Here’s the latest outlook for Australian equities from Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

CONCERNS about a material second wave of COVID-19 infections have increased over the past week. This reflects a rise in cases in some parts of the US and other countries.

Here in Australia the spike in Victorian cases needs to be watched. Although small in number it may challenge the theory of a faster re-opening here.

The market rose +1.6% last week despite these issues emerging. This was driven by continued constructive economic data and optimism on further policy support. There was some rotation back to growth — the market sees value stocks more at risk in a potential second wave.

Second-wave risks

Concerns of a second wave are focused mainly on the US. However there are also clusters in Beijing, Germany, and an acceleration of cases in Latin America and India along with an increase in Victorian cases.

The issue from the market’s perspective is the degree to which this will impede the recovery. We think it unlikely the US will return to a broad lockdown, but targeted restrictions will limit some activity. The larger risk is the possible negative effect on consumer and business confidence.

This is a critical test of the US’s ability to absorb periodic increases in infections. If it can be managed, this may begin to build further confidence.

The headline numbers from the US are not encouraging. New daily cases have almost returned to where they were at the previous peak. The concern is this may lead to more hospitalisations, more stress on ICU units and more deaths.

Increases in US cases are concentrated in certain States. For example, Texas has seen cases double in the last few days while Florida is experiencing new daily cases at double the rate of its peak. Declines continue in north-eastern States that were hit hard earlier.

At this point hospitalisations are not picking up on a nationwide basis. The increases in Texas and Florida are not at concerning levels.

Since the previous peak a number of medical developments have emerged — notably awareness of the importance of anti-coagulants and steroids which can help reduce the severity of cases. ICU capacity has also increased.

The key issue to watch this week is whether the combination of much higher testing, physical distancing and better care prevents a significant escalation in severity.

While the uptick in Victorian cases is relatively small in number, it may be highly significant for the market. The consensus view is that disease has been successfully suppressed in Australia, which has led to a more optimistic view on the Australian economy relative to other countries.

If people start to expect restrictions around the country will remain in place longer than first thought, it will have a meaningful impact on market optimism and positioning within it.

Economy

Economic data remains constructive and is doing enough to offset burgeoning concerns over a second wave at this point.

Indicators out of the US remain strong. This partly reflects the fact that the north-eastern States so far avoiding a second wave make up a larger part of the economy than those facing the need for potential new restrictions.

Last week’s US retail sales data were better than expected. The Citi economic surprise index – which tracks the outcome of various data points versus expectations — is at its highest level in 18 years.

In Australia employment data was also better than expected. Monthly hours worked fell -10% from March, versus the -15% to -20% that the market had predicted.

Valuation versus liquidity

Liquidity is helping prop up the market despite more negative news – and is trumping concerns about near-term valuations.

The Fed and other central banks have pumped money into the system, most of which has found its way into cash and bonds.

This is reflected in the surge in FUM in retail money market funds. There has also been record issuance of investment-grade and high-yield bonds.

The overall market position has become more a neutral than a supporting factor. But it is far from a headwind. The liquidity program has allowed access to capital so companies can sort out their balance sheets and become more resilient.

Crispin Murray is Pendal’s Head of Equities. He has more than 27 years of investment experience and a strong track record leading Australian and European equities funds. He manages a number of our flagship funds along with one of the largest equities teams in Australia.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

What are the different ypes of sustainable investments, how did they develop and why are they growing so quickly? Pendal CEO Richard Brandweiner explains in this Lonsec webinar from June 10, 2020.

Watch the video above or read the transcript below.

RICHARD BRANDWEINER: Sustainability is a particularly relevant topic right now for many reasons.

This is not just because of what we’ve experienced recently through bushfires, floods, famine — and the perspective that the economy is intrinsically linked to these events and our behaviours.

But also because regulators around the world and people are starting to evolve and adapt and change.

Your clients — and yourselves — are starting to buy goods and services based not just on what a company does, but how they go about doing it.

These are fundamental shifts in our psyche that are underpinning a wholesale move towards greater thinking about how we invest.

I’d like to take you on the journey of how we’ve got here and how we’ve evolved in the investment profession from “ethical investing” all the way to “impact investing”.

Then I’ll give you some thoughts about how we at Pendal are adapting to that and have adapted to that over many years.

Then I’ll put that in perspective around the latest development — positive impact.

Ethical investing — where it started

This all really started years ago as ethical funds began to emerge in the 1980s and 1990s.

The idea of “ethical investing” then was very much about values. It was mainly church-based or faith-based groups investing in ways that were aligned with their moral code or their values.

It was really about screening: about not owning tobacco, not owning gaming, not owning other types of companies that do harm.

Externalities

This movement grew in the first part of the 2000s around the concept of “externalities”.

Externalities is an economic concept that refers to an activity’s second and third-order effects on the broader ecosystem.

It is best illustrated by an economic problem known as “the Tragedy of the Commons”, which was first talked about in the early 19th century by an English economist, William Forster Lloyd.

Lloyd observed that if I graze my cattle on common land, it’s in my interests to put more cattle on the land. But if everyone did that, acting in their own best interests, the external impact was the devastation of the land for everybody.

So there was a conflict between your internal motivations and what’s best for society — and ultimately for you in the long term.

Now we recognise pollution is an externality. We recognise supply chains generate externalities. Even employment generates externalities.

Little by little, as we became more sophisticated, we understood you could measure those externalities — and they weren’t free. The costs were borne by society.

As regulation evolved and as we became more aware of externalities, it became clear they ended up affecting your earnings over time — as regulations shifted or consumer demand changed.

And that ultimately leads to a change in your cost base.

A good friend of mine from asset consultant Willis Towers Watson wrote a wonderful article that said “past performance is not even a good guide to past performance”.

What he means is the performance of stocks and securities over a period of time is not fully reflective of the true, intrinsic earnings of those companies — because they didn’t factor in a lot of the externalities those companies were generating.

A good example is tobacco.

Tobacco was the best-performing sector in the world over the last century. I don’t think that will be the case over the next century. But the reason why it performed so well in the past is that as a society we didn’t understand the externalities.

We didn’t understand the impact of the products being sold. We weren’t factoring that properly into an assessment of the companies.

Environmental, Social and Governance (ESG) factors

So the United Nations principles for Responsible Investments grew and the emphasis on this new idea of ESG — environmental, social and governance criteria — became an idea around long-term risk management.

ESG recognised that if these externalities are real — and if we expect over time they will be increasingly factored into the price of securities — then as investors we should start thinking about these factors now.

It wasn’t about values. It wasn’t about what you believe is right or is wrong. This evolution from ethical investing to ESG was in its early incarnation about long-term risk management of making an investment decision.

Sustainable investing

Then things evolved another step.

We recognised these externalities — these second and third-order impacts — were real. And as investors we recognised the potential to build portfolios in a way that was more sustainable and recognised the impact of these externalities.

We could build a “sustainable portfolio” that not only managed ESG risks and factored them into the pricing of securities. It could also bias a portfolio towards more sustainable companies or sectors over time.

Why might you do that? There are two reasons.

You might believe there’s an alpha source there. You might believe those sorts of companies will perform better over time.

As consumer behaviour changes, they’ll be more attracted to products and companies that are sustainable. Companies that are less sustainable will actually do worse over time.

The other reason is because you want your capital to be invested in positive ways.

This is happening more and more. Sustainable investing is one of the fastest-growing parts of the investment management universe.

About nine out of 10 Australians in recent Roy Morgan research have said they expect their investments to be managed in a sustainable way.

That is something we really can’t ignore.

Impact investing

But there’s a final step to this — and that is impact investing.

