We know this much – the trade war by China against the US has been going on for years. To the extent one wants to call this a trade war, we are determined to win it.

Mike Pompeo, US Secretary of State, September 2018

One defining feature of the Trump administration from an emerging market perspective is the willingness, even enthusiasm, to confront the United States’ geopolitical rivals. The US has significantly expanded sanctions applied to Russian companies and individuals while applying increasingly severe tariffs to Chinese exports. The effects have been felt in both countries, notably through currency weakness that does not seem to reflect the healthy external balances both countries enjoy.

One defining feature of the Trump administration from an emerging market perspective is the willingness, even enthusiasm, to confront the United States’ geopolitical rivals. The US has significantly expanded sanctions applied to Russian companies and individuals while applying increasingly severe tariffs to Chinese exports. The effects have been felt in both countries, notably through currency weakness that does not seem to reflect the healthy external balances both countries enjoy.

There is a temptation to view the actions of the US administration as both driven by the President and targeted at the popular vote, but we feel it’s important to look at some of the statements by other administration members to see where these policies might be headed, and what that might mean for emerging market investors.

Vice-president Pence recently summed up the administration’s view as “Beijing is employing a whole-of-government approach, using political, economic and military tools, as well as propaganda, to advance its influence and benefit its interests in the United States.” Whilst the military rivalry between the two powers has been visibly building over the last couple of decades, the focus on economic competition is a newer feature, and one with a strong advocate in the Trump government.

The Death by China script

Peter Navarro is an American economist and author who has been a hard-line advocate of a confrontational US trade policy towards China, most notably in his 2011 book Death by China. Having served as an adviser to the Trump campaign, he was appointed to an advisory post in the administration in December 2016, and much China policy since then can be seen to follow his views. Navarro very much sees the trade relationship between the two as akin to a war, accusing China of ‘cheating’ through uncontrolled pollution, poor labour standards, government subsidies, exporting counterfeit and dangerous goods, currency manipulation, and intellectual property theft. He has been a strong advocate of large tariffs on Chinese exports, with steel seen as a priority, and this is the exact policy path that has been followed. If there was any doubt, the Trump administration’s unusual step of creating a military space force is exactly what is called for in chapter eleven of Death by China.

One defining feature of the Trump administration from an emerging market perspective is the willingness, even enthusiasm, to confront the United States’ geopolitical rivals.

James Syme, Senior Portfolio Manager JOHCM

It is in this light, therefore, that we note with concern the recent Bloomberg scoop alleging that Chinese intelligence agencies caused highly specialist computer chips to be covertly placed in computer servers being exported to the US, thereby deeply compromising security at various US companies and government agencies. The potential for this to happen was highlighted in chapter ten of Death by China and this significantly increases the likelihood that the US seeks to disentangle some of its supply chains from China, not to improve the trade balance, but as a fundamental matter of national security.

Implications for emerging markets

This would have profound implications not only for China, but also for some key emerging market industries. It may create market share opportunities for Korean and Taiwanese companies at the expense of Chinese ones, but it is also likely to raise prices to consumers, increase capital expenditure and reduce returns on capital and reduce economies of scale. It is also likely to see continued weakness in the Chinese renminbi in response to diminished export opportunities, and will not be supportive of Chinese equities. Yet the Chinese reaction in September was to turn down further trade talks and to summon the American ambassador to Beijing to protest sanctions imposed on the Chinese military. Despite the economic consequences, there has been no backing down by China. As Lord Kitchener said, “No financial pressure has ever yet stopped a war in progress.”

More reading

Pendal Global Emerging Markets Opportunities Fund

Update – 15 October 2018: The following article was initially published on 21 September, based on prevailing valuations, to outline our thoughts on the inherent risks for FAANG stocks. This cohort have subsequently experienced significant share price declines in October after broader market sentiment particularly towards the US technology sector turned negative. On the surface our article may appear prophetic, however we don’t see the recent correction as a reflection of the key risks highlighted in this article these are yet to be acted on by the market. Regardless of whether the FAANGs decline further or even recover from this point, our fundamental reasons for not investing in Facebook, Apple, Amazon and Netflix remain unchanged. Similarly, our rationale for investing in the owner of Google remains valid and is in line with our long term approach to investing.

