Fund Manager commentary for the month ended 28 February 2018 covering market reviews, BT Investment Management fund performance and outlook for the period ahead.

Access the commentary here.

The February flash crash served as a warning shot to the market to expect further volatility ahead. The goldilocks narrative of strong growth with benign inflation morphed into ugly inflation and deficit concerns in the US, driving bond yields higher which dragged equity markets lower. Within five trading sessions, the S&P 500 index undid the melt-up of the first three weeks of the year, and by the close of the 8th of February, the market was down over 10% from the peak.

In this Newsletter I take a close look at how global FX markets have been behaving and delve deeper into the prevailing narratives currently underpinning a bidless environment for the US dollar.

View the newsletter here.

“Ramaphosa inherits stagnant economy and divided party”

Financial Times, 15 February 2018

One of the unfortunate facts of emerging market investing is that emerging market political leaders who come to power with promises of much-needed reforms tend to disappoint. Even in the last few years, leaders from Jokowi in Indonesia to Enrique Peña Nieto in Mexico have started their leaderships with significant progress but subsequently disappointed (“Jokowi’s 35,000MW electricity program only reaches 3.8% progress” – Jakarta Post, 4 March 2018; “Release of jailed union boss reveals Mexican president’s empty promise” – Guardian, 21 December 2017).

The latest new national leader to promise a break with the past is South Africa’s Cyril Ramaphosa, elected the country’s president in February following the resignation of Jacob Zuma after a raft of corruption allegations. From the December 2017 confirmation that Cyril Ramaphosa would replace Jacob Zuma to the February 2018 transition of power, the South African rand rallied 14.0% against the US dollar, reflecting optimism for political and economic reforms under a Ramaphosa administration. In particular, his decision to recall previous ministers Nhlanhla Nene and Pravin Gordhan (both sacked by Zuma) suggests improved prospects for economic policy and governance.

However, it is our view that South Africa faces serious economic challenges with no obvious solutions, while the broad political grouping that is the ANC will further constrain the new Government’s ability to act.

We regard all incoming EM political reformers as ‘show-me’ stories, but this is particularly true of Cyril Ramaphosa, as we cannot even see the reform path that would turn South Africa around.

The most serious problem for South Africa is its failure to generate economic growth. The National Development Plan requires a 5.4% economic growth rate to make a serious dent in the country’s 27% unemployment rate. Growth in the last five years has averaged 1.4%, and consensus expectations are for 1.5% in 2018 and 1.7% in 2019. There are various reasons for the poor growth rate, but South Africa’s failures in the last 20 years to support both infrastructure and education are particularly to blame. While the recent water supply shortage in Cape Town has attracted the most news coverage, a chronic undersupply of electrical power has had far worse effects on business and the economy. To address either the infrastructure or education problems will take large sums of state investment as well as considerable time, which make improvements seem simply impossible.

The South African fiscal budget remains materially stretched. The fiscal deficit is estimated to have been 4.3% of gross domestic product (GDP) in 2017, Fitch and S&P cut South Africa’s sovereign credit rating to junk last year, and Moody’s put the country on review for a credit downgrade in November 2017 (which is expected to be confirmed later this month). Meanwhile, parastatals like electricity power utility, Eskom, face financial distress. Eskom has recently sought ZAR20 billion (AUD$2.15 billion) in emergency credit from the Government just to remain operational. The higher education sector needs an additional ZAR 12 billion (AUD$ 1.3 billion) in financing this year.

In addition, the good news of the appointments of Nene and Gordhan is balanced by the problematic appointment of David Mabuza as Deputy President. Being an old ANC party insider from the struggle against apartheid, Mabuza has been the subject of very serious allegations in the last few years, including links to corruption and violence. The Ramaphosa administration is emphatically not a clean break from the Zuma years.

We regard all incoming EM political reformers as ‘show-me’ stories, but this is particularly true of Cyril Ramaphosa, as we cannot even see the reform path that would turn South Africa around. We remain cautious on the South African economy and currency, and prefer to invest in South African companies doing most of their business in other emerging markets.

Each year on the 8th of March, women the world over commemorate International Women’s Day. This year marks the 110th anniversary of the movement, and the fundamental reason for its existence is just as relevant today. Gender equality has long been an issue facing society and progress has been iterative. Pendal’s Head of Responsible Investment, Edwina Matthew, provides a detailed insight into not just the social imperative, but the economic value to corporations in adopting a broader focus on diversity that actually extends beyond the gender divide.

Diversity is an issue with growing prominence across corporate enterprises. Although the issue most readily raises a connection with gender equality, the concept of diversity has broad-reaching demographic variants that cover gender, age, ethnicity, religion, and much more. Collectively, these form a nucleus of economic value for a business that leverages diversity from the board level right through the company’s organisational structure.

