Changes to the Pendal Ethical Share Fund (APIR: RFA0025AU, ARSN 096 328 219)

The Fund’s investment strategy, including how we take labour standards and environmental, social and ethical considerations into account when selecting, retaining or realising investments of the Fund, will be changing from 12 October 2020.

Investment strategy

From 12 October 2020, the Fund will be a high conviction, values-oriented, concentrated portfolio of typically 15-35 stocks that invests in businesses that in our view, in aggregate, provide a net benefit to Australia’s future economy and society.

Pendal will adopt a principles-based approach in identifying the Fund’s investments which aims to:

• Avoid companies whose industries, business models and products or services are not sustainable or cause significant harm, having regard to what we believe most investors would want to avoid in a values-based investment portfolio.

• Invest in companies that demonstrate, or offer or enable more sustainable practices, business models or products and services.

• Invest in companies that advance or participate in the transition of the Australian economy to one that is more sustainable.

• Engage with management of companies in which we invest to manage risk, effect change and realise potential value over the long term.

From 12 October 2020, the following exclusionary criteria will apply to the Fund.

|

In managing the Fund, we avoid investing in companies which: |

|

|

Fossil Fuels |

· directly undertake fossil fuel exploration or extraction (specifically, coal, oil and gas); or · earn more than 10% of their revenue from fossil fuel-based power generation, or from fossil fuel refinement or distribution (coal, oil and gas); or · earn more than 10% of their revenue from the provision of supplies or services which relate specifically to the fossil fuel exploration or production industries (coal, oil and gas) |

|

Uranium |

· directly undertake uranium mining for weapons or power generation; or · earn more than 10% of their revenue from nuclear energy-based power generation |

|

Logging |

· earn more than 10% of their revenue from unsustainable forestry or forest products, including non-Forest Stewardship Council certified forest products or non-Roundtable on Sustainable Palm Oil certified palm oil production |

|

Gambling |

· directly manufacture, own or operate gambling facilities, gaming services or other forms of wagering; or · earn more than 10% of their revenue from the indirect provision of gambling (for example, through telecommunications platforms) |

|

Pornography |

· produce pornography; or · earn more than 10% of their revenue from the distribution or retailing of pornography |

|

Weapons |

· produce or distribute controversial weapons (such as cluster munitions, landmines, biological and chemical weapons), or supply goods or services specifically relating to controversial weapons; or · produce or distribute non-controversial weapons or military equipment; or · produce or distribute civilian firearms, or supply goods or services specifically related to firearms, or to firearm manufacturers |

|

Alcohol |

· produce alcoholic beverages; or · earn more than 10% of their revenue from the distribution or retailing of alcoholic beverages |

|

Tobacco |

· produce tobacco (including e-cigarettes and inhalers); or · earn more than 10% of their revenue from the distribution of tobacco (including e-cigarettes and inhalers) or supply of goods or services specifically related to the tobacco industry (for example, packaging or promotion) |

|

Animal Testing |

· directly undertake animal testing for cosmetic products |

|

Predatory Lending Practices |

· directly provide products or services with lending practices that are unfair or deceptive to ordinary borrowers, including small amount short term loans at higher than commercial rates of interest (for example, payday loans, pawn loans or the use of aggressive sales tactics) |

|

Breaches/ misconduct |

· we consider to have been found to have significant breaches of social or environmental norms or regulations, or are subject to serious and substantiated allegations of unethical conduct, which we consider have not been remedied or adequately addressed. |

Why are we making the changes?

We believe it is in the best interests of investors for the new and tighter exclusionary criteria to be implemented for the Fund. These screens are expected to better meet investors’ expectations regarding the holdings of an ethical fund, which have evolved considerably since the Fund was launched in 2001.

Most notably, investors in ethical funds have increasingly sought to avoid allocating capital to companies whose activities significantly contribute to climate change. For this reason, we will be introducing fossil fuel-related screens in the Fund.

The investment team will be applying a framework that places a greater focus on stocks and industries that meet our investment criteria, responsible investment priorities and philosophy, resulting in a high conviction, values-oriented, concentrated portfolio that is expected to deliver better risk-adjusted returns for investors in the Fund.

Transition into the new investment strategy

The changes will require a number of stocks in the Fund to be sold from 12 October 2020, as these stocks do not meet the new exclusionary criteria. These stocks are relatively liquid and we expect to be able to complete the sell down within one day under normal market conditions.

Management fee

There is no change to the management fee of the Fund which will remain at an issuer fee of 0.95% p.a.

About the Fund’s Portfolio Manager

The Fund will continue to be managed by Crispin Murray, Head of Equities.

Crispin was appointed as Head of Equities in 2003 and is responsible for overseeing Pendal’s Australian Equities business and currently manages A$15 billion of funds under management.

In managing the Fund, he will be supported by the Pendal Australian Equities Team, a team of 19, one of the largest fundamental Australian Equities Team in the market.

Here’s what’s impacting Aussie stocks at the moment, according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Strong US jobs data last week suggests the reduction in fiscal stimulus is not yet biting.

The Victorian lockdown continues to drag on Australia’s national economic pulse. As a result Australia is a negative outlier in global industrial surveys.

There was a sharp sell-off in growth stocks late last week, which dragged on markets as a whole.

Key near-term factors

- US cases: New case numbers are plateauing; it’s important to watch for a pick up as students return to school

- Australian cases: Trends continue — numbers falling in Victoria, steady in NSW.

- Vaccine/therapeutics: No new material news.

- US economy/policy: Stronger data – no signs of lower unemployment insurance payments stalling rebound. Policy impasse remains.

- Australia economy/policy: Rising expectations for tax cuts in upcoming budget

Australian outlook

Victoria’s seven-day moving average of new cases continues to trend lower, dipping back below 100. Having crept back up a few weeks ago, NSW remains steady at around 10 new cases a day.

Victoria’s decision to pursue an effective elimination strategy is material. It means stricter restrictions for longer, with a greater impact on activity, the economy and budget deficits.