Impact investing not only recognises those externalities, it deliberately builds a portfolio targeting the creation of positive externalities.

It’s not simply asking: “is this a sustainable company in a sustainable industry?” It’s recognising a company can generate very positive and profound outcomes for the world.

Impact investing is about targeting those sorts of investments and then measuring the outcomes beyond the financial returns of the company.

Impact investing is the point of the arrow. This is the bit where we actually recognise that capital has real power and that all of us — financial advisors, fund managers, asset owners — are in a very unique position.

We are in a position of responsibility. A position to operate as fiduciaries recognising the way we invest matters.

There is a purpose to our financial system. The purpose is not money in its own right. It’s not an end in of itself.

The purpose is to channel capital towards productive enterprise and to create our future.

There’s about $130 trillion globally that sits in pension funds, super funds, sovereign wealth funds advised by financial advisors, fund managers, insurance companies. That’s almost twice the value of annual global GDP.

The way that money is invested will help shape the world that your clients and you and me will retire into.

That makes impact investing hugely important for us as fiduciaries, advisors and allocators of capital.

This is about our growth as investors — as humans recognising the world is not two-dimensional. It is a complex, adaptive system.

The third axis

We can think of this as the third axis of investing.

In the beginning there was one axis — returns. Back in the 1940s and 1950s we really only spoke to our clients about the returns we generated.

Then with modern portfolio theory the idea of risk emerged and we had two axes — risk and return.

Today it seems like madness to think about return without understanding the risk we’re taking to get that return. But it was always there — we just didn’t measure it.

Now we realise there is a third axis — the impact of the investment or the company or government we are lending money to.

Again — the third axis was always there. We just didn’t measure it like we are starting to do now.

Pendal and Regnan

We helped found an organisation called Regnan, which is now one of the leading ESG research and engagement providers in Australia.

Regnan’s business originated with work done in conjunction with Monash University in Melbourne in the 1990s to think about the impact of environmental change on company earnings.

Recently, Pendal bought out our other Regnan partners to bring it a lot closer to our investment decision-making.

We’re now using Regnan to grow the impact investing space.

We recently launched a product called the Regnan Credit Impact fund, which lends money to investment-grade borrowers, governments, super nationals and corporates for green and social bonds. Then we measure the outcomes of all that lending.

Even at launch with a small initial seeding of $30 million, the fund is already taking something like 13,000 tons of carbon dioxide out of the atmosphere on an annual basis.

It’s restored 60 hectares of forests.

It’s generated 16,000 megawatts of renewable energy a year.

It’s provided 340 jobs.

It’s created 50 loans to female-owned small enterprises.

And all of that with high-quality, investment grade credit paying strong returns.

So you’re getting liquidity and high-quality, investment-grade credit. And at the same time these externalities are being measured and targeted.

For us, that’s a huge leap.

Pendal sustainable funds

Pendal offers a range of sustainable products across different asset classes. We have been doing this for a long time and they are well-rated.

- Pendal Sustainable Balanced – Est. 1984 – Diversified/Multi-Asset

- Pendal Sustainable Conservative – Est. 1989 – Diversified/Multi-Asset

- Pendal Ethical Share – Est. 2001 – Australian Equities

- Pendal Sustainable Australian Share – Est. 2001 – Australian Equities

- Pendal Sustainable Australian Fixed Interest – Est. 2016 – Australian Fixed Income

- Pendal Sustainable International Fixed Interest – Est. 2016 – International Fixed Income

- Pendal Sustainable International Share – Est. 2016 – International Equities

- Pendal Sustainable Future Australian Shares SMA – Est. 2018 – Australian Equities

Regnan funds

This year we are launching high-impact investment strategies globally under our Regnan brand:

- Regnan Credit Impact Trust – Est.2020 – Australian Fixed Income

- Regnan Global Equity Income Solutions – To be launched in late 2020 – Global Equities

Richard Brandweiner is Pendal’s Chief Executive Officer, Australia. Richard has more than 20 years of experience in investment management and is responsible for the Australian arm of Pendal Group, including asset management, operations, sales and marketing.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

Murray Ackman, Anna Hong and Thomas Ciszewski (l-r) have joined Pendal’s Bond, Income and Defensive Strategies team

PENDAL’s Bond, Income and Defensive Strategies team is excited to share details of three new appointments and a promotion.

The new hires will focus on areas of growth in the boutique and support our ambition to be a leader in Environmental, Social and Governance (ESG) fixed income investing while providing objective-based income solutions and defensive strategies.

Assistant Portfolio Manager

Oliver Ge, a portfolio analyst who has been with the team for six years, has been promoted to Assistant Portfolio Manager in recognition of his increased experience and responsibilities.

Volatility Analyst

Thomas Ciszewski has been appointed a Volatility Analyst. He will work on the Active Long Volatility Strategy Fund as well as structuring defensive strategies across a range of funds. Tom joins us from SouthPeak Investment Management where he successfully implemented volatility risk premia and delta one strategies. Prior to this Tom held a number of positions in a trading capacity for Deutsche Bank in Hong Kong and Sydney, managing global equity derivatives, delta one, ETF and cash facilitation trading teams.

Tom has also worked in Chicago for Actis Capital as an equity options Volatility Portfolio Manager. He holds a Master of Applied Finance with a focus in derivatives valuation, exotic options and risk and portfolio management from Macquarie University, Sydney. He also has a Bachelor of Arts in Economics and Business Administration from the University of Vanderbilt, Nashville.

Assistant Portfolio Manager

Anna Hong is joining the team as an Assistant Portfolio Manager working on the Australian Composite and Cash Funds. She is currently a Portfolio Manager at Uniting Ethical Investors for their enhanced cash and fixed income funds. Prior to this Anna held positions at BlackRock and Challenger and was responsible for investment analytics and quantitative solutions. Anna holds a Master of Business Finance from the University of Technology, Sydney and a Bachelor of Science in Mathematics from the University of New South Wales.

Credit/ESG Analyst

Murray Ackman has been hired into the team as an ESG Credit Analyst. He will work across our range of credit funds with a particular emphasis on Pendal’s new Credit Impact Fund (CRIMP). Most recently Murray worked as an independent consultant for Australian private equity firms reporting on ESG measurements of Australian companies with less than $1 billion market cap.

Prior to this Murray was a Research Fellow at the Institute for Economics and Peace where he led research for the Institute on SDGs, violent extremism and engagement with business which included projects determining the strategic priorities and direction of clients such as UNDP and the OECD. Murray holds a Bachelor of Arts in Politics and International Relations, a First Class Honours degree and a Bachelor of Law specialised in International Law from the University of New South Wales.

Finally, Arpit Mathur, one of our quantitative analysts, has resigned to join a friend’s business. We wish him well for his next role and thank him for his contribution and the hard work he has given Pendal.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Contact a Pendal key account manager:

https://www.pendalgroup.com/about/our-people/sales-team/

How will the journey from deflation to inflation impact portfolio construction, defensiveness and income in this zero-rate world?

On May 28, 2020, Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor and senior team members Amy Xie Patrick and Tim Hext and outlined the implications for investors in their half-yearly “Lighthouse Series” live webinar.

This is a recording of Amy’s presentation which addresses fixed income investing in a zero-rate world.

Watch the video above or read the transcript below.

This presentation will focus on what bonds are supposed to do in your portfolio.

What do we want from our fixed income portfolios and how do we make sure that in this disappearing yield world, your fixed income allocation is still able to do the jobs that you need it to do?

Looking at the chart below, this really is what underlies the income problem we are all having.

What we’ve shown here is starting yield at the beginning of every crisis you’ve had since the tech crash in 2002.

