Ashley Pittard, Head of Global Equities at Pendal recently presented his thoughts on the extent of risk that has developed in global equity markets at the Portfolio Construction Forum’s Strategies Conference 2019 – “20/20 Vision” . This article outlines the insights shared around why investors need to adopt a different mindset when it comes to investing in global equities in the 2020s.

Today global equities investors are facing into markets where the risks go well beyond trade wars and currency tantrums.

I’m proud of the first quartile performance Pendal’s Concentrated Global Share Fund has achieved since we commenced.

But it’s now more important than ever for investment managers in the global equities sector to have the right active strategy for the 2020s.

The extreme risk in global equities right now requires a different mindset as we enter the new decade.

September 15 marks the 11th anniversary of the Lehman bankruptcy and Global Financial Crisis (GFC).

That event sparked one of the greatest credit and equity bull markets in history as central banks adopted extreme and unprecedented monetary policies.

Along with conventional monetary policy actions including 735 interest rate cuts around the world, central banks took unconventional actions such as $US13 trillion worth of quantitative easing which essentially refers to “printing money”, preventing debt default and deflation.

End of the post-GFC era

Over the past ten years broad investment in global equities has been a great investment decision.

Investing in an index fund, exchange traded fund or a growth theme such as tech stocks would have done very well for your retirement savings instead of holding money in the bank.

After the GFC investors benefited from tail winds that drove share prices higher – such as falling interest rates, lower volatility, a declining Australian dollar and quantitative easing.

But that’s now changing.

The 2020s will be very different to the past decade.

In the new environment investors will need to be very selective rather than pursuing broad market exposure for their portfolios.

Macro supports such as cheap money and big government balance sheets won’t provide a blanket for all listed companies.

At Pendal we are contrarian, long-term fundamental stock pickers when it comes to global equities — so this environment plays to our strengths.

Markets in the new phase

Why am I so confident that these 10-year tail winds will become headwinds – even when volatility measures suggest risk is low in global equities?

It’s a hard ask for market valuations to be compelling when the market is trading at all-time highs. Price-to-Earnings ratios are over 17x and the S&P500 Index has grown to nearly four times its value since its GFC lows.

Bifurcation in the market is extreme and distortions are occurring within equity markets. We have a handful of mega cap technology-related stocks that have carried the market higher, while at the other end of the spectrum sectors deemed to be eternally disrupted have languished.

Growth sectors are significantly over-valued on traditional historical measures while value sectors are shunned.

This year just 6 % of the MSCI World Index stocks have accounted for 53% of the return for the global equity index.

Meanwhile, interest rates are down a long way. We have had 29 cuts from central banks in 2019 and government bond yields for the largest economies are at a 120-year low.

It is hard to say they will be going significantly lower. Consider the US 10-year bond as a proxy. In 2012 when the market believed the euro would break up and European banks would be nationalised, the US 10-year bond touched 1.36%. In 2016 when the ‘Brexit’ vote occurred, it touched 1.36%. In August it has drifted past the 1.75% level.

The Aussie dollar has collapsed from $1.10 over the last decade to hover around the US$0.70 level within a small range. Currency volatility for the major economies is at the lowest level since 1992.

But we have just started to see the US officially label China a currency manipulator.

It is timely to recall the 1995 Plaza Accord, a joint-agreement between France, West Germany, Japan, the United States and the United Kingdom, to depreciate the US dollar in relation to the

Japanese yen and German Deutsche Mark by intervening in currency markets. This event turned currencies upside down at the time and placed Japan into its lost decade. This event turned currencies upside down at the time and placed Japan into its lost decade.

It’s interesting that many economists saw this accord as a direct response from the US to the threat from Japan’s growing status as an economic superpower.

In my view equity risk is the highest in more than 20 years – regardless of what traditional volatility measures suggest.

When you have $US13.7 trillion of negative yielding debt globally investors have been pushed up the risk curve to chase ever decreasing yields.

And when you fundamentally change the value of cash massive distortions occur. We are seeing this on many levels.

Global debt is now 3.2 times the size of global GDP – again at an all-time high.

