Changes to the Pendal International Share Fund (APIR: BTA0056AU, ARSN 087 593 299)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal International Share Fund | Pendal Concentrated Global Share Fund No.3 |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50%1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

Distribution frequency

The Fund’s distribution frequency will change from quarterly to annual. Effective 21 February 2020, the Fund will generally pay distributions at the end of June each year.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund/.

[1] The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Changes to the Pendal Core Hedged Global Share Fund (APIR: RFA0031AU, ARSN 098 376 151)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal Core Hedged Global Share Fund | Pendal Concentrated Global Share Fund Hedged |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50% 1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) hedged to AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

The Fund’s foreign currency exposure will continue to be fully hedged back to the Australian dollar to the extent considered reasonably practicable.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund/.

1 The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Changes to the Pendal Core Global Share Fund (APIR: RFA0821AU, ARSN 089 938 492)

Investment Manager

We have decided to replace AQR Capital Management, LLC (AQR) as the investment manager of the Fund and appoint the Pendal Global Equities team. The change will take place on or around 21 February 2020.

Pendal’s concentrated, benchmark agnostic investment process aims to add value through active bottom-up stock selection and fundamental company research, whilst AQR’s investment process employs quantitative investment strategies that aim to add value through active stock and industry selection and proprietary investment research.

The Fund will continue to be an actively managed portfolio of global shares. The Fund will invest in companies that offer attractive investment opportunities predominantly in markets such as the USA, UK, Continental Europe, Asia and Japan.

The new investment strategy has been implemented by the Pendal Global Equities team for the past 3 years. Further information about the team is provided below.

Why are we making the change?

We have decided to make this change because we believe it is in the best interests of investors to appoint the Pendal Global Equities team to manage the Fund, as a result of our ongoing review of the investment manager. Pendal’s investment process is expected to deliver an improved investment outcome, providing investors with better risk-adjusted returns over the medium to long term.

Fund Name

We are also taking this opportunity, with effect from 21 February 2020, to rename the Fund as set out below:

| Previous Name | New Name |

| Pendal Core Global Share Fund | Pendal Concentrated Global Share Fund No.2 |

Management Fee and Buy-Sell spread

Effective 21 February 2020, the Fund’s management fee will decrease from 0.97% pa to 0.90% pa. At the same time, the Fund’s buy-sell spread will increase from 0.10% to 0.50%1 reflecting the higher brokerage costs expected to be incurred by the Fund following the change in investment process.

What will stay the same?

The Fund’s benchmark will continue to be the MSCI World ex Australia (Standard) Index (Net Dividends) in AUD and the Fund will still aim to provide a return (before fees, costs and taxes) that exceeds this benchmark over the medium to long term.

About Pendal Global Equities team

The Pendal Global Equities team is led by Ashley Pittard. Ashley was appointed as Head of Pendal’s Global Equities boutique in 2016 and is responsible for setting the strategy, processes and risk management for both the boutique and funds managed within it.

Ashley’s experience in the finance industry spans over 24 years, including 20 years as a global equities fund manager.

The five person Global Equities team is organised on an industry basis and has an average finance industry tenure of over 10 years. The team are also able to utilise Pendal Group’s global resources including those of J O Hambro Capital Management Limited (100% owned by the Pendal Group), an investment manager with offices in London, Singapore, New York and Boston.

You can access information on Pendal’s global equity strategy on our website, at https://www.pendalgroup.com/concentrated-global-share-fund

[1] The buy-sell spread is retained by the Fund (it is not a fee paid to Pendal) and represents a contribution to the transaction costs incurred by the Fund such as brokerage and stamp duty, when the Fund is purchasing and selling assets.

Cast back to the year 1998 when Paul Wimborne, co-manager of the Pendal Global Emerging Market Opportunities Fund started looking at Emerging Markets, and the world was a different place: the US was impeaching its President, Argentina was heading towards default and we had a big tech bubble forming on the NASDAQ with unsustainable returns, and of course the Australian cricket team retained The Ashes. Unprecedented times indeed!

But consider the structure of today’s emerging markets and its clear there have been some more permanent changes. Emerging economies are a fairly disparate group, with many barely recognisable to the asset class that existed in the 1990s and 2000s, where a crisis in one particular market usually spread rampantly across many others.

In the past three decades, many of these countries have embarked on monetary and fiscal reforms, building defences against such external shocks. This difference was evident through the past year when the US dollar strengthened, prompting investors to exit emerging markets. Countries with these policy defences escaped relatively unscathed, while others like Argentina and Turkey showed their vulnerability.

