Thankfully, I do not have to make predictions on markets. Looking back to January 2017, who would have guessed the direction and particularly the trajectory of markets in Asia? With that said, we are to some extent in the business of estimating future outcomes. By buying or holding certain stocks, I do make implicit assumptions of what I hope or anticipate might occur over time.

Questions, questions, questions

There are several big issues for markets to grapple with. We are in a synchronised global economic recovery. Commencing around mid-2016, growth has accelerated globally in 2017. How strong and how long it will last is the big question. Central banks, especially the Federal Reserve, seem to indicate a determination to ‘normalise’ monetary policy. Will the Fed raise rates four times in 2018? Will the unwinding of its balance sheet be smooth, or will it disrupt asset prices across the world? Geopolitics, both in the Middle East and around North Korea, keeps hitting the headlines. With President Trump seemingly embroiled in several unfavourable domestic issues, will the US resort to distracting domestic attention towards foreign entanglement? In my naïve analysis, signs of inflation seem to be sprouting everywhere – whether it’s commodity prices or wage inflation or in the general cost of doing business. Will inflation reflect in the numbers in the US and drive long bond yields higher? And, finally, a benign liquidity environment has powered a rally in momentum growth stocks. Does that pause or continue? Will out-of favour sectors and countries be the beneficiaries if that happens?

Liking North Asia, tech and financials

By looking at the allocations in the portfolio, the tilts you can observe are towards North Asia for countries and technology and financials for sectors. Technology stocks have delivered high growth but valuations have expanded as well. With that combination comes susceptibility to a pause in momentum investing as well as a rise in bond yields which can impact valuations for these names. I am reviewing some of my technology holdings in the hardware manufacturing area with a high possibility that I could trim some of them. A large allocation to China indicates my assumption of a benign outlook in China. GDP growth might not be stellar, but growth in cash profits and earnings for corporate China could be surprisingly robust. Internet-related companies are likely to sustain growth over time.

The tilts you can observe are towards North Asia for countries and technology and financials for sectors.

In the ‘old’ economy, a couple of developments are worth noting. The resolve demonstrated by the government in removing capacity in the steel, cement, coal and aluminium industries has been, in my view, a significant event. Take steel as an example. By shutting approximately 7% of capacity in the past 15 months, the surviving companies are generating solid cash profits.

After sustaining cash losses in 2015 and early 2016, the steel industry in China is now earning substantially higher cash margins per tonne of steel. Once considered a big negative in China – diktat by the government – now looks like the saviour. Whether it is due to environmental pressures or the threat of trade sanctions, these capacity restraints have helped the steel industry recover smartly. Cynics will ask how long can this last. Can the government remain committed to these shutdowns? Will such high profits not tempt the industry to reopen those plants that were shut down? Of course there are valid questions and there is a risk of re-openings. However, in my view, apart from the survivors which benefit from capacity shutdowns, there is an unintended positive impact on China’s banking sector. In the past, banks were directed to lend to companies that created jobs and resulted in GDP growth. Never mind that the rising capacities imperilled the profitability of borrowers and in turn hurt the banks due to rising non-performing loans. With several ‘old’ industries generating better growth in profit and cash flow, the banking sector in China is starting to see a positive change in the health of their leveraged borrowers. GDP growth might not be stellar, but, for a change, cash flows and profits for industrial China are growing. If this lasts, it will be positive for macroeconomic stability and for the banking system as a whole.

Rising Chinese bond yields

For banks and financials in China, another development worth noting is the rise in 10-year government bond yields. A rise in the cost of money is exactly what China needs. In the past, I’ve commented on the fact that money was too cheap and abundant in China, which in turn allowed growth in leverage and misallocation of capital.

The clampdown by authorities on capital outflows is likely one reason for this increase in the cost of money. The shutdown of irrational borrowers, like the Anbang Insurance group or the HNA group, and the recent crackdown on P2P lenders and micro-lenders are signs of a return to some rationality in China. As these irrational borrowers disappear from the scene, the genuinely good financial institutions (yes, there are some in China too!) are starting to assert their competitiveness. We own two of them: Ping An Insurance and China Merchants Bank. If my analysis is right, not only will they benefit from higher margins but also from a large increase in market share at a time when economic growth is stabilising and profits for China corporates in general are better. In sum, I am a bit more sanguine on profit growth in China, wary of momentum and aware that the biggest risk we face is a dislocation of bond yields if inflation reflects in numbers in the US. I do think we have a balance in the portfolio to mitigate some of that inflation risk, but, as always, time will tell.

