“US consumer staples plunge as bond yields rise”

Financial Times, 24 May 2018

We wrote last month about the negative effect of rising US bond yields on some emerging economies (and their currencies). The sharp sell-offs in Argentina and Turkey in May support our views, but there are also some key sector effects in this environment.

So far 2018 has seen ample evidence of a strong global growth environment, but with gently building inflationary pressures putting upward pressure on bond yields. From a starting level of 2.4%, US 10-year Treasury yields reached 3.1% in mid-May. The increase in risk-free bond yields puts pressure on other income-generating assets around the world, including emerging market bonds, but also including low-beta, dividend-paying stocks, the so-called ‘bond proxies’. These stocks, principally in the consumer staples, telecom and utilities sectors, have generally performed well in recent years, but now face a less favourable environment.

This has been the case in emerging markets year-to-date. With the MSCI Emerging Markets price index down 1.0%, MSCI EM indices for consumer staples, telecoms and utilities are down 3.2%, down 9.8% and up 1.5% respectively. The portfolio is significantly overweight consumer staples (in India, Mexico and Russia, which provide exposure to domestic demand; in South Korea, China and Brazil as more defensive positions), and broadly neutrally-weighted in telecoms and utilities.

The consumer staples position has been a negative contributor to the portfolio’s performance year-to-date, but within the sector there has been a broad range of returns. The investments with exposure to China include Tingyi (noodles) and South Korea’s LG Household & Health (cosmetics), which have both performed well after a strong 2017, and also Hengan International (infant care), which has lagged year-to-date after a strong 2017. We see continued strong growth in the Chinese consumer sector in 2018, despite monetary tightening, with companies holding strong brands able to push through earnings-enhancing average-selling price increases in 2018. Also generating positive performance despite a weak country performance has been retailer Walmart de Mexico (Walmex).

India’s ITC (tobacco) and Russia’s Lenta (retail) are about flat year-to-date. Both countries are seeing a pick-up in economic growth, but the higher oil price is a tailwind for the Russian consumer and a headwind for the Indian consumer. Tax increases have also been a drag on ITC’s operational performance. Also in Russia, retailer Magnit has been weak this year, as investors wait to see the effects in a change of corporate leadership.

Our process remains assertively top-down, but stock selection also remains a key part of the process, as can be seen in recent performance.

The bulk of our underperformance in consumer staples has come from Brazilian food producer BRF, which has underperformed even a generally weak Brazilian equity market. It has struggled to maintain margins despite lower input prices and the weakness in the Brazilian real. As it the case with Magnit, there has been a change in management, the effects of which are yet to be seen.

Nonetheless, the positive contribution of telecoms and utilities has more than offset the drag on performance from consumer staples. In each case we have a single Chinese holding. China Mobile reported impressive 2017 results but declined slightly, in line with the MSCI EM Telecommunication Services Index, but our utility investment, ENN Energy, performed very strongly (+46.3% in US dollar terms), on continued strong demand for natural gas in Chinese urban areas.

Overall, the portfolio has seen a positive contribution from its investments in bond proxies. While some of this came from good top-down calls, it was principally through stock selection. Our process remains assertively top-down, but stock selection also remains a key part of the process, as can be seen in this case.

This case study on Pendal’s credit risk assessment based on ESG factors was published by the PRI — the world’s leading proponent of responsible investment — as part of their ESG in credit ratings initiative which aims to enhance the transparent and systematic integration of ESG factors in credit risk analysis.

In this case study, George Bishay, Portfolio Manager of the Pendal Sustainable Australian Fixed Interest Fund, shares his insights into the rationale for limiting exposure to credit issued by Coca Cola Amatil. The decision reflects long-held concerns over the social risks associated with high sugar and the consequences of structural shifts in consumer behaviours. This case study provides a timely illustration of the impact on corporate profitability from non-financial considerations and the value that can be added through integration of ESG assessments in credit analysis.

Click here to view the case study.

