Kaitlyn McRae found an affordable home through Argyle Housing which is partly funded via Regnan’s Credit Impact Trust. Pic: Argyle Housing

WHEN Kaitlyn McRae fell pregnant she didn’t think she could afford to raise her child in a nice house.

Then the 20-year-old came across Argyle Housing, which develops affordable housing for Australians on low-to-moderate incomes.

One of Australia’s most experienced Tier 1 Community Housing Providers, Argyle Housing in Kooringal is partly funded by investors in Regnan’s Credit Impact Trust.

“When I began searching for a place of my own to start my little family of two, I wasn’t sure what I was looking for until I came across a place in [western Sydney suburb] Glenfield, which was operated by Argyle Housing,” Kaitlyn says.

“It had already been leased — but they had this beautiful property in [Wagga Wagga suburb] Kooringal which was brand new.

“When I arrived, I thought to myself ‘wow’ I never would have thought moving out for the first time at the age of 20, that I would even have a chance to live somewhere as nice as this.

“Now I wake up every day loving where I live, how quiet the area is, having the perfect sized home for me and my bub who is due in January.”

Social bonds provide low-cost loans for community housing

Argyle Housing — which supports 4500 tenants in 2700 properties across NSW and the ACT — is partly funded by low-cost loans from the federal government’s affordable housing organisation, the National Housing Finance and Investment Corporation (NHFIC).

“Hearing the positive outcomes of housing young mums, makes me really proud of the work we have done in creating new affordable housing in Wagga Wagga with the support of NHFIC funding,” says Wendy Middleton, CEO of Argyle Housing.

NHFIC raises money (so far more than $1.2 billion) by issuing bonds to investors such as Regnan.

Regnan is a global fund manager specialising in investment strategies that seek attractive returns while also making a positive impact in the community.

Regnan’s Credit Impact Trust — distributed by Pendal in Australia — invests in a range of green and social bonds including those issued by NHFIC.

NHFIC offers community housing providers lower interest rates at better terms than banks, saving tens of millions of dollars — while providing attractive returns to investors.

“NHFIC is very important for financing, because it’s possibly as low a cost for borrowing you could ever achieve — and it’s performed very well,” says Wendy Hayhurst, chief executive of the Community Housing Industry Association.

“It’s performed very well because it’s got a government guarantee.”

Demand for NHFIC bonds looks set to grow because Australia will need up to a million community housing homes by 2036, Ms Hayhurst says.

To fund demand, the community housing sector will need to quadruple in size, she says.

Community Housing Providers are “the most cost-effective way of solving this problem because we don’t need 100 per cent subsidy,” she says. “We can go out and borrow to cover some of the costs of construction using NHFIC.”

That’s a win for community housing providers, Regnan investors and for Kaitlyn and her soon-to-be-born bub.

“I honestly couldn’t have asked for a more beautiful home or easy process to jump start my future,” she says.

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com.

Regnan thanks Argyle Housing for their co-operation in producing this article. Argyle Housing’s vision is to deliver quality housing options and connections to the community. Find out more about Argyle Housing here.

Nasima Khatun found a career thanks to low-cost loans provided via IFC social bonds. Picture: Gazi Nafis Ahmed/IFC

EIGHT years ago Nasima Khatun (pictured, above right) started work as casual labourer at Bangladesh food and beverage producer PRAN Group.

Today the 30-year-old mother of two is a full-time line supervisor in the tomato-processing division at PRAN’s plant in Natore, 250km north-west of Dhaka.

“Before working here, I did not know that women too could work and earn a living,” Nasima says. “I have now become smarter and have learnt a lot about women’s empowerment and about life.”

Now Nasima believes in her ability to work, earn a living and contribute significantly to her family’s well-being.

More women like Nasima are finding career paths with help from Regnan and Pendal investors.

Nasima’s job is partly funded by International Finance Corporation’s social bond program, which is supported by investors in Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund.

$US3 billion from social bonds for low-cost loans

The IFC — a triple-A rated bond issuer — has raised more than $US3 billion via 40 social bonds since 2017.