I wish you a Merry Christmas and a prosperous 2018.

Tax reform legislation finally seems to be moving along in the US. While the equity markets cheer, the consequences for junk-rated issuers can be very unpleasant. As much as 4/5 of the high yield issuers could be worse off as a result of the proposed changes, which may in turn exacerbate and accelerate the current default cycle.

Under the current tax “reform” bills that have been passed by the US Senate and House, legislators have imposed a cap on interest deductibility at 30% of EBIT and EBITDA, respectively. On the flipside, issuers will also receive a lower rate of tax at 20% and have the ability to fully expense capital items in the year purchased rather than depreciate over a number of years. It has been argued that allowing immediate expensing of capital expenditure will promote more spending and economic growth.

Our concerns with these likely tax changes are both the intended as well as unintended consequences to credit markets. Various estimates suggest that under the House version of interest deductibility (maximum 30% of EBITDA) approximately 40% of non-financial issuers will be unable to fully deduct their interest expense. However, that is the more generous of the two proposals. Under the Senate version that has interest deductibility maximum of 30% EBIT, approximately 83% of non-financial issuers will be worse off than present. Prima Facie, with no change other than the interest cap, investors can determine that high yield companies that do not have greater than 3x interest coverage (‘low end’) will be worse off. The negative impact of the proposed legislation largely affects B and CCC rated issuers, and will lead to increased spread dispersion among high yield issuers – a trend that has been developing over much of this year even in the absence of the latest set of tax proposals.

Our concerns with these likely tax changes are both the intended as well as unintended consequences to credit markets.

The proposals not only put further pressure on the already strained cash flows of many high yield issuers, but also amplify the downside of credit cycles. Since the deductibility of interest is a function of earnings, as earnings wane so will the issuers’ ability to claim a deduction for interest, creating a double-whammy effect on corporate earnings and liquidity in late economic cycles. Consequently, such a tax law will only increase the volatility of cashflows experienced by high yield issuers. This increases the jump-to-default risk of levered issuers that have low levels of interest coverage.

As such, we believe a cautious stance towards high yield credit remains warranted. This is alongside a number of other concerns for the area including a wave of industry disruption, which poses a particular threat to the Consumer Discretionary and Telco sectors. Considered within the context that spreads are near their pre-GFC lows, the potential limited rewards do not justify the increasing risks.

A track record of stability and performance in Australian equities

Our Australian Equities boutique is one of the largest, most experienced and stable in the industry. We apply proprietary, fundamental research at the company level to gather insights and inform investment decisions with the aim of generating excess returns for our clients.

A proven structure delivering results

An independent business, solely focused on investment management, we have operated a boutique model since listing on the ASX ten years ago, where investment team members have ‘skin in the game’ through a fair and transparent profit share model, driving alignment with client interests, accountability and talent retention.

The success of this model is seen in our long term team stability and a performance track record above the industry peer average1 and above benchmark2 across a range of portfolios.

More information?

Subscribe to our regular communications

Read how we manage money

Contact a Pendal Key Account Manager

1 Peer rankings are determined by Pendal using Morningstar’s universe of Equity Australia Large Blend, Equity Australia Large Growth, Equity Australia Large Value, Equity Australia Mid/Small Blend, Equity Australia Mid/Small Growth and Equity Australia Mid/Small Value funds. See here for more details.

2 Performance net of fees, before taxes versus relevant Fund benchmark. We have more information on fund benchmarks and fund performance.

This year I’ve made significant changes in the portfolio. In our monthly updates and calls, I’ve mentioned the challenges I’ve had with performance over the past 12 months. The reasons can be summed up in three buckets:

1. A couple of stock-specific mistakes (Giant Manufacturing and PChome Online, both listed in Taiwan) where disruption of their businesses by internet-enabled competition affected them in a sudden and unexpected manner.