We have been here before

The tech sector – especially the FAANGs (Facebook, Amazon, Apple, Netflix and Google)- have been the darlings of the bull market for the last 10 years.

Real estate and utilities stocks have also been drivers of market returns, thanks largely to declining interest rates.

But the elephant in the room is the tech sector.

It has tripled its index weight since the GFC and doubled its index weight in the US market over the past five years.

Tech has been at the epicentre of this self-fulfilling circle — declining interest rates, exploding debt and rampant passive investing have helped to triple its representation of the market.

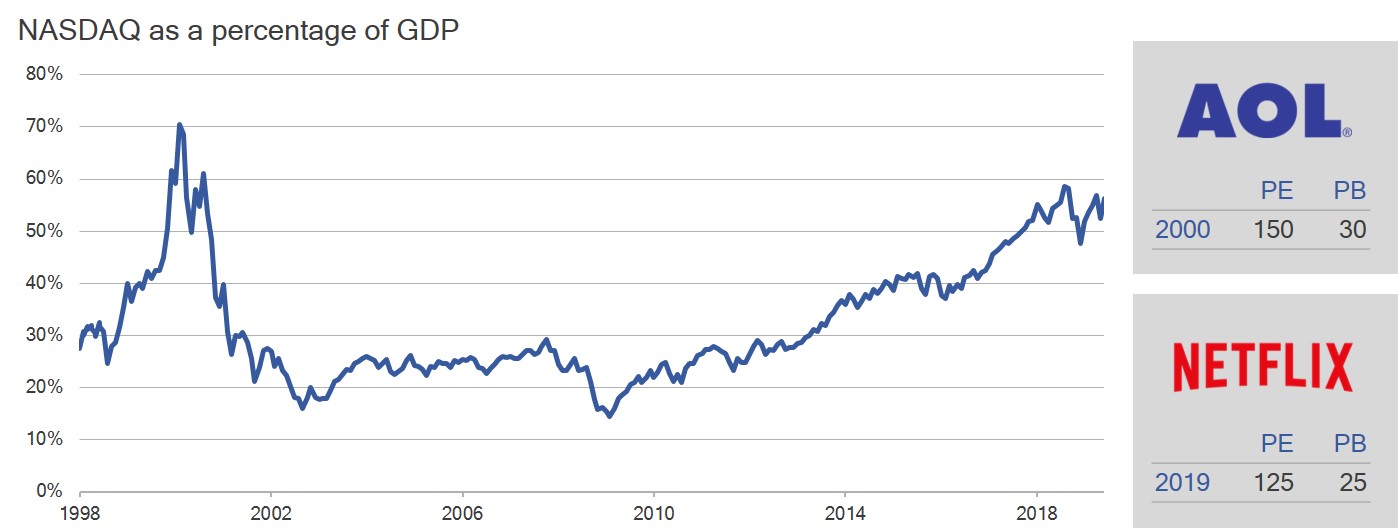

No doubt these are great businesses but it’s amazing how big their market capitalisations are — especially when compared to the GDP of some countries.

If we use the 2000 technology bubble as another proof point, the valuations again are stark.

It’s uncanny how AOL at its peak traded at similar levels to Netflix today.

Look at the metrics on the right hand side of this graph:

* Source: Bloomberg, Pendal. PE refers to price-earnings ratio, PB refers to price-book ratio.

You could argue about the relevance of using a price-book ratio for these tech names but as a long term valuation tool across different sectors, price-book is still a clean gauge of value.

And Nasdaq as a percentage of GDP is near historical bubble levels.

The extreme size of valuation premiums is a key risk driver.

Passively fulfilling a virtuous cycle

Here’s another aspect of the self-fulfilling circle. Passive and index-hugging strategies are reinforcing these valuation trends.

Over the past 10 years $US4.1 trillion has gone into passive investment funds versus outflows of $US1.5 trillion out of active.

In the year-to-date we have seen 65% of stocks in the MSCI World proceed into bear markets as passive inflows top $US7.4 billion and outflows from active strategies top $US22.4 billion.

The issue here is index and traditional strategies — by their inherent design — see more and more investors bet on higher growth for what has already risen.

