How will deflation impact investors in a low-rate environment?

Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor (pictured above) explains in this plain language keynote presentation from the Conexus Fiduciary Investors Symposium on May 19, 2020.

TODAY I want to run through some of the unprecedented numbers we’re seeing and outline how this economic environment could play out.

What is the economic outlook?

Let’s put the current situation in perspective. Take the non-farm payrolls number (see below). This graph, which goes back to 1940, puts into context how monumental this slowdown has been.

It’s becoming more of a consensus view that the size of the lockdown — and the commensurate policies that have come with it — have largely been the wrong ones.

We arguably shouldn’t have stopped the economies as quickly as we did. We should have followed a different model and now we’re trying to pull ourselves out of this massive economic contraction we are experiencing.

There is no getting away from the fact that this is a massive shock.

Shocks historically have started in the financial system, for example the dot-com and GFC crises. This one started as a health crisis which flowed into economics then through to financial assets. So it’s a very different beast than the crises we have seen before.

That is why the authorities have had so much trouble dealing with it.

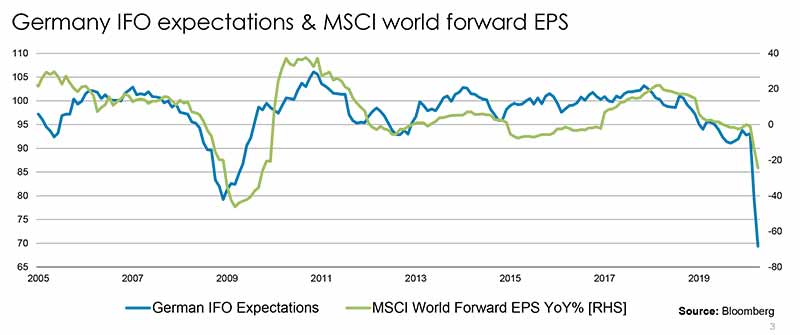

This chart below shows Germany, but I could have used pretty much any country.

I’ve used the IFO expectations which is a PMI and I’ve just put it up against MSCI world for EPS. We can see how the situation is going to get worse before it gets better.

Global data is awful. The April US retail sales number was down 16% — which puts it down about 30% since February (excluding food).

It is quite clear many businesses will not survive this crisis. High-end restaurants run with a margin of around 5% to 8% and they’re going to be running at 10% to 30% capacity.

Yes, we have dealt with the liquidity issue but we’ve got a solvency issue which is going to come up and hit us later. Do we have enough firepower to deal with that?

We’re going to see a tsunami of bankruptcies — there’s no other way to think about this.

The reason we’re not seeing these bankruptcies already is the government lockdowns and life-support mechanisms are delaying the process.

We can see here that earnings are going to be terrible. But we know the S&P is down only marginally from the levels we came into the year — so what’s happening?

It’s about multiple expansion. P/E multiples expanded on the back of liquidity, but earnings have been decimated — and it’s very clear earnings are going to get hit further.

Central banks responded very quickly. They did the usual: conventional monetary policy, cutting rates to zero. This was followed by unconventional monetary policy, yield curve control and more quantitative easing at a size we’ve never seen before.

Quantitative easing in the US is five times the size of all the quantitative easing we’ve seen in the last 10 years put together — unbelievably large.

The Fed and other central banks then started going into the fiscal policy area — somewhere they’ve not normally gone before.

They start supporting the markets and the economy directly, bypassing the banking system.

The Fed and central banks around the world have thrown every measure they possibly can to get rates down and flood the system with liquidity.

It’s my strong belief they will have to take rates negative. They don’t want to take rates negative — Powell talked about that last week about the fact that they don’t want to do it.

We know operationally the US isn’t ready yet and there is very strong resistance from the lobby groups and the banks.

But when nominal interest rates are 50 basis points in the US and you’re going to get a big wave of deflation, you’ll have real interest rates rising — which is just going to crunch the US economy further.

So, we believe the only material thing the Fed will be able to do is cut rates to negative with a short, sharp shock the way Kenneth Rogoff has recommended.

They clearly don’t want to. But I think there’s no choice — which would mean bond yields across the world would go negative as well.

What are defensive assets today?

While yields are already low, you can very clearly own 10-year Treasuries until they’re at -1%. I think they’ve got a lot of juice left in these markets. People don’t want to be owning them here but they should be.

The more bonds rally, and the lower yields go, the more people will need to buy them.

The Fed has done everything — conventional monetary, unconventional monetary and now they’re doing fiscal policy.

This chart shows investment grade spreads relative to non-manufacturing PMIs:

You can see we’d be off the scale if the Fed wasn’t artificially supporting credit spreads — we’d be at 600 to 700 given the non-manufacturing PMI.

The slowdown in the economy should lead to much wider spreads — but it hasn’t because of the backstopping by the Fed.

Not only is the Fed backstopping investment grade corporates via ETFs, they’re now doing high-yield fallen angels.

They’re effectively doing everything they possibly can to stop the markets dislocating and to plug this hole. But what they’re doing is plugging a solvency hole with liquidity, and ultimately it will fail.

We know the size of the central bank response has been massive, but then we had this coupled with the response by the governments as well.

