The market continues to price two rate cuts in Australia over the next twelve months as the RBA grapples with sluggish consumption and subdued inflation. This was evident in first quarter inflation data released last week. This quarter’s update was written before the release and in light of the softer picture, we have brought forward our RBA cuts from August and November to May and August. This is in spite of the current resilience of the labour market. In the April update we take a longer term look at the structural forces at work in the Australian economy and why rates will remain low into the next decade. Also in this update, we examine what has contributed to the recent strength in domestic credit, how we have positioned our credit funds and what dangers remain lurking on the horizon. In cash markets, very front-end rates recently fell to their lowest on record – our Cash PM, Steve Campbell explains why and what lies ahead. Finally, the quarter also featured International Women’s Day, which we thought would be opportune to educate investors on gender equality bonds, a growing segment of Responsible Investment.

We hope you find the piece useful and welcome feedback from readers.

View our Australian Quarterly Update

Fund Manager commentary for the month and quarter ended 31 March 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Quarterly commentary

Monthly commentary

What separates environmental, social and governance (ESG) investing; impact investing; ethical screening; and socially responsible investing (SRI)?

While they are all unique approaches to investment, there are some areas that overlap.

Susheela Peres da Costa shares insight on how to navigate this complex landscape and get responsible investment governance right.

View the article

It is clear to us that the domestic opportunity in Mexico has a better fundamental underpin than in South Africa, and we are positioned accordingly.

One of the defining characteristics of emerging markets (possibly even the defining characteristic) is that there are positive price (and liquidity) correlations between bond and equity markets. If you hit a crisis and your equity market sells off and bond yields spike, congratulations – you’re an emerging market.

For us as equity investors it means we need to pay attention to bond markets, including credit ratings of emerging market sovereign issuers. That is where two interesting stories have been developing recently – South Africa (and its relationship with parastatal power company Eskom) and Mexico (and its relationship with parastatal oil company Pemex).

South Africa’s Eskom

South Africa (long-term foreign currency debt) is currently rated Baa3 by Moody’s and BB+ by Standard & Poors. These ratings are respectively just above and just below the critical investment grade threshold at which many investors will choose to disinvest. Key to this is the parlous state of South Africa’s state-owned electricity utility Eskom. Eskom has struggled for years with high operating costs and a steadily increasing debt burden. The costs are from a variety of problems, including poor choices for capital investment (specifically two of the world’s largest coal-fired power stations, both behind schedule and over budget), poor execution of those investment decisions (including serious operating problems at those power stations), low employee productivity and failure to collect receivables from local municipalities. Eskom currently has a total indebtedness of ZAR 420bn (US$29.6bn) and trailing 12-month EBITDA of only ZAR 44.3bn (US$ 3.4bn).

Without major financial support from the state, Eskom will be bankrupt. But this is simply not an option as the lights must be kept on. South Africa is already struggling with a series of crippling rolling electricity blackouts, and Eskom must be rescued both as a financial entity and as an operating concern. Analysts estimate that Eskom needs around ZAR 150bn of financial support, or ZAR 23bn per annum. Finance Minister Tito Mboweni’s maiden budget in February included a promise of ZAR 69bn of aid for the next three years, sparking statements of concern for South Africa’s sovereign credit rating.

Mexico’s Pemex

Mexico, despite better credit ratings of A3 (Moody’s) and A- (S&P), has also seen the ratings agencies express concern about state support for a huge parastatal. Pemex, the state-owned national oil company, has debts of MXN 2.1trn (US$ 106.7bn) and trailing 12-month EBITDA of MXN 494.8bn (US$ 25.8bn). Fifteen years of declining oil production and underinvestment have created a powerful short-term funding squeeze – a quarter of its debt matures in the next three years, which with capital expenditure requirements more than exceeds the company’s available financial resources. Meanwhile, oil output per employee runs at about 15 barrels per day (Colombian peer Ecopetrol manages 80).