The number of people dining out demonstrates the impact of Victoria’s lock-down on the national economy. In NSW restaurant-going has returned to pre-Covid levels, while Queenslanders are eating out more than they were in January.

However at a national level dining out remains 20-30% below pre-Covid levels, due to the drag from Victoria. This remains a headwind for the domestic equity market and specific companies.

US outlook

The rapid spread of Covid-19 among students returning to university has seen new daily cases in the US plateau at around 40,000 – after falling from a mid-July high of about 60,000. Hospitalisations continue to fall. But this may change given the lagging effect with new cases. Mortality rates continue to fall.

The main news out of the US was last week’s strong jobs data. The payroll data was reasonable – probably a little better than expected. But the household survey of employment was very strong, suggesting unemployment fell 2% over the month to about 8% – half its pandemic high-point. The hours-worked survey confirmed the same trend.

Margins of error are likely to be larger than normal. But the change is beyond anything that could be explained by such margins – and paints a picture of a strong V-shaped economic recovery.

The easier gains are likely to have been made and it may get harder to maintain momentum from here. But this helps explain why markets have been as strong as they have. The rebound has simply been much better than many feared. It also confirms falling government payments are not crimping the rebound.

Global GDP growth forecasts have progressively improved as analysts become less pessimistic. There’s been a sharp pick-up in expected growth rates for Q3 2020 since mid August.

This is supported by underlying activity in key sectors such as autos, where US production is now running above pre-Covid levels. The rebound in China and Japan is also strong. This has been driven by income support and pent-up demand helped by an aversion to public transport. Other sectors are languishing, however this demonstrates the speed with which key parts of the global economy are rebounding.

Most industrial surveys in key economies around the world are in expanding territory and improving. Australia is an outlier in this regard. The drag from Victoria has prompted deteriorating industrial surveys and a more neutral outlook for the economy. The effective elimination strategy is likely to see this drag continue for a while longer.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

There are some interesting differences among major Latin American countries that are important for emerging markets investors right now. Here senior portfolios managers James Syme and Paul Wimborne take a closer look, explaining which countries they favour and why.

WE believe growth metrics and policies designed to support growth are the key data points to track for markets — with stimulative monetary policies and attractive valuations present almost everywhere in the emerging world.

But we note some interesting differences in inflation dynamics among major Latin American countries.

Brazilian consumer price inflation, which ended 2019 at a 4.3% year-on-year increase, fell to a 20-year low of 1.9% in May 2020, recovering slightly to 2.1% in June.

Mexican consumer price inflation, which ended 2019 at 2.8%, rose to 3.3% by June.

Clearly there are some very different dynamics at play here. Why, and what does it mean for investors?

Firstly, both countries have had difficult coronavirus crises.

Brazil was third and Mexico sixth in total new cases for the two weeks to August 3, according to European Centre for Disease Prevention and Control figures. (USA and India were one and two. South Africa and Colombia were four and five).

Both countries have experienced very significant disruption to economic activity.

In Brazil, industrial production and retail sales to May were -21.9% and -7.2% respectively. In Mexico those figures were -30.7% and -23.7%.

Historically for both countries, the imported component of inflation has been volatile, driven at times by exchange rate volatility. The Brazilian real fell 28.1% against the US dollar in the first seven months of 2020. The Mexican peso fell 16.4%.

A closer look

With a deeper slowdown in Mexico (which should have eased demand pressure on prices), and a smaller fall in the currency, why has Mexican inflation proved so sticky?

A deeper look into the Mexican data shows a very stable core CPI rate (year-to-date the range has been 3.6%-3.7%, with declines in housing, non-food merchandise and services offset by significant price pressure in food merchandise).

The food, beverages and tobacco price index rose 6.6% in the year to June, which the central bank attributes to a reallocation of household spending and to disruptions in the supply of certain goods.

Spikes in food prices (up and down) are common in emerging markets. But they are typically short-lived as supply and demand adjust quite quickly.

The expectation of the Mexican central bank — and of many observers — is that policy interest rates could be cut in the second half of 2020.

The deputy governor of the central bank said recently: “In my personal opinion the cycle hasn’t ended [and] we’ll look to take our monetary stance to an expansive level in accordance with the current economic situation”.

The central bank has cut rates from 7.25% at the start of the year to 5% at the last meeting. Under consensus expectations the rate will fall to 4.2% by the end of the year.

By comparison, Brazilian interest rate cuts may have been front-loaded this year, with a decline from 4.5% to 2.25% so far. Any additional rate cuts would be “small”, the central bank’s monetary policy committee said in the minutes of its last meeting.

Reflecting Brazil’s extremely weak fiscal position, the minutes described current monetary policy as “close to the level from which further interest rate reductions could be accompanied by asset price instability”.

There are a number of reasons why we (cautiously) prefer Mexico to Brazil at this time, including Brazil’s difficult coronavirus statistics and extended fiscal deficit.

The outlook for monetary policy in the second half is another reason.

James Syme and Paul Wimborne are senior fund managers and co-managers of Pendal’s Global Emerging Markets Opportunities fund.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Here’s what’s impacting Aussie stocks at the moment, according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

The S&P/ASX 300 gained 1.3% last week, driven largely by resources (+4.9%) while uncertainty over the impact of the Victorian lockdown weighed on the banks (-1.3%). The key near-term factors were on balance neutral to slightly positive, which helped support the broader market: Key short term issues

- US Covid trends: Continue to improve, with falling hospitalisations.

- US earnings season: Continues to surprise on the upside, albeit off a very low base of expectations.

- Vaccine & other therapeutics: Novavax trial reports positive, raising possibility of an alternative vaccine platform.

- US policy: A continued stalemate on fiscal package. Progress is expected this week; if not the market will start to worry.

- NSW and Victoria’s Covid trends: Victoria is showing early signs of stabilisation while NSW holds the line. Broadly in-line with expectations.

- Australian Policy: Federal government will make payments to support self-isolating Victorians unable to earn an income. Emphasises approach of policy plugging economic gaps.