This chart below shows the change in cyclically adjusted primary fiscal balance, this measure will give you an idea of how big the government fiscal response has been.

You need to think about this in terms of the US.

I’ll put it in perspective in terms of the US.

We came into this crisis with a fiscal deficit around 5% in the US. That’s ridiculously large on the back of the longest expansion in history. Plus we’re at full employment.

We came into COVID in the worst situation. We had very high debt levels in both government and corporate debt, and investors had portfolios which were pushed out the risk curve as they stretched for yield

So the virus hit us at exactly the wrong time.

Coming into this crisis the US was running a 5% fiscal deficit, we’ve now had support packages in the region of 15%. The economy has slowed dramatically which will lead to a drop in tax revenue of about 3% to 5%.

Nominal GDP is also going to detract about 5% over the calendar year, so we’re looking in the US for a fiscal deficit somewhere 20% and 25% of GDP.

This next chart shows you how unsustainable this is. The US Congressional Budget Office (CBO) estimates below show numbers back to 1790.

There’s zero chance they’re going to be able to pay this money back. Zero chance.

So how will they close the hole?

They have to defaults — either implicit default through inflation (the preferred course of every central bank and government in the world) or explicit default (restructuring, tax rises and spending cuts).

We talk about rebuilding the budget in Australia and trying to pull things back.

But there is zero chance across the world this money’s being paid back, so we need to engineer inflation or we need to do some type of debt jubilee, or a combination of the two.

The outlook for inflation

Lots of things drive inflation over the long run.

Factors that have kept inflation down over the last 30 years include the three Ts — trade, tech companies and titans.

Up until recently we had free and growing trade; we’ve had the influence of the tech companies (eg Amazon and its pricing power and ability to push prices down); and the titans (the rise of massive companies with oligopolistic or monopoly positions).

You’ve also had the two Ds — debts and demographics.

All these factors have been weighing on inflation. It’s quite clear here in the next chart showing M2 minus real GDP — but you can put any measure of money supply for any country in the world and the US is the poster child for this.

Money supply is absolutely ballooning.

Initially, the run-up in the money supply was unexpected as corporates drew on their revolving lines of credit.

That increased money supply as the banks were forced to lend to them. Then the Fed began pumping money in the system.

The three-month change in M2 in the US shows it is running at over 100%.

These are numbers you couldn’t even imagine. At some point that will start feeding through to inflation.

When you think of Irving Fisher’s theory of money, on one side you’ve got money supply and on the other side you’ve got velocity. Multiplying the two together gives you nominal GDP.

But the velocity of money’s been falling since 2006-07 because the economy’s been slowing, nominal GDP is coming down and nominal interest rates have been falling.

Now it’s been falling off a cliff because there are no transactions happening in the economy.

The government’s trying its best to slow down the velocity of money by throwing all of these fiscal packages at it. At some point, whether it’s six months or a year when we start coming through this, we’ll see velocity of money stop falling and then probably start rising.

That means you’ve got this massive money supply up against the velocity which isn’t falling. That has to lead to higher nominal GDP and nominal inflation.

There is no question in my mind that we will be hitting an inflationary episode in the US over the coming medium-term — one to three years out.

I think that’s what the governments want. They want to deflate the debt away.

Even before the virus, the Fed told us they wanted to move to average inflation targeting — running inflation above the target to get the 15-year average up.

Now they might have to run this at 3% to 5% — so you’re talking some quite big numbers. The problem is we’re going to hit deflation first, then inflation after.

In the long run you get these structural forces — monetary policy, fiscal policy, demographics, debt, trade, etc — which influence a long-term inflation rate.

In the short run inflation is largely driven by the business cycle. It’s quite clear we’re going to hit GDP growth of minus -5% in the US this year, which will give you a deflationary environment.

The thing that really worries me in the US is the fact that shelter inflation — the part of inflation that has been holding up the inflation rate in the US — is now flat and starting to fall.

Excluding shelter, the CPI number we saw last week was 0.6% and this is falling rapidly.

So we’re going into a deflation episode in the US. I think the Fed has to counter that with negative interest rates.

Then when we start coming back to work and hopefully get a vaccine, that point is going to be super inflationary because I cannot see an environment where the central banks of the world pull back monetary policy anywhere near the pace they need to.

It’s quite clear they and the governments have over-delivered. They’ve filled a solvency issue with massive short-term liquidity.

When we talk about the deflation-inflation picture we can’t forget about the US Dollar’s role as the reserve currency. They call it the exorbitant privilege.

This shows you what that privilege is worth. You can see on this next chart as currencies weaken you tend to see bond yields fall.

The US can get bond yields falling while the currency strengthens and that’s a massive advantage.

The world certainly doesn’t like that advantage. China, Russia and Europe don’t like it. There will be a move away from the dollar standard at some point — it’s just a question of how long it takes.

I think that will go hand in hand with some kind of debt jubilee over the medium term and some greater role for crypto currencies.

The focus of the crypto world is Bitcoin for me. You can like it and not be part of the shiny hat brigade. All you have to do is accept the fact that crypto is going to be a much greater part of the financial markets going forward.