This creates distortions in the market as passive ETFs focus on the largest companies in a sector, not the best companies.

Why we’re different

At Pendal, we are clearly very different.

We don’t look at the largest companies — just the best companies.

We focus on leading number one or number two franchises in their space when they are out of favour — regardless of size.

That is the lowest cost producer if it’s a commodity or largest market share if it’s a bank. We like monopoly assets.

We look at industries horizontally — not vertically as do many traditional index strategies.

We focus on fewer higher quality businesses and build a deep understanding of them like a business owner would.

We launched our Concentrated Global Share Fund three years ago and we have been very happy with the 1st quartile performance over the three-year period which reflects this very different approach compared to passive index following strategies.

Our philosophy and process has been the same since I started at BT Australia (the former entity name of Pendal) more than 20 years ago.

We have a universe of about 500 leading businesses that we follow.

We spend a lot of time focusing on disruption in industries. Usually we are buying businesses when we think they are cyclically depressed — while the market may think they are structurally impaired.

In our experience, only 15-20% of the market is attractive at any point in time.

You need to be very selective to grow wealth over the long term. Our top 10 holdings (see table) are very different to the index. We have a very large active positions.

We hold specific industry leaders such as Anheisser Busch Inbev – a leader in the beverage market.

We hold Colgate – makers of toothpaste around the world. We hold Total – Europe’s leader in oil and gas production.

We don’t hold these companies because they’re included in the Index or have driven returns. We hold them for very different reasons.

Consider the recent Amazon Wholefoods acquisition as an example.

The consumer staples sector shows how we like to research, stay patient and use disruption to our advantage.

We focus on the best businesses, understand fundamentally how they work, then stay patient and wait until they are out of favour.

There is no doubt the Amazon Wholefoods deal will change food distribution globally.

As a result of this disruption the market discounted the sector as they questioned the brand value longer term post the deal.

We looked at the industry differently and focused on market share and their return on investment (ROI).

It was clear you only wanted to focus on P&G and Colgate with greater than 60% market share and 100% ROI.

We never wanted to own Kraft Heinz, Campbell soup or Kellogg’s due to their lower market shares — even though they were larger in the index.

Think differently to drive different results

Overall I believe you need to think differently, have a concentrated highly active and very selective stock picking approach,

Think like an owner in a group of #1 unique premium assets, be patient on valuation and get paid a dividend to wait while the business normalises.

This will serve you well as we enter the next decade.

The global technology giants have dominated market attention for much of the past few years. But taking a deeper perspective on the industry highlights the importance of being very selective.

Hear from Ashley Pittard on where he is selectively investing in the digital media industry.

Find out more about the Pendal Concentrated Global Share Fund.

– Developed market yields continue to slide on concerns regarding the outlook for growth; trade tensions continue to increase; the US dollar continues to strengthen; and Chinese growth continues to gently disappoint.

– However, within these broad drivers, there are concerns that some policies and reaction functions are changing.

Despite the volume of newsflow in recent weeks, it does not seem as though there has been a regime shift in the broad drivers of emerging markets. Developed market yields continue to slide on concerns regarding the outlook for growth; trade tensions continue to increase, obviously the US-China relationship, but also others, eg Japan-South Korea; the US dollar continues to strengthen; and Chinese growth continues to gently disappoint. This remains a challenging environment for the emerging world, and we believe that emerging market equities should continue to be seen as a source of country-specific opportunities rather than as an opportunity in the whole. Alpha, not beta.

However, within these broad drivers, there are concerns that some policies and reaction functions are changing. Specifically, the developments of the last few days have raised concerns regarding Chinese currency policy. At the start of August, President Trump announced a 10% tariff on the remaining USD 300b of imports from China. In response (it is assumed), both the domestically-traded CNY and the internationally-traded CNH weakened substantially and, significantly, broke the 7/USD level. Subsequently, China suspended purchases of US agricultural products and the US Treasury announced its intention to investigate China as a currency manipulator.