- Australian earnings season: Mixed results, but too early for discernible trends. ResMed (RMD, -11.4%) was negative; REA Group (REA, +4.6%) was positive; Insurance Australia Group (IAG, -1.2%) was in-line.

Covid-19 update There was no material change in trends in Australia last week. While it’s too early to make a call, it’s reasonable to assume the Victorian lockdown will work based on previous experience. NSW case numbers need to be watched. However we note that swift identification of clusters and contact tracing means the numbers are better than many had feared. Signs that NSW continues to hold the line — and that the Victorian lockdown is yielding results — should be well received. Any signs of an acceleration in NSW would hurt sentiment. US trends are generally positive. Test numbers are falling — but not as much as case numbers, so the ratio of positive results is falling. There is some evidence that base levels of immunity are helping in the worst-hit states. More importantly hospitalisations are falling. This is helped by a younger age skew, better adherence to safety protocols and possibly the weather. Even in the hotspot states hospitals have been coping and pressure is now being relieved. This has fed through to a much better outcome in terms of mortality. Deaths reached half the rate of the April peak and are now falling. This is likely due to age skew and protocols. But it’s also due to a wider geographic spread of cases, allowing the healthcare system to cope better — with more experience and better treatments. At this point we are likely to see a Sweden-like model in the US, where cases remain persistently high. If the community believes a third major surge can be avoided under this model — and acute cases are better managed — activity will start ramping up again, supporting markets. This is a very different situation to Australia. Here we are prepared to accept more short-term economic damage in exchange for effective elimination. The key risk in the US is children returning to school at the end of August. This will be a key swing factor moving into September. The US reporting season has so far yielded the largest ever quarterly decline in earnings and the largest upside surprise to expectations. US earnings are down 35%. This is far better than consensus expectations, which have obviously re-based too low. This has helped the market offset the negative effects of the Covid second wave and stalled fiscal negotiations. Economic update The US remains in a holding pattern. Mobility data and outlook surveys are all trending sideways. Employment data was better than expected, but still a material step down from improvements in June. Elsewhere around the world ISM survey data suggests good momentum on improving growth from June, albeit off a low base. Vaccine update The development of a viable vaccine remains the most important medium-term issue for the economy and markets. The result of the Novavax trial was encouraging, but not a silver bullet. Its platform is based on introducing a protein rather than the current approach of using a genetic message to prompt the immune system to produce the required protein. This is important because it offers an alternative route for vaccine development and increases the overall chances of success. The method of vaccination also has a better history of success. Consensus expectations among experts about the likelihood of developing a vaccine for delivery in material amounts next year have increased markedly in recent weeks. Gold Gold has run hard in recent weeks and become the hot topic in financial commentary. Traditional measures of sentiment suggest it may have over-heated near term. The RSI, for example, has reached its highest point in over a decade. This suggests near-term consolidation may be likely, particularly if we see more positive news on the vaccine front. Nevertheless, we continue to see this as a buying opportunity. In our view gold plays an important role in the portfolio, protecting against two key issues (outlined below) and risks facing investors:

1. The decline in real rates

As we’ve noted before, the Fed has clearly signalled it will allow inflation to rise through the target range rather than pre-emptively tightening. They are taking the view that avoiding structural economic deterioration and potential social consequences is paramount. So we are likely to see the use of their balance sheet and other tools to hold nominal yields, even as inflation expectations rise. This should support economic growth. But there is also an imperative to hold rates down given the explosion in debt — much of it short duration — with which the US treasury has been funding itself. Even a small increase in rates could see a massive increase in interest expenses, which the US budget would struggle to accommodate. The outcome is likely to be long-term suppression of real rates, which in turn is driving a lower USD, lower credit spreads, lower equity risk premiums — and a higher gold price. It also has a significant effect on performance within the market, as referenced last week. It is more nuanced than a simple rotation to value. Value does not necessarily outperform, given this could be a headwind for financials. But it will help certain industrials. Growth stocks are okay in this environment, but they lose the tail wind they have had for 10 years. Outside of equities, low real rates are beneficial for other real assets. This has constructive implications for housing. Mortgage affordability in the US is rising and history suggests low real rates are good for house prices. It is worth putting some perspective around moves in the USD, given its relationship to this issue and to gold. It, too, looks oversold in the near term. Some are pointing to the fact that it is back to a reasonable historical range when measured by the DXY (US Dollar Index). However the latter is dominated by value versus the Euro (58% of the measure). On a trade-weighted basis (TWI) the USD remains very strong compared to history. It has room to fall further once the near-term move has consolidated.

2. US-China relations

The second driver of a gold position is the deterioration in US China relations, which is unlikely to look any better ahead of the election. While the tension remains largely rhetorical at this point, there have been material moves that elevated risks and risk premiums in the market. The US has acted against Chinese companies such as Tik Tok and WeChat. It has also sanctioned politicians, increased carrier group activity in the South China Sea and sent the US health secretary on a visit to Taiwan. China has responded via moves in Hong Kong, increased activity in the disputed regions of the South China Sea and dragging its feet on a phase one trade deal. With the US and China using this friction for domestic purposes, this situation is unlikely to disappear in the near term. Heightened tension is prompting investors to allocate more to gold for portfolio insurance. Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia. Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management. Find out more about our investment capabilities: https://www.pendalgroup.com/about/investment-capabilities Contact a Pendal key account manager: https://www.pendalgroup.com/about/our-people/sales-team/

What’s the outlook for bond yields right now? Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor explains in a new video interview with online business channel Ausbiz.com.au.

Watch the video above or read the transcript below.

TRANSCRIPT

AUSBIZ interviewer: Vimal Gor is joining us from Pendal Group. I would like to get your reflections on Jerome Powell’s media conference on the reiteration of monetary policy stance in the US. What was your big takeaway?

VIMAL GOR: He was pretty much as dovish as he could have been. There’s this big debate around when they’re going to move to an average inflation targeting framework.

They pretty much said last night that they’re already doing that and even though they haven’t officially announced it yet. They are already running the policy which effectively means the monetary policy is going to be easier than it would have been under the old regime.