Most of the world’s central banks are currently working on crypto and some kind of stable coin right now. These are the equivalent of IMF SDRs — there is no doubt it will become more mainstream.

American billionaire Paul Tudor Jones had a note out just a couple of weeks ago expounding the benefits of Bitcoin. Literally, it’s the only tradable asset in the world where there’s a known fixed maximum supply.

You’re buying it because you don’t trust in central banks and governments. You’re buying it because they can’t deflate its value away — they can’t devalue your Bitcoin.

Whether you like Bitcoin as a construct or not, I think you have to accept the fact that the world is moving away from allowing the US to be the reserve currency.

We’re moving to a new regime. How we move away from a US reserve currency and how crypto impacts the long-term inflation-deflation dynamics have yet to be determined, but they will be material.

Vimal Gor leads Pendal’s Bond, Income and Defensive Strategies team.

Find out more about Pendal’s investment capabilities.

Important Updates

Pendal Dynamic Income Fund (APIR: BTA8657AU, ARSN 622 750 734)

Pendal Enhanced Credit Fund (APIR: RFA0100AU, ARSN 089 937 815)

Pendal Fixed Interest Fund (APIR: RFA0813AU, ARSN 089 939 542)

Pendal Monthly Income Plus Fund (APIR: BTA0318AU, ARSN 137 707 996)

Pendal Sustainable Australian Fixed Interest Fund (APIR: BTA0507AU, ARSN 612 664 730)

Effective 22 May 2020, the buy-sell spread for a number of Pendal funds (the Funds) will decrease as set out in the table below:

|

Fund Name |

Old (%) |

New (%) |

||

|

Buy |

Sell |

Buy |

Sell |

|

|

Pendal Dynamic Income Fund |

0.07% |

0.36% |

0.07% |

0.23% |

|

Pendal Enhanced Credit Fund |

0.07% |

0.32% |

0.07% |

0.23% |

|

Pendal Fixed Interest Fund |

0.06% |

0.12% |

0.06% |

0.10% |

|

Pendal Monthly Income Plus Fund |

0.07% |

0.25% |

0.07% |

0.20% |

|

Pendal Sustainable Australian Fixed Interest Fund |

0.05% |

0.13% |

0.05% |

0.09% |

Table 1: Old and New Buy-Sell Spreads

The buy-sell spread is an additional cost to you and is generally incurred whenever you invest in or withdraw from a Fund. The buy-sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy-sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy-sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Funds.

The further reduction in buy-sell spread reflects continuing improvement in market liquidity for Australian issued investment grade securities.

Pendal will continue to monitor market conditions and review and update the buy-sell spread regularly as required. You should therefore review the current buy-sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy-sell spread for each Fund.

The COVID-19 crisis underlines the importance of considering Environmental, Social and Governance factors when investing. Regnan’s head of advisory Susheela Peres da Costa expains why in this interview with online business channel Ausbiz.com.au.

Watch the video above or read this transcript:

AUSBIZ.COM.AU INTERVIEWER: We were speaking earlier about Environmental, Social and Governance (ESG) and it was pointed out that in this crisis ESG is still front of mind — perhaps more for the social impact than the environmental impact. Is that how you see it?

SUSHEELA PERES DA COSTA: Absolutely. Often during more ordinary times it’s the social factors that get short shrift. But as a result of this pandemic we’ve become very alert to things like the working conditions in factories that might be making our protective gear or protective equipment in factories far away.

We’ve become quite alert to the working conditions for people who are essential workers in the community, who we need to be healthy, and be able to be willing to continue to put themselves at the service of the community in times that are quite difficult.

These are just some examples of social issues.

INTERVIEWER: Do you see a real opportunity when it comes to ESG principles and gauging a company’s compliance when it comes to supply chains? Most people say supply chains are not going to look anything like they did pre-COVID.

SUSHEELA PERES DA COSTA: Yes, one of the really interesting things is that in boom times we tend to see efficiency as a good in itself.

Very often the idea of just-in-time inventory or very short supply chains where we’ve taken as many costs as possible out of the ultimate cost of a product is seen as a good thing.

But really efficiency comes at the expense of resilience and a little bit of redundancy is often a good thing.

It allows you to make changes as you need and to modify areas of risk that might come offline. That goes for pandemic conditions, but it applies equally to a flood or a fire or even a trade embargo that happens in different parts of the world and can affect supply chains that we’ve come to rely on.

These types of trade-offs are parts of ESG that are typically under-appreciated. We get headlines around things like climate change and modern slavery — ESG issues that the community is aware of — but they are the tip of the iceberg.

There’s a significant amount that’s less amenable to media interest during good times, but very, very apparent when anything goes awry.

The ultimate goal of ESG is to look a little bit further ahead and a little bit wider in your field of view than what’s typically in focus for business and investment.

Being able to widen that view and lengthen that horizon allows you to make better investment decisions for the long term.

INTERVIEWER: That’s a really good point. Even ESG as it stands — the E being first — [means] everyone talks about the environment as if that is front and center. But … where is that [capital] being deployed? Which part of that ESG is it trying to move to?