This case study is included in Appendix 2 (pages 56-57) of the ‘Shifting Perceptions: ESG credit risk and ratings‘ report which explores the disconnects encountered when integrating non-financial risk assessments. The report delves into PRI’s findings on the challenges encountered by credit practitioners in integrating ESG-related risks, together with practice guidance on the implementation of risk assessments and engagement with credit ratings agencies.

Fund Manager commentary for the month ended 31 May 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Infrastructure develops at a glacial pace in Manila. On a short visit, you would hardly notice any meaningful change in this often chaotic city. Bumper-to-bumper traffic, it took us almost 25 minutes to exit the airport and traverse 500 metres across a traffic junction.

Yet there is change. ‘Entertainment City’ houses three of the four newly-built integrated resorts and casinos, the first of which opened in 2013. That whole area is wide open with broad boulevards, a sea-facing frontage and swanky new buildings. A new expressway, completed in 2016, connects the airport to these casinos and has cut travel time to just 20 minutes from more than an hour prior to 2016. It is no wonder that tourism to Manila, in particular from China, has started to pick up, as has the revenue of those casinos. Several large areas that are converted townships are witnessing a boom in property construction. Even outside Metro Manila, in Visayas and Mindanao, there are new roads and airports under construction.

Effective January 2018, Filipinos had a relatively big change in their tax policies. Under the first part of the reform process, income tax for low and mid-level salaried employees was substantially reduced. However, taxes were raised on a host of items, including petroleum products, cars, tobacco and sugar-sweetened beverages. In the next stage, the government wants to reduce corporate taxes from 30% to 25% while simplifying the myriad of incentive schemes given to states.

During a time of rising oil prices and a weakening peso, these changes in taxes are affecting several parts of the economy. For one, costs have increased across the board as petroleum prices have risen. In general, inflation is rising and the pernicious effects are being felt by the most vulnerable and poor sections of society. Companies which cater to the low income part of society, such as Universal Robina, have seen sales slowdown while companies like Robinson Retail, which cater primarily to middle income families, have seen a bump up in sales. The middle-income cohort seems to be in a much better position, especially as they benefit from the income tax reduction. Yet, so far, overall consumption is relatively benign.

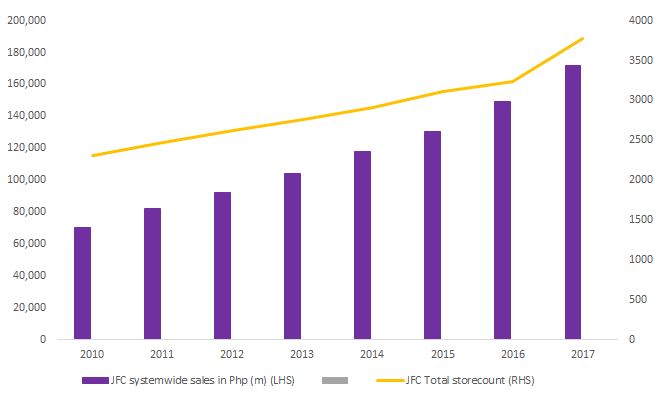

We spent a fair bit of time with Jollibee Foods (JFC), the only Philippine stock we currently own in our portfolio. It is a leader in the quick service restaurant (QSR) business in Philippines, with an expanding footprint around the world. If done right, QSR businesses can be very profitable and scalable. American chains such as McDonald’s or Chipotle are prime examples of the model. I’ve seen analysis on QSR models where the EBITDA returns on total investment per store can range from 18-30% pa. In JFC’s case, their main brand Jollibee earns returns per store upwards of 35%.

Over the years, JFC has expanded its offerings of different cuisines in the Philippines. One brand they acquired in 2010, ‘Mang Inasal’, has expanded its store network from 345 to 495 stores in the past seven years. However, by improving sales per store by almost three times, total revenues for that brand increased from Php2.3bn in 2010 to Php17bn in 2017. Once a concept is successful, JFC expands to destinations abroad where there are Filipino nationals.