The Fed has a target of 2% and average inflation has been running over the last few years at about 1.5%, therefore they need to make up that shortfall inflation.

They will have to run an easier policy which is kind of what everyone was expecting, but the way that he reiterated that was really interesting.

It means they’re probably going to have to announce this in the September meeting, so it just means easier monetary policy pretty much forever in the US.

INTERVIEWER: I noticed one of the questions in the press conference that Jerome Powell was asked was whether the Fed would consider buying equities directly. And he said a flat out ‘no’. We have seen in the past that markets can go and bully the Fed into making particular moves, do you say that the Fed will never, ever buy equities?

VIMAL GOR: I fully expect the Fed to buy equities. They say they never going to do things and they do them. They’re talking about buying CMBS and they’re already buying ETFs and high yields.

If you’re buying a fallen angel high yield bond which has a massively high correlation to equities, why won’t you just buy equities as well? Bank of Japan has been buying equities for many years.

In fact, they are the largest shareholder of most of the companies and Niko. This is the next level when the economies don’t bounce back because the way the markets and the Feds are expecting, they have to add more stimulus in and they’ll just continue to throw package after package.

Interviewer: The first time we spoke, early in this pandemic, you were absolutely unequivocal that we would see rates going to zero and potentially negative. Do you still have that conviction?

VIMAL GOR: Yes, very much so. The CPI numbers we saw last week highlight that. We talked about the difference between nominal yields and real yields, and that’s behind this whole conundrum right now.

The market focuses on nominal yields and about nominal yields going below zero, but it’s all about real yield. If nominal yields don’t move then we will have deflation like what we have in Australia, the real yields are increasing and that slows the economy.

That is the last thing the RBI needs. If you bring it back to the Fed, and what the Fed has done is lock itself into this situation. It certainly wasn’t predetermined, but they’ve found themselves in a situation where they’re controlling nominal yields, the same way the RBA. RBNZ and ECB held nominal yields.

Now what they’ve found themselves in is a situation where they can get inflation expectations moving in the US. Would it bring real yields down, which continues to boost the economy?

Unfortunately, in Australia our inflation rates are low and inflation expectations are low. If nominal yields don’t move and inflation expectations come down, we’re seeing real yields rise at some point that I would still expect bond yields in the US and Australia to go negative across the whole curve.

AUSBIZ: Do you think all this is going to work? We’re in a pandemic, we’ve got mass unemployment, and things are looking pretty grim. Is it going to have the desired effect?

VIMAL GOR: Absolutely not. The desired effect is to slow the pace of the slow-down. We have a massive multigenerational hit to economies. It’s a solvency issue, many companies will need to go bankrupt and go under.

And what has happened by the monetary and fiscal policy we’ve seen from authorities across the world is from a large degree of liquidity at a solvency issue.

It doesn’t mean that the companies won’t go under, but what you’re doing is you’re drawing out the amount of time over which they go under. Therefore the drawdown in economic growth isn’t as deep or as quick.

And so effectively you’re hoping that you can grow out of this over time. If you took it over one or two quarters the effects would be unbelievably bad. They’re just trying to buy time for the economies and hope the economies heal somewhat.

But there’s no question that when you take the growth that drawdown in a short period or a long period, it’s still going to be monumentally large.

Interviewer: We saw the 10-year real yield in the United States at record lows last week, the big dollar suffering wounds and gold has hit record. What happens next?

VIMAL GOR: It goes higher and we can talk about gold. I think last time we also talked about crypto, and I’ll talk about that very briefly in the same context. The fed has bypassed the US banking system, and it’s pumping money directly into Main Street now.

If you’re a corporate in the US you can go directly to the Fed to get a loan. And when, in all likelihood, they’re going to forgive that loan anyway. So it’s just free money. And that’s why money supply growth in the US is running at 30%, 40%, the largest by magnitudes that this has run since the sixties.

At some point, there has to be inflationary and the market is reacting to that, not right now, but in the medium term. Plus a loss of confidence in the fear currency system, because every government in the world is just ignoring debt levels now.

And so those two things coupled together have met the gold’s going up. The other reason for gold is that normally other assets yield positive and gold is a negative-yielding asset.

But you buy a rock and then you dig a rock up, you sell it somewhat. And I put it back in the ground, but it costs you to hold in the ground because there’s a holding cost for like storage and security, etc.

So gold is a negative-yielding asset. Now, virtually every asset in the world is a negative-yielding asset. Therefore gold on a relative basis looks better. And then you can take that argument on Bitcoin.

If Bitcoin is considered a store of value and a store value is purely a social construct. Then it is better than gold as it’s transferable as you don’t need to go and physically pick up a big heavy bar and just give it to someone else.

It has an advantage over gold. Plus it’s a call option on the digitalization of the world, which is very clear where we’re going with all the central banks in the world, looking at their own coins. At some point, if you believe in the social construct like Bitcoin has a store of value.

Well, then you would expect Bitcoin to start really going in here as well. Gold and Bitcoin are going up for similar reasons in loss of confidence in the financial system, but they’re also going up for different reasons, pieces of a call option on arguably a new financial future, and the digitalisation of the world.

Vimal Gor – Head of Bond, Income and Defensive Strategies

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

EACH year responsible investment adviser Regnan engages with a range of ASX-listed companies seeking better management of Environmental, Social and Governance (ESG) issues.

Here Regnan’s Head of Engagement Alison Ewings (pictured) outlines our progress

REGNAN’s corporate engagement work encourages market disclosures that support better decision-making, improved responses to climate-related risks, greater oversight of conduct and progress in corporate governance issues.

In 2020 the work could not be more relevant after a horror Australian bushfire season, closely followed by the COVID-19 pandemic and global debate on inequality highlighted by the Black Lives Matter movement.

Regnan — a wholly owned subsidary of Pendal — has just released its annual Engagement Impact Report covering the outcomes of its meetings with 41 companies over the past year.

The report shines a light on the importance of three key issues: capacity, resilience and interdependency.

“ESG engagement has often sought assurances regarding capacity and resilience — invisible assets that can receive scant attention when things are going well,” the report says.

