Here’s what’s impacting Aussie stocks at the moment, according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

Main points

- Equity and bond markets remain in a holding pattern at an aggregate level, with the S&P/ASX 300 at -0.1% for last week

- A weaker shift in the US dollar was the catalyst for a shift higher in gold and prompted signs of rotation from growth to value

- In the US there are early indications that case-load growth and hospitalisations are peaking in the worst-affected states

- Domestically we saw extensions of the JobKeeper and JobSeeker packages; while the RBA has clearly signalled its intention to continue providing policy support

Australian outlook

So far the Victorian government has refrained from imposing Level 4 restrictions, but the growth in cases remains disappointing.

There are signs restrictions in Melbourne are slowing economic activity, while voluntary behaviour is having the same effect in Sydney.

This in part prompted clear policy signals last week. The federal government extended its packages, however comments from RBA Governor Phil Lowe were of most interest.

Lowe emphasised the view that social costs and degradation from recession and persistent unemployment were too high to allow the normal clearing mechanism of labour and capital markets. Instead, policy makers must do everything in their power to mitigate the effects of this crisis.

This shift in thinking away from a free market approach may be driven by considerations around the social effects of income inequality. It could also be driven by a view that labour markets are too rigid to react in a timely fashion to a shock of this nature.

Regardless, it suggests policy makers will continue to shore up growth, with Governor Lowe suggesting there are several more tools available if needed.

Global outlook

New daily US cases have levelled off over the past week and hospital occupancy rates remain stable in hotspot states such as Florida, Texas and Arizona. If the market starts to believe the health situation is moderating, it should be positive for sentiment.

Nevertheless US economic data was softer. Jobless claims rose week-on-week for the first time since March.

Real-time indicators such as restaurant bookings suggest momentum has stalled after an initial surge. However, the environment is uneven. Demand continues to grow in sectors such as housing.

The next tranche of policy support appears to have been delayed while the Republicans seek agreement on a package. We are now likely to see a gap of a week or two between the end of payments under the previous package and the start of the new.

Elsewhere, the speed and scale of a €750 billion package announced by the EU came as a pleasant surprise given the debate between the “Frugal Four” northern states and southern countries likely to be the main support beneficiaries.

Markets

The weaker US dollar was driven by a combination of factors:

- Worse Covid case load in US vs Europe, and its expected impact on economic recovery

- Positive policy surprise in Europe versus delays in US

- Growing uncertainty about the upcoming US election

- The impression that ineffective fiscal policy in the US puts more pressure on the Fed to ease in various forms.

Weakness in the USD adds to the bull case for gold. It is increasingly evident that virus spread is hampering economic re-opening in the US and is becoming a limiting force on growth.

Unlike places such as China, which have effectively eradicated the virus, it is making it harder to return to pre-Covid levels of economic capacity.

However policy-makers are baulking at allowing this to trigger a significant recession and are falling back to stimulus such as more debt and more money supply growth.

This has several important effects, including question marks over longer-term strength of the dollar. This is seeing strength in the value of real assets. In some ways this is positive because it suggests expectations around policy-supported growth remain reasonable.

A reversal in US dollar weakness would suggest a flight to safety on increased concern.

Inflation expectations have been rising in recent weeks, but have only recovered to pre-crisis levels. Further increases in inflation expectations would require people to start factoring in tighter labour markets, which appears unlikely at this point.

That said, inflation is showing up in areas such as real assets.

Value had a small bounce versus growth in equity markets last week. There is a case for further value outperformance if we see US cases plateau, more fiscal stimulus — and if US tech earnings don’t bring any further upside to already high expectations.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Here are the key factors influencing Australian equities this week, according to Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

BOND and equity markets remain in something of a holding pattern. The S&P/ASX 300 gained +1.8% last week despite poor news on the COVID front including tighter restrictions and evidence of a slowing economic recovery.

The focus is now on key developments including:

-

- Imminent fiscal policy announcements in the US and Australia

- Medical strain resulting from the US caseload

- Victoria’s restriction level and NSW’s ability to contain the outbreak

- Upcoming earnings seasons in Australia and the US

Equities and bond yields have been relatively flat for a while and it feels like the above factors could drive volatility at some point in next 4-6 weeks. However it’s very hard to call how that plays out.

