest.”

“There are still some opportunities. With cash rates virtually zero, it’s very hard to put a meaningful part of a portfolio in cash. So you need to look for options. Some of the listed real assets – listed REITS (Real Estate Investment Trusts) for example – are still reasonably cheap,” he says.

“We have an overweight [view] because REITS will be beneficiaries of the re-opening of the economy. There are still a few structural headwinds, particularly around shopping centres, but people are heading back to the office.

“They haven’t rallied as hard as other parts of the market and we are at this point of incredibly low yields. So people will go: where can I find some income?”

The “re-opening trade”

Critical is the roll-out of the vaccination program in Australia and elsewhere. If successful, economies will pick up again and real assets should benefit. In investor parlance, it’s the “re-opening trade”.

“REITs have decent yields backed by real assets. You might see a bit of inflation which people have been forecasting for a long time. It hasn’t happened yet, but the ingredients of fiscal and monetary stimulus are there,” Blayney says.

“You’ve seen inflation flow through to house prices already. Who would have thought in a recession and with rising unemployment you’d get a pop in house prices?”

What about outside equites and real assets?

“Australian and US bonds look better than they did a month or two ago,” Blayney says. “But they could go a bit lower over the remainder of the year. There is a one in the front of the yield, and they can at least give a decent return over cash.”

“But investors need to be looking at high-grade bonds because with a lot of the high-yield stuff, you are just not being paid for the risk you are taking.”

Blayney says, candidly, that there just aren’t as many attractive opportunities in the market at the moment.

As a result, multi-asset funds need to be thinking about the relative value of assets.

“It might be large caps versus small caps. We’ve put on a couple of positions like that. It’s very difficult for a retail investor to do that unless they take on a multi-asset fund like ours,” he says.

“A lot of the opportunities now are in relative trades. Even if you think about value stocks, which were smashed by COVID-19 and were trading on low price-to-earnings multiples.

“That tailwind isn’t quite as strong. Even in growth assets, the opportunity is more around relative value opportunities,” he says.

“It’s really a relative value opportunity now, rather than the great buying bonanza that it was back in March and April.”

About Michael Blayney and Pendal’s Multi-Asset capabilities

Michael Blayney leads Pendal’s multi-asset team.

Michael has more than 20 years of investment management and consulting experience. He was previously Head of Investment Strategy at First State Super and head of Diversified Strategies at Perpetual.

Pendal’s diversified funds provide investors with a variety of traditional and alternative asset classes and strategies.

The team — which includes Stuart Eliot, Allan Polley and Rita Fung — manages our multi-asset portfolios with a focus on strategic asset allocation, active management and tactical asset allocation.

The Fund’s investment strategy, including how we take labour standards and environmental, social and ethical considerations into account when selecting, retaining or realising investments of the Fund, will be changing from 7 April 2021.

Investment strategy

Effective from 7 April 2021, Pendal will apply our sustainability assessment framework to the Fund’s investments which draws on both qualitative and quantitative inputs to determine which companies meet our sustainability criteria.

Our sustainability assessment framework considers a company’s characteristics, including:

- The extent to which its products or services are beneficial to the environment and/or society;

- The manner in which it conducts its business and employs leading sustainability practices; and

- Its management of its environmental, social and governance (ESG) risks.

The Fund typically favours companies which demonstrate leading sustainability characteristics under this assessment framework, and typically avoids those which rate poorly. The Fund may invest in companies which do not rate well but otherwise meet our minimum sustainability and exclusionary screen criteria. Any investment in the Fund, regardless of its sustainability assessment, must also pass our rigorous fundamental investment criteria before being owned in the portfolio.

In addition to employing a sustainability assessment framework, the Fund utilises exclusionary screens to avoid companies involved in industries or business activities which cause significant social and/or environmental harm.

In managing the Fund, we avoid investing in companies which:

Fossil Fuels

- Directly extract or explore for fossil fuels (specifically, coal, oil and gas); or

- Derive 10% or more of their total revenue from fossil fuel-based power generation, or from fossil fuel refinement or distribution (coal, oil and gas)*; or

- Derive 10% or more of their total revenue from the provision of supplies or services which relate specifically to fossil fuel extraction or exploration (coal, oil and gas)*

*Companies with a climate transition plan may be exempted from this exclusion, provided that they have in place a Paris Agreement aligned transition plan and produce climate-related financial disclosures annually, which in both cases we consider credible.

Uranium

- Derive 10% or more of their total revenue from directly mining uranium for the purpose of nuclear power generation

Logging

- Derive 10% or more of their total revenue from unsustainable forestry or forest products, including non-Forest Stewardship Council certified forest products or non-Roundtable on Sustainable Palm Oil certified palm oil production

Gambling

- Directly manufacture, own or operate gambling facilities, gaming services or other forms of wagering; or

- Derive 10% or more of their total revenue from the indirect provision of gambling (for example, through telecommunications platforms)

Pornography

- Produce pornography; or

- Derive 10% or more of their total revenue from the distribution or retailing of pornography

Weapons

- Manufacture or distribute controversial weapons (such as cluster munitions, landmines, biological or chemical weapons, nuclear weapons, blinding laser weapons, incendiary weapons, and/or non-detectable fragments); or

- Manufacture non-controversial weapons or armaments (including civilian firearms or military equipment); or

- Derive 10% or more of their total revenue from the distribution or retailing of non-controversial weapons or armaments (including civilian firearms or military equipment)

Alcohol

- Derive 10% or more of their total revenue from the distribution or retailing of alcoholic beverages