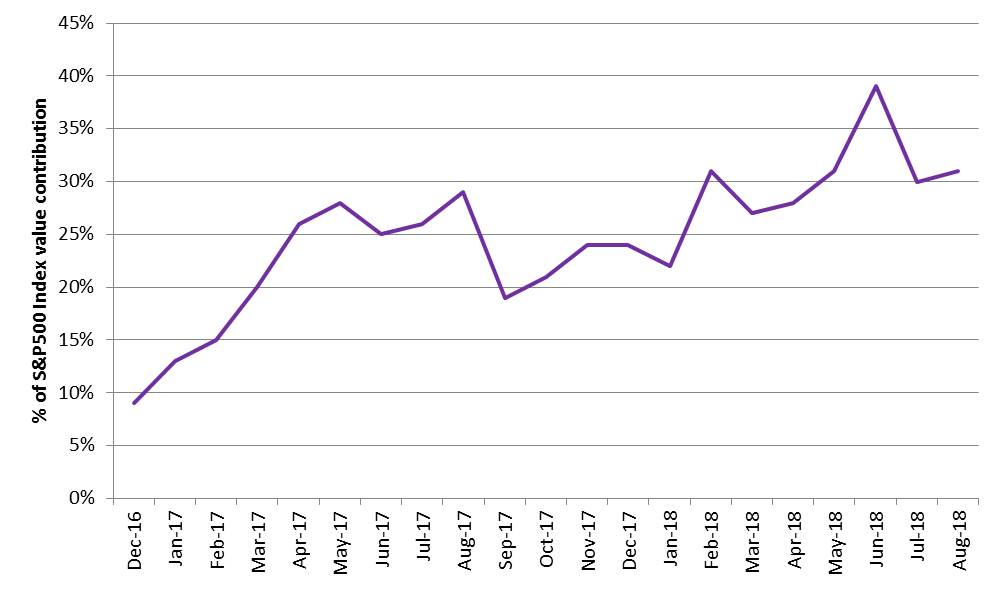

Many people love an acronym these days and fund managers are no exception so we’ll start this article with a somewhat cryptic collection of terms. The reference to FAANG stocks has been gaining broader recognition as a result of the meteoric rise in the share prices of its constituents. In 2018 this dynamic has led to a situation where the FAANGs have often determined the direction of the US S&P500 stock index. As with any stock, the higher the share price rises, the greater the risk of a correction, but we believe the inherent risks for some FAANG stocks are much deeper.

The collective of mega-cap global consumer technology companies known as FAANG stocks — Facebook, Apple, Amazon, Netflix and Alphabet’s Google — have rapidly grown in value over the past two years as a result of success in global penetration of their consumer products and platforms. These five stocks have become increasingly integral to the broader market’s performance and now represent around 15% of the S&P500 by weight. Their growing concentration within the US market has meant they account for 20-30% of the market’s movement in value. Expressed another way, for the first half of 2018, the positive return for the S&P500 was due to the FAANGs as they collectively added more than twice the value that the rest of the market lost. The growth in passive index tracking products also contributes to this self-fulfilling cycle, where price rises lead to index weight increases which then push prices further. Both Apple and Amazon reached milestones of US$ 1 trillion in total market value this year and are now larger than the annual output (GDP) of some countries such as Switzerland, Saudi Arabia and The Netherlands.

12 month rolling percentage of S&P valuation created by the FAANGs

Source: Pendal, Bloomberg

For simplicity we’ll continue to use the FAANG abbreviation to represent this group of five leaders in global technology enablement as we address a pertinent question on the minds of many onlookers: Could the Fear Of Missing Out on the massive share price gains become the more satisfying notion of Lucky To Miss Out? There are a number of valid reasons why at the present time, would-be investors in FAANGs can afford to be more sanguine about avoiding these stocks.

FAANGs reached their peak valuation in June before the market was made aware of earnings disappointments from Netflix and Facebook. Netflix’s share price was down 14% for the month; Facebook’s shares declined 20%, or US$ 120 billion to represent its largest one-day loss in value. This was a strong market reaction to the company’s future earnings prospects and the concerns are legitimate. Facebook’s core product is mature and revenue growth is primarily based on increasing prices for advertising. Netflix is now basing its expectations on user growth rates with little consideration for the incremental cash it will generate from each subscriber.

Similar concerns exist for other stocks in this group. Amazon’s business model is all about growing their share of online retailing with a focus on generating revenues rather than profits. At some point one will have to justify the other. Apple has a somewhat similar approach to capturing the biggest slice of the mobile device market. Its unit sales haven’t grown over the past two years and despite claims of its customers being captive to Apple’s iOS ecosystem, its market share has actually declined. And while Google has grown its share of the competing Android platform, it is heavy exposed to the highly cyclical online advertising market.

While these factors don’t necessarily mean these are bad companies they do increase the downside risk if current strategies fail to deliver. We would argue this is more than a remote possibility, considering the rapidly advancing intersection between technology, competition and fickle consumer preferences which can abruptly impact revenues.

Regulators on the trail

Until recently, FAANGs have been fortunate to grow while being relatively unfettered by government controls. Effective control over these behemoths of the technology world is far from simple to achieve, but the renewed vigour of regulators together with the rise of populism and anti-establishment political forces now present as a sizeable risk to the FAANGs’ business models, pricing structures and market access. Consider Facebook and its unintended leakage of personal information to Cambridge Analytica. This not only drew the ire of its millions of users but also resulted in CEO Mark Zuckerberg being hauled in for a ‘please explain’ grilling by US Congress. At the hearing he argued Facebook is a technology platform rather than a media company, although he conceded Facebook is responsible for what is posted on its platforms. This is an important distinction in the US as media companies face stricter regulations, are legally responsible for the content they publish and can be sued over the content of their platforms.