“This year has provided an opportunity to test and underscore the importance of these, from straightforward aspects such as director over-commitment, to more complex questions of maintaining an appropriate balance between efficiency and resilience.

“But the pandemic has also revealed the extent of interdependencies within our system, many of which lie beyond the boundaries of the portfolios in which we invest.”

Positive progress

The good news is, Australian companes are listening and acting.

More than 95% of Regnan’s active engagements have demonstrated progress, including 79% in the past 12 months.

As well as reporting on the impact of its ESG engagement with companies, Regnan also explores the implications of current world events for active asset owners.

Engagement on complex social issues has increased relative to previous years, the report notes.

Political lobbying, supply chain and issues of cultural heritage and stakeholder relations all feature more prominently, attracting media and community attention.

On the topic of modern slavery legislation Regnan encourages a “beyond compliance” approach focused on making a meaningful difference.

CLICK HERE TO READ THE FULL REPORT

Regnan is a global leader in long-term value, systemic risk analysis and responsible investment advice.

Last year Regnan appointed a London-based impact investment team to launch a Global Equity Impact strategy in late 2020.

Regnan recently co-authored a paper with the Principles for Responsible Investment, Active Ownership 2.0, which includes tips for owners seeking to be more active.

Regnan is wholly owned by Pendal Group.

Liquidity everywhere – the chase for yield: portfolio manager Steve Campbell (pictured) of Pendal’s Bond, Income, and Defensive Strategies team will discuss this in the article below.

The Reserve Bank’s Statement on Monetary Policy in May contained its forecasts for the Australian economy out to June 2022.

The statement highlights significant headwinds ahead for the Australian economy, even allowing for the fact that some forecasts may be too pessimistic.

In its most recent economic forecasts, the RBA revised down economic growth for the year to June 2020 by almost 10% to -8%. For the year to December economic growth is forecast to be -6%, a downward revision of 8.7%.

This would normally result in an aggressive cut to the cash rate. But with a starting point of just 1.50% from mid-2019 – and the RBA’s aversion to negative interest rate policy – we have seen the cash rate cut by just 125 basis points.

If the magnitude rather than the level matters, it’s paltry when all else is considered. Contrast this with the GFC experience and the RBA’s forecast revisions around that time.

For the year to June 2009, economic growth was revised down from growth of 2.25% in August 2008 to -1.25% in May 2009. A 3.5% fall in forecast economic growth saw the cash rate cut from 7.25% to 3% versus a 10% fall in forecast growth that has seen the cash rate cut from 1.50% to 0.25%.

The RBA is not alone in the limited ammunition available via conventional monetary policy.

The following graph shows the total changes to cash rates during the GFC and the most recent moves due to COVID-19.

What does this mean going forward? The RBA has moved into more unconventional areas with the use of yield curve control and the term funding facility. With the damage wrought on the economy, further stimulus is warranted – be it fiscal or monetary.

Modern Monetary Theory is something that will garner more and more discussion in this period. The output that has been lost as a result of COVID-19 will take a long period to recover.

For cash investors returns are going to remain extremely low. If other central banks implement negative interest rates it cannot be ruled out here either. Although the RBA certainly won’t be leading the charge into the next wave of negative rate club members.

Steve Campbell – portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Tailwinds for credit: portfolio manager George Bishay (pictured) of Pendal’s Bond, Income and Defensive Strategies team will discuss this in the article below.

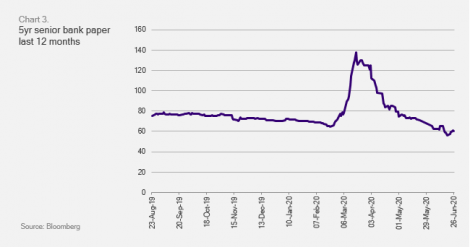

Credit markets had a strong quarter following the chaos of March. A number of key policy decisions taken by central banks in mid-March provided a bedrock for a strong recovery in credit spreads. We also saw somewhat better health and economic outcomes through May and June –particularly in Australia. However these are being tested in July.

The Reserve Bank introduced Yield Curve Control in mid-March, anchoring 3-year rates at 0.25% for at least three years. This started a grab for yield – or as bond managers call it, “carry and roll”.

Bonds with maturities fewer than five years across the spectrum were huge beneficiaries as one element of uncertainty was removed. The RBA also started a Term Funding Facility (TFF) for banks, providing 3-year funding at a super-cheap 0.25%.

There are limits on this, but it has removed the banks’ need to issue term funding for the rest of the year. The take-up of the RBA’s TFF has been gradually increasing over the quarter, with total drawdowns to date of just over $A12 billion out of a total funding allowance of $A135 billion.

Bank spreads are now tighter than before the crisis, providing a knock-on effect to other credit sectors.

The third measure the RBA took in April was to widen repo eligibility to include senior AUD issued investment grade credit. This stopped short of the actual buying of corporates which a number of other central banks undertook. But the impact gave another strong tailwind to credit spreads.

This has seen spreads between non-financial bonds and financials widen compared to historical levels. The typical spread of 20bps is now sitting at 60bps as lower bond issuance combines with strong demand for higher-rated banks bonds.

These three RBA policy decisions were seen as part of a “whatever it takes” mantra by global central banks and governments. In past decades we’ve had the Greenspan put, the Bernanke put, the Yellen put and now clearly the Powell put. For Australia you can throw in the Lowe put.

The perception is that if conditions deteriorate again central banks will have your back. As Virgin Australia discovered it is not limitless. But for key locally-owned firms in significant industries, being part of Team Australia has its benefits.

Governments around the world are also deploying significant fiscal packages to support employment and stimulate economies. These have encouraged equity and credit markets.

In the medium-term the focus of markets will switch back to the underlying credit fundamentals of companies.

Many companies across the globe improved their credit quality by raising equity to support their balance sheets. We have favoured those companies keen to keep gearing under control and protect their credit rating in the face of potential asset write-downs. We are also watching closely the dynamics from this crisis impacting different sectors in the long term. There is no doubt the world has changed, which will bring permanent damage to certain industries.