In the yellow bar is the starting yield in Australian government bonds. The 10-year part of the curve.

In the purple is the US. Obviously what happens in Australian yields is governed quite a lot by what goes on off shore as well.

Now, time and time again, and especially in the more recent crises, you’ve seen that all these yields have come down and it’s a structural trend that’s been happening for a long time.

But what it means is that at the beginning of every crisis, we’ve got seemingly less and less room to play with.

So a lot of investors that we’ve spoken with, not just over this most recent period, although this most recent period has clearly accelerated things further, but over the last three, four, five downmarket cycles in equities, what use really is bonds to me, when yields are this low? Can bonds still be defensive?

And the answer to this is, even through that period in 2018, when the Fed was incredibly belligerent about that hiking cycle, when push came to shove, when you saw stress in the equity markets that negative correlation still comes through.

But what’s really obvious at these very low yields is that there’s just a glaring asymmetry in terms of where yields can go. Not to say that we don’t think they can go into negative territory.

Quite clearly they have gone into negative territory in certain parts of the world, but with yields being quite so low, what we say is that now more than ever, you need your fixed income allocation to be constructed in a very active way.

Active not only in terms of the direction that you face, and whether you’re long or short bonds, but also active in the way that you think about your overall fixed income portfolio composition as well.

Now, as yields have come all the way down, the role of fixed income is to be a defensive part of your portfolio, but it’s also supposed to generate income, because led by risk-free yields, income levels have been coming down across the world, what you’ve seen is our response to it, which has facilitated this to happen.

The chart bellows illustrates the growth in global debt, that’s been issued mostly by way of bonds through a multiple of different sectors.

As you can see, post the GFC debt was growing all over the world anyway, during the GFC, but post the GFC, you had a massive shift down in global rates equilibrium.

And all of a sudden, you had this massive savings glut.

It’s normal to see savings books come out at the end of every crisis, every pandemic, and every war.

And so all of these were looking for yield and income — at first relatively safe and good yield and income, but eventually as yields continue to fall, we look for more and more.

Most of this debt expansion in the world has been taken up by corporates, not so much government debt.

Government debt has obviously grown as well, but a lot of the growth in bonds and bond debt that we’ve seen in the world has essentially been us investors saying to these corporates, please give us more. Please issue more and more because we have certain return targets, we have certain income targets.

If it means that we need to be holding less high quality portfolios, if it means that we need to reach further out on that liquidity and that risk curve, then so be it.

Probably for most investors that consideration of having gone down the quality spectrum, isn’t front and centre in their minds, because that is buying the overall return hurdle or that overall yield hurdle has been front of mind.

A key problem with the way that fixed income portfolios shifted in the pre versus post GFC era. In the pre GFC era fixed income was largely considered to be a purer asset class. The dominant sub asset class of your fixed income piece was really high quality government bonds.

But obviously as yields continue to drift lower, they don’t offer you enough income. They don’t offer you enough yield. So you reach further and further up the curve and off shore, especially what you’re seen is that investment grade no longer is synonymous with that same high level of quality that you used to see before the GFC era.

Now that means a very important key difference in terms of the way your fixed income portfolio behaves. In the pre GFC era when investment grade as an asset class was truly viewed as quite a safe haven asset class. What you saw in times of equity market stress was slightly negative correlation to equity markets.

So investment grade belonged with that high-quality government bucket in terms of offering that safe haven portfolio, that safe haven allocation. But now, as we have seen, these investment grade entities become victim to this quality drift, this ratings drift down the quality spectrum.

In the post-GFC era, what you get with investment grade credit is actually positive equity beta, and on top of this, what a lot of global asset managers also been happy to do is to harvest more carry, more yield, more return in their portfolios, by sacrificing liquidity in those portfolios.

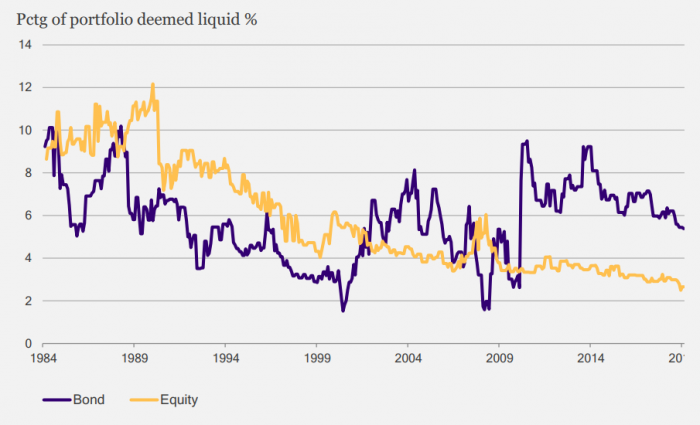

Here on this chart, what we show you is that both in equities portfolios in the yellow line and your bond portfolios, asset managers have generally not prioritised liquidity. Apart from when the crisis hits like the GFC you can see in the purple line all of a sudden managers go to the defensive part of the portfolio, that fixed income part of the portfolio, looking for liquidity.

And it’s not there.

It’s a wake-up call to go back and restore liquidity in that part of their portfolio. But again, since that crisis was a long time ago, this longer term trend of wanting to sacrifice not only quality, but also liquidity in their portfolios, has polluted traditional fixed income allocations with more and more problems as time goes on.

Now, all of these problems with going down the quality curve, and going up the liquidity curve is all the more exacerbated in Australian portfolios. And on this next slide what we show you on the left-hand side, how much Australia remains a global outlier in terms of just how much we don’t like fixed income.

We see no use for it in our portfolios, we like equities and we like property.

And so the key point to make here is that even within that small fixed income piece in the average Australian portfolio, what most investors probably don’t realise or don’t want to think about too much, is how much of that truly behaves like fixed income and how much of that has morphed slightly into the land of equity beta.

And then to the portion that is truly pure fixed income, that is truly defensive, how much of that is really active?

Portfolio Construction within Fixed Income

We mentioned that when yields are this low, you need that active lever to be able to pull, because of that asymmetry, in where yields can go when they’re this low. If all of that pure fixed income allocation is in passive, then you’re not really able to retain a very nimble fixed income portfolio as uncertainty remains quite high.

So in Australia, I think we have an even bigger conflict within ourselves. On the one hand our portfolios, the way we position them, tell us that we want risk, and not so much for the sake of risk, but we want returns, we want yield.

But then when crises hit, we complain that our fixed income allocations don’t do the job that they’re supposed to. But all the while we’ve positioned them to look more and more risky.

So all of that is probably a big spoiler to how I’m going to talk about the way that we approach constructing fixed income portfolios. Particularly with this idea of wanting to test this by a certain threshold in this very low-yield environment.

Now, necessarily we look at fixed income buckets along this risk-reward spectrum like everybody else.

But we do pay a lot more attention to what is the inherent liquidity characteristics of each of these buckets of fixed income.

Because yields are so low, high-quality government bonds, their main job in your portfolio these days, while they do still exhibit some positive carry, because that traditional sense of being able to get, carry and roll out of a pure government bond portfolio is long gone and we don’t think it’s going to come back any time soon.

So high-quality government bonds live in your fixed income allocation, not because they’re your primary yields generator, but because they still act as that defensive part of your portfolio, that pure fixed income part of your portfolio.

So naturally you go up the risk spectrum a little bit, but you stay in what we think is quite important to prioritise -good quality investments. So when you go into the land of corporate credit, while acknowledging that these days, by going into investment grade credit you are naturally taking on more equity beta, nevertheless, you need that allocation to be as high quality as possible.