Widening the lens

Historically, diversity within the business community has tended to be thought of as an “insurance policy” against brand or reputation or operational risk. More recently, diversity has become an important social and governance issue, heralding an era of closer scrutiny by customers, shareholders and other stakeholders on behaviours and actions of corporate leaders. Increasingly, companies need to earn a social license to operate from both internal and external sources.1

From an investor perspective, the focus on diversity may be linked to management quality, to others it may represent awareness of particular stakeholder priorities, while for others it may be associated with expected benefits related to fewer instances of bribery and corruption . Regardless of the motivation, recent trends across the investment industry have helped to widen the lens on diversity.

Building the (“smart”) business case for diversity

There is a growing body of industry reports and academic research supporting a connection between diversity and shareholder value. A 2016 Credit Suisse study found a positive relationship between gender diversity and return on equity. Their research suggests companies with at least one female board member earned an annual excess compound return of 3.5% over the MSCI All Country World Index since 2005.2

Looking at diversity from another direction, studies have also found a positive link between increasing participation of women in labour markets and a sizeable improvement in GDP and world leaders are taking note. Canadian Prime Minister, Justin Trudeau, has spoken strongly on the need to address the gender imbalance “not just because it’s the right thing to do, or the nice thing to do, but because it’s the smart thing to do.”3

In Japan, Prime Minister Shinzo Abe introduced a program (“womenomics”) incentivising Japanese companies to hire more women, especially at levels of leadership in an effort to alleviate pressures on the Japanese economy in relation to the nation’s aging population.

Diversity and the generational dollar

Another demographic influence supporting the business case for diversity is the growing influence of the millennial generation as consumers and members of the workforce. By 2025, millennials are set to make up 75% of the global workforce, revolutionising businesses from both an employee and consumer perspective.4 A number of studies report that millennials place a higher value on diversity than older generations and they actively look for diversity and inclusion programs in their prospective employers before making a job decision.5 This and other studies highlight the imperative for businesses to cater to the expectations of this generation, not only as employees, but as customers.6

Diversity and disruption

Today’s rate of technological change is a form of disruption and is challenging many business models. Advances in technology can ironically introduce the potential for unintended bias, including gender bias. For example, despite the technology intensity and specialist skills deployed in developing Artificial Intelligence, there is actually a role for corporate governance and ethics-based oversight. Companies need to better understand consumer patterns and need to design gender-neutral products that also work for 50% of the population.

For the sceptics, there are plenty of examples through history of what can happen in technology when homogenous working environments fall prey to group think. Take the example of the early incarnations of air bag design for automobiles. Researchers suggest a fundamental lack of diversity goes some way to explaining failures of the technology which resulted in casualties. Consider that the engineering and automotive design professions were heavily dominated by males, who only consulted height, weight and body structure metrics for the average male. This approach overlooked suitability for females and children who are naturally different in stature.

Diversity applies beyond the board room

Diversity is becoming an important attribute for analysing the effectiveness of boards and senior leaders of companies. Bringing a team together with differing views and experiences can and should lead to rigorous debate and stress testing of proposals at the board and management level. Leaders need to be conscious of their own biases and demonstrate objectivity in making decisions.

“It’s the combination of diversity and inclusion initiatives that drive sustainable organisation change and thus deliver the diversity dividend”

Edwina Matthew, Head of Responsible Investment, Pendal Group

However, to be successful, a diversity policy needs to go beyond the boardroom. Without education and reinforcement on the value to the company it merely forms a discretionary guideline and can be tokenistic in nature. A company that fails to empower people to share ideas and debate initiatives risks failure in innovation. In other words, it’s the combination of diversity and inclusion initiatives that drive sustainable organisation change and thus deliver the diversity dividend.

Asset owners share the prerogative

The growth trend of adopting responsible investing principles is promoting a focus on diversity within company engagement and proxy voting activities. In its analysis of the 2017 proxy voting season, PRI noted diversity-related shareholder resolutions as one of the three key global environmental, social and governance (ESG) themes in 2017. Regnan (leading Australian ESG data, research and engagement service provider) also notes growing attention to diversity as an engagement theme locally.

This week (8th of March) the world celebrates 110 years since the campaign behind International Women’s Day began. This year’s theme is #PressforProgress in support of gender parity. However, this call to action could also apply to a broader definition of parity. Attitudes are shifting as companies, policy makers, asset owners and consumers all come to understand the negative effects of a diversity deficit. All along the investment chain we are witnessing a greater sense of shared responsibility for ESG issues, and pressing for progress on diversity is a priority.

The bottom line

A company’s approach to diversity can be an important indicator of overall business resilience and management quality. In this new era of heightened stakeholder scrutiny, combined with the growing social conscience of the younger generation, means that explicit attention to ESG issues such as diversity will continue to increase in importance. Organisations that pursue diversity-smart leadership, operations, product design and technological innovation and take the steps to capture the opportunities it offers, will be better placed to understand the world in which we operate, better able to identify the risks and opportunities, and ultimately achieve better business outcomes.

This article is an extract of a more in-depth discussion on the social and economic value of broadening diversity practices.