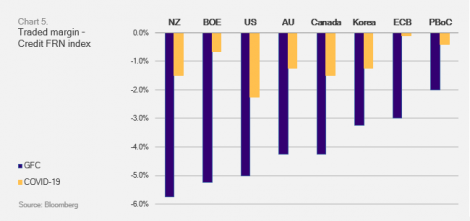

The Australian iTraxx index (Series 33 contract) traded in a very wide 115bp range finishing the quarter 87bps tighter to +88bps.

Physical credit spreads were generally narrower, on average tightening 18bps for the quarter. The best-performing sectors were domestic banks, telcos and supranationals narrowing 57bps, 45bps and 19bps respectively. The worst-performing sectors were infrastructure and Real Estate Trusts (REITs) which widened 32bps and 13bps respectively.

New issuance picked up in May and June. Brisbane Airport (BBB) launched a 6-year and 10.5-year tranched deal. The book received $1.75 billion in orders over both tenors and $850 million of bond issuance. On the back of strong demand and attractive pricing the 6-year and 10.5-year tranche pricing tightened 35bps during the offer.

Other issuance in the corporate bond market included Westlink M7, the 50% Transurban-owned entity that operates the M7 concession around Sydney. It issued $155 million in 10-year bonds. The deal was 7.6x over-subscribed which saw its pricing tighten from first indication of 225bp to 215bp. It ended at 185bp. Singtel Optus got in on the action with a 5-year and 10-year bond issuance for a total of $850 million on a total book of $2.8 billion (3.2x over-subscribed).

In the supra-national space the National Housing Finance and Investment Corporation returned to the market with a very successful $562 million 12-year social bond. An Australian government guaranteed issuer, it came at 38 over Australian Commonwealth Government Bonds and is now trading at 18 over.

Overall most credit outperformed government bonds, helped by swaps spreads going further under government bonds.

Our outlook is still positive. However we remain cautious with the slowing pace of spread-tightening as we test multi-year tights in some sectors (domestic financials). Uncertainty stills exists in other market sectors.

Bid-side liquidity has significantly improved. Bid offer spreads compressed as many banks returned to the market after an absence in March and early April.

The balance between technical factors – such as central bank support, driving spread performance and the longer-term impact of the virus and subsequent economic fallout – remain critical to the future performance of credit markets in the months ahead.

George Bishay – portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Avoiding a double-dip recession: portfolio manager Tim Hext (pictured) of Pendal’s Bond, Income and Defensive Strategies team will discuss this in the article below.

My first year in markets was 1989 and my first trade was buying some bank bills at 18.5%. I should have bought a 30-year bond!

Crushing inflation had become a cruel venture, bringing on the recession that Paul Keating said we “had to have”.

Living in Melbourne in 1990 was to witness first-hand an imploding economy. Businesses closing almost every day. Unemployment soaring. House prices collapsing. People struggling. Any job was a good job — forget whether it was inspiring.

Recessions were seen as a natural part of the business cycle.

In the early 1990s, even the most optimistic economist would have expected another recession within 10 years. The odds of a 30-year wait would have been longer than Parramatta or Carlton going without a premiership for decades. The true miracle was avoiding a recession during the GFC. China rode to the rescue and the real economy avoided the fate of financial markets.

Walking around a number of shopping centres and strips in the past month brought back memories from Melbourne in 1990. “For Lease” signs everywhere and shops boarded up. I stopped to look in the windows of closed businesses. Some signs said “Opening Soon When Safe” – but sadly many have closed for good.

Large numbers of retail stores were marginal before the crisis. Rent relief beyond 50% was at the behest of landlords. Some landlords have worked to keep tenants but others have merely added the other 50% to future bills.

Perhaps the crisis has merely accelerated the push to clicks over bricks – and retail will bounce back. If enough workers are still getting paid they will spend it online. Restaurants may survive via delivery. The fleets of electric bikes around my neighbourhood have swollen.

Last quarter I spoke about the shape of the recovery as the economy cautiously began to open up.

Adding to the list of V, L, U and W we now have the Reverse Square Root, the Nike Swoosh, and other shapes showing the speed of the recovery.

This quarter I will look at the progress so far and ask the question: when will we get back to where we were in February? We did not know it at the time, but the high-water mark fell in between the bushfires and COVID.

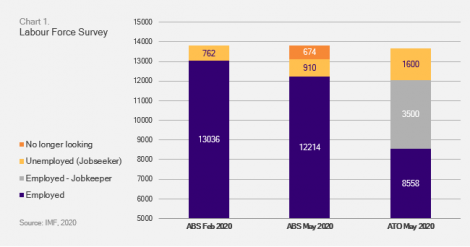

In February 13,056,700 Australians were employed. This was an all-time high. Australia’s population was 25.5 million. The population increased by 350,000 in the prior year including 210,000 being migrants. A record 66% of Australians over 15 years of age were either working or looking for work, meaning an unemployment rate of 5.1%.

Flash forward to May 30 and 7.5% of jobs had been lost according to tax office data. This equated to 980,000 jobs. At the worst point in April, it was 9% or 1.18 million. These are jobs where people are not getting paid. How many will return with the re-opening of the economy and how many have disappeared permanently? That remains to be seen.

Graph 2 shows the different measures of employment. Since March the Bureau of Statistics has released tax office data in a weekly payrolls report. This data is electronic rather than survey-based like the official labour force numbers. This is a far more accurate measure. It captures the large cohort of workers laid off but waiting for businesses to reopen so they can hopefully get their jobs back.

On March 20 Newstart was renamed JobSeeker and increased from $550 to $1100 a fortnight. About 1.6 million Australians are now on JobSeeker, up from 700,000 on Newstart in February. The labour force survey shows 835,000 jobs lost from February to May.

Where it gets interesting is the collapse in the participation rate from 66% to 63%. The labour force survey suggests only 210,000 people joined the unemployment queue with the rest dropping out. This conveniently keeps unemployment at 7.1%, not the 12% other measures are showing.