Tobacco

- Produce tobacco (including e-cigarettes and inhalers); or

- Derive 10% or more of their total revenue from the distribution of tobacco (including e-cigarettes and inhalers) or supply of goods or services specifically related to the tobacco industry (for example, packaging or promotion)

Animal cruelty

- Directly undertake animal testing for cosmetic products

- Directly undertake live animal export

Predatory lending practices

Directly provide products or services with lending practices that are unfair or deceptive to ordinary borrowers, including small amount short term loans at higher than commercial rates of interest (for example, payday loans, pawn loans or the use of aggressive sales tactics)

Breaches/Misconduct

We consider to have been found to have significant breaches of social or environmental norms or regulations, or are subject to serious and substantiated allegations of unethical conduct, which we consider have not been remedied or adequately addressed

Most notably, investors in sustainable funds have increasingly sought to avoid allocating capital to companies whose activities significantly contribute to climate change. For this reason, we will be applying tighter fossil fuel-related screens in the Fund.We believe it is in the best interests of investors for the new and tighter exclusionary criteria to be implemented for the Fund. These screens are expected to better meet investors’ expectations regarding the holdings of a sustainable fund, which have evolved considerably since the Fund was launched in 2001.

Why are we making the changes?

Transition into the new investment strategy

The changes will require a number of stocks in the Fund to be sold from 7 April 2021, as these stocks do not meet the new exclusionary criteria. These stocks are relatively liquid and we expect to be able to complete the sell down within one day under normal market conditions.

Management fee

There is no change to the management fee of the Fund which will remain at an issuer fee of 0.85% p.a.

About the Fund’s Portfolio Manager

The Fund will continue to be managed by Rajinder Singh in Pendal Australian Equities Team who has more than 18 years’ industry experience.

In managing the Fund, he will be supported by the Pendal Australian Equities Team, a team of 20, one of the largest fundamental Australian Equities Team in the market.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Find out about Pendal’s Focus Australian Share Fund here.

EQUITIES dropped and bond yields rose as markets tested policy makers’ commitment to keep rates lower for longer in the face of fiscal stimulus.

The pace of rising bond yields was material in a historical context. It implied the first rate rise would be brought forward to 2022. Central banks stepped in by the end of last week in a co-ordinated move to stabilise yields.

The challenge facing central banks is not so much how to drive yields lower again — but ensuring the pace of increases remains slow and controlled. The next few weeks will be a key test of their ability to do so.

The S&P 500 fell 2.4% to finish the month up 2.8%. The S&P/ASX 300 lost 1.5% for the week and is up 1.5% for February. The move in bond yields saw a further rotation from growth to cyclicals.

Reporting season ended up as one of the strongest in years including upgrades for F21 EPS from about 7% to 14%. This was driven by sharper bounces in earnings from resource-related stocks and Covid “winners” like retail.

That said, the latter were some of the worst performers for the month as growing confidence in the vaccine roll-out – coupled with the bond sell-off – dragged on momentum names.

In context of the overall market, the biggest shift in market expectations came from the banks. Expectation for FY21 EPS growth shifted from flat in January to more than 20% by the end of February.

We continue to expect equity markets to remain well supported following this period of consolidation, helped by good in-flows and strong earnings growth.

Covid and vaccine outlook

It is more of the same on the Covid front internationally. Countries rolling out vaccines continue to see falling new cases and hospitalisation rates.

Poor weather weighed a little on the rate of vaccinations. But in recent days the US has been nearing 2.3 million shots a day as the pharmacy network is brought into distribution. The approval of Johnson & Johnson’s vaccine — plus increased production of existing vaccines — has the potential to drive US to more than 3 million shots a day.

The UK’s program is also showing momentum. But European vaccination rates remain far lower, apparently due to greater public scepticism. This is likely to see Europe’s recovery lag the US. This could also act as a dampener on US bond yields. If the spread between European and US bonds widens we could see a shift in capital flows between them.

Policy and economics outlook

Bond yields are the current key issue. The bond sell-off is material in a historical context — particularly given its speed. It was exacerbated by a poor auction of US 7-year bonds, with the worst bid-to-cover ratio in ten years.

There are two factors to note:

- The increase in short-term rates indicates expectations of a first rate hike at the end of 2022. Expected rates for mid-2023 are now 40bps higher than they were at the start of the month. These expectations are well ahead of the Fed’s stated position. This effectively tests its resolve given the expected scale of growth coming through.

- The volatility occurred in real rates as opposed to break-even rates. The market is effectively saying they don’t buy real rates staying this low given the fiscal stimulus. The question is whether the Fed can hold its nerve as we see growth and inflation begin to rise.

One paradox was that inflation expectations actually started to roll over. This would be inconsistent with a continued rise in real yields.

The yield curve continued to steepen, which has been supportive for financials in the equity market.

We saw a bigger move in Australian bonds than US. This has taken our yield curve to its steepest in more than 20 years. The RBA increased Quantitative Easing to hold the 3-year yield. This worked, but also reinforced concerns about the 10-year yield.

We have seen a concerted effort by central banks to ease concerns in response to these moves. The issue for countries outside the US is that they are seeing the rise in yields, but do not have the same degree of stimulus as the US. Therefore the rise in rates is a negative for any recovery.

The Fed is the only central bank not to respond so far. But we’ve seen two new speeches placed in the diary: Lael Brainard pre-market open on Monday and Chair Powell on Wednesday. We expect both to be more explicit on not raising rates and not announcing specific bond market intervention yet.

In the near term the current extreme positioning in terms of bond shorts — coupled with Fed jawboning — could see a relief rally in bonds which would support a rotation back to growth.