Why? Because if you’re constructing a fixed income portfolio, presumably you want to be able to rely on that income. And if you’re putting a lot of, let’s say hybrids, into this part of the portfolio, well hybrids aren’t fixed income, bank hybrids exist in the part of the capital structure so that the bank can access that capital when they most need it, and when they most need it, is probably when you, as the security holder, wants your income the most.

And it’s when they’re most likely to switch off the coupons on those hybrids.

So as you go out the quality spectrum, the less you can count on that stability of income from those assets. So here being high in quantity really does matter. High in quality in this piece though, one point to stress, not because you think that this is also supposed to provide you liquidity in times of crisis.

Since the GFC, we haven’t really been able to find liquidity anywhere further than high-quality government bonds anytime the equity market’s been through significant stress. It’s just not the way the world works anymore.

Liquidity in terms of secondary market trading liquidity, all those incentives by banks to provide that liquidity has significantly changed, because of the GFC and all the banking regulations that have come on board since the GFC.

Because yields are so depressed because spreads have been crunched before this Covid crisis you naturally had to reach out that quality spectrum further and go into the land of maybe high-yield, maybe offshore, maybe loans.

A lot of investors talked to us about liking private debt, because there’s no live mark to market. So it seems like it’s not very volatile. I think all of that comes with very obvious risks.

But here we say that when you’re reaching for the higher risk assets, while acknowledging that you need boosters in your portfolio, be mindful of how much that makes up of your overall fixed income allocation.

You want it to complement not dominate your fixed income portfolio.

And more of the point you want to be able to implement it in such a way that when you start to get concerned that the market’s are no longer benign, that you can turn this off very quickly.

So, when push comes to shove, do I want to sacrifice liquidity for quality or quality for liquidity?

I would argue that when constructing an income portfolio and you’re going out the risk spectrum, you actually need to prioritise liquidity.

What are the Opportunities?

Crisis brings about dislocation. One of the areas that we do prefer is Australian investment grade.

On the table below very simplistically illustrates the current market spreads in each of these major fixed income asset classes from Australian investment grade, to US investment grade, emerging market sovereigns and US high yield.

What is the implied five-year cumulative default rate at current spreads?

As you can see Australia is a massive stand-out. What this chart is really telling you is that the sell-off we’ve had is about liquidity premiums spiking. It’s about everyone wanting to hoard cash.

It’s not necessarily the case that the market is pricing market genuinely thinks that in Australian investment grade 10% of the index is going to default in the next five years.

Relative to the worst-realised default rates in the history of each of these asset classes Australia clearly remains a stand-out. And unlike some of those offshore investment grade indices, we’ve not seen quality drift to nearly the same extent in Australian investment grade.

Another one to highlight on this slide for us is emerging markets sovereign.

It does belong in that higher risk bucket that we just showed you, but it retains features that are unlike corporate credit, and it’s worthwhile thinking about in terms of making your fixed income portfolio mix if you are going to reach for more risk in that way.

In terms of what’s implied for the next five years for default rates, very high compared to the worst that’s ever been realised in emerging markets.

But to highlight a point, which is perhaps misleading, just because the spreads are so high, is US high yield. Trading around 600 basis points at the moment. Seems amazing in a world of zero rates and cash rates…

But what we see on the left or the right hand side of the slide is that just taking it on face value, Moody’s base forecasts the US high-yield default rates, you can see that even though the market’s widened out a lot, for their base case, and even their optimistic case default rate forecast, the market hasn’t moved nearly enough.

Not nearly enough risk has been priced in and similarly when you look at current breakevens to see how much cushion in available there simply isn’t enough for the potential risks.

Markets have already moved a lot and at current spreads they’re forging another level of cushion. Different thickness of that cushion in different markets, again in Australia, particularly attractive.

And when you compare that with what’s the typical end cycle, move that whole widening move in all of these asset classes in previous historical cycles, you can see relative to what’s going on in the past, what we’re currently going through right now, break evens that are currently embedded look quite attractive, especially for Australian investment grade.

And the last exercise we did here was just taking the most liquid representation of Australian investment grade, which is iTraxx, to look at previous episodes of crises and say, nobody can time getting into the markets at the wides, but let’s say after the first say, 100 basis points worth of widening in that index, had you gone long then, in the GFC, in the European sovereign crisis, and after the China crash in 2015, what would your total return outlook have been like over the next three months, six months, one year and two-year?

And these returns are not been annualised, they’re just total returns. And it’s really just to highlight that outside of the GFC, on a medium-term outlook, these are incredibly attractive medium-term return opportunities to be looking at right now.

And the last point I wanted to highlight is just that, why don’t we think this is like the GFC?

In many ways, this crisis is worse. It’s involving the real economy. It’s a real sort of stop to the global economy and, questions as to whether the policies in place can reignite all of that again. But the crucial difference with the GFC is, in the GFC we had these key points of stresses, that largely pertained to our financial system, that we don’t see today.

And the reason we don’t see them today is partly because of all the regulations that have been put in place since the GFC, but also risk aversion is a little bit higher in the financial world.

So you’re not going to go through this protracted period of forced deleveraging.

This protracted period of forced deleveraging is really what caused those return protocols in the six months to one-year period in the GFC time for investment grade credit and credit as an asset class overall, to underperform for such a significant period of time.

If you don’t believe that the system needs to go through a disorderly and protracted period of deleveraging this time, and it doesn’t seem to be the case, then all the more reason to start engaging with investment grade, a bit more as part of thinking about your income solution.

So going back to my earlier point, because the mix of fixed income portfolios has naturally gravitated to taking on more and more risk, more and more positive equity beta, we’ve got to be cognisant that, all the while you have to be balancing that with still very traditional high quality government bonds and with yields this low, a very active approach to managing those government bonds.

Amy Xie Patrick is a portfolio manager with Pendal’s Bond, Income and Defensive Strategies team

Amy joined Pendal Group in February 2017 to focus on emerging markets and global credit indices. Amy is a Multi-Asset Fixed Income Fund Manager with extensive experience and expertise in emerging markets, global high yield, and investment grade credit.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

How will the journey from deflation to inflation impact portfolio construction, defensiveness and income in this zero-rate world?

On May 28, 2020, Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor and senior team members Tim Hext and Amy Xie Patrick outlined the implications for investors in their half-yearly “Lighthouse Series” live webinar.

This is a recording of Tim Hext’s presentation which addresses the end of the Central Bank era and what that means for investors.

Watch the video above or read the transcript below.

I’LL HIT the two key themes straight away, and then we can talk more about them.

The first one is that we are at the end of an era. And I’m calling it the era of the central bank. Central banks, as we all know and are now tapped out.

Rates are at zero. And from this, a new economic framework will emerge. Really we’re entering the era of fiscal policy.

The second thing I’ll be talking about is the fact that, of course, under that year of fiscal policy, it’s government, not central banks who need to step up.

My concerns, which I’ll talk a bit about, are the fact that I don’t think all governments are going to be in the mindset that we are in this new era.

And that some of the conventional thinking is going to slip back in as we come out of this immediate crisis. And what that will mean potentially a double-dip recession next year.

So let’s move on to what I’m calling the cult of the central bank.

Now cult might seem a strong word. I doubt we all worshipped our central bankers, but certainly for people like myself, we’ve been in markets for around 30 years, we’ve lived in an era where central banks have been front and centre of everything.

Now I’ve putting a picture of two US central bankers up there. I think Alan Greenspan loved the fact that he wants the high priest of the central banks.

I spent many an early morning trying to decipher what the hell he was saying.

So he certainly pushed that idea. I think Bernanke who ended up being sort of Superman through the GFC and saving the US economy, I put a quote showing he’s a little bit more circumspect about the role of the central bank.