JFC ventured into China in 2005 and for a long time after that the China business was a struggle. Intense competition, rising wage costs, and lastly a structural shift to online ordering of food have tested its Chinese business. After stagnating for almost three years as management figured out a way to deal with challenges, 2017 has seen a low double-digit same-store-sales growth.

Jolly steady growth at Jollibee Foods

JFC recently took over Smashburger, a burger chain in the US, and increased its existing stake in a company that is expanding in Vietnam to a majority. In the past couple of years, the management team has invested a fair bit, expanding new stores and acquiring new formats. Given their past record of accomplishment, I have reasonable confidence in their ability to execute on this expansion. It is a challenging time for the business: peso depreciation, rising inflation, tax changes and structural changes to the restaurant industry from online food delivery businesses. Yet with a 16% growth in system-wide outlets, a healthy balance sheet and the ability to increase prices and maintain margins over time, JFC should be able to grow through these tough times.

Well that was certainly fun. Over recent months we have been making the strong case that as a result of the normalisation of global monetary policy, global liquidity will recede and market volatility will rise. Well it certainly did in May as Italian yields puked and global asset markets reacted. The era of Quantitative Easing (QE) boosted asset prices and bought forward future asset returns to today. We expect that in a period of Quantitative Tightening (QT) the reverse is going to happen. To be crystal clear, a normalisation of the QE experiment requires adjustments, and those asset prices that have benefited the most from the abundance of liquidity are likely to be the ones that will require the greatest of adjustments.

This month, I focus on the current key events, the casualties of May and how markets will continue to unfold.

View the newsletter here.

The Pendal Defensive Equity Income Fund closed to applications and reinvestments effective 7 June 2018 and will terminate effective 17 July 2018, with the assets liquidated and the net proceeds returned to investors.

More information

The Pendal Balanced Equity Income Fund closed to applications and reinvestments effective 7 June 2018 and will terminate effective 17 July 2018, with the assets liquidated and the net proceeds returned to investors.

More information

Market headlines in the final week of May were dominated by developments in Italian politics. Uncertainty over which parties would lead the country’s government and what policies they would pursue drove some sizeable price swings that extended beyond Italian bonds. We will delve into the details and explore the situation in more detail in our upcoming newsletter. For now, we thought it would be timely to highlight some of the more noteworthy market movements and the relevance to broader risk-sentiment.

The most dramatic reaction to the Italian turmoil has arguably been witnessed in yields for Italian bonds, the fourth largest bond market in the world. As illustrated in Chart 1 below, the 2 year Italian yield spiked an alarming 304bps during the month. This benefited our positioning for a widening in the spread between Italian and German yields. Given the arithmetic of the election results in March, there was never a possibility of a market friendly outcome. The best outcome for the establishment parties was a second election, but in reality this would have just bolstered support for the populist parties. Moreover, while there were echoes of the French election worries that ultimately fizzled last year, as we explore later – the market environment has changed and risk sentiment is more vulnerable than 2017.

Chart 1: Italian 2 year yield

Beyond Italy, the sharp correction for risk appetite spread through the region with Spanish bonds suffering a smaller but still significant spike (2 year yields from -34bp to 7bp). Similarly, the region’s common currency endured a 3.2% slide, the largest monthly decline since November 2016. The spill-over effects were also felt in the credit arena, where the cost of protection on European high yield jumped 51bps. This accelerated the trend higher calendar-year-to-date as visible in Chart 2. These sizable moves served our short credit and short Euro exposure well.

Chart 2: European High Yield CDS Credit Spread

In terms of the economic landscape, we have previously pointed to reasons why we believe the European growth story has tired and has already turned a corner. This includes the gusting tailwind of strong export growth fading to a breeze as the surge in Chinese imports drops, coupled with the looming effects of trade wars.