Zuckerberg sees greater investment in artificial intelligence as part of the solution but he knows there is some way to go on that front. Facebook have committed to hiring 10,000 new cybersecurity and content monitoring employees by the end of 2018. But of even greater concern is the broader impact of content restrictions. Facebook’s engagement metrics are most valuable at the extremes of content, so any material restrictions on content will have direct implications for advertising revenues. The US currently lacks a single comprehensive law regulating the collection and use of personal data, but the tide against the capitalism supports for mega companies like Facebook cannot be ignored. Recall the US Department of Justice case against Microsoft in the late 90s when the regulator sought to break up Microsoft on anti-trust law violations. Microsoft retained its structure on appeal, but it did result in the death of Netscape and subsequent ascension of Google.

Being a global platform also means offshore regulators share an interest. In July the European Union regulatory authority fined Google €4.3b (A$6.9b) for abusing Android’s monopoly to push Google’s apps on its own platform. The ruling determined that Google forced phone makers to preinstall its Chrome browser as a condition for accessing the GooglePlay app store and illegally paid manufacturers to preinstall its search app exclusively. Google are now required to give manufactures and phone providers free choice on the apps they install.

Margrethe Vestager, the European Commissioner for Competition, has been busy over the past few years increasing her efforts to limit the commercial power held by these companies. It makes sense that Europe rather than the US take the lead as it assumes all of the downside from social issues, interference with elections, job destruction, tax avoidance and anti-competitive behaviour but little of the upside from high-paying jobs, donations and value creation. The General Data Protection Regulation (GDPR) which came into effect in May is the most stringent legislation to date and aims to provide more control to citizens over their personal data. While it is still early to assess the real impact from GDPR, the cynic in me thought the timing of Facebook’s downgrade on their second-quarter earnings was interesting.

A little more than luck at stake

We acknowledge these are great companies, leading in their field with a global footprint. But everything has a price and as stewards of our clients’ capital we are reticent to invest on the basis of market leadership alone. Our process involves buying leading companies which have fallen out of favour with the market, often for reasons external to their underlying operations. They must be leaders in their industry but must also be attractive in terms of free cash flow, dividend yield, and trade on a buyout ratio of at least 8%. Our analysis needs to identify a clear catalyst for higher earnings. On these factors, Google (Alphabet Inc) is the only FAANG that qualifies for investment.

Google operates a robust business model with a 90% share of online search, 70% share of the mobile operating system (Android) and 45% of the online advertising market. YouTube is a clear leader in video and becoming a meaningful grow driver for the group. The regulatory risk for Google is considerably lower than for other FAANG stocks.

The only conceivable regulatory action that would have a meaningful impact on Google would be for its search algorithms to essentially become a utility where by the market is granted access under a regulated fee and licensing regime. We don’t view the likelihood of this happening any time in the foreseeable future as very high. The great advantage of Google’s search product is that it ages in reverse its algorithms become more powerful the more they are used. It also operates in a duopoly as online advertisers are effectively limited to two platform choices. Facebook and Google together account for about 80% of the global (ex-China) online advertising market.

The stock trades on a 16x earnings valuation multiple (excluding cash and losses from its non-core business) which is reasonable even after considering the risks. This collection of businesses is expected to generate earnings growth in the mid-teens for the current fiscal year.

By comparison, Amazon trades on a valuation that is very hard to justify. If we separate Amazon’s two core business Amazon Web Services and Marketplaces and value them separately, in order to justify Amazon’s current valuation our analysis concludes that the Marketplace business would need to achieve a 15% earnings margin. That margin would be three times larger than the best food retailers have ever managed to sustain in one of the most competitive and price sensitive industries in the world.

As for the other FAANGs we don’t see their current valuations as justified on the measures we focus on. We also believe the risks to their future earnings from regulatory imposts are yet to be appreciated by the market. Cyclical and product specific factors also arise when considering the maturity of some business lines. Market momentum factors may act to support their share prices in the short term, but at prevailing valuations I prefer to remain a humble user of iOS, transact via EFT, stream VOD and PM my contacts without sharing the nascent, yet real risks as a shareholder.

Regnan has released its annual report on ESG Engagement and Advocacy activity throughout FY18. Increased scrutiny of corporate conduct, mostly due to the Royal Commission, saw a higher number of engagements on this longstanding theme. Climate risk remains an ongoing engagement theme with ASX200 companies, in particular, to pursue enhanced climate-related disclosures, management of energy transition risks, and acknowledgment of the physical impacts of a changing climate.

Download Regnan’s Annual Report report here:

About Regnan

Regnan – Governance Research & Engagement Pty Ltd was established in 2007 to evaluate the relationship between environmental, social and corporate governance (ESG) factors and investment value. Regnan has evolved to become a global leader in long term value, systemic risk analysis and sustainable investment advisory.