We remain far more positive on the outlook for Mexico, however. The Mexican finance ministry has said it will exhaust its other options before offering an explicit guarantee of Pemex’s debt, while the unpalatable alternative of seeking foreign joint venture participation in Pemex is, at least, a possibility. The South African treasury is already bailing out Eskom, and the chances of attracting foreign capital into Eskom are nil. Finally, the Mexican economy (2019 forecasts: current account deficit 1.5%, fiscal deficit 2.5%) remains in fundamentally better shape than the South African economy (deficits forecast at 3.6% and 4.0%, respectively). Whatever opportunities may exist in exporters in these markets, it is clear to us that the domestic opportunity in Mexico has a better fundamental underpin than in South Africa, and we are positioned accordingly.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighborhood

Key highlights

• Home and personal care companies are relatively new entrants to the Fund.

• The Amazon onslaught provided a clear opportunity to buy into two industry leaders at depressed prices.

• Consumer goods companies are many and varied, but only some are actively investing in the brands which can underpin their continuing success.

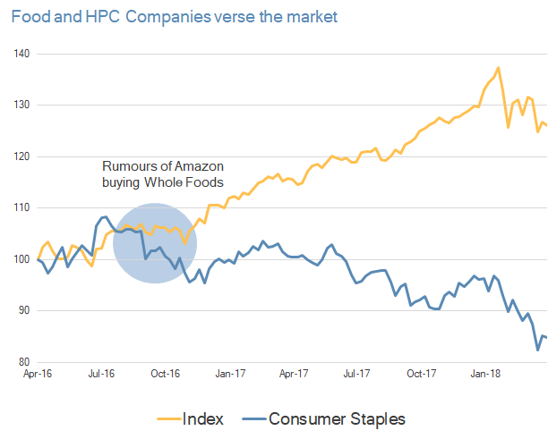

We identified food and home & personal care (HPC) companies as a key research focus in 2017 after Amazon’s $US13.7 billion acquisition of upmarket grocery chain Wholefoods.

At the time, the market’s reaction reflected concerns Amazon would disrupt the US retail and digital food landscape – and no brand would be safe.

Food and HPC companies underperformed after the Wholefoods deal as you can see here:

Source: Factset

But we saw an opportunity.

We intensified our research on the major food and HPC companies and soon came to a different conclusion to the market.

We believe global brands are still in demand. Those that can develop an effective and sustainable digital strategy will be able to drive traffic online as well as in store.

Many global brands have larger market shares online than they do in store, because online shoppers are time-poor and tend to be more brand conscious.

This research led us to initiate positions in two companies: Colgate-Palmolive (Colgate) and Procter & Gamble (P&G).

Both companies enjoy strong market shares, driven by management that understand the need to consistently invest in their brands to drive long-term sustainable growth.

Reviewing the thesis

To test our research and conviction in these names, we attended the Consumer Analyst Group of New York (CAGNY) conference in Boca Raton, Florida.

This industry conference is the largest of its kind, run by a not-for-profit group and designed to facilitate robust dialogue among investors, analysts and consumer industry executives.

The February event provides management the opportunity to discuss their new products and strategy for the coming year.

This year’s conference featured presentations by senior managers from 31 consumer companies, including Colgate and P&G.

A key theme was refocusing on investment and innovation to drive top-line growth, alongside the opportunity to drive online sales through targeted digital strategies.

This is very much a change from the last couple of years where the focus has been on driving margin improvements through cost savings.

Our process tends to de-weight companies with a binary focus on cost saving initiatives. From experience they tend to be unsustainable beyond the short term.

Many of the companies at CAGNY have come to the conclusion they were too aggressive in cutting costs as a means of driving sales growth – and now need sustainable investment behind their brands.

This was poetically demonstrated when Kraft Heinz — the epitome of this singular focus on margins — released their Q4 earnings results during the conference. (They were not in attendance).

The stock was down 27% the day after management cut the dividend and conceded the need to step up spending on their brands to reinvigorate revenue growth.

By comparison, the HPC companies we own have been consistent in their approach to brand management and investment. In 2019 they are focusing on the latest innovations and product launches.

Colgate-Palmolive – cleansing the market’s palate

In 2019 Colgate is embarking on one of the biggest projects in its 200 year history — a relaunch of its bestselling Total toothpaste.

The company already holds a dominant market share for its oral health care range across a number of countries, but there is little evidence of complacency when it comes to product development.

This new iteration of the classic Colgate product is the result of 10 years of research and development.