The funds are lent at low rates and on good terms to organisations that focus on under-served populations in emerging markets including women and low-income communities with limited access to essential services, basic infrastructure and finance.

IFC’s 2019 bond — which was supported by Regnan and Pendal — provided a $US15 million low-cost loan to Pran Group to create new jobs while investing in food lines that source from small farmers and micro businesses.

PRAN makes high-quality, low-cost, processed and packaged food readily available to lower and middle-income earners in Bangladesh and other countries.

IFC social bonds also put students into schools, supply technology and provide micro business loans and housing loans.

Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund invest in a range of social and green bonds that support projects which make a positive impact in communities — while also earning returns.

Regnan thanks the International Finance Corporation for their co-operation in producing this article. Find out more about the IFC’s social bond program.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information about Regnan Credit Impact Trust, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com or Regnan Chief Operating Officer Lisa Boyce at lisa.boyce@regnan.com.

About Pendal

Pendal is an independent, global investment management business focused on delivering superior returns for our clients through active management.

Pendal’s Bond, Income and Defensive Strategies team is one of the most experienced and well-regarded in Australia, managing some $22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Luna and mum Stacey found a place to live through Argyle Housing, which is partly funded by Pendal and Regnan investors. Pic: Argyle Housing

THE first years of little Luna’s life were spent “surfing” from one relative’s home to the next with mum Stacey.

“I haven’t had a home to call my own,” said single parent Stacey. “It was never easy, and I always felt like I wasn’t where I needed to be.

“Since falling pregnant and having to leave work early due to the pregnancy being at high risk, I returned home to Wagga, to raise my baby.

“Being a single parent is hard. Basically, surfing from house to house made things even harder.

“The pressure and the cost of living made me feel like it was impossible. So, when the opportunity was given to me to live in such a wonderful home at cost that I could actually manage I was over the moon.”

That opportunity came from Argyle Housing, a top Australian Tier 1 Community Housing Provider which develops affordable housing with help from investors in Regnan’s Credit Impact Trust and Pendal’s Sustainable Australian Fixed Interest Fund.

Community Housing Providers such as Argyle Housing develop and lease affordable housing to Australians on low incomes.

“Hearing the positive outcomes of housing young mums, makes me really proud of the work we have done in creating new affordable housing in Wagga Wagga with the support of NHFIC funding,” says Wendy Middleton, CEO of Argyle Housing.

Social bonds help Aussie on low incomes

Argyle Housing’s funding comes partly from the federal government’s National Housing Finance and Investment Corporation (NHFIC), which raises money by issuing bonds to investors such as Pendal and Regnan.

Regnan is a global fund manager offering investment strategies that aim for strong returns while also making a positive impact in the community. Regnan is part of ASX-listed investment manager Pendal Group.

Regnan’s Credit Impact Trust and Pendal’s Sustainable Australian Fixed Interest Fund invest in a range of green and social bonds including those issued by NHFIC.

NHFIC lends out the money raised (more than $2 billion so far) to housing providers at lower interest rates and on better terms than banks — while providing attractive returns to investors.

“NHFIC is very important for financing, because it’s possibly as low a cost for borrowing you could ever achieve — and it’s performed very well,” says Wendy Hayhurst, chief executive of the Community Housing Industry Association.

“It’s performed very well because it’s got a government guarantee.”

Social bonds in demand

Demand for NHFIC bonds looks set to grow because Australia will need up to a million community housing homes by 2036, Ms Hayhurst says.

As house prices rise across the country many more Australians like Stacey and Luna will need a hand.

“I’m ever so grateful for the opportunity,” says Stacey.

“I’m a single mum of a beautiful two-year-old girl, Luna. I’ve been given the opportunity to reside in one of the Argyle Housing affordable units in [Wagga Wagga suburb] Kooringal.

“To have such a beautiful place to call home I feel truly blessed.

“It really has felt that since moving in, my life with my daughter has truly begun. I want to say thank you to Argyle Housing for giving me the ability to turn my life around and to make a home for my daughter.

“Luna and I are extremely grateful.”