SUSHEELA PERES DA COSTA: It’s more about taking everything into account. One of the interesting things about ESG is we’re quite focused on labelling categories within ESG, for example the environment or supply chains.

But actually a lot of these issues interact with each other. Understanding how that can alter the shapes of economies, alter business profits and alter investment returns, is some of what ESG seeks to highlight.

To give an example, we might commonly hear about things like a business being a heavy emitter of carbon. But that may ignore the fact that it is also exposed to physical risks of climate change.

When you put those together, you can see how they might interact.

For instance, it might be after a season of bushfires that the community is more alert to climate change and more ready for regulation that limits carbon emissions.

The contingency plans a company makes to deal with one of those possibilities could be derailed by the other.

It’s really the interaction of many of these kinds of risks that form some of the biggest areas of potential risk for ESG. And of course also the biggest opportunities in addressing them.

INTERVIEWER: Are you seeing lots of positive forward momentum on this front in Australia? Are there plenty of opportunities, plenty of companies that you can hitch your bandwagon to because you truly believe they’re getting it?

SUSHEELA PERES DA COSTA: Momentum has been really strong. We’ve been talking to companies at Regnan since the early 2000s. The degree to which they are understanding and impounding the ESG ideas into their own business strategies and business models has never been swifter.

It’s actually quite an exciting time for people to be working on those projects inside companies and investors.

There are always pockets of laggards and that’s a reality that investors need to work with. But there are some interesting opportunities out there too.

Susheela Peres da Costa is head of advisory at Regnan, a global leader in long-term value, systemic risk analysis and responsible investment advice. Last year Pendal appointed a London-based impact investment team to launch a Global Equity Impact strategy in late 2020.

Regnan is wholly owned by Pendal Group.

Pendal Sustainable Conservative Fund (APIR code: RFA0811AU, ARSN 090 651 924)

Effective 21 May 2020, sustainable and ethical investment practices in the Pendal Sustainable Conservative Fund (Fund) will be broadened to also include a portion of the Fund’s investments in alternative investments. Sustainable and ethical investment practices are currently incorporated into the Fund’s Australian and international shares and Australian and international fixed interest allocation.

Alternative investments sustainable and ethical screens

For a portion of the Fund’s alternative investments component, the Fund will not invest in companies or issuers directly involved in the following two activities:

• tobacco production; and

• controversial weapons manufacture (such as cluster munitions, landmines, biological or chemical weapons, depleted uranium weapons, blinding laser weapons, incendiary weapons, and/or non-detectable fragments).

For a portion of the Fund’s alternative investments component, the Fund will also not invest in companies or issuers directly involved in the following activities, where such activities account for 10% or more of a company’s or issuer’s total revenue:

• the production of alcohol;

• manufacture or provision of gaming facilities;

• manufacture of non-controversial weapons or armaments;

• manufacture or distribution of pornography;

• direct mining of uranium for the purpose of weapons manufacturing; and

• extraction of thermal coal and oil sands production.

Investments will be reviewed regularly to ensure they remain within the sustainable and ethical screens of the Fund. If the review process identifies that an investment ceases to comply with the screens, the investment will usually be sold as soon as reasonably practicable having regard to the interests of investors, but this may vary on a case by case basis.

Pendal Sustainable Balanced Fund (APIR code: BTA0122AU, ARSN 637 429 237)

Effective 21 May 2020, sustainable and ethical investment practices in the Pendal Sustainable Balanced Fund (Fund) will be broadened to also include a portion of the Fund’s investments in alternative investments. Sustainable and ethical investment practices are currently incorporated into the Fund’s Australian and international shares and Australian and international fixed interest allocation.

Alternative investments sustainable and ethical screens

For a portion of the Fund’s alternative investments component, the Fund will not invest in companies or issuers directly involved in the following two activities:

• tobacco production; and

• controversial weapons manufacture (such as cluster munitions, landmines, biological or chemical weapons, depleted uranium weapons, blinding laser weapons, incendiary weapons, and/or non-detectable fragments).

For a portion of the Fund’s alternative investments component, the Fund will also not invest in companies or issuers directly involved in the following activities, where such activities account for 10% or more of a company’s or issuer’s total revenue:

• the production of alcohol;

• manufacture or provision of gaming facilities;

• manufacture of non-controversial weapons or armaments;

• manufacture or distribution of pornography;

• direct mining of uranium for the purpose of weapons manufacturing; and

• extraction of thermal coal and oil sands production.

Investments will be reviewed regularly to ensure they remain within the sustainable and ethical screens of the Fund. If the review process identifies that an investment ceases to comply with the screens, the investment will usually be sold as soon as reasonably practicable having regard to the interests of investors, but this may vary on a case by case basis.

Rebalancing can materially improve outcomes for investors when done thoughtfully. But it’s a surprisingly complex subject.

Here Pendal senior portfolio manager Stuart Eliot (pictured above) offers some practical, plain-language tips.

REBALANCING is a surprisingly technical subject.

There is no shortage of articles out there that discuss the topic using a load of formulas and heavy-duty number crunching.

Instead, here we’ll explain in plain language the practical aspects, illustrating with examples based on the recent market volatility.

Why rebalance?