Giant’s bicycle manufacturing business, which I thought was relatively immune from the challenge of online retail, was upended by the proliferation of app-based bicycle sharing business models in China. The novelty and ease of renting bicycles has dramatically cut back the desire to own them, especially the high end ones. Giant’s sales growth in China and margins overall suffered as a result.

PChome Online had a reasonably dominant hold on online shopping in Taiwan until a private/venture capital-funded company (which only recently listed) came up with a much better user interface and offered free delivery for goods, forcing PCHome Online to respond and sacrifice margins and profits. I have since sold out of those names.

2. Post the US elections, interest rates rose a trifle, coinciding with a global cyclical recovery. China Mobile and KT&G in Korea, (both are cash-generating business with low to slow growth) suffered a de-rating on their multiples. I sold out of both.

3. Indian Prime Minister Modi’s decision to demonetise high value currency notes in November 2016 caught me off guard – some of our holdings were rural consumer focused; the impact of the withdrawal of notes was felt mostly in rural India where cash still remains the primary medium of exchange. Small businesses across the country and the agricultural sector were hurt badly and many people employed in these areas witnessed a tough economic situation. Many consumer-oriented businesses reach rural India through the ‘wholesale’ trade. The wholesalers – middlemen – in turn reached far corners of the country dealing with ‘mom and pop’ stores in rural areas. This part of the chain deals in physical cash. This link of the distribution chain was severely affected. Some of our holdings had an adverse adjustment to their business models and they are still recovering from that blow.

India in focus

A year since demonetisation, I thought it would be apt to take stock of its impact, the performance of stocks as well as the exposure of our portfolio to India, which has come down over the past year. It’s not just my reduced holdings but also the composition of those holdings which has changed. From 2015 when almost one third of the portfolio was invested in quality Indian stocks, our exposure to India stands at around 12%, of which half is in cyclicals.

Many commentators rightly point to the long-term attractive nature of the Indian market. I have never disagreed with that premise. I won’t bore you with the details but favourable demographics, rising income, aspirational middle class, well-managed businesses and, of course, a change in government in 2014 were just some of the arguments in favour of India. Yet, in my opinion, the Indian stock market does not seem to be as attractive relative to the other Asian markets.

For any asset to deliver positive investment returns, we need a combination of three factors: the asset has to be cheap on an absolute or at least on a relative basis; the asset should display either rising earnings or improving cash flow profile; and we must encounter a benign and improving liquidity environment.

A benign liquidity environment, thanks to a depreciation of the US dollar has been a common factor for all of Asia. However, only in North Asia have all three factors come together in my view. India, on the other hand, remains a haven for liquidity. The external benign liquidity remains turbocharged by the super abundant domestic liquidity. This was a direct result of demonetisation, when all of the cash in circulation was forced into the banking system. Deposit growth surged at a time when loan growth moderated due to a much weaker economy.

While the liquidity situation in India remains very conducive, in a regional context, the stock market is not cheap.

Two traditional stores of value, gold and property, were adversely affected by demonetisation. These asset classes were typically the repositories of unaccounted cash and, after 8th November 2016, it was not easy to transact in those assets. In effect, savers in India had very little choice. By default, equities became the preferred asset. Inflows into the domestic mutual funds have sky-rocketed in the past year.

This mismatch between deposit growth and the need for loans/funding by the economy was so wide that interest rates started to come off sharply. Since that initial shock to demand, especially in the rural and agricultural parts of the economy, demand conditions have remained subdued. Reported GDP numbers for India have shown the nature of the slowdown in India. Witness the credit growth conditions in India broken down by regions and scale of industries below.

But in this subdued environment, there is just one area which has witnessed an exceptional boom: personal lending – some for mortgages but mostly for unsecured loans – soared.

There are several explanations for this. As the shock of demonetisation affected smaller industries, many smaller businesses and individuals were forced to borrow money to stay afloat. State-owned (SOE) banks are in dire condition due to non-performing loans (NPLs) and are in no position to lend. As interest rates fell, non-banking financial companies (NBFCs) benefited the most from a reduction in their cost of borrowing; they have more than adequate capital. Along with better technology to assess borrowing needs, wider reach through branches and agents in urban areas and credit bureau infrastructure to assess risks, almost all NBFCs have powered ahead in their lending spree.