But there is no doubt for all of our careers and I’m not just talking about our careers in markets, but the economic framework we’ve operated under, has the central banks front and centre. To sum it up in one line, the government outsourced cyclical control to central banks.

End of an era

The era of course is now over. It’s just a fact when you’re at zero rates, your arsenal of things you can do becomes very limited.

And there are a few little things they can do, but in terms of shifting the dial significantly, they are out of the game.

So it’s the end of an era. It’s an era from which we’re about to emerge, and we need to consider what the new framework looks like.

I’m just going to quickly recap what happened during that era, because it gives us a good understanding.

So the golden age of central banks, if you like was from ’93 to ’07. I use ’93 in Australia because that’s when inflation targeting came in.

Of course it came in slightly earlier in other countries, particularly New Zealand. Now under this era, fiscal policy was basically resigned to trying to balance the budget through the cycle.

Of course it would go up and down as the economy went up and down.

For the federal government, the two main things of course are taxation and welfare spending. So you would get surpluses and deficits.

But the aim of fiscal policy under this narrative was it should try and balance things through the cycle.

And it was left the monetary policy to be the accelerator and the brake under which we operated.

We had a nice framework targeting inflation and full employment.

And from that came all sorts of other ideas, which we sort of took as second nature and we started to believe were sort of almost like a natural order.

So there’s two concepts.

One was NAIRU, of course, where unemployment starts to become inflationary.

And the other idea was the idea of a neutral rate and I even heard people talk about it over the last 10 or 20 years as the natural rate of inflation.

And I think that speaks to the fact, a lot of people thought we’d finally landed on a framework, which somehow was a natural framework, that the economy was a bit like science.

It had rules that followed and here we had finally uncovered the magic on how to make it work for us.

Of course there was very good economic management through that period from central banks. They didn’t get everything right, but largely they did.

Two tailwinds

But what people only now really looking back realise is just how significant two tailwinds were.

The first was they were operating under very positive demographics.

We all know this story, that through the ’90s and into the Noughties, there was a massive increase in the percentage of the working age population.

Supply and economy was expanding and you could expand it under those circumstances. The second tailwind of course was globalisation, which was a massive move towards goods price deflation, which offset what you were seeing elsewhere. And you put those two together. And it was really the golden age.

As I mentioned, GDP in Australia, averaged 3.75 per cent through this period, inflation almost spot on the 2.5 per cent target, and I think everyone agrees it was a success.

And then of course it wasn’t. The GFC hit.

Now the GFC in a sense should have put some serious dents.

But two things happened. Firstly, fortunately for central banks rates were high enough that they could do massive interest rate cuts to help the economy in Australia.

It was almost 4 per cent worth of cuts.

The second thing, more offshore than in Australia, was the emergence of QE [Quantitative Easing].

The two of them together as we emerged from the GFC appeared to have solved the crisis.

So we entered the next era from ’07 to 2010 where the cult of the central bank in fact was strengthened, not loosened by the crisis.

It looked like they had saved the day. So as we entered this decade, we just finished, central banks were very much again front and centre.

But then the cracks started to appear. Not for a while, but they slowly started ekeing out here in the last decade.

We all know this story, but it’s just good to recap it. For a while there it looked like things were returning to the pre-GFC normal. That we could target growth about 3% and inflation at 2.5%.

What we found as the decade went on, of course, is that we just weren’t hitting those targets consistently.

And despite interest rate cuts, we just weren’t getting there. Fiscal policy should have been balancing. Unemployment was going down.

Yet we seem to have almost structural deficits.

Monetary policy, even though, there were numerous rate cuts through this period, inflation was going down, not up. But, and here’s the important part, the narrative was still held by everyone, including importantly to central banks. In Australia, the Reserve Bank kept forecasting that we were going to get back to these levels.

It was just going to take maybe a year or two years.

But right through this period their forecast always had inflation going back to 2.5% and GDP above 3%.

Of course, what followed were consistent downgrades.

So what started to happen in the second part of the last decade was a few question marks appearing.

Was there something structural coming on and you heard Phil Lowe talk about this.

Was it technology? Was it changes in the workforce that were causing these moves to happen? No one was quite sure. But what we started to see was the realisation that what was going on is far more structural than cyclical.

Now we’ve been going down this path for a long time and all the recent crisis has really done is accelerate it.

I wouldn’t say it’s the crisis we had to have because it did come completely out of the blue.

But in a sense it revealed these cracks, made them wider, and made the whole system come under severe pressure.

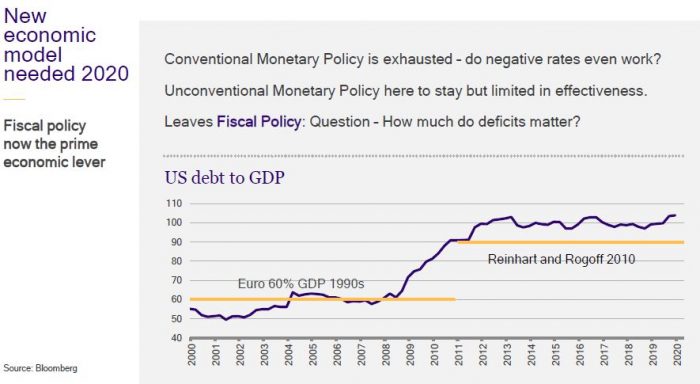

So there is no doubt that we need a new economic model.

Conventional monetary policy is exhausted.

Negative rates may be tried in some places. I think the Reserve Bank’s attitude in Australia is they don’t work.

They do more harm than good.

End of conventional monetary policy

So conventional monetary policy is over. Unconventional monetary policy – well, that’s here to stay.

There’s certainly a lot more they can do. You can expand yield control, you can do a larger QE. But really they are playing around the edges.

Remember the aim of unconventional monetary policy is just to bring term rates down because you can’t necessarily control them without directly controlling them towards zero. And that may yet happen, but that’s quite limited.

It’s not going to save the day. It’s not going to really move the dial a lot.

So we are left with fiscal policy. Now we should, in a sense, be comfortable with that.

We should go ‘well, the government has a lot of power’. Because remember the government, the federal government I’m talking about here, has something that no individual company or even State government has, and that’s the ability to create money.

So they should use that super power that we’ve given them to really help the economy when it’s needed.

But here’s the problem.

Conventional economics has created a strong narrative that debt and deficits are bad things. It’s a narrative which is very hard to shift.

And it’s a narrative which I grew up with studying economics in the 1980s. And there’s a narrative that it’s been reinforced constantly since.

So the minute you start running high deficits, of course, all the worry starts to come out from this group of people and conventional thinking. So back in the ’90s the magic number of debt to GDP, and I’ve put the US debt to GDP here, was 60%.

That’s what you needed to get into Euro.

If you flash forward to the GFC, we had famous papers like Reinhart and Rogoff who told us that if we went through 90%, that you were going to severely impact the economy.

And of course the US has since sailed through that. And that hasn’t happened.

The poster child, of course, Japan, has got a lot higher than this and they are still functioning well.

So you’re going to get this happening in the next few months, and indeed the next few years.

You’re going to get that group of conventional-thinking economists talking about why this is all heading towards doom and disaster. The terms they’ll use I’ve even heard used in the last month by the prime minister himself.

Terms like: how are we going to pay for this? We’re going to burden our children with this debt.

And they really talk about the government as though it’s like a household or something else, which has to sort of live within its means, otherwise people stop giving it money.

The government doesn’t need people to give it money. It creates the money itself.

As Vimal will mentioned, done a whole paper on this so I won’t go into too many details.