Leading investment research firms like Lonsec argue that today’s emerging markets warrant a dedicated place in an overall global equity portfolio. While emerging markets only represent around 10% of the MSCI All-Country World global share index, they are materially underrepresented based on their true share of the global economy. Today, emerging markets account for 59% of global GDP. There are now more than 120 companies that have joined the Fortune 500 which are facing into emerging markets.

So why does this discrepancy in recognition persist? There are a few reasons but the prime explanation is found in the underlying structure of share market indices. They are generally based on market capital weightings, which essentially represents the total value of a company’s shares on issue. Take the global technology behemoths for example — Apple, Microsoft, Google and Amazon — their collective representation in the index accounts for around 8% of the developed markets index, not far from the total index weight of all emerging markets.

Valuations now attractive

China epitomises the extent of this discrepancy. Despite its status as the world’s second-largest economy, China is still defined as an emerging market due to low household income levels, which are just 15% of what they are in the United States.

“Valuations look attractive, even in spite of trade wars …”

Veronica Klaus, Head of Investment Consulting, Lonsec

And the US-China trade war and associated rhetoric has played its part in driving lacklustre returns from emerging markets in recent years, leading many investors to write off the asset class.

“Valuations look attractive, even in spite of trade wars …” according to Veronica Klaus, Head of Investment Consulting at Lonsec.

Lonsec believes many of the fears are overdone, although this is not a blanket statement to cover all 1,149 stocks in the emerging market index as they’re not without risks. Klaus refers to the volatile nature of parts of the emerging world. For the year to date, Chile’s share market has declined by 7%, while Russia is up 32%, precisely why Lonsec impresses upon the importance of active management for the asset class.

Lonsec argue for an active, selective approach to emerging markets for clients with a long term growth horizon. Klaus says “What is important is to look for active management, and look to a manager and a strategy that is moving away from these higher risk scenarios and looking towards the long term valuation opportunities.”

Lonsec sees value stocks within emerging markets as being particularly cheap, “trading at their largest discount since December 2001”.

“It’s much more attractive compared to US shares and Australian bonds.”

Lonsec holds an overweight stance in emerging markets across their suite of balanced or growth oriented model portfolios.

Click here to download the complete article

Importance of the country’s business model

Paul Wimborne, co-manager of the Fund concurs on the point of being selective. We are not compelled to buy any stock; regardless of what is or isn’t in the benchmark, the investment has to measure up on our country-level macro assessment and the bottom-up fundamentals of a company.

“The key question you have to ask yourself is, do I want to be invested in that country…or not?”

Paul Wimborne, Senior Fund Manager

We don’t say bottom-up analysis isn’t important in emerging markets, but we are very different to the conventional approach. Our bottom up analysis recognises that the key factors we put into our company analysis models are actually top-down in nature. Our process is inherently designed to reflect the belief that emerging markets go right or wrong at the country level.

Take Argentina’s 45% stock market crash in August this year; it didn’t matter if you were in the best Argentinian company that day. The business model of that company is not going to help you out. “The key question you have to ask yourself is, do I want to be invested in that country…or not?”

In emerging markets there are always countries that go wrong. We need to satisfy ourselves with regard to what we like about the macroeconomic environment that means the equity market is going to do well. Then we find the companies that will benefit from the macroeconomic environment and avoid companies that are susceptible. It is vital to understand the country’s operating model in all of its guises, as it is intricately linked to the success of a company.

Unlike in the developed world where there is a greater degree of synchronicity in economic factors between countries, emerging markets feature a much more diverse group. Variables like GDP, interest rates, inflation, regulation, cost of capital and terminal growth rates can be materially different and much less correlated relative to developed markets.

When will emerging markets turn?

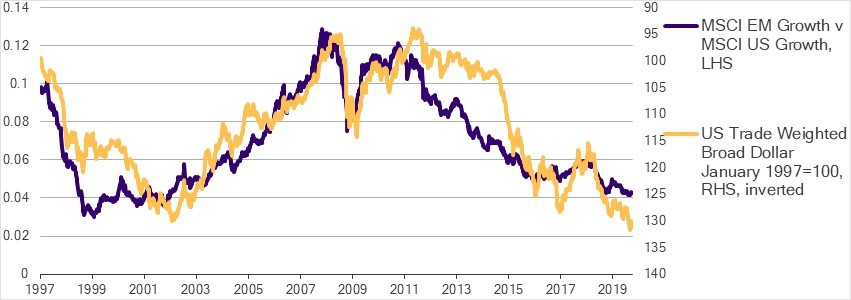

Our team believes there are two key conditions conducive to delivering strong performance in emerging markets: robust global growth and a weak US dollar. Clearly neither of those factors are in place – and until they are the team are being very selective and taking advantage of idiosyncratic opportunities in the asset class.