This depth of reinvestment into what is already a market leader is testament to the value Colgate places on its brand.

The financial pay-off comes in the form of improved price control. Developing core products like Colgate Total into a premium category can place HPC companies in a strong position to exercise pricing power and expand margins while still growing sales volumes and consumer loyalty.

The new Colgate Total is designed to provide even more benefits to the consumer including relief from sensitivity, stronger enamel and fresher breath.

The company’s other categories reflect effective innovation in targeting consumer preferences.

Colgate Naturals toothpaste — with ingredients such as lemon, charcoal and even seaweed — address a growing consumer preference for natural ingredients over manufactured alternatives.

The Palmolive purifying clay body wash is another example of innovation through using natural ingredients.

Intersecting innovation with distribution

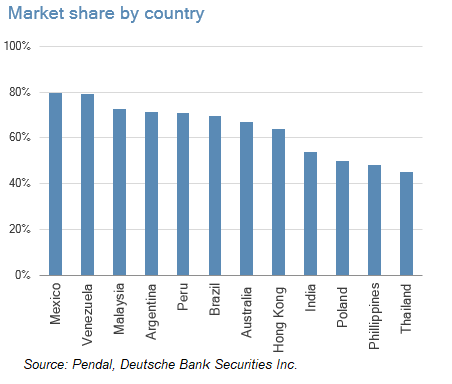

Addressing growth in emerging markets is another key feature of the company’s growth strategy. Colgate derives 50% of its sales in emerging markets, with leading positions in the following countries.

Colgate achieves this high market share through its price pack architecture which includes products for all income levels. As incomes rise in these markets, consumers can trade up to the higher priced products.

Educating customers is of paramount importance for Colgate and offers further opportunity.

Educating customers is of paramount importance for Colgate and offers further opportunity.

In Colgate’s markets, 68% of the population brush their teeth less than once per day. Greater education on the importance of brushing morning and night can double consumption.

The company’s education programs begin in schools through the Bright Smiles, Bright Futures program, which provides dental care resources to teachers.

The program has been in operation since 1991, reaching more than 850 million children in 80 countries. The company has ambitions to reach 1.3 billion by next year.

In developed markets they introduced Colgate Magik, a tooth brush that uses augmented reality to teach kids how to brush their teeth. Take a look at the promotional video.

Programs like these exhibit the long-term power of capturing and nurturing customer loyalty from a young age — an approach often overlooked by companies.

In our view, Colgate stands out for its leading brands and a strong management team willing to operate the company for long term value creation.

A long term approach

Similar to Colgate’s management approach, we also apply a long term approach to investing and take the required time to build conviction.

We purchased Colgate for the first time in June 2018 when it was trading at a buyout yield (our preferred valuation measure) of 8%.

The stock had traded sideways for around five years so the burden of proof for the upside potential was squarely with the company’s management team.

We then waited another six months before adding to the initial investment, which was further complicated by short-term impacts from foreign exchange fluctuations, rising commodity input costs and a trucking strike in Brazil which weighed on market sentiment and the stock price.

Notwithstanding these externalities, we have confidence in the company’s ability to capitalise on its investments in the brand and deliver above-market growth over the longer term.

Procter & Gamble – harnessing environmental and digital dividends

We made an initial investment in P&G in December 2018 at the time when its share price reached a buyout ratio of 8%.

The updates from P&G at CAGNY were particularly insightful and in time may provide a useful case study on the synergies of innovation, operational leverage and ecological awareness.

P&G showcased its new waterless soap DS3 Clean brand at CAGNY.

Established as an incubator brand, DS3 is sold on the crowdfunding and product innovations digital platform, Indiegogo. DS3 Clean has a multi-faceted approach to delivering value:

1. Addressing environmental concerns about water use and packaging waste.

2. Reduced emissions through reduced transport costs.

3. Increased customer convenience by shifting the final stage of production to the household. DS3 products are delivered to the customer in solid form and convert into a liquid when exposed to water, allowing for less packaging and easier shipment.

DS3 cleaning products include laundry detergent, toilet cleaner, surface cleaner, hand wash and even shampoo and conditioner. Take a look at the DS3 demo.

Expansion of the brand will benefit P&G margins because products are priced at a significant premium to the innovative pods product under the Tide brand.