1. In October 2017 the European Securities and Markets Authority (ESMA) announced new diversity disclosure requirements for large, listed companies in the European Union. In Australia the ASX Corporate Governance Council requires explicit disclosure on progress towards achieving measurable diversity objectives for all Australian listed companies. The United Nations supported Principles for Responsible Investment (PRI) is actively working in partnership with a number of other UN initiatives to assist stock exchanges around the globe enhance the quality and quantity of reporting on gender-related factors.

2. Credit Suisse, “CS Gender 3000: The Reward for Change”, 2016.

3. World Economic Forum, “Justin Trudeau’s Davos address in full”, Davos, 23rd January, 2018

4. Catalyst, “Generations: Demographic Trends In Population and Workforce”, 20th July 2017

5. PwC, “Millennials at work: Reshaping the workplace in financial services”. A survey conducted in the US by the Institute for Public Relations in 2016 found that nearly half (47 percent) of the millennials surveyed actively look for diversity and inclusion programs in their prospective employers before making a job decision.

6. Macquarie Research, “Millennials – more to invest in than avocados”, 19th June 2017

We often like to highlight our “common sense business person’s approach” to investing. We are contrarian by nature and focus on the leading businesses in areas that are out of favour, facing change, or are depressed in the near term. Since the launch of our Concentrated Global Share Fund in 2016, no industry sector represented this better than the old media pay television space in the US. The sector serves as an interesting case study on the merits of buying quality assets at or below their replacement value.

We have all read the doom and gloom about “cord cutting” and millennials preferring Netflix over traditional cable and satellite services. But what some may not be aware of is the rich hunting ground this industry has been for our Fund, with two takeover offers within the last year. When we launched the Fund, our thesis was clear: Pay TV content channels need to consolidate as scale is becoming more and more important.

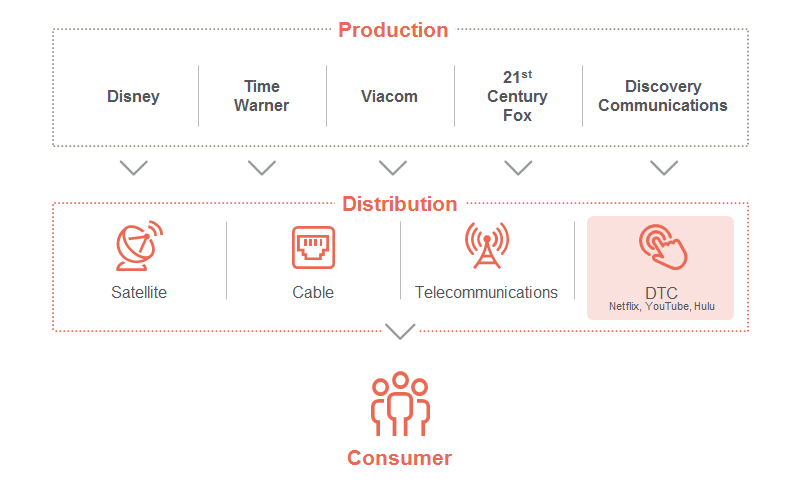

The value chain of the media industry below highlights the shifting balance of power between the content generators and distribution platforms to the consumer, with the Direct-to-Consumer (DTC) paradigm providing opportunities for the content producers to encroach on the platform territory and better target content to the end consumer’s preferences. Historically, consumers paid a premium to access bundled channel content through distributors. With the DTC model and disruptors like Netflix and YouTube coming to the fore, the distributors are progressively dismantling their ‘fat’ bundles to offer ‘skinny’ packages that are more tailored and competitively priced. This dynamic naturally has implications for the content generators, which is playing out through a wave of merger and acquisition activity.

Media value chain – content is king!

This consolidation dynamic is true not just in television but across many sectors. We have witnessed significant consolidation themes play out over the past two decades across different industries which we have held in our portfolios. But what has remained constant is our focus on identifying unique, high quality assets and then having the patience to let our thesis play out. This is the core foundation of our contrarian philosophy.