We do think the second of these catalysts may come through. When that does happen we should see emerging markets begin to outperform developed markets, in keeping with their historical relationship.

Weaker dollar to drive EM recovery

Source: Pendal, Bloomberg as at 4 October 2019

The rationale for this to occur at some point is fairly clear. First, the US dollar retains its reserve currency status. This means the US can borrow lots of money at cheap rates, and they are certainly borrowing plenty and driving up the deficit. Heading into the US election year, all signs are there for whoever takes office, that spending will all but continue and add to the deficit. The question will be who is going to finance the fiscal deficit? Over the last few years it has been the Fed and sovereign investors like China that have been buying US treasuries and adding to their expansive reserves.

Evidence is now emerging that China is increasingly moving to price commodity contracts outside of the US dollar payments system. At the margin, this means there is less rationale for holding all of your reserve assets in US dollars. So if it’s not foreigners buying as many US treasuries, and it’s not China or the Fed, who will be financing the deficit?

Evidence from prior crises shows that typically when currencies blow out, it’s driven by financing of enlarged fiscal deficits. When they can’t get foreigners to finance it, the Government turns to the local banking sector and you get a crowding-out effect. Essentially this means the banking sector becomes constrained with less money to lend to the domestic economy. The recent spike in US repo rates may have something to do with this dynamic.

When and how this happens can’t be predicted with certainty, but when it does we’re likely to see growth-focused investors switch preferences from NASDAQ tech stocks to emerging markets. But until this occurs we remain focused on country-specific, self-help opportunities through countries like India, Korea and Turkey.

The team believes India has the strongest growth potential over the next few years. Among the many differentiators, it is one of the only countries in the world which hasn’t had an increase in the credit-to-GDP ratio since 2008.

One reason is a number of loans made in the banking system went bad prior to 2008. The Modhi-led Government has made a concerted effort to redress shortcomings of the previous Bankruptcy Code. They have strengthened the banking sector with fresh capital and we should see a credit-driven recovery for the banking sector. There has been a delay in this cycle as credit growth has fallen in response to the collapse of a non-bank lender. However, we believe the recovery should eventuate, bolstered by a series of other reforms implemented under the Modhi Government.

Then there’s Korea, a very different opportunity. Korea has been one of the cheapest markets historically, largely due to its poor governance record. This is changing as political and social pressure is driving different behaviour in the ‘chaebol’ conglomerates which dominate Korea’s corporate landscape. One key, tangible benefit is an increase in payout ratios, helping lift Korea’s traditionally poor dividend yield. We see this trend continuing, which will likely lead to a substantial re-rating of Korean equities and potentially, its eventual graduation into the developed markets category.

Source: MSCI, Bloomberg as at 31 December 2018. Free cashflow is cashflow from operations less capex

Other bright spots in the emerging market world are Russia, Mexico and Turkey — all for very specific reasons. Turkey serves as an example of how quickly conditions can turn positive. With 2019 GDP growth revisions of -1.5%, Turkey was until recently the second-weakest of all emerging economies this year. However, the pricing of that forecast slowdown became wildly excessive, and the Turkish stocks we bought in May have outperformed substantially. Interestingly, Turkey’s 2019 GDP growth estimate has since been revised upwards, suggesting that the worst of the selling pressure (and the greatest opportunity for investing) was right before the turn in May.

These and other examples serve to validate our view that success in emerging markets relies on a balanced assessment of fundamentals and valuation. We look to use both to identify top-down, country-level opportunities in emerging markets, irrespective of how good or bad the global environment is perceived or otherwise at that moment. We see the key macro catalysts for re-rating as likely as conditions in the global economy evolve. When they do arrive, it will likely add to success for our country-specific investment decisions.

We think the challenges and opportunities in emerging markets underpin the importance of our country-driven approach. We continue to identify opportunities — such as those discussed — which exist despite the headwinds to the asset class more broadly. Meanwhile, we monitor the landscape for signs of a change in those headwinds, positioning the portfolio to benefit at the point when the tailwinds return to emerging markets.