Tide pods are a unit dose product designed for convenience and efficiency over the liquid detergent variant. US household penetration of pods grew from 16% in 2016 to 26% in 2018, highlighting the growth opportunity that still exists for this product and also the potential to grow the DS3 brand.

The Tide pods product is driving growth in the US laundry category and has allowed P&G to build a greater share of that market (US market share of tide pods is 80%).

As customers gravitate towards e-commerce, P&G is looking for innovative packaging solutions that delight the customer – and save costs.

The Tide Eco Box liquid laundry detergent pack is one example. It doesn’t require additional boxing for online sales, takes up less space due to the box design and uses less water.

In addition to innovation drivers, P&G is undergoing a five-year $US10 billion cost reduction program (2017-2021). Some of the savings will inevitably be reinvested in the business. We believe a proportion will translate to the bottom line.

This, combined with the diverse portfolio of products and a focus on innovation, makes P&G an attractive investment.

The company is valued on an 8% buyout ratio and is generating substantial free cash flow to support an attractive 5.1% dividend and buyback yield.

A key philosophical principle of our investment approach is to only invest in companies that command leading positions in their respective markets and actively invest in their brands.

Invariably this is a function of a company’s brand strength and longevity in the market.

Attending CAGNY reinforced our belief that companies which are able to consistently reinvest in their brands will drive long-term value creation for shareholders.

We see Colgate and P&G as industry leaders with a strong trajectory of sustainable growth ahead.

Click here to find out more about the Pendal Concentrated Global Share Fund.

Followers of the Pendal Global Emerging Markets Opportunities Fund will be aware of our belief that one of the most exciting stories in the emerging market world right now is the ongoing corporate governance revolution in South Korea, and the resultant unlocking of the extreme value that exists in the Korean equity market.

A number of factors have combined to drive this revolution, including an ageing population, low returns from Korean and global fixed income markets, and the intervention of activist investors. Now, the social pressure for governance reform is slowly turning into political pressure.

At stake is the one of the world’s lowest dividend payout ratios, and the web of interlocking and circular shareholding structures that enable it. As we wrote in 2017, ‘The behaviour of corporate Korea and the related lack of dividends has become an increasing issue in Korean politics, as an ageing population needs income from its investments. We feel that both the Korean public’s response to the corruption scandal, and the resulting election of a left-wing administration, will put huge pressure on Korean companies to reform.’

We have since highlighted the steadily increasing dissent rate of the National Pension Scheme (NPS, the largest investor in Korea and the third largest public pension fund in the world), as further evidence of the widespread demand for change. From a normal level of about 10%, the rate at which the NPS has voted against Korean corporate management rose to 12.9% in 2017 and 20.5% last year. We have also seen wide reform of Korean corporate structures, partly driven by shareholder pressure and partly by the increasingly shareholder-friendly regulations brought in by the Korea Fair Trade Commission (FTC).

This process will have milestones. One was reached in October 2015 when Samsung Electronics reformed its shareholder return policy. Another was reached on Wednesday (27 March 2019), when Cho Yang-ho, the chairman of Korean Air, lost his position at the head of his own board, as the NPS voted against Mr Cho’s reappointment.

Mr Cho failed to receive the required two-thirds majority of shareholders’ votes to retain his position, with the NPS joined by some of Korean Air’s largest foreign institutional shareholders in voting against him. While by international standards this may not seem controversial (Mr Cho is accused of embezzling company funds and unfairly awarding contracts to family members, while his daughters have also been caught up in several scandals at the company, including the ‘nut rage’ incident that readers may recall), the outcome of the vote has shocked the generally conservative Korean business community.

The Cho family will retain their control position at Korean Air, and only the week before the NPS had voted with company management and against foreign activist shareholders at the Hyundai Motor annual general meeting.

This revolution will not arrive everywhere at once, and not all cheap Korean companies will see value unlocked in the near-term. But we are confident that Korean corporate governance is undergoing irreversible and revolutionary change and the NPS rejection of Mr Cho is a powerful symbol of that. We remain overweight Korea in the portfolio.

Be a part of the world’s fastest growing economies

No use buying the best house in a bad neighbourhood

The following speech was delivered by Richard Brandweiner, CEO of Pendal Australia, at the KangaNews 2019 Sustainable Debt Summit on 18 March 2019.