Regnan and Pendal thank Argyle Housing for their co-operation in producing this article. Argyle Housing’s vision is to deliver quality housing options and connections to the community. Find out more about Argyle Housing here.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information about Regnan Credit Impact Trust, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com or Regnan Chief Operating Officer Lisa Boyce at lisa.boyce@regnan.com.

About Pendal

Pendal is an independent, global investment management business focused on delivering superior returns for our clients through active management.

Pendal’s Bond, Income and Defensive Strategies team is one of the most experienced and well-regarded in Australia, managing some $22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Pendal and Regnan investors helped finance this solar farm in Nyngan, NSW. Pic: Getty

AUSTRALIA was once famous for “riding on the sheep’s back”. But some of the land trodden by woolly livestock now supports new, sustainable industries such as renewable energy.

A former sheep paddock near the central NSW town of Nyngan has been transformed into one of the Southern Hemisphere’s biggest solar farms.

AGL installed more than 1.3 million solar panels on the flat land here to create a 102-megawatt solar plant which became operational in 2015.

Ideally positioned to receive strong, constant solar radiation, the Nyngan Solar Farm is expected to generate about 230,000 megawatt hours (MWh) of renewable electricity each year — enough to power some 43,000 average Australian households.

The plant is partly financed by investors in Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund.

Attractive returns and positive impact

Regnan is a global fund manager offering investment strategies that aim for strong returns while also making a positive impact in the community. Regnan is part of ASX-listed investment manager Pendal Group.

Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund invest in a range of green and social bonds including Westpac’s Climate Bonds. These bonds help finance clean energy projects — including AGL’s Nyngan solar plant — at low rates and on good terms.

The result is “pretty amazing” says Richard Armstrong, AGL’s Asset Leader NSW and Queensland for Wind and Solar.

“It’s a very reliable asset,” Mr Armstrong says. “It hasn’t skipped a beat since it was first built.

“We’ve actually got a viewing platform which gives you a good view over the 1.3 million panels. You can’t really see the end of it once you’re standing on the platform. It looks like an ocean — all those solar panels.

“I think for the town of Nyngan it’s a really positive investment and a positive project. We do a fair bit with the community.”

Climate bonds that support clean energy

Solar power is booming in Australia. When it was built, the AGL-operated Nyngan plant was the biggest solar farm in the Southern Hemisphere.

But there are now some eight or nine bigger solar farms in the Southern Hemisphere that have been completed, commissioned or are under construction, Mr Armstrong says.

Every hour the sun delivers more power to the Earth than the entire world consumes in a year. Unlike fossil fuels it’s an unlimited source of clean energy.

“Australia’s got some unique challenges in terms of our size and moving electricity from the outback to the population centres, but the resource the sun provides is certainly abundant,” Mr Armstrong says.

By investing in such renewable energy projects such as Nyngan Solar Farm, climate bonds do more than generate millions of megawatt hours of clean energy. They aid the global effort towards a zero net emission outcome by 2050.

Besides the Nyngan solar plant, Regnan Credit Impact Trust and Pendal Sustainable Australian Fixed Interest Fund help finance a variety of projects that make a positive impact in the community while generating attractive returns.

These include sustainable projects (such as wind farms, green buildings, low-carbon transport and clean water solutions) and social bonds that lend money on good terms to community housing providers, schools and micro-businesses.

About Regnan

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information about Regnan Credit Impact Trust, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com or Regnan Chief Operating Officer Lisa Boyce at lisa.boyce@regnan.com.

About Pendal

Pendal is an independent, global investment management business focused on delivering superior returns for our clients through active management.

Pendal’s Bond, Income and Defensive Strategies team is one of the most experienced and well-regarded in Australia, managing some $22 billion invested across income, composite, pure alpha, global and Australian government strategies.

Here’s what’s influencing Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

NOVEMBER was heading for the best monthly return for the S&P/ASX 300 since 1988 despite a quieter period last week.

The index lifted 0.98% to take the month’s gains to 11.58% by the end of Friday.