So the new economic model where fiscal policy is at the centre, needs new economic thinking, if it’s to be used properly. And unfortunately, a lot of the economic thinking we have is still found in times gone by.

This concern about debt and deficits. Of course, we’ve seen the national debt clock in the US, the Tea Party jumped on the back of that.

And they were very vocal for a long time there, coming out of the GFC, that apparently the government being active and running deficits was going to cause all sorts of problems. Well they’ve gone quiet.

Of course, Tony Abbott has since left the building down in Canberra. Although I fear the ghosts of Tony Abbott still lurk around the corridors, but of course when he got elected in 2013, one of his big slogans was to end wasteful spending and pay back Labor’s debt.

The myth of government surplus

So the myth, I say, is that a government surplus is good policy.

Now don’t get me wrong. It would be great if the government could run a surplus, but a budget surplus should be the result of a strong economy.

It should not be an end in itself. And the fact that last year, as recently as last year, the government was trying to run a surplus, despite a lot of excess capacity in the economy, is just plain ridiculous.

And it’s not just me saying that. I think even Phil Lowe was down in Canberra, voicing similar sentiments.

Now you’ve got to remember the flip side of a budget surplus is a private sector deficit.

A budget surplus means a government is taking more money out of the economy than it’s putting in. You only really want to drain money from the economy if the economy has an inflation problem.

And you only get that inflation problem, if the economy is at or close to full capacity. I think we can all agree it’s a long way from there at the moment.

So what is a budget deficit?

The word deficit sounds terrible, but really a budget deficit is you’re putting more money into the economy then you’re taking out. You’re actually creating a private sector surplus.

And more importantly, you’re creating activity in the private sector, which should see it come back. So it’s entirely appropriate.

You should be running deficits. And in fact, I would argue a budget deficit should almost be the natural state of things when you have the ability to print money. We can come back to that in a minute.

The myth of inflation

So just moving on, the second myth I think I’m hearing a lot more of in the last couple of months after this dramatic escalation in the budget deficit, is that the government printing money directly creates inflation.

It’s the idea that as the government puts all this money in, as the Reserve Bank does QE, all this money enters the system and creates inflation as more money chases goods.

An important thing to remember here, and this is a topic for a whole other presentation, but a couple of key points just for now.

Firstly, the private sector always nets to zero in the money system.

If you think about it, every dollar that we borrow comes from someone else. Every dollar we spend goes to someone else.

The private sector system always nets to zero. So if a government creates extra cash or drains extra cash, it has to do the opposite to offset it.

Now, normally running a budget deficit, what the offset is, of course, is the government then borrows that money back from the private sector, via the AOFM.

But it can choose to do another thing. And we’ve seen this in the last few months. It can choose to actually have the Reserve Bank create the money itself and the money therefore comes back by excess reserves.

Now it’s quite technical, but for those who follow these things, those excess reserves have gone up

considerably. But here’s the important point.

The government printing money does not directly create inflation. Only the private sector who does credit creation can do that.

And we saw that 15 years ago at the peak of the last boom, when we had a massive investment boom.

The private sector was running double digit credit creation. And therefore we got 3% to 4% inflation.

At the time the government was actually draining money via a surplus.

So the only way the government influences is by creating activity, which therefore creates confidence in the economy, which therefore creates investment in the economy, which therefore creates a lot more broad money.

And therefore we can start getting inflation back to where it should be.

So again, entirely appropriate for deficits to be run and if needs be for the Reserve Bank themselves to create that money.

As, as I mentioned, please look at my paper. If you don’t have it, ask for it. It’s a much better explanation that I’ve just given you there.

A new model emerging

So what is the new model that’s emerging?

As I said, monetary policy is basically dead. Now it hurts me to say this.

As I mentioned, I’ve made a whole career out of watching all the movements coming out of Martin Place and Washington and other central banks. We’ve hung on their every word. We’ve lived and breathed everything they’re doing.

And as an investment manager it’s been front and centre of our decision making.

But they’re out of the game effectively. They’re now spectators.

Sure, they’ve got still an important part to play in liquidity and if the crisis were to worsen again. I think the job they did in March and April was excellent.

And they’re still there to do that. But they are not there anymore to create inflation. Only the government can do that.

Now what concerns me, is does the government fully realise this?

The government, of course, again has done a great job in this crisis. A crisis like the GFC brings out this

side of government that they have to act.

They have to do something and suddenly they’re not scared of deficits.

But you can see as we emerge, we’re already seeing this creep back to the old way of thinking.

Not just at a federal level, but at a State level.

People are talking about, wow we have to have budget repair to claw back all this money

we spent. That is not the case.

And if that thinking comes in it virtually guarantees a double dip recession.

Now the themes under this new model, (Amy, as mentioned, will be talking about these), clearly

“carry and roll” are your strong friends.

Income is something, investment grade’s got an important part to play.

Inflation

And of course you can look at yield enhancements. Now for the last part, I’m going to talk about inflation because it’s a question I get asked a lot.

Really with short rates stuck at zero for the next five or maybe even 10 years, the long end will be buffeted around by what’s going on in inflation.

Clearly, the COVID-19 crisis has thrown the whole thing up in the air.

What we’ve seen over the last decade was a lot of merge towards that 2%. It was very little dispersion between various parts of the CPI basket.

Everything seems to go around there.

What we’re going to see now is a lot of dispersion between various factors.

Some will actually be stronger than they were pre the crisis, but a lot will be considerably weaker.

Inflation catalysts

So what are some of the upside catalysts to inflation that we’re thinking about in our framework? The first two, trade disruptions and supply chain reorganisation, would probably go under the theme of the peak of globalisation.

We are seeing some unwind.

Again, that was already happening through the crisis, but the crisis has dramatically escalated that.

Now it’s fairly obvious that if you’re going to source a lot more locally and you’re going to lose some of that benefits of globalisation or specialisation as we were taught back at university.

You will see some inflation emerge in certain product areas. That’s a given.

The second thing, which is actually pro inflation is the cyclical rebound won’t be weighed down by the same de-leveraging we saw after the GFC, particularly in Australia.

Maybe in the US less so. But the third one’s going to be very interesting.

There are certain sectors of the economy where we’ve got to suffer structural supply shocks from this

crisis.

In other words, certain things just won’t be coming back. A lot of marginal businesses will be closed forever. You can even see things like Target stores recently. You can see things like Virgin Airlines. If it were to come back, talk about being a lot smaller scale.

You are going to see some areas where as demand returns it’ll be pushing up against a much lower supply and you will see inflation in certain sectors.

However, those sectors as part of the CPI basket overall are not that high.

Which turns us to what the deflationary factors are.

Unemployment

The first one is obvious across the economy. High unemployment means zero wage growth.

Even the RBA themselves don’t have unemployment coming back anywhere near what’s needed for the next three or four years.

Slowing population growth

The second one is a new one, and this is the first time we’ve faced this in decades.

The population not growing.

Now it is temporary. But it is temporary for at least 12 or 18 months. We’ve seen a lot spoken about this recently.

This has big implications for housing particularly. Not so much house prices, which will be partially

saved by zero rates, but in the areas which actually feed into the CPI basket of rents and building costs.

Now rents, building costs, together with with utilities and rates make up almost a quarter of the CPI basket.

And we’re going to see rents and building costs go negative over the next 12 months.

In the case of rents, perhaps significantly negative. And they’re a huge part of what’s going on.

I actually had a different view the end of last year. I thought we’re starting to signs of a recovery, but it is a massive shift when you go from immigration of the levels we have seen down to zero.