From fringe to foreground – the evolution of sustainable investing and the opportunity for investment management

In the beginning of our modern sensibility, there was only one axis.

Returns.

Investment returns, company profits, GDP growth.

As individuals, we would go to a stock broker to invest on our behalf and outcomes were judged solely on returns.

In the 1960s and 1970s, the investment industry discovered it was able to measure a second axis. With the advent of modern portfolio theory, we came to understand that there was volatility which could be measured which was inherent in achieving those returns. We pretended we could forecast it, and risk became the second axis. Now many generations later, no self respecting professional investor would ignore volatility in making an investment decision. In fact, we have become obsessed with it, almost as if it’s the fulfilment of our craft.

So, is that where it ends?

Is the entirety of the purpose of investment management encapsulated in getting as far to the top left of that neat two dimensional chart?

Where does our role as an intermediary fit?

An allocator shifting capital from savers to borrowers or businesses. Determining, as part of a supreme collective, what deals live or die, where profits are to be made and how the users of capital should behave.

All the while, contributing towards externality after externality, both positive and negative.

There is, in fact, a third axis. But we are only just starting to become aware, and we are certainly a long way away from being able to measure it.

The third axis is impact.

Glenn Stevens put it neatly – “For finance is not, for the community, an end in itself. It is a means to an end. Ultimately it is about mobilising and allocating resources and managing risk. Finance matters. Its conduct can make a massive difference to economic development and to ordinary lives – for good or ill.”

“There is, in fact, a third axis. But we are only just starting to become aware, and we are certainly a long way away from being able to measure it.

The third axis is impact.”

Maybe, the third axis doesn’t matter.

Maybe if we just allocate to the most profitable enterprises and leave them be – as specialists in what they do – the world will continue to become a better place.

Except for two things….

1) Firstly, time horizons and incentives are not aligned.

In terms of time horizons, as we know, the big things that really matter move more slowly than the impact of short term financial returns.

And in terms of incentives, given the opaque industry of agents within financial services, with its specialised expertise and discretion to act on behalf of others, unless it recognises a bigger purpose, it has considerable opportunity to act in ways that are not in the interests of the outside world that it is there to serve. I no longer think this is a controversial statement.

Yet, the externalities generated by allocating capital are real. Markets generate economic value, and there is little that can match their ability to allocate goods and services and encourage innovation and technological improvement. The allocation of capital impacts employment, infrastructure, productivity, taxation and, of course, our society and our environment more broadly.

I suspect, as I’m sure many of you do, that the impact of these externalities far outweigh anything else and are much bigger than we generally realise. Like an iceberg. What we don’t’ see because we can’t measure it, in all likelihood dwarfs our simple view of the world.

Of course, a proper market and effective competition, like Adam Smith envisaged, requires companies to bear their real costs and not leverage asymmetries of information and power.

And fortunately, as each day turns into the next, and time horizons evolve from one to another, externality after externality gets priced in. We can see consumer behaviour shifting as we speak.

2) Secondly, the size of the financial system – its volume – is too significant in our small world, and so the responsibility becomes too real.

Over $7 trillion turns over in capital markets globally every single day. That’s equivalent to about 10% of annual global GDP.

The financial services sector comprises between 15 and 20% of the global economy, and has doubled over the last fifty years.

The Willis Towers Watson Pension Fund Survey puts the total capital controlled by asset owners and fund managers globally as $131 trillion, equivalent to almost twice the annual production of our entire world.

The financial system controls the assets of the world.

Whether you’re more interested in the Gospel of Luke – “from everyone who has been given much, much will be demanded” or simply Uncle Ben from Spiderman, “with great power comes great responsibility” – it is impossible not to recognise the immense responsibility that comes with power of allocating such vast volumes of capital in the world.

The world into which we retire will in no small part be a function of how we invest. Those who invest for short term profits and ignore the impact of their allocations of capital are not creating real value.

I’m reminded of a famous sermon by John Wesley in the nineteenth century:

“And it is our bounden duty to do this: We ought to gain all we can gain, without buying gold too dear, without paying more for it than it is worth. But this it is certain we ought not to do; we ought not to gain money at the expense of life.”