When asked in the survey “are you looking for work”, it appears for various reasons a large number of people are saying “no”.

JobSeeker numbers reveal the true damage. Numbers suggest everyone who lost a job is now on JobSeeker – even if they tell the Bureau they are not looking for work. The JobSeeker eligibility requirement of “actively looking for work” has been temporarily waived, but will return shortly.

Then there is JobKeeper. This is designed to keep people employed even if they are not working – or are working fewer hours. The $1500 fortnight payment, designed to roughly match the minimum wage, is paid through the employer in arrears. Businesses must have suffered a 30% fall in turnover if less than $1bn or 50% fall if greater than $1 billion. Numbers on JobKeeper are estimated to be 3.5 million after a mistake initially predicted 6.5 million, or half the workforce.

JobKeeper is scheduled to end on September 27 although it may be tightened rather than abandoned altogether. No system is perfect. Some businesses believe they are more viable while closed under JobKeeper, which the government doesn’t want to encourage. For smaller businesses 80% turnover means losing JobKeeper – while also likely remaining unprofitable.

GDP is a volume-based measure. It’s called a chain volume because it’s linked quarter by quarter. There are three approaches to measuring chain volume – income, expenditure and production. Headline GDP is a simple average of the three.

In volatile times like this GDP can be confusing because it’s always reported as a growth number. The real question is how long it will it take the economy to get back to pre-COVID levels. The following graph shows the actual GDP rather than the rate of change. The graph also shows GDP per capita, a better measure of productivity in the economy.

It will take until early 2022 for the economy to return to its December 2019 size, based on estimates from the RBA’s May Monetary Policy Statement.

The RBA has tended to overestimate GDP in the past five years. Health outcomes make forecasting extremely difficult of course, but this assumption looks optimistic.

Viewed from a GDP per capita basis, however, the picture is less dramatic. Almost half of Australia’s GDP growth over the last decade has been due to immigration. Australia’s population growth has now collapsed and is unlikely to resume to pre-COVID levels for a number of years. This may mean GDP per capita has a better chance of improving.

Forecasting medium-term inflation followed some simple rules over the past 25 years. From 1993 to 2012 tradables (40% of CPI) were largely flat. Non-tradables (60% of CPI) were 4%, landing around the 2.5% target. In the last decade, non-tradable inflation started to fall to around 3%, led by health and education. This meant CPI settled closer to 2%.

Even before the crisis non-tradables were beginning to slip to 2% and CPI closer to 1.5%. This was largely due to a fall in housing (rents, building costs and utilities), which we viewed as cyclical, not structural. This meant we entered 2020 sharing the RBA’s confidence that CPI would drift back to 2% over 2020 as population growth and a lack of new building activity kicked in. COVID-19 has shot down that view.

The story of the economy is now one of widespread excess capacity. Shutdowns meant demand and supply were both hit. Coming out of shutdowns there are pockets of demand exceeding supply as global supply chains have been hit. However, in the larger items – particularly labour – excess supply dominates.

Joining this mix is a move to wage freezing. This is led by governments but is also likely in the private sector. The recent minimum wage decision gave a 1.9% increase, down from 3% or higher compared to recent decisions. However, as the pool of labour supply increases in many areas, new employees may come in on lower wages.

The real area of concern for inflation is rents. Rents make up 8% of the CPI basket, large enough to move the dial overall.

In pockets of inner-city Sydney and Melbourne, rents are already down about 6%. The levelling of the population means negative rent growth will spread to wider areas in these cities, which rely heavily on students and international workers for tenants. Other cities and rural areas may be less affected. But if rents were to fall 3% nationally this would feed into a 0.25% fall in inflation. There may also be second-round effects.

Until recently the RBA was happy to forecast and accept 2% CPI as the long-term average, despite a formal 2-3% target. Markets now have that closer to 1.25% over the next decade, after falling as low as 0.5% at one point. From a bottom-up perspective even 1% looks optimistic over the next few years.

CPI will be negative 1% or even lower in the June quarter, largely due to free childcare during the quarter. This will be removed, but an era of frozen costs seems here to stay across wide areas such as education, healthcare and government charges.

Excess supply in the economy will be with us for at least the first half of this decade.

Structural forces already in place were accelerated by COVID-19 and low GDP and inflation have pushed rates close to zero. The RBA believes negative rates do more harm than good, so they have stopped at zero. The stimulus required from monetary policy for a crisis of this scale was not there – otherwise rates would now be -3%.

Unconventional policy has held down term rates but this really only helps around the edges. Put simply, the RBA has done an excellent job from a liquidity role during this crisis – but from an economic stimulus role it has turned up with a knife to a gunfight.

The federal government now has all the firepower. The initial response to the crisis has been excellent overall. Fiscal policy needs to more permanently enter a new era. Ghosts of Tony Abbott’s debt scaremongering still seem to have an influence in Canberra.

Already there is talk of how we are going to pay for all this stimulus and that we are labouring future generations with our debt. You would think the government is a household; with a printing press out back it is not. If Australia is to avoid a lost decade we need to get comfortable with government debt sooner rather than later.

Short rates stuck at zero mean longer rates will also be supported. Any sell-offs in bonds as the economy opens up and data picks up should be bought into. Term premium should not drift higher despite the usual scaremongering around money supply pushing up inflation.

The same voices were out there after Quantitative Easing during the GFC. Once again they will be disappointed. One of the best trades earlier in the decade was harvesting the high carry and roll available. Levels today are not so generous, but still offer good value.

Australia has begun the long, slow grind of re-opening the economy.

Some damage will be repaired quickly while other damage has been terminal. As always, health outcomes partly hold the key to the speed of the recovery. However, the federal government is now front and centre and its actions can either prevent or cause a double-dip recession. The more timid their fiscal policy, the longer, deeper and more painful the slowdown.

Bond markets will remain well supported. Plenty of countries have been down this path before us and so far only the US managed, at least for a while, to emerge from the anchor of zero rates. They look like the exception, not the rule.

The grab for yield is once again upon us. For now it is a trend you must go with rather than fight.