Beyond this, we think the trend in US 10-year yields towards 2% will remain in pace. The Fed’s aim is not drive to yields down from here, but to make sure the increase is gradual and orderly.

A continued accelerated surge in yields would be an issue for equity markets. But we believe the underlying data will allow the Fed to maintain its current approach, rather than being forced into a dramatic U-turn.

Markets

Equities sold off last week, led by growth stocks. US 10-year bond yields stabilised to end last week up only 7bps — but they are up 34bps for the month. Australian 10-year yields rose 48bps for the week and 78bps for the month.

There was strength in commodities as an inflation hedge. Brent crude was up 6.3% and copper 4.3%. If we do see a relief rally in bonds we could see a near-term reversal in commodities.

The rotation from value to growth — when seen via proxies such as US regional banks (value) and Cloud-tech ETFs (growth) — had a move of similar scale to November’s, when the first surge in vaccine optimism occurred. Banks may be due a pause here following strong gains.

Equity fund inflows across the globe have remained very strong. US$414 billion has flowed into equity funds in the past four months, dwarfing anything seen since the GFC. This — along with solid corporate earnings — should help support the market if we see a stabilisation in bonds.

Reporting season

Overall it was a strong reporting season. FY21 EPS growth increased from +6.9% at the start of February, to +14.8%.

The ratio for companies upgrading guidance by more than 5%+ to downgrading by 5%+ was two-to-one. It was the same for dividends.

Banks delivered the biggest surprise sector-wise. Lower bad-and-doubtful debts, better margins and volumes encouraged FY21 earnings growth expectation to climb from 0% earlier in the year to more than 20%.

Our preference here remains Westpac (WBC) and ANZ (ANZ) which have the greatest leverage to positive trends.

Stock-wise reporting season was very much a story of inflation hedges and less-loved stocks turning the corner while tech, gold and high-performing retailers all got hit.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and leads one of the largest equities teams in Australia.

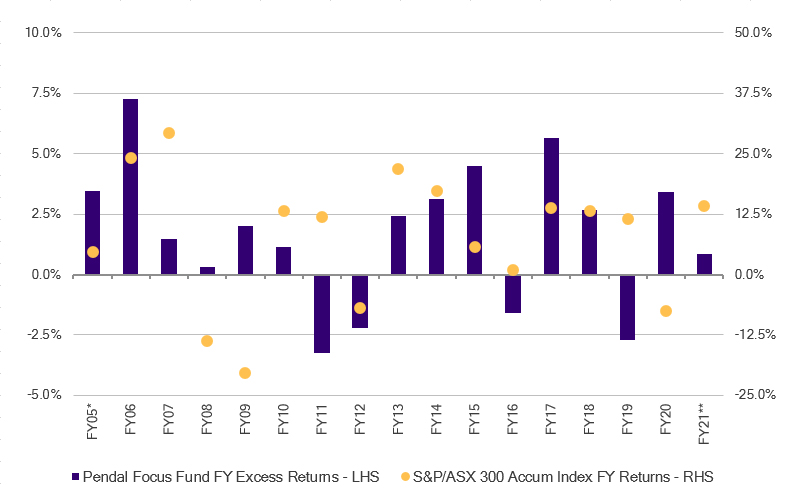

Crispin’s Pendal Focus Australian Share Fund has beaten the benchmark in 12 years of its 16-year history (after fees), across a range of market conditions , as this graph shows:

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Which emerging markets have the fiscal firepower and structural advantages to benefit from the next phase of the global recovery?

James Syme (pictured), co-manager of Pendal’s Global Emerging Markets Opportunities Fund, shares his insights in a new Pendal webinar. This is a summary of the webinar.

- Watch: View James Syme’s Emerging Markets webinar (18 mins, registration required)

- Presentation: Download the webinar presentation (pdf)

- Brochure: Download a Pendal Global Emerging Markets Opportunities fund brochure (pdf)

- Web page: Visit the Pendal Global Emerging Markets Opportunities fund web page

EMERGING MARKETS are at an historic inflection point as the US dollar begins to reverse a decade of strength, setting the scene for a strong rally in regional equity markets.

The US dollar is the currency of choice for at least half of all international trade invoices — around five times greater than the US share in imports — giving the dollar an out-sized role in the global economy.

This means emerging markets are highly sensitive to movements in the US currency, London-based senior fund manager James Syme tells clients in a new webinar. Syme co-manages Pendal’s Global Emerging Markets Opportunities strategy with Paul Wimborne.

“Periods of dollar weakness have led to the great economic market booms in emerging markets,” Syme says in the webinar. “Dollar strength has led to some great stresses in parts of the emerging world.”

The US dollar has been strong since 2011, putting significant stress on parts of the emerging world. But from last year, it has started to enter a period of weakness.

In strong dollar environments since 1989, investors in emerging markets equities have, on average, lost money, Syme says.

“In contrast, the annualised equity return in US dollars since 1989 in weak dollar environments is nearly 27% per year.

“It’s a pattern that still exists – in the last eight months of 2020 with a weaker dollar, emerging markets as an asset class rallied over 40 per cent.”

Still, Syme suggests investors should use care when selecting emerging market investments and should take a genuinely diversified, selective approach to asset selection.

Types of Emerging markets

Syme divides emerging markets into three broad groups:

- High current account deficit markets with high sensitivity to the US dollar like much of Latin America, South Africa and Russia

- Countries with strong domestic demand that are less exposed to the global economic cycle like India and south east Asia

- Current account surplus manufacturing exporters like China, Korea and Taiwan that are significantly exposed to the global economic cycle.