Advisors invest considerable time with their clients to determine an appropriate investment portfolio based on important criteria such as risk tolerance, income, stage of life and return objectives.

This is ultimately expressed as a set of strategic or neutral asset allocations to various asset classes or as a risk profile (say balanced) which drives the choice of investment portfolio.

In either case the optimal portfolio expresses assumptions about long-term risk and return behaviour of asset classes. Once the portfolio is established, the relative weights between asset classes will change due to market movements, taking the portfolio away from the optimal asset allocation.

Eventually these changes build up to the point where the investment begins to exhibit risk characteristics different to the optimal portfolio – warranting a rebalance.

For example, let’s say the optimal portfolio holds 50% equities because the client can tolerate a mark-to-market loss of 10% if equities fall 20%.

After a strong market rally, equities now comprise 60% of the portfolio which would result in a mark-to-market loss of 12% in the same scenario. (In addition, diversifying investments have fallen from 50% to 40% of the portfolio, offering less than the intended amount of protection.) This is more than the client would be willing to accept – therefore rebalancing would be required before this point was reached.

Rebalancing is an essential part of managing a portfolio to ensure it remains consistent with a client’s objectives.

How or when to rebalance?

There are three general ways of managing the rebalancing of a portfolio. Each comes with pros and cons.

1. Calendar-based rebalancing

Often portfolios are rebalanced at the end of each month, quarter or after a regularly-scheduled portfolio review. The benefit is they can be planned in advance and can facilitate the bundling together of trades to achieve economies of scale.

However, they tend not to be able to take advantage of large intra-period market movements and can potentially result in significant drift from the optimal portfolio.

(Fun fact: if an investment process was developed or back-tested using monthly data for example, it would be implicit in the investment process that rebalancing was performed at the end of every month.)

2. Trigger-based rebalancing

This means rebalancing the entire portfolio, or an asset class/investment within the portfolio, when a trigger level is reached. A trigger could be the distance of a single investment’s weight from the target, the sum of all absolute differences from target, or an estimate of tracking error relative to the optimal portfolio.

This approach has the benefit of keeping the actual portfolio sufficiently close in character to the optimal portfolio while taking advantage of large intra-period market movements.

However this method is more operationally burdensome because it requires regular monitoring to check whether rebalancing is required.

3. Flow-based rebalancing

There are various approaches to flow-based rebalancing. The following approach is representative. The cash balance in the portfolio goes up and down due to deposits, withdrawals, purchases, sales, income and expenses.

When the cash balance is too high the surplus is used to top up the most underweight investments. When the cash balance is too low additional cash is raised by trimming the most overweight investments.

The main benefit here is that transactions costs are minimised. But if cash movements are small and market movements are large, the portfolio can move a long way from its target.

Which approach is best?

The most appropriate rebalancing strategy depends on an investor’s specific circumstances.

At Pendal Group we manage the rebalancing of our diversified funds using a blend of the second and third approaches.

Each day we monitor the weight of each investment in a portfolio (generally unit trusts for asset class and strategy exposures and futures contracts for active tilts). When an investment gets too far from its desired weight we rebalance back to the target.

As an extra tweak – in asset classes where it makes sense to do so – we often rebalance using futures contracts because these tend to have lower transactions costs than unit trusts or the individual securities they hold.

Apart from staying close to the desired asset allocation, this also imposes a robust discipline to managing the portfolio when things get wild, as they have done recently.

We naturally believe all investments we hold will deliver a positive return over time, although we can’t know when. Therefore as the price of an asset declines, through the rebalancing process we gradually buy more as it becomes cheaper while reducing the holdings of other assets as they become more expensive. Our choice of rebalancing approach is driven by a combination of the structure in which we happen to operate combined with our own research.

Our basic insight is that markets tend to:

1. Trend over days

2. Mean-revert over weeks

3. Trend over months

4. Mean-revert over years.

Trigger-based rebalancing capitalises on the first two of these timeframes. We find that doing so results in better expected returns through time than calendar-based approaches. The latter two timeframes are the domain of our active asset allocation processes.

Rebalancing in volatile times

We’ll conclude with a few insights from the recent volatility which may help in setting up portfolios to benefit from future volatility – when it inevitably arises again.

The first is using flexibility to reduce transactions costs.

As mentioned above, Pendal makes use of futures as part of the management of diversified fund rebalancing. This was particularly useful in March when the equity market was experiencing huge intraday moves on a regular basis – resulting in regular and sizeable rebalancing flows. By trading futures – rather than unit trusts or individual securities – we were able to trade with materially lower market impact.

This also gave us the ability to choose our time and price if desired, rather than being captive to the end-of-day price. Not everyone is able to trade futures, but a near identical outcome can be achieved by holding a portion of the investment in relevant asset classes in highly-liquid ETFs or other passive vehicles – of which there are many to choose from. In fact we do exactly this in our multi-asset SMA portfolio models.

Another insight relates to transactions costs – though in a different way. During the worst of the March equity market plunge, the natural systematic rebalancing flow across the market was to buy equities (which had become under-weight as the price declined) and sell fixed income. In Australia, many fixed income mandates are managed to a government plus credit benchmark. Because of this, redemptions from generalised fixed income placed pressure on already-stressed credit markets, causing some funds to widen their bid-ask spreads. At the same time our longer-term valuation models were telling us credit was attractively cheap and we should be adding exposure in our portfolios – which on the surface would seem expensive given the wider spread.