Most surveys suggest investors are bearish and expect the next move to be down. This already depressed sentiment could support a break higher if upcoming fiscal packages or management of the second wave of infections is better-than-expected. Higher infection rates make it easy to be bearish – but we caution against the view that a drawdown is inevitable.

The Australian outlook

There are three key issues at play:

-

- Will Victoria implement greater restrictions? The estimated economic effect of the current lockdowns is 0.5% to 1% for Australian GDP. This could more than double if Victoria moves to level 4 restrictions, halting all retail and construction activity. There is a lot of pressure to avoid an extension of restrictions, but ultimately the case load will dictate this.

- To what extent will an increase in NSW cases lead to more restrictions? Any economic impact would be 50% greater than Victoria.

- How would a renewal of NSW restrictions impact fiscal policy? The Victorian situation has increased expectations about the size of a fiscal package due to be announced this week. There is talk of an additional stimulus worth 1% of GDP. This would offset much of the concern over a “fiscal cliff” and highlights the fact that policy makers continue to underwrite the economy and prop up markets.

The US outlook

Hospitalisations are rising dramatically in the US, closing on the previous peak and set to go well past it. This has not yet converted to a material increase in mortality, given a wider spread of cases and better understanding of treatment. Pressure on hospital system is building and risk remains — but health infrastructure is coping so far.

Rising US cases have triggered a behavioural response which should help. Some 77% of American live in areas now requiring masks. Mobility data is signalling that less interaction is occurring, albeit without too severe a retracement in activity.

The most effective models suggest this US cycle in cases should peak in early August at the current rate. If this ends up breaking higher, a more restrictive economic environment is likely to occur.

The vaccine outlook

The market continues to react positively to any positive news flow on vaccines. This triggers sharp rotation away from tech back towards value and cyclicals, which highlights the challenge in constructing portfolios in this environment.

Overall there remains a reasonable degree of confidence on the potential for a vaccine around year-end. Still, we are mindful of a set of subsequent issues, such as how effectively can it be produced and distributed, frequency of dose, people’s willingness to take it and the potential for new variants of the virus to require new vaccines.

Economic outlook

The debate over suppression versus elimination continues to rage. There is a growing push-back against harder lockdowns given the degree of economic impact.

As this plays out, we are mindful that higher case numbers can impact confidence even if governments avoid further restrictions. Surveys suggest Americans have lost confidence in dining out and public entertainment in recent weeks. This is reflected in broader indicators of consumer sentiment, which were not so constructive in recent weeks.

The slowing pace of recovery is likely to influence the next round of US fiscal stimulus, set to be announced soon. Markets are suggesting an expectation that the government will continue underwriting the economy.

Elsewhere, Chinese data remains supportive, while there are positive economic signs emerging in Europe.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Some country-level factors are more important than others for Emerging Markets investors right now. Here are the latest insights from James Syme and Paul Wimborne (pictured), managers of our Global Emerging Markets Opportunities fund.

FOLLOWERS of our emerging markets investment process know we group our selected country-level market drivers into five broad groups.

But we recognise some of these are more important than others at particular times.

The current environment is one of these times, where pre-existing balance of payments strengths and weakness have outweighed the effects of monetary and liquidity stimulus applied across emerging markets.

When we look at the liquidity and monetary environment in emerging economies, we are focusing on the rate of increase of monetary aggregates and lending/credit in the economy.

We are then assessing how sustainable that is in light of inflationary pressures and the degree of leverage in the economy.

Generally, faster rates of money/credit creation are supportive of economic activity and asset prices. Typical beneficiaries are the more cyclical industries such as banks and non-bank financials, capital good and autos and real estate, cement and construction.

Similar to developed markets, the response to the COVID-19 crisis in emerging markets has involved an aggressive monetary policy response.

Rates of money-supply increase and bank-lending increase are up substantially in many countries. This might normally imply a positive outlook for risk assets in these markets. But these are exceptional times and we must act accordingly.