Our journey through media ownership

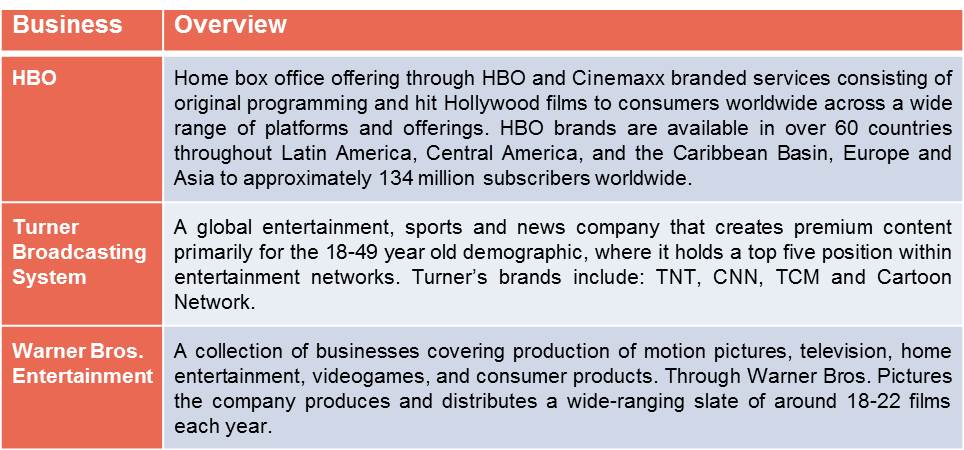

At the time of our Fund launch we only held one investment in Media, being Time Warner Inc. (TWX). We loved Time Warner’s unique asset base, with one of the world’s leading news channels (CNN) and premium drama content via HBO. It was no wonder that in July 2014 Rupert Murdoch tried to purchase the business but was rebuffed. Time Warner is more than just CNN and HBO, the company has a suite of fully scripted channels that include TBS, TNT Sports, Cartoon Network, and a blockbuster movie studio centred on the Warner Bros and DC Comics franchise.

Time Warner – operating divisions

In October 2016 AT&T made a $107.50 share offer for Time Warner which valued Time Warner shares at a multiple of 19.5 times (x) its 2016 earnings per share and a 12.4x enterprise value multiple (EV/EBITDA). The consideration was an equal proportion of shares and cash representing a premium of 40% to the prevailing share price at the time. On completion, Time Warner shareholders would own 15% of the combined company.

Following the bid, we used the strength in the stock price to sell our entire position in Time Warner. We believed the bid fully valued Time Warner and also held the view that AT&T could face an uphill battle with the Department of Justice (DOJ) Antitrust division to obtain requisite approval for the merger. As an aside, the DOJ has recently filed to stop the bid and now it is heading to the courts for resolution.

The proceeds we realised from the sale of Time Warner were redeployed into 21st Century Fox. This is a common theme in our Fund whereby we look to realise investments that have reached their intrinsic value. We then look for other opportunities within the industry with similar unique premium assets that are hard or impossible to replicate and are trading below their replacement or build value. 21st Century Fox (“Fox”) fit that criteria and we invested.

Consistent with our prior media investments, we place considerable value on the Fox assets. The company was formed through the spin-off of News Corporation’s publishing assets in 2013 and operates a broad collection of businesses across cable network programming, filmed entertainment, television, and Direct Broadcast and Satellite TV. The company’s television assets are primarily focused on news and sports content, together with entertainment programming through FX Networks and non-fiction science and exploration content through the National Geographic channel. The prime assets of the company are its Fox News and regional sports networks, which hold leading positions in their categories in North America. Outside of its home region, Sky Plc holds the number one position in the UK; Star India distributes content through over 40 channels across India and more than 100 other countries; and National Geographic is a global leader in its space, reaching over 440 million homes in 171 countries and broadcasting in 45 languages.

Fast forward to December 2017 and another stalwart of the media world, Disney, launches a bid to buy the majority of Fox’s assets in an all-stock transaction for US$66.1 billion (A$88.0 billion) including debt of $13.7 billion. The deal represents an 11.9x calendar 2018 EV/EBITDA valuation for the assets sold, leading the stock to rally more than 40% from its recent November 2017 low. The assets to be sold include Fox’s Film and TV studio, FX Networks, National Geographic, Fox Sports Region Networks, Fox Networks Group International, Star India and Fox’s interests in Hulu, Sky, Tata Sky and Endemol Shine. Prior to acquisition, Fox will spin-off its remaining assets into “New Fox” including the Fox Broadcast Networks and TV Stations, Fox News Channel, Fox Business Network, FS1, FS2 and the Big 10 Network.

Time once again to take profits

Following the Disney bid we reviewed our thesis and decided once again to use the strength in the stock price to sell our whole position in Fox. We believed the bid fully valued the business and longer term, we believe that New Fox, which will be effectively run by Rupert and Lachlan Murdoch, will merge this entity into News Corp’s newspaper businesses. We believe that such an entity does not represent a premium unique asset as newspapers today are a highly commoditised business, heavily disrupted by digital formats and have little or no pricing power. The sale represented an average holding period gross return of 18.5% (before fees and taxes) for our investors.

The realised proceeds from the sale were once again redeployed into the sector, this time Discovery Communications (DISCA) was the recipient. Discovery operates a portfolio of premium non-fiction, lifestyle, sports and kids programming brands. Content is distributed to more than three billion cumulative viewers across pay-TV and free-to-air platforms in more than 220 countries and territories through highly recognised and endorsed channels.

Discovery Communications – brands suite

Source: Slideshare

We have been closely following Discovery Communications for some time as it also offers a unique set of assets, difficult to replicate and occupies the number one position within the non sport male demographic within the US pay television market. The company has engendered some strong leadership positions in distinct segments, such as the Oprah Winfrey-lead OWN Network with a strong following within the female African American demographic, and Europe-focused sports programming and broadcasting through its Eurosport business.