We do not believe the move through 7/USD represents a shift in China’s currency policy. In the first instance, the official policy is to manage CNY against a basket of currencies, and the steady strengthening of the US dollar against the currencies of China’s other trade partners implies a weaker CNY/USD exchange rate. Secondly, whatever goes into PBoC’s ‘countercyclical factor’, it is clear that the effects of tariffs absolutely justify a relative weakening of CNY.

On the other hand, it has seemed that PBoC has previously defended the 7 level. In both late 2016 and late 2018, CNY approached 7 but did not trade through it, despite the powerful risk-off sentiment in emerging markets at those times, so it does seem as though there has been a behavioural shift within the latitude of policy. Whatever concerns Chinese policymakers have about domestic sentiment towards the exchange rate have clearly been overcome by macro circumstance.

In terms of what this means for investors, we think the environment hasn’t changed. The intensifying trade war and the slide in US yields suggest a difficult environment ahead for export-based economies (very much including China), while the strengthening US dollar suggests the positive effect of lower yields on the domestic-demand/carry-trade led emerging markets will be delayed.

If we wanted to create a positive narrative from this week’s events, we would observe that the 2015-16 Chinese stimulus was led by a steep devaluation in CNY in August 2015, potentially relieving pressure on the exchange rate before aggressive injections of liquidity. While this is a compelling story, some of the statements from Chinese leaders (“Now there is a new Long March, and we should make a new start,” – President Xi Jinping) don’t point to an overwhelming desire to take the easy road.

The US decision to label China a currency manipulator is a surprising one, both because it was not in line with the normal semi-annual assessment cycle, and because China doesn’t meet the US’s own definition. There is a lot of interesting stuff happening around currencies and global imbalances, which deserves its own report, but the short version is that China has a robust history of currency manipulation but really isn’t guilty at the moment.

In terms of the regime change, when it comes, there would seem to be two likely ends: The first is that the trade war reaches a ceasefire, because one or both sides cannot take the pain any more – that would be hugely bullish for export EM (China, Korea, Taiwan, Mexico); the second would be that the rally in the dollar ends – with low yields that would be hugely bullish for domestic/carry-trade EM (particularly commodity importers such as Turkey, India and Pakistan). Until such point, we will remain selective in both groups.

Regnan has delved into the benefits and risks of corporate virtue signaling in its latest opinion piece. How should companies approach issues with financial and societal implications when choosing to articulate their stance?

Download a copy of Brand risk: social licence to operate, corporate virtue signaling and brand assets and visit Regnan.com.au for additional insights and research reports on responsible investing.

About Regnan

Regnan – Governance Research & Engagement Pty Ltd was established in 2007, co-founded by Pendal Group to evaluate the relationship between environmental, social and corporate governance (ESG) factors and investment value. Regnan has evolved to become a leader in long term value, systemic risk analysis and sustainable investment advisory.

Regnan provides ESG integration, advisory and stewardship services to Pendal to drive improved ESG performance in S&P/ASX200 listed companies. Regnan meets with directors and senior company leaders, in a constructive manner, to influence change on issues with the potential to impact value over the long term.

Regnan is also a regular contributor to the public debate on long term value and sustainability, and is an active commentator in the media and at corporate and financial industry events. Regnan also provides submissions to government and other policy makers to improve both sustainable investment and the identification of systemic risks.

Regnan’s research insights are applied to Pendal’s Sustainable, Ethical and mainstream funds where relevant, as well as enabling us to work with other institutional investors in meeting their sustainability objectives.

DISCLAIMER

This document has been prepared by Regnan Governance Research and Engagement Pty Limited (ABN 93 125 320 041), (“Regnan”) and is republished with Regnan’s permission. It is for general informational purposes only and should not be relied upon in making a decision to invest or a decision in relation to an existing investment. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information relates only to Regnan’s assessment, based on its research and the information available to it, of the performance of a company in relation to environmental, social and governance issues and should not be regarded as a recommendation or statement of opinion by Regnan on:

i. any other aspect of the company’s performance;

ii. the prospects of the company; or

iii. the company’s suitability or attractiveness from an investment perspective.

The views expressed in this document are exclusively those of Regnan and the information contained within is current as of the date of publication. Pendal Group is the owner of Regnan and commissioned the company to provide research and engagement services for use as inputs into the decision making processes for Pendal’s investment activities. The views of Regnan expressed in this article may differ from those held by Pendal Group.