Altogether, this is about the third axis, the third dimension. Perhaps not the fulfilment, but a step towards a greater understanding of investment decision making. Our challenge is to improve measurement in the third dimension, to make it real for all agents and to institutionalise it in the way that modern portfolio theory changed our profession.

Now, it is debt that brings us together today –

ESG was all about the equity gang, partying, as they do down at the bottom of the capital structure, blindly holding on to their ‘first loss’ pieces of paper.

In the ecosystem of sustainable investment, equities investing is like the showy spring flowers: – flashes of newsworthy colour, high profile divestment announcements and all the drama of activism and only seasonal proxy voting.

Yet the reality is that most of the equities action is taking place in secondary markets – at least a step removed from the processes that direct funds to the real economy.

Debt, of course, is far more cool.

– the proportion of new issues to debt traded in secondary markets dwarfs that of equities

– the need for borrowers / issuers to come back to the market regularly (this is the exception in equities, not the rule)

– and, of course, debt’s depth of penetration into economies. At any moment, it creates exposure to many more segments, asset sizes (right down to microfinance) and organisational structures.

It is uniquely placed to meet the vast challenges we face in the 21st century, because our very model of sustainable development– the one the world has agreed on in the form of Sustainable Development Goals – focus on issues that are more frequently handled by the entities that issue debt rather than equity – banks, governments, corporates of course, but also many unlisted assets and enterprises.

The annual SDG financing gap in developing countries is estimated at approximately USD 2.5 trillion, and although this seems huge, it constitutes only 3% of GDP, 14% of global annual savings, or 1.1% of the value of global capital markets.

There is a role for all of us to play to galvanise debt markets to fulfil the challenge, opportunity and responsibility of investing. Whether we are Issuers, Arrangers, Fund Managers, Asset Owners or Ratings Agencies.

Or Private Investors, themselves.

I’m here to ask you to come with us, a fund manager, on this journey

– to be mindful of externalities and seek out investments that create positive outcomes

– and to continue to call for more accountability and for more transparency.

“There is a role for all of us to play to galvanise debt markets to fulfil the challenge, opportunity and responsibility of investing. Whether we are Issuers, Arrangers, Fund Managers, Asset Owners or Ratings Agencies.”

For us, at Pendal, it reinforces what we believe is the critical importance of active management. We see our role as stewards of capital – generating returns while being mindful of externalities, and holding issuers and management to account.

This is something that passive or algorithmic strategies simply cannot do.

Active managers bring a unique analytical discipline to the task of sifting the value from the noise and being able to identify debt instruments that contribute to the solutions.

One part of it is very much about understanding the fundamentals of the contract – there’s good evidence, at least on the equities side, that focussing on the sustainability issues that intersect with business fundamentals can deliver meaningful alpha.

And furthermore, demand based on these fundamentals will impact the cost of capital over time and ensure markets do their thing, with the right information.

But we need to go further than returns, even over the medium to longer term.

We need to understand how efficient capital allocation gets the non-financial environment and social outcomes we need. It boils down to a commitment to – at least considering – ‘what needs funding?’ in the mix of questions about what assets we seek out as we build a portfolio.

And this can provide some counterintuitive results for those who hear ‘sustainability’ and think ‘ethical screening’ – but it can prompt a rich dialogue with clients as well as issuers. For instance

– It might be more sustainable to finance a company with a high CO2 emissions profile so that it can invest in new technology that lowers those emissions.

– It might be more ethical to fund a bank that needs to invest in changes to its systems, governance structures and its people, rather than to divest at just the time they need support to make changes.

– Controversially, it might be better to invest in a tobacco company and push them through engagement to cease their cynical marketing to young people in the developing world.

Thinking about ‘what needs funding’ is most relevant when it comes to ‘impact’ investments – many of which are green bonds or social impact bonds.

The role for asset managers in this space is significant. There are thousands upon thousands of genuinely useful, sustainable activities and enterprises out there that need funding and these are of such great interest to our clients, that it’s fair to say that demand for quality offerings exceeds what we would describe as investment-grade supply.