Apart from Discovery’s unique content, its share market valuation is compelling. Discovery Communication trades at a current PE of 9x, has significant excess depreciation and trades on an 8x 2018 EV/EBITDA, which represents a 50% discount to the two most recent private market takeover prices. Additionally, the synergy benefits from their recent acquisition of Scripps Network, which operates the HGTV, Food Network and Travel Channel subscription offerings, would represent an additional 15% of their total cost base and contribute double-digit earnings over time. We believe there are no competitors capable of replicating their library or asset base at such extreme valuations, even though we do acknowledge that it does face headwinds with consumers cancelling subscriptions and becoming more selective about the content for which they pay. They are losing traditional pay television subscribers and need to get into a ‘skinny’ lower priced bundle package. But beyond the short term, we believe if you have superior content, media companies will go direct to the consumer, similar to what Netflix have done with their original “House of Cards” content.

Discovering value

Part of our investment philosophy is to look for businesses that have an owner-operator management mentality. They are in tune with commercial and operational facets of the company and hold significant financial stakes in its success. John Malone — a pioneer in the US cable business and the largest owner of US private land — is Chairman of Discovery’s board and is its former CEO and founder. Malone has visibly backed his convictions through doubling his stake in Discovery in December, increasing his share in Discovery by 30% to become the largest individual shareholder. His combined stake in the company is now worth in the vicinity of US$400 million. Malone’s position clearly fits our criteria which adds to our conviction in Discovery.

It is worth recalling comments from a November 2017 interview with CNBC where John Malone articulated his views on the media industry which aligns with our longer term view. According to Malone, “Scale [is] even more important in a media business where scale always was important. So it’s all about scale … can Netflix get enough scale that nobody really can challenge them?”

BT Concentrated Global Share Fund – media sector investments

Source: BTIM, Bloomberg

Re-shaping the media landscape

It is still too early to speculate how the remaining assets in the media landscape will play out, but it is obvious to us that superior content will increasingly be delivered direct to consumers via an app on multiple devices, and failing this, takeovers will increase over the coming decade. Viacom will most likely merge back with CBS and Discovery may find a home with a larger content provider. Ultimately, the cable distribution providers are likely to converge with the telecommunications providers as 5G spectrum deployment quickens.

Across our investments in media content generators, a common rationale for the purchase decisions was the ability to buy these assets at prices below the replacement value of their content library.

“[Discovery] have good brand recognition globally and he owns all of his content. He doesn’t just license it, he actually creates it, produces it and owns it, all rights in all markets”.

John Malone, Chairman of Liberty Media entities and board of Discovery Communications

We have bought different viewership segments that are leaders within their category and have allowed the time for their value to be appreciated. Our latest investment in Discovery Communications continues that theme. It is a leader in the non-fiction 18-40 year viewership bracket and despite its below-par valuation, is generating a return on equity of over 130%. We recognise the intrinsic value of the growing content library which, once created, becomes an asset that can be syndicated through other platforms or via DTC approaches to generate additional revenues for little further outlay. The same dynamic doesn’t apply to the platform providers who are increasingly reliant on the content kings.

BT Concentrated Global Share Fund (APIR: BTA0503AU, ARSN: 613 608 085) – Important information

Reduction in management costs from 1 March 2018

With effect from 1 March 2018, the Fund’s management costs will reduce.

The management costs are currently made up of an issuer fee of 1.25% pa. The issuer fee will reduce to 0.90% pa from 1 March 2018.

Fund Manager commentary for the month ended 31 January 2018 covering market reviews, BT Investment Management fund performance and our outlook for the period ahead.

Access the monthly commentary here.

Irony – A figure of speech in which the intended meaning is the opposite of that expressed by the words used; usually taking the form of sarcasm or ridicule in which the laudatory expressions are used to imply condemnation or contempt.

“The Walrus and the Carpenter were walking close at hand; they wept like anything to see such quantities of sand: ‘If this were only cleared away,’ they said, ‘it would be grand! If seven maids with seven mops swept it for half a year. Do you suppose,’ the Walrus said, ‘that they could get it clear? I doubt it,’ said the Carpenter, and shed a bitter tear.” Lewis Carroll, The Walrus and The Carpenter

Why we underperformed in 2017

2017 was a tough year for the Pendal Wholesale Asian Share Fund. I’ll recap the main reasons for the underperformance, not just so that I have it in one place (I’ve commented on some of the mistakes in my monthlies last year), but also for me to reflect on and explain what I’ve done to the portfolio since.

As you are aware, I do own cyclical businesses in our portfolio. However, compared to the index, which has perhaps a 40-45% weighting, I own no more than 25%. In 2016, I had started increasing my cyclical position closer to 20-22%, but in a year like 2017 with a huge cyclical-biased rally, I will underperform. The reason I own cyclicals is to lessen the underperformance during a cyclical recovery. Shares of quality and defensive-oriented businesses generally do not perform as well in a year in which we have cyclical rallies. Some clients have asked if I would increase the weighting in future to mitigate this risk. It’s unlikely for the simple reason that cyclical turns are macroeconomic events and therefore difficult for me to predict. In my opinion, cyclical stocks do well (most of the time) because of a change in risk perception, not because they are good businesses to own.