Regnan provides ESG integration, advisory and stewardship services on behalf of institutional investors including asset owners, fund managers, wealth managers, retail and investment banks to drive improved ESG performance in S&P/ASX200 listed companies. Regnan meets with directors and senior company leaders, in a constructive manner, to influence change on issues with the potential to impact value over the long term.

Regnan is also a regular contributor to the public debate on long term value and sustainability, and is an active commentator in the media and at corporate and financial industry events. Regnan also provides submissions to government and other policy makers to improve both sustainable investment and the identification of systemic risks.

Regnan’s research insights are applied to Pendal’s Sustainable, Ethical and mainstream funds where relevant, as well as enabling us to work with other institutional investors in meeting their sustainability objectives.

DISCLAIMER

This document has been prepared by Regnan Governance Research and Engagement Pty Limited (ABN 93 125 320 041), (“Regnan”) and is republished with Regnan’s permission. It is for general informational purposes only and should not be relied upon in making a decision to invest or a decision in relation to an existing investment. It has been prepared without taking into account any recipient’s personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation.

The information relates only to Regnan’s assessment, based on its research and the information available to it, of the performance of a company in relation to environmental, social and governance issues and should not be regarded as a recommendation or statement of opinion by Regnan on:

i. any other aspect of the company’s performance;

ii. the prospects of the company; or

iii. the company’s suitability or attractiveness from an investment perspective.

The views expressed in this document are exclusively those of Regnan and the information contained within is current as of the date of publication. Pendal Group is the owner of Regnan and commissioned the company to provide research and engagement services for use as inputs into the decision making processes for Pendal’s investment activities. The views of Regnan expressed in this article may differ from those held by Pendal Group.

Edge – the projecting ledge or brink, as of a cliff; the part farthest from the middle; line where something begins or ends; the verge or brink, as of a condition

During times of risk aversion prompted by tighter liquidity conditions, as geopolitical risks re-emerge and long-term trade agreements unravel, it is rational to get a sense of revulsion when stock market volatility increases with downside bias, in conjunction with a large sell-off in emerging market currencies.

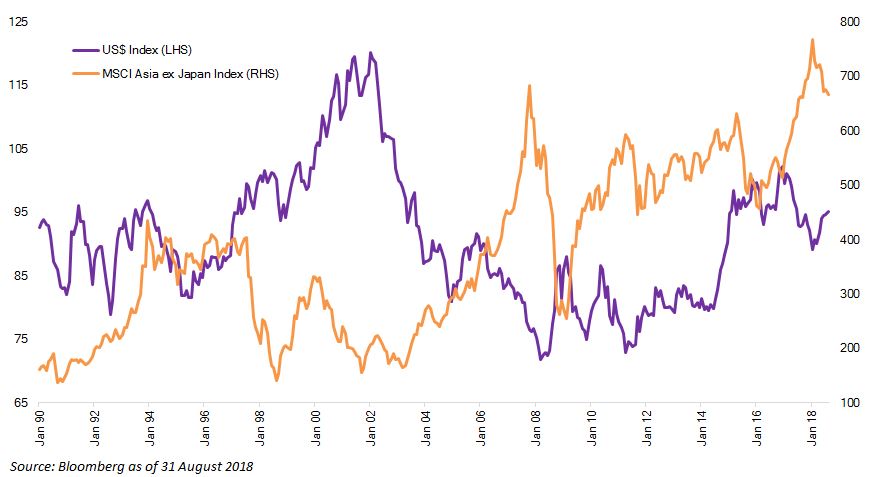

The US dollar trade-weighted index is a near perfect proxy for liquidity conditions in emerging markets, which in turn impacts all underlying asset prices including equities.

The mighty US dollar carries all before it

There is now near unanimity that emerging markets are in a tough spot, after years of loose monetary policy that led to higher debt levels in several of those countries. When those debts are US dollar-denominated, it exposes the weakness and tension between capital flows, rising domestic inflation and slowing growth. The trade off, in a simplistic way of thinking about the conundrum, is that growth has to slow and savings have to be rebuilt (a current account surplus). That should be either by raising domestic interest rates or by letting the currency weaken. In some countries, like Argentina or Turkey, the measures have been drastic. In Asia, none of the countries is in that dire a state but the taint of emerging markets and increase in debt levels is the common thread.

There is now near unanimity that emerging markets are in a tough spot, after years of loose monetary policy that led to higher debt levels in several of those countries. When those debts are US dollar-denominated, it exposes the weakness and tension between capital flows, rising domestic inflation and slowing growth. The trade off, in a simplistic way of thinking about the conundrum, is that growth has to slow and savings have to be rebuilt (a current account surplus). That should be either by raising domestic interest rates or by letting the currency weaken. In some countries, like Argentina or Turkey, the measures have been drastic. In Asia, none of the countries is in that dire a state but the taint of emerging markets and increase in debt levels is the common thread.