Equity markets look a bit extended in the near term. A period of consolidation is possible. But we remain positive given the combination of stimulus, negative real rates, vaccine roll-out, growth momentum and earnings upgrades.

US Covid cases remain a risk. But European restrictions are taking swift effect with far less economic impact than before.

With vaccines on the horizon, the market seems to be looking through near-term Covid risks to focus on a more positive 2021.

Health outlook

New daily cases in the US fell last week though this is distorted by delays in reporting in some States due to Thanksgiving.

The next couple of weeks remain important with concerns that cold weather and more travel could see an acceleration in case trends.

Hospitalisation data is not great — new admissions remain high. But it is not as bad as many feared and most States have spare capacity.

European trends continue to improve. New daily cases in France have plummeted as lockdowns take effect.

Importantly there has been a lower economic cost than last time. Toll road traffic troughed with an 80% fall in the first lockdowns. This time it was down 40% and is already showing signs of improvement.

French hospitalisations appear to have peaked for this wave and are broadly the same as the first wave despite many more infections.

On the vaccine front questions emerged over the quality of the most recent AstraZeneca trials. They appeared to be small in sample size with a skew in age profile.

This may lead to a delay in approval as further data from different trial groups is collected.

This is a material issue for vaccination plans in countries outside the US. The US plan is skewed towards Pfizer and Moderna. In places such as the EU, UK and Australia the AstraZeneca vaccine plays a bigger role. In Australia this means far more significance on the Novavax trials.

This could see a vaccination program rolled out faster in the US than in other parts of the world, with implications for relative rates of economic growth.

Economic outlook

Data points are emphasising a paradox in the US economy. On one hand consumer sentiment remains soft. Real-time economic indicators have stalled or even show signs of deterioration.

On the other hand, GDP indicators continue to accelerate.

The gap is partly explained by inventory rebuild and net export growth.

Industrial production remain strong as a result. The housing market also remain strong, which is flowing through to other parts of the economy.

Corporate profits have rebounded faster than many expected, which is feeding through to capex and jobs.

One of the key swing factors for the economy is the savings rate. After peaking at about 34% of household income earlier in the year it fell to 13.6% in October.

If this returned to a normalised level of about 8% it would add a further 4% to 2021 GDP. This potential pent-up demand could be released as a vaccine rolls out.

Liquidity and monetary stimulus remain supportive. Combined money supply across the US, EU and China was up 18% year-on-year in October.

It is worth noting that forward indicators such as credit spreads continue to trend down, also supporting markets.

Market outlook

Confidence in the economic recovery continues to drive commodity price gains. Copper was up 3.2% last week and is up 11.7% for the month — well above pre-Covid levels.

Brent Crude gained 7.2% and is up 28.6% for the month. At US$48.18 a barrel it is nearing the major technical resistance point of US$50.

Demand remains a key difference between copper and oil. A lack of air travel continues to weigh on the latter.

We would not be surprised to see a near-term pull-back in oil. But once air travel recovers we could see it returning to the US$60 range next year.

Bond yields are holding recent levels despite good news on vaccine and economic growth and the improvement in sentiment suggested by commodity prices.

There is a suggestion yields are being supported by a view that less need for stimulus means less bond issuance and debt.

Gold continues to sell off as the need for safe haven reduces for now.

There is much debate about where the US dollar goes as the US dollar index (DXY) continues to trend down.

Bears point to a weaker dollar given the surge in Covid alongside twin deficits. We are not as negative, given better-than-expected economic performance.

While the USD is unlikely to retrace recent falls in the near term, we think it may hold up better than many are predicting. Either way a weaker USD is helpful for markets.

An 11% gain in the S&P/ASX 300 month-to-date leaves the market looking a little over-bought on technical factors.

Some near-term consolidation would be unsurprising. But the market’s recent breadth has been encouraging with both growth names and cyclical stocks making gains.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds.

He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Regnan’s head of impact investment Tim Crockford interviewed by Investment Magazine (Nov 2020).

IMPACT investing — which aims to generate a financial return and a positive impact on society — is a fast-growing market.