In my opinion, cyclical stocks do well (most of the time) because of a change in risk perception, not because they are good businesses to own. Samir Mehta – Senior Fund Manager, J O Hambro Capital Management

Unfortunately in 2017, the timing of my stock-specific mistakes in my core holdings coincided with the powerful cyclical rally. In the past when I’ve made mistakes, they were usually compensated by my other stock holdings performing equally well or better. That was not the case last year. Not just the cyclical rally but its narrowness played against me as an all-cap fund.

Tilting towards financials and materials

As to the current portfolio, you will observe that I made a reasonable tilt towards the financials and materials sectors in 2017. In the past, both were poorly represented in our fund. Financials should generally benefit from low valuations, falling risks on non-performing loan (NPL) provisioning, falling risk of regulatory fines, rising loan growth and possibly higher margins leading to sustained earnings growth. A sweet spot, if any could be defined. Materials, on the other hand, are benefiting from an anti-supply shock in China. In terms of countries, North Asia and select exposure to Malaysia and Indonesia reflect my confidence in the global economic recovery, as well as the possibility of this rally broadening out from the narrowness we experienced last year.

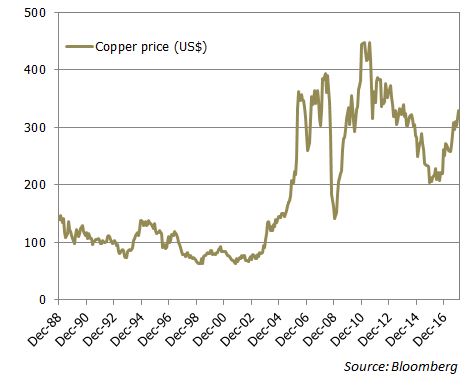

On the topic of materials, let me reflect on the events of the past two decades, which help put things in perspective. China’s accession to the World Trade Organisation in December 2001 was a watershed moment. Around that time, the US was dealing with the fallout of the internet bubble, while Asia was cleaning up after the Asian financial crisis of 97/98. The Greenspan-led Federal Reserve cut interest rates aggressively to counter slowing GDP growth. American corporates were keen to outsource to China in order to reduce costs. China’s vast land mass, cheap exchange rate and unlimited labour pool set in motion the long bull market in most assets from 2002/3 onwards.

I attribute a demand shock from China to be one of the foremost reasons for that bull market in commodity prices. As China’s economy grew, capital flooded in, infrastructure investments picked up; cheaper and easier access to credit fuelled a concurrent rise in consumption as well. Some people compared it with Japan’s industrialisation, only much bigger in scale. In the early 2000s, as global growth went on steroids, commodity prices in particular rose very sharply. Of course, that was before it all nearly ended with the 2008/09 crisis.

Copper is the new gold

Too much stuff

A supply response did emerge for commodities and metals. Most projects planned and implemented during the boom fructified between 2008 and 2013. Commodity prices remained elevated after the 2008/09 crisis, thanks in no small measure to the gigantic stimulus plan by China and the QE policies of central banks across the world. However, by 2013, as the Federal Reserve spoke about ‘normalising’ policy and the effects of the stimulus started to wear down, excess supply was in plain sight. What was once a demand shock was now blighted by supply excess. Everywhere you looked, just like the Walrus and the Carpenter, you could see just too much stuff. China’s severe downturn in 2015/16 gave rise to the possibility of widespread deflation. As industrial China floundered, the country’s banking system came under stress.

In my view, the Fed’s decision not to raise rates in March 2016 was in hindsight the pivotal turning point for China, the global economy and commodities in general. It allowed the Chinese authorities breathing space to deal with capital outflows that were snowballing into capital flight. Subsequently, a clampdown on outflows and a bit of economic stimulus helped stabilise demand. Regardless, the added positive for commodity prices has been a desire to control pollution in China and the associated supply side reforms. This has led to a significant shut down of capacities in steel, cement, coal and aluminium, in particular.

A Chinese supply-side shock

The dictatorial fiat – what in normal times is considered anathema to capitalism – was in this case a boon for capitalism. We know that in North Asia (Japan, Korea and China) businesses were driven more by market share ambitions rather than by generating the highest return on capital for their shareholders. This attitude, combined with cheap access to capital and the state’s desire to grow GDP at any cost, resulted in over-investment in several industries. If the Chinese government does maintain its focus on pollution, which then translates into more discipline on future expansion, the result will be lower GDP growth (as fixed asset investments grow at a slower pace) but much better cash flows and profits. A demand shock from China caused the first boom in commodities; ironically, an anti-supply shock from China is driving commodity prices higher now. So far, there is evidence that the clamp down on industries to reduce pollution, especially in and near the big cities, is genuine. Take the cement industry as an example.