There is no doubt that a good credit bureau system and use of technology to assess risks are big positives. As I mentioned, SOE banks are on the floor and in no position to compete. With unsecured loans still a very small percentage of GDP, there is genuine room for growth.

All these are very valid and sane arguments. Yet there is always an element of unbridled optimism when it comes to unsecured lending. Currently in India, there is a surge in new finance companies (not just fintech) starting up to take advantage of this big opportunity. With the government about to recapitalise the SOE banks, they, too, might be in a somewhat better position to compete in this space. I do not mean better from a risk assessment or technology standpoint, just better on interest rates. Ultimately, similar to any banking system in the world, the price of loans will be the key area of competition, thus in a way undermining the risk characteristics of this lending opportunity.

India’s near-term blues

The bigger question that plagues my mind is the effect of a slowing economy on disposable income. So far, almost every company we meet remains very optimistic for the long term, but over the next 12-18 months suggest a very uncertain and muted demand environment. The effect of the Goods and Services Tax (GST) in consolidating industry structures in favour of the bigger listed firms is self-evident. Yet there are teething troubles in implementation of GST. That is a minor impediment. The bigger one is the disruption to small-scale businesses which leads to a fall in employment. Similar to the rest of the world, technology disruption will also have a dampening effect on employment generation in India. Data is hard to come by, but anecdotal evidence suggests that job creation still remains the single biggest challenge for the country. Demonetisation and introduction of GST in quick succession has dealt a significant blow to small enterprises.

While the liquidity situation in India remains very conducive, in a regional context, the stock market is not cheap. Indian stocks have always enjoyed a premium over the region, but that was at a time when the rest of the region had little to no earnings growth. As we look into March 2018 and March 2019 growth estimates, what strikes me is the very narrow group of stocks particularly in materials and banks that will contribute to the earnings growth expectations.

While private sector banks and NBFCs will deliver 15-25% earnings growth, they trade on P/E multiples of over 20x while their price-to-book ratios average 4x for 20-22% ROEs. That is not cheap in my view, by any means. These premium multiples I cite for banks are what I also observe for comparable Indian businesses in the quality space. As the saying goes, that the grass is always greener on the other side. But my question is: is this grass or AstroTurf?

Edwina Matthew, Head of Responsible Investments at Pendal, talks about our approach to responsible investing and current issues we have been working through with investors.

BTIM’s Davidson and Forrest on how Amazon is reshaping malls

From the Australian Financial Review; by Vesna Poljak; published 12 November 2017

Reproduced with permission from Fairfax Media

BTIM’s Pete Davidson and Julia Forrest. Photo: Daniel Munoz / Fairfax Syndication

When Myer declined to renew its lease at Westfield Hurstville, a Scentre Group shopping centre in NSW, a chill went through the property trust sector.

“They needn’t have worried,” says Julia Forrest, one of the portfolio managers behind BT Investment Management’s listed property strategy. “That space that was doing $30 million is now doing $100 million,” she estimates. “It’s a buzzing centre, it was an amazing opportunity to transform what was an old, tired centre into a food hub with lots of services, some mini-majors, that has just driven traffic through the roof.

“If Myer wants to close some boxes there’s certainly opportunities across the portfolios to really invigorate that space.” As many as 19 of Myer’s 63 stores could close or shrink, the department store has flagged. “I’m sure they’re looking at other spots where maybe Myer won’t renew and are thinking the same thoughts.”

Forrest and Pete Davidson, who is BTIM’s head of listed property, heard the drums beating about Amazon’s arrival in Australia many years ago. And while they do not take the seriousness of this threat lightly, they argue the property sector has not got enough credit for how it is responding.

“This is the long game, it’s probably going to be a 30-year game.”

“What people probably underestimate is the response from the shopping centre industry. The ability to use technology to improve the shopping experience be it parking or be it what’s offered to customers, that’s something that isn’t in the equation at the moment,” says Davidson. “This is the long game, it’s probably going to be a 30-year game.”

Westfield Group, which the fund is overweight, surged last week as global interest in top mall operators returns. New York-listed General Growth Properties was linked to buyout talks with its major investor, Brookfield, but Davidson says sentiment towards Westfield had already been turning.