To give a sense of the scale of change, consider Brazil.

In the past 10 years policy interest rates in Brazil have averaged 9.6% and consumer price inflation 5.8%, giving an average real policy rate of 3.6%. At the end of June policy rates reached 2.25% (down from 14.25% in 2016), with consensus inflation expectations at 2.75% for the next 12 months.

Meanwhile, M2 money supply growth reached 23.2% in the year to May, compared to a 10-year average of 10.4%.

At first glance, this is a super-bullish environment for equity investors in Brazil.

However in extreme circumstances, as Keynes noted, monetary policy can amount to no more than pushing on a string.

These are extreme circumstances, and these monetary policy settings have failed to return Brazil to growth.

Although real rates are negative and money creation abundant, loan growth has reached a disappointing 9.2% year-on-year. (In the 2007 boom, when money supply also grew rapidly, bank lending grew 28.8%).

GDP growth in 2020 is predicted to be -6.5%, a forecast that continues to worsen. Similarly, 12-month forecast earnings for the Brazilian equity market (using the Bovespa index) are 36% lower than the start of 2020.

Similar pattern in other emerging markets

Brazil is an extreme case. But there is a similar pattern in other emerging markets where weak current accounts have meant high exposure to external sources of financing, which have proved difficult to support in the current crisis.

Mexico, South Africa, Turkey, Indonesia, the Philippines and India are among other markets with sustained current account deficits that have high levels of money creation but extremely weak economic outlooks.

Markets with generally strong current accounts have been able to maintain stronger levels of economic growth (and even stronger levels of banking lending growth) from a far less aggressive monetary response. These include China, Korea, Taiwan, Malaysia and Thailand.

Even in these unprecedented times, the big risk beta in emerging markets remains largely unchanged.

It remains our view that a diversified emerging market equities portfolio needs selected exposure to both groups of countries – even if one is doing better than the other.

While we have significant exposure to Korea and China, we also retain exposure to India, where corporate earnings expectations have held up better than other countries in the high-risk group.

We also have exposure to Mexico, which we believe is a high-quality market with significant opportunity in more defensive names.

COVID-19 is a shocking new development this year, but it is playing out across emerging markets very much along established lines that we have seen many times before.

James Syme and Paul Wimborne are senior fund managers and co-managers of Pendal’s Global Emerging Markets Opportunities fund.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

As the COVID-19 pandemic continues to impact the global community, we remain focussed on taking proactive measures and precautions to ensure the health and safety of our employees, while maintaining our ability to service our clients and manage our business.

Our JOHCM and Pendal Australia staff have been working from home since mid-March 2020. Pendal Group has comprehensive Business Continuity Plans in place for all of our offices allowing us to continue to operate uninterrupted in these circumstances. Additionally we remain in regular dialogue with our core suppliers to ensure there is no disruption to services.

The Group has supported staff working from home through the use of technology and ongoing support programs. As restrictions are wound back and depending on the jurisdiction and government advice, employees where they can and are comfortable to do so are starting to return to the office, although this is a gradual and controlled process.

We continue to prioritise communication with our clients, keeping them informed through market updates and thoughtful insights on how to navigate through these uncertain times. I encourage you to visit the Market Insights, Education and Resources page on our website for the latest information.

These are unprecedented times for all of us and the situation remains fluid. We closely monitor the local and World Health Organisation updates and practices in local jurisdictions and where required we will take further sensible and informed action.

Our hearts and thoughts goes out to everyone who has been directly impacted and especially those families who have had to endure the loss of loved ones. We wish you and your family the best of health.

If you have any questions or concerns, please do not hesitate to reach out to your Pendal Group contact.

Emilio Gonzalez

Group Chief Executive Officer

Pendal’s head of equities Crispin Murray (pictured) outlines how the latest COVID-19 developments are impacting the outlook for Australian equities.

Quick take-outs

- Markets held up relatively well despite worse COVID-19 case and hospitalisation data last week.