Cement prices – at levels not seen for years

I started buying China’s Anhui Conch, one of the largest cement manufacturers, in March 2016 as part of our contrarian approach to cyclicals. As cement prices have climbed, profits for cement companies are running at levels not seen since 2011. Fear drove price-to-book multiples in 2016 to extremes; I’m hoping that greed will drive the price-to-book ratio to well above mean levels at a time of rising book values. If the government stays firm on capacity controls, that outcome is likely some time later this year, in my view. I’ll be happy to give the stock away to those who are fearless then.

Anhui Conch – fear no more

“Alibaba: We reiterate OW rating and raise our TP to USD 270”

Broker report, February 2018

Different perceptions of the value of an asset are at the heart of capital markets and are the key to active investment management. For any given investment process, there will be periods when the consensus view seems to be completely unjustifiable and must be opposed. For us, this is such a time. Here are three significant mispricings in the current emerging market asset class, all relating to the very largest stocks in the asset class.

Firstly, the disconnect between Chinese internet company Tencent and its South African shareholder Naspers. We feel the Tencent business model is one of the strongest in the world. Whilst its total addressable market is smaller than Facebook’s, its core business continues to grow revenues successfully without overly relying on advertising. Against this, though, is the degree to which the share price has outrun earnings. Tencent reached over 40x 12-month forward consensus earnings, which is around the level that has historically formed the upper limit to the stock’s valuation range.

Tencent headquarters at Nanshan Hi-Tech

The valuation situation is different at Naspers, a South African holding company with a 33.2% stake in Tencent. Naspers trades at a very deep discount to its underlying net asset value. At the end of January, Naspers traded at an improbable US$62bn discount to its stake in Tencent alone. That negative US$62b covers US$3.8b of other quoted holdings, US$1b in net debt, and various media and internet assets in emerging markets, including pay television and e-commerce.

“We are as confident in these positions as in any we have ever held.” James Syme, Senior Portfolio Manager, J O Hambro Capital Management

Secondly, Samsung Electronics, which since 2015 has delivered incredibly strong operational performance across its business units and a highly positive set of corporate governance reforms. That performance might be expected to have been reflected in the stock’s valuation, especially with the run-up in the overall price/earnings multiple of the emerging market asset class, but that has not been the case. From 2010-2015, Samsung Electronics traded at an average price/12-month forward earnings discount to the MSCI Emerging markets index of 22.2%, but in the last year that has expanded to 46.8%, with Samsung Electronics at 6.9x 12-month forward earnings, and the index at 13.0x.

Thirdly, within the group of companies that constitute the Alibaba group, the cloud computing business is thought by other analysts to have a valuation that we cannot comprehend. The strong performance of Alibaba shares in 2016 and 2017, well ahead of the growth in underlying earnings, partly reflects increasing confidence in the newer business units the group has launched, including the cloud computing business. That unit had, in the fourth quarter of 2017, revenues of RMB 3.6b (US$553m), up 104% on a year earlier. Unfortunately, the growth was not accompanied by profitability. The reported operating margin for the quarter was -22.0%, down from -19.2% a year earlier. How much might a loss-making business with an annualised US$2b revenue stream be worth?

A review of published analysts’ estimates reveals some robust estimates, with an average valuation for the unit of US$60b. It is this approach to company valuation that has helped Alibaba reach a market capitalisation of US$523b. Our portfolio has benefited substantially from the run-up in Alibaba’s share price, but we cannot justify continuing to hold the stock and have sold our position.

The portfolio’s largest active positions are overweight Naspers and Samsung Electronics, and underweight Tencent and Alibaba. We are as confident in these positions as in any we have ever held. We are invested in our strategy alongside our clients. Nothing can out-run its fundamentals forever.

The year 2017 unexpectedly marked the end of Westfield – at least in relation to the corporate entity that carries the name of well-known shopping centres. On December 7th investors in Westfield Corporation (WFD) received a proposal to merge with the Dutch origin property giant, Unibail Rodamco (‘Unibail’). The deal was consummated by an in-principal acceptance by the Lowy family and directors which valued the company at $33 billion, a 32% premium to the prevailing share price. If the deal meets all regulatory hurdles and shareholder approvals, it will represent the largest corporate merger in Australia’s history.

Unibail itself has an illustrious history as a company. It was formed in 1968, initially as a finance leasing company before winding down this business in the 1990s to establish itself as a commercial property operator. In 2007 the company merged with Rodamco Europe to form a large regional player in European property, representing approximately 16% of the EPRA/NAREIT Developed European Index. The merger makes strategic sense, considering the complementarity of the respective Westfield and Unibail asset portfolios. Unibail’s footprint consists primarily of 71 shopping centres across the region together with 13 office buildings and 10 convention centres in Paris and surrounding areas. Retail property accounts for about 85% of its portfolio.

If the deal meets all regulatory hurdles and shareholder approvals, it will represent the largest corporate merger in Australia’s history.

Westfield’s offshore asset base consists of large shopping centres in the US and the UK, along with development opportunities for new and existing centres, as well as residential apartments. Bringing these entities together will result in a largely retail property behemoth representing US$72 billion (A$96 billion) of assets.