The value of Australian impact investment products is expected to grow to $100 billion in the next five years — up from $20 billion in 2019, according to the Responsible Investment Association Australasia.

Impact investment manager Regnan — distributed in Australia by Pendal — is about to launch its Global Equity Impact Solutions fund.

Here is the fund’s portfolio manager Tim Crockford making his first Australian appearance live from London at Investment Magazine’s Fiduciary Investors Symposium on November 18, 2020.

Regnan is a responsible investment leader with a long and proud history of providing insight and advice to investors with an interest in long-term, broad-based or values-aligned performance.

Building on that expertise, in 2019 Regnan expanded into responsible investment funds management, backed by the considerable resources of Pendal Group.

For more information, please contact Head of Regnan and Responsible Investment Distribution Jeremy Dean at jeremy.dean@regnan.com or Regnan Chief Operating Officer Lisa Boyce at lisa_boyce@regnan.com.

Pendal Active High Growth Fund (APIR: BTA0488AU, ARSN 610 997 674)

Effective 25 November 2020, the buy-sell spread for Pendal Active High Growth Fund will increase as set out in the table below:

|

|

Old (%) |

New (%) |

|

Pendal Active High Growth Fund |

0.34 (0.17/0.17) |

0.38 (0.19/0.19) |

The buy-sell spread is an additional cost to you and is generally incurred whenever you invest in or withdraw from a Fund. The buy-sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy-sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy-sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Funds.

Pendal will continue to monitor market conditions and review and update the buy-sell spread regularly as required. You should therefore review the current buy-sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy-sell spread for each Fund.

Pendal’s head of equities Crispin Murray explains his vision for our newly renamed Pendal Horizon Fund (formerly known as Pendal Ethical Share Fund).

The year 2020 demonstrated some fundamental truths about the modern investment environment.

The world is vulnerable to shocks — from climate change to pandemics. Change is accelerating. Successful companies must confidently manage a wider set of risks than in the past, including environmental, social and governance (ESG) risks.

What are the implications for investors? What have we learned and how is Pendal responding?

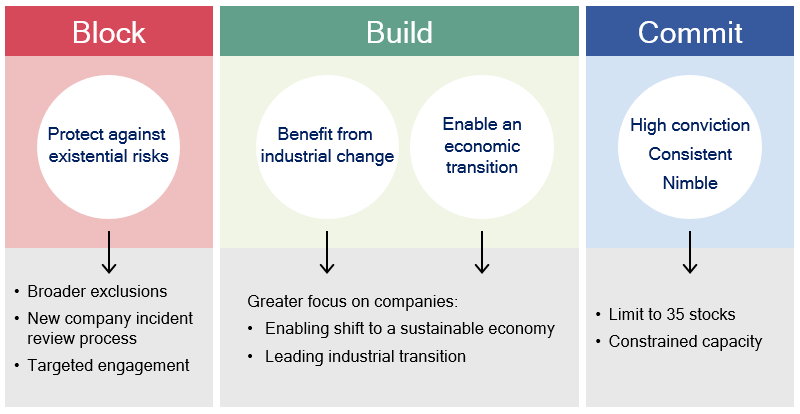

We believe investors need:

• Strategies that can protect against unpredictable outcomes.

• Investments that benefit from and are leveraged to structural changes.

• Investments that can enable and facilitate positive change while avoiding harm.

• A high-conviction, all-weather, nimble portfolio.

Our approach to sustainable investing is grounded in these beliefs.

Block, build, commit … the foundations of Pendal’s Horizon Fund

Now we have taken the Pendal Ethical Share Fund, with its 19-year history, and re-engineered it for the next two decades as Pendal Horizon Fund.