- Australia’s probability of suppressing the virus has taken significant step back, impacting Real Estate Investment Trusts and domestic cyclicals

- Liquidity is still clearly prevalent as the NASDAQ hit new highs, driven by the FANGMAN stocks (Facebook, Amazon, Netflix, Google, Microsoft, Apple, Nvidia) and others. Tesla is up some 60% in two weeks. The Chinese market has also broken out – Ali Baba is up 21% in two weeks.

- Commodities are performing well, reflecting their real asset status

- The on-going disconnect between economy and markets continues. This is a distortion created by fiscal stimulus propping up spending and central bank actions underwriting government and corporate bonds – and effectively equities.

This accelerates structural trends supporting growth stocks in the market, with their higher weightings in indices, momentum created by passive funds, active funds forced into growth – and now day traders.

The key is to build portfolios that are able to hedge enough of this rotation. An important part of that is positioning right now in real assets, notably gold.

Australian focus is on Victoria

The big issue for investors is rationalising the fact that markets are still behaving relatively well despite negative headlines and case surges.

The focus is on Victoria – which represents 25% to 30% of national GDP – and assessing the risk of this surge affecting consumer confidence in other States.

It is right to be concerned about the near-term effect on the market. But we can see in Brazil and the US that markets can easily disconnect from poor COVID case data. These markets continue to rally as case numbers spike.

The number we are paying closest attention to right now is the positive test rate, which has continued to rise.

However, there is a ramp-up in the amount of testing in Victoria, which is critical in preventing new outbreaks from building. When this number rolls over it will be the first sign that things are improving.

US health system stability is a key issue

A key question in the US is the severity of strain on hospitals and the associated impact on death rates.

Hospitalisations are moving higher with a two-week lag. It’s becoming apparent that the south of US is effectively following the Swedish approach of “controlled spread”. It is unlikely we will see a significant reinstatement of lockdowns.

The US hospital system is still largely coping – Phoenix and Houston are the two worst-affected areas. Elective surgery has been suspended in Texas and some big city hospitals in Florida and California. Capacity is still available though.

Some of the market’s apparent ambivalence can be explained in favourable statistics (which will need to be watched carefully).

For example the US death rate for hospitalised patients has dropped from 20% to 10%. The rate peaked at 25% in New York and has since dropped to between 5% and 10%.

Treatment techniques have also changed, leading to fewer patients on ventilators – down from 25% to 15%. A slower rise in death rates may result from wider use of facemasks, more testing, improved awareness of safety protocols in nursing homes and younger patients.

Global growth signals

It’s clear the economic V bounce is slowing in the US. But other global growth signals are holding up reflecting China’s recovery (copper), strong housing (lumber prices) and ample liquidity.

In fact, liquidity is overwhelming other factors. The world’s two biggest economies, the US and China, have increased money supply 18% year-on-year. This drives financial assets and supports parts of the economy such as housing.

The Chinese market has broken through a five-year down-trend and US mortgage rates are making new lows as a result.

Bull case vs. bear case

The bull case narrative for August/September centres on these potential outcomes:

- Decelerating cases in US

- Death rates remaining lower

- Vaccine progress

- Large US fiscal stimulus

- Resumption of Fed balance sheet expansion

Meanwhile the bear case scenario looks like this:

- US economy goes into second effective shutdown as death rates follow hospitalisations

- Consumer confidence slumps

- US economy stalls as the market loses confidence in policy-makers’ ability to do enough

- Growth stock premiums begin to unwind

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Pendal has announced a new appointment to its Bond, Income and Defensive Strategies (BIDS) team.

Philip Treharne joins the team as a Quantitative Analyst from July 20.

Philip is a highly skilled quantitative researcher and investment analyst with extensive experience in portfolio management, research, modeling and trading.

In a previous role as a senior investment analyst at a systematic investment fund Philip specialised in strategy development and portfolio risk management.

Philip holds a PhD in Applied Maths from Cambridge University in England.

At Pendal Philip will reunite with another recent BIDS team appointment, volatility analyst Thomas Ciszewski.