The deal is unlikely to face any material resistance. Westfield’s shareholders will be furnished with independent valuation reports prior to voting on the proposal and can be expected to support the combined scrip and cash offer. There remains a chance that another party could show its hand and conduct a raid on the register, although we see this as a relatively low probability event. The sheer size of the transaction limits the potential bidders to a small handful of property companies with the requisite balance sheet strength. This list of potentials would realistically be limited to the largest US REIT and sovereign wealth funds. With all hurdles being met, the merger should be completed by mid-2018.

The choice for shareholders

The next question on the minds of existing Westfield shareholders is whether their Australian-listed holding will be subsumed into an offshore listing. Under the terms of the offer, existing shareholders will receive around 35% of the value as US$2.67 in cash for each Westfield share held together with the option of receiving the remainder as Unibail Netherlands-listed stock or Chess Depository Interests (CDIs) which will be tradeable on the ASX. It is likely that the majority of Australian domiciled investors would opt for the latter and retain exposure to the enlarged entity. Existing shareholders may hold some concerns over the value of the deal, given that Westfield’s share price has remained below its post-announcement level. However, this is largely a reflection of US dollar weakness and the translation of value for its underlying assets rather than a concern over the deal’s intrinsic value.

Index implications

Despite the loss of an iconic name and major component of the Australian REIT Index, the sale is a net positive for investors as it will reduce the size of the retail sector and improve diversification. Westfield’s representation within the Index under the combined CDI security will fall from around 15% to 5% and the retail sector will fall from 44% to 35%. There is also likely to be some re-weighting into office, industrial and logistics assets from proceeds of the sale. The aggregate cash component is the equivalent of about two years’ worth of capital raisings across the sector, so we’re likely to see a bolstering of capital accounts within the majors like Stockland, Dexus, GPT and Goodman Group.

The aggregate cash component is the equivalent of about two years’ worth of capital raisings across the sector

REIT opportunities abound

Beyond Westfield and the other major REITs there are a number of good opportunities in new segments such as childcare, retirement living and storage. Demand for such assets in Australia is growing along with the well-publicised shortages of child care and accommodation needs associated with demographic shifts. Supply of these assets remains short and the release of Westfield capital will benefit these areas of the market.

Storage is another area with growing demand credentials. This sector’s growth is being driven by issues like cybersecurity and shifts to cloud data storage. An example of operators in this space is Iron Mountain. Our fund recently invested in the company, which provides a range of data storage and document management services. The operational leverage of companies like this is substantial, with limited incremental capital spend required to expand capacity. In simple terms, the company is able to lease out eight cubic metres of lettable space for each single square metre of floor space. Fundamentally, success in property investment is a function of acquiring quality assets and generating productivity and operational efficiency. Iron Mountain clearly fits those criteria.

Investors may look at Barangaroo and associate these mega towers with compensating supply, but over 90% of the three towers is already leased.

The office sector represents another area of interest. Office space in Sydney and Melbourne – the vast majority of index exposure – is operating at supply-constrained levels not seen for many years. Take a close look at Sydney’s CBD and you see a considerable loss of office space, courtesy of some large office buildings being torn down in Martin Place and Hunter Street to make way for the Metro and alternate uses. Investors may look at Barangaroo and associate these mega towers with compensating supply, but over 90% of the three towers is already leased.

Property managers have been reporting buoyant conditions on the leasing side, to the extent that tenant incentives typically associated with long term leases like rent-free periods and fit-out contributions are no longer being offered to entice new tenants. Melbourne’s CBD office space is showing similar space constraints, reflecting a combination of both gains in white collar employment and centralisation of businesses from suburban markets to the CBD. Vacancy rates in the CBD have fallen to close to 6%. Melbourne is seeing a boom in construction activity and while this will ease supply constraints, the lead time to completions is significant. A similar dynamic applies to the Sydney office market.

Value across the REIT sector

The property securities sector has been exposed to the headwinds of interest rate markets, with the US having passed three rate rises since it began the tightening cycle. Further unwinding of monetary stimulus is likely in the US, followed by Europe at a later stage, which casts a shadow over the sector’s relative valuation metrics. Inflation expectations are also starting to reflect in valuations, while a soft domestic retail sector reflects the impacts of household leverage and stagnant wages growth. These amount to notable risks for the sector, but pricing dynamics within the sector sound a more positive tone. In the private markets for direct property, recent transactions have been completed at cap rates – a measure of prospective cash flow yield for the capital outlaid – close to 4%. Cap rates in private markets should translate to support for valuations in public markets.

The Westfield merger is part of a broader global thematic that reflects strong appetite to acquire public market assets. UK-listed property company, Hammerson, launched a bid in December for a smaller UK property rival, Intu, at a 28% premium to its prevailing share price. In the US there will be potential corporate activity in other large mall owners – Taubman, General Growth and Macerich – with activist shareholders on their registers. The operators of large property portfolios are clearly keeping bond market movements in perspective and see longer term value in prime property assets. These dynamics suggest that opportunities for investors are significant, both within and beyond the big names.