One of the most important things we can do is to educate the market on what ‘good’ looks like. We just released a paper on gender bonds with our Responsible Investment Research boutique – Regnan, which took a look at what next generation gender bonds could look like, based on would be attractive to our funds and clients.

And of course, there is a critical role for us to play in demanding greater transparency and improved measurement. As we have invested in more and more green and social bonds, we note the market has some way to come. There is a parallel in terms of corporate sustainability reporting (lots of push back, slow up take and difficulty in sourcing information). We recognise it’s an evolution – the first step is the hardest – but with guidance, ‘leader transparency’ and experience this steep learning curve should flatten out over time. There is already plenty of evidence that better corporate sustainability reporting tends to be ‘rewarded’ over time.

“The role for asset managers in this space is significant. There are thousands upon thousands of genuinely useful, sustainable activities and enterprises out there that need funding and these are of such great interest to our clients, that it’s fair to say that demand for quality offerings exceeds what we would describe as investment-grade supply.”

The recent Climate Bonds Initiative’s report into post-Issuance reporting practices globally in the green bond market found that, of the 367 issuers in the CBI research universe only 53% provided impact reports. Interestingly, these CBI findings are in line with our own analysis across our holdings of Australian Green Bond issuers.

Impact reporting aims to provide insights into the environmental or social benefits of Green, Climate, Social or Sustainability bond financing. Best practice is evolving to incorporating the quality of the E or S outcomes that are part of the underlying projects as part of the security selection process. We need this to improve over time.

Ladies and gentlemen,

Investors and allocators of capital are, in no small way, the architects of our future. All of us here are at the drawing board. We have the unique power that comes with a privileged position in our society. Please, let us act together to create the future that we want.

Because the future is worth investing in.

Read more about Pendal’s responsible investment capabilities

The Australian Sustainable Finance Intiative – helping steer the Australian economy through a critical decade

A sustainable and resilient economy – one that prioritises human well-being, social equity and environmental protection – is the foundation for ensuring Australia’s prosperity throughout the 21st century. That’s why the leaders and senior executives of Australia’s major banks, superannuation funds, insurance companies, financial sector peak bodies, civil society and academia are coming together to set out a roadmap for realigning the finance sector to support greater social, environmental and economic outcomes for the country.

The Australian Sustainable Finance Initiative, launched on 27 March, is an unprecedented collaboration to help shape an Australian economy that prioritises human wellbeing, social equity and environmental protection, while underpinning financial system stability, in what it says is a ‘critical decade’ ahead.

Pendal is proud to represent the investment management industry on this critical initiative. Over the past decade we have seen growth in a number of groups individually advocating for greater cohesion with business, financial, social and environmental imperatives. Bringing the wider financial industry together through the Australian Sustainable Finance Initiative means we will now have a truly collective approach to developing a comprehensive roadmap that will address the many present and future challenges.

The Roadmap development process will be overseen by a Steering Committee consisting of senior financial services, academic and civil society representatives. Richard Brandweiner, CEO Pendal Australia, has been appointed to the Steering Committee. Richard is looking forward to contributing to this important initiative, drawing upon his deep experience in the fields of impact investing and responsible investment practices.

Richard is a passionate advocate for responsible investment and delivering societal outcomes. He shares his expertise through current appointments on the NSW Social Impact Investment Expert Advisory Group and as Vice-Chair of the Australian Advisory Board on Impact Investing.

Find out more about the Australian Sustainable Finance Initiative.

In this second of our two-parts series, Samir Mehta looks at the oligopolistic paints industry as an example of disruption risk and continual reinvestment to support future growth.

In Asia, there is one difference when compared to developed markets. Good long-term growth opportunities for several companies are still robust, albeit frequently interrupted by macroeconomic challenges. Take India as a case in point. After disruptions due to demonetisation and the introduction of a GST, we now confront geopolitical tensions. I have no opinion of how this situation will resolve, but suffice to say that in the past, saner heads have prevailed. Results for the quarter ending December 2018 are almost through. Companies that managed the disruption of GST and demonetisation well were rewarded handsomely by the market; P/E multiples for the better-managed firms remain high.