“A genuinely diversified portfolio would contain some exposure to each group but would still have the opportunity to be highly selective,” he says.

Syme cautions that the major indexes may not offer investors true diversification as they become dominated by the mega-cap tech stocks of the region.

Four mega-cap tech stocks – China’s Alibaba and Tencent, Taiwan Semiconductor Manufacturing Company and Korea’s Samsung Electronics – now make up 21.3 per cent of the MSCI Emerging Markets Index.

Many emerging market funds hold all four of the mega-caps, concentrating risk and lifting exposure to China where he is becoming more cautious on the outlook.

China’s regulatory crackdown on Alibaba in late 2020 has the potential to affect the whole sector while US government restrictions are creating a tricky investment environment for Chinese state-owned enterprises.

Taiwan and Korea have much better fundamentals with strong operating conditions, but valuations are starting to look stretched in some parts of the market, particularly in Taiwan.

“If we use consensus earnings estimates as a marker of recovery … we can see strong recoveries in Korea and Taiwan as well as the clear signs of a slowdown in China,” he says.

Recovery in India

Elsewhere, India enjoyed the shallowest earnings downturn in the region during COVID and is experiencing a powerful recovery, Syme says.

“We also know that India has some of the best prospects for coronavirus vaccination. It is the world’s largest exporter of pharmaceuticals and is gearing up for a very significant vaccination program. India is one of our favourite emerging markets.”

South east Asia is suffering from the tourism downturn and the commodity sectors have not made up the shortfall.

On the contrary, the macroeconomic environment is very supportive of the big emerging markets commodity exporters like Brazil, Mexico and South Africa.

“Support for exports from terms of trade, mostly driven by commodity prices and the resulting strong trade balances, suggest that currencies are cheap and that the recoveries we’re seeing in domestic demand could be quite sustained for a long period of time,” he says.

“There is also significant potential for positive earnings revisions, which would therefore have the potential to lift those equity markets.

“These are very positive macro attributes that we think have been ignored by many investors in emerging markets, who have been focused on the large cap tech space.”

James Syme is a senior portfolio manager and co-manager of Pendal’s Global Emerging Markets Opportunities fund.

Find out more about the fund HERE.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Find out about Pendal’s Australian share funds here.

RISING bond yields last week reflected concerns about inflation. In equities, higher yields saw a rotation away from growth and defensives to financials and resources.

News flow was driven mainly by reporting season. In aggregate, results were better than expected for the banks, resource companies and a number of industrials. However this was not reflected in the S&P/ASX 300’s muted reaction (+0.01%). This is tied to the market’s strength going into reporting season, as well as the headwind of rising bonds.

Ultimately we believe there is a strong chance that decent earnings, more stimulus and pent-up demand following the vaccine rollout will underpin and drive markets further following some consolidation.

Covid and vaccines

New daily cases and hospitalisation rates continue to fall in the US, UK and Europe. Vaccination rates stalled a little, due to poor weather. With the involvement of pharmacies it is possible to see vaccinations in the US continue to accelerate into Spring.

Economics and market

We finally saw a crack in the bond market with sentiment around vaccines improving, cases continuing to fall, increased fiscal stimulus size increasing and central banks determined to hose down any suggestions of tightening. Ten-year government yields backed up 13bp in the US and 21bp in Australia as inflation risks were priced in.

Interestingly, this move in yields is more linked to rising real yields. This suggests the market is questioning the Fed’s resolve to maintain its commitment to current rate settings in the face of huge fiscal stimulus.

So far there is no sign of the Fed feeling the need to react and buy bonds. Equities have also absorbed the move well, credit spreads are stable and liquidity remains plentiful. A steeper yield curve is also good for banks and ultimately will encourage credit growth.

The usual flow-on effects occurred, with a rotation to value (notably financials) and growth underperforming. Traditional defensives such as utilities and consumer defensives were worst hit.

Commodity prices rose after the Lunar New Year. Oil stalled with the Texas freeze supporting prices, but was offset by signs Saudi may ease up on supply restrictions.

There were potential early signs of sentiment rolling over towards some recent pockets of excess such as IPO ETFs, Tesla and renewable energy ETFs. Bitcoin, however, surged onwards.

Results summary

Overall reporting season has been good so far, with strong free cash flow generation and positive momentum on earnings. So far consensus EPS expectations are up 5.3% from last month (+2.4% ex-resources).

Good results

The banks delivered surprisingly good results. Westpac (WBC, +8.8%), ANZ (ANZ, +7.2%) and Bendigo Bank (BEN, +5.7%) all reported bad and doubtful debts (BDDs) were falling away – particularly so at WBC. More importantly better margin performance — driven by the deposit side — lifted pre-provision profits forecasts about 5% and out-year earnings some 10%+. ANZ and WBC are our preferred exposures: they sit at big valuation discounts to Commonwealth Bank (CBA, -5%) and National Australia Bank (NAB, +0.7%).

BHP (BHP, +5.8%) and Rio Tinto (RIO, +5.0%) delivered solid operational results. Stronger prices saw an uplift from their copper divisions. Cash flow was through the roof and management are returning it to shareholders. Both companies surprised on the upside in terms of dividends. BHP’s, for example, was up 55% on the same half last year. Both companies are likely to yield in the 7-8% range.

Fortescue Metals (FMG, +0.6%) also delivered strong cash flow and dividends — its interim yield was almost 6%. But the attention was focused on the immediate departure of several managers and slashed bonuses for a couple more, including the CEO. This was related to a delay and $400 million (15%) increase in cost of the Ironbridge development. The sanctions appear to be related to concerns over how senior managers have been focused on the issue – and how it has been communicated internally — rather than indicating a more serious problem. We are mindful of keeping watch on FMG’s future investment program. The company is suggesting that up to 10% of profits will be channelled into renewable energy and green hydrogen investments. This is a lot of money at current iron ore prices and investors will need to make sure this capital is used productively.