“The challenge, as I see it, is not just over resilience of the businesses we own but also on the ravages that liquidity induced sell-offs and currency depreciation will bring to markets.” Samir Mehta

The big concern for all of us, not just in Asia, surely remains how China manages this transition of tighter liquidity and slower growth. We came close to a similar looking edge in 2015/16. At that time, too, we appeared to be on the cusp of a hard landing. I distinctly recollect the scare when an unexpected change in the way China managed its currency led to fears of a meltdown, which further exacerbated capital outflows from China. By February/March 2017, with the US dollar appreciating, equity markets sold off aggressively, and we all thought this was the moment when China paid the price for its extreme indebtedness. A pause by the US Federal Reserve in its path of raising interest rates gave us the breathing space to come back from the edge. In that moment, it looked and felt like we were standing by a dark and bleak chasm, but, in hindsight, this turned out to be just another edge.

I have no clue whether the edge that we peer at today is a real precipice. As I’ve mentioned over the past couple of months, I have certainly reduced the portfolio’s cyclicality and added names that we perceive to be very resilient businesses. The challenge, as I see it, is not just over resilience of the businesses we own but also on the ravages that liquidity induced sell-offs and currency depreciation will bring to markets. Caution prevails.

Politicians think of their own survival and that means taking action that the population likes. Nobody talks about the need for pension reform anymore, and that’s worrying.

Robson Andrade, head of the Brazilian National Industry Confederation, quoted in Bloomberg article, 29 August 2018

Regular followers of our process will know that we consider a country’s current account balance to be a key indicator to watch. That doesn’t mean that it’s the only place where deficits matter, though. There are times when the fiscal balance is the more important metric. That has been the case in the ongoing crisis in Argentina (where we have had a zero weight), but also forms the backdrop for October’s presidential election in Brazil.

Argentina is in an economic crisis. To the end of August, the MSCI Argentina price index was down 54.5% in US dollar terms, as the currency sold off despite policy interest rates being hiked to 60%. At the heart of Argentina’s problems is a huge fiscal deficit (forecast to reach 5.0% of GDP this year). The monetary system’s financing of that deficit has driven credit growth at an annualised rate of over 30%, which was great for assets until foreign investors lost confidence, at which point it wasn’t. Argentina now has to brutally tighten both monetary and fiscal policy at the same time.

This is unfortunate timing for Brazil, as it grapples with its own economic pressures, very much including the fiscal deficit. Like Argentina, Brazil has a large sovereign debt outstanding (75% of GDP, compared to Argentina’s 65% pre-crisis and an estimated 85% now), which comes with very substantial interest payments. That makes it imperative that the primary fiscal balance (i.e. before interest payments) is positive, but that is neither the case in Brazil (primary deficit 1.4% of GDP) nor Argentina (primary deficit 2.5% of GDP).

And yet from this chaos, in the next seven weeks, must come the man or woman who will rescue the Brazilian national finances from future crisis.

Brazil’s two significant additional weaknesses are intertwined. The first is its utterly unsustainable pension system. The various generous pension systems, implemented during the transition to democracy, use a pay-as-you-go model in which the current workforce is taxed to pay pension payments. This system faces collapse with an ageing population; the combined annual shortfall of the pension schemes is close to 4.5% of GDP and set to rise.

In Brazil, only a constitutional amendment can modify pension laws, because the right to retirement benefits is engraved in the 1988 Constitution. Reform is incredibly politically difficult, needing the support of three-fifths of Congress to amend the constitution, and has proved impossible for both previous governments and the current Temer administration.

The second weakness is the chaotic state of Brazilian politics: there is a presidential election in October; the incumbent seized power through a controversial impeachment of his predecessor and has a popularity rating of 5%. At the time of writing, the two most popular candidates are campaigning from a prison cell (Lula, currently banned from standing) and a hospital bed (Bolsonaro, who has just survived an assassination attempt). All the candidates have negative net preference from the voters. And yet from this chaos, in the next seven weeks, must come the man or woman who will rescue the Brazilian national finances from future crisis. It is completely unclear as to who this will be or how this will happen, but it has to happen to avert disaster.

The second weakness is the chaotic state of Brazilian politics: there is a presidential election in October; the incumbent seized power through a controversial impeachment of his predecessor and has a popularity rating of 5%. At the time of writing, the two most popular candidates are campaigning from a prison cell (Lula, currently banned from standing) and a hospital bed (Bolsonaro, who has just survived an assassination attempt). All the candidates have negative net preference from the voters. And yet from this chaos, in the next seven weeks, must come the man or woman who will rescue the Brazilian national finances from future crisis. It is completely unclear as to who this will be or how this will happen, but it has to happen to avert disaster.