Amazon brings threats as well as opportunities if you know where to look says Ashley Pittard, Pendal Group’s head of global equities

AMAZON’S $US13.7 billion acquisition of upmarket grocer Wholefoods a few years ago put big pressure on consumer goods stocks.

At the time, investors thought Amazon would disrupt the US retail landscape – and stocks such as Colgate-Palmolive, P&G, Kraft, Heinz and Kellogg’s came under pressure.

Some investors questioned whether consumer staples companies had been earning greater-than-normal profits and would come under severe pressure to reduce prices as the Amazon phenomenon took hold.

“The stockmarket de-rated these businesses because they were concerned Amazon would commoditise food exactly like they did with books and all the other products they’d gone into over time,” said Ashley Pittard, who heads up global equities at asset management group Pendal.

>> For more information on Pendal’s global equities capabilities click here

But not all consumer stocks were in the same boat after Amazon’s move.

Mr Pittard believed brands that had a strong affinity with consumers were likely to retain considerable bargaining power when it came to pricing negotiations with Amazon and other major distributors.

In the wake of the Amazon-Wholefoods deal, Mr Pittard saw a number of opportunities.

“We look for crown jewel assets that are out of favour – those where the stock price has been flat for a number of years or are down 30 to 50 per cent near term.

“Here we focused on Colgate-Palmolive and Procter & Gamble.”

Consumer were stocks sold down in the wake of Amazon’s move on Whole Foods

Colgate – a global household name in oral health – and P&G – makers of a wide range of iconic brands in home and personal care products – had the highest market shares and the highest return on capital, Mr Pittard said.

“Colgate’s market shares range between 40 and 80 per cent. When you have that type of market share, you have pricing power.

“You can innovate, setting you apart from other market players.”

Premium positioning drives price

Colgate has been able to attract higher margins by enhancing flagship products in relatively minor ways such as incorporating elements of nature, sustainable sourcing or adding vitamins or supplements.

“Remember as a kid you cleaned your teeth with white toothpaste – now look at the range of toothpaste,” said Mr Pittard.

“It’s white, it’s coloured, it’s got mints in it, it’s got natural products, it’s for sensitive teeth…”

“And the difference in price is from about $1 all the way up to $14.”

As an investment, Colgate stood out for a number of reasons, Mr Pittard said:

– The stock had been de-rated and had gone sideways for five years

– Management was focused on reducing costs and generating a good dividend yield

– Longer term there was pricing power and room to innovate because of a large market share

Hear more from Ashley Pittard on finding value in consumer stocks

Disrupting the distribution, not the brand

“When you look back at what people were buying on Amazon, it was the exact same type of well-known brands they were buying at the shop,” Mr Pittard said.

“The only difference was, it was the convenience of using the Amazon delivery.”

“So yes, Amazon are disrupting the space – but they’re not disrupting the brand, they’re disrupting the distribution.”

For more information on Pendal’s global equities capabilities click here.

This article has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and the information contained within is current as at 25 July 2019. It is not to be published, or otherwise made available to any person other than the party to whom it is provided.

PFSL is the responsible entity and issuer of units in the Pendal Concentrated Global Share Fund (the Fund) ARSN 613 608 085. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. You should obtain and consider the PDS before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested.

This article is for general information purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information in this article may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information in this is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information.

Any projections contained in this article are predictive and should not be relied upon when making an investment decision or recommendation. While we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections.

– The outlook for emerging markets in the second half of 2019 and beyond has two main macro drivers: US rates and yields, and Chinese growth.

– While the expectations are for a slowdown in the future in the US, economic growth in China is unambiguously soft.

– EM equities remain in aggregate a highly cyclical asset class, but the first half of 2019 has shown that a slowing cycle still creates great opportunities within the asset class.

The outlook for emerging markets in the second half of 2019 and beyond has two main macro drivers: US rates and yields, and Chinese growth. This is obviously always the case, but these variables significantly surprised in the first half of the year and will remain of great interest ahead, unlike, say, the oil price (weakening demand but producer discipline), Asian and Middle Eastern geopolitics (both noisy but seemingly not yet at the point where any major player abandons the current system), or developments in Europe (messy politics should not distract from super-low bond yields).