This enhanced strategy is:

• Built for performance. It’s a concentrated, high-conviction strategy of 15 to 35 stocks that draws on the company insights and risk management underpinning Pendal’s long and strong track record in performance

• Actively invests in companies that enable a more sustainable and “future-proof” Australian economy. This allows the fund to benefit from trends shaping coming decades, from digitalisation to decarbonisation. We allocate capital to companies that directly contribute — or enable others to contribute — to areas such as:

Pendal’s Horizon Fund directs capital into these areas

• Avoids activities that undermine a more sustainable economy (see graph below). We screen out harmful industries such as fossil fuels, alcohol, gaming, tobacco, weapons, logging, predatory lending and companies that breach standards:

Pendal’s enhanced Horizon Fund operates exclusionary screens in these areas

• Uses Pendal’s deep responsible investment capabilities. This includes the advice of Regnan — our wholly-owned subsidiary — in assessing companies on their contribution to a sustainable, future-oriented Australian economy and their management of ESG risks.

• Prioritises active stewardship and engagement with companies to promote sustainable characteristics and minimise ESG risks. This leverages Pendal’s depth of corporate access and scale of funds under management, allowing us to be an effective agent of change.

The outcome is a fund that is built for performance while also acting as a force for positive change in Australia’s future. The fund is aligned with developing trends while benefiting from Pendal’s proven capability.

Click here for more information about the Pendal Horizon Fund (formerly Pendal Ethical Share Fund).

Contact Us

For more information, please contact Pendal’s Head of Responsible Investment Distribution Jeremy Dean at Jeremy.Dean@pendalgroup.com.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Here’s what’s influencing Australian equities this week according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

MARKETS were mixed last week. On one hand there were fears the US Covid-19 surge could prompt restrictions that weigh on growth. On the other, we saw further positive vaccine developments.

The S&P 500 fell 0.73%, but Australian equities rose 2.11% (S&P/ASX 300) as the virus remained under control domestically.

The risk to growth from the current US Covid wave must be watched. However we still see plenty to support equity markets through to the end of the year, including policy stimulus, economic resilience, strong liquidity and the prospect of good corporate earnings growth as previous weakness is cycled.

Vaccine news

There was positive news on the vaccine front last week, with Moderna’s interim results showing 94%+ effectiveness. Pfizer also updated their results to show a similar outcome.

This is good news for the economy and markets.

From here, several factors need consideration:

• Side effects: Initial data looks reassuring on this front, particularly for Pfizer. A small subset of trial patients report some minor irritation, but at this point there seems nothing too serious.

• Impact on older patients: Data indicates that older cohorts are so far responding well to vaccines.

• Durability: This is still to be determined. Time will tell, but indications on immunity thresholds suggest it should work for at least a year.

• Manufacturing and distribution: The combined expectation is that Moderna and Pfizer will have 70 million doses available by the year, which can be used on 35 million people (each vaccination requires two doses). About 70% of these doses are expected to be used in the US. The area to watch is the production ramp-up. Moderna are saying they will ramp from 7 million doses per month now to between 50 million and 80 million by mid-2021. This means widespread vaccination will be possible by the June quarter.

• Take-up of vaccine: Surveys indicate the high vaccine efficacy rate is increasing the propensity for people to take it.

• Virus changes: The potential for new strains of Covid – and the impact on vaccines – remains a key unknown.

The next expected developments include emergency approval for Pfizer’s vaccine – anticipated by end of the year. AstraZeneca’s interim results are also expected in the next two to three weeks.

Covid outlook

The focus is on how things play out in the US. Rolling average daily new cases continue to climb, but at a declining rate — up 25% week-on-week versus 40% the previous week.

However bottlenecks are emerging in testing capacity, which is reflected in case numbers and in a continued increase in the proportion of positive test results.

US hospitalisations increased 20% week-on-week — a marginally slower rate than the previous week. Patients remain spread out geographically and we are still seeing spare capacity in the system.

The next two weeks will be critical. Some modellers are predicting an acceleration in cases and hospitalisations, partly due to the Thanksgiving holiday.

Case trends continue to improve in Europe. At this point Europe seems to have avoided a crisis in the hospital system. France appears to be turning around, which supports the case that better treatments and protocols are helping manage the scale of the crisis.

Policy outlook

The Trump administration’s treasury secretary last week declined to approve beyond January 1 the facilities that have been the back stop of credit markets.