From a market viewpoint, the election of a president who can manage reforms could ignite a powerful rally in Brazilian assets. Year-to-date, the MSCI Brazil price index has fallen 20.8% in US dollar terms, to a 12-month forward price/earnings ratio of just 10.2x. The potential for large moves up or down certainly exists. We remain cautious in the face of all this, but equally are alert for the opportunity to participate in a powerful upward move should the political environment improve.

“We haven’t seen a trade war hit emerging markets. If it does I think it will be quite specific in terms of where it hits.”

James Syme, Senior Portfolio Manager, Pendal Global Emerging Markets Opportunities Fund

Investor caution towards emerging markets has increased this year as a strengthening USD creates real challenges for a number of EM countries. This caution has accelerated more recently with trade war rumblings and Turkey’s economic flashpoint.

In this quarterly update, Senior Portfolio Manager James Syme:

– explains, using Russia, Brazil and Turkey as live examples, why active top down country selection is so important in EM

– sets out the team’s rationale for key country-level overweight and underweight positions

– discusses the role the USD and oil prices will play in driving EM performance dispersion.

Further reading:

Be a part of the world’s fastest growing economies

Fund Manager commentary for the month ended 31 August 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

You’d be surprised how easy it is to take for granted the state of the world that you know.

You thought everything was fine, but then the GFC happened. Luckily, central banks covered up the mess with a put and plenty of liquidity.

You believed in the status quo, and then Brexit happens. Populism and nationalism have been ‘on trend’ ever since.

You never questioned the idea that global free trade is good, yet Donald Trump has started a trade war. He might just put the nail into the WTO coffin whilst he’s at it. Seismic shifts are happening right beneath our feet. Globalisation, it seems, can go no further in its current form.

Through all of this and more, China has remained the one constant. For all the talk of reform and economic transition, the recent shift towards domestic easing policies highlight that the old economic model remains dominant. This model has relied on a largely closed-economy system, with a currency that has been artificially kept weak over the last 30 years to support a flourishing manufacturing exports sector.

Cross-border capital flows have not been permitted, thus allowing the Chinese authorities fuller control over the financial system. This control has directed cheap credit to various industries from steel and cement to solar and high-speed rail. Debt-fuelled fiscal stimulus has been used to support growth at every turn.

What’s more, this model exists under a one-party socialist government. We in the West tend to view planned economies with disdain. There is a certain arrogance about governments who believe they can do a better job of allocating resources than the pure signal of market prices. The bad-debt problems now sitting with a swathe of zombie state-owned enterprises (SOEs) in China is case in point.

However, survival of the Chinese Communist Party and the political order that goes with it depends on continued economic progress, and its ability to carry the entire population along. This is a key point of difference between China and other socialist regimes such as Venezuela that have ended in suffering and demise.

Over the last 30 years, through its own poverty alleviation efforts, China has contributed as much as 70 per cent to global poverty reduction. Socialism with Chinese characteristics seems to offer a template for pragmatic implementation of the socialist agenda.

Since World War II, the US has tried to spread the liberal world order across the globe. By inviting China into the WTO, it was hoped that this spread could continue. Instead, whilst Chinese exports have hugely benefited from WTO membership, its industrial and political practices have moved even further away from liberal Western ideals.

The allure of the sheer size of the Chinese market has forced foreign firms to surrender their intellectual property. In return, they get to sell to and operate in China. Under the cover of subsidised cheap debt and de-facto protectionist policies that have limited the force of international competition on Chinese firms, ‘indigenous’ national champions have risen in various sectors across the Chinese economy (alongside many zombie companies to boot).

And if it can have its way, these continued practices to circumvent the spirit of international trade law would enable the success of its Made in China 2025 plan.

But the US has put its foot down. Among other things, Trump is viewed as the disruptor of global free trade. Tariffs and tweets are like hand grenades to him, thrown around to shake up the status quo, irrespective of how and where they land. Whilst his weapons are blunt, his motivations are widely echoed across party lines.

From China’s perspective, its industrial policies have been smart, but the US thinks they have been cheating. And if China’s rapid rise in the global pecking order is down to this type of behaviour, then Trump wants to fight fire with fire.

Theoretically, there is a high road that he could take, by engaging in the rule of law and soliciting support from its traditional allies. However, knowing that the law could never deliver any necessary punch, there really was no alternative for him than to get down and dirty with the same tactics as he’s witnessed from China.

If China’s $US3 trillion foreign reserve position is a symptom of unfair currency manipulation over the last two decades, then the least that Trump could do is talk down the US dollar. If China has been surreptitiously breaking WTO rules, then Trump will turn his back on the institution entirely. And if China has used fiscal stimulus funded by a ballooning debt stock to prop up growth and various industries, then Trump will unleash the largest fiscal package ever to be witnessed outside of times of war or recession.

Is this progress? It’s hard to recognise it as such when it spells the end of globalisation as we know it. Is this creative destruction? We will only know if these protectionist policies lead to a sustainable pick up in US industrial productivity – a tall order given that this declining trend has been impossible to turn for over a decade.