The shift in the US yield curve, and the associated expectations for interest rates, has been dramatic. At the end of June 2018, the effective Fed Funds rate was 1.82% and the US 10-year Treasury yield was 2.86%; a year later, those rates were 2.40% and 2.01%, respectively. Even the 30-year Treasury, at 2.53%, is almost trading below the policy rate. This inversion of the longer end of the US yield curve has generally occurred before difficult times in markets, including the early 1980s twin recessions, the savings and loans crisis, the Asian crisis and end of the tech boom, and the global financial crisis. US data remains reasonably strong, but clearly US fixed income markets see the long economic boom that began in 2009 coming to an end.

Chinese slowdown

While the expectations are for a slowdown in the future in the US, economic growth in China is unambiguously soft. Recent disappointing data include a 49.4 reading for June’s manufacturing PMI survey and May’s industrial production number slipping to 5.0%, a 17-year low. Other related data such as Taiwan exports (-5.8% to May), Korea exports (-13.5% to June) and the copper price (down 7.9% in the second quarter of 2019) all show the endemic weakness in Chinese demand. While China notionally has a wider set of policy options than almost any other emerging market, internally imposed constraints mean there is no easy way to stimulate growth while also managing the Renminbi exchange rate.

In addition, trade tensions and related uncertainty may be partly to blame for this developing sense of slowdown. From an EM point of view it doesn’t matter if export demand is sliding because of the natural evolution of the economic cycle or because of a political overlay. It is clear that economic data, positioning in bond markets and revisions to forecasts point to an environment that is negative for the cyclical, export-driven part of EM. For countries, that means Taiwan, South Korea, China, Mexico, Malaysia and Thailand; for sectors, it means information technology and parts of the industrial, materials and consumer discretionary sectors.

At the same time, though, lower interest rates in developed markets mean the opportunity for lower rates in emerging markets. Year-to-date, various EMs, including Russia, Malaysia, India and Chile, have been able to cut policy rates, both in response to declining inflation and to reduced concerns about US monetary policy tightening.

EM winners in 2019

So, in this seemingly slower-growing world, what were the winning trades in the first half? From an EM country perspective, the best performing markets were Greece (MSCI USD price index +29.3%) Russia (+28.0%), Argentina (+27.2%) and Egypt (+24.9%). What these markets have in common is that they are generally very cheap (in each case because of some fairly obvious political and economic dysfunction), and their strong performance reflects investors increased appetite for risk as risk-free rates decline. If global rates and yields are to remain depressed, this rotation into risk is likely to endure, even if the headlines remain troubling.

This isn’t to make an argument for investing in the (long-underperforming) value style tilt in EM. Value may also capture many industries that are, at this point in time, strategically challenged by industrial and technological changes (such as retail, autos and telecoms). In addition, falling costs of capital should be proportionally more beneficial to companies with longer duration cashflows, i.e. growth companies. Rather, this is about the increased attractiveness of cheaper, riskier markets, both through value (to equity investors) and through carry (to bond investors).

Individual country opportunities despite a slowing cycle

We feel that this points to some markets that have lagged the rally in risk, year-to-date. Turkey remains very difficult from a political and policy standpoint, while the economy continues to work through the legacy of the strong credit boom that ended in mid-2018. Nevertheless, it is the emerging market that seems to be cheapest across the equity-rates-currency spread, with single-digit P/Es in the equity market, policy rates 830bp above trailing consumer price inflation and a currency far from its real effective exchange rate trend.

South Korea is a highly cyclical economy and equity market, with substantial exports to China, but extremely low valuations there (price/book value for the market of 1.0x) also reflect investors’ sense that governance risk in Korea is elevated. Followers of our strategy will be aware of our expectation that increasing payout ratios will add a carry opportunity to the existing value opportunity there. Korea is also attractive because it should provide a hedge in the event that there is a recovery in the global economy, with a resultant back-up in yields.