Domino’s Pizza (DMP, +12%) was the strongest performer in the ASX100. Covid provided a tailwind for its European and Japanese businesses in particular. Its business model has a circularity — more profit growth enables faster franchisee store roll-out.

Tabcorp’s (TAH, +3.4%) earnings came in about 5% above expectations due to strength in lotteries. The wagering turnover was reasonable, growing 5%, but yields were a bit light. This highlights continued competitive pressure in the segment. The market remains focused on the price they may be able to extract from suitors for their wagering business.

Treasury Wines (TWE, +10.2%) delivered good performance in the parts of its market unaffected by trade disputes. Cash flow was good and management were able to demonstrate how they are reallocating wine away from China without hurting their margin. This was a better outcome than many expected, but the company still has a long way to go to.

JB Hi-Fi (JBH, -2.3%) continues to see strong sales growth in 2021, in stark contrast to trends at Coles (see below). In January JB Hi-Fi Australia enjoyed 18.6% sales growth versus the same month last year, while the Good Guys was up 14.4%. At this point, pent-up demand appears to be still be coming through in consumer electronics.

Cochlear (COH, +7.4%) is seeing a quicker return to normality than expected. While Q1 sales fell 8%, they rose 7% in Q2. There are signs the company is winning market share.

Goodman (GMG,-4.1%) delivered a good result and earnings upgrade. But expectations were high heading into the result and the stock got caught in a rotation away from growth and defensives.

Mixed results

CSL (CSL, -0.8%) delivered a very strong first half. The company is not yet seeing the impact of plasma collection issues from last year. But management were particularly cautious on the next two halves, before signalling a strong recovery beyond that. Recent performance suggests the market looks like it hasn’t the patience to wait near term, given funding needs to raise weights in resources and banks. Looking through the near-term supply challenge, we continue to see strong growth in demand.

As always QBE (QBE, +3.8%) was complicated. Recent provision top-ups remain an issue in the near term. But the company is seeing the benefits of accumulated premium growth which suggests decent margin improvement next year and double-digit top-line growth. As long as provisions remain under control QBE could be heading into a sweet spot for the next few years.

Star Entertainment (SGR, +0.3%) and Crown (+3.6%) remain disrupted by lockdowns and restrictions, though these are easing. Management have taken out costs and both are at the end of an extended period of capex spend, so becoming more interesting. The key risk is a regulatory burden that is more onerous than expected. On this front the disappearance of overseas VIP as a profit source is positive.

Origin Energy (ORG, +2%) told a tale of two very divergent businesses. Its LNG division is benefitting from higher prices and lower costs, generating a lot of cash flow. However it energy markets business is under enormous pressure from falling prices, which are not being fully offset by costs.

Disappointing

Gold stocks were hit hard on the rise in real yields and were the market’s worst performers. This was not helped by poor communication from Evolution (EVN, -10.6%) on development of its recently acquired Red Lake mine.

Coles (COL, -9.6%) disappointed. Like-for-like sales growth slowed to 3.3% in the first six weeks of 2021 – sooner than most expected. There is a positive read-through for our preferred position in Metcash (MTS, -4.6%). COL management called out their large CBD stores as the key source of weakness. In contrast, regional and convenience-style stores continue to do well. This is helpful for MTS’s IGA franchise.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds.

Crispin manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

India has experienced a powerful demand recovery in recent months while Brazil, Mexico and South Africa have been more mixed.

Here James Syme and Paul Wimborne (pictured above) — managers of Pendal’s Global Emerging Markets Opportunities strategy — explain their latest EM thinking.

WE HAVE had a steadily evolving interest in the traditionally higher-beta emerging markets, as followers of our views will know.

We see domestic recoveries that have a good distance to run based on current trade balances and a reset to credit and demand cycles that 2020 created.

Some powerful upward moves in terms of trade (the ratio of export prices to import prices) in some of these economies are supporting those trade balances.

First among these has been India.

India has experienced a powerful demand recovery in recent months after a weak economic environment in 2019 and the effects of Covid-19 lockdowns.

PMIs have generally been printing above 55 and vehicle sales remain strong. The recovery began into the autumn festive season. Companies were unsure if it would last, but it has.

In particular companies are reporting strong demand and a reduced need to fund promotion and associated expenses to generate sales.

The recovery has been driven by:

- Urban demand — which slowed in 2019 and 2020, even for FMCG companies, but has

revived as Covid cases continue to fall - Premium segments as disposable incomes and consumer confidence improve

- Real estate — helped by lower mortgage rates and improved affordability.

Recoveries in Brazil, Mexico and South Africa have been more mixed. But some data points such as Brazilian bank-lending growth and South African retailer results show firm recoveries.

We particularly note the potential for these recoveries to continue for much longer than markets are pricing in. This suggests continued positive surprise in corporate results can drive equities and currencies higher for longer in these countries.

Where to take care

To be clear, we see these countries as the least understood and consequently most attractive part of Emerging Markets.

Yet with the exception of India we have been relatively cautious about adding exposure — even as these economies recover and portfolio capital that fled in the first half of 2020 returns.

Why?

There are two main reasons for short-term caution despite our longer-term optimism.

First, there are significant challenges from Covid second waves in some of our preferred markets.

Brazil has a major second wave underway. This is centred on the city of Manaus where a new variant is causing the majority of infections.