Fortunately in most of Pendal’s diversified funds we hold government and credit exposures separately within the fixed income asset class. So we were able to “buy” the credit exposure almost T-cost free by executing the rebalancing through selling just the government bond holding. The net result is an overweight to credit without having to pay the wider spread.

Pendal senior portfolio manager Stuart Eliot has day-to-day responsibility for the monitoring and management of all portfolios within the Multi Asset team.

Find out more about Pendal’s investment capabilities

Which factors are likely to impact Australian equities in coming weeks? Here’s an outline from Pendal’s head of equities Crispin Murray (pictured above). Reported by portfolio specialist Chris Adams.

THERE are a number of things to watch for in terms of potential market impact in coming weeks:

1. Policy

There may be some risk of disappointment on the policy front in coming weeks, as we move through the era of “peak policy”.

The rate of balance sheet expansion is likely to decelerate, while agreement on additional fiscal programs in the US will become increasingly difficult.

The market may also start to look through to the end of June when some of the initial measures start to roll back.

2. Geopolitics

There are also some noises on the geopolitical front. The US has dialled up the rhetoric around China’s role in the coronavirus pandemic — and followed up with restrictions around Huawei’s access to American technology.

China, for its part, has been sending messages to Australia as various government officials call for an inquiry into how China initially handled the outbreak. Sanctions have been announced against Australian barley and beef.

Despite some noise we think material restrictions on iron ore are unlikely given the impact it would have on the Chinese economy. Nevertheless, further tension here could shake market sentiment.

3. Oil

We are nearing a roll-over in futures contracts of the kind that prompted a sharp fall in oil prices last month. Fundamentals have improved as some production has been shut in and the outlook for demand improved.

At this stage a re-run of last month’s volatility looks unlikely, but this week could prove to be a key test.

Key indicators of market sentiment

We think there are four areas that are helping gauge the market’s current sentiment:

1. Gold continues to climb higher. In some ways this is serving as an each-way bet. It is a hedge on central bank policy and the potential longer-term risks that come with massively expanded balance sheets.

However if it transpires that the policy response has not been enough and we start to see widespread bankruptcies, then it is also seen as a hedge in a risk-off environment.

2. Negative rates have been raised as a possibility in the US. The Fed says it isn’t required – while not ruling it out either. The US two-year note is still trading at a premium to cash rates, which indicates the market is not yet expecting negative rates – but this remains an area to watch.

Rates moving negative would suggest the economic outcomes are much worse than expected – and would also be very negative for sectors such as financials.

3. Corporate bond yield spreads serve as a good proxy for expected bankruptcies. These have stabilised after central banks stepped in to back-stop the corporate credit market.

Another blow-out here would indicate the market thinks things are moving beyond the control of policy makers.

4. The US Dollar was volatile through February and March but, like corporate spreads, has settled down and stabilised in recent weeks. Any signs of the USD breaking materially higher against other currencies could be a sign of increasing risk aversion and be negative for equity markets.

China’s experience

As restrictions roll back in Australia and overseas it is useful to track China’s trajectory as a potential guide. China retains material restrictions at a national level, while individual cities have seen lockdowns dialled back up in response to outbreaks.

China’s economic rebound was initially quite sharp, before slowing in recent weeks and then seeming to stall at about 90% of its previous level.

Persistent weakness in some areas of discretionary spending is holding the economy back from reaching its previous level.

It will be important to see if industrial production can continue to hold up if people are buying fewer discretionary items. Services (such as eating out) have been slow to respond. In the US there are expectations that 15% to 30% of restaurants may shut.

Durable goods and industrial production has recovered quite well. Auto sales, in particular, have seen a sharp bounce given an aversion to public transport.

This is feeding through to traffic, which is picking up and may move to higher levels than pre-COVID-19. This will be a key area to watch here and in the US.

It is becoming clear that some parts of the economy will pick up faster while others may see longer-lasting, deeper structural damage. This has important implications for portfolio construction.

Find out more about Pendal’s investment capabilities

What’s the outlook for negative rates? Pendal’s Head of Bond, Income and Defensive Strategies Vimal Gor gives a snapshot here in a new video interview with online business channel Ausbiz.com.au.

Watch the video above or read the transcript below.

TRANSCRIPT

AUSBIZ.COM.AU INTERVIEWER: Is the Fed continuing to backstop equity markets going to end in tears at some point in your view?

VIMAL GOR: Yes. I don’t think this negative rates thing is about back-stopping equity markets. I think it’s more borne out of necessity.

The problem the Fed has is that interest rates are at zero, 10-year Treasury is, call it 50 basis points, and we’re going to enter into a period of quite pronounced deflation in the US economy.

And that’s because the inflation rate is largely driven by the economic cycle.

We know the economic cycle is being curtailed because of what’s happened with the virus. So we’re going to have deflation in the US of somewhere between 2 per cent and 4 per cent over the coming months.