Some other EM assets should also benefit from the current environment. Although Pakistan continues to face multiple economic challenges, the market is cheap and the recent IMF loan deal underpins the policy environment. In addition, gold has performed well in this period of low cost of capital, driving strong gains from EM gold miners.

EM equities remain in aggregate a highly cyclical asset class, but the first half of 2019 has shown that a slowing cycle still creates great opportunities within the asset class.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighborhood

In May 2019 the Pendal Property Securities Fund was awarded Best Property Securities Fund at the Money Management Fund Manager of the Year Awards.

In announcing the award, Money Management and its research partner Lonsec stated:

The Pendal Property Securities Fund has a ‘core’ investment style with a ‘quality’ bias, and is managed by highly-experienced and long-serving Portfolio Managers Peter Davidson and Julia Forrest. The team benefits from extensive industry contacts and sharing of ideas and news flow ideas from Pendal’s other asset class teams. The Fund has an extensive track record of outperforming peers over multiple investment cycles.

Responding to the award, Pendal’s Head of Listed Property Pete Davidson addressed some key questions facing the sector:

1. What do you think drove your strong performance in the last year? How did the management of the Fund contribute to this?

• Our focus on having a valuation toolkit and using a variety of valuation measures meant we could identify value in stocks that had strong equity-style valuation.

• Traditional NTA based stock valuation lagged. Many NTA supported stocks became value traps rather than traditional value.

• There was a strong divergence in stock performance, which was better for active managers.

2. What asset allocations and/or market conditions did you find most advantageous?

• Our overweights in fund managers and industrial, logistics stocks supported our performance.

• Falling bond rates have supported fund managers.

• Underweights to traditional mall / retail assisted our performance. These stocks have been impacted by the weakening macro economic environment in Australia.

3. Do you anticipate continued strong performance?

• Yes, our portfolio is positioned in pockets of growth and good reliable cash flow, such as child care and traditional industrial property, which will outperform the slowing economy.

• Yes, we are now overweight the Perth and Auckland office markets which have very good and improving fundamentals.

• Our underweights to traditional mall retail should continue to perform. We believe asset values will decline in this sector over the coming year.

Read more about the Fund and our capabilities

Fund Manager commentary for the month and quarter ended 30 June 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Access the quarterly commentary here.

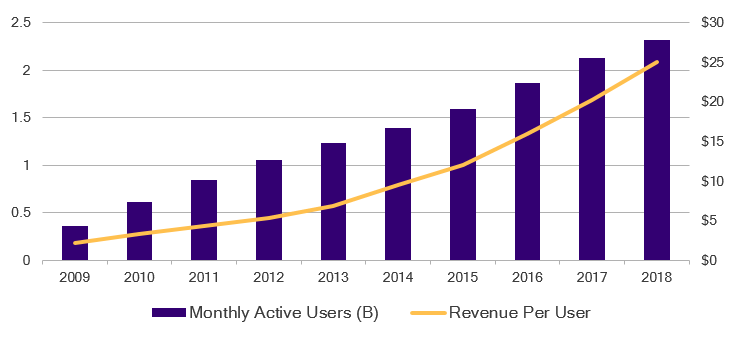

Engaging via social media has become an essential part of daily lives for people the world over. The deeply entrenched use of smart phones and other mobile devices has superseded the traditional computers experience for an increasingly mobile population who have gone from periodically ‘logging on’ to ‘always on’.

No company is benefiting more from this trend than Facebook. It has been successful in leveraging its platform to facilitate user interactions at scale in a myriad of different ways, at any time of the day. While the ‘always on’ user views, posts, likes and shares, Facebook is working away in the background collecting a share of the value created in the form of advertising.

Today, 93% of its total advertising revenue is generated from mobile which is still growing north of 20% a year.

Facebook – user revenue growth (US$ millions)

While Facebook is the type of business we love to own in the Fund, we had been cautious on buying it. Recall our prior discussion on the rationale for details on our view.

Our investment process favours companies with dominant market shares and a growth profile capable of sustaining a competitive advantage over peers. We then look for an opportunity to invest in these companies. This usually occurs after they have experienced a substantial drop in their share price or have had flat earnings for an extended period of time.