Thai capital Bangkok is known for vibrant street life and the boat-filled Chao Phraya River… but is it a good investment?

One of the reasons we believe it’s crucial for Emerging Market (EM) investors to be knowledgeable about the history of the asset class — and the countries in it — is the dynamic nature of different emerging markets as they grow and develop.

There is possibly no country in the EM universe that has undergone a greater shift in its macroeconomic fundamentals — and the relationship of its capital markets to those fundamentals — than Thailand.

The Asian crisis of 1997 was one of the great landmark events in the history of EM.

Whereas the 1994-95 Tequila crisis in Latin America was confined to a group of countries with a history of economic volatility (see: Latin American debt crisis, 1982), the Asian crisis tore through a regional economic miracle.

First domino to fall

Thailand was the first domino to fall in 1997, with the default of major property developer Somprasong marking the beginning of the crisis.

Looking back, in the late 1990s Thailand was as capital-deficient, liquidity-driven and high-beta as Turkey, Argentina or Russia. The turn in global liquidity in 2002 would set in motion an economic and stock market boom of similar magnitude to those other countries.

However, a genuine transformation of the economy occurred at this time, with Thailand developing deep and widespread capability in exports of electronic products and processed foodstuffs, as well as a highly successful tourism industry.

As well as driving GDP growth, this shift massively strengthened the Thai current account balance, which has moved from a deficit of over 8% of GDP in 1995 and 1996 to a surplus that has averaged nearly 9% of GDP in the last three calendar years.

This has in turn led to a 180-degree turn in the policy objectives of the Bank of Thailand (BoT), which went from holding the baht up (to keep imports cheap and hard currency-denominated debt affordable), to holding the baht down (to maintain export competitiveness).

The BoT has pursued the latter strategy as single-mindedly as any other mercantilist EM.

Challenges ahead

What is more, Thailand is approaching some challenges as the limits to conventional interventionist-mercantilist policy are reached.

These include disquiet among trading partners at the suppressed valuation of the currency, and the zero lower-bound to policy (policy rates in Thailand were recently cut to 1.25% but are likely to continue to fall).

Unconventional monetary policies such as asset purchases, directed lending and negative rates could be employed, but the large current account surpluses will continue to pose a problem for Thai policymakers.

The upward pressure on the baht does not make Thailand particularly attractive for equity investors.

The hit to competitiveness from the stronger currency has an overall drag on the economy, while the central bank’s sterilisation of capital inflows limits liquidity growth.

Domestic demand in other late stage-mercantilist-interventionist Asian economies like South Korea and Taiwan has consistently disappointed, while returns on capital (particularly in the financial system) have trended lower and lower.

This also has echoes of the Eurozone, which has also chosen to suppress demand in order to run huge current account surpluses. Indeed, a current account surplus can be thought of as representing a country’s deficiency of demand relative to productive capacity.

Equity market opportunities

As we have seen in Europe, South Korea and Taiwan, equity market opportunities tend to be concentrated in export sectors during global upswings.

We continue to see the potential for US Federal Reserve accommodation to improve global US dollar liquidity and weaken the dollar in the coming year.

This has the potential to drive very strong economic uplift and equity market returns in the capital-deficient, liquidity-driven and high-beta emerging markets.

Thailand was one in 1999; it isn’t 20 years later.

James Syme is a London-based senior fund manager with Pendal subsidiary J O Hambro.

Disruption is the key investment theme of the decade and even fixed assets such as real estate are not immune.

The winds of change are buffeting all major investment classes in the sector, from office and commercial through to industrial and retail properties.

A recent briefing by senior managers of AEW Capital Management – underlying manager of the Pendal Global Property Securities Fund – highlighted the risks and opportunities thrown up by unprecedented market shifts occurring against a backdrop of one of the strongest runs by the sector in decades.

Like any sector, property moves in cycles – and globally the decline in interest rates has put a floor under the market.

The JLL Global Office Index – which tracks returns from commercial office assets – jumped 49 per cent from its 2004 low to 2008 peak. It’s still risen by about 32 per cent in the subsequent nine years – a more modest, but sustainable performance.

The changing valuation equation

Underpinning global property markets are negative yields on sovereign debt, coupled with a heightened risk of geopolitical uncertainty.

Against this backdrop, real estate remains an investment class that continues to offer sustainable yields along with diverse investment opportunities offering sustainable growth. But capturing that growth can be a challenge.

Large direct holdings of property assets can hamper an investor’s ability to quickly take advantage of market shifts, both locally and abroad.