This means the Fed will no longer be able to buy corporate credit, provide main street loans or municipal loans. The Treasury is also asking for the return of unused capital.

Originally the Cares Act pledged $454 billion to the Fed, which could be leveraged up. To date they have received about $100 billion.

While the extension can be re-approved under Biden’s administration, the bigger issue is that the returned funds would not be immediately available. They would remain locked up until Congress authorised them.

The Fed has some access to other funding sources via the Exchange Stabilisation Fund. But this is in the region of $70 billion – far less than the existing package.

While markets continue to function normally this should not present a major issue. But it adds to the downside risk of negative events emerging. It is also likely to encourage the Fed to do more Quantitative Easing.

Another negative on the horizon is a further step down in fiscal support as jobless benefits expire for another 7 million to 12 million workers. This equates to $35 billion to $70 billion less fiscal stimulus in the first half of 2021.

The last step down was relatively benign, as households drew on elevated savings rates to smooth the effect. Any fiscal deal may also restore some version of these payments. However this risk needs to be watched in the near term.

Economy outlook

Rising cases and shifting behaviour are having some effect on US economic indicators. But activity is so far proving more resilient than many had feared.

The Atlanta Fed’s GDPNow real GDP estimate is improving. It’s most recent prediction is 5.6% GDP growth in Q4 – well above consensus – driven by strength in housing, retail sales and industrial production.

Elsewhere, the weekly US Consumer Comfort index rose to a new post-pandemic high, probably helped by the election and vaccine news.

Existing house prices rose 15% in October, implying a US$10 trillion gain in consumer net worth. In combination with increasing money supply (still up 25% year-on-year), tight credit spreads, stronger copper prices and the scope for better corporate earnings, it suggest that while sentiment is nervous, there are plenty of supportive factors at play in markets and the economy.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. Crispin manages a number of our flagship funds and leads one of Australia’s biggest equities teams.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

Looking at tech stocks in emerging markets? Take care to consider investments with a catalyst to unlock a company’s potential and share price. Global Emerging Markets Opportunities portfolio managers James Syme and Paul Wimborne (pictured above) explain

TECHNOLOGY companies generally face an extremely supportive operating environment at present.

Covid-19 has hugely accelerated online migration. Along with the rise in artificial intelligence and machine learning this requires massive investment in new hardware.

Pendal’s Global Emerging Markets Opportunities portfolio has significant exposure to companies that are benefiting from these trends.

But we retain a preference for investments that also have a catalyst to unlock the company’s potential and its share price. This includes some of the largest holdings in the fund.

Naspers, Prosus & Tencent: Twin discounts

One of our largest aggregate portfolio positions is in the related companies of Naspers (a South African holding company), its subsidiary Prosus (a Dutch media conglomerate focused on the internet in emerging markets), and Prosus’s biggest investment, Tencent (a Chinese internet giant).

One of the oddities about the listings of these three is that Naspers trades at a discount to the market value of its shares in Prosus; and Prosus trades at a discount to the market value of its stake in Tencent (let alone the value of Tencent and Prosus’s other listed and unlisted investments).

Naspers has a market capitalisation of US$85 billion (all data as at October 31, 2020 unless otherwise indicated). Almost all of the Naspers balance sheet consists of its 72.5% stake in Prosus. Prosus has a market capitalisation of US$162.7 billion, making that 72.5% stake worth US$117.9 billion.

There are various explanations — mostly around the gap in liquidity, index membership and investor market access between South Africa and the Netherlands.

Sitting behind that valuation anomaly is another, more complicated and potentially larger one.

Prosus owns 28% of listed Russian internet company Mail.ru, 22% of German-listed food delivery company Delivery Hero and 6% of US-listed Chinese online travel retailer Ctrip. These three holdings are worth US$7.7 billion.

Crucially, it also owns 30.9% of Chinese social media and gaming behemoth Tencent. That stake has a market value of US$225.8 billion.

A long tail of unlisted emerging market online companies in classifieds, food delivery, payments, travel, education, and social media has a value (while harder to assess) conservatively estimated at more than US$20 billion.