As such, our investment in this area thus far has been limited to Alphabet Inc. (Google’s parent entity). We haven’t seen value in most of the other names, that is until recently.

Facebook’s share price underperformed the market from mid-2018 following news that confidentiality of its user data had been compromised. It traded below levels last reached in 2016, prompting a deep dive review of the company.

Facebook – share price performance vs S&P 500

The digital difference

Facebook and Google collectively account for 75% of all global (ex-China) online advertising spend. Such is the powerful combination of digital advertising and a captive, engaged user base. For advertisers the potential return on investment offers a distinct advantage over traditional forms of advertising.

Large, well curated social platforms offer advertisers the ability to have much more bespoke, targeted ad campaigns that can be enhanced and re-channelled through the course of the campaign, thanks to clever analytics that can be extracted to inform success or otherwise of the campaign. Unlike ads on TV, radio or printed materials, the advertiser doesn’t know who is watching TV, who lives in the house, what goods they’re buying online and at what time of day.

Considered together, Facebook and Google represent a powerful market share which provides clear competitive advantages.

Monetising the monopolies

Within its stable, Facebook owns and operates Instagram which was acquired in 2012. Within six years Instagram grew to amass one billion active users. Facebook is now in the process of ramping up monetisation of this asset which has become the largest growth driver for the company. The key medium of video presents a richer platform for both creators and advertisers to become more creative with their interactions.

This is similar to the opportunity we see with our investment in Google and its under-monetised Google Maps and YouTube assets.

Platform risks abate

The key concern for us with owning Facebook in the last two years has been their ability to control and monitor the content on their platform following a series of scandals. With our conservative approach we felt we needed to wait until we had clarity on the eventual new cost base and likely regulatory impact before investing.

Two recent developments have supported a change in our view:

1. Cost growth peaking – The company has had to significantly increased its expenditure on content control in 2018 and 2019. Given the direct impact on its margins and earnings we were happy to wait for signs that cost growth has peaked. In its most recent earnings update, Facebook reduced its expectations for capital expenditure in 2019 by US$1b. This means capital expenditure requirements will no longer continue to erode margins which will provide a base for profitability.

2. Regulatory impact not as bad as feared – Analysis of the company’s first quarter results showed a US$3b expense accrual based on expectations of a fine from the FTC in the range of US$3-5b. From our perspective, we could not forecast this potential outcome with any certainty, but comparing it to similar fines levied against Alphabet in the past couple of years gave us confidence Facebook won’t be penalised at a significantly higher level.

News reports in July indicate a Facebook has reached a settlement with the FTC of US$5b for the privacy breaches, which is within the company’s earlier guidance. The market has responded positively to the news, which was reflective of our premise on this issue.

We believe that the regulatory scrutiny will continue for some time and there will be associated costs. However, we also believe company management have acknowledged the reality of the situation and are driving operational change to reduce such risks and improve profitability.

Giving Facebook a ‘like’

We have held a favourable view on Facebook’s fundamentals for some time, but its valuation, unquantifiable regulatory risks and uncertainly of its ultimate profitability had precluded an investment. With an improved valuation (cash adjusted price-earnings multiple of 16x and a buyout yield — our preferred whole-of-company valuation measure — of 8%), greater clarity on the aforementioned costs and importantly, management’s actions to ameliorate operations for the platform, we have been able to improve our conviction.

We initiated a position in Facebook for the Fund in April and will look to add to our exposure as we see further evidence of the company sustaining its operating margins and containing costs.

What happens when a straight ‘A’ student starts bringing home ‘Bs’? We discovered one outcome of this report card for the Australian economy with back-to-back rate cuts from the Reserve Bank in June and July. In this quarter’s update we discuss why such easing was required, but more importantly what lies in store for future policy in Australia, including the possibility of quantitative easing. We also assess the outlook for Australian credit, which remains a balancing act between the global forces of trade war concerns and speculation of central bank action. Finally, we discuss a moving firsthand experience with responsible investing and how it has improved the outcomes for housing the homeless and victims of domestic abuse.

We hope you find this piece useful and welcome feedback from readers.

Australian Quarterly Update