This article was first published by the Australian Financial Review on 26th August 2018.

Fund Manager commentary for the month ended 31 July 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Resilience: The ability to bounce or spring back into shape and position

There is always a debate in markets about what is the right price to pay for a good quality business. During this market cycle, since the 2008 lows in equity markets, businesses with growth characteristics have been rewarded with even richer multiples. Over the past nine years, with few exceptions, value as a style has remained unloved. On occasions, we did witness the value style outperforming growth (especially in times of macroeconomic stress or industry-specific worries), but that outperformance proved ephemeral. Despite an environment of reducing liquidity (central banks moderating QE) and rising interest rates, we have, so far, not seen any marked de-rating in valuation multiples for growth businesses. It is also a fair comment that in every market fewer businesses have delivered sustained growth in the face of several challenges, or are perceived to be in a position to do so.

Resilience matters

In the past few months, as I rejigged our portfolio, one big challenge I have grappled with is the high multiples for good quality businesses. Do I just buy stocks which appear to be squarely in the momentum trade, for whom valuation multiples already trade at significant premiums to the market? What if I misjudge the growth trajectory or the risks of industry disruption, currency volatility or a slowdown in the economy? In addressing those questions, the one metric I decided to re-emphasise was resilience. Every business invariably goes through challenging times. When it does, it is either the inherent resilience of the business, or the ability of management teams to deal with and engineer the requisite change, that differentiates it from more pedestrian businesses.

The unwelcome Maggi gift

One such resilient business I have added to our portfolio is Nestlé India (NI). A subsidiary of the Swiss multi-national, NI has operated in India for over a century and built upon its iconic brands in milk, nutrition, beverages, prepared dishes, chocolates and confectionery.

One of NI’s biggest sub-brands by far was and is Maggi Two-Minute Noodles. Between 2009 and 2014, NI aggressively expanded its factories to take advantage of potential growth in India. Yet, under the direction of its parent, NI shifted strategy to focus on improving margins at the expense of volume growth. It cut back on low-priced, lower margin products. That strategy may be appropriate in developed markets, but in a poor/emerging country like India, it made little sense, in my view, for NI to focus purely on enhancing margin at the expense of market share, growing the market and innovation. To an extent, that misstep by management led to lacklustre revenue growth in the past.

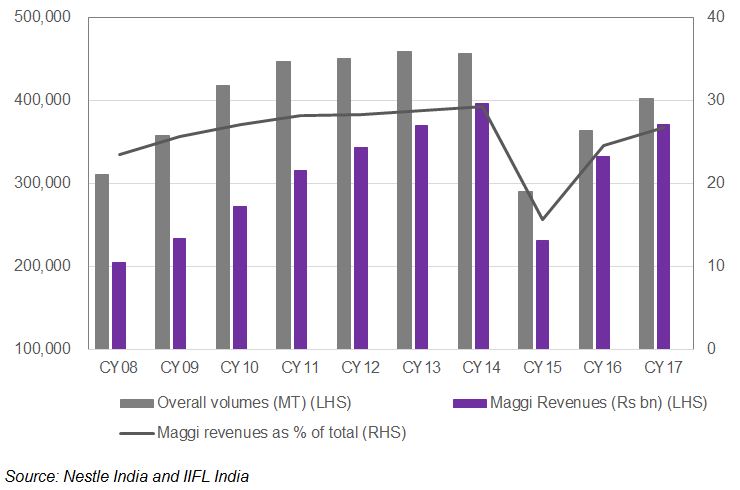

To add to this, in June 2015, one of the regulators in India banned NI from selling Maggi noodles due to food safety concerns. The food safety commissioner of Uttar Pradesh, the most populous state in India, claimed that a package of noodles contained seven times the permissible level of lead. Despite the fact that NI was convinced about its safety and quality record, NI decided to recall the product. All associated products, like Maggi jams, ketchups and beverages, were also badly affected, as consumers were naturally cautious. From a dominant 60-65% market share in noodles, NI’s market share almost halved overnight.

Nestle and Maggi Volumes

A fresh approach

But the brand was and remains iconic and NI had a lot at stake. Tackling the problem head on, NI appointed a new CEO, an old India hand. Under his direction, the management team and the company addressed the safety issue as a priority to regain trust. Simultaneously, it changed course and enhanced its innovation capabilities. In the subsequent couple of years, 42 new products were introduced. NI’s strategy turned 180 degrees, away from higher margins to growing volumes and market share with the help of innovation.