In fact the population will only probably be positive by natural bursts in the next 12 months. That, as I said, will eventually come back, but it is years away.

Government-led zero inflation

The third one though, which really has me concerned, is what I call government-led zero inflation.

This is a version of the paradox of thrift, where all of us save, it might be in our own interest to save, but if all of us keep saving, the economy goes backwards.

Now this is a similar thing with inflation. A lot of government policies during the crisis and emerging from the crisis, all look good in their own right.

For example, the NSW government announced a wage freeze for public servants this last week for the next 12 months.

Now on the surface, that might look good. You might think that the private sector has got no wage growth, it’s the responsible thing to do.

Their budgets have been hit. They need to pull back spending. The trouble is as that thinking seeps into more and more areas, it starts to become self-fulfilling that you get zero inflation.

You can even look at things like the free childcare, which of course is going to cause a negative inflation print for this quarter, but will the government decide to keep that going long or maybe decide to keep some sort of subsidy in place above and beyond the crisis?

No matter where you turn governments seem to be adopting a policy that no growth in rates – and remember we’ve had a healthcare charge freeze as well – there’s going to be a lot of things that used to tick over at 2%, 3% or 4%, are now going to be at 0% possibly for years to come.

This will lock in that zero-rate inflation rate environment and be a big factor.

And it worries me that this thinking seems to be creeping in more and more. Particularly at the federal level

where they should be doing the opposite.

They should be trying to create activity.

Credit creation

Finally sluggish credit creation. There’s hardly an earnings call that goes by, where rather than mention the great opportunity this crisis provides to buy more businesses, people talk about having to shelve investment plans to repair the balance sheets.

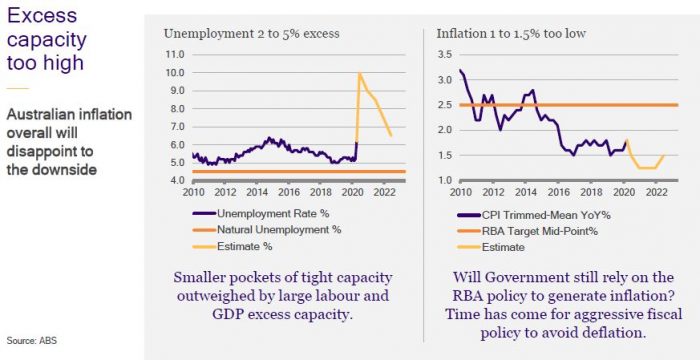

All of these things together mean that we very much land on the side of inflation is going to be a problem to the downside. Excess capacity, quite simply is too high.

As you can see here – unemployment. This yellow line is the RBA’s forecast.

You could argue 4.5% for NAIRU was too high anyway. We’re not going to get within cooee of that. So we have a major problem.

And finally inflation, as you can see there has very little chance of getting – this is underlying inflation, not headline – headline will be negative.

Underlying inflation has very little opportunity.

So what we call upon in a sense, and the conclusion I make is that unless we get a rethinking of the framework by the federal government, unless we start to see them truly step up and use fiscal policy to avert the crisis that the RBA previously would have averted, then we’re going to head for a double dip recession, and we’re going to head towards zero inflation.

I hope they wake up to that, but for a fiscally conservative party, it’s going to be a difficult road to trade. So I’ll leave it there now and I’m going to pass on to Amy to talk about how we’re looking at fixed income investing in a zero rate environment. Thank you for your time.

Tim Hext is a portfolio manger with Pendal’s Bond, Income & Defensive Strategies team.

Tim joined Pendal Group in February 2017 with responsibility for managing Australian Bond portfolios. Tim has extensive experience in banking, financial markets and funding.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Find out more about our investment capabilities:

https://www.pendalgroup.com/about/investment-capabilities

Here’s the latest outlook for Australian equities from Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

EQUITIES continue to surge, driven by optimism over the pace of economic recovery.

The rotation away from defensives and growth to deep cyclicals and value continues. This is providing better breadth to the market as previous laggards start to catch up. It also continues to squeeze a market which has been defensively positioned.

Last week the S&P/ASX 300 gained +4.2%.

Economy and policy

The equity market seems to be disregarding earnings on the basis that everyone knows the current period will be woeful, while one year into the future is impossible to predict.

As a result, the delta on economic news flow is driving returns – and this remains better than expected.

Last week’s US payrolls are a case in point. Non-farm payrolls rose by 2.5 million in May – versus a consensus expectation of a 7.5 million fall. Unemployment fell from 14.7% to 13.3% versus a consensus of 19%. There is debate around the numbers and classifications used. However, the underlying signal is that re-hiring is better than expected.

While fiscal stimulus is driving better outcomes, monetary policy also remains very pro-cyclical as we are effectively at the zero bound.

A strong recovery leads to less fear of deflation, which means lower real rates, which helps further stimulus and higher valuations, creating a virtuous circle. This could of course turn vicious if we start to see economic expectations deteriorate – however for the moment the fiscal backstop appears sufficient.

The combination of these two effects is driving equity markets and squeezing the broadly consensus bearish positioning in terms of sector allocation.

Digging into the US job data, leisure and hospitality saw the best results, with an increase of 1.2 million jobs in May. However this was against 8.3 million lost in the previous two months. While the delta is good, this sector is still well below its high-water mark. There were an additional 400,000 jobs in construction, which has recovered almost half the jobs lost to Covid-19.

While unemployment is a lagging indicator, more real-time indicators are also constructive. PMI numbers are stabilising. While still signalling a contraction, the market is focused on the positive trajectory versus recent results.

Elsewhere US auto production estimates for Q3 are almost back to the pre-Covid levels. This has a positive read-through for supply chain inputs such as steel and components. Mobility data and trends such as AirBNB searches are likewise painting a picture of an economy recovering faster than many predicted.

The US FOMC meeting this week will shed light on their rate of asset-buying going forward and how they are seeing the economy. The next US fiscal package is expected to be announced in July at US$1 trillion to US$1.5 trillion – with a focus on helping the re-start rather than income support. This will be a more contentious process and could represent a risk to the market.

Markets

There is a view – backed by data on brokerage account openings – that retail money is driving this rally, supported by various government cheques.

We are mindful this market has shrugged off lot of bad news and uncertainty in the form of tensions with China and US civil unrest. ETF flows have been to defensive assets such as bonds and gold – while equity ETFs remain in material outflow since late March. The market is climbing the proverbial wall of worry, which is a constructive factor.

The reflation trade of the past few weeks continues to dominate price action. In equities, we see it in the continued rotation from growth to value, which is broadening the market’s rally. This can continue while the economic data remains supportive.

In other assets it is seen in US 10-year bond yields rising, credit spreads narrowing, a higher copper/gold price ratio and a stronger AUD.

There are a number of near-term issues to be mindful of:

- Valuation: P/E valuations have surged. Many see P/Es as meaningless given uncertainty over earnings and at this point the market does not seem concerned. However, this could change.

- Technicals: The market’s recent momentum has only been equalled 10 times in the last 30 years and suggests we might see some near-term consolidation.

- Put/call ratio: The case for near-term consolidation is supported by a shift in put/call ratios from super-bearish to a more optimistic stance.

The balance of probabilities suggests we might see consolidation – but not necessarily a material fall. But there are two issues that could potentially de-rail the market and need to be watched closely:

- A second wave of infections: The market’s concern here seems to be diminishing – which does leave it vulnerable to any resurgence. In this vein, it is important to understand the improvement in US case numbers is driven by the hardest-hit States of the north-east. Other States are showing flat-to-rising trends, albeit at low levels. Given we are seeing genuine second waves in places like the Middle East – particularly in Iran and Saudi – this needs to be watched.