While the situation in Europe is likely to continue capturing investors’ attention in the near-term, the real story is one that we have spoken of repeatedly this year, namely; the return of volatility. It is a story driven chiefly by the withdrawal of an unprecedented swell of liquidity in the financial system. A tide that had lifted all asset classes, but more importantly a force that had lured investors to those offering higher yields, which are now those that are the most at risk of an unwind. We won’t rehash all the implications here – our March newsletter discussed some of the dangers in more detail. What is worth emphasising is that the aforementioned moves across Italian bonds and high yield credit are part of this much larger story, which arguably has many more chapters ahead.

In the weeks leading up to Easter, the Pendal Concentrated Global Shares Team completed its latest round of due diligence which took the team to parts of Europe and the US to review companies involved in various industrial functions, energy, financial services, real estate, and consumer goods. This trip provided the team with the opportunity to identify new investments, stress test existing portfolio positions, and confirm the underlying tenet of our portfolio that the global economy has reached an inflection point remains intact.

Company meetings – March-April 2018

Our meetings did very little to dispel our belief that the global economy remains on a path of growth. Interestingly, no group of companies were more positive than the industrials, despite President Trump’s tariff impositions, which evolved from rhetoric to reality during our trip. From the humble tractor maker to the builder of aircraft, confidence was shared by all and stems from the fact that much of the demand to date has related to replacement rather than expansion, with any over-enthusiasm being kept in check by a supply chain struggling to keep up. Quantitative measures such as equipment pricing, rental rates, and backlogs are all trending favourably and are supportive of the view that growth will extend beyond what is shaping up to be a very strong 2018. While a lot of the industrials space has already re-rated, opportunities remain and we look forward to sharing these in due course.

With regards to the businesses already in the portfolio, the trip left us comfortable with our ownership of Boeing, despite the value of the company having doubled over the past year. We believe the quality of the business continues to be underappreciated by many in the market which, under the leadership of CEO, Dennis Muilenburg, has been re-engineered to become a more responsible allocator of capital and generate persistent growth in free cash flow. Since our last update, Boeing has continued to make solid progress in its key aircraft program. The company is continuing to grow its order book and has committed to increasing the production of 787 aircraft from 12 per month currently to 14 per month. Boeing recently delivered the inaugural 787-10 to Singapore Airlines and continues to undertake due diligence on the much anticipated ‘middle of market’ airframe.

New portfolio investment

The latest addition to the Pendal Concentrated Global Share Fund is Seven & I Holdings. This Japan-listed company exhibits many of the characteristics favoured by the team and our process. In this edition of our Global Research Trip notes we share our insights from recent site visits to the company’s US outlets and the opportunities we see for investors.

—————————————————————————————————————————————————————

Who is Seven & I Holdings?

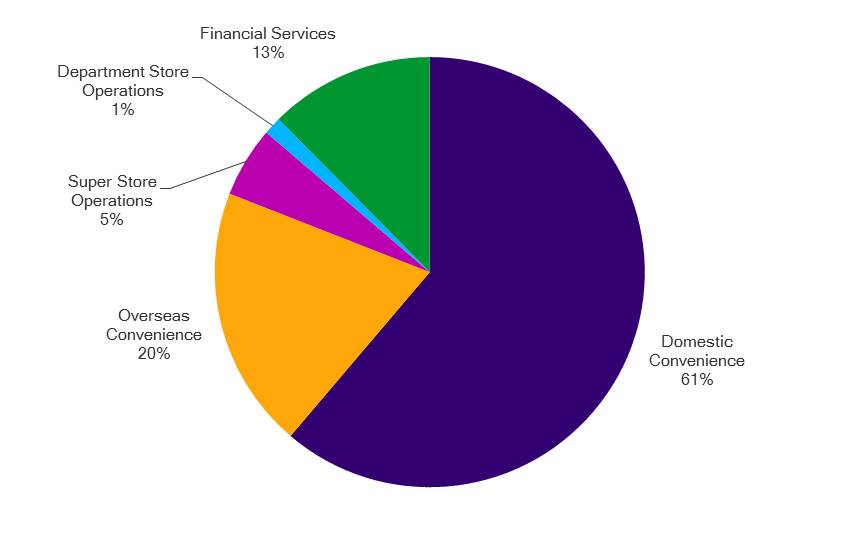

Seven & I Holdings (herein referred to as 7-Eleven) entered the team’s investment radar late last year during a research trip to Japan. The business operates/licenses/franchises stores under the 7-Eleven brand and is the leader in Japan’s convenience store (“C-store”) market. The company is building upon its 44% market share through a fresh food offering that resonates with the country’s demographic and lifestyle demands. Complementing the C-store business in Japan which makes up 61% of earnings is the overseas C-store business where 7-Eleven is a top player in the consolidating US market. The company also operates a profitable financial services business and a portfolio of shopping centres and department stores in Japan.