That’s one reason real estate investment trusts have become an attractive investment option, says AEW director J.T. Straub.

“The returns screen has always been attractive,” he argues. “We see the returns of the past several years continuing. There are also attractive sub-sectors such as data centres.

“In addition, their liquidity gives us flexibility. So for example, we’re underweight Hong Kong, and use these types of environments to take advantage of situations.

“To go from a 6 per cent to 10 per cent property allocation takes time if you hold property directly”, Straub says. “But if you invest via a REIT, the flexibility means shifts in portfolio allocations can be achieved quickly and painlessly.

“The key is that the central banks are helping. Once one central bank cuts, others have to follow. It is likely the Fed will cut again and others will too,” says AEW’s Singapore-based Peter Ho. “As rates decline, valuations will go up.”

This will continue to drive demand for sustainable returns and keep real estate markets buoyant, he says.

“There is a lot of capital coming into the sector that can’t find a home,” says Ho. “To get into Australia, you need to know the REITs. It is the same in Singapore.”

AEW doesn’t take regional bets; rather it takes sectoral bets. It holds an overweight exposure to offices in Asia, for example, and underweight in other regions.

Looking broadly at the global market, AEW is underweight in areas of falling rent such as Hong Kong office and retail sectors, along with US shopping malls.

Similarly it is underweight retail in both Japan and Singapore, even though the decline in rents is slowing.

Areas of rising rents, such as US industrial and ‘other’ residential, along with UK and Australia industrial rents and data centres in Asia, has prompted it to take an ‘overweight’ investment stance.

New economy, new opportunities

Areas of the ‘new economy’ are throwing up both challenges and opportunities.

In the commercial office sector, flexible working operators such as WeWork have attracted a lot of attention, bringing both opportunity and threat. This sector alone accounts for an estimated 7 per cent of total stock.

“In Amsterdam, co-working is a large portion of the market, but it is still less than 15 per cent,” AEW’s Straub says.

“In London it is around 6 per cent. In Sydney and Melbourne, around 2 per cent.”

Straub argues growth in co-working has helped drive net absorptions in the office market globally – although the difficulties of WeWork’s IPO has focused attention on the downside potential.

“There is a liability mismatch,” he says. “Some see [flexible working] as being bad for REITs,” AEW’s Ho says. “If co-working continues its current trajectory, it will double the demand for space.”

“The challenge of the WeWork model is that since it is loss-making with a long-term lease, how much space do you want exposed?

“There is potential credit and liquidity risk. For example Regus has better credit quality.”

Environmental, Social and Governance impact

Listed property investors are also increasingly taking into consideration environmental, social and governance (ESG) factors, says AEW’s Ho.

ESG has gone from “nice-to-have to a need-to-have over the past decade”, he says. And there’s a range of data demonstrating a correlation between higher ESG scores and profitability.

Commercial properties in particular can be energy-intensive and tend to have environmental impacts —not only in construction but also through ongoing maintenance programs.

Industrial property revolution

Demand in the industrial real estate sector has also been driven by e-commerce.

As digital natives, Millennials are driving a wholesale shift in demand for industrial real estate.

“Increasingly a shed is not just a shed,” as AEW’s Straub puts it. Occupants are demanding automated storage systems, renewable energy and tracking systems spanning fleet management through to efficient truck-dock management.

“In Tokyo, there has been a lot of industrial supply,” AEW’s Ho says. “In three years there’s been a 50 per cent increase in industrial warehouses. Demand is so strong even with record absorption. And with [a low] 2.7 per cent vacancies, rents are rising.”

The strong underlying demand has AEW positive on the sector. The manager is overweight industrial assets in Asia, Europe and North America.

Data centres are an adjunct sector to new economy real estate. The rise in cloud computing is driving demand both for ‘last-mile’ centre operators located near client offices and data centres servicing a single client, which can be located in distant locations.

Either way, these centres are big energy users with ready access to electricity a prime driver of location.

Still, the longer the present market strength continues, the more investors will be asking how much longer can it go.

“We keep waiting for real estate to over-build,” AEW’s Straub said. “That’s how it ends.

“But the banks have been tightening lending restrictions – they’re not over-lending.

“There will come a time, but we’re not there yet.”

Edwina Matthew, Head of Responsible Investments at Pendal, talks about our approach to responsible investing and current issues we have been working through with investors.

James Syme (pictured) is a London-based senior fund manager with Pendal subsidiary J O Hambro.