The pair, who worked together at Deutsche Bank and SouthPeak Investment, will collaborate on key initiatives to ensure Pendal’s BIDS products are optimised for the new economic and market environment.

These appointments mean the BIDS team now operates with a dedicated equity volatility skillset.

Philip will report to Vimal Gor, Head of Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Which fiscal factors will impact investors in the months ahead? Here’s a quick snapshot from portfolio manager Tim Hext (pictured) of Pendal’s Bond, Income and Defensive Strategies team.

MELBOURNE’s second virus shut-down was the story of this week — and will no doubt cause slower-than-expected growth this quarter.

An increase in cases was expected as economies re-opened, but the speed with which this wave hit parts of the Victorian capital was a surprise.

Nevertheless, unlike the massive initial shock in March, markets barely skipped a beat.

Equities saw some moves within sectors, especially those exposed to the Melbourne economy. But overall equity and bond markets were almost unchanged.

The government will again play a key role in buffering the impact.

We have written a lot in recent months about the transfer of economic control from monetary to fiscal policy. Economists have turned their gaze from Martin Place in Sydney to Langton Crescent in Canberra.

A number of key markers will be laid in the months ahead. JobKeeper and JobSeeker are due to end in late September. We expect more colour in the weeks ahead on how they may be extended or adjusted.

Then a budget is due in October. The need to encourage investment should see more aggressive schemes and tax breaks introduced.

The big fiscal question is whether tax changes will be brought forward. The government has two big tax cuts scheduled for July 2022. The 19c tax cap is due to be raised from $37,000 to $45,000 and the 32.5c cap from $90,000 to $120,000.

This would bring significant tax relief to most taxpayers. Given the current environment these could be brought forward.

Another, more controversial tax cut is due in July 2023. This would establish a single tax rate of 30c for $45,000 to $200,000 — a massive cut for middle and higher income earners. Whether the Senate agrees to bring this one forward may be more controversial because it favours higher income earners.

Tax cuts would put more money in taxpayers’ pockets. But would they have the confidence to spend it rather than save it?

As always, lower income earners have a much higher propensity to spend — so it could be argued keeping JobSeeker at a higher level beyond September would be more help.

Other ways of injecting activity into the economy may be more difficult, short of handing out coupons rather than cash. Infrastructure is already operating at capacity and housing will not be helped by the static population.

Either way fiscal policy will be left doing the heavy lifting.

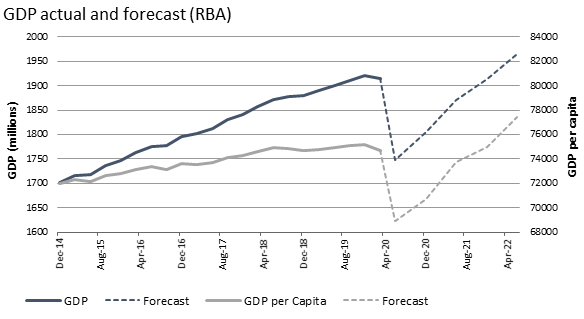

Graphic: Bloomberg

In regard to bonds, we continue to watch the massive excess capacity gap and attempts to close it.

The RBA expects GDP output to take until mid-2022 to return to pre-crisis levels — but even that looks optimistic.

Inflation will see the first negative annual print since the 1960s in late July. It will bounce back, but when combined with wage freezes, low population growth and sluggish housing, the medium-term outlook is not promising.

We remain comfortable that bonds will continue to do their defensive job in portfolios.

Tim Hext is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

Pendal’s head of equities Crispin Murray (pictured) outlines how the US experience with COVID-19 and the latest vaccine developments are impacting the outlook for Australian equities.

Quick take-outs

- Despite negative sentiment from increased COVID-19 cases, equity markets continued to rise

- Economic data has been supportive, but there are early signs of a slowing in the V bounce

- We’ve seen some positive vaccine news flow

- Locally it’s an important week for sentiment with the risk that stocks leveraged to economic recovery could be impacted by the Victorian lockdown

As bad as it feels with the negative news flow around rising COVID cases in Australia and parts of the US, the market hasn’t responded as some may have expected — and has continued to grind higher. We are now at a juncture where:

- We could see a more significant leg down if case load data continues to worsen;

- But if evidence emerges that virus management has improved, we could get squeezed higher — bearing in mind that overall market positioning has turned more defensive.