- US Presidential Elections: Trump has seen support ebb and Biden is now the favourite for November’s election. The odds that Democrats win five seats to take control of the Senate appear even at this point. This raises the possibility of Democrat control of Washington – with policy implications in areas such as tax which could present a risk to equity markets.

Fixed income impact investment is a fast-growing but still relatively new segment of capital markets. Here Pendal portfolio manager George Bishay (pictured above) takes a deep look at impact bonds and answers questions we often hear from our clients.

EACH year, more and more sustainable bond investments become available, covering all aspects of the environmental and social spectrum.

There are bonds where companies in underlying projects reduce their carbon footprints and bonds that help finance companies with strong gender equality records.

Some bonds finance governments to build railroad and solar power plants, others help build affordable housing.

As the market rapidly grows, debate is intensifying about pricing and returns and how these bonds are trading in high-demand secondary markets.

More than $US465 billion of sustainable debt was issued globally in 2019 — a new record and up 78 per cent from the previous year. More than $US1 trillion in sustainable debt has been issued since the market began.

This growth is driven by soaring demand as investors seek ways to “do good” with their investments amid growing concern about climate change and social issues.

At the same time, corporations and governments are becoming ever keener to behave responsibly and to be seen doing so.

Types of impact bonds

There are two main types of impact bonds:

– Environmental bonds which finance projects that benefit the environment

– Social bonds which address a social need or improve an outcome for underprivileged people

Issuers are usually certified by an independent organisation such as the International Capital Market Association or the Climate Bonds Initiative.

Most of these bonds also adhere to the UN Sustainable Development Goals.

Why do companies issue impact bonds?

A key question we get asked is why corporations and governments issue impact bonds instead of traditional issuances. In our experience, they are issued for a number of reasons.

One reason is to signal confidence in the sustainability of a wider business.

Corporations issuing impact bonds are implicitly inviting scrutiny of their wider business practices and signalling they are confident in their sustainability credentials. This also leads to future benefits.

More and more traditional fund managers are incorporating Environmental, Social and Governance (ESG) factors into their investment processes.

This is partly because ESG risks genuinely affect performance and partly at the behest of end investors such as superannuation funds.

Companies that issue impact bonds are stamping their ESG credentials, which can ultimately be supportive of credit spreads they have to pay down the track.

A third reason is simply to cater for market demand.

Across the world investors are seeking access on behalf of clients to investments that are sustainable or make a positive change in the world.

Issuing impact bonds can also help diversify an issuer’s funding by attracting new types of investors.

Research also shows green bonds get the tick of approval from equity holders.

They can trigger a positive stock price reaction as markets react to expectations the bonds will improve long-term shareholder value by lifting company performance.

Examples of recent impact bonds include a $400 million, five-year bond issued by supermarket giant Woolworths to improve carbon emissions from refrigeration and lighting in its stores.

NSW TCorp, the bond issuer for the NSW state public sector, issued a $1.8 billion bond to further public transport projects and fund a sustainable water project.

Queensland’s QTC allocated bond proceeds to light and heavy rail projects, cycleways and a solar farm.

How do impact bonds perform?

It is true that impact bonds tend to perform well in the secondary market — but the reasons for this are nuanced.

We often say there is excellent secondary market liquidity for impact bonds if you’re looking to sell — but not so much if you’re looking to buy!

There should of course be no difference in pricing between impact bonds and their vanilla counterparts. This is true because the same credit risk applies to non-green bonds issued by the same issuer.

The credit risk is that of the issuer, not the underlying green or social projects.

This is most pronounced in bonds issued by supranationals such as the World Bank. The collapse of an underlying project has no effect on bond holders, who are assured by the triple-A rating of the World Bank itself.

Fundamentally, this also means investors are not penalised for investing in green bonds.

Investors in impact bonds get the same credit spread as if they invested in an equivalent vanilla bond from the same issuer.

Nevertheless, a “greenium” — a premium paid for green bonds — can be observed from time to time in the secondary market.

Often the explanation for the premium is simply an excess of demand over supply.

When Woolworths issued its first green bond last year it found demand five times stronger than its issue size and priced better than initial guidance. It traded even more strongly in the secondary market.

Whether this was demand for the green aspects of the bond — or simply demand for exposure to Woolworths — is difficult to determine.

But this differential can be a benefit for dedicated sustainable fixed income funds buying in the primary market. They are often handed a better allocation than a competing vanilla fund, putting them in an advantaged position in the secondary market.

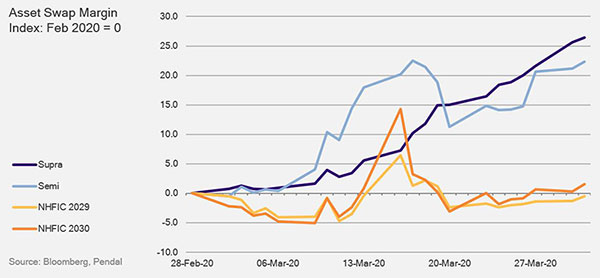

During increased volatility at the end of the March 2020 quarter we saw one of our impact holdings do very well relative to a similar non-impact bond.

The bonds were issued by the National Housing Finance and Investment Corporation (NHFIC) — an independent Commonwealth entity that operates the Australian Affordable Housing Bond Aggregator.

This organisation provides cheap, longer-term secured finance for community housing providers by issuing bonds in Australia’s debt capital markets.

The funds raised by the bonds were loaned to community housing providers to help finance more than 2000 properties in Victoria, NSW, Queensland, Western Australia and South Australia.

This included supporting the supply of more than 360 new social and affordable dwellings.

The bonds, which typically trade in line with other supra nationals and semi-government bonds, outperformed in March 2020 as can be seen in the chart below.

Looking ahead

The truly dedicated sustainable funds are not yet big enough to soak up all the impact bonds issued in Australia.

Some $6 billion of impact bonds were issued in Australia last year and the pure impact funds accounted for only a sliver of that supply.

This has the effect of keeping pricing in line with non-impact bonds.

Vanilla funds are required to fill the book and need to be offered at the same pricing as they would get in an equivalent non-impact bond.

Only when the dedicated sustainable sector is big enough to take out whole books will we start to see some difference in pricing.

Right now, that looks to be some way off.

George Bishay is a portfolio manager in Pendal’s Bond, Income & Defensive Strategies team.

George has managed dedicated Sustainable fixed interest portfolios for a decade. He has also worked across numerous fixed income, credit and money market portfolios in portfolio management, credit analysis and dealing roles for over 20 years.

In 2019 he was awarded the Alpha Manager status by Money Management’s FE fundinfo, in recognition of his career-long performance in the asset management industry.

Pendal is an independent, global investment management business focused on delivering superior investment returns for our clients through active management.

Our Pendal’s Chief Executive Officer, Australia, Richard Brandweiner discusses why the way we invest can make a big difference to the world around us.

Watch the video above or read the transcript below.

TRANSCRIPT

My name is Richard Brandweiner, and I’m the Chief Executive of Pendal in Australia.

These are very challenging times, but they remind us of just how interconnected our world is, how our economy and our financial markets are intrinsically linked to our human ecosystem.

Also how important it is, the decisions that we make, and how we treat other people, what the ramifications are. That’s perfectly true with our capital and our wealth as well.

The way we invest can make a big difference to the world around us and importantly the world into which we, or our children, are going to retire.

And that’s one of the reasons why we’re seeing such extraordinary growth in sustainable and ethical investing.

Consumers are increasingly demanding different things from their service providers. It’s no longer just about what product or service you provide, it’s also important how you go about it.