“There’s been a lot of circling interest in the stock, which needed a catalyst. Most people accept that there’s a great NAV or asset value uplift that’s coming there through the developments such as Croydon, Milan and most recently Century City,” he says. “Also US retail is recovering. Really the market’s just looking for some guidance for next year, which we’ll probably get at the AGM in February.”

However, they do not share the same confidence for “B-grade” office and “B-grade” malls.

‘Shrink more to greatness’

The US mall experience is useful in approximating Amazon’s impact but it is flawed too. American malls do not have supermarkets as anchor tennants because grocers, as they are known, are located on “strip” shops.

“There are some areas of weakness, obviously discount stores and department stores, which are probably going to shrink more to greatness,” says Forrest. “But the generation of foot traffic going to supermarkets – if you’re doing two visits a week, you’re generating a massive amount of foot traffic that you don’t see in the US.”

Davidson thinks the Amazon factor peaked when it acquired Wholefoods. “But if you follow it at the moment, Amazon are actually withdrawing some of their fresh offer across nine states in the US because it’s quite hard to make it work,” he says. “Yes it’s a concern but I don’t think it’s terminal. If you assume that Amazon got 3 per cent share of Australian retail sales in the next few years that’s roughly equivalent to $9 billion, which equates to the sales of Big W.”

Before funds management, Davidson started out as a treasury dealer with Midland Montagu. Forrest was investigating organised crime. They have been at BTIM 23 and 15 years respectively.

The strategy is reducing office exposures, but they note the incredible levels that assets are changing hands at because of the influx of offshore money.

“B-grade office is selling 19, 20 thousand [dollars] a square metre, which is above replacement cost,” Forrest says. Even so, “the [listed] sector’s actually cheaper than buying direct, you can access better quality assets in the sector cheaper than if you were to go to the direct market and you obviously don’t have any transaction costs.

“If you were to go buy an office building on this street [in Sydney’s financial district] you might be paying 4, 4.5 per cent and you can buy a vehicle that may be yielding 5, 5.5 per cent with growth and obviously you don’t have to manage it yourself.”

In New Zealand, they own Precinct Properties and Vital Healthcare, and in childcare, another sector they like, the fund owns Arena and Folkstone. “The working for families initiative means there will be a big release of government payment next year to boost the sector and it’s also defensive and reliable,” Davidson says.

Strong assets

Mirvac is the fund’s largest stock overweight at the moment. It “has got some of the best earnings growth in the sector, very good management team, great ESG, good office portfolio,” Davidson says. Its retail assets are in “really strong urban locations” that are not experiencing as sharp wage pressures as elsewhere in the economy, according to Forrest.

Beyond Westfield and Mirvac, the third main overweight position is Charter Hall, which is exposed to rising asset values in office and industrial.

“Like most property tragics, we end up with phones full of photos of shopping centres,” says Davidson, who scrolls through hundreds of images of shop fitouts and al fresco dining areas.

The discussion has turned to Stockland Wetherill Park in Western Sydney, a property where Stockland has also utilised rooftop solar targeting 1,200,000 kWh annually.

“They’re recreating a little bit of a Melbourne vibe, it’s like a Melbourne laneway in Wetherill Park. And you can do that, it’s got a nice inner-urban feel about it,” says Davidson.

“It’s worth noting they focus a lot on walkability within their new subdivisions so that’s great, you can only admire that. They’re looking at the whole issue of a better sense of community, a better sense of belonging, more exercise and better health outcomes.”

In terms of assets, he also rates highly Scentre Group’s Chermside – “Brisbane’s Chadstone” – and North Lakes, another Queensland attraction. Mirvac’s 200 George Street gets the tick as an innovative office property, and Goodman’s logistics joint venture out at Oakdale is “in some ways the mall of the future”. He has also been to an Amazon distribution centre in Shanghai, which spanned 400,000 square meters or two-thirds of the size of the Pentagon.

“It could be New York, London or it might be Maitland. We’re there.”

Forrest nominates Westfield London as the best shopping centre in the world, “in terms of curation, presentation, market presence, domination, transport and keeping it relevant and dynamic”. She also recommends the Tramsheds foodhall at Harold Park in Sydney, a Mirvac project linked to its residential development.