Our portfolios are positioned defensively — but not aggressively so. We have stated several times in this weekly Australian equities note that a balanced portfolio with a good mix of recession insurance and recovery plays is very important in this unpredictable and fast-moving environment.

US Economic data surprises to the upside — but there’s evidence of the V stalling and no improvement in US case numbers

Published economic data continues to be positive.

Jobs data is strong, which has supported the market. On the employment front “Hours Worked” (+8.3%) and “Household Employment” (+6.6%) surprised to the upside. Similarly, the PMI diffusion indices are heading in the right direction indicating a stronger growth momentum than many anticipated.

We are now looking at an 8% drop in US Q2 GDP versus an 11% to 12% drop — as most estimates suggested we were facing a few months back. Still a lot to make up, but significantly better. Clearly interest rates will continue to be supportive.

However there is still some evidence that things are slowing. Markets must gauge not only the economic effect of the lockdowns, but a perception of risk that is deterring consumer spending.

A recent University of Chicago study concluded that sentiment — rather than the lockdowns themselves — are the biggest headwind. We know that only around half of the stimulus has been spent so far. This is something to keep watching in the US and Australia.

There are signs of this slowdown coming through in the last week in the worst-affected states of Florida, Texas, California and Arizona — which make up about a quarter of the US population. Restaurant bookings in the Open Table app tapered off quite sharply last week after a post-lock-down recovery.

Cases in the US continue to rise and hospitalisations are increasing — though they remain below the previous peak and deaths are still low. In Florida overall numbers are worse, though there is less strain on hospitals. In contrast, Phoenix and Houston are close to ICU capacity. We are now seeing “surge plans” implemented in many of these cities such as LA, including the deferral of elective surgery.

The data shows some smaller US states have seen improvements — but not the major states such as Florida, Texas and California.

Vaccine news flow is positive

One positive consequence of rising cases is the acceleration of some Phase 3 trials. There is some talk of the first batches being available before year-end.

The three main trials are:

- Moderna

- Aztrazeneca (in partnership with the University of Oxford)

- Pfizer (four variants of a vaccine in development)

Pfizer has just released results of Phase 2 trials on one of its vaccines, which indicate a) the drug is safe to use and b) it is triggering an immune response. This means it can progress to the final Phase 3 trial, which will be 30,000 patients. The rate of new cases actually helps determine the efficacy of the vaccines.

In the best-case scenario, the drug will be approved by October. Pfizer estimates it could produce 1.2 billion doses in 2021, which would equate to 600 million treatments. This shows the problem likely will not be solved by a single vaccine. To meet demand we will likely need several vaccines to be approved.

Pendal portfolio manager Amy Xie Patrick outlines the outlook for bonds and explains where to look for fixed income opportunities in this interview with online business channel Ausbiz.com.au.

Watch the video above or read the transcript below.

TRANSCRIPT

AUSBIZ.COM.AU INTERVIEWER: In the never-ending chase for yield, our next guest Pendal portfolio manager Amy Xie Patrick, is warning investors not to get spooked. She joins us live in the studio. Great to have you here. It’s a really interesting spot that we find ourselves in right now. We know of all the potential dangers, all the potential risks out there. But it’s as if is if there’s FOMO forcing people into equities as people are looking for a return that is hard to find.

AMY XIE PATRICK: Absolutely. I think you’ve hit the nail on the head. Is it because people want all this extra risk in their portfolios right now? I don’t think it is. The risks are well known, but the outcomes of those risks are still highly uncertain as it’s to do with the fact that we’re in a zero-interest rate world.

For most major jurisdictions in this world, policy rates are as low as those policy-makers feel they can go. In the search for return income yield, you have to grab whatever you can. I don’t think it’s so much that people want to go further out the risk curve, but we’re being forced to. When you come out of a crisis, you tend to be more risk-averse and thinking about saving for the future.