We remain long duration and in portfolios with credit overweight investment grade. These themes have further to run in the quarters ahead.

Tim Hext – portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Fixed income impact investment is a fast-growing but still relatively new segment of capital markets. Here Pendal portfolio specialist David de Ferranti (pictured above) takes a deep look at impact bonds.

This quarter we saw COVID-19 impact the way businesses organise physical workforces. Social distancing measures closed doors across industries such as the local cafe, a favourite hotel or the office foyer. Despite difficult and ongoing challenges posed by such restrictions, it is encouraging to see new doors opening for some of those most at risk in the current environment.

Those in need of more affordable housing options — such as disadvantaged youth, the homeless and victims of domestic violence — will be among the beneficiaries of significant proceeds raised by a social bond issued in Australia last month. The deal from the National Housing and Finance Investment Corporation (NHFIC) amounted to A$562 million. It was the largest amount raised by a domestic social bond to-date. The issuance was well-received by investors and Pendal’s sustainable fixed interest strategy was able to participate.

In our Beyond the Numbers report we have written about the positive impact Community Housing Projects (CHPs) financed by the NHFIC can have for individuals at risk. Now, during the coronavirus crisis, affordable and social housing providers are even more critical. This is true not only for those impacted by reduced employment options. The benefits also flow to the residential construction sector, which brings broader benefits to the Australian economy amid a very tough economic outlook.

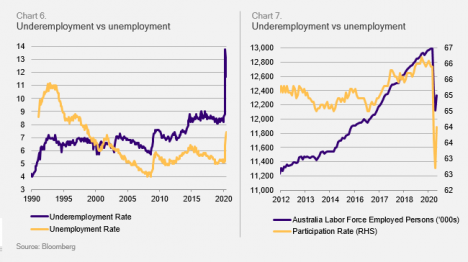

Domestic employment data shows the virus’s severe impact on our labour market. Some 664,000 jobs were lost between March and June this year, bringing the unemployment rate to 7.4%. The percentage of those seeking more hours and categorised as underemployed rose to 11.7% (Chart 6). Many individuals left the labour force altogether, reflected in a lower participation rate. This led to a dramatic drop in the number of total employed across the country (Chart 7).

The government’s JobSeeker and JobKeeper subsidy packages have offered some reprieve to those who have found themselves in financial distress. However, these stopgap measures do not address core issues faced by financially disadvantaged individuals over the longer term. Even with JobSeeker payments, only 1.5% of rentals are considered affordable, while with no JobSeeker rentals in the majority of Australian capital cities are unaffordable.1 Before the pandemic there was already a significant supply shortage of affordable and social housing. Australian Institute of Health and Welfare data shows roughly 140,000 Australians were on a waiting list for social housing, often equating to years in the queue.2

Certain demographics continue to be disproportionately affected by housing-related challenges. This includes women living in regional areas. Roughly one in eight have been homeless in the last five years and one in five know a homeless woman, according to the YWCA’s Women’s Housing Needs in Regional Australia report. When asked what would improve their situation most, about half responded with a reduction or subsidy of housing costs.3

Beyond the negative impact on individual financial situations, COVID-19 threatens further weakness for the residential construction industry, where activity was already on a downward trajectory. New commencements are expected to follow building approvals lower. HIA forecasts a fall in dwelling starts to 134,000 in FY2021, down from a peak of 230,000 in FY2018. This reduction in new supply of homes threatens not just the at-risk individuals noted earlier, but the livelihoods of those in the residential building industry.

The proceeds of the latest NHFIC social bond will not resolve the issues described here. But they will make a significant contribution to the lives of those in need of housing assistance and help keep a number of tradespeople in work. Some 7100 new homes and management of existing properties have been financed by the NHFIC issues to-date.4 The latest deal financed 10 CHPs, which have operations in a range of regions and are targeted at different demographics.

This includes Women’s Housing Limited which received a $9 million loan to refinance existing debt and buy new properties.5 These new properties will house women escaping domestic violence, who will be able to pay a rate much lower than the market rent. This helps essential workers in vital services such as healthcare and hospitals live closer to their workplaces.

The biggest recipient of financing was Sydney-based SGCH, the largest CHP in NSW. Its loan will help support 305 existing dwellings and 235 new homes in Australia’s most expensive rental market. The low rate provided through the NHFIC facility was estimated to save $40 million over its term — funds that can be invested in hundreds of other homes.6

Other recipients included Argyle Housing which supports regional communities via affordable housing. Recent projects have included new homes in Griffith for workers in the agricultural industry, as well as areas with at-risk youth in Wagga Wagga. Housing Choices Tasmania received financing for new developments across the state.

New homes created by these CHPs will make direct and indirect contributions to the residential construction industry. For each $1 million of output for the sector, nine jobs are supported and $2.9 million of output and consumption is created for the broader economy, the NHFIC estimates. This multiplier effect is calculated as the second-largest across all 114 industries in the Australian economy.7 Powerhousing Australia estimates the construction of a standard stand-alone three-bedroom house helps 43 trades and sub-trades gain employment.8

In this landscape of lockdowns, social distancing and housebound workers, a place to call home is of paramount importance. A safe and stable home has become even more critical. Building new homes for at-risk individuals brings security to the recipients and generates broader benefits to the Australian economy at a vital juncture. As investors in these bonds, we believe these outcomes also allow our clients to have a positive impact on fellow Australians when they need it most.

David de Ferranti – portfolio specialist with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

1 https://about.bnef.com/blog/sustainable-debt-sees-record-issuance-at-465bn-in-2019-up-78-from-2018/#_ftn1

1 Rental Affordability Snapshot, April 2020

2 AIHW, Housing assistance in Australia 2019

3 YWCA, Women’s Housing Needs in Regional Australia, 2020

4 NHFIC, NHFIC finalises largest social bond issue from an Australian issuer, 2020

5 Women’s Housing Limited, 2020

6 SGCH, 2020

7 NHFIC, Building Jobs: How Residential Construction Drives The Economy

8 Powerhousing Australia, Australian Affordable Housing Report F2021, 2020