The problem is when nominal interest rates are at zero and you get deflation, it means you get rising real yields.

Now the economy is driven by real yields, not nominal yields.

So the problem is we’re in this terrible situation where we’ve got really weak growth and we’re going to see rising interest rates in the US.

So the Fed needs to counter that somehow. But the problem is they have limited tools now.

They’d like quantitative easing, but as I said, 10-year Treasury are only 50 basis points and moving them to zero is going to do largely nothing.

They’re doing all this funky stuff. We’re buying ETFs and high yields and stuff, but that’s largely trying to throw a lot of liquidity at what is ultimately going to be a solvency issue.

So now they’re thinking about cutting interest rates negative. And I think it’s a great idea and they should do it the way Rogoff talked about it in his Project Syndicate article over the weekend.

They should do a short, sharp shock that would take rates to -2 per cent or -3 per cent quickly and force the financial institutions to have to deal with it.

They need the banks to be ready and the banks in the US are not ready. But I’m sure they’re working with the banks to make them ready, were this to become an eventuality.

INTERVIEWER: One of those tools they do have left in their arsenal is just rhetoric and the mouthpiece. And that’s what the Fed’s (Federal Reserve Chair Jerome H) Powell has effectively been trying to do — push that message onto Congress: ‘We want that fiscal assistance’. He’s doing everything in his power, it would seem, verbally to avoid those negative rates. Just how long can he keep trying to play that game?

VIMAL GOR: I think Powell has zero credibility left now anyway. Yes, we need fiscal. But fiscal is, as I said, a stop gap. It’s a liquidity issue that isn’t going to affect the long-term solvency of these companies. They’re still going to go under.

Also how much more fiscal can we do? Yes, there’ll be an infrastructure package and yes there’ll be a few more after it, but we’re already staring down the barrel of budget deficits of 20 per cent in the US.

You can throw more money after it again and again and again, but it’s the same old thing. We have this growing problem in the US since the GFC around quantitative easing, pushing up financial assets and benefitting Wall Street but not helping Main Street.

And they’re doing the same again. That’s what’s happening now. You’ve got unemployment north of 15 per cent, heading to 20 per cent in the US, and the S&P is not far off all-time highs.

This disparity needs addressing at some point.

By doing negative interest rates it actually helps Main Street and it kind of hurts the richer demographic part of the population. So it works on a number of levels.

Obviously the lobby groups and the banks will be strongly against it and people will have a tough time getting their head around it.

But ultimately when you realise that real yields in the US have been positive and negative a lot of times over the last 50 years, it’s not that much of a departure anyway.

INTERVIEWER: Donald Trump, the US president, would be happy to hear your reasoning on negative interest rates. He’s definitely in the pro camp. What’s a time-frame? You say that it should be done in a snap reaction, get things going, get things moving. So when are we likely then to see this coming to fruition?

VIMAL GOR: Well we’re going to see the unemployment numbers get worse in the short term. We’re going to see the inflation numbers — we saw CPI this week which was bad. We’re going to see that get materially worse over the next few months.

So the time is now. Whether operationally they can move before year-end I’m not too sure. The RBNZ gave the banks till the year end to fix their problems with operation and be able to handle negative interest rates. It doesn’t mean they can’t pre-announce though.

Ultimately whether the Fed does move to or not, the fact that they’re considering it is what’s important here, because the markets will now start pricing it.

As we saw this week, that markets started pricing negative interest rates already in the US and that opens up a part of the distribution that hasn’t existed before.

So therefore now it means the market will now price positive and negative interest rates.

Whether the Fed actually delivers on them or not — it’s important, but the market was already starting to price it. So that’s a really key thing.

The fact they’re having these discussions is material and given the fact that they didn’t want to counter the idea of negative rates just a few months ago.

The way they introduced negative rates in Europe, Japan — they did it incorrectly with hindsight. They did it too slowly and they did it too weakly, too slowly.

They cut rates a small amount sub-zero, then they increased it a little bit, a little bit, a little bit. You don’t deal with the underlying malaise in the economy and therefore you get the problem still there.

You get the back-end of the curve rallying, the yield curve flattens, which crunches your banks and it destroys credit creation. It makes the problem worse.

But if you’re to go in and move interest rates quickly and materially negative, we should hopefully not have those problems because you force the banks and financial institutions to lend money.

Which is ultimately the whole point of negative interest rates.

Important Updates

Pendal MicroCap Opportunities Fund (APIR: RFA0061AU, ARSN 118 585 354)

Effective 14 May 2020, the Pendal MicroCap Opportunities Fund (Fund)’s buy-sell spread will decrease from 1.40% (with 0.70% payable on application and 0.70% payable on withdrawal) to 1.20% (with 0.60% payable on application and 0.60% payable on withdrawal).

The buy-sell spread is an additional cost to you and is generally incurred whenever you invest in the Fund. The buy-sell spread is retained by the Fund (it is not a fee paid to us) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets. The buy-sell spread also reflects the market impact of buying and selling the underlying securities in the market. Importantly, the buy-sell spread helps to ensure different unit holders are being treated fairly by attributing the costs of trading securities to those unit holders who are buying and selling units in the Fund.