“You know you’re passionate about a job when you do it for free, it’s so interesting,” says Forrest. At Westfield Stratford City, another Westfield property in the UK, shoppers can only walk in one direction on the busiest trading days because the mall is so congested, she says.

“We’d categorise the market into fortress malls, and alternatively, safe neighbourhood. It’s the piece in the middle which is a little bit riskier,” says Davidson. “There’s risks there, but I think largely in the price.”

In the next couple of weeks he is going to Maitland to look at a new Stockland shopping centre. “It could be New York, London or it might be Maitland. We’re there.”

The importance of diversifying your diversifiers

We understand advisers are responsible for deciding how client assets are spread across markets. We know different advisers draw on different resources to determine how asset allocation decisions are taken, and how allocations are monitored and re-balanced.

It’s important for advisers to stress test the capabilities of those they rely on to help decide a client’s asset mix. Do they have the time, tools and experience required? Are their processes proven across the investment cycle?

We believe advisers should think about ‘diversifying their diversifiers’, meaning they should consider a combination of resources to ensure portfolios are properly structured and managed to meet client goals.

One enduring way to effectively – and efficiently – manage at least part of the asset allocation process is through the use of multi-sector funds.

Multi-sector, multi-purpose

Multi-sector funds remain a popular choice with as the nucleus of broader, more complex portfolios. Multi-sector managers employing active management between asset classes can serve as an ‘auto-tilt’ outside periodic reviews and guard against portfolio drift. Actively managed multi-sector funds can also be a good complement to passively managed allocations.

There is also ongoing demand for self-contained investment solutions for lower balance clients or clients with a lower level of sophistication. Multi-sector funds can achieve most (or even all) of the investment needs of these client types, where advisers can efficiently entrust the strategic and tactical allocation within and between asset classes to experienced investment teams with proven processes.

Solutions available

BTIM actively manages a suite of multi-sector portfolios. BTIM’s Diversified Strategies team assess the longer term outlook across all major markets and tactically adjust sector allocations in a disciplined and efficient way. Active investment management is then used within each investment sector and investors access capabilities including those managed by BTIM’s Crispin Murray, Vimal Gor and Ashley Pittard.

So in the one fund clients can obtain extensive diversification, active management at the fund and sector levels and value for money.

Talk to your Pendal Key Account Manager today for more information.

We think getting the country calls right is the biggest driver of successful investment in emerging markets. Currently India is one of our two favourite emerging markets, with both a strong trend growth rate as well as potential for a cyclical recovery in the Indian economy. The near-term potential is from an upswing in the credit cycle combined with fiscal support.

In recent years both private sector credit/GDP and the loan/deposit ratio of the banking system have declined as the Indian economy has de-levered, most notably through an undershoot of private sector capital investment and restrained consumption growth. This decline in leverage stands in marked contrast to the ramp-ups of credit seen in some other emerging markets. More recently, inflation has come in below expectations, giving the central bank policy flexibility. We feel the Indian economy resembles a coiled spring waiting to be released.

Government can be the trigger that unleashes the spring.

We have also been expecting the government to provide fiscal support for both consumption and investment ahead of the 2019 election. In addition, we consider the Modi administration to be the most pro-reform government in any emerging market right now, and see some of the policies (eg tax reform, infrastructure investment and improvement, switch to cash benefits for the poorest citizens) as providing direct and visible uplift to economic growth. Government can be the trigger that unleashes the spring.

A double helping of good news

Recently we saw two major developments in India that only add to our optimism over the Indian economy and, by extension, Indian equities. The first was the announcement of a recapitalisation of the state-owned banks of approximately US$32 billion over the next two years (US$20 billion through recapitalisation bonds sold by the government to the banks and then reinjected as equity, cleverly avoiding any liquidity impact, and US$12 billion directly from the fiscal budget). This is by far the most significant move of any recent Indian government to tackle the under-capitalisation of the state-owned banks. Banking sector stocks reacted accordingly with sharp upward moves.