South Africa also had a second wave with a new variant at its heart, though case data there is now rapidly improving. Mexico’s second wave has been much more severe than its first — though again case data is now improving.

These second waves, and others, may lead to a short-term setback in economic recoveries and investor optimism.

Secondly, we are concerned about the potential for a short-term inflationary bulge as rising commodity prices meet the year-on-year effect of the March/April 2020 base.

The Brent oil price per barrel was US$17.30 at the end of March 2020, US$40 at the end of January 2021 and nearly US$60 at the time of writing. Soybeans (based on the Chicago bushel price) traded between US$6.50 and US$7 in the first few months of 2020, but are nearly US$14 at the time of writing.

The same pattern exists for diverse commodities — from wood pulp to copper, from wheat to ethylene.

In the higher beta emerging markets, stronger currencies have (and can continue to) offset the domestic inflationary effects. But we are concerned there is a risk of more challenging inflation prints in coming months.

We are particularly concerned about Brazil and Russia where inflationary pressures were starting to emerge before Covid hit. However differing reaction functions are more likely to see rate hikes and slower growth in Russia — and currency and bond market weakness in Brazil — should this occur.

Neither of these issues reduce our long-term enthusiasm for these markets.

India has been a powerful example of what a domestic demand recovery can mean for equity investors. Those same commodity prices are highly supportive of economic fundamentals and financial markets in more commodity-sensitive EMs such as Brazil, Mexico, South Africa and Russia.

We continue to look to increase our exposure to markets such as these. But we also look to be tactical in timing our portfolio shifts.

James Syme and Paul Wimborne are senior portfolio managers and co-managers of Pendal’s Global Emerging Markets Opportunities fund.

Find out more about the fund HERE.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Here’s what’s driving Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Find out about Pendal’s Australian shares funds here.

MARKETS were relatively quiet on the macro front last week. US bond yields rose a touch, while the USD weakened and commodities were higher.

We think these trends can continue, supported by the immense scale of US fiscal stimulus and its size relative to the output gap.

Australian equities underperformed last week, falling 0.46% (S&P/ASX 300) versus a 1.28% gain in the S&P500. This was likely a knee-jerk response to the Victorian lockdown.

So far reporting season has been reasonably constructive, though the market has been in a mood to punish disappointing results.

Covid and vaccine outlook

Recent trends continue. New daily cases continue to plummet from early-January highs in the US and UK. German cases are also trending down.

Hospitalisations are also falling away. The US hospitalisation rate has almost halved from its peak.

Vaccine roll-outs continue to progress in line with plans. The US has stepped up to a daily rate of 1.6 million vaccinations, consistent with herd immunity by July.

We are starting to see the impact of vaccinations on case numbers. For example in Israel overall new cases are dropping — but this is happening much faster in the over-60 age cohort. This is a key positive marker.

Northern hemisphere mobility data is a second area to watch. We’ll be looking for signs that warmer weather, looser restrictions and vaccine-induced confidence are encouraging people to venture out again. This should feed into economic activity and further bolster confidence.

At this stage there are only tentative signs of improvement in mobility data.

Economics and policy outlook

There’s an increasing probability that the US fiscal package will be close to US$1.9 trillion as the Democrats pursue the “reconciliation” approach to passing the package, reducing the need for Republican support.

Key Democrats seem determined to avoid the “mistakes” of the Obama administration — ie not stimulating enough in the wake of the GFC.

This determination is leading to vocal debate as to whether the package will create an inflationary impulse.

Former Obama adviser Larry Summers makes the point that the Obama stimulus was equivalent to half the output gap at the time. The proposed package is three times the current output gap.

A total of US$3.3 trillion in stimulus was passed last year. It’s thought US$1 trillion of that amount is still unspent.

Adding another $1.9 trillion suggests cumulative stimulus is 14% of GDP at a time when pent-up demand is being released.

There is noise that a follow-up infrastructure package later this year will be around $2 trillion — although this spending would be spread out over a longer period.

Finally, Fed Chair Jerome Powell continues to highlight the goal of getting the labour market tight enough to help the most marginalised workers.

Markets outlook

There are signs that point to another sell-off in bonds. Yields have been inching up, commodities have strengthened and the US dollar is weaker. Higher bond yields would continue to support cyclicals and financials in the equity market.

The S&P/ASX 300 fell 0.46% last week.

Resources bounced back as commodity prices recovered. Industrials were hit hardest due to stock specifics and the Victorian lockdown.

Results and company-specific news

Well-received

IAG (IAG, +8.1%). After some recent disappointing updates and a capital raise linked to further provisions, the market was relieved by a lack of news. The new CEO articulated some cautious targets and laid the groundwork for expectations that coming halves will not disappoint.

Macquarie Group’s (MQG, +7.3%) quarterly trading updated indicated an uplift on full-year guidance. The commodities business is benefiting from hedging activity related to rising prices and volatilities.

Gold miner Newcrest’s (NCM, +4.4%) result indicated a plan to drive higher-than-expected production from its Lihir mine in PNG, helping offset headwinds in other parts of NCM’s portfolio.

James Hardie’s (JHX, +3.6%) strong result reflected a combination of surging US housing demand, alongside gains in market share and good margin leverage. JHX outlined an aggressive plan to grow its presence in the “repair and remodel” market, which should help alleviate constraints from supply bottlenecks in new housing.