Take Asian Paints (AP) for example. On the face of it, the stock has always appeared expensive on both an earnings as well as price-to-sales multiples. In my opinion, there is a logical reason for this: the structure of the paint industry. The world over, the paints industry is an oligopoly. Even in America it has yet to be disrupted by the internet giants. In India, too, the industry is a cosy oligopoly, with AP the clear market leader. As of March 2018, total industry revenues were estimated at approximately Rs500bn (US$7bn), of which AP reported revenues of Rs166bn (US$2.3bn). The unorganised sector (small mum-and-dad chemical plants that have low-end paints with no brand resonance and poor distribution) still account for 30-35% of total sales. That share is likely to fall over the next decade, in my view. This will partly be driven by trends of rising incomes and aspirations of customers who gravitate to branded offerings, but moreso due to the introduction of the GST in 2017 and lowering the GST slab to 18% compared with 28% in prior years.

The world over, the paints industry is an oligopoly. Even in America it has yet to be disrupted by the internet giants.

To illustrate the hold the four big companies AP (52,000 dealers), Berger (23,000), Kansai Nerolac (21,000) and Akzo (14,000) have on the market, it is instructive to look at the progress of a couple of firms that entered the industry early this century. Indigo Paints started in 2000 and Kamdhenu Paints opened in 2008. It is difficult to get exact data of these unlisted firms but, from public data sources, Indigo has approximately 12,000 dealers while Kamdhenu has 4,000. After 18 years in the business, sales for Indigo are approximately Rs5-6bn pa. To put that in perspective, the top four firms collectively spent Rs13bn in advertising and promotions in 2018.

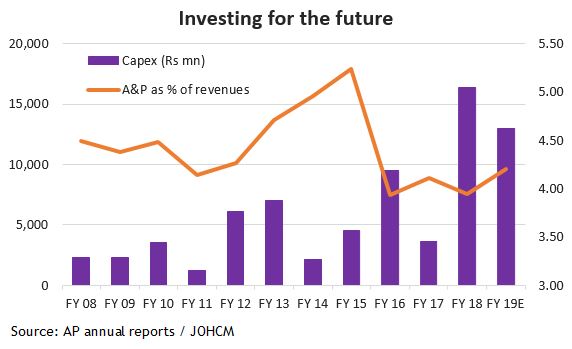

The cost of painting an apartment varies from 1-3% of the cost of purchasing the apartment. Paints are integral to decoration and aesthetics of the house. There is an umbilical link to the health of the real estate industry. In the past 7-8 years, home prices in India have, on average, remained flattish. A big bull market in property prices, which began in 2001/2, created an overhang of supply. Even in tough years, paint volumes have averaged growth of 6-8% pa. Fortunately in the past couple of years, the Indian government has refocused its efforts on the housing sector. Providing subsidised rates of interest for affordable housing, changing GST rates for finished and unfinished homes and recognising that building and construction industries can provide ample employment opportunities. The industry is working with the National Skills Development Corporation to impart skills in its effort to train painters and increase engagement with architects. Current penetration levels of paints in India is low. Housing demand in India is likely to grow steadily as income levels grow and joint families splinter over time. As the industry leader, AP is using its cash flows to create capacity well in advance of anticipated demand. In the past five years, AP has invested Rs46bn in capex compared with just Rs20bn in the five years prior. Its A&P spend remains around 4% of sales, even on a much higher sales base.

“My view on the persistence of industry growth and confidence in Asian Paint’s industry positioning and execution abilities overcomes the concerns that the company has always appeared expensive on both an earnings as well as price-to-sales multiples.” Samir Mehta, Senior Portfolio Manager

Given this dynamic, my view on the persistence of industry growth and confidence in AP’s industry positioning and execution abilities overcome the concerns about valuation. Unlike Heinz, this company’s focus remains on the growth potential that lies ahead in the decades to come. It has invested in distribution, brand and capacity and is continually increasing its lead over competitors. The free cash flow for the firm in the next five years could possible double (or more) if demand for property starts to pick up in India. Even when the economy was slowing and inflation was high, AP demonstrated it had pricing power. It continues to toggle between retaining margins and reinvesting in the business. Overall, I do not foresee a fate similar to Heinz. On the contrary, AP’s approach to business might be one that Heinz is forced to veer back towards.

Read more about the Pendal Asian Share Fund

Fund Manager commentary for the month ended 28 February 2019 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.