The second, which has received less attention than the bank news, was the announcement the same day of a US$105 billion five year road-building plan to improve transport infrastructure to allow the economy to more fully benefit from the liberalising effects of the national goods and services tax (GST). These steps, we feel, are indicative of a government keen to ensure that the positive effects of its reforms are felt before the election.

Above-average valuations justified

Whilst Indian equities are not cheap in an absolute sense, the premium they attract over the average for emerging markets is slightly below its normal level, and we feel that the very strong growth opportunity and the prospects for further reforms justify current valuations. We remain heavily overweight Indian equities, with a focus on domestic sectors including, notably, banks.

Read more

Learn more about the importance of country allocation

Understand the advantages of emerging market equities

Corporate Australia delivered earnings growth of 18% in FY17, with the market relying on Resources to do most of the heavy lifting. Disruptive and cyclical challenges remain a defining feature, but a pick-up in capex, a controlled housing slowdown and increased infrastructure spending suggest an improving economic landscape. Australian equities retain support from liquidity and dividend yield, with lucrative opportunities available to the engaged, active and agile investor. With all this in mind, in this update BT Investment Management’s Head of Equity Strategies Crispin Murray provides his views on the outlook for Australia’s economy and equity market.

Economic outlook

We are more sanguine about the economic backdrop following the August reporting season than was the case six months ago, for three reasons. The first is that, at this point, the slowdown in housing appears to be orderly and is not providing the headwind to economic growth that some feared. This factor demands close observation however, with employment strong and interest rates low, the backdrop is relatively benign.

The second factor is that headwinds from declining capital expenditure have abated and capex should begin to be a more positive contributor to growth.

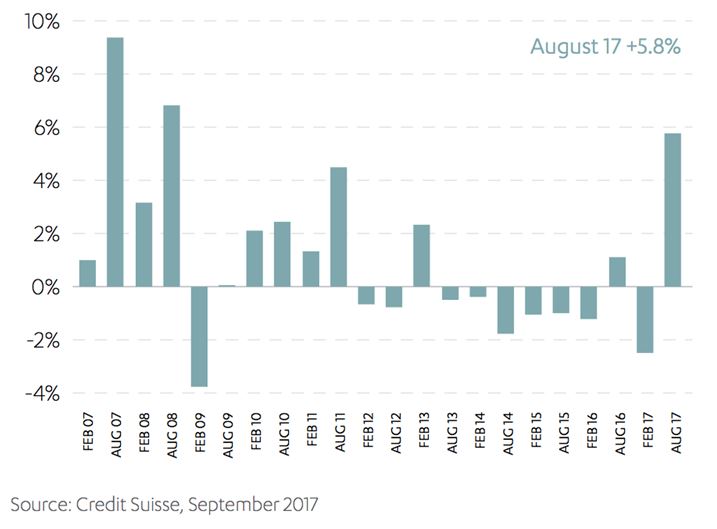

S&P/ASX 200 ex-financials FY18 expected capex spend

There is a balance to be struck here, as it has been capex discipline which has allowed companies to generate cash flow, de-risk balance sheets, and increase payouts in an otherwise sluggish environment. Nevertheless, signs that companies are starting to spend provides a tailwind for the broader economy that we have not seen for some time.

The third component is the pipeline of infrastructure as governments roll out a programme of road, rail and metro projects. This has been well telegraphed and has a long lead-in time, but there are now signs that we are moving into a significant uplift in spending. This is coming at a point where mining companies are no longer scaling back on investment, providing a tailwind for employment and activity, which, again, has been missing for some time.

As active managers, this is a fertile environment. Uncertainty creates mis-pricing – and mis-pricing creates opportunity.

Market outlook

From here, we expect more of the same: a mid-single digit return, driven by earnings. A reasonably cautious unwinding of European QE and only marginal tightening from China means that liquidity is not a headwind. The market is also enjoying support from the significant yield premium it enjoys over bonds. At this point, with little sign of recession and absence of some geopolitical shock, we see the market able to hold its valuation rating. This leaves earnings as the market driver, with consensus expectation of +7% for FY18.