There are two broad drivers of the emerging market equity asset class: global growth and US dollar liquidity. This update serves to point out that neither of these drivers is showing any sign of being supportive, but also that a robust investment process and differentiated portfolio can still find opportunities in the asset class.

Global growth is sick and failing to respond to treatment because no treatment has been applied. In the developed world, the US has seen the weakest ISM manufacturing survey in 10 years as well as weakness in the crucial services data, while eurozone 2019 real GDP growth forecasts have been steadily revised down to the current level of just 1.1%.

In the emerging world, recent Chinese data has been particularly soft, with fixed asset investment (+5.5% year-on-year), retail sales (+7.5% year-on-year), industrial production (+4.4% year-on-year) and exports (-1.0% year-on- year) all coming in both low and below expectations.

Exports and the dollar

The exports of the most cyclically-exposed emerging economies tell a similar story, with Korean exports -11.7% and Taiwanese exports -4.6% in the year to September. Meanwhile, the inherent strengths of the US economy relative to the rest of the world, combined with the asymmetric impact of the trade war, have kept investors more optimistic about US assets and/or more pessimistic about the need to have sufficient US dollar-denominated assets. This has happened despite the enormous increase in the US fiscal deficit (federal government gross issuance will be around US$11.3 trillion in FY2019, up from around US$10 trillion in FY2018, with the majority of that issuance at maturities of six months or less), which represents a huge drain on global dollar liquidity.

The net effect of this has been a resumption of the uptrend in the US dollar relative to other global currencies that began in 2011. The slide in growth and tight liquidity have been transmitted into emerging economies, with negative GDP growth revisions in almost all of the 26 emerging market economies during 2019. Even previous areas of strength, such as India, Pakistan and Thailand, have been caught up in the slowdown, with the 2019 GDP growth estimate revised down 0.8% in India, 1.2% in Pakistan and 0.8% in Thailand. Global conditions remain tough.

Country focus yields opportunity

Our investment process is designed to seek opportunity, principally at the country level, and we have found various areas of opportunity through our process this year. One would be areas where GDP growth estimates have held firm, including Eastern Europe, where aggregate GDP revisions are about flat year-to-date. We have held some exposure in the Czech Republic, which has been a slight laggard, and considerably more in Russia, which has substantially outperformed.

Another source of opportunity is in the pricing (both equity and currency) of these macro conditions. Even where growth is weakening, panicking investors can drive valuations to levels that overstate the challenging fundamentals, and we aim, through a disciplined monthly review, to identify these opportunities.

One such opportunity has been Turkey. With 2019 GDP growth revisions of -1.5%, Turkey has been the second-weakest of all emerging economies year-to-date (Brazil, at -1.6%, is in last place). However, in May the pricing of that slowdown became wildly excessive and the Turkish stocks we bought at the end of that month have very substantially outperformed (and, importantly, have actually made money for investors). Interestingly, Turkey’s 2019 GDP growth estimate has in fact been revised up since the end of May, suggesting that the worst of the selling pressure (and the greatest opportunity for us) was right before the turn. Most, perhaps all, investing is a trade-off between fundamentals and valuation, and we look to use both to identify top-down, country-level opportunities in EM equity, no matter how good or bad the global environment is at that moment.

With another cut from the RBA in October and expectations for further easing, in this update we examine the outlook for one of the central bank’s key targets; inflation. Our cash manager, Steve Campbell assesses the direction for the other – the labour market, which received greater emphasis in the latest statement from Governor Lowe. Meanwhile, the path of domestic credit continues to be directed by the global macro backdrop and as such we explain why we maintain flexible positioning.

Finally, humans’ impact on the environment has garnered even greater attention over the past several months and its importance for our clients continues to grow. We explain the evolving area of impact investing and illustrate the positive contributions it makes to the environment and broader society.

Australian Quarterly Update

Updated asset allocation ranges and neutral positions

Following a review of the asset allocation ranges and neutral positions of Pendal’s diversified funds (Funds) and Pooled Superannuation Trusts (PSTs):

• the asset allocation ranges will be changed effective 6 November 2019 and

• the asset allocation neutral positions will be changed effective 6 November 2019.

Details of these changes can be found here. The Funds’ Product Disclosure Statements (PDS) have been updated and are available here.

The changes are expected to deliver an improved investment outcome for investors through better expected risk-adjusted returns. The changes reflect our latest asset class assumptions for return, risk and inter-asset class correlations and position the funds to take advantage of future market conditions.