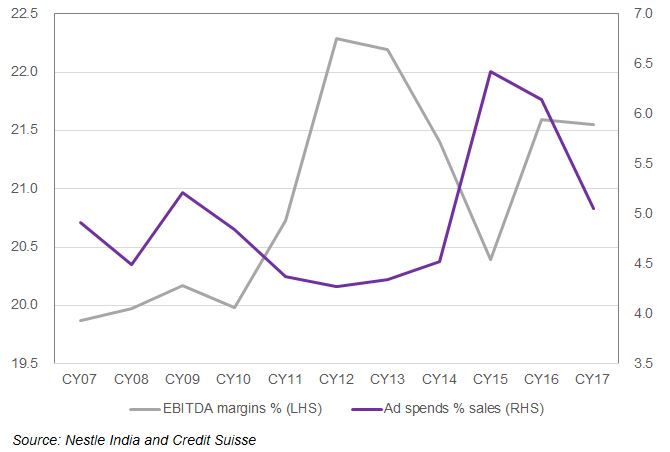

This new approach manifested itself in increased advertising and sale promotion spend. Just to put it in perspective, Nestlé globally has close to 2,000 brands; in India, it had just 20. India represents just 2% of global sales for Nestlé but has always remained a country that has great promise. There is an increased recognition by its parent that India needs to be run to meet the aspirations of Indian consumers; the local management team has been given the freedom to do so. Fortune favours the brave. This time around, NI has some tailwinds to aid what now seems to be a path towards sustained and highly profitable growth over the next few years.

Nestle India – EBITDA margins and ad spend

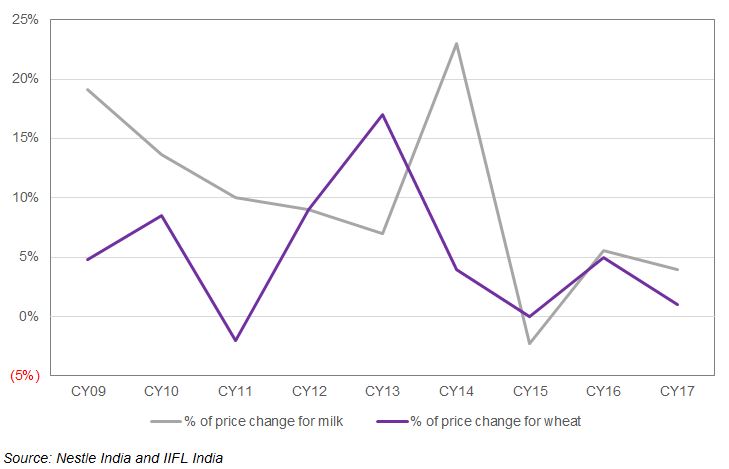

Commodity prices, particularly the ones most relevant to NI such as milk and wheat, have eased across the globe. This enables NI to take the higher costs from oil-related packaging products in its stride without feeling any pressure on margins. There is evidence of a recovery in consumer demand after two years of disruption post demonetisation and introduction of a Goods and Services Tax (GST). This nascent recovery could sustain as India heads into a general election, scheduled by May 2019 at the latest.

Milk and wheat price change

As is typical of governments when they approach elections, Prime Minister Modi’s administration has started to loosen the purse strings and hand out largesse to rural voters to appease them. As the rural economy starts to see better income growth, I do think NI will keep innovating and introduce more brands from the parent into the Indian market.

A rich valuation but consider the growth prospects

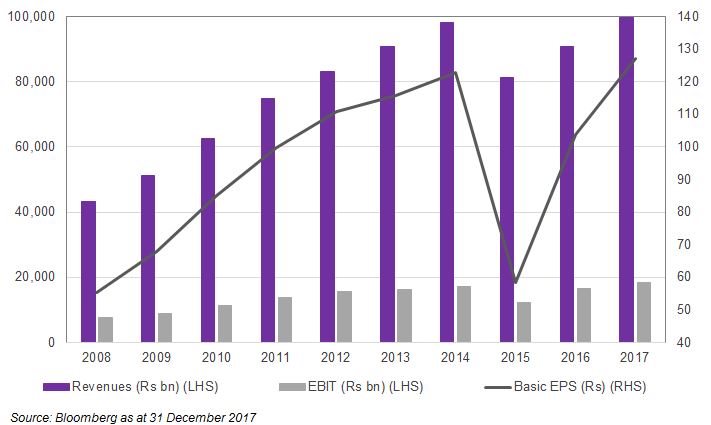

This leaves us with the question of NI’s valuation: the stock trades on a 50-52x multiple for 2019 earnings. For some, that’s a nosebleed-inducing valuation. On the face of it, that multiple does look rich. Yet I would suggest we put in perspective, looking at financials from 2013 onwards. In the past four years, NI’s revenues, earnings and earnings per share have barely budged.

Revenues, EBIT and EPS have flat-lined

There were genuine reasons for a below par performance. However, in my view, we are on the cusp of change. If the company does execute on its plans, it is quite feasible that in the next four years revenues and earnings double from where they were at the end of 2017. In what could be a turbulent period for macroeconomic reasons across the world, that kind of resilient sustained growth will deserve premium multiples. That’s why I am willing to take this positive view on Nestlé India.