At its December 2019 capital markets day, Prosus management indicated a desire to create at least US$100 billion in shareholder value over the medium term.

As a step towards achieving that, in October 2020 Prosus announced a US$5 billion buyback, consisting of US$1.37 billion in Prosus shares and US$3.63 billion in Naspers shares. This sits alongside a commitment to increase Prosus’s free float by reducing the Naspers stake to below 70%.

The really big step, however, would be Prosus selling some of its stake in Tencent to do further buybacks.

There are no immediate indications that this is about to happen, but it should be noted that the last such sale (in March 2018) followed a very strong share price run in Tencent, as we have seen year-to-date.

Through these twin discounts in the group’s market capitalisations, there exists very substantial potential for gains to shareholders from proactive steps to buy back shares. We have seen a concrete step towards this in October and expect further steps in current months.

Samsung: Reform in the chaebol sector

Another one of the portfolio’s largest positions is Samsung Electronics (SEC) in South Korea. SEC is a multi-faceted conglomerate operating across various consumer electronics and IT products.

Using its last four quarterly results as a guide, the biggest division by revenue is IT & Mobile, which produced US$9.7 billion in operating profits on US$85.4 billion in revenue with a margin of 11.4%.

The next biggest (but most profitable) division is semiconductor products, which produced US$15.4 billion in operating profits on US$59.8 billion in revenues with a margin of 25.8%. There are also smaller units producing display products and consumer electronics which together produced US$4 billion in operating profits.

This operational profit translated into US$21.3 billion of free cash flow for the period.

SEC has a market capitalisation of US$297.8 billion. But crucially, its balance sheet is extremely cash-heavy.

At the end of September SEC had US$105.2 billion in cash and only US$17.5 billion debt. The company has tended to grow organically, and does not use its cash for acquisitions, making this essentially surplus cash able to be returned to shareholders.

Since 2015 SEC has had a far more positive approach to dividends and share buy-backs, currently operating a shareholder return policy of paying out KRW 9.6 trillion (US$8.7 billion) in dividends each year.

It is seeking to return a minimum of half of free cash flow over the three-year period 2018-2020 through dividends or share buy-backs.

The company was due to announce an update to this policy in the fourth quarter of 2020. However, Samsung group chairman KH Lee passed away on October 25, having been unwell since a heart attack in 2014.

Mr Lee had led the Samsung Group since 1987 following the death of his father, Samsung founder BC Lee. He had transformed Samsung into a world-leader in multiple sectors, with SEC at the heart of the group.

Mr Lee’s son JY Lee has been acting chairman of SEC since 2014 and drive the change in shareholder return policy.

JY Lee is set to inherit stakes of major Samsung group companies, including SEC, and we expect SEC to continue to improve its shareholder return policy.

The Lee family’s control over SEC may decline as it sells down stakes in related group companies to meet inheritance tax obligations, while the Moon government’s pressure on chaebol holding structures continues to increase.

(Chaebol refers to a business conglomerate structure that originated in South Korea in the 1960s, creating global multinationals with big international operations. The Korean word chaebol means business family or monopoly.)

This is likely to increase the role of minority shareholders in major decisions at SEC, which should drive an improving shareholder return policy at SEC. As a result, the announcement of the new shareholder return policy has been moved to late January.

This will be a key moment for SEC.

The buy-back program has been on hold since mid-2018 because a capital expenditure bulge meant the KRW 9.6 trillion dividend payment commitment met the free cash flow return commitment.

However the last four quarters have seen free cashflow run at an annualised level of around KRW 25.6 trillion (US$21.6 billion).

This suggests that either the commitment to pay dividends increases, or the buy-back program resumes.

In conclusion, we certainly find many opportunities in the broader technology space, but prefer to focus our larger positions on those with strong operating momentum and an additional potential driver of returns from restructuring and the unlocking of value.

We are particularly excited about potential newsflow for these holdings in the next few months.

James Syme and Paul Wimborne are senior fund managers and co-managers of Pendal’s Global Emerging Markets Opportunities fund.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/