Seven & I Holdings (herein referred to as 7-Eleven) entered the team’s investment radar late last year during a research trip to Japan. The business operates/licenses/franchises stores under the 7-Eleven brand and is the leader in Japan’s convenience store (“C-store”) market. The company is building upon its 44% market share through a fresh food offering that resonates with the country’s demographic and lifestyle demands. Complementing the C-store business in Japan which makes up 61% of earnings is the overseas C-store business where 7-Eleven is a top player in the consolidating US market. The company also operates a profitable financial services business and a portfolio of shopping centres and department stores in Japan.

Seven&I Holdings – business overview

Why we invested in Seven & I Holdings?

We initiated a position in 7-Eleven at the start of 2018 after our initial due diligence revealed a business where the troubled performance of its non-core assets (i.e. department stores, supermarkets and shopping centres) was overshadowing the dominant position held by the Japan-based C-store business and the opportunities within a consolidating US market. The non-core assets of the business have been so overbearing that there is now a significant valuation disparity compared to C-store operators both in Japan and North America.

Japan retail sales growth by segment: 1998-2016

Source: Japan Ministry of Economy, Trade and Industry. Growth has been indexed; 1998 = 1.00

Under the leadership of CEO Ryuichi Isaka, we have confidence that the significant value we see in the business will be unlocked. Appointed in 2016, Isaka-san’s approach to the business can be summarised as one of capital discipline, having outlined a strategic mandate that has demanded smarter investments in the Japan C-store business, improve in-store execution in the US C-store business, and close or divest department stores and shopping centres. In his first year, Isaka-San closed four department stores and 11 shopping centres/general merchandise stores, with more to come under his five-year plan. Over time, the rightsizing of non-core assets will help further de-risk the business and re-focus investor attention to the company’s core competencies. In the interim we are paid to wait through a circa 2.5% dividend yield.

What we learned about the business from our US trip

As part of our initial due diligence it was suggested to us that the US C-store market is primed for consolidation, with more than 150,000 stores of which, 65% are owned by operators of fewer than 10 stores. The two biggest operators, 7-Eleven and Alimentation Couche-Tard, have less than 10% market share each and were expected to be benefactors of the impending consolidation.

Our visits to numerous C-store operators in the US confirmed the validity of the consolidation thesis. We observed a significant gap in execution between the independents and chains a gap that will only get wider as the chains make investments to differentiate and enrich their food offerings and improve their technology capabilities. With some independents already struggling to fund working capital (e.g. empty shelf slots), it’s likely they’ll be left behind in the current investment push.

Conclusion

Overall, we left the US confident of 7-Eleven’s strategy in the US. The growth trajectory is significant as the independent operators, who are struggling for capital, act as market share donors for the chain operators for decades to come, either organically or through mergers and acquisitions. Since buying the stock, it has outperformed the MSCI AC World ex-Australia (A$) Index by nearly 7% as it continues to gain market share from Japan convenience store peers, execute on cost efficiencies, and return non-core businesses to profitability. Continued execution on these fronts should help reverse the valuation discount to peers, which is in excess of 20%. Having served 7-Eleven in a range of roles since 2009, Isaka-san knows the convenience store business well and exhibits the commercial acumen to drive organic growth in a strident, yet sensible manner.

Fund Manager commentary for the month ended 30 April 2018 covering market reviews, Pendal fund performance and our outlook for the period ahead.

Access the monthly commentary here.