Crucially, we believe we are at an inflection point in Australian equities. The dominant trend of recent years – falling bond yields, which fuelled a surge in defensive yield and growth stocks – has waned and bond yields now look range-bound. Chinese policy remains supportive of resource stocks, but is no less opaque than in the past and its future direction rests on the political transition in October. Oil prices likewise look range-bound, with Saudi Arabia’s efforts to cut production and raise prices nullified by production increases from non-OPEC countries. At the same time, we have a market facing unprecedented disruption in the form of new technology, competition, and regulation, which is providing structural challenges to long-standing Australian oligopolies.

Uncertainty creates opportunity

In short, uncertainty abounds. Themes and trades which have been ‘one-way’ in recent years are no longer. Many companies which have done well are looking challenged. As active managers, this is a fertile environment. Uncertainty creates mis-pricing – and mis-pricing creates opportunity. In this environment there will be divergence between sectors and, crucially, divergence between companies within the same sector.

This is where the ability to scour the entire market for opportunities comes to the fore. This is where the opportunity to meet management, gauge their strategy and quality, and to assess their ability to navigate a tricky environment become crucial for an investment outcome. We remain mindful of the challenges and cognisant of the uncertainty, however we believe that our bottom-up, fundamental approach employed by one of the largest teams in the Australian market, is positioned to do well.

31 October 2017

BT Defensive Equity Income Fund (APIR: BTA0427AU, ARSN: 159 947 298) – Important information

Reduction in management costs from 1 November 2017

With effect from 1 November 2017, the Fund’s management costs will reduce.

The management costs are currently made up of an issuer fee of 0.99% pa and an expense recovery of 0.15% pa. The issuer fee will reduce to 0.75% pa and the Fund will no longer charge expense recoveries.

Changes to the Fund’s investment strategy from 1 December 2017

Following a recent review, we will be changing the Fund’s investment strategy with the aim of enhancing the Fund’s ability to perform in a range of different market conditions.

The Fund invests primarily in an actively managed portfolio of shares in the S&P/ASX 200 Index and uses options and other derivatives to generate income and reduce market risk. The Fund’s portfolio is constructed using three key steps.

From 1 December 2017, the Fund’s portfolio construction process will comprise the following steps:

1. Investing in a selection of shares in the S&P/ASX 200 to generate income from dividends. The portfolio will generally include 20-60 companies, with a bias towards high dividend yielding stocks with franking credits based on our positive, fundamental company analysis. BTIM’s fundamental company analysis focuses on four key factors: valuation, franchise, management quality and risk factors (both financial and non-financial risk);

2. Selling call options over some or all of the shares in the portfolio and/or the S&P/ASX200 Index to generate certain income from option premiums in exchange for forgoing a significant component of the potential gains on the share portfolio. Any share call options sold will be fully backed by holding the shares in the portfolio; and

3. Buying put options over the S&P/ASX 200 Index and specific shares held in the portfolio with the aim of significantly reducing the Fund’s downside market exposure.

How is this different to the current portfolio construction process?

The new portfolio construction process enables the portfolio to generate income from option premiums, by selling call options over some or all of the shares in the portfolio as well as the S&P/ASX 200 Index, instead of selling call options over all the shares held in the portfolio. This change allows the portfolio greater flexibility to tailor exposure to where BTIM believes the best risk/reward benefits lie. For example, where BTIM’s analysis indicates the medium to long term outlook of the share outweighs the premium that would be received from selling the call option, the portfolio would have the ability not to sell the call option over the share.

The portfolio construction process will now also include buying put options over specific shares held in the portfolio, in addition to the current portfolio construction process of buying put options over the S&P/ASX 200 Index. The current process of buying put options over the S&P/ASX 200 Index protects the Fund against broad downside market exposure, but not all sectors and stocks perform in line with the index. The ability to buy put options over specific shares is expected to better protect the portfolio from sector and stock specific downside exposure.

The Fund will continue to invest in a selection of shares in the S&P/ASX 200 Index and generally hold 20-60 companies with a bias towards high dividend yielding stocks with franking credits. As the Fund can now sell options over the shares in the portfolio and/or S&P/ASX 200 Index, this reduces any potential bias in the portfolio towards shares whose options are more liquid.

The overall exposure limits of the strategy are not affected and we do not expect any material change to the Fund’s risk return profile. Furthermore, there is no change to the Fund’s investment return objective.