The reduction in the Fund’s buy-sell spread reflects continuing improvement in trading conditions. Pendal will continue to monitor market conditions and review and update the buy-sell spread regularly as required. You should therefore review the current buy-sell spread information before making a decision to invest or withdraw from a Fund.

Please refer to our website www.pendalgroup.com and click ‘Products’ for the latest buy-sell spread for each Fund.

Which way will equities markets go from here? Here Pendal’s head of equities Crispin Murray (pictured above) outlines the case for both bull and bear scenarios. Reported by portfolio specialist Chris Adams.

At the end of last week the ASX 300 had rebounded 20% from its low, recapturing just over a third of the drawdown from the February high. However this lagged the 31% bounce in the S&P 500, which has retraced about 60% of its fall.

It is tough to make a high conviction call on market direction from here.

As we have mentioned previously, the scale of the two opposing forces – economic downturn and policy response – is material.

This is why we continue to position the portfolio to perform across a range of scenarios, rather than making a heroic call on the outcome.

The bull and bear cases for equities at this point can be summarised as follows:

Bear case

1) Risk of a second wave of infection

There is a widespread view that the US is re-opening too quickly. The risk is that a second wave of infections could prompt a return to restrictions, hitting the economy and market sentiment.

There is some mitigation from the scale of testing, which can help identify and contain outbreaks on a localised level. There have been flare-ups in China and South Korea which will provide some indication of how successfully this can be managed. Case numbers therefore take on added significance in coming weeks.

2) The economic rebound is overstated

A US survey suggests 80% of people laid off in recent weeks believe they will soon been re-employed. The usual ratio is 10-15%. This reflects a high degree of optimism that there will be jobs to return to. In the meantime the government is back-stopping incomes.

The risk is that changes in consumer behaviour are reduced, but ongoing social distancing restrictions dampen the rebound. This could mean more precautionary saving, softer demand, business closures and fewer jobs –which could feed through to areas such as housing, creating another feedback loop.

3) Valuation

BY the end of last week the ASX 300 was down only about 18% year to date despite FY20 earnings revisions of -20% to -30%, suggesting markets are not that cheap. We are also seeing the relative performance of some growth stocks quickly break back to all-time highs.

An additional factor to watch here is the view on whether US rates go negative. Various technical factors highlighted this debate last week. However the two-year note continues to trade at 16bps yield, suggesting it is not yet a foregone conclusion.

The prospect of negative rates might provide some short-term support for equities – in the sense that they become relatively attractive. However there are also implications for an economic outlook which is worse than the equity market is currently factoring in.

4) Technical resistance

The rapid and almost two-thirds retracement in the S&P 500 has now neared an important technical resistance level.

5) Politics

While the market is not yet focusing on the US Presidential election, in coming months it may start to pay attention to what is shaping up as a close race.

One factor to consider is that if the Democrats do win, they will control the White House and both Houses of Congress. We may start seeing talk of tax reform – rolling back Trump’s corporate tax cuts, which could reduce earnings by as much as 20%.

The other factor is China trade. The election is likely to focus on maximising the turnout from a candidate’s base, rather than swaying a marginal voter.

This means increased China-related rhetoric and the risk of some issues on trade, which could also feed through to corporate earnings. It is fair to say the bear case is easier to make, given how quickly the US market, in particular, has run.

That said, there is a cogent rationale for the market’s rebound – and the possibility of it continuing.

Bull case

1) Policy

This is the lynchpin. The Fed’s balance sheet has surged from $US4 trillion to $US6 trillion in short time with more to come. This effectively underwrites the investment grade credit market and funds government debt.

The combination of monetary and fiscal response is estimated at around 25% of US GDP.

At a global level, the “free liquidity” – surplus liquidity relative to GDP growth – is estimated at around 9% of global GDP. This is not yet the scale reached at the depth of the GFC. Nevertheless, this liquidity is finding its way into financial asset markets and continues to fuel outperformance of long-duration growth stocks.

This is important because governments and central banks are effectively saying they will continue to pull the policy lever as long as it is needed.

2) Health breakthrough

There is nothing concrete here yet, however vaccine trials have been brought forward and we may have a result sooner than many anticipate.

There is also mounting evidence that a combination of existing drugs and therapies have had some success in helping reduce the length and severity of infections. This is important in helping manage stress on medical systems for countries pursuing herd immunity.

3) Economy

There are signs an increasing number of companies think the economy may have troughed in April. As recently as two weeks ago only 25% of US companies thought the economy’s trough would be in April. Now it’s 40%.

A sense of having turned the corner is good for market sentiment.

4) Sentiment

The market remains bearishly positioned. Cash levels are as high as during the GFC. Surveys suggest most people expect the market to go down from here. It is not a euphoric market.

There is also a sense the market may have accepted near-term earnings will be terrible – and are looking through these to FY21. This means near-term earnings announcements may not be as relevant as usual – particularly given the dispersion in the range of S&P 500 earnings estimates is at 15% versus 3-7% in normal times.

The analogy here is that we are in the doctor’s waiting room and haven’t yet had the test results. Until then we can choose to be optimistic or pessimistic.

Find out more about Pendal’s Australian equities investment capabilities