But when I put my savings in term deposits or my savings account, it gives me nothing. And I’ve got to think about my children, right? So how do I get some return out of that saving? I’m pushed further out the risk curve and the savings glut that the world was facing before.

AUSBIZ.COM.AU INTERVIEWER: Amy, the fixed income world is large and very wide. Where would you be investing in this type of market at the moment? Corporate bonds and investment-grade high yield, how would you be playing them?

AMY XIE PATRICK: There’s a great range of thought on this. The majority of the consensus seems to be that you need to chase more yield and government bonds simply don’t give you that much yield anymore.

You need to turn your back on them and go further out the risk curve — especially with the fed buying not only investment-grade debt, junk-rated debt and fallen angel debt. People feel safer going down the risk curve that way.

I would just caution against chasing risk too much down the quality ladder because, at the end of the day, the economic crisis and health crisis is still in full swing. It may mean chasing good headline income now, but what if those bonds default and they don’t pay you any income at all in the future?

You only need to look as far as Japan and Europe to see that just because yields start from a low point, doesn’t mean that they can’t go lower. The power of duration in fixed income means that if you buy longer-dated bonds, you get that beautiful multiplier effect as yield goes lower as well.

AUSBIZ.COM.AU INTERVIEWER: When it comes to Aussie 10-years now we’re seeing record lows. It’s trading at 0.9, 0.92%. Can it go lower?

AMY XIE PATRICK: A year ago, two years ago, the exact same conversations were being had right at 1.5%. Can they possibly go lower? You know, at 1%, can they go low? Well, they did go lower, so we’re just back around that one percentage level. A lot of people’s arguments with longer-dated bond deals and the reluctance to chase them because they think they can’t go lower.

It’s purely because a lot of central banks rightly or wrongly feel that at the zero bound that’s enough, they can’t deliver any more rate cuts. But if you compare the current episode to what happened in the global financial crisis, this hit to economic activity has been far worse than what happened in the GFC.

And yet the number of basis points of cuts that central banks have delivered have been so little compared to what they were able to deliver in the GFC.

Even though zero cash rate sounds like a really easy monetary policy setting. Actually, it might not be that easy. It might actually still be quite tight. And as long as policymakers don’t want to inject extra fiscal stimulus we’re locked at this zero lower bound at the front. How can long end yields really sell off meaningfully?

And then what if we get another shock? Even though lots of people say with yields so low, the asymmetry is actually that yields go higher. With all these risks, the asymmetry is probably still lower.

AUSBIZ.COM.AU INTERVIEWER: I’m curious to know when it comes to central banks when you hear the FOMC when you get minutes from the RBA, what is it that you zone in on to help form your view of where bond opportunities could go and where opportunities in fixed income could lie?

AMY XIE PATRICK: I think you just have to take them at face value. The consensus is deafening right now especially with the market rebound, equities are roaring up.

I think there’s a lot to hold central banks back right now. Not to say that they’ll always be held back, but for me, the more medium-term risk is not so much what the central bank says, but what our governments say.

Will this fiscal stimulus be with us for as long as the economy needs or will there be this urgency to claw back to some kind of fiscal discipline again? Will all that fiscal stimulus get withdrawn right before the economy gets traction in the recovery trajectory? And what happens then?

So it’s not so much reading what the central bank has said, because quite frankly what they say right now is fairly boring. They’re saying that we’re at zero, we’ve done as much as we can. Fiscal, please take over.

Amy Xie Patrick, Portfolio Manager – Bond, Income, and Defensive Strategies team.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

What is the outlook for retail REITs in a post-COVID world?

Should retail landlords charge rent based on a tenant’s turnover?

Pendal portfolio manager Julia Forrest tackled this hot issue at The Australian Financial Review’s Retail Summit on June 26, 2020.

Watch the video above.

Julia Forrest is a portfolio manager with Pendal’s Australian Equities team. Julia has managed Pendal’s property trust portfolios for more than a decade and has 25 years of experience in equities research and advisory, initial public offerings and capital raisings.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/