Telstra’s (TLS, +3.2%) actual result was mixed. Covid had a negative impact on revenue with the enterprise business continuing to suffer from the shift to NBN. But there was strong growth in mobile subscribers relative to competitors. The outlook was more positive. Management indicated the company was at a turning point. Underlying EBITDA is expected to grow in 2H FY21 and into FY22. There are two key drivers: lower costs and increased average revenue per user (ARPU) in mobile as better pricing comes through. Cash flow should be strong as capex falls. Management committed to the current dividend — implying a 4.9% yield — while potential asset sales could support future capital management.

Downer (DOW, -1.5%) delivered a decent result, in-line with expectations. Cash conversion was good, with signs of improving performance and higher prospects of capital management as the company divests some segments. The result emphasised Downer’s shift from an unpredictable, capital-intensive business to a capex-light urban services strategy with a more predictable workflow.

Telecom provider Megaport (MP1, +4.1%) was among the market’s strongest. A good reaction (despite pre-announced results) was driven by optimism on new product launches.

Mixed

Commonwealth Bank (CBA, -2.0%) delivered a pretty good result. Credit growth picked up and the capital position is very strong. It is looking like it has over-provisioned for bad and doubtful debts. But the market was disappointed as expected capital management was deferred. The company announced a further $300 million of investment in technology. CBA has outperformed peers over the past year, given the perception of relative safety. But other banks have greater leverage to rising bond yields.

Suncorp (SUN, +0.1%) sounded positive with some ambitious longer-term targets. Near-term guidance pointed to weaker underlying margins. There are questions about provisions for potential business interruption claims.

Gold miner Northern Star (NST, +1.6%) has now merged with Saracen. Both segments are delivering well operationally. The merged entity offers a good combination of underground and open-pit assets, good long-term projects and decent near-term cash flow.

The Transurban (TCL, -4.7%) result was a touch disappointing. Traffic to airports was a bigger headwind than expected. This issue is small in the scheme of things but however the Victorian lockdown looms as a bigger near-term issue.

Crown (CWN, -0.9%). The Bergin review was in line with our expectations. There is a path to open and run the Sydney casino. Crown will outline its response in April. The market is looking for changes in management and the board as part of this. The current CEO has announced his departure.

Poorly received

AMP (AMP, -16.2%) is facing headwinds on several fronts. Ares pulling out of a potential takeover was a further blow. The company is focusing on cost-out opportunities but the market’s attention is on short-term revenue trends.

Challenger (CGF, -12.9%) disappointed. The market was looking for higher margins, driven by a shift to more risk assets. Issues with capital intensity have precluded this for now.

Boral’s (BLD, -7.9%) Australian business is in worse shape than expected major projects ending and delays to new ones. Weather and a slower apartment market have dampened concrete demand and pricing. The US business overall was better but not enough to satisfy the market, particularly given a dusty outlook for fly ash.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds.

Crispin manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Water sanitation innovator Ecolab is featured in new report by responsible investing leader Regnan which outlines four areas of investment in sustainable agriculture.

ECOLAB’S mission is clearly spelled out on its website – it simply wants to make the world a better place.

The NYSE-listed company is a world leader in water sanitation and the prevention of food borne pathogens.

Ecolab is a vital link in the global food chain by helping prevent food loss to spoilage.

The business is featured by responsible investing leader Regnan in new report that outlines four areas for investment in sustainable agriculture (find the report here).

Food waste occurs at every stage across the food supply chain – from growing to packing, processing, distributing and retailing.

A key cause of food waste is food pathogens – microorganisms like viruses, yeasts and moulds that can spoil food, taint water systems and contaminate equipment.

Food waste is one of the most pressing problems humans face. Close to one third of all food produced each year is lost to waste.

Source: FAO 2011, Regnan 2020

The global economic, environmental and social cost of food wastage is estimated at an annual US$2.6 trillion, which is nearly equal to the GDP of France and about double the total annual food spending in the US.

In the US alone, it is estimated that a 20 per cent reduction in food waste over the next 10 years would avoid almost 18 million tonnes of greenhouse gas emissions annually – equivalent to removing about 4 million cars from the road.

“The way that we feed the world’s population is a key part of the solution for climate change,” says Mohsin Ahmad, Regnan fund manager and co-author of the report Catalysing Sustainable Agriculture and Food Production.

Prevention of pathogens across food system value chains also benefits human health. The US Center for Disease Control and Prevention estimates that each year there are some 48 million cases of foodborne illness.

Ecolab has a goal of helping its clients provide high-quality and safe food to 1.8 billion people by 2030 and to prevent 11 million foodborne illnesses.

Today, Ecolab’s food safety products are used in more than 36 per cent of the world’s packaged food and 44 per cent of the global milk supply.

Ecolab is a holding in the Regnan Global Equity Impact Solutions Fund.

You can find a copy of the Regnan Catalysing Sustainable Agriculture and Food Production here.

Who is Regnan?

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Recycling innovator Tomra is featured in new report by responsible investing leader Regnan which outlines four areas of investment in sustainable agriculture.

MOST people know Tomra from its reverse vending machines – those big metal kiosks that swallow your empty bottles and cans in exchange for a deposit refund.

The Oslo-listed company’s machines use sophisticated scanning technology to identify a bottle or can by its shape, material and barcode, sort it into the right recycling queue and provide an appropriate payout.

But that optical sorting technology has wider uses than recycling and it is now playing a key role in helping the agricultural industry manage food waste.

Tomra is featured by responsible investing leader Regnan in new report that outlines four areas for investment in sustainable agriculture.

Extraordinary challenge

Food waste is an extraordinary challenge for the planet.

Some 1.3 billion tons of food is lost annually, including 45 per cent of all fruit and vegetables, 30 per cent of cereals and 20 per cent of all meat.

This means every year we lose the equivalent of 3.7 trillion apples, 1 billion bags of potatoes – and 75 million cows.

The impact on the planet is immense. Not only does lost food not reach consumers, but the extra resources required to replace the food wasted puts pressure on everything from soil quality to the water system – even ultimately affecting climate change by lifting greenhouse gas emissions.

Waste occurs throughout the food production systems, from growers, through to processors, distributors and retailers.

Tomra’s sorting technology is being used by the food industry to inspect millions of pieces of produce with the aim of preventing food unnecessarily going to waste.

Tomra knows a bad apple

“The sensors are sophisticated enough to detect the sweetness of an apple,” says Mohsin Ahmad, Regnan fund manager and co-author of the report Catalysing Sustainable Agriculture and Food Production.

“They can detect the quality of the produce, if there’s any defect, the shape and size and so on.”

The key is that rather than disposing produce with visual defects that is otherwise sound, producers can divert the produce to an alternative purpose such as juice production.

“It’s really helping to reduce food waste,” says Ahmad, adding that Tomra sorting technologies are helping to divert 5-10 per cent of produce from going to waste.

Across its global customer applications, waste diverted is approximately equivalent to 25,000 trucks worth of potatoes per year.

Tomra is a holding in the Regnan Global Equity Impact Solutions Fund.

Find a copy of Regnan’s Catalysing Sustainable Agriculture and Food Production report here.

Who is Regnan?

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

The Regnan Global Equity Impact Solutions Fund invests in mission-driven companies we believe are well placed to solve the world’s biggest problems.

The Regnan Credit Impact Trust (available in Australia only) invests in cash, fixed and floating rate securities where the proceeds create positive environmental and social change.

Both funds are distributed by Pendal in Australia.

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Pendal Group Limited (ASX: PDL or Pendal) today announced the appointment of Mr Bertrand Lecourt and Mr Saurabh Sharma to establish a global equities sustainable water and waste investment strategy within the Regnan business.

Based in London, Mr Lecourt will join Regnan as Senior Fund Manager and Mr Sharma as Fund Manager.

It is expected the investment specialists will commence in April 2021, with the investment strategy to be launched in the UK and Europe in the second half of calendar 2021.

The team joins from Fidelity International where they manage the Luxembourg-domiciled US$2.4 billion Fidelity Funds Sustainable Water & Waste Fund.

The investment strategy will invest in companies involved in the design, manufacture or sale of products and services used in the water and waste management sectors.

Emilio Gonzalez, Group Chief Executive Officer of Pendal Group, said: “The appointment of Bertrand Lecourt and Saurabh Sharma demonstrates our ability to attract superior talent and progresses Regnan’s plans to become a global leader in providing environmental, social, and governance (ESG) investment strategies and solutions to clients.

“Regnan’s focus is on delivering innovative and specialist sustainable and impact investment solutions, drawing on over 20 years of experience at the frontier of responsible investment.

“The team’s appointment is the second investment team hire since Regnan expanded into investment management and follows the appointment of the Regnan Equity Impact Solutions team in December 2019, led by Tim Crockford, who joined from Federated Hermes.

“Clients are increasingly seeking out investment strategies that address environmental concerns in a sustainable way.

“The development of new technologies and proper water and waste management will be critical to manage the increasing demand for clean water and waste management as populations grow and become more urbanised.

“This will drive investment opportunities that Bertrand Lecourt and Saurabh Sharma will be able to capture through the unique combination of a diversified water and waste global equities portfolio with strong ESG credentials.”

Team biographies

Bertrand Lecourt, Senior Fund Manager

Bertrand Lecourt joined Fidelity International as a Portfolio Manager in 2018, where he launched and managed the Fidelity Funds Sustainable Water & Waste Fund.

Previously he was a Portfolio Manager at Polar Capital and the founder and CIO of Aquilys Investment Management. Prior to moving to the buy-side, Bertrand was Head of Equity Research, France at Deutsche Bank and a utilities analyst at Dresdner Kleinwort Benson and Goldman Sachs.

He holds an MSc in International Finance from HEC School of Management, France; an MSc in Money, Banking and Finance from Birmingham University, UK; and a DEA in Monetary Economics from Orleans University, France.

Saurabh Sharma, Fund Manager

Saurabh Sharma joined Fidelity in 2014 as a Product Specialist before becoming an Assistant Portfolio Manager in February 2020.

Previously, he held equity research analyst roles at Moody’s Analytics and GlobalData.

Saurabh has an MBA in Finance from IBS Hyderabad School in India and is a CAIA and ICFAI Charterholder.

Who is Regnan?

Regnan is a responsible investment business within Pendal Group with a vision to grow its funds under management and become a global leader in providing environmental, social, and governance (ESG) investment strategies and solutions to clients.

Regnan exists to drive positive impact and investment for a sustainable future and works towards this by developing and promoting more principled, rigorous and outcome-oriented approaches in responsible investment. It has a long and proud heritage in engagement and advice on ESG issues.

Regnan has produced pioneering research that has changed the way investors think about their wider responsibilities to society including advising influential organisations, such as the Principles for Responsible Investment (PRI).

Regnan can trace its roots back to a collaboration with Monash University, Melbourne in 1996, with an investigation into overlooked ESG-sources of risk and value for long-term shareholders in Australian publicly listed companies.

Regnan has since taken its ESG expertise globally. Its diverse experience in advocacy, regulation, academia and advising investment managers has enabled Regnan to offer ESG-related advisory, engagement and research services.

Visit Regnan.com

Find out about Regnan Global Equity Impact Solutions Fund

Find out about Regnan Credit Impact Trust

For more information on these and